Americans and their Debts. Long-defaulted federal student loans, after coming out of the woodwork, whack delinquency rates.

By Wolf Richter for WOLF STREET.

Total household debt outstanding in Q4 – mortgages, HELOCs, student loans, auto loans, credit card balances, and other consumer loans such as personal loans and BNPL loans – rose by 1.05%, or by $195 billion, from Q3, to $18.8 trillion, according to the Household Debt and Credit Report from the New York Fed today, which obtained this data via its partnership with Equifax.

Year-over-year, household debt rose by 4.1%, or by $744 billion.

Over the years, the number of households has grown, and the income per household has grown on average over the years, and combined they have grown faster than household debt, and the burden of this debt in terms of their combined income has declined over the years, as we’ll see in a moment.

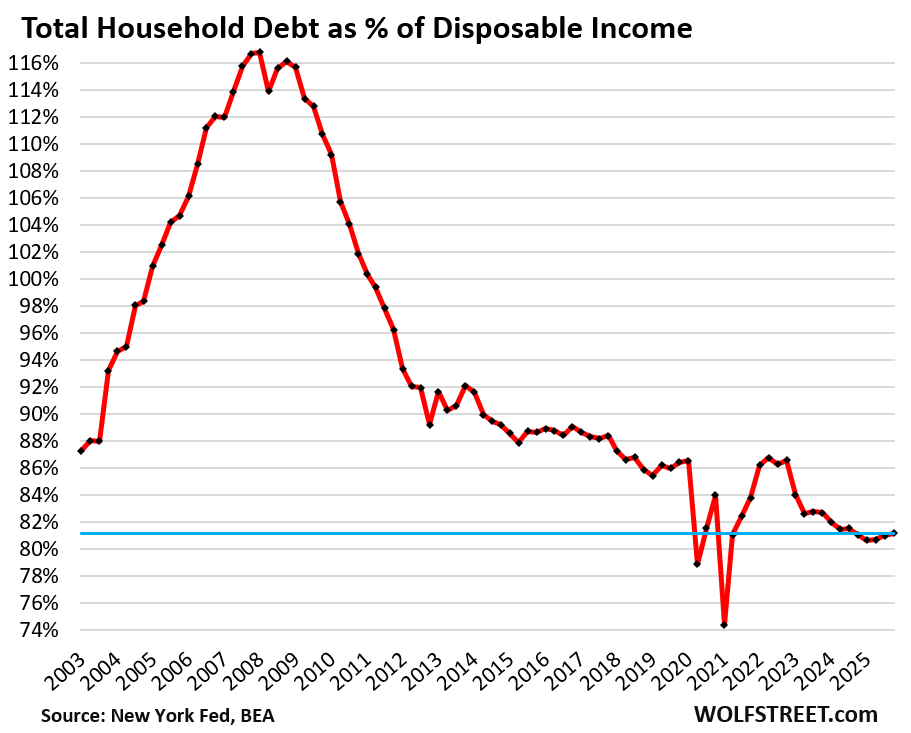

The burden of household debt: Debt-to-income ratio.

The debt-to-income ratio is one of the classic ways of evaluating the burden of a debt. With households, we can use the debt-to-disposable-income ratio.

Disposable income, released by the Bureau of Economic Analysis, is essentially the monthly after-tax income consumers have available to spend on a monthly basis for their daily costs of living, and to service their debts, and then to save and invest the rest.

It excludes income from capital gains, which is where the super-wealthy make most of their money, and this upper echelon of income is excluded here.

So income from after-tax wages, plus income from interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc.

The debt-to-disposable income ratio in Q4 edged up to 81.2%, a tad higher than in the prior three quarters, which, except for two stimulus-era quarters, had been the lowest in the data going back to 2003.

Consumers are making record amounts of income, and there is a record number of consumers, and their aggregate balance sheet is in good shape: 65% own their own homes, and about 40% of them own their homes free and clear, and another big portion have only small amounts of debt left on their homes. Over 60% of households have at least some equities, and their prices have exploded. Many hold precious metals and cryptos. And households are sitting on a record pile of interest-earning cash. The economic entity of American households is in good shape.

But as the chart below shows, that wasn’t always the case. In the run-up to the financial Crisis, consumers were heavily burdened with debt, and by the time the ratio went over 115%, that debt had already started to blow up.

But, but, but… subprime-rated borrowers. This is a small subset of consumers with a low credit rating because they have a high debt-to-income ratio, missed payments, delinquent loans, and a bad credit history.

“Subprime” means bad credit, not “low income.” The high-income young dentist that got into it over their head is a classic example of high-income subprime. They’ll get it worked out and clean up their credit, but for a while they’re subprime. Credit problems are driven by this small subset of consumers.

Low-income people can rarely borrow a lot, if at all. And if they get in trouble, it’s with relatively small amounts. Consumers have to be higher-income to be big borrowers.

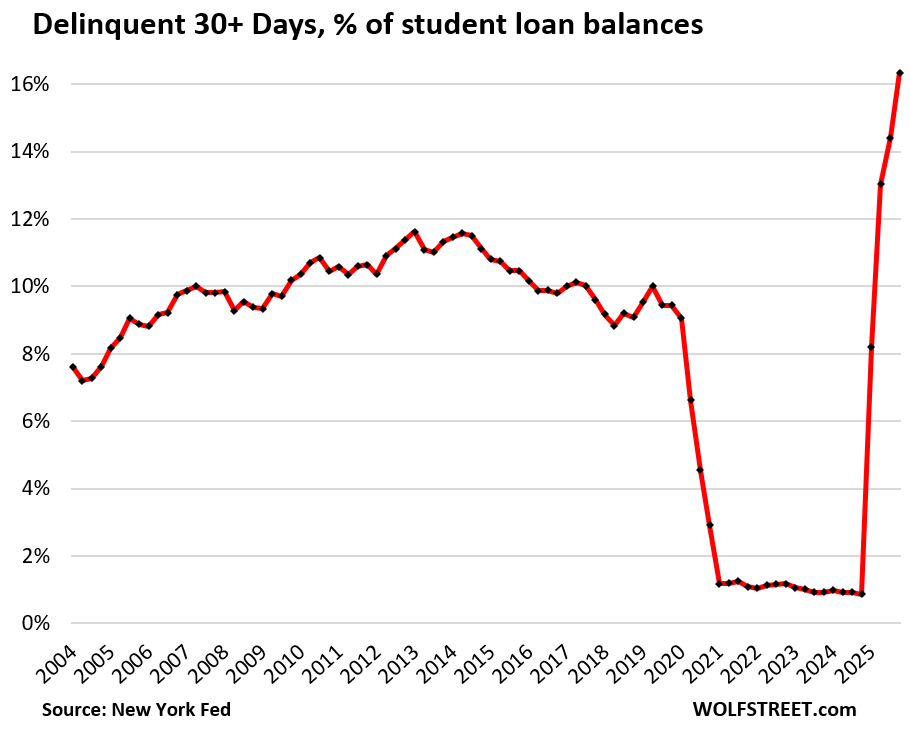

30-day student loan delinquencies continue to spike as defaulted student loans count as defaulted again. In 2025, federal student loans that had been covered by the government’s forbearance policies since 2020 came out of forbearance. During the government’s forbearance program, borrowers didn’t need to make payments, but their loans weren’t counted as delinquent. That’s over. Those federal student loans suddenly showed up on credit reports again, and delinquency rates exploded.

The 30-day delinquency rate spiked to 16.3% in Q4, the worst ever, up from around 1% during the forbearance era, according to the NY Fed’s report today, based on Equifax data.

Of the $1.66 trillion in student loans outstanding, $271 billion, or 16.4%, were 30-plus days delinquent in Q4. The whacky chart below is testimony of bad government policy.

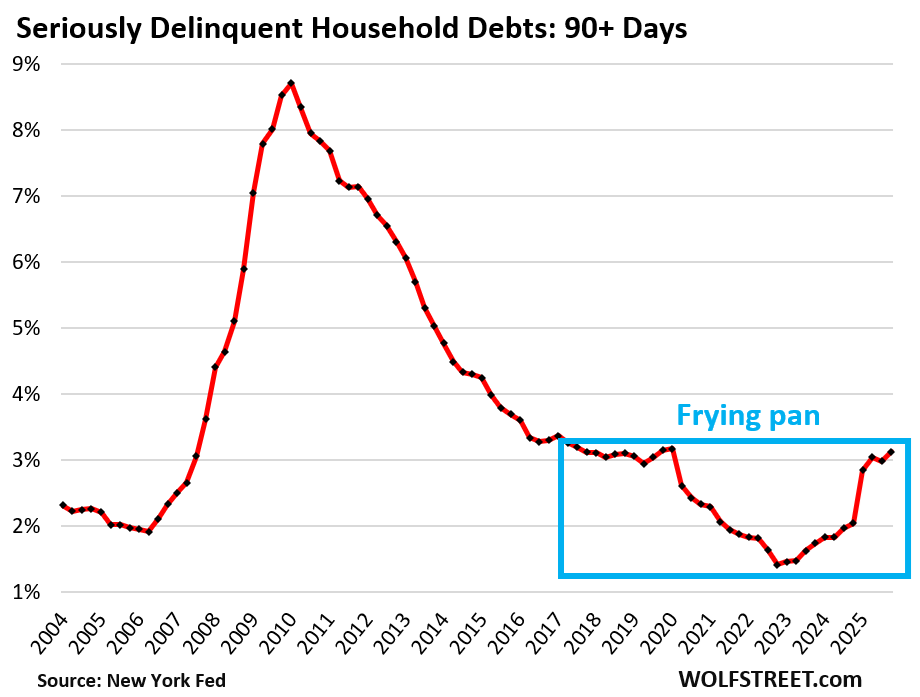

90-day delinquency rate whacked by student loans. The 90-day-plus – or “serious” – delinquency rate rose to 3.1%. This is the amount of debt that was 90 days delinquent at the end of Q4 (delinquency rate = delinquent amount divided by the amount of the debt).

In dollar terms, $586 billion were 90-plus days delinquent, of which $159 billion were student loans, up by about $150 billion from a year ago.

The 90-day delinquency rate for mortgages was 0.9%. For student loans, it was 9.5%. Note how the delinquency rate shot up in Q1 2025, when the first big batch of defaulted federal student loans came out of the woodwork.

I have called this pattern a “frying pan” because that’s what it looks like. It has cropped up in a lot of metrics and is the result of the stimulus era pushing down the metric, and then it normalizes again.

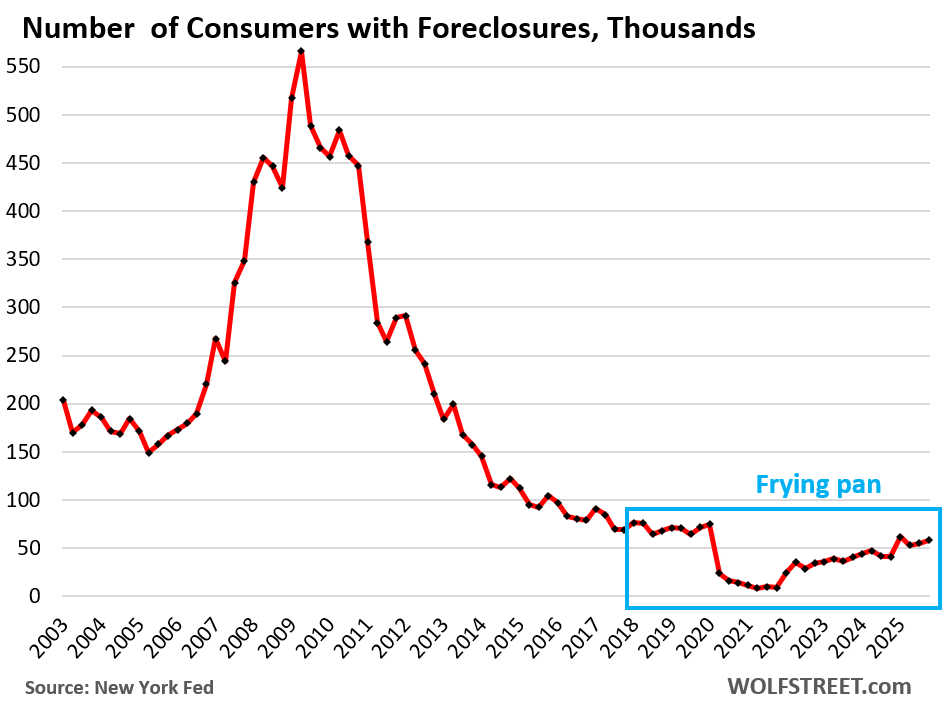

Foreclosures are historically low. The number of consumers with foreclosures in Q4 edged up a hair to 58,140, well below the low end of the 65,000-to-90,000 range of the Good Times in 2018-2019, and was far below the number of foreclosures in prior years.

The increase comes off the artificially low near-zero level during the era of mortgage-forbearance, when foreclosures were essentially impossible. So it’s an increase off those artificially low levels. The current levels aren’t even back to the Good Times normal yet, though they might eventually get there.

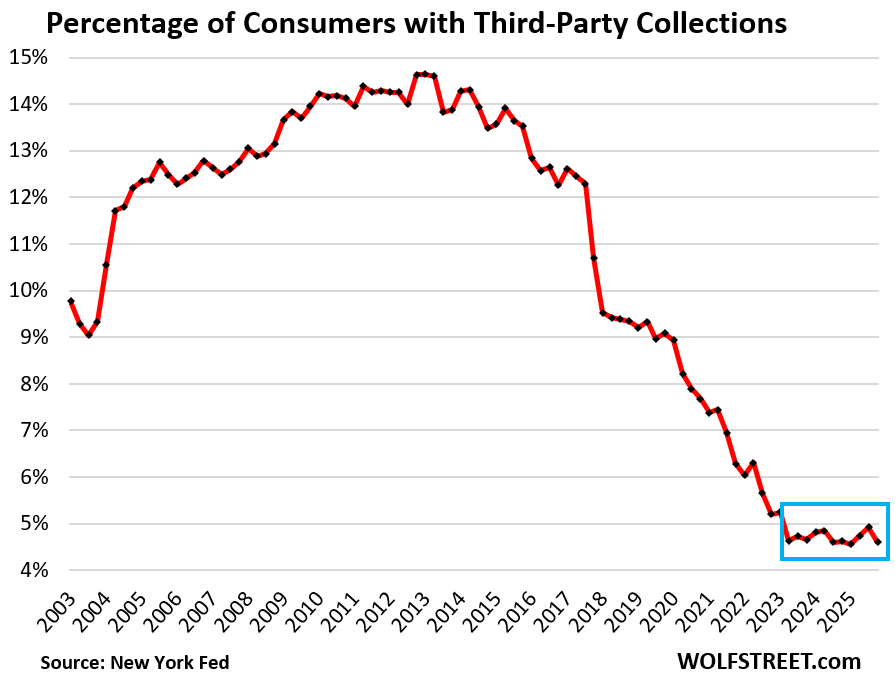

Third-party collections re-hit rock-bottom. The percentage of consumers with third-party collection entries on their credit reports hit rock-bottom again of 4.6% in Q4 – the record low in the data, shared by several prior quarters since Q2 2023, when it hit that level for the first time.

In 2013, coming out of the Great Recession and the unemployment crisis, over 14% of consumers had third-party collection entries on their credit reports.

A third-party collection entry is made into a consumer’s credit history when the lender reports to the credit bureaus, such as Equifax, that it sold the delinquent loan, such as credit card debt, to a collection agency for cents on the dollar. The New York Fed obtained this third-party collections data in anonymized form through its partnership with Equifax.

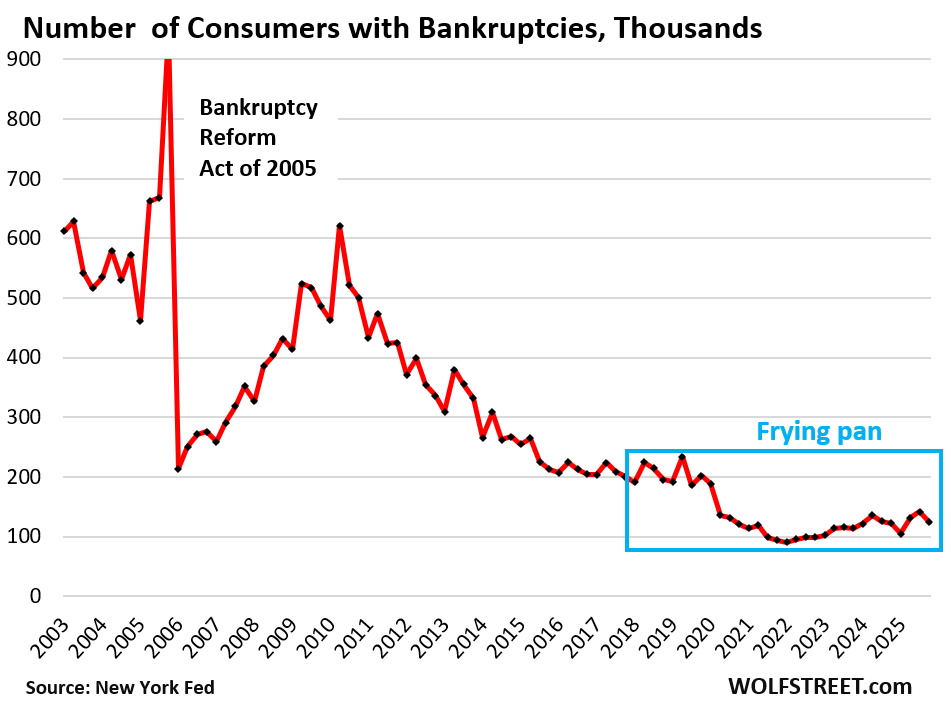

Bankruptcies creep along rock-bottom. The number of consumers with bankruptcy filings fell to 123,820 in Q4.

During the Good Times before the pandemic, that metric ranged from 186,000 to 234,000, which had already been historically low.

I will discuss housing debt, credit card debt, and auto debt in three separate articles over the next few days. Next one up is housing debt.

And in case you missed it: Not Seasonally Adjusted, Retail Sales Spiked by $80 billion, the Most for any December Ever by far, to $817 Billion, the Most Ever

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The average household’s balance sheet appears very healthy, the government’s balance sheet appears very unhealthy. Do you know if there is a historical reference where there was a similar divergence between the two and what the economic consequences were?

Corporate balance sheets are also strung out. In some corners, debts are bursting at the seams, especially PE-owned companies and companies borrowing in the private credit markets. There are huge risks here.

So one of the three economic players – households – is in pretty good shape. The other two — corporate and government — are over-indebted. The Fed has been warning about this for years in its financial stability reports. But no one pays attention to them, least of all the members of the FOMC that set monetary policy.

Prob why all players want 0% interest rates on loans ASAP!

Re finance All That Debt.

Yep, for some reason we refuse to let the bad debt clear. The longer this goes on the larger the chaos when it finally blows up.

Hedge accordingly.

“The average household’s balance sheet appears very healthy.

The government’s balance sheet appears very unhealthy.”

“Corporate balance sheets are also strung out.”

I understand these discordancies can run on for a long time, but does history show they can become permanent?

Pretty good chance a lot of those delinquencies are holding out for the next “bad government policy” by democrats to “forgive” their student loans. Just waiting it out in other words.

One could also consider it bad government policy to have such high secondary education costs. Plenty of countries consider college to be a societal need instead of a debt trap. That said, government policy is mostly bad either way.

Yes, this has basically been our strategy since 2009. Push all pain onto the federal balance sheet, so that it isn’t felt anywhere else, and we can avoid recession.

That works for so long as the U.S. can issue treasury bills at reasonable yields. Quite frankly, I’m shocked that we still have people falling over themselves to lend money to Uncle Sam at 4.2% for 10 years.

Households are credited with low tax rates, subsidized mortgages, a strong dollar, and various other subsidies and incentives that allow them to earn high incomes and float massive debts.

The Government is debited via a rise in the national debt.

Monetarily sovereign government debt is not the same as household debt

Thanks for your work on this. I wonder what the kids are going to do. I read somewhere that starting salaries have dropped. Add in. The threat of AI taking entry level jobs, and the future for the young graduates doesn’t seem good.

“I read somewhere that…”

No, overall starting salaries have not dropped.

But SOME inflated starting salaries for people fresh out of college have dropped from the ridiculously inflated levels in 2021 ($74,000 average with a bunch of graduates pulling $150,000+ lol something wrong with this picture), they’re just coming back to reality. And that one report was on an inflation adjusted basis. Without inflation adjustment, they may not even be lower.

Seems to me that the Federal student loan program has failed and has resulted in nothing but hyperinflated college tuition and piles of debt, and young adults that complain they were victimized and now need a bailout.

Stop the program cold turkey. No more federal student loans, set all existing loans to 2% fixed to pay for the cost of servicing, and let the problem run itself out. If colleges lose customers then they need to improve the product and pricing. A four year degree in “personal identity studies” may not actually have a lot of economic value. Could be worth $20k but not $200k.

Sounds good with one big addition. Colleges MUST have some skin in the game. They need to be on the hook for some losses as well as be accountable for the product they are delivering. Some QC related to the loans.

They would if the federal government didn’t issue student loans and they became dischargeable in bankruptcy again.

Student loans are unsecured. Private lenders would not lend for people to get crap degrees from crap schools if they’d be unemployable and file for bankruptcy.

Yes, agree with you and Ol’B. Get the government out of the college loan business, make the schools bear at least half of the risk, and the problems will take care of themselves, especially the overinflated tuition rates caused by colleges with more employees than students (which is how DEI first got a toe-hold, and now supports “_____ studies” degrees, with the colleges then hiring those graduates to become new staff members and also professors).

I know some young couples are forgoing the formalities of marriage in order to avoid one spouse inheriting the student loans of their partner. They go on with this facade and pay higher taxes as single people forever. The student debt is left UNPAID. They are waiting for an administration to come in and grand “FORGIVENESS”. The rest of the taxpayers and honest people have to pay for this crap.

Vast majority are just paying off their student debts, stop throwing tantrums. Education is free in most civilized countries anyway, it’s the voters choice to put young folks in debt to start their lives.

Who told you its free? I think you’ve had a bad education.

“Vast majority” – did you look at the vertical chart in the article above?

“In most civilizedcountries” – please enlighten us and name these countries where education is free?

Free? What country has all of these professors and administrators serving as unpaid volunteers?

I did read the chart and the text; perhaps you should too. The long-term average 30‑day delinquency rate was about 9.5% on student loans. The recent dip and hike are due to regulatory changes, not changes in payment behavior. First, student loans were excluded from counting as defaulted loans (drop), and now they’re included again (hike). There’s not enough data to suggest that the current hike sets a new long‑term average rather than being a one‑time spike due to regulatory uncertainty.

Next: delinquency ≠ never paying off student loans. Delinquency is exactly that: a failure to pay in a 30 window period, either direct payment failures or through a submission to pause payments. Go ahead, look up how many people never pay off their student loans over the duration of the loan. If you find anything other than “the vast majority pays them off in full over time,” let me know and I’ll call the paper for you.

Lastly, “free” — nothing is free, except being pedantic perhaps. I meant free to the students, not free to society. But while we’re on the topic, we do have the highest cost of higher education among most civilized countries though, so we’re the furthest removed from free that we could get. Again, all by choice.

The “interpretive dance basket weaving” cohort defaulting had always been propaganda. The largest group of defaulters and excessive debt are people who don’t graduate, people at for profit colleges, and lastly people with associate degrees. Its rarely PhDs since graduate school by nature is both already selected out likely failures and isn’t as subsidized.

The failure is simply frontloading kids without much plan or credit, not even colleges who are often forced by states or boards to accommodate as many new students as possible. Also frontloading kids with a debt they can never get out from under, allowing loaners minimal risk.

Yes, I saw this dynamic in person 25 years ago. Even then it seemed odd to me that so many people who were not interested in the academic aspect were partying their way through an extended high school “experience” only to drop / flunk out. It was as if their tuition was subsidizing the low level classes for the rest of us.

Howdy Folks. Live within your means for a happy life. You then will not care what Govern ment or others do. You will be laughing all the way to the bank…. So to speak….

Advice from an old fool squirrel….

THanks, CPT Obvious

Howdy James. Its so Obvious so many cannot even add and subtract.

I read somewhere, but I didn’t RTGDFA…oh no! Oh!

I read somewhere, but I didn’t RTGDFA…ooh, ooh, oo-ooh

And they say it is a capital offense .

(With a nod to Bob Marley and Wolf)

Delinquencies for auto, mortgage, credit card, etc. debt will rise when the government gets serious about garnishing wages and tax returns to service student loans. Current efforts are piddly, at best.

A lot of these people think their student loan debts will just be waived away eventually. The forbearances created a huge moral hazard. I personally have tertiary family members (two second cousins) who haven’t paid a dime on their student loans in six years — their families both bought homes and new cars in that timespan though. Not until these people are whacked with $1,000+/mo garnishments will anything change.

It’s still La-La-Land and Good Times until the student “hot potato” debt actually means something.

According to Ben “I saved the world” Bernanke “debt doesn’t matter”…

LOL! This guy should be tried for treason and violating the contractual mandate with congress. When found guilty, put his head on a pike. So long as we will continue to reward bad behavior nothing will change. We will arrive at the same place the former Soviet Union did in 1990.

Hedge accordingly.

Would be fun to see US broken up into various smaller countries. Not really a constitutional process for that.

Central bankers are useful scapegoats for the politicians.

In that way a person like yourself can simultaneously be pissed at the direction the nation is going, and also remain a fan of the leaders who brought us here.

K. Warsh got the nomination by promising to be the fall guy. It’s the essence of the job.

Reading comprehension clearly isn’t your strong suit. I fully acknowledge that CONgress has not done it’s job. I an definitely no fan of “leadership”.

Why not just tell everyone which bank or financial firm you work for? The paper-pushing era is done. Time to be a really useful engine.

The same thing could (should?) be said about the Treasury debt and deficit spending!

Just wait until they get serious about protecting the currency, and raise interest rates off of zero (in REAL terms)!!!!

Ring, ring: Reality check!

“Oh, what? Yes, I was alive in 2022. It WAS a terrible few weeks for government debt. Hello? MMT? Yes, he’s here. Ok, we’ll get these real rates to zero as quickly as possible.”

(SMDH)

Wolf, what about auto repos? Now at levels of 2008 or 2011, depending on how measured. And private credit, with estimated debt at 3 trillion? Any thoughts? I think so-called “private credit” is largely B-to-B. Not sure. But there seems to be potential trouble here, already surfacing with certain companies.

This auto repo stuff is just context-less bullshit by the crisis clickbait media that keeps getting slung around. Auto loans are fine. You’ll have to wait until I do the auto loan segments in a few days.

Private credit doesn’t belong here. That’s corporate debt. See my comment above on corporate debt.

Wish I could post the screenshot from of the side by side articles in my newsfeed this morning. This one and “Foreclosure bloodbath deepens as banks seize 40,000 homes in just a month – and the pain is only beginning.” Thanks Wolf for reporting the facts and not adding unnecessary embellishment.

Wolf!! Over decades do you think the average American is more financially savvy today than in the past? I think so. Reason is 62% have exposure to equities. Deposits in CDs and Savings at record high. Credit scores are far better than ever. What do you think? Thanks

Probably more savy, but probably less disciplined.

One thing that is hardly being reported by the main stream media is that investors in Crypto are losing their shirts. The price is plunging to zero as we speak. I predict it will get below zero. Many of these crypto contracts are purchased at 100 to 1 leverage. The Crypto. investors are getting margin calls and getting stopped out of their positions. Trumps efforts to make US the Crypto capitol of the world will crash and burn along with the price of all the Crypto stocks which will soon be listed on Wolf’s list of imploded stocks.

Stablecoins are crypto and appear to have at least some strategic .gov/.fed thinking going on. This may go away, but similar thinking at the ECB/BIS and in China/India/Japan suggest some form of crypto is here to stay.

While nobody is using crypto for regular purchases, or to take on debt, the Europeans launched the EuroPA transactions platform to get away from Visa, Mastercard, and American fintech, and they already have tens of millions of users.

BRICSpay is evolving into something similar.

And in just the past couple of weeks, the Chinese announced ambitions to float the yuan.

At some point, the rationale for an ex-USD currency is gone. My emergency fund money is in Swiss francs, not even invested in anything, and I’m up 4.75% YTD against the USD.

“I predict it will get below zero.”

What set of conditions would create that outcome? There are no carrying costs, unlike for a physical commodity, e.g, corn or oil. Sure, those can go below zero if you’re stuck with the stuff and just want to get them out of your silo or storage tank and are willing to pay somebody to take them. But some bytes on a disk? It doesn’t cost anything to just leave them there.

Wolf, any thoughts on household savings and savings rates? Savings rates seem to be dipping below levels that hit before previous recessions, etc. Just curious what you think..

People confuse this all the time. There was an uptick in the “savings rate” during covid. That’s a rate: money not spent divided by money earned. Consumers have continued to add to their pile of savings every single month since then, with a positive savings rate since then, but at a slower rate. Those savings are not going down; they keep going up. What has gone down is the “savings rate.” But it’s still positive.

To see actual cash in bank CDs and money markets, click on the link in the article. Those balances have ballooned in recent years with higher interest rates! People are sitting on an ever-larger piles of interest earning cash.

True but… a low savings rate suggests (but does not guarantee on any timeframe) that the savings rate can only go up. That is, if the savings rate reverts to the mean in the future, it will come out of the savings rate.

Likewise, a high savings rate implies (but does not guarantee on any timeframe) that consumers have more ammunition available to increase their consumption rate in the future. They are stockpiling money that will be spent in the future, and so the future has an economic tailwind.

^ “come out of the savings rate” should be “come out of consumption”

As a millennial, I’m constantly reading how I’m in a minority by being a home owner. Yet these stats look very healthy. Any chance you’ll touch on generational differences in the upcoming breakdowns? I feel like things are not great but not bad for my generation yet people act like owning a home is out of reach for people my age and younger

I just ignore all that generational BS. It’s just fabricated to create clickbait and division.

It’s tough as $@?T thats for sure.

The prices of homes are really high.

Not to mention around 2021-2022, appraisers just decided to add 15% more house to all homes square feet. Making each home on average $25k more expensive.

Houses seem more cheaply made. You prob need to DIY as much maintenance as you can. I follow several DIY channels on YouTube.

Pros cost about 6-8x more that just you and elbow grease + supplies from Lowe’s.

It’s only out of reach for people living in expensive places. I just looked at a 1900sf cosmetic fixer upper with a pool in a B-/C+ neighborhood that is asking $159k in my deep south market with a 4.0% unemployment rate.

In my B neighborhood there are lots of 3BR SFH’s in the $225k range. People in the average neighborhoods of my city pay much less.

So all these influencers who bemoan how they’ll never be able to mortgage a house or start a family are making a decision to live where they live, which is where such things are unaffordable. They’ll justify it with mumbo jumbo about the “good jobs” that in their own markets don’t pay enough to enable home ownership. Actually what they’re not willing to give up is the status symbol of not living in flyover country. Cry me a river, influencers.

all that publicly traded corporations have to do, is stop the share buybacks/repurchases to get their debt down. Govt needs to start taxing the wealthy again. charts at the bottom bottom make me nervous.

Wolf – thought on why are housing foreclosures/ bk still so low? What fundementally changed from 2019. I recall a moratorium on foreclosure at one point.

When people have jobs, they keep paying their mortgages. And people have jobs! Unemployment rate is historically low, and wages have grown a lot. SO it would take a period of much larger unemployment to trigger more foreclosures.

When prices shoot up, people have equity in their homes, and when they get in trouble, they can always sell the home, pay off the mortgage, pay the brokerage fees, and walk away with some cash. So no foreclosures in those cases, even if the homeowners lose their jobs.

Problems arise when prices fall, and homeowners, who lost their jobs, cannot sell the home for enough to pay off the mortgage and the fees. This is always the case somewhere.

There are now many cities where prices have fallen a lot, but employment is still strong, so people keep paying.

You do good work, Wolf.

Thank you.

Student loans can be in several different statuses: In-School, Grace (6 mos after graduation), Deferment (Grad School), Forbearance (Unemployment, Admin-Covid) and Repayment. Repayment is only status where a borrower is expected to make payments and borrowers often move w/in several different statuses.

Q4 2025 FY (9/30/2025) Federal Student Loan Portfolio listed $602.4 billion in Repayment status representing 19.15 borrowers:

Current ( 30 days delinquent: $169.2 Billion (28.09%)

6.58 million borrowers (34.36%)

$25,714 avg. borrower balance delinquent

Many of these borrowers have not made payments since 2020 and several of them were defaulted prior to 2020 and granted special forbearance to bring them current so that cohort may have not made a payment in 10+ years.

Many more borrowers are still awaiting their return to Repayment status from Administrative Forbearance. These borrowers opted into a Biden era Student Loan Repayment Plan called SAVE that in many cases represented interest payments of no, partial or full interest payments due and almost no principal payments and no past due principal capitalizing on the loan balance. Supreme Court struck down the repayment program but many borrowers have not been placed in a less favorable repayment plan proposed.

Q4 2025 Administrative Forbearance: $490.4 billion 8.98 million borrowers w/ average borrower indebtedness of $54,610.

This cohort has not made payments on their loans for 6 years buying cars and homes and having children which will have an even greater impact on the economy when they are finally have to make payments on the loans.

In summary, delinquency rates are much lower than indicated when only looking at the entire student loan portfolio outstanding vs. those loans required to make a loan payment. Another cohort of borrowers has not transitioned into repayment and although smaller in # of borrowers represent 2x the outstanding indebtedness implying grad students or extended education and higher salaries but probably already at their debt service coverage ratio for other debt taken out.

Trump already pulling back on garnishing wages looking at Mid-Terms and will probably slow walk Admin-Forbearance for same reason just like the Biden Admin. Kick the can!

I’m shocked 40% of homeowners own their homes outright. But I also live in a VHCOL (is there a category higher, lol).

Maybe I’m reading that incorrectly too

I’m not shocked Many people bought their houses decades ago. Even if they hadn’t paid them off early, they’d be owned in full in 30 years. Many do pay them off early.

I know a lot of people my parents’ generation who did pay them off early, simply because it wasn’t worth carrying a tiny mortgage (relative to their then-income) for 12 years and having to deal with the paperwork. There are lots of other people who refinanced into 15 year mortgages to get better rates.

Plus, there’s also family homes that have been owned outright for generations.

You’re thinking through the lens of professional couples under 40 who bought in the past 10 years. The housing market is far, far larger than that.

I read this alarming headline

“Foreclosure bloodbath deepens as banks seize 40,000 homes in just a month – and the pain is only beginning”

And then came here for the reality check. It’s amazing people get paid to churn out that decontextualized crap! Thanks for keeping the books straight.

Great post. So much work goes into these posts. You make difficult material easy to understand. Thank you.