The five-month surge is a sign of strong business investment, partly driven by the AI infrastructure buildout.

By Wolf Richter for WOLF STREET.

Orders for durable goods reported by manufacturing plants in the US fired on all cylinders in November, rising by 5.3% from October and by 12.3% year-over-year, including huge orders for civilian aircraft, a very volatile component, according to data from the Census Bureau today.

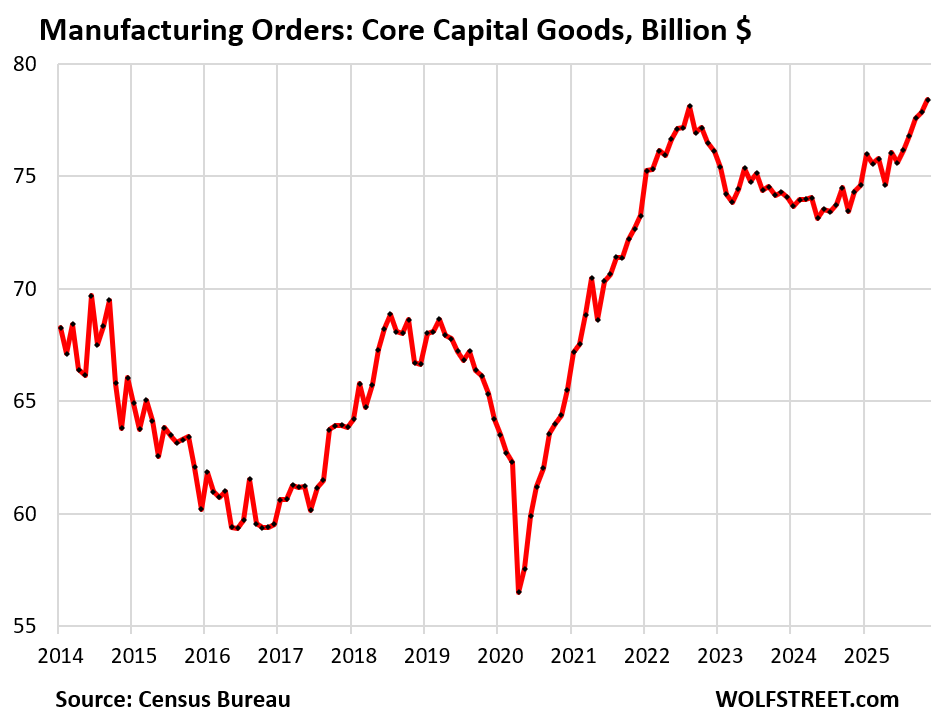

Orders for core capital goods (“nondefense capital goods excluding transportation”) are particularly interesting because they reflect future investment expenditures by businesses and more broadly, domestic business conditions in the manufacturing sector.

Orders for core capital goods rose by 0.7% in November from October, by 3.7% over the past five months, and by 5.5% year-over-year, to a record of $78.4 billion.

Manufacturers of core capital goods include manufacturers of fabricated metals, machinery, computer and electronic products including semiconductors, electrical equipment, and others.

They’d shot out of the lockdown, amid shortages, distortions, and inflation from mid-2020 through August 2022, then declined for two years. But in mid-2024, they started rising again, and over the five months, they have surged and in November hit a new record, surpassing the old record of August 2022:

The surge in orders over the past five months is another signal of strong business investment fairly broadly, but also related to the buildout of AI infrastructure that has been going on for some time.

Orders for fabricated metal products rose by 1.0% in November from October, by 3.9% over the past five months, by 5.5% since March, and by 5.3% year-over-year, to a record $42.4 billion.

Industries in the Fabricated Metal Product Manufacturing category (North American Industry Classification System NAICS code 332) use processes such as forging, stamping, bending, forming, machining, welding, and assembling metals into intermediate or end products, other than machinery, computers and electronics, and metal furniture.

Also note the 8-month 5.5% surge since March:

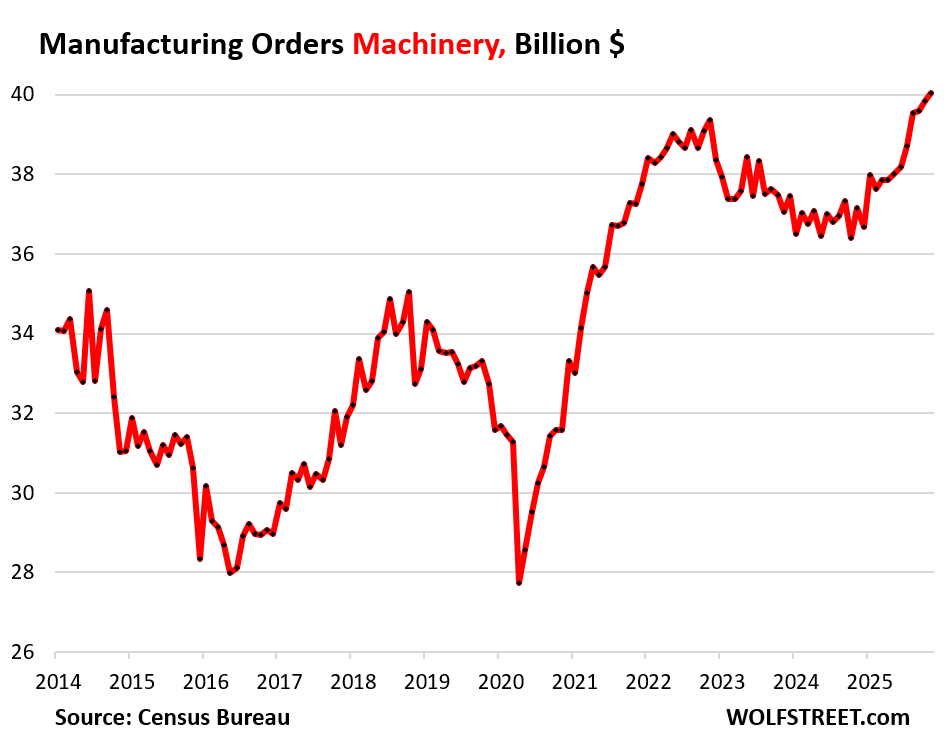

Orders for machinery rose by 0.5% for the month, by 4.8% for the past five months, by 5.8% since March, and by 7.7% year-over-year, to a record $40.0 billion in November.

Several of the subsectors below supply the AI infrastructure buildout.

Industries in Machinery Manufacturing (NAICS 333) consist of:

- Agriculture, Construction, and Mining Machinery Manufacturing

- Industrial Machinery Manufacturing

- Commercial and Service Industry Machinery Manufacturing

- Ventilation, Heating, Air-Conditioning, and Commercial Refrigeration Equipment Manufacturing

- Metalworking Machinery Manufacturing

- Engine, Turbine, and Power Transmission Equipment Manufacturing

- Other General Purpose Machinery Manufacturing

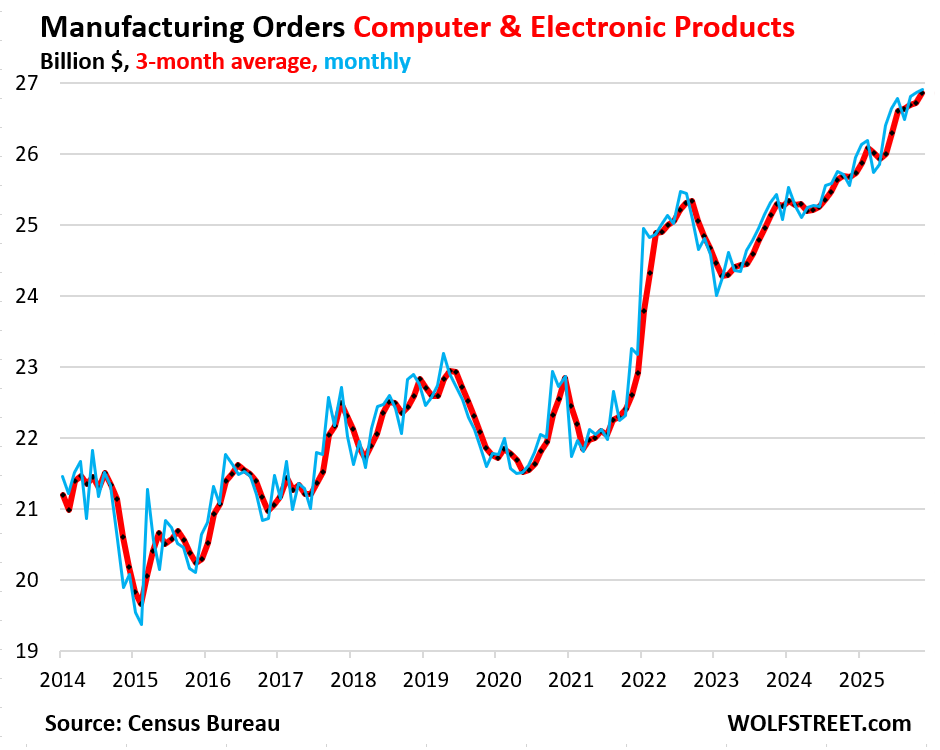

Orders for computer and electronic products rose by 0.2% for the month and by 5.3% year-over-year (blue in the chart below).

This is volatile data with big monthly up-and-down squiggles. So the chart below also shows the three-month average, which irons out the squiggles and shows the trend better (red).

The three-month average rose by 0.5% in November from October and by 4.6% year-over-year.

Industries in Computer and Electronic Product Manufacturing (NAICS 334) consist of:

- Computer and Peripheral Equipment Manufacturing

- Communications Equipment Manufacturing

- Audio and Video Equipment Manufacturing

- Semiconductor and Other Electronic Component Manufacturing

- Navigational, Measuring, Electromedical, and Control Instruments Manufacturing

- Manufacturing and Reproducing Magnetic and Optical Media

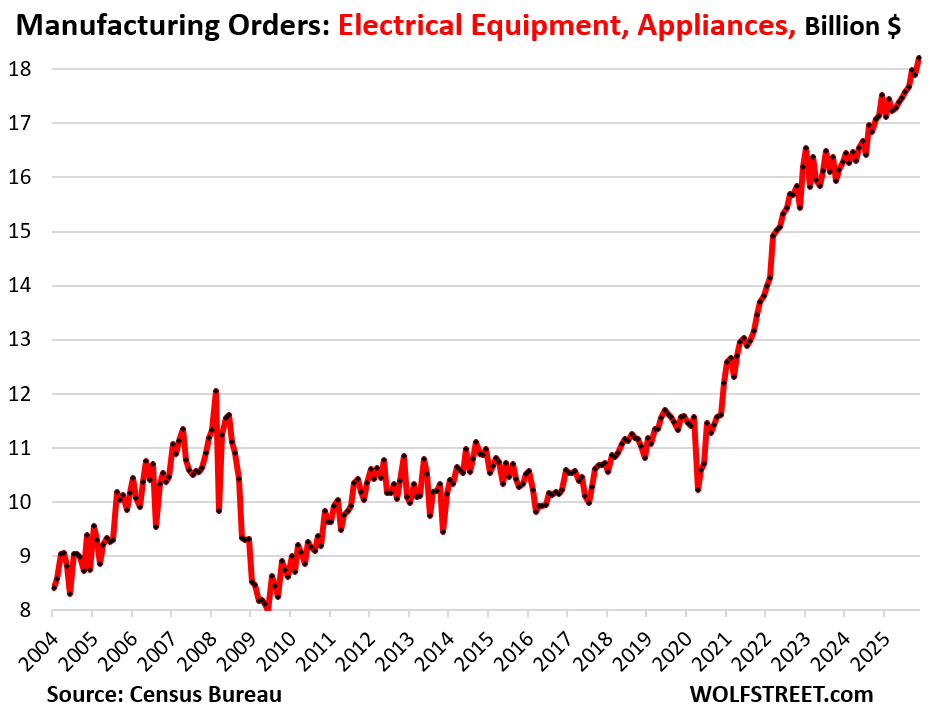

Orders for electrical equipment, appliances, and components jumped by 1.7% in November from October, by 4.2% over the past five months, and by 6.3% year-over-year to a record $18.2 billion.

From November 2020 through November 2025, orders have surged by 57%.

Industries in Electrical Equipment, Appliance, and Component Manufacturing (NAICS 335) consist of:

- Electric Lighting Equipment Manufacturing

- Household Appliance Manufacturing

- Electrical Equipment Manufacturing

- Other Electrical Equipment and Component Manufacturing

As we have seen in other data, part of this economic growth is fueled by strong business investment, in part driven by the AI infrastructure boom. It takes a while for the announced AI infrastructure projects to actually turn into orders for manufacturers, and that boom of announcements in 2025 – the portion of projects that will actually come to fruition – will turn into orders for US manufacturers over time.

It’s hard to imagine an economic slowdown until this business investment boom fizzles.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I think it continues until something happens to make people realize that their “AI investment” is not actually turning into revenue, at which point investors start defaulting on capital calls, banks start tightening lending standards, and the wheel come off.

Expand this logic to all the other business investment, which relies on the assumption debt-fueled consumers will be able to keep buying.

Is it possible that the Administration’s boasts about growth are true? more inward investment leading to higher employment demand. run it hot is the goal, I believe, but we seem likely to see strong numbers, at least through the mid terms

“It’s hard to imagine an economic slowdown until this business investment boom fizzles.”

As you mentioned, there is a lag time before the funding for projects materializes into orders. What happens if PE investors begin to pull money at a faster clip or interest rates rise significantly? There’s already considerable worry that mark to market is hiding the true value of assets.

There have been bubble concerns for a while. And when this bubble implodes, it’s over. But that isn’t happening yet. The investments keep piling in.

I said this in Nov 2024:

https://wolfstreet.com/2024/11/10/we-might-not-get-our-recession-until-the-ai-spending-bubble-implodes/

And again in Oct 2025:

https://wolfstreet.com/2025/10/10/is-it-really-different-this-time/

It’s not over until the fat lady sings.

Agreed, though one note of concern is that this appears to be a lagging indicator (by about 6 months) compared to the stock market.

AI = Atrocious Idiocy

I wonder how much of this investment is being pulled forward in time. The counter-narrative, based on things like the business surveys and hiring rates, is that there’s too much chaos and uncertainty right now for businesses to do any real investing, but plenty of reason for them to do some stockpiling (see for example: 100% tariffs on Canada).

A couple of different people I read also think the AI bubble will blow this year; probably led by an OpenAI bankruptcy. Meanwhile, “Gold Storms Past $5,000” based on geopolitical chaos and the “debasement trade”, according to Bloomberg. Who needs entertainment media anymore when we have the news.

“Gold Storms Past $5,000”

As a in hand stacker of gold and silver this does not make me feel good.

>Who needs the entertainment media anymore when we have the news.

I have been thinking that too… just remember it’s designed to pull you in just like a good TV show

This is true. I notice that they both use the same strategy too: I’m sitting there watching it going “this is so f***king stupid,” and I can’t look away. Is that intentional?

Business investment outrunning consumption growth is a classic recession story: “Oops, we built too much capacity”.

The part I can’t wrap my head around is inflation. All those nominal charts would need to go up and to the right even if there was no trend and it was just prices rising at 2% per year. Similarly, nominal consumption would look like a rising trend even if everyone bought the exact same things each year.

But yea, even the inflation adjusted metrics I look at show a rising trend of real consumption and business investment…. and debt. This can work as long as productivity increases, but spending can also outrun productivity.

This country hasn’t had a traditional “business cycle” recession since the “deficits don’t matter” attitudes started over 40 years ago with Reagan. You can enjoy a lot of prosperity endlessly charging significant items to the national credit card.