Of the largest 20 IPOs, 14 trade below their IPO price; only 6 trade above it. Many plunged from their post-IPO pop.

By Wolf Richter for WOLF STREET.

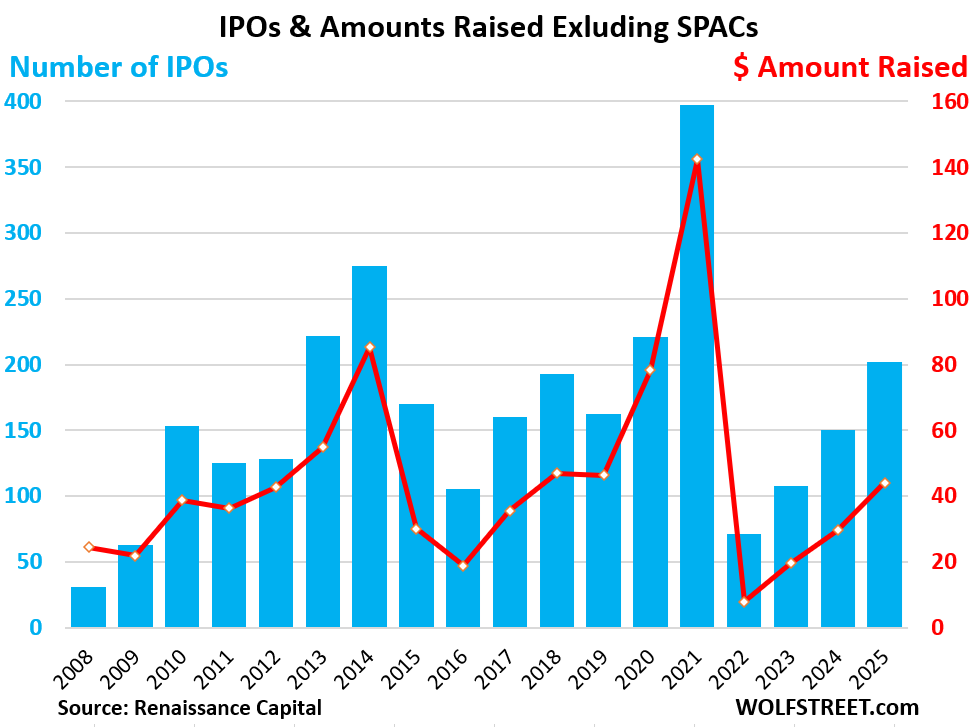

There were 202 IPOs in 2025 – not including the 144 SPACs that went public – the most since the IPO boom in 2021 (blue columns, left scale in the chart). But a big part of that volume was driven by foreign micro-IPOs of minuscule outfits. So the total amount raised by the 202 companies was $44 billion (red line, right scale), driven by a few big immensely hyped IPOs: The largest 20 IPOs (by amounts raised) accounted for $25 billion of the $44 billion raised. The top nine raised each over $1 billion, and $16.5 billion combined.

The drama that occurred were the first-day “pops” followed by long plunges from the intraday highs. By Friday, December 26, the stocks of nearly all of the largest 20 IPOs had plunged from their intraday highs, with 11 of the 20 plunging by over 40%; and four – we’ll include Figma here though it barely missed being in the largest 20 – plunging by 73% or more. This includes crypto and AI heroes.

And of these largest 20 IPOs, the stocks of 14 had dropped below their IPO prices by Friday. The IPO price is the price at which the company sold shares to institutional investors the day before the stock starts trading publicly.

The largest 20 IPOs by amounts raised, plus Figma.

The list below shows the largest 20 IPOs by amount raised in 2025. The largest of the 20 was Medline, which raised $6.27 billion in the IPO. The smallest of the top 20 was Fermi, which raised $683 million during the IPO.

I added Figma to the list, though it didn’t make the cut-off (it raised $412 million) because it was a hugely hyped IPO with a mega-spike during the first two days and then a hard plunge.

The right column shows the percentage decline from the intraday high.

The second column from the right shows the percentage change from the IPO price – the price at which the company sold the IPO shares to institutional investors the day before the stock started trading publicly.

The negative percentage changes are marked in bold.

| The 20 Largest IPOs in 2025 | |||||||

| IPO Price | Intraday high | Dec 26 close | % from IPO price | % from high | |||

| 1 | Medline | MDLN | 29.00 | 45.50 | 44.13 | 45% | |

| 2 | Venture Global | VG | 25.00 | 25.50 | 6.95 | -72% | -73% |

| 3 | CoreWeave | CRWV | 40.00 | 187.00 | 76.42 | 91% | -59% |

| 4 | SailPoint | SAIL | 23.00 | 26.35 | 21.15 | -8% | -20% |

| 5 | Klarna Group | KLAR | 40.00 | 47.48 | 29.59 | -26% | -38% |

| 6 | Bullish | BLSH | 37.00 | 118.00 | 41.14 | 11% | -65% |

| 7 | Circle Internet Group | CRCL | 31.00 | 298.99 | 81.27 | 162% | -73% |

| 8 | NIQ Global Intelligence | NIQ | 21.00 | 20.39 | 16.38 | -22% | -20% |

| 9 | BETA Technologies | BETA | 34.00 | 39.50 | 29.84 | -12% | -24% |

| 10 | Navan | NAVN | 25.00 | 25.00 | 15.53 | -38% | -32% |

| 11 | Netskope | NTSK | 19.00 | 27.99 | 18.29 | -4% | -35% |

| 12 | Firefly Aerospace | FLY | 45.00 | 73.80 | 23.34 | -48% | -68% |

| 13 | Chime Financial | CHYM | 27.00 | 44.94 | 26.49 | -2% | -41% |

| 14 | Alliance Laundry | ALH | 22.00 | 27.48 | 21.35 | -3% | -22% |

| 15 | SmartStop Self Storage | SMA | 30.00 | 39.77 | 31.52 | 5% | -21% |

| 16 | StubHub Holdings | STUB | 23.50 | 27.89 | 13.28 | -43% | -52% |

| 17 | Figure Technology | FIGR | 25.00 | 49.49 | 44.05 | 76% | -11% |

| 18 | Legence Corp. | LGN | 28.00 | 50.20 | 44.60 | 59% | -11% |

| 19 | Accelerant Holdings | ARX | 21.00 | 31.18 | 16.51 | -21% | -47% |

| 20 | Fermi | FRMI | 21.00 | 36.99 | 8.88 | -58% | -76% |

| Figma | FIG | 33.00 | 142.92 | 38.54 | 17% | -73% | |

Some of the standouts among the largest IPOs in 2025.

#1 Medline [MDLN], the healthcare supplies giant, was one of the exceptions that is trading near its high.

But the stock has been trading for only seven days, as of Friday, during the quiet pre-holiday period.

It raised $6.3 billion in its IPO on December 16, the largest IPO since 2021, at an IPO price of $29 a share. It popped by 40% on the first day of trading on December 17 to $41, giving it a market capitalization of about $55 billion. On Friday, it closed at $44.13.

This IPO opened the exit door for the PE firms Blackstone, Carlyle, and Hellman & Friedman, that had bought 79% of the company in 2021 from the founding Mills family in a leveraged buyout, at a deal value of about $34 billion. It then went on an international shopping spree. The LBO and the debt-funded shopping spree left the company with nearly $17 billion in debt. During the IPO, the company raised $6.3 billion, which will help reduce that pile of debt.

#2 Venture Global [VG] went public in January 2025 at an IPO price of $25 a share, raising about $1.75 billion, and giving the company briefly a market cap of about $60 billion.

That IPO price, which had already been lowered in the days before the IPO, was about the high for the stock, which topped out at $25.50. On Friday, it closed at $6.95, down by 72% from its IPO price and down by 73% from its intraday high:

Venture Global liquefies US natural gas and exports the LNG from its four export terminals to customers around the world (data via YCharts).

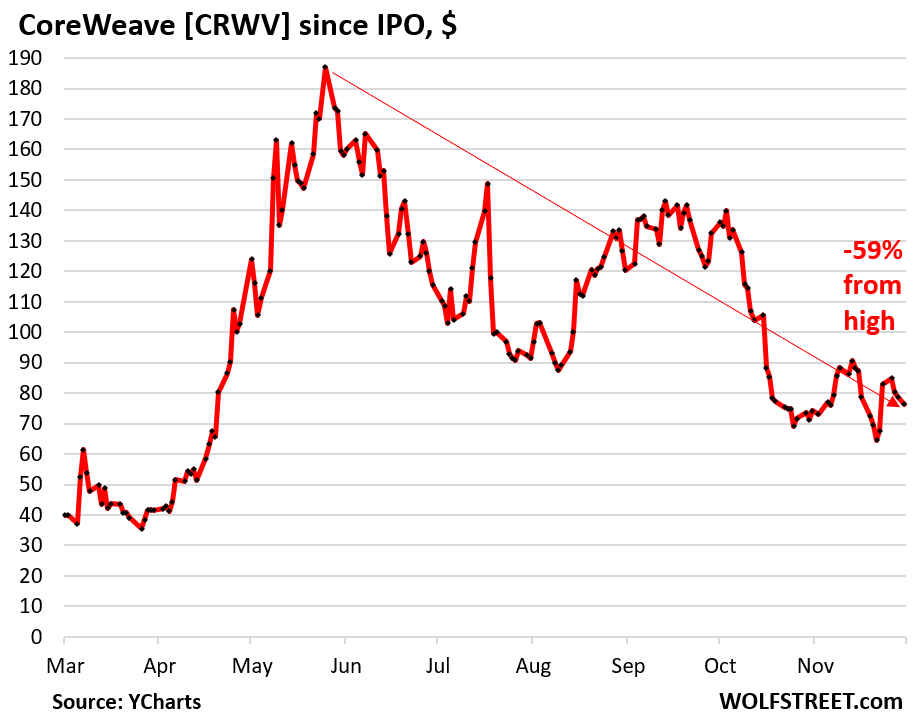

#3 CoreWeave [CRWV], one of the AI infrastructure companies, went public in March and raised $1.5 billion at an IPO price of $40 a share. Among the institutional investors that bought shares at the IPO price was Nvidia ($250 million).

Shares started exploding in late April to peak at $187 on June 20 amid AI-mania, and have since then plunged by 59%. But they’re still up by 91% from the IPO price.

CoreWeave leases data centers from landlords, equips them with AI-servers powered by Nvidia chips, and then rents out the computing power. It funds the purchases of the servers with large amounts of expensive junk-rated debt, with the servers as collateral.

#5 Klarna Group [KLAR], a Swedish provider of Buy-Now-Pay-Later and other payments services to the ecommerce industry, went public in September at an IPO price of $40 a share and raised $1.37 billion.

The stock, at $29.59 on Friday, has plunged by 26% from the IPO price and by 38% from the intraday high:

#6 Bullish [BLSH], a cryptocurrency exchange and blockchain technology company headquartered in the Cayman Islands, went public in August at an IPO price of $37 a share and raised $1.11 billion.

The shares exploded to a high of $118.00 during the first-day pop, giving the company a market cap for a few seconds of $18 billion, then plunged. On Friday, they closed at $41.14, down by 65% from the intraday high, but still up by 11% from the IPO price.

#7 Circle Internet Group, a platform for stablecoin and blockchain applications, went public in June at an IPO price of $31 a share, raising $1.05 billion. Then came a phenomenal 867% multiday spike to the intraday high of $298.99 a share, followed by a 73% plunge from that high that left the stock still 162% up from the IPO price.

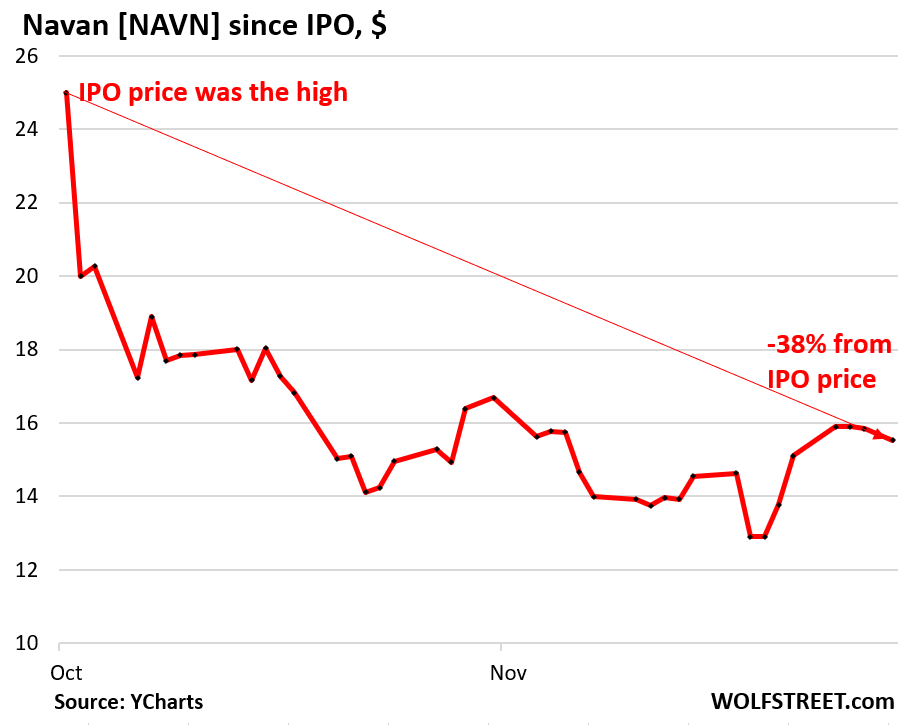

#10 Navan, Inc., a corporate travel and expense management platform, went public in October at the IPO price of $25 a share, but on the first day of trading, shares dropped right out of the gate and never traded at the IPO price. The intraday high was $22.75 on the first day.

On Friday, shares closed at $15.53, down by 38% from the IPO price and down by 32% from the intraday high.

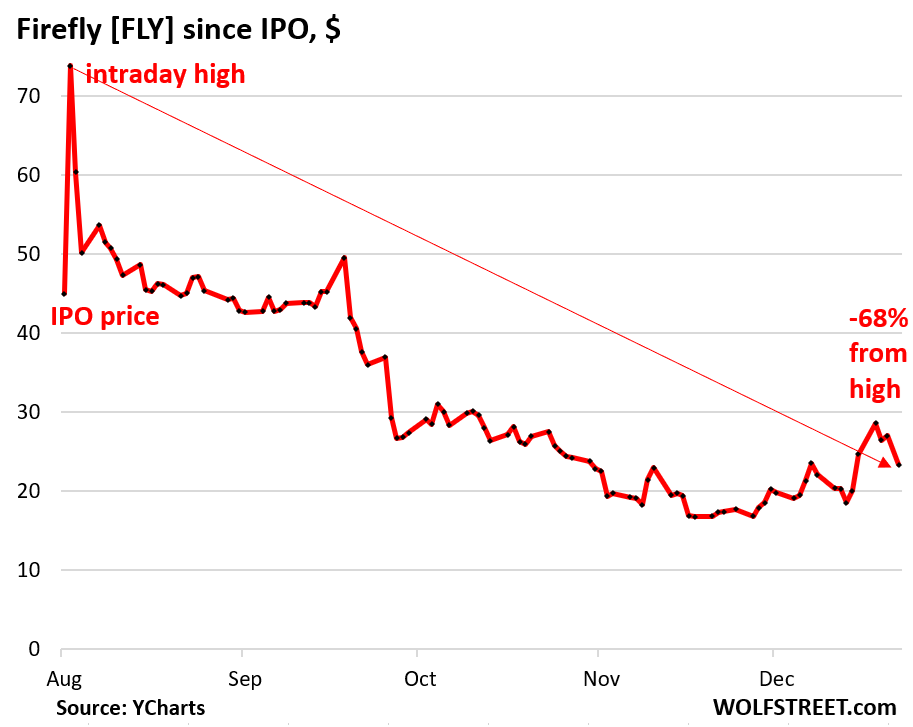

#12 Firefly [FLY], a space and defense company, went public in August at an IPO price of $45 a share, raising $868 million. Then shares spiked to $73.80 on the first day before plunging. On Friday, after a 13.7% plunge, shares closed at $23.34, down 68% from the intraday high and down by 48% from the IPO price.

#20 Fermi [FRMI] went public in October at an IPO price of $33 a share, raising $683 million. On the second day of trading, shares reached their intraday high of $36.99, then plunged. On Friday, shares closed at $8.88, down by 58% from the IPO price and by 76% from the intraday high.

Figma, the design software company, missed the cutoff for the largest 20 IPOs, but it’s included here because it had an iconic IPO. It went public in July at the IPO price of $33 a share, spiked to $142.92 during the first day of trading and closed at $115.50.

VC firms Index Ventures, Greylock, Kleiner Perkins and Sequoia “are sitting on $24 billion worth of stock after massive IPO pop,” CNBC gushed after the first day of trading.

By Friday, the stock had plunged by 73% from the high, but was still up 17% from the IPO price.

And in case you missed it:

WHOOSH, Went the Economy in Q3. The Fed Needs to Watch Out, Economy Is Running Hot

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Looks like many, not all, that got initial shares will still make a mint but seems like that is the goal with many of these IPOs. Short term payout over any long term viability.

You can see in the second column from the right which IPOs still made money off the IPO shares. You can count them. As I said in the article, 14 of the top 20 fell BELOW their IPO price (indicated in bold in the second column from the right). So, how many IPOs made money for investors in the IPO shares? 20-14 = 6. The table also shows Figma, under the top 20 and not part of the top 20.

Slightly ignorant question.

For those involved in the company at time of IPO do they simply get a chunk of shares for essentially nothing but then just have to hold them for a period of time? This was the group of people who I thought might be cashing out.

If and likely when OpenAI has an IPO in next few years I would assume Altman would get a bunch of shares and then employees based on some criteria(seniority, value, etc). That will likely be an insane IPO if the hype holds up, although they have partnered with Microsoft although not clear on all the particulars. Seemed like just to get a headstart for co pilot.

Employees who have received shares in the years before the company went public in theory could sell shares during the IPO if that is written into the IPO plan (S-1 filing). For example, the founder might sell some shares. But usually employees have to wait selling shares until the end of the lock-up period, such as 90 days or 180 days. They also have blackout periods around earnings, etc.

I will testify that we all are vulnerable too gambling, which in my case has a variable history, similar too everybody else. The great unwashed that drives capitalism.

Clueless, since the passing of the WW2 veterans.

The lost art of organization, perhaps.

How many of those IPO starter spikes were Politicians cashing in?

Probably about…..none.

Someone close to Martha Stewart once said she worked hard and stuff, but when her company had its initial public offering , that’s when she truly felt rich for the first time.

She was dumbfounded how rich she became just because a bank (like Goldman Sachs) had offered stock.

Pretty cool!

As a Nigerian Prince, I delegate all the necessary bloodletting to my royal surgical team.

They also take busted Nigeran startups out behind the woodshed when necessary.

See guys, this is how you amass a fortune that you can then give away to random people out of the kindness of your heart.

The least valuable asset given across the generations is obvious.

Just read an article about Private Equity selling their own companies to themselves.

Apparently since rates haven’t dropped enough, they are better off just valuing these companies for a ton and then somehow they sell and purchase them or whatnot.

There have been a lot of losses to public statements fund investors cuz of these shenanigans.

The problem is that these PE firms have owned these portfolio companies for many years and need to cash out. They typically have a 7-year time span in mind. But for many portfolio companies, that 7 years has come and gone.

What they did over the past few years is sell their portfolio companies to each other. But now that scheme got stuck in the mud of super-high valuations that other PE firms don’t want to pay anymore. So they had to come up with a new scheme: a PE firm sells one of its portfolio companies that is in its Fund X to its Fund Y, thereby allowing investors in Fund X to cash out.

But they’re also doing lots of cash-out leveraged loans, put onto their portfolio companies, to pay special dividends back to investors, so that they can get at least some cash.

Private Equity (PE) and private credit are super ripe. They’re now both trying to get retail investors to bail them out.

“Ripe”…is definitely…a word for it…

“that is in its Fund X to its Fund Y, thereby allowing investors in Fund X to cash out.”

Man oh man that just sounds like lawsuits waiting to happen…a/the key player in these deals (the GP – general partner) is on *both sides* of the deal – working with (and in theory having a fiduciary responsibility to *both* the buyer and seller).

Under a fiduciary standard, I’m fairly sure that is an inescapable conflict of interest and breach of the duty of loyalty (as in, exclusive loyalty)

I’m sure these PE firms try and contract around any fiduciary responsibility (not easy for GPs in limited partnerships) but since entities like public pension funds and college endowments are supplying the majority of the actual money to these PE firms, when things blow up (and how could they not with over inflated portfolio company valuations and opaque self-valuations of those untraded entities) judges/taxpayers on the hook are going to want heads on a platter.

I guess the GPs can join America’s politicians when they defect to China…

Retail will get “ripe” like ripe pumpkins after Halloween in Texas in those years when it has been 85 degrees for a couple of weeks – so rotten and mushy that even the squirrels won’t eat them.

My 8th grade chart reading skills.

Sell 100% of your IPO stock within a week of the IPO and then stay away.

The only problem?

The vast majority of shareholders (numerically, not in terms of ownership %) are contractually “locked-up” – they can’t sell/dump their hard-earned shares for 6+ months.

The NYC underwriters, their favored clients, and a handful of IPO company insiders are the only ones free to liquidate a portion of their shares in the immediate days following and IPO.

(That’s the exact reason why the share prices crash in the first place…those insiders substantially dump shares into a market thin with buyers for a brand new company, followed by the equity-holding employees months later, after the lock-up. 25+ years ago things weren’t quite this…abusive…but like most everything else in American life, it has degenerated.)

I once shorted mining stocks. Had I been able too cover the margin call I would have been richer.

Instead, I lost betting against impossible odds

holding when I had the chance too exit from my heavily leveraged position with a tolerable loss proved what is true. Man is an imperfect representation of the ten commandments in everyday life.

Most investment houses have flipping rules. If you buy and sell your IPO allocation within 60 days, then you can no longer buy IPOs. Existing owners get out by transferring their stock to IPO buyers then the price crashes as IPO buyers all look to get out.

The hustle is to become accredited, but pre IPO, then dump the first week, but only the ultra wealthy can do that

I’ve seen that movie, except I think it was penny stocks, not IPO shares. “Boiler Room”. Vin Diesel played a scam arti^H^H^H^H^H^H^H^H stock broker.

Given the consistent record of price collapses, *somebody* is dumping shares within a couple weeks of IPOs (and this has been going on for 25+ years).

1) Underwriters are pretty much running the show (“No bucks…no Buck Rogers”) so I’m assuming they pretty much give themselves a very free hand (Corporate insiders may try and push back but it is the rare IPO company that has the kind of buzz to make their opinion stick in the face of underwriter resistance).

2) Underwriters *also* make a ton of money servicing their HNW clientele – so I imagine (“rules” notwithstanding) the upper half of that HNW client base gets a pretty darn free hand to dump IPO shares at will. The underwriters may not particularly like it…but without that HNW clientele to service, Wall Street broker dealers have a much, much smaller business period. HNW people tend not to get that way without being demanding/getting what they want.

3) The core insiders likely get a fairly free hand too – basically to buy them off and shut them up (and to get the IPO business in the first place). But I’m sure the underwriters work very hard to point out that if high percentage shareholders (like the founders/insiders) dump, a) it looks absolutely terrible and b) the supply will absolutely destroy share prices – even beyond the documented common price declines.

4) Employees with options…usually treated like mushrooms (keep them in the dark and bury them in…). *Those* are the people for whom the lock-ups are truly binding. All too many stock option incentivized employees really don’t understand just how fragile IPOs prices are.

Is there a simple way of seeing the aggregate performance of the 2025 IPOs? In other words, if an index fund had bought and held 1% of each and every 2025 IPO, what investment result would it have had?

Renaissance Capital has the IPO Index, but it includes IPOs from some years ago. The IPO indexes biggest holdings include Reddit (IPO in March 2024), Arm Holdings (IPO in Sep 2023), Instacart (IPO in Sep 2023). So it’s useless for the 2025 vintage of IPOs.

The IPO ETF based on the index [IPO] is up 4.2% YTD.

The SPY ETF, tracking the S&P 500, is up 17.5%.

I researched SMA – it’s not too bad. Their third quarter FFO was .47 a share with a distribution of .14, looks like they’re pretty solid. They have not yet filed a 10-K as a public company – I always like to see that.

7:46 AM 12/29/2025

Dow 48,516.58 -194.39 -0.40%

S&P 500 6,908.51 -21.43 -0.31%

Nasdaq 23,477.24 -115.86 -0.49%

VIX 14.64 +1.04 7.65%

Gold 4,351.60 -201.10 -4.42%

Oil 58.22 +1.48 2.61%

High yield bond ETFs like JNK and HYG are worth taking a look at, they should start to wash out(trade lower) tomorrow. High yield junk is like a piece of protection for trad rock climber(risk on trader), when JUNK fails other pieces of protection will zipper down in the fall. its building up , you can feel history in present time with the markets. I was ski bum in Breckenridge CO, when Japan peaked on todays date in 1989, a year earlier the Japanese bought Breck ski resort with some golf courses, they had so much confidence, just like we do today. You can feel it in time, wash rinse repeat. the Algo of life :) its going to make a great movie.

I feel once JNK goes under $96 all hell will break loose.

LOL, yeah totally. :) spot on $vix will get above 18.52 when Jnk goes below 96. :) thanks for the kind expression last week. All seriousness we are setting up for a storm. Yesterday, I listen to a friend share about his fears during late 2008 and early 2009 and empathetic feeling about the real estate investors in our town that lost everything. I didn’t tell him my take on what’s happening now. Smart people will listen to their intuition when it speaks to them. :)

I reviewed my stock portfolio today. 200 shares in a company that went out of business ages ago issued to me as an employee of a darling work environment

Stocks open lower — and volatility perks up — as silver and gold pull back with gold plunging a record $200 an ounce…

At the start of 2022 the 🐻 button was hit.

Start of 2026?

Sold some scrap gold jewelry and some silver to a shop in SF on Friday. Literally marked the top. The guy checked his phone, silver was $79+. They cashed me out at $78, and $4285 for gold. Asked girlfriend to estimate how much I will get for the lot. She’s Asian and very good with math – said $80 for the whole bunch. I got $1200. Lol

I’ve been saving all my Monopoly money since I was age 5 so I can buy the Wolf Street IPO. I’m ready.

I agree. Wolf is mostly or often correct in his interpretation of the data that Wolf meticulously presents.

I am boggled by the private equity and other investments in these types of companies. They often have highly unrealistic business expectations and the goal is to hit on 1 or so big time but feels like such a waste of resource. Feels like in the prefabricated home building this exists as well although I suppose a few are profitable but will be interesting to see how Boxabl does this Spring in SPAC if goes through. Prefabrication happens in a lot of areas to my understanding but for residential and small / tiny homes not clear the overhead pays off.

Along these lines, take a look a the Renovo home renovation company PE implosion.

A generally non-moron PE firm attempted to roll-up a ton of mom-and-pop-ish home renovation companies and (not terribly unsurprisingly) this didn’t work out – to the terrible extent that the mess went straight to Chapter 7 liquidation (not even an attempt at a Chapter 11 turnaround…which is pretty darn rare).

Without salable corporate assets with *some* residual value, PE investments are extremely risky. I wonder who the suicidal lenders on the Renovo deal were.

Renovo:

https://wolfstreet.com/2025/12/23/whoosh-went-the-economy-in-q3-the-fed-needs-to-watch-out-economy-is-running-hot/#comment-665430

Renovo brands:

Dreamstyle Remodeling

Alure Home Solutions / Alure Home Improvements

Reborn Home Solutions / Reborn Cabinets

NEWPRO Home Solutions

Remodel USA (Remodel US / Remodel USA)

Woodbridge Home Solutions

Minnesota Rusco

A guy who I think ran Yale’s endowment fund was the first one to stick his toes (and Yale’s) in Private Equity.

He made insane amounts of money for them as PE did even better than the stock market for years and years.

I think Buffett was picking his brain for a bit. He wrote a book about it all. Swenson, that’s the name.

In the private VC backed companies, so many down rounds in the past 3 years but not advertised. XYZ raised an additional 30m to grow but in reality the prior 200m invested was going to zero out without new capital to keep the doors open. Time decay is real. Eventually investors will say no more good money after bad money. The hard no to the capital calls will be the end to pretend unicorn world. On a side note gold at 2650 by end of June 26, symmetrical with numbers?…6 months to give up the past year rise. The Algorithm has targets they are usually invisible without modifications. The person who has the most fun and the most love wins the game!

Gives the most love wins the game! Enjoy

Man I sure am glad the federal government is pushing all these crypto things that happen to be based on islands where you can’t get your money back.

And yet, somehow, all those venture capital firms made money, a lot of money…

What a joke the american eCONomy is.

good stuff. thanks wolf

The failing IPO’s fundamental error was not mentioning AI in their prospectus. Otherwise, they would still be to the moon.

What you point out, that the hype is that AI is a beneficial technology when clearly there are gaping holes between authenticity or the cheap AI knock off.

In my mathematical experience I found the machine learning models to be constrained by the parameters negotiated as which portion of humans are worthy of having a mimic of their realty to be selected as desirable

“Technology

Time from Public Release → Mass Adoption

Internet

~10–15 years

Smartphones

~5–8 years

AI Models

~2–5 years

AI is spreading faster because it:

• Is cloud-based (no physical distribution)

• Requires no new hardware for users

• Piggybacks on existing internet & smartphone infrastructure”

Any journeyman participant in the financial life has an opinion on the valuation metrics applicable too PE firms.

IPOs, stock splits, reverse stock splits, corporate bonds, stock options, bonuses, bailouts, leveraged buyouts, private equity funds, hostile takeovers, trillion dollar companies, insane P/E ratios. The fact is, Wolf, that our economy is in large part a casino. Just way more profitable than Vegas!

The financialization of pretty much everything within sight…

It’s going to be interesting when retail investors are allowed to pour money into PE. Will retail still pour money into because of FOMO if they already have exposure? What will be the new exit strategy if IPOs won’t be able to generate enough profit to reduced leverage?

“Hanging ten off the lip

Sand between our toes,

Even though we’re not real brite

We strive to walk the nose.

Here come the surfmen.

The surfmen, ride like nobody can.”