Spike of defaults in January was triggered by two Manhattan office towers; one of them is heading to a foreclosure sale.

By Wolf Richter for WOLF STREET.

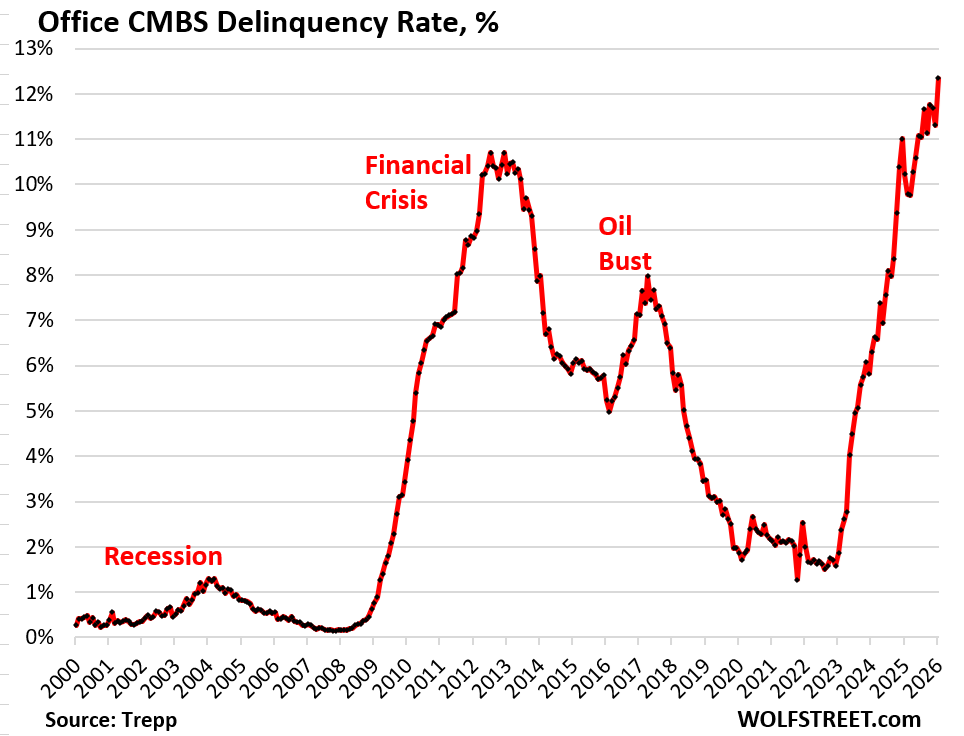

The delinquency rate of office mortgages that have been securitized into commercial mortgage-backed securities (CMBS) spiked by over a percentage point in January to 12.3%, once again the worst ever, and 1.6 percentage point above the worst moments of the Financial Crisis, according to data by Trepp , which tracks and analyzes CMBS.

The CMBS were sold to institutional investors around the world, such as pension funds, bond funds, insurers, etc. The banks that originated the loans are off the hook.

High vacancy rates in new fancy office towers allow companies to move from an old tower to a new tower when the lease expires, thereby upgrading and downsizing at the same time. This “flight to quality” is pulling the rug out from under older office buildings.

Spike of defaults was triggered by two huge Manhattan office towers.

One Worldwide Plaza, $1.2 billion of debt: The 49-story 2.05-million-square-foot tower on 825 Eighth Avenue in Manhattan, built in 1989, includes 1.8 million sf of office space, 30,000 sf of retail space, a five-stage off-Broadway theater, a 38,000-sf fitness center, and a 132,000-sf parking garage.

The $1.2 billion in debt is composed of a $940 million senior CMBS loan and a $260 million mezzanine loan. In January, the property had insufficient cash flow to pay the January 2026 tax bill and make the note payment that was due in December and is now 30 days delinquent.

The landlord – an entity of RXR, SL Green, and New York REIT (New York REIT itself is liquidating) – is already facing a UCC foreclosure auction, triggered by Extell Development which had acquired the $260 million mezzanine debt to position itself to foreclose on the property.

This strategy, and the foreclosure auction originally scheduled for mid-January, got tangled up when the landlord sued to stop the foreclosure auction, calling it a “sham.” Last week, a New York judge ruled for Extell and rejected the landlord’s request to stop the foreclosure auction, and the auction can go forward. Extell is currently the only qualified bidder for the property.

The vacancy rate jumped to 37% in 2025, from 10% in 2024, after the global headquarters of law firm Cravath, Swaine & Moore, with 617,135 sf, vacated the property; and after the Americas headquarters of Nomura Holdings exercised the option to downsize by 75,000 sf to 705,089 sf.

The collateral had been appraised at $1.7 billion in 2017 for purposes of refinancing the building and securitizing the loan in 2017 and 2018.

Last fall, Trepp reported that the collateral was re-appraised at $390 million, a 77% haircut from the 2017 appraisal, and far less than the outstanding $1.2 billion in debt (image via NYRT).

Extend and pretend didn’t work. The CMBS loan was modified in March 2025, allowing it to tap into reserves to fund the property’s operating expenses and debt-service shortfalls, Trepp reported at the time.

The $940 million loan is split across several CMBS deals:

- $705 million, in four slices, make up the single-asset WPT 2017-WWP

- $100 million makes up 11.01% of GSMS 2017-GS8 (part of CMBX 11)

- $50 million makes up 6.09% of BMARK 2018-B1;

- $50 million makes up 4.69% of BMARK 2018-B2;

- $35 million makes up 4.26% of GSMS 2018-GS9 (part of CMBX 12).

One New York Plaza, $835 million loan. The 50-story 2.6-million-sf tower in Manhattan’s Financial District, completed in 1970 and renovated in 1994, went into maturity default in January, when the balloon payment of the loan, due in December, was not made. Until December, the property was current on the interest.

The loan backs the single-asset ONYP 2020-1NYP deal.

Extend and pretend didn’t solve anything. But Brookfield Properties, the landlord, with no further extension options remaining, is still seeking an additional extension, according to CoStar.

The vacancy rate rose to 35% most recently, according to CoStar. The largest tenant is Morgan Stanley (44% of the space), which is trying to sublease a 46,913-sf portion. Its lease runs through 2034. The second largest tenant is the law firm Fried Frank (16%), with the lease running to 2039.

Several smaller loans were “cured” and came off the delinquency list in January. The largest one was the $211 million loan backed by an office property in Plainsboro, NJ, leased by Novo Nordisk US headquarters.

The 770,000-sf location made the news in October with the NJ labor department’s WARN Act disclosures that Novo Nordisk, the Danish pharma giant, would cut 811 jobs at its Plainsboro office by the end of 2025, more than tripling the 265 layoffs Novo Nordisk had publicly announced a month earlier as part of 9,000 job cuts globally.

The loan had become delinquent for the November and December payments amid borrower disputes over force-placed insurance (FPI), according to special servicer commentary in December, cited by Trepp. The special servicer has advanced funds for the canceled FPI, with over $1.68 million outstanding. A settlement to resolve the insurance dispute has been circulated, and a resolution is expected, according to Trepp.

Who is on the hook for office mortgages? A big part is spread across investors around the world via office CMBS (see above), mezzanine loans (see above), CLOs, and mortgages that are held by bond funds, insurers, private or publicly traded office REITs and mortgage REITS, and by PE firms, private credit firms, and other investment vehicles.

Banks hold only a portion of office CRE loans and have been disclosing write-downs and losses for three years, and have been busy selling their bad office loans to investors at big discounts to get them off their books. All this dented their earnings, and some of these banks were big foreign banks that had been pursuing the glories of US office CRE in trophy cities.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Holy Crap!

it’s small investors holding these notes via mutual funds, pension funds and like

banks love them which is why they are so bad for investors

privatize profits and socialize losses(taxpayers)

Well, when you have a media empire (Wolfstreet) being run out of a basement room, what do you expect? Empty buildings.

Top floor executive suite!

I wonder how many billions of dollars are invested in CMBS by pension funds?

Is the Titanic heading straight for the iceberg?

Heading….,already hit it!

Makes me sick to think about it.

Be interesting what happens in long run. These building continue to have significant costs even when empty I assume. Too expensive to convert, too expensive to tear down. Perhaps cities have to ” eat” it after long enough.

I might consider a loan for backstage passes to a really good show, but not for mezzanine tickets.

Like One New York Plaza, developers can redefine the building’s purpose and turn it into housing. If landlords were more proactive this would already be the trend and they’d be making $$$ instead of crying crocodile tears.

Yep, it’s all easily explainable by that physical office occupancy chart from yesterday’s post on WS.

Occupancy dropped to 14% of the pre-pandemic rate in March 2020, then steadily worked its way up until it hit a brick wall at about 48% right after Labor Day 2022. Since then it’s only gone up to about 55%.

The leases involved here are very long duration. In other words, there’s more pain to come in the office sector.

So far losses have been spreadout and the stock market is unaffected. Is there any potential for economic damage here? Or is office space just going to be repriced?

In other industries you’ll see this boom and bust cycle and assets get sold off for pennies on the $ and everything repriced. At a certain point things are low enough that their profitable or so much supply comes off the market slowly demand begins to outweigh supply and prices increase and cycle repeats…. but this feels like a permanent drop in demand paired with a very fixed over supply – so do the builds just end up vacant?

There is absolutely no wide scale impact.

The losses would be distributed to thousands of entities all over the world holding these CMBS.

Ofc, the assets would be repriced.

“At this juncture, however, the impact on the broader economy and financial markets of the problems in the sub-prime market seems likely to be contained.” – Ben Bernanke, March 2008

I turn my head left and right and see levered assets dropping in value all around us at the same time. “CDO” and “CDS” have already been used; what other letter combinations does the does the alphabet contain that in hindsight turn out to be three-letter-words for “exploding landmine”?

Getting twitchy.

It really does seem odd that delinquencies are already higher than well into the GFC, and massive investor losses have not caused any forced selling of other assets, or any other collateral damage, pun intended.

Some office space is slowly being converted into residential, but only in areas with very high housing cost and demand.

It is slow and difficult due to regulatory, financial, construction, architecture, historical, demographic and other impediments.

https://www.brookings.edu/articles/understanding-office-to-residential-conversion/

The drop in value seems way in excess of what’s happened to your in San Diego. I haven’t heard of anything else dropping more than by half in even New York City. Irvine corporation sold the 80s office tower that also has a San Diego symphony building for about half what they paid about $150 a square foot, about 300 paid 11 years ago. At 1:50 a square foot people will really buy heavily as Warehouse space is selling at $350 a square foot and office towers used to be triple the price of Warehouse. Irvine is selling because that part of San Diego is become the home of the homeless.

Irvine is not part of San Diego and not even remotely closed to SD.

The “Irvine Corporation” is not the same entity as the city of Irvine.

Irvine Company owns properties in cities other than Irvine.

Irvine *Corporation* is actually permitted to buy and sell outside of the place they are named after.

Dude, SoCalBeachDude, not a brilliant post considering your handle.

You’ll be encountering challenges when trying to fit a fully autonomous storage system that needs a few stories of hight into an office building.

Even a “dumb” warehouse needs access for forklifts.

The crazy thing is that investors got very crappy yields relative to the risk for many of these CMBS bonds.

As you often write, ZIRP turned these people’s minds to mush.

Office CMBS is blowing up – Yep! And that is bad.

But the real scary story is the buildings didn’t ghost themselves. Workers bailed — proudly — turning WFH into a belief system. – Ideology has come home to roost.

The office was “obsolete.” – The commute was “oppressive.” – Presence was “optional.” And their companies let them have it thier way.

So for now, the towers will remain dark, the loans delinquent, and everyone’s pretending this is a real‑estate story.

It’s not. – It’s a labor story — and a self‑inflicted one especially in blue cities, of course – NYC, SF, Seattle, Chicago.

In the end, the loans will get reworked, the buildings will get repurposed, the cities will eventually retrofit their way into something else… but the workforce that made itself optional doesn’t get a retrofit any time soon.

AI will continue to walk straight through the door workers propped open. – Same tasks. – No drama. – No politics. – No PTO days.

Workers? Did workers overbuild office space? Did workers inflate prices of office space into the absurd?

In what world are companies not glad for not having to pay for offices for their employees. Or even for not having to pay high salarys to offset high living expenses population centers.

Workers didn’t just decide one day that WFH was better. Most were told in 2020 that if they didn’t stay home they were going to get sick and possibly die. So they stayed home, upgraded their home internet and office chair, and realized it made sense four out of five days to just work from there. Log in and get down to business.

These big empty office towers can’t be easily converted into residential. But they could make great data centers with some power upgrades. Maybe the first 40 floors should be computers crunching away 24/7 in the dark and the top ten floors refurbished and leased as office space for hybrid workers and the executive suite.

@toby – “Workers? Did workers overbuild office space?”

You’re answering a question I didn’t ask and missing my point.

My point is about behavioral causality, not blame. CRE didn’t implode because of blueprints — it imploded because a labor shift removed the demand those blueprints assumed.

Sure, no offices, no employees and ghost towns … what could go

wrong.

@Ol’B – “Workers didn’t choose WFH — they were told to stay home in 2020.”

Actually, WFH started swelling well before COVID and many cities and businesses chose to keep workers in the office.

The part you’re skipping is what happened after the over hyped emergency ended. A temporary mandate turned into a permanent preference, then into a cultural identity.

WFH didn’t stay because of virology — it stayed because millions of workers decided the old model was optional. That’s the labor‑side shock I’m pointing to.

Your data‑center idea only reinforces my point: when humans vacate the space, machines move in.

However, EASILY Converted – nope. Have you ever toured one? They are monsters to build from the ground up not to mention retro one hundreds of feet high. The HVAC alone is a nightmare. We won’t see one done.

@Mick – “Are you suggesting AI wouldn’t have happened without WFH?”

No — AI was coming regardless. What WFH did was remove the friction that used to slow automation.

When workflows became fully digital and supervision became virtual, it became obvious how many tasks didn’t require a human in the loop.

You’re right that some office rituals were nonsense. But those rituals also masked how automatable certain roles were. Once the rituals disappeared, the automation math got brutally clear. That’s the door I’m talking about — not hype, but opportunity.

And some of the rituals kept people connected as humans, socially but now we see depression and isolation spiking.

Are you suggesting AI would not have been hyped to the moon without WFH? Or that there would have been any supplication level from the workers that would have been sufficient for the bosses to not try to juice the company’s stock price by announcing AI layoffs?

What WFH exposed was that 90% of the office rituals are utterly useless cargo cult management practices, the days filled with dead time (from the business benefit perspective). The trick, of course, is how to find out the 10% that is actually crucial. So the more clueless organizations waste everyone’s time with endless motivation-draining Zoom/Teams/Slack meetings, or ever-increasing reporting requirements, or “info sessions”, or remote monitoring the workers’ keystrokes, never admitting that they are actually useless at what management is actually about – and after a few years try to issue back to office edicts because they don’t know what is going on and why nothing “just works” the way it used to.

WFH stayed because it made sense for a lot of business and a lot of workers.

Times change. At one time we were all feudal serfs manually slaving on farms…should we go back to that?

@Gaston – “Times change. Should we go back to being serfs?”

Nobody’s arguing for serfdom or cubicles. I’m pointing out that every labor shift has a cost, even the ones that feel liberating.

WFH made sense for many people — agreed. But it also made a large portion of the workforce physically optional, and once you make yourself optional, you shouldn’t be shocked when companies eventually treat you that way.

This isn’t nostalgia; it’s consequences.

I agree that a company should always determine the value of their employees output whether physically in an office or WFH. That never changes.

Maybe you didn’t mean to but you seem to make the argument that workers shot themselves in the foot. I’d say they used their end of the bargain for conditions beneficial to them. It would be like telling someone to take a lower pay package because they may fire you in the future because of it.

I don’t think being physically present makes you less likely to be replaced with AI. I think that is false hope but that’s just like my opinion man

The other part of this story is that office worker productivity went up after WFH went into effect. Workers applied their commuting hours and water cooler gossip hours to doing useful work. Meanwhile, the cultural shift led to the cessation of a lot of meetings that could have been emails and other rituals.

S&P500 profit margins hit an all-time high at the peak of WFH in late 2021*. Then they corrected as dinosaur managers insisted on a RTO so they could again manage people with their 20th century butts-in-seats / “management by walking around” methods. Still, not everyone RTO’d and so S&P margins have not yet fallen below the highest point of the booming twenty teens.

So what really happened? An entire culture realized that networking and communication technology advancements meant it was no longer necessary for employees to drive from their homes to centralized buildings to make edits to data in computers. This freed up the economic cost of commuting (tens of thousands of dollars per year for many urban knowledge workers) to be split between workers and stockholders, at the same time it reduced expensive overhead expenses from maintaining a physical office. New remote management techniques were invented to capitalize on these gains – at least in the less-backward companies.

So yea, most office buildings are obsolete now. We’re near full employment with galloping GDP growth and also at peak vacancy rates. Downtown areas are about to enter another 30 year cycle of being ghost towns, with these empty towers looming over them.

Source: https://dqydj.com/sp-500-profit-margin/

@Chris B, – “Productivity went up, margins hit highs, WFH was efficient.”

I’m not arguing spikes or a lot of other things being brought up here. Missing the point.

You’re describing the short‑term upside; I’m describing the long‑term structural shift.

Only one of them collapses office towers and creates ghost towns.

Workers are to blame for CRE meltdown as

Voters are to blame for bad politicians.

It’s always the fault of the little guy, which is why all power and wealth is to be concentrated to the few.

Seems to me the insurance taken out on those loans, you know those pesky credit default swaps should have exposed this little ruse long ago but nary a peep that I can see. Whoes paying out on those and how bad did those spreads blow out? . Just another in a long list of let’s play hide the schitt sandwich all over again. In order to fix something is broken, you would think they’d at least identify the break and go from there, but no. All seriousness aside, and the builders continue to build…. Oh my! Only in the matrix.

So much for “survive to 2025” eh?

“Make it to 2027 before the debt goes to heaven?”

Hahah, but I think unpaid debts have an alternate destination :-)

The Fed?

NYC mayor can take it over and provide free office and residence space. Current tenants with leases can pay an additional tax to make it work, and he can forbid them to leave. Problem solved by the warmth of collectivism. Easy peasy.

Thanks to “mark to fantasy” accounting, enabled by The Fed the business cycle and deflation are a thing of the past.

Hedge accordingly.

I’ll try to keep this from being too radical but: I really believe that speculative real estate is the ‘root of all evil’ in cost of living. When you go to other countries capital cities, there simply isn’t the same excess of speculation.

Crazily enough, landlords in other countries want rents instead of just holding assets that will constantly go up in value! This translates to more businesses operating and providing cheaper services because their own [possibly largest] expense is more affordable.

I think most of us here in medium to large cities in the USA can recognize the depressingly common phenomena of empty store fronts in prime locations. Why rent to the comic book and board game shop when you could hold out for a Chase Bank or Sweetgreen that’d pump up the property’s apparent cap rate and let you flip it!

I look forward to seeing a great reset on this and the economic activity it spurs once businesses aren’t getting strangled by rents.

It’s a combination of subsidies (GSE’s buying your 30y mortgage, road expansions covered by city taxpayers) and restrictions (zoning, nonsense codes, NIMBYism) that together have resulted in an explosion of housing costs.

To the extent other countries didn’t orient their whole societies around pumping up asset prices, they have affordable housing.

Fantastic piece by wolf. Great locations for both of those buildings. 825 8th built 1989, the other renovated 1994. Are they considered old now?

Regarding the two posts immediately above, Miguel and Chris B., it would be great to provide specific examples, rather than ‘other countries.’

Painful, but the upside is cheap space for new business ventures. The business cycle continues. Fortunes are made/and lost during times like these. Someone will profit from this and we’ll be reading about them in 10 year’s time…

the problem is that office rents have not come down significantly.

is that part of kicking the can as well? it’s so complicated. Wolf and I live in the SF Bay Area. I was in SF 10 days ago. It’s so depressing. An important big mall, across from the key tourist attraction cable car at Powell and Market, closed its door last week. For SF, it’s an absolute disaster, and will take years to sort out. I wanted the Swedish solution to deal with it, early on, to deal with covid. I think that would have been the better path, but this country is/was so polarized it couldn’t even be discussed. This isn’t even a country now. The balkans.

Thousands of indoor malls have shut down across the US. Dead and zombie malls are everywhere. The business model of indoor malls is dead. I have been describing it in my articles since 2016 under the category: “Brick and Mortar Meltdown.”

They’re converting indoor malls into housing… that’s easy to do because there isn’t much to tear down and most of the land is parking, with no buildings around the perimeter. That’s what is happening all over the country, including in San Francisco. The Stonestown Mall, the largest one in SF, is getting over 3,000 housing units and a shopping “Main Street.” And that’s easy to do because it has huge parking lots.

And that’s a good thing. And I’m glad to see it. There is nothing depressing about it. I have always hated malls. They’re huge gigantic depressing properties that are eyesores. Shopping in them is an endless aggravating waste of time. Malls have completely outlived their usefulness in the age of ecommerce.

The mall you’re talking about is in a very complex property. Part of the land is owned by the SF Unified School District because there used to be school there, so the building comes with a ground lease, which makes it harder to sell. It’s a huge old building, maybe 8 floors high, and there is no parking lot. And because it has such a big floorplate, it’s tough to convert into housing (each unit needs to have windows). But it’s a beautiful building, and they’ll keep it. The lender now owns it. And they may sell to a developer to redevelop it into something other than a mall.

I’m looking forward to it getting redeveloped. I’m sick of malls. Get them outa here. The faster the better. There is nothing depressing about change for the better!

I haven’t been to a mall here for at least 20 years. I agree with Wolf that going there is a waste of time. There is nothing in there for me. They eliminated all the businesses that I used to go there for. Like Radio Shack and photo shops. Now its all catering to teenagers and losers who have time to waste. Malls here are all closing up. Even the food courts are closing up and being replaced by food trucks selling overpriced junk food.

I buy nearly everything on line and from mail order catalogs.

Maybe they can use some of these buildings for ICE detention centers instead of buying warehouses across the country for this purpose. I going to make this suggestion to the powers to be.

Here’s another comment, that Wolf can delete he wants. The Trump company owns 30% of one of the go-to buildings in SF. I think the roof was used in Dirty Harry, in the first scene. The old Bank of America Building. I believe that occupancy is still high. I don’t want to get into politics, or have that in this site in the posts, but it would be fun to understand how all this relates to the Trump company’s buildings in New York City, like 40 Wall Street in NYC.

175 W Jackson in Chicago sold this week. Brookfield asset management the sellers.

Empty office towers, closed malls, and shutting movie theaters might look like progress, but its actually a warning.

SOCIETY is the economy stupid.

Down-towns are turning into ghost-towns with people walking around, doom scrolling, covered up in black hoodies and dark sunglasses – Don’t talk to me.

Local shops are disappearing, and the everyday interactions that spark ideas, friendships, and families are fading fast.

Birth rates are crashing and the wealth gap is growing.- But hey Porn-Hub is crazy busy.

When people stop connecting—it hurts jobs, growth, and creativity. – Uber up some robots and AI software please.

Man walked out of the cave once—and now he’s back in it – in a recliner – never leaving home to eat, work, or play.