The “rate check” on Friday to put a floor under the yen was the latest step.

By Wolf Richter for WOLF STREET.

On around midday Friday came the latest step, a “rate check,” with which Treasury Secretary Scott Bessent attempted to put a floor under the yen that had plunged against the dollar, and push back down long-term US Treasury yields that had surged, as he saw the turmoil in the Japanese bond market, and the plunge of the yen, bleeding over into the US.

The New York Fed, at the request of the Treasury Department and acting as fiscal agent for the Treasury Department, asked its primary dealers what exchange rate they would get if the NY Fed started buying yen through them. This “rate check” was a signal that the US government is ready to intervene in the currency market to support the yen against the USD.

As soon as this happened around midday Friday, the USD began to plunge against the yen, and the yen jumped from 159.2 yen to the USD to 155.7 by Friday evening (hourly chart via Investing.com):

On Wednesday, Bessent had blamed the surging long-term US Treasury yields on the bond-market meltdown in Japan, during which the 30-year Japanese Government Bond yield spiked by 42 basis points in two days and drove it to 3.91%, the highest since the 30-year bond was introduced in 1999. The crucial 10-year JGB yield surged by 15 basis points in two days. And the yen re-plunged against the dollar. The trigger had been Prime Minister Sanae Takaichi’s call for increased government spending with simultaneous tax cuts.

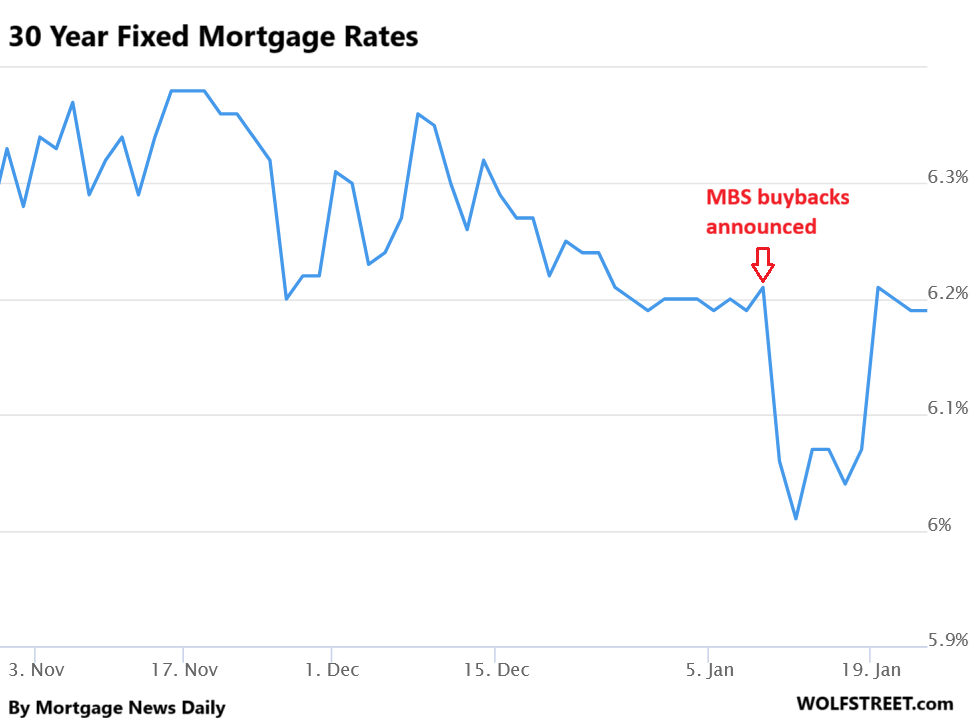

The 10-year US Treasury yield had surged to 4.30% on Wednesday morning, up by 17 basis points in a week, even as the Trump administration is trying to get mortgage rates to come down. But mortgage rates track the 10-year Treasury yield, with a varying spread. And this surge of the 10-year yield caused mortgage rates to jump back to 6.20%, from 6.01% a few days earlier, according to the daily measure of 30-year fixed mortgage rates by Mortgage News Daily. And Bessent blamed that on the bond market meltdown in Japan.

“It’s very difficult to disaggregate the market reaction from what’s going on endogenously in Japan,” Bessent told Fox News at the time. And he said that he’d gotten in touch with Japanese officials, and said that he is “sure that they will begin saying the things that will calm the market down.”

With this two-step three-day jawboning — first on Wednesday when Bessent said he “got in touch” with Japanese authorities, and then on Friday, with the “rate check” — the 10-year yield dropped from 4.30% to 4.23% (hourly chart via Investing.com).

To help push mortgage rates down, the Government Sponsored Enterprises Fannie Mae and Freddie Mac started buying back some of the MBS they’d issued. This started in 2025. But on January 8, this was moved to the front pages when Trump directed Fannie and Freddie to buy back $200 billion in MBS, about the maximum they can buy back under current legal limitations.

But they don’t have the available cash to do that, they only have enough available cash to buy some MBS. They could also issue bonds and then use the cash proceeds to buy those MBS, but that would put further pressure on the bond market. So whatever.

This announcement was a masterful if temporary stroke of jawboning down mortgage rates, which plunged by 20 basis points combined on Friday January 9 and Monday January 12.

It didn’t last long, however. By Wednesday January 20, mortgage rates where right back where they’d been on January 8. They’d just done a big U (daily chart via Mortgage News Daily).

Obviously, Bessent wouldn’t blame the surging long-term Treasury yields on the ballooning US deficit and the flood of new supply of bonds coming on the market that investors will have to absorb, and he wouldn’t blame it on inflation that accelerated further and that worries the bond market. Jawboning is a lot easier to do than to address those issues.

The bond market might not be happy for long with this jawboning. Inflation is a big issue for bond investors as bonds lose purchasing power due to inflation, and yield is supposed to compensate for the loss of this purchasing power, plus some. But long-term yields are too low to compensate investors for hotter inflation in the future.

And inflation keeps moving further away from the Fed’s target, amid government policies of prodigious deficit spending and Trump’s pressure on the Fed to cut short-term interest rates. They want to run the economy “hot,” meaning higher growth and more inflation, which provides fertile ground for inflation to bloom. Given this scenario, the bond market is still very sanguine, surprisingly sanguine, despite the recent ripples.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Still waiting to buy any bond beyond 2 years. I suspect there will be a bear market in bonds for quite a while, no sign of serious deficit reduction. When the administration wants to run the country hot, one doesn’t want to buy bonds.

I was around in the late 1970s in a professional role, it got very ugly for bonds there at the end until Volcker, Reagan and the populace got serious about curtailing Inflation.

If you really want a safe long term bet, it looks like despite all safe deposit box costs and insurance, physical Gold outshine all fiat based government bonds.

Gold plunged by 50% over a span of 3 years starting in late 2011. In its history, gold had huge surges and plunges = risk.

Yep,but to stackers holding for the long run feel tis a good asset to have in the basket along with silver,in hand of course.

I have done very well in that regards recently after holding for years but see no need for fiat at moment.That said,you have a big expense that needs being taken care of feel soon perhaps sell and take some profit.

Volcker never learned a lesson. He injected too many legal reserves again in 1983.

Not even negative nominal interest rates will extricate the government’s largess from the present morass of a cumulative debt > 33 trillion dollars.

President Richard Nixon’s move of devaluing the dollar would work great to raise the value of the yen. Then follow that with Nixon’s famous wage and price controls. Federal Reserve Chairman Burns, I mean Powell, should know how to do this.

I suppose Bessent has dislocated his jaw to be able to open his mouth so wide… Stormy Daniels might be impressed.

I’m sure Mr. Bessent’s husband, John Freeman might be impressed.

Both replies Epic!

The problem is debt and inflation. No one in Goverment is willing to admit what the problem is.

Even recession will increase spending and make the issue worse.

All the chatter about hard assets and our strong economy is just that. It is a big world and we will no longer control the price of anything.

Open trade was the best thing that ever happened for the average person! While we play silly games, the world will finds ways to prosper without us.

I wonder if the US treasury buyback for liquidity went over the plan 2B on Friday by full magnitude(factor of 10). You think we will find out? The exact amount?

10x I am guessing it took 20b to push down the yield on Friday with the US dollar being down ,9% on that day.

If I recall correctly, the Fed has a huge amount of notes and bonds coming due in 2026, something like $9T+. Since US deficit spending is unlikely to be curtailed, most, if not all, of the maturing debt will be financed by new issuance. This figure is just for existing debt and does not include new debt that must be financed.

At what point will supply outstrip demand? And what about the political damage being done, how many of our former allies start selling their UST holdings and start boycotting treasury auctions? Given this backdrop, it’s hard to believe that rates beyond the 2-year will be heading lower. Best guess the 10-yr UST will be priced to yield between 5% to 5.25% by the end of 2026.

I keep watching a number of things. E.g. 1) the crosses of the 3 largest traded currencies (EUR, USD and Yen). 2) the US 10 and 3) US 30 year yield. If these yields and the USD “go ballistic” then it’s time to “enter the lifeboats”.

I am curious to see where all the US yields go when the market(s) has/have peaked. I actually still expect US yields to go lower for a (short ? long(er) ?) while.

I assume that the falling USD/Yen is a sign the yen carry trade is “vulnerable” (to put it friendly). For the time being I don’t worry too much.

Something has to give. That looks like long-standing carry trade. If the Caymans based carry trade begins to unspool in a less than controlled manner, IMHO bonds likely to rocket higher and dollar potentially plummet. This is magnified by potential for other countries to begin treating US like 21st century pariah state.

Do you mean bond prices or bond yields will rocket higher?

Bondholders have little leverage here. They have nowhere to go. Other assets such as stocks and RE are probably even more overvalued, and if bondholders do revolt, the Fed can probably QE or twist them again with full support of Wall Street.

Bonds mature constantly. SOME current bond holders can decide to sit out some of the auctions, and SOME new investors might demand higher yields and wait for those, and that would be enough reluctance on the margins to push up yields. Treasury securities are not a fixed sum, but a constantly growing sum that constantly gets rolled over.

Putting cash on hold still pays over 3.5%.

You can get plane ticket to Ireland or many countries open a bank account and transfer money, buy a home abroad, etc it’s all normal and acceptable to diversify pay taxes here in the USA from returns overseas. Bitcoin is down 3% today when futures open it may be deep red. limit down day tomorrow morning? Will find out shortly. Selling will pickup as the night goes on. The world is paying attention to our affairs, a Vote of no confidence is coming!!!

Waiting for US debt to top 40 trillion. Probably before the end of the calendar year. 45 trillion plus in Jan 2029 as Trump’s term ends.

Hard Assets – what all does that include? Recent article posturing that US small businesses are doing great, but I disagree. I help insure many Midwest small businesses and their reported assets or those available to use as collateral are leveraged at least X2 just to meet operating budgets and payroll. US small businesses are in the black but only on paper and if they start missing loan payments; well good luck to the banks on figuring out who’s in first position to collect because their underwriting standards are less than credible.