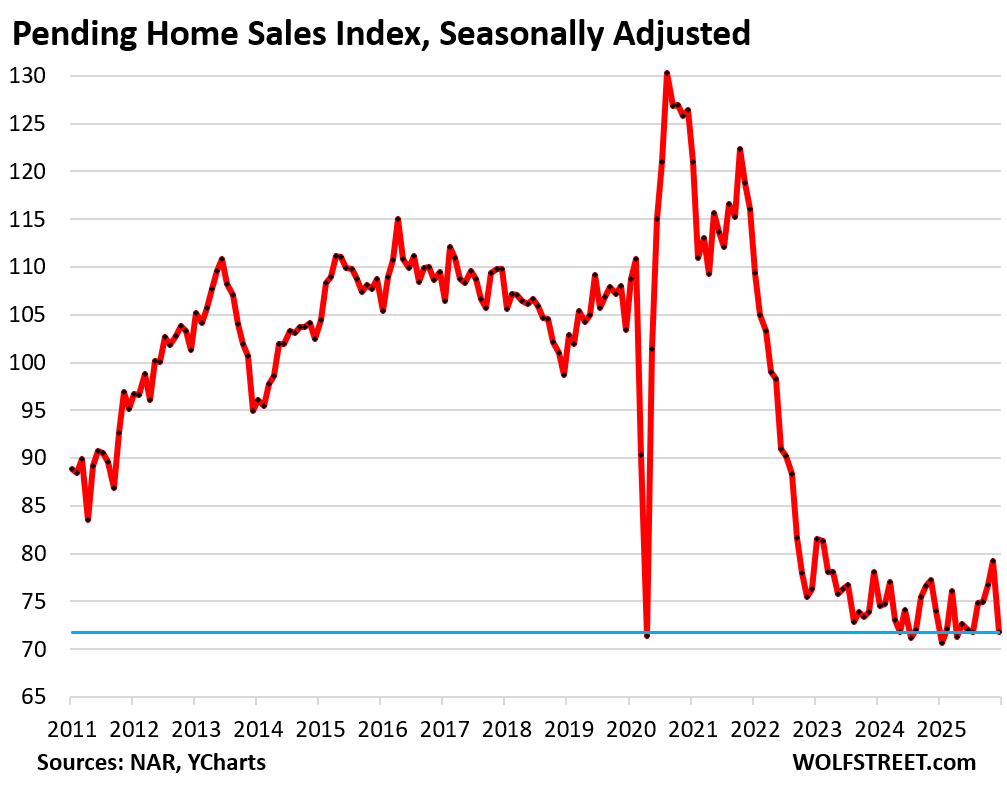

For the US overall, worst sales for any December on record. The housing market took a bad turn, from already low levels.

By Wolf Richter for WOLF STREET.

Pending home sales, which track the number of contracts signed in December, plunged by 9.3% seasonally adjusted from November, to the lowest level for any December on record in the data by the National Association of Realtors, which goes back to 2010. Compared to December 2010, during the Housing Bust, pending sales were down by 21.5%.

The market is now well into its fourth year of the collapse in transactions, and there has simply been no improvement.

Pending home sales compared to the Decembers in prior years (historic data via YCharts):

- 2024: -3.0% (year-over-year)

- 2023: -8.1%

- 2022: -5.9%

- 2021: -38.2%

- 2020: -43.2%

- 2019: -30.6%.

The metric of pending sales tracks contracts that were signed in December but that haven’t closed yet and could still get canceled because buyers cannot afford homeowner’s insurance, or cannot sell their own home, or for other reasons. The rate of cancellations has been running high in 2025.

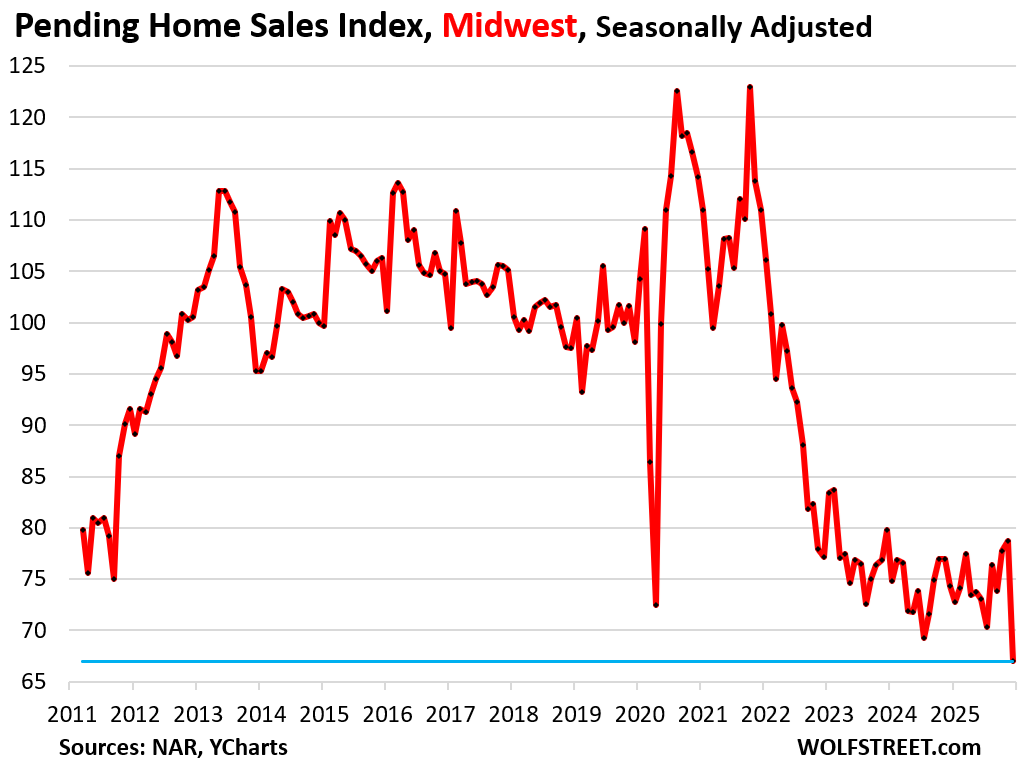

The December downturn in pending sales occurred in all four regions, from already low levels, but was particularly pronounced in the Midwest, where sales collapsed by 14.9% seasonally adjusted to a new record low.

Pending home sales by region.

A map of the four Census Regions is posted in the comments below.

In the Midwest, pending sales plunged by 14.9% seasonally adjusted in December from November and by 9.8% year-over-year, to a new record low level of sales in the data going back to 2010.

Compared to the Decembers of prior years:

- 2024: -9.8% (year-over-year)

- 2023: -16.0%

- 2022: -13.2%

- 2021: -39.6%

- 2020: -41.3%

- 2019: -31.7%.

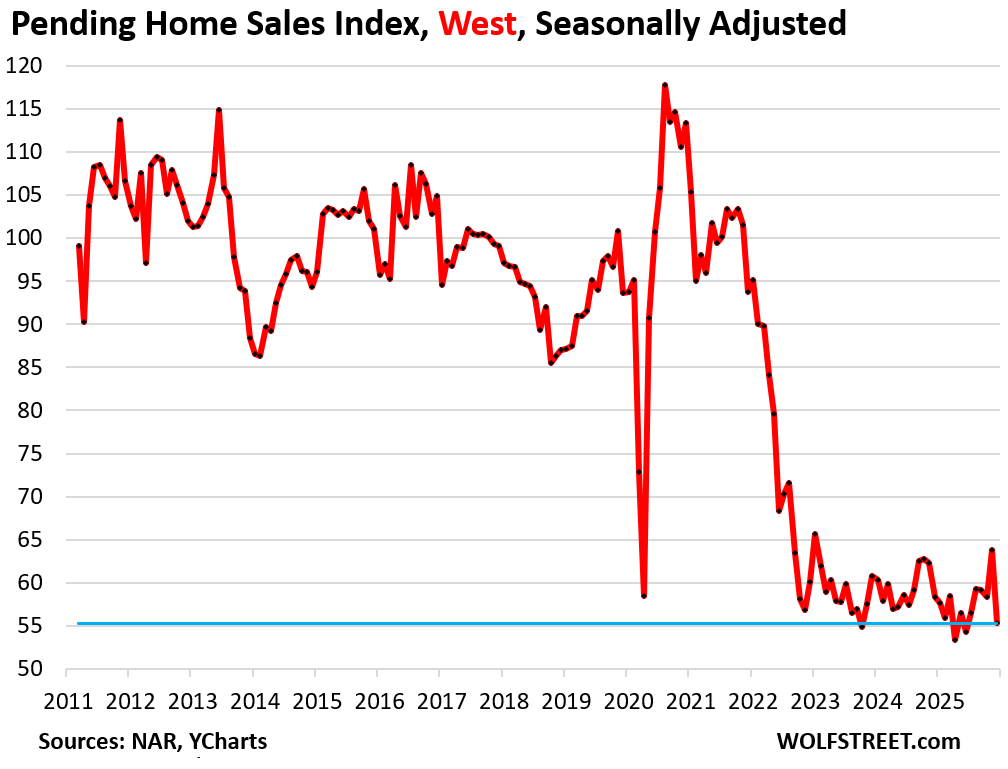

In the West, pending sales plunged by 13.3% in December from November, seasonally adjusted, to the worst level of sales for any December on record, and to the fourth-lowest level of sales for any month.

Compared to the Decembers of prior years:

- 2024: -5.1% (year-over-year)

- 2023: -9.0%

- 2022: -8.0%

- 2021: -41.0%

- 2020: -51.2%

- 2019: -40.9%.

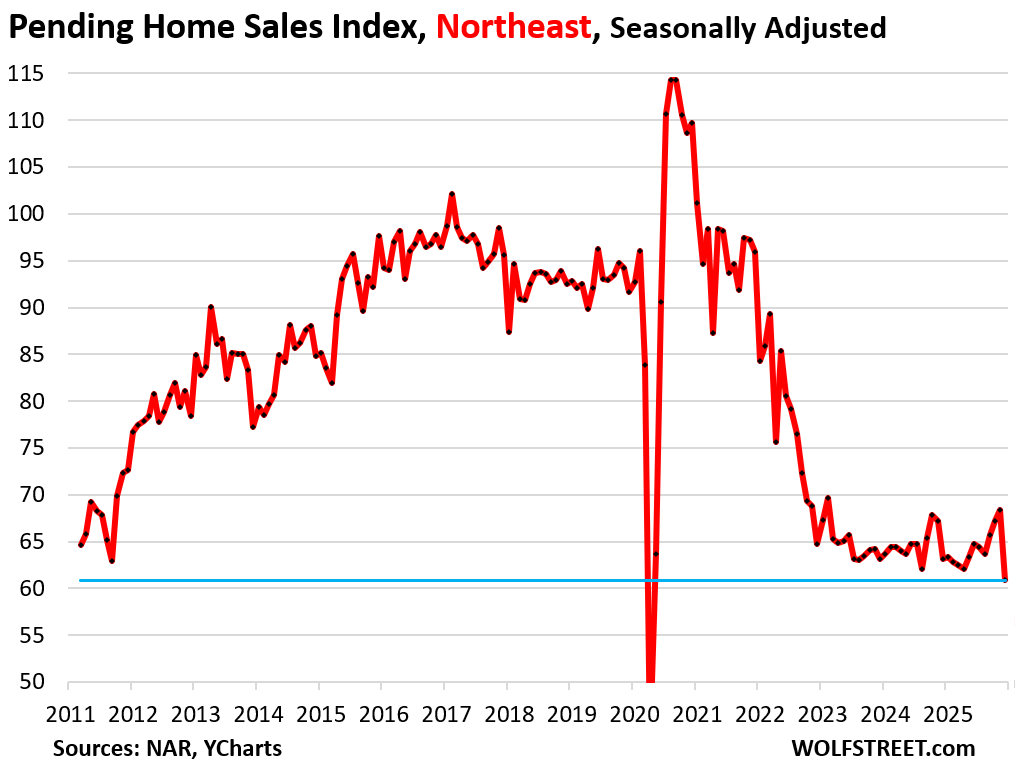

In the Northeast, pending sales plunged by 11.0% month-to-month, to the second-worst level of sales on record.

Compared to the Decembers of prior years:

- 2024: -3.6% (year-over-year)

- 2023: -3.5%

- 2022: -6.0%

- 2021: -36.5%

- 2020: -44.5%

- 2019: -33.9%.

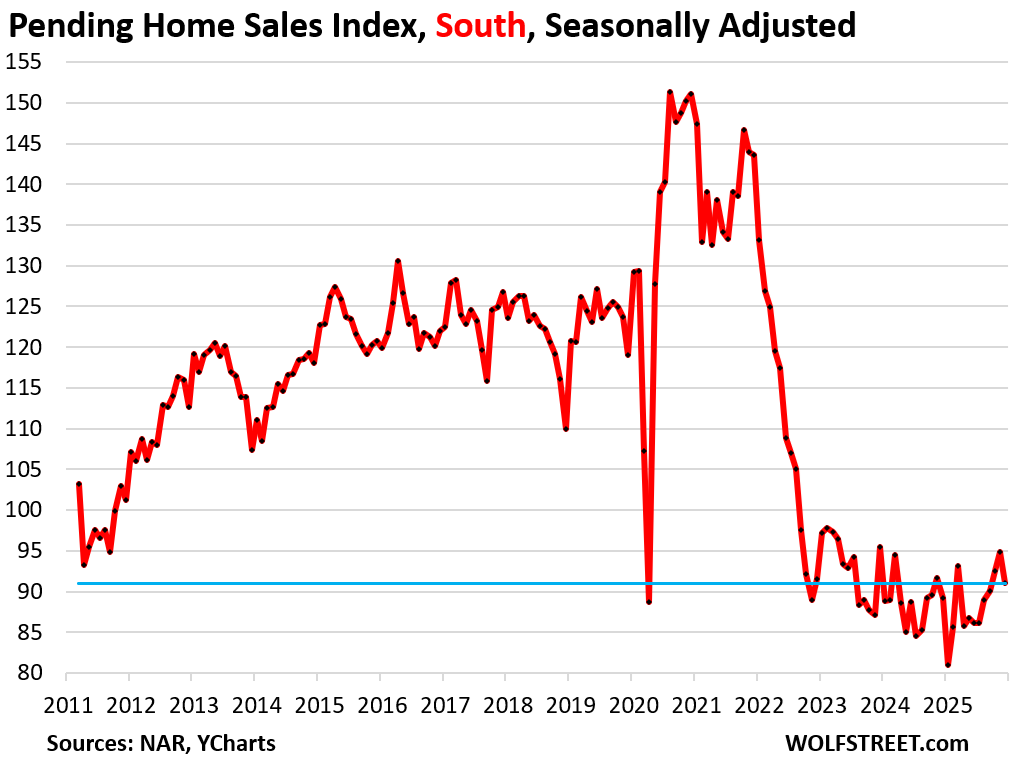

In the South, pending sales fell by 4.0% in December. Compared to the Decembers of prior years:

- 2024: +2.0% (year-over-year)

- 2023: -4.7%

- 2022: -0.7%

- 2021: -36.6%

- 2020: -39.8%

- 2019: -23.5%.

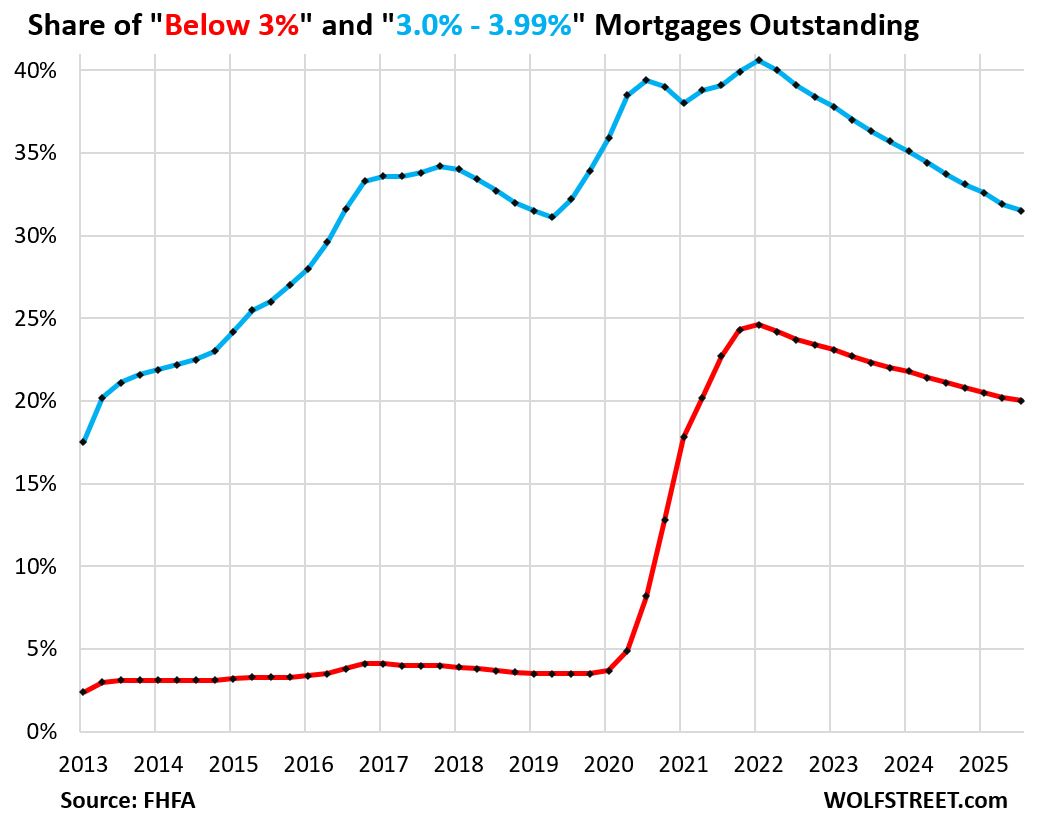

At fault are the ultra-low mortgage rates of 2020-2022 that ended up destroying the housing market in two ways: By causing prices to explode in a two-year time span, and by “locking in” homeowners with ultra-low mortgage rates who now cannot afford to move, which has destroyed the dynamics that come with a functioning housing market, such as mobility, where people are able to move.

The unwinding of the below-4% mortgage rates is occurring, and so the lock-in effect is gradually loosening as these mortgages get paid off nevertheless, but at a snail’s pace [“Locked-in” Homeowners Nevertheless Pay Off Below-4% Mortgages: their Share Drops to Lowest since Q4 2020

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The four Census Regions of the US:

To realtors who may be struggling to find work right now, try these helpful tips:

– cut back on avocado toast

– make your own coffee instead of buying Starbucks

– get a fifth or sixth job like DoorDash for spending cash

– sell some old NFTs you may be sitting on

The Ministry of Truth states “simulations prove the average meal costs $3”, so you should be able to feed yourself on $15 a day. If you find yourself spending more, you’re living a life of luxury with room for cutbacks.

I’m about to enjoy my piece of chicken, piece of broccoli, and corn tortilla shell.

I wonder what I should have for the one other thing?

Add some hot sauce for your fruit portion. The President said tomatoes were fruit back in the 80’s.

If I had a nickel for everytime I’ve heard, “piece of chicken, piece of broccoli, and corn tortilla.” Just saying.

– cut back on avocado toast

Sorry, that one is strictly reserved to blame millenials on why they can’t afford to buy a house….

An Avocado is $2 each.

Toast could be $1

cutting up the Avocado, mashing it and applying it to the toast will be another $10.

With tip let’s just round it to $20 even.

Avocado on a slice of bread is a super cheap meal if you prepare it yourself, and don’t buy the $18.00 version at the cafe. Avocados are good, and good for you. It is also easy to prepare. Take avocado…. place on bread… done!

I am a millennial and own a home and eat an avocado nearly once a day. Avos are good for you. Try them instead of complaining so much for the last few years.

I usually make two slices and slap a few fried eggs on the avocado makes it mo’ better.

Mashed avocado with salt, lemon juice, garlic and chili flake makes an excellent accompaniment to scrambled eggs and is a good source of a

omega complex fats. Not that expensive either

Wolf said, “The market is now well into its fourth year of the collapse in transactions, and there has simply been no improvement.”

I submit that the asking price is too high whereby reality becomes a step behind rather than ahead. The sellers have to lower the asking price by 45 pct.

The economic prognosis by my reckoning is that the accumulation of wealth by those that least deserve it is plummeting towards rock bottom

The population is hungering for a progressive plan to preserve the bill of rights, employ everyone that wants a job, imo the Canadian PM, Carney, made an agreement with the devil

exactly as the Chinese trade Canadian manufacturing jobs in exchange for the low value agricultural jobs. The same mistake the US made.

100% on target

I was waiting to see this exact comment! I’m sick and tired of these kinds of articles and instead I’m waiting for the one that says median price is now in the low- to mid-300k range. Everything else is noise.

And stop buying your daughters so many dolls! We’re announcing a one-doll policy.

This is epic!

We are reaching 4chan business levels here,feel folks have just had it with the insanity(as have I)!

I do not eat avacado toast,perhaps this is why I am a cash buyer?

I’m a Millennial and I’ve literally never had avocado toast. Why would you put avocado on toast? It takes too long anyway. I don’t eat anything that can’t be microwaved in 90 seconds.

I think my family of 4 rarely spends more than $1800 on groceries and we aren’t all that thrifty when it comes to food. I actually think this $3/meal is pretty accurate.

What I don’t know is whether a realtor can afford that right now.

“Pending” home sales “dropping” doesn’t mean that buyers backed out of buying a home listed as “pending” (v. “Contingent”) on Realtor.com et. al.

It means less people put their homes on the for sale market.

The Midwest is bitter cold now and snowy, icy, so few people are looking to buy; therefore, few have listed homes for sale.

Unless I’m missing something.

“Unless I’m missing something.”

Yes. You fell for it. It was December. That stuff happens every December. Over the holidays inventory gets pulled off the market in huge numbers, always. And sales are always low over the holidays. But those figures here are seasonally adjusted, which compensates for the seasonality.

Dec and January have been much colder than last year where I am (Western NY). Heat consumption is up 70% and we haven’t changed the thermostat. Maybe this has spilled over into RE activity a bit.

Brent,

I feel for you. But weather in the huge West has been fairly warm and calm, marked by disturbing lack of snow. So where was the RE activity? Go have a look at the chart above for the West.

Compared with the last decade of generally milder, less-snowy Midwestern winters, 2025–26 so far feels and statistically is colder and snowier in many places.

Snow cover and snowfall totals have been above average early in the season.

Same here in the saintly part of the TPA bay area Bruce.

Born and raised here, but only back a decade to take care of elderly parents.

Veterans Day 2025 was the coldest day in the ten years we have been back, with ”wind chill” below freezing…

OTOH, the crotons in the front (N facing) yard continue to indicate no ”freeze” yet…

Neighbors in the hood say no frost for at least 30 years,,, so far…

Including one lady in late 90s who has been here over 50 years now, still living and loving life by herself,,, and get’s a lot of attention from neighbors and off spring…

It was 70 degrees on Christmas Eve here in Denver, so no such excuses in the Rockies this year. Glad you guys are getting snow out east, could ya send some our way?

Same here Sendug, I’m in northern Colorado but was in FL for xmas, was shocked to come back to warmer temps than the ones in FL! Heck this month FL has technically gotten more snow than our part of CO.

On that same wave-length, December was the warmest avg temp on record for nearly 100 years, so I would also ask you guys to share some snow with the West!

Nobody wants to live in the midwest. lol

People prefer more expensive houses near the coasts.

It’s ambiguous but I don’t think your notion of pending home sales is correct. Pending home sales means of the available homes for sale, how many were pending during the data collection period. As Wolf said, this is then seasonally adjusted to account for patterns that occur at the periodicity in the data. This means that compared to recent Decembers, this year’s pending sales were even worse than usual.

This *could* be due to less homes being listed (less supply) while purchasing *rate* stays the same.

e.g. 100 houses on the market, 5% go pending in Decembers = 5 houses pending; 60 houses on the market *this* December, 5% go pending in *this* December = 3 houses pending. This would be seasonally adjusted but would still appear lower because it’s a weaker-than-normal reading.

But if we think about things like weather’s impact, it’s pretty unlikely weather would differentially affect buyers and sellers. Maybe it would affect buyers more, but it’s also the midwest, where I lived most of my life and things don’t shut down just because of snow. The listing broker would have the place plowed and scooped and salted if they were getting showing interest. The seller doesn’t have to leave their house, since most homes on the market are vacant for sale.

The Census does quarterly surveys about houses vacant for sale (Q4 due out in Feb 2026) that could shed some light on this. Q3 numbers suggest quite a bit MORE vacant homes for sale than usual, so the sales funnel was “wider” going into Q4 than usual.

Tough times ahead. It’s taken 4 years for a 4% mortgage to drop from 40% to 30% of all loans. I can’t imagine it being folks paying off their mortgage, rather locked into a smaller home, or cost burdened.

Good article. Curious to see how this trend will affect those with ARMS.

“Curious to see how this trend will affect those with ARMS.”

I have seen more in the northeast homes for sale for this time of year,some move/many sit,have seen in N.H. some better pricing to a degree,perhaps my time is coming.

I will say as a stacker of pm’s am not sure whether to celebrate and party or cry and bunker down,luckily,both options available.

Me too but then I think better to live life and die than struggle to survive. We only have one life and that too limited time ( at least for old folks ).

Different strokes for different folks but I believe in ‘Die with Zero’.

Die with zero is kind of a silly thought process when end of life care is the most expensive unknown cost.

Die with zero is more like Underestimate because I’m greedy.

End of life care is also overdone. It doesn’t have to be one of the most expensive categories of healthcare, as a society we just make it that way because many people value length of life over quality of life.

In the end, I plan on watching Gunsmoke, the Andy Griffin Show, Murder …She Wrote and The Father Dowling Mysteries from the comfort of my own home. Cheaper ice cream, too.

End of life care = people trying to fight nature 3-6 months too long. Spend your last days in a hospital in agony or put a grandkid through college? I know which option I’ll choose.

It’s why some people travel to WA state, where you can get an injection to avoid the misery. You just need a note from a doctor saying you are terminal, which we all are to varying degrees.

Ah, the Cult of Death. Make them afraid of the inevitable and they’ll pay whatever or do anything to stave it off. But fear not…I expect the good folks at Apple are working on that finality of incineration right now. Just tap the Upgrade button to the IOS 99.9 system and you can be instantly downloaded from that mortal corpse to join the new legions of Cybermen. And for a special introductory enrollment you’ll get 2% back on every planet you conquer in the name of the Empire. Get yours now! Death is dead.

I think there may be a spark of wisdom within the envelope of your hypothesis.

Life, live it or love it

Not bashing on the data or analysis which is always spot on. Appreciate you putting these together, Wolf. Honest question though, is December really meaningful for us since the “prime time” to sell/list is in the early Spring?

For markets like mine it is. When weather is in the 60s and 70s, people go outside more. Look at what happened in 24 with rates from Nov 23 to May of 24 to see what happened then. I’m not saying the rate of change will be similar, but ultimately rates increase through that time frame. Maybe this time is different?

The data is seasonally adjusted. The issues are about the same every December. And seasonal adjustments compensate for it. NAR, which is always painstakingly optimistic, also made downcast comments about the turn of events.

One month is never all that meaningful, it’s just one month, which is precisely why I give you the long-term charts so you can see long-term how that one month fits in.

Investors love holiday shopping. Banks sitting on foreclosures and people who really need to sell are the ones left, properties that after several months have to drop prices to move. Since it’s relative, YOY, it does matter. One thing the above data tells you is that even flippers are not jumping at the reduced winter prices. They’re not at the foreclosure auctions as much either.

The other negative affect and pandemic era distortion caused by the lack of listings listed above. The supply of homes for sale is held down, preventing normal supply and demand adjustments. People wanting to live in desirable neighborhoods will pay the high price. Prices there are frozen at high levels because of the shortage of listings. In less desirable neighborhoods, we’re seeing price plunges as people drop their prices to get bids on their distressed properties.

Yes there is scarcity of supply of affordable homes. Even homes in desirable areas are waiting to be sold as they are priced high.

Sellers can wait, there are buyers out there but can’t afford at current price and/or rates.

I live in Gulfport Florida part of St Petersburg. Homes and Condos between 100K and $450K are struggling. Over 90 days old in the listings. On the other Hand the New 42 Story in Downtown has all of the Condos starting at over 1 million with robust sales. There is another 50 plus storied building with units starting in the $750K and up range that are in progress and over 25% have agreements to purchase. Just an Observation

Why weren’t 100% of all units presold – to then be resold by these condo flippers usually before construction is completed? That’s how it used to be. Preconstruction sales were a big thing. They partially funded those developments. Where are those buyers? Why do developers STILL own those units?

Some developers do not allow re-assignment of contracts, forcing the flippers to close and then re-sell which reduces flipping altogether, but does reduce sales upfront.

All that stuff in Gulfport st. Pete flooded from the Hurricane Helene which has kept prices and sales down. People are still freeked out about round 2 hurricane. Plus the insurance companies took full advantage and tripled rates for homeowners and flood polices which basically cost almost as much annually as your mortgage payments here. I know I live in the area. At least it’s not like shore acres. People are having to vacate in some areas because code upgrades won’t allow them back in unless they raise elevations. It’s a long slow process getting prices way down but insurance companies are surely hastening this process here. Downtown sky rises are built up higher but they will have those inflated HOA’s to contend with too.

From my perspective this housing condo downturn has just begun to rear its head.

And now the Don wants to eliminate investor purchases. Throw that in the mix and watch what happens.

Relief is coming. 50-100 basis cuts coming in a few weeks, combined with corresponding declines in mortgage rates. It’s all part of a grander plan! Plus with midterms coming up all those affordability promises definitely will happen. Time to crack a Modelo.

You still didn’t get the memo? In 2024, when the Fed cut by 100 basis points, mortgage rates rose by 100 basis points! The bond market said: ” Make my day.”

The Fed sets its overnight policy rates, the bond market sets long-term rates including those of MBS, which determine mortgage rates. If the bond market is worried about a lax Fed and worsening inflation, long-term rates go up, no matter what the Fed does on the front end.

Should have labeled my post pure sarcasm!

🤣👍

I thought that was a possibility because you assiduously checked off all the points, but here in the trenches, I think a lot comments are sarcasm, when they aren’t. So it’s always good to note, or deal with the fallout.

I love sarcasm because it lays bare how empirics are ignored by the common man in search of easy anything.

LOL at your narratives….there’s always /REbubblejerk that will be more welcoming to your point made here, I am sure they will be in agreement to the same sentiment, afterall you often find posts mocking any caution that this bubble will burst soon or some major price correction.

I cant let

You need to drink the whole case. The 10 yr is no longer following the Fed Funds Rate. There have been +/- 100 basis point reductions and the 10 yr is still at +/-4.2%.

LOL!!! Pay attention, the more the Fed cuts (they ONLY control the short end) the HIGHER interest rates go in the bond market.

Wake up dingbat, risk/trust is being repriced globally and the world does not trust America. You want me to loan America money? LOL, FU, pay me MORE interest!

Wish charts went back to the turn of the century to offer greater perspective by including the lead up to, and the housing crash of the late 00s.

RTGDFA

LOL! Classic.

I keep reading these GDFA’s and can find the “Wish Charts” anywhere. Have I somehow missed the Hopium graphs? 😂😂😂

Crazy. The housing bulls assured us sales would boom once 30 yr mortgages went back to a 5 handle. Wrong again bulls. Sales won’t boom until prices come down

I’ve really debated paying off multiple mortgages I have at 2.75%, but with the cash sitting earning 4%, I’m gonna wait a bit….

You’re literally backstopping the entire American Economy. Otherwise it’s all paper mache’! lol 😆

Almost a wash depending on your tax bracket.

Not really. At those low rates DK is paying off principal more than interest each month. So whoever is paying him 4% is paying down his principal for him at a fairly rapid rate. FYI, you can achieve the same result with a 15 year mortgage sub 5% although it’s slightly less effective because of only receiving the 4% return.

You could buy STRC and earn 11%. Stock is liquid.

Comments like this evince a remarkable lack of understanding. All you’re doing is looking at two different rates and you think you’re making money off the spread, but you aren’t even thinking about the fact that if you pay off the mortgages, the effective rate of interest on the remaining principal is zero, not 2.75%. That is a guaranteed 2.75% amortized rate of return on whatever you still owed, compared to the 1.25% you were making on the spread.

What are you giving away that money for, to a bank of all people, when you could have the peace of mind of not owing any more mortgage debt?

Huh?

I think you need to rethink that.

I will tell you what, if you want, you can lend me as much money as you want at 2.75%. I won’t even make it uncallable (like a regular mortgage).

Banks are making a while hell of a lot of money borrowing at much higher rates than 2.75%.

Yes but you’re not a bank lending out that borrowed money in the original example, you are using that money to love your life.

You are not creating personal wealth by consuming the loan yourself.

Your second example would be true, if you took the loan and reloaded it to someone else at a higher rate, then yes, but that’s not true for being the loan endpoint

You literally could not be more wrong.

On the old Motley Fool message boards (RIP), I am noted for my efforts during the housing crisis to get a mortgage on my already paid off house.

I was 90% of the way to the finish line, but banks were laying off loan officers left and right so my file kept bouncing from one laid off persons desk to another’s. Finally after numerous phone calls and such I was able to close on the mortgage. I was able to borrow about 50% of my home’s value at a ridiculously low rate.

I took the money, opened a investment account at Schwab where I bought a bunch of high dividend stocks (mostly pharmaceutical companies, defense stocks, with some oil and cigarette companies mixed in). I left a small chunk in cash and set my mortgage to be auto-payed from the account each month.

Initially I would have to log in every few months and sell a small portion of the stocks to replenish the cash balance so my mortgage could be paid. However after a few years, the dividends grew enough that they were enough to pay the mortgage. No more selling needed.

Meanwhile the stocks appreciated. They more than doubled in a few years since I had bought near the bottom.

I made literally hundreds of thousands of dollars simply because I had access to a low rate, uncallable loan.

Right now, if someone offered me access to money at 2.75%, I would take the money and invest it in short term treasuries while simultaneously selling puts on selected stocks. The treasury interest would more than cover the cost of the loan and the premium from the put sales (or getting the stocks at reduced prices) is just a bonus.

Having access to below market rates on money is a godsend. It is how banks survive.

A shorter version is that being able to borrow money at 2.75% and lend it to the U.S. government at 3.75% is an easy moneymaker.

I’m in a much more position of power holding a few hundred grand in cash, than paying off two notes….

Optionality is a thing, yes. And if that’s what you want, go for it. But do understand that this is a psychological comfort, not a financial argument.

I agree.

As an example, if I had a 100K balance on a 2.75% home mortgage and US government bonds were paying 4%, what would bring me the most peace of mind?

If I had a 100K windfall, what would I do with the money?

1) For safety, an investment in US bonds at 4% would be safest. It is very unlikely (end of world order?) you will lose anything.

Taxes may take 25+% of the income lowering your effective “spread”. Ie at 25% tax bracket, the new spread is 0.25% and you are still making money vs the mortgage payment. You also have the flexibility if/when bond vigilantes re-appear and if bond rates increase. By my calculations, if bond rates go above 6%, the bond interest will cover both the principal AND interest on the mortgage payments and you get to keep the 100K. This is the safest and would bring me the most “Peace of mind”. However, bond rates may drop to zero again like in 2020. The temptation to pay off the mortgage may become a valid decision.

2) You could pay off the mortgage and never have to worry about sending in a mortgage payment again(Just taxes and insurance. Insurance is even optional if you want less peace of mind.) . As an investment, this is far riskier than US bonds. During 2008-2012 period, houses lost 30-50% of their value and unlike bonds, your 100K was not producing any cashflow. Just hope you don’t have to cash in due to life events during downtimes. Also, expensive repairs not covered by insurance may require cash which you don’t have.

2) You could invest in stocks or a safer S&P 500 ETF at a historically much higher return. However, due to the higher risk of a down market, can you pay the mortgage if the market drops 50% and your 100K becomes 50K(or less). You may lose 50K AND your house like 13M people did in 2009. Personally, there isn’t much peace of mind despite the success of all of those Bitcoin multi-millionaires.

3) Vegas roulette is a final option if you feel lucky.

I’m sticking with US bonds and waiting to see if rates go above 6% and lock in a 10, 20, 30 year to pay off my house while keeping the 100K. Or, I’ll just pay off the house (or refi again) if rates plunge to zero again.

Mr. Wolf: I don’t really get the West coast graph versus the December vs December percentage data. The graphs look like they drop off a lit more than the percentages would indicate.

This maybe hard to see because it came off the jump in the prior month, and those two lines (left up, right down) may be hard to distinguish. It was a huge drop from 63.8 in Nov to 55.3% in Dec (-13.3%). But the month before, there was a jump. To see it better, you can right-click on the chart and select “open image in new tab” or similar, depending on browser. This will open a bigger version of the chart, and you’ll see.

Thanks wolf

Wolf, I enjoy your reports and find the majority helpful.. I wanted to point out that the residential and commercial real estate market in the Florida Panhandle is alive and well. Lots of construction, lots of demand for all prices and they are closing. In other words a very vibrant market here.

The Panhandle is kind of special. You have lots of undeveloped land along the Gulf (of Mexico GDI!). You have little industrial growth. The country has lots of well-off folks in a K shaped, bifurcated economy looking for a winter home. So it is a perfect place to build new homes at a much lower cost than buying from some sucker who paid way too much. Where I live along the east coast of Florida, build-able land is almost non-existent. Either because the good land is already built, or what’s left is completely owned by a big national builder, trying to minimize production to keep prices up. I bought my first house in 1993. I was able to buy an undeveloped 1/4 acre parcel for $5000, and contracted with a local builder to build a 1550 sq ft concrete block house for $66,000. It is no longer possible to purchase your own land and hire your own builder, except for the very wealthy.

Some people in high places seem to think the problem is that institutional buyers have bought up all the houses, so there aren’t any available for buyers to purchase

Large investors own about 3% of single-family homes. It’s the mom-and-pop investors that own the vast majority of single-family rentals, plenty of them here in the comments too. Mom-and-pop investors own about 11 million SFRs.

That’s why it’s comical for the king to try to address the affordability problem by banning institutional buying. Not that I am advocating for the institutional investors but like Wolf said bulk of investment properties are mom and pop, why don’t we ban them from buying or how about addressing afforability problem by actually dealing with the run away price increase or actually allow deflation of home value…nah, can’t have that, that might be one thing that will actually motivate the asset class to go to the streets and protest like the yellow vest in France or french revolution. Dismantling our system, yeah that they can willfully ignore as long as it doesn’t affect them personally, come after their wealth effect and piggy bank…pitchforks are coming out..

The higher up solution is almost, if not worse than the problem…ban 3% investors, 50 yrs mortgage, portable mortgage…etc….dog and pony show at best, at worst, another look over tactic meant to resolve nothing while the divide grow ever larger.

In a way it’s good: one less bogeyman for the masses to complain about. As Wolf says they’re only 3% of the market, but most people think it’s way more.

The 50-year mortgage though are not a solution, for the same reasons that 7-year car loans and even student loans are not solutions to the affordability of their respective markets. Why can’t we subsidize homebuilders to make smaller, non-luxury starter homes again? I’d also like more wagon/hatchback options as opposed to the more expensive and oversized crossover/SUVs/trucks.

The POTUS will absolutely NOT do anything to harm Property owners and sellers. If he could lower mortgage rates to one percent or less he would do it. No matter what this POTUS says this administration will not enact anything at all that will harm property owners and sellers.

They already did in multiple ways, including: Trump’s executive order this week attempts to block large institutional investors from buying single-family rentals, thereby removing deep-pocket demand from the market.

Wolf, I have a question that I have not been able to figure out and wondered if you with your vast sources of information has the answer.

When looking at corporate investors, how do they differentiate houses that are bought by corporations for rental and houses that are bought by corporations that are owned by the person living in the house?

I know a couple of people who use corporations to purchase their house (for tax and anonymity reasons) but they own those corporations. They even charge themselves rent, but they are literally paying themselves.

Obviously these situations are not adding to the really minor problem of corporations driving up the cost of hime ownership.

It’s not counted that way. The large institutional landlords have investors and stockholders and have to disclose, and are eager to disclose, how many single-family rentals they own. I’ve covered the largest 6 of them that together own 422,000 SFRs by looking at their financial filings. So check out this article (it also has a list of the largest multifamily landlords):

https://wolfstreet.com/2025/09/15/the-biggest-single-family-rental-landlords-and-multifamily-landlords-in-the-us-big-shifts-underway/.

I think the point is that at least in my area of the South, institutional/corporate investors own a large percentage of the houses that would be purchased by First Time Homebuyers. That is the lower end of the value range. Most of these were putchased between 2009-2015. They also purchased many 2-4 Family Properties. However, within the last 12 months, the three largest institutional investors have sold almost all of the 2-4 family and maybe 10% of the single family properties in the lower end of the value range. Many of these have been purchased as rental investment properties by the “Mom and Pop” investors or larger local SFR rental investors.

What the current Adminstion is doing is forcing “Institutional” investors to do Build to Rent Properties. We have some of these building/buying in new subdivisions, 1800-2500 sf, and there enough inventory in our area that it does not push out the first time buyer in this new home price range.

It feels like a standoff. People list at ridiculous prices they at one time saw on Zillow and then when no one wants to pay those prices they pull the houses. With the supply significantly outstripping demand if there’s ever a panic or even the realization prices are trending moderately down for the foreseeable future then I think there will be a race to the exit. For now though people keep listening to the realtors hype, rates are going to drop and prices will sky rocket.

I met a developer for large company and a land speculator while traveling last year and both separately told me that they’re forecasting zero price appreciation for CO for the next 5 years. The problem is the realtors have not gotten the memo and thus a lot of the population who blindly listens to them have not gotten the memo

Also would help if the main stream media would get increasingly negative on housing. Basically something needs to change the collective mindset

Oh so the numbers aren’t amazing with maths?

Hahaha

Have you ever known a good salesman to ever be negative about what they are selling. Realtors are salesman, not real estate financial advisors.

As for zero price appreciation…it’ll be interesting. But CO is overbuilt and expensive. High prices cure high prices. And I think our host has a saying about straight lines

Right but people seem to think of realtors as real estate experts to get advice from, not sales people.

And yes CO is overbuilt, the mass COVID influx is slowly leaving, and tourism is slowing especially with our terrible snow this year.

And forecasts are just forecasts, but the actual real estate professionals thoughts were based on demographics, migration patterns, income levels, other investment in the area. They also said they were forecasting significant declines in certain parts of the state, moderate declines in others and flat in some areas. When they said no price appreciation for the next 5 years they didn’t mean a straight line. They meant there’s no money to be made in CO in a 5 years horizon.

It’s not a zero appreciation market, it’s straight up declining and has been since the summer of 23. My elementary school teacher daughter was looking at an entry-level purchase 2 years ago, now she is renting by choice, demanding and receiving rent concessions from the landlord, saving and watching prices move down a couple percent per year. For her sake I hope this continues for at least 5 years.

A bad winter plus what’s going to be a really bad fire season should also leave a lot of Airbnbs struggling

It perspective and whether you view housing as a place to live/save or an investment vehicle. A mix is probably best. I think the later has been the dominant force in the last decade.

My personal belief is that the seemingly shift to view housing as an investment has resulted in large value swings that your average citizen cannot accommodate. I don’t think that is beneficial to a society where one needs to participate in that volatility just to have a roof over their head

Isn’t there an inverse relationship between mortgage interest rates and home prices? Add in the effects of withdrawing the Covid stimulus helicopter money and the increased property taxes associated with inflated home prices and isn’t the resultant slowdown in home sales inevitable?

Structural imbalances that years to create won’t disappear anytime soon, will they?

yes, every single one of my housing articles has been saying that for over three years, including this one:

“At fault are the ultra-low mortgage rates of 2020-2022 that ended up destroying the housing market in two ways: By causing prices to explode in a two-year time span, and by “locking in” homeowners with ultra-low mortgage rates who now cannot afford to move, which has destroyed the dynamics that come with a functioning housing market, such as mobility, where people are able to move.”

Perhaps the American dream is changing and nobody notified all the real estate maggots.

Many younger adults do not want kids or all the crap that comes with owning a home. It may be more than just what someone can afford.

A close friend sold and now rents a very nice smaller place. They love it and the freedom they now have.

I am thinking they may be right. If I sell, I would have more in the bank than rent money for the rest of my life.

I am also certain most children would rather have cash than their parents old home when that time comes.

Just maybe the American Dream has changed.

If the American Dream is changing to exclude homeownership, sound to me like an argument for those that can afford it to buy more rentals. People have to live somewhere.

Trump said he doesn’t want more supply on the market because then the price of existing homes would go down and that would be bad for existing homeowners. Of course, Trump says a lot of things …. I’ll stop there.

As always, his solution requires you to be gold medalist in mental gymnistic to comprehend, us normies just can’t grasp the brilliance behind that big beautiful brain.

It’s really something to watch the Supreme Court, which created this monster and which let him fire every other federal agency head without cause, now tie themselves in knots trying to rationalize why he can’t fire everyone on the Fed board so he can lower interest rates.

He thinks zero interest rates will fix the housing market? LET HIM DO IT, Roberts! What’s different about the Fed? He’s the Unitary Executive, after all! Let him go full Erdogan and see how that works out! What are you a chicken, Roberts?

…Anyway I’ll stop here as well. I’m going to go to bed and hope we’re not storming the beaches of Greenland when I wake up in the morning.

The Fed is a totally non Constitutional construct. The entire administrative state is also not in keeping with our founding document. SCOTUS is wisely starting to tear down the edifice of this unconstitutional mess.

But yes, they will twist themselves in knots to keep an independent Fed, the founders never conceived of fiat money, never considered that we would need a non elected entity to keep the executive branch from debasing the currency, because they assumed sound money based on the gold standard.

I would take that construct over fiat currency and the Fed all day long.

I agree that a Fed beholden to the president is bad, but I’m not sure that a Fed beholden to Wall Street is any better.

Oh, look, they chickened out on the tariffs case, too. SCOTUS on recess and no ruling until February. Come on, Roberts! Aren’t you as eager as we are to see what the bond market is going to think of about another four trillion in unfunded tax cuts, political firings at the statistical agencies, a sudden return to ZIRP, and now a giant bill for like $200 billion in tariff refunds?

People buy housing payment and not the house. Prices have to go down.

There’s actually a third lever to housing affordability here: housing price, mortgage rates, and personal income. While slow, income growth is outpacing inflation the last few years.

I think slow income growth and slight price readjustment is more likely and better than an outright crash in housing prices.

We have a HUGE inventory of houses that were built with CHEAP LABOR in the 70s, 80s, 90s, and 20s. Construction workers (a.k.a. immigrants) who were naive/cut off to compensation data and negotiation skills. In essence, they were taken advantage of pure and simple (they had no leverage and were simply glad to have a job). As a result, the equity in these properties went through the roof over the following decades.

Then, social media came along and allowed people who have been a faceless commodity to gain knowledge – and the dynamics change. Those same immigrants (and their successors) became more educated and savvier to their value. Fast forward, labor as well as materials and land “go through the roof” compared to those houses from the 70s, 80s, 90s, and 20s.

Now there is this collision/mash up of “vintage” properties with lots of paper equity (either paid off or very low interest rates) competing with “current” properties with little to no equity. It’s a hot mess…real estate agents try to “compare” houses to price per square foot but it’s analogous to pricing different cars by the pound.

Do you think kids that have been brought up playing video games 24/7 in air conditioned houses want to tight rope walk across a two-story wall plate in Texas’ blistering heat while carrying a bunch of 2 X 4s on their shoulder – good luck with that. And if they don’t, their moms’ will scream on the evening news that Johnny isn’t getting the compensation and benefits he deserves.

What’s the point of my rant…we’re not going back. Single family residences will never be cheap again – never. And any realized equity will be much more modest – not a golden parachute. Those house prices from the 70s, 80s, 90s, and 20s is a fever dream. Over time those older homes will get sucked into an inter-dimensional portal like the house in Poltergeist and vanish. But it’s going to take time.

A hell of long winded way to say this bubble is different and this time is different…

Why would I be walking a wall plate with 2×4’s,weird scenerio.

I feel would have me second floor joists up and plywooded.

I would have before wall went up already marked me plates for layout,including later added top plates tying walls together.

Couldn’t this just be viewed as smoothing out that apparent jump in November?

Humpty Dumpty (the housing market) is just fine.

He’s sitting on the wall, laughing and happy as a lark. Drinking (bourbon), celebrating, talking, living like there’s no tomorrow. And what are drunks famous for – not caring or thinking about consequences. When Humpty falls off and breaks his neck, it’s all over! No one will be able

to put Humpty Dumpty (the housing market) back together again – not lower interest rates, not tax refund checks, not homeowner down-payment assistance – NOTHING and NOBODY. Nobody will be able to put time back into a bottle or turn back the clock. ⏰ 🏡

I follow markets like a hawk. This is going to end badly. Tragically, there is NO Humpty Dumpty – there are MILLIONS (homeowners) of them.

Nice new home designed for wealthy singles or empty nesters @1.8 million and it’s exactly 10 ft from the Waffle House parking lot.

That’s America, that’s the housing market, that’s what the Fed and the banks and the private systems have brought us in every market.

Elsewhere in the town is a 25 year old with a very good grad degree living at home, who may never be married.

Hope it all works out don’t we? Who wants some long term bonds?

The usual reasons that sales fall through or that buyer or the property doesn’t qualify for the mortgage. Normally 90 to 95% of contracts close. The data for closings lags the pendings by a month. So if you convert the pending sales index to a baseline year and derive the actual number of sales and compare that with the subsequent months closings data, That ratio plotted over time is a good leading indicator for problems for the financial system as a whole.

The low level of sales is symptomatic of the problems that Wolf indicated.

The inability to find homeowners insurance in some markets is another issue that has exploded in the last 5 years.

Sales volume is so low that in effect we don’t have a real market price. We will find out what that clearing level is only when owners are forced to sell. Meanwhile the market limps along in la la land with inflated prices being reported but not actually attainable at normal market clearing levels of volume

i know a woman in FL who realizes this is a HUGE housing

bubble about to crash. she lowered her price, dumped the

house, and bought silver bullion at $95. housing will crash

much worse than 2008, and silver will go to the moon. the

stock markets will crash with housing. the Shiller P/E ratio

is 40 and should be 12. the Buffett Indicator is a neverbefore-

seen 225 and should be 80. 99% of the population is deaf,

dumb, and blind. the Much Greater Depression is near.

It would seem that housing and the stock market have nowhere to go but down, as you say, though crazy can always stay crazy for longer. But suppose those markets really crash. Why would silver go through the roof?All the sudden all this paper wealth that people thought they had vanishes, and instead of folks using what they have left just to get by, they are like “Imma buy me some silver, and name your price! I’ll pay any price!”

Silver and gold will go down with stocks and real estate. Who’s going to buy your overpriced PMs when everyone’s broke?

It’s a fool that looks for logic in the chambers of the human heart. But perhaps the valves that control those chambers will soon be regulated by micro-chips,and that might require the use of more silver. Regardless, whether prices head far away up or down from a $95 buy-in, you’d probably experience a self induced heart attack that no stock of electro-circuitry could prevent. If you were going to jump ship it would have been better to have stashed while prices were cheap so you could have a good laugh no matter what way this all goes. That’s Entertainment, and better than anything the Hollywood crowd can come up with now.

PMs: early to soar, late to crash.

Yet, the mania is followed… by a crash.

Silver is probably “worth” $100/oz… to someone in some time. A flatscreen allegedly has an ounce or so in it. The number of flatscreens in the landfill is growing daily.

Once gold tags $5k, I don’t see a ton more upside for this rally. Same: probably “worth” $10k, somewhere/ somewhen.

I think we’ll see $2600/oz gold before $10,000/oz tho.

Ha. Is the knowledge of a women in FL doing something supposed to give credence that something?

Well Florida man is a joke of a human being, but Florida woman is modern day profit…

“It’s only one month! December isn’t prime home buying season! It’s been really cold in the Midwest!”

The PHSI has been 20-30% below 2019 levels for the full year…

I just looked at a US housing inventory graph dating back to 2000. Today, there is less inventory than at any time previous to Dec 2020, and by a lot. As long as we have persistent inflation coupled with historically low inventory, from a national level, there will not be a price crash.

But, on a local level, some markets are in serious trouble. Some markets in FL, TX and many other markets in the south are going to crash.

Active listings in December were up by 22% to 95% from the prior four years and down 15% to 25% from 2017-2019. See stacked chart below. But pending sales in December have plunged by 31% from 2019 and by 35% from 2017, and so months’ supply has spiked. Inventory in a vacuum doesn’t matter. What matters is the relationship between inventory and sales. Sales have been down by about 30% to 40% from the pre-covid years for three years in a row. And months’ supply based on closed sales has been high, and will jump when these low pending sales become low closed sales over the next two months.

Thanks WR for this reply.

We all have biases and hence we think like that.

People invested in real estate in So Cal ( like me ) would think that come what may, all places can crash but So Cal because things are different and we are so special. Then we think about arguments why it can’t happen in our place.

But it takes courage and open mind to see the facts as they are.

I hope she has in hand metals(woman who sold home).

PM’s drop dramatically would buy more(in hand),but,tis something excepting emergencies leaving to others on the time of my unfortunate/untimely death.

I realize demand for goods requiring silver or gold will drop sales wiise at that point but in it for the long haul.

“Price elasticity of demand (PED) measures how the quantity demanded of a good responds to changes in its price, indicating whether demand is elastic or inelastic.”

Is the price of housing inelastic?

Kona Coast past 6 months

Homes over $8m steadily selling

9 closed, avg $14.3m, highest $26m, avg 94% sold price to list price and 63 days on market

6 in escrow avg $15.2m, highest $25m

25 active avg $14.4, highest $26m

Apparently the centillionaires and billionaires think buying a home now is just fine.

A billionaire paying $26m for a house is like someone making $100,000 paying $2,600 for a house.

Do we know the fraction of 5/1 7/1ARM loan and how it affect the ease of lock in effect? It seems 2027 will be the peak of the year 2020-2022 ultra low ARM unlock

The share of ARM loans is MINUSCULE.

https://wolfstreet.com/2026/01/03/locked-in-homeowners-nevertheless-pay-off-below-4-mortgages-their-share-of-all-mortgages-drops-to-lowest-since-q4-2020/