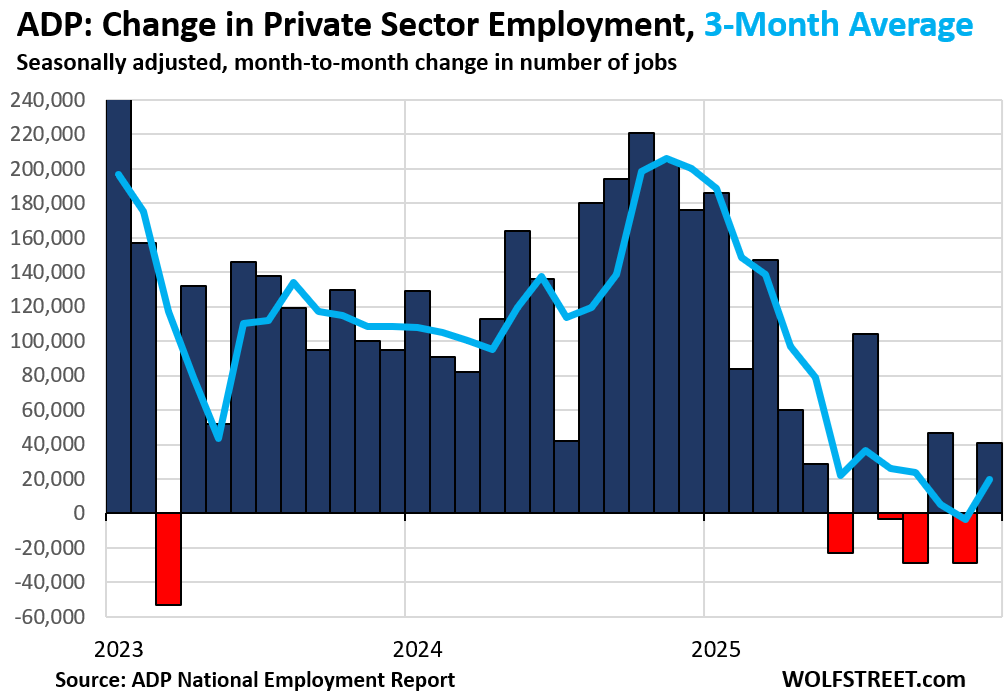

Private-sector job growth slowed to a crawl in the second half.

By Wolf Richter for WOLF STREET.

Private-sector employers added 41,000 jobs to their payrolls in December, after the drop in November. Of that increase in payrolls, 34,000 occurred at employers with 50-499 employees. Small employers added 9,000 jobs, large employers added 2,000 jobs, according to the ADP National Employment Report today, based on data from companies whose payroll it processes.

The three-month average payroll increase (blue line in the chart), which had turned negative in November for the first time since August 2020, rose to about 20,000.

The declines in August and September were a result of the annual adjustment for the 12-month period through March 2025, applied to August and September, which turned those two months negative, from low-level growth before the adjustments were applied.

The decline in November may have been influenced by the uncertainties for companies around the government shutdown, to where some companies put hiring on hold until the dust settled down. With job creation lethargic, it doesn’t take much to turn low growth into a decline.

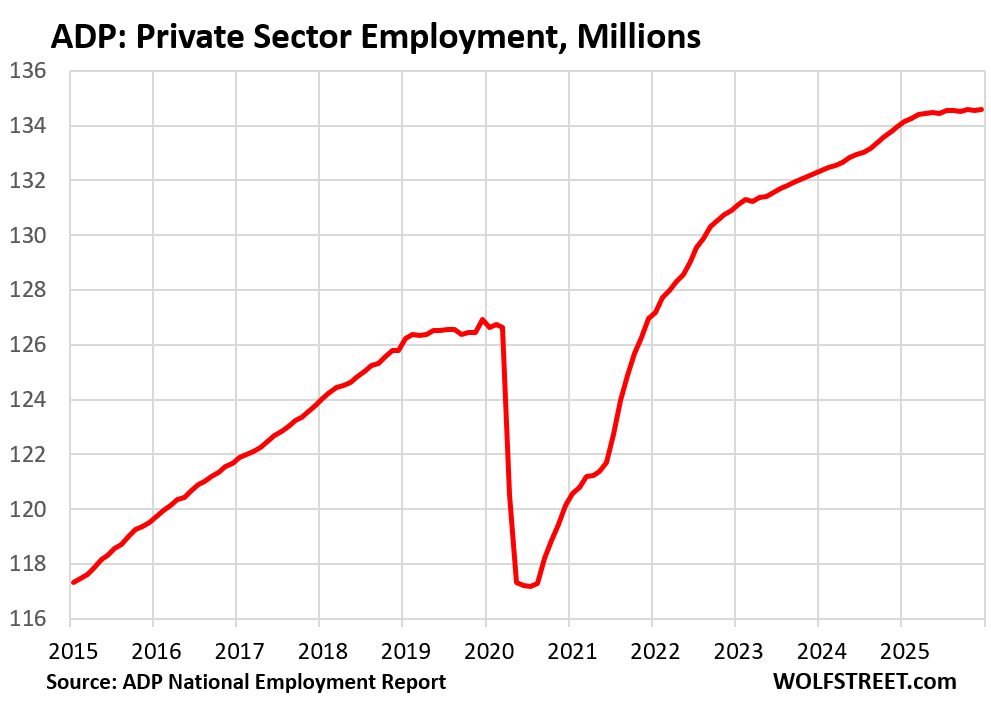

For the whole year 2025, private-sector payrolls rose by 614,000, the smallest annual gain since the job losses in 2020.

With the gains in December, payrolls rose to a record 134.59 million. The chart shows the trend: Private-sector job growth continued in 2025, but that growth was much slower than in prior years and slowed to a crawl in the second half.

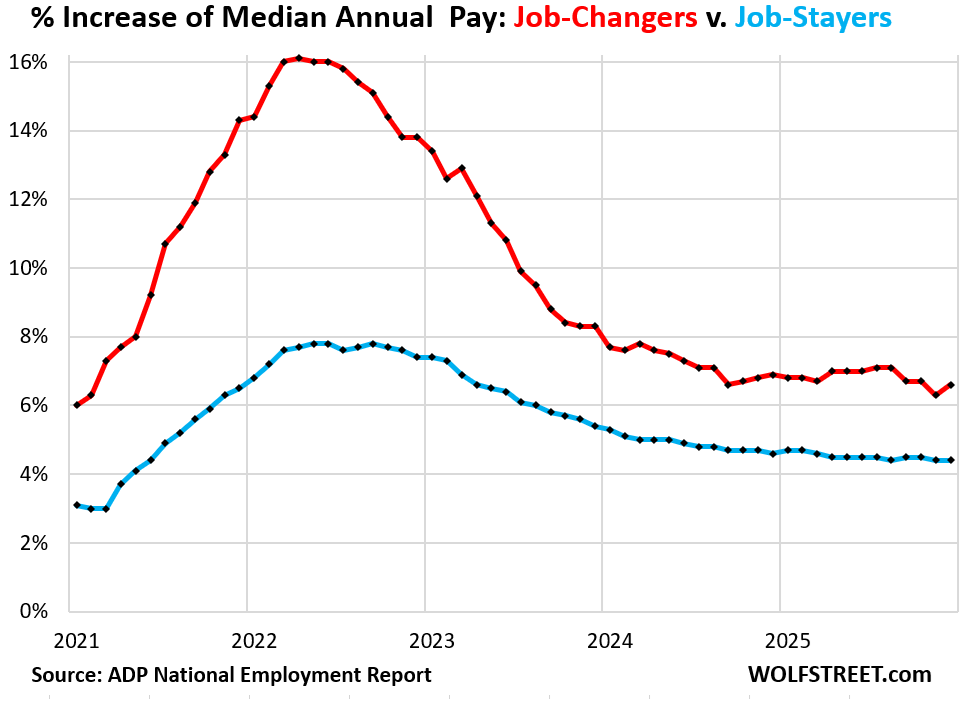

Median wages increased year-over-year for:

- “Job Stayers”: +4.4%.

- “Job Changers”: +6.6%.

The wage data from ADP is based on a subset of 14.8 million workers employed for at least 12 months, whose paychecks ADP processed, and includes salary and hourly wages, overtime, tips, bonuses, and commissions.

Of that sample, over 13.8 million are job stayers, 39% of whom are salaried employees and 61% are hourly employees. And over 1 million are job changers.

ADP’s data only goes back to late 2020, so comparisons to periods before the pandemic are not possible.

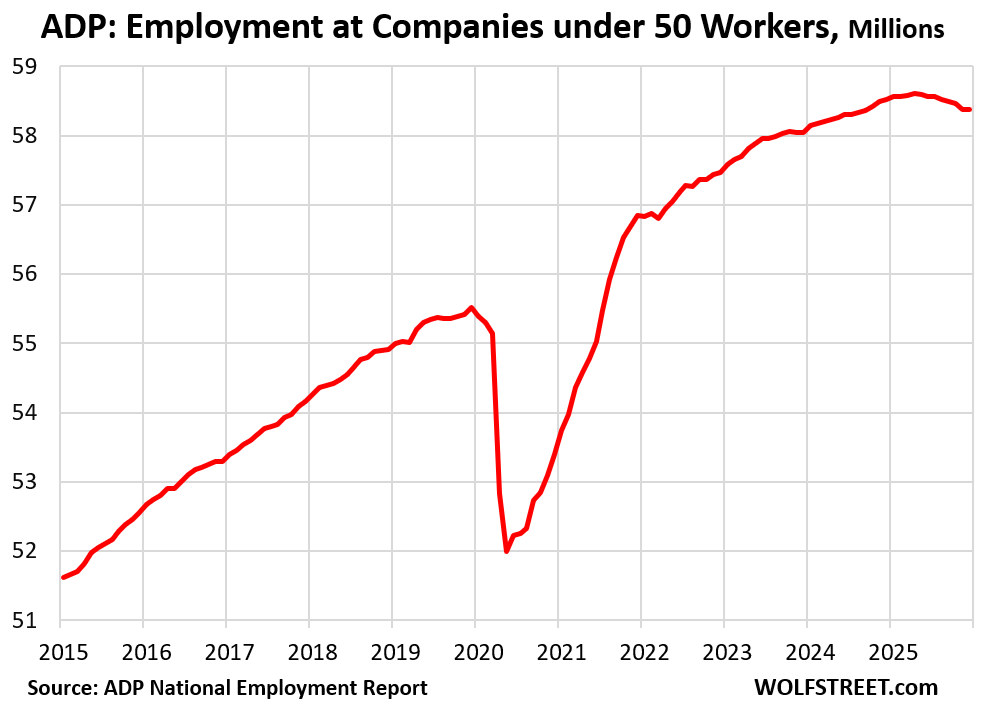

Small companies with fewer than 50 workers added 9,000 workers in December, the first increase since July, bringing the total to 58.38 million workers.

From May through November, payrolls at these small companies had declined by 240,000. The next few months will show if the gain in December was actually a change of direction of that downtrend.

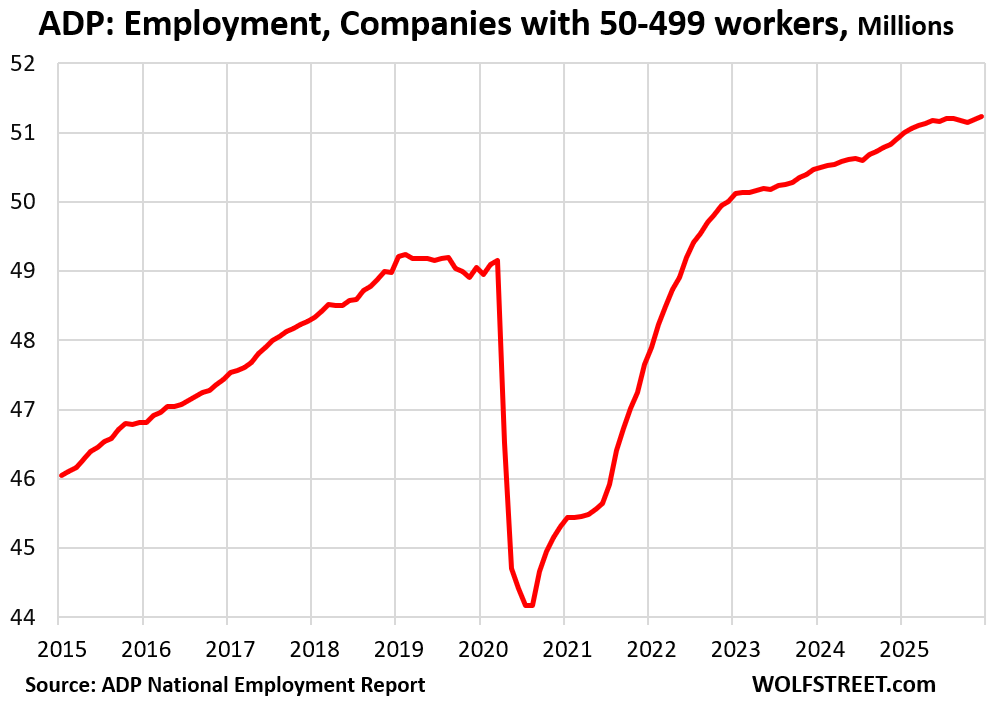

Medium-size companies with 50-499 workers added 34,000 jobs to their payrolls in December, the second increase in a row (November +45,000), after three months of declines, bringing the total to a record 51.23 million employees.

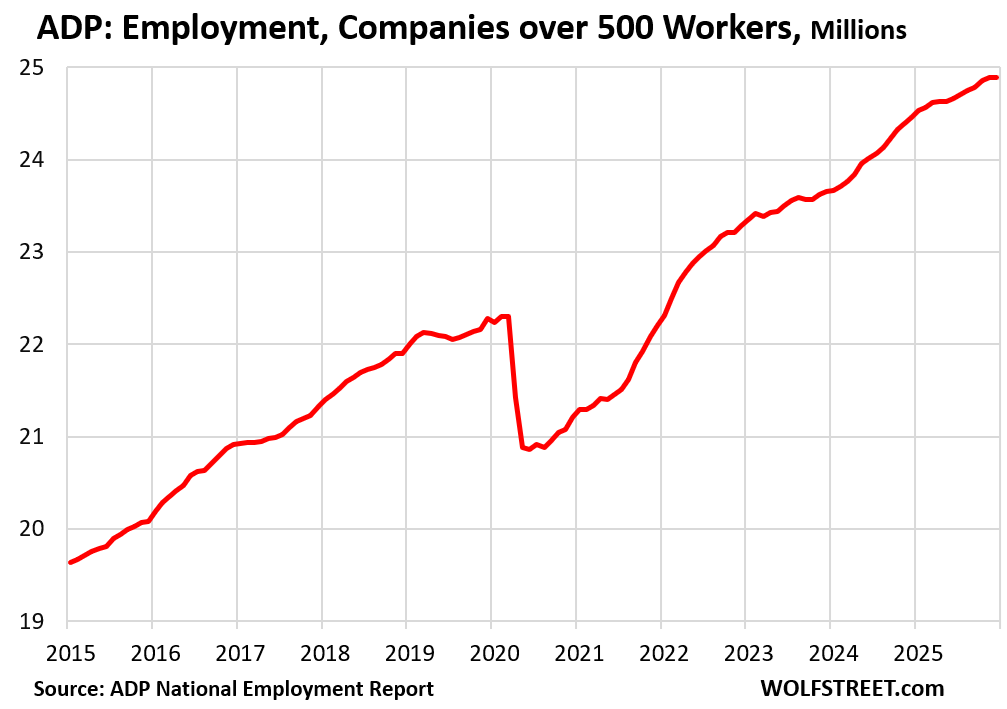

Larger companies with 500 and more employees added only 2,000 jobs in December, after the job gains in the prior six months (+264,000). Their payrolls rose to a record 24.89 million.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thanks for the article.

Since it’s pretty hard to tell what kind of jobs have been added, it would be interesting to see the breakout of hourly versus salary employees in some of these charts (assuming that’s possible).

Also, since many of the December jobs would be seasonal, looking at salaried employees might help filter that out a bit…

Thanks again

Here is ADP employment by industry, each industry with its own long-term chart of employment:

https://wolfstreet.com/2025/12/03/private-sector-job-trends-by-major-industry-from-job-destruction-in-information-to-job-creation-in-mining-natural-resources/

Wolf, since ADP does not do payroll for all the companies, do they extrapolate their data. Or do they conduct surveys? How do they come up for the entire private sector

ADP’s employment report is based on data from the payrolls it processes, and it extrapolates then to all companies. ADP also does an annual benchmark adjustment (Aug & Sep) when it brings its data in line with the payroll tax data from the BLS’s Quarterly Census of Employment and Wages (QECW) released by the BLS in early September 9. The QCEW provides a quarterly count of Paid Employment based on the quarterly payroll tax filings by employers, covering about 95% of payroll jobs, but the BLS releases it annually with a long lag. And ADP benchmarks its figure to that in September, spreading the adjustment over Aug and Sep (which is why they dropped).

I just have a few comments regarding the video which I enjoy watching–

I don’t expect any big market moving news Friday with respect to the tariffs, the implied volatility of the SPY and QQQ options is about normal, it’s not indicating anything unusual. It’s not even elevated considering it’s a “Jobs Report Friday.” Anything can happen of course, but the IV and the options premiums are not showing it right now.

As far as silver, it remains extremely overextended, in addition to being 40% above its 50 day average, it has not closed below the 50 day since May, which would be 8 months running; I looked at the chart of the silver ETF (SLV) going back 20 years, and it has never stayed above the 50 day for this many months. Sooner or later it will have to fall to at least the 50 day again, so whenever the “metals mayhem” stops, I would expect to see a big move down.

The past is not precedent, especially considering the blatant manipulation being admitted in the commodities “market”.

There are 8+ billion people demanding and competing for a decent standard of living. Something that requires a tremendous amount of commodities and energy (which also requires commodities), so you’ll excuse me if I take the other side of that trade. I’d argue that there is evidence to suggest we haven’t had true price discovery for 20+ years, so it’s no surprise the “50 day moving average” is a garbage indicator. Add to that the loss of trust(FAITH) and repricing of risk that is occurring globally. Regardless, it never hurts to hedge your “bets”, because this sure as hell isn’t “investing” and it hasn’t been for quite some time now.

There is usually a downswing in Feb through mid-March.

Why do the components not add up to total?

41k – total

2k – large

34k – medium

9k – small

43k – sum of parts

My initial thought was large companies perhaps cut 2k instead of added, which would then make the parts line up with the total.

The sum of your parts calculation would actually be 45K. But I’m not answering for Wolf on the bigger question. I’d just guess 4 thousand were discounted because it was found they were all huddling in groups in a corner area staring at their dern smartphones and getting nothing done.

Rounding. ADP rounds each figure to the nearest thousand (such as jobs at companies with more than 500 workers: 24,894,000). There are five categories which I added into three groups. So five rounding errors added together.

Wow 2025 was TERRIBLE!

no wonder everyone on Reddit was complaining about the job market. It sucked

Please take this comment with the approximation of thought it was contrived from.

AI is playing a role in adding jobs and reducing jobs. In the former, the construction of the data centers comes to mind. In the labor market, many entry-level jobs were augmented by AI, and thus, a company that intended to hire 3 people went with 1 hire.

If this thesis holds water, I suspect you will see difficulties in some areas for people seeking new employment.

Could immigration or lack thereof also influence this?

Agree with you. Here in my part of central Texas rents are dropping. Traffic on the roads less congested. There are visible changes in restaurant staff – brace yourself- where I see white workers rather than the previous all Hispanic crew. Any increase in total employment surprises me. I’m shocked employment is rising.

MW: Help wanted? Not really. U.S. economy is barely adding workers.

Interest rates could be on hold ‘for some time,’ Fed minutes show

We could get a surprise 4.4 % unemployment rate tomorrow, labor participation rate could drop hence the 4.4% rate. The whack mole game of preventing risk from rolling over must be getting exhausting for the master trading algorithm..

“Markets” and small businesses in particular want certainty and stability. Given that the current CONgress and administration refuses to act responsibly, I don’t see these numbers improving anytime soon. In addition, it is crystal clear that our owners want war. Hedge accordingly.

Certainly nothing in these numbers that would justify rate cuts, or 1.5 trillion in war spending…

I wonder what role demographics is playing into the report? With an exodus of immigrants (voluntary or involuntary), and a generally shrinking population due to birth rate, the increases couldn’t be perpetual.

S does not equal I. There are leakages, funds dissipated in financial investment instead of real investment and funds impounded in the banks.

FINANCIAL speculation, stoking asset bubbles, provides a relatively insignificant demand for labor and materials and in some instances the over-all effects may actually be retarding to the economy.

Compared to REAL investment, FINANCIAL investment is rather inconsequential as a contributor to employment and production. Only debt growing out of REAL investment or consumption makes an actual direct demand for labor and materials.

Thanks wolf