Central Banks diversify their holdings into dozens of smaller “non-traditional reserve currencies.”

By Wolf Richter for WOLF STREET.

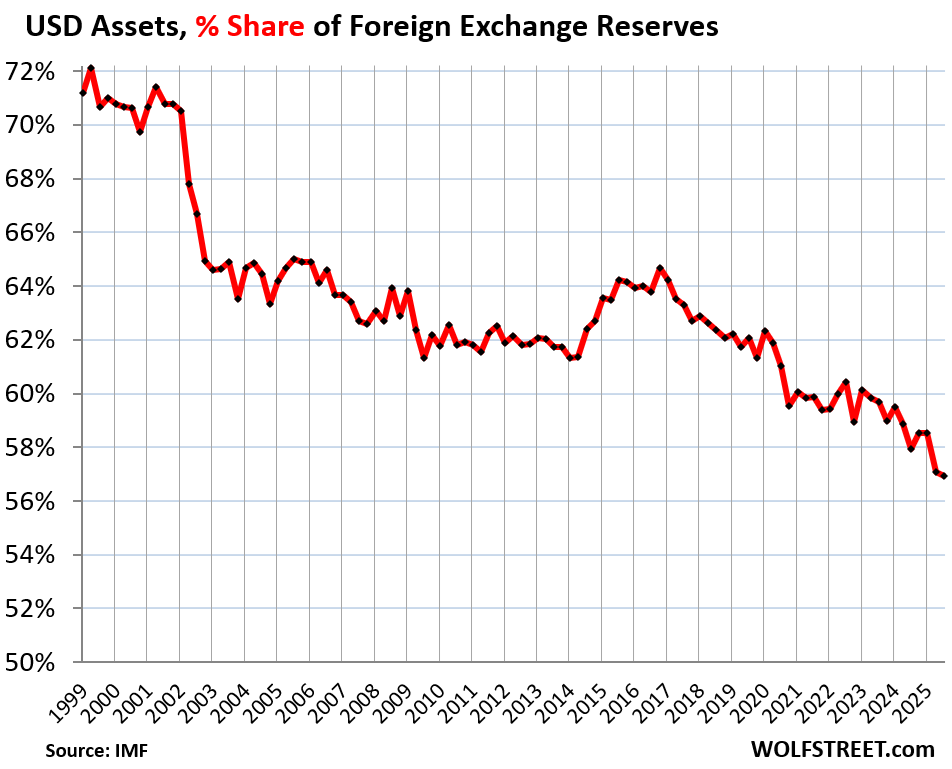

The share of USD-denominated assets held by other central banks dropped to 56.9% of total foreign exchange reserves in Q3, the lowest since 1994, from 57.1% in Q2 and 58.5% in Q1, according to the IMF’s new data on Currency Composition of Official Foreign Exchange Reserves.

USD-denominated foreign exchange reserves include US Treasury securities, US mortgage-backed securities (MBS), US agency securities, US corporate bonds, and other USD-denominated assets held by central banks other than the Fed.

Excluded are any central bank’s assets denominated in its own currency, such as the Fed’s Treasury securities or the ECB’s euro-denominated securities.

It’s not that foreign central banks dumped US-dollar-denominated assets, such as Treasury securities. They did not. They added a little to their holdings. But they added more assets denominated in other currencies, particularly a gaggle of smaller currencies whose combined share has surged, while central banks’ holdings of USD-denominated assets haven’t changed much for a decade, and so the percentage share of those USD assets continued to decline.

As the dollar’s share declines toward the 50% line, the dollar would still be by far the largest reserve currency, as all other currencies combined would weigh as much as the dollar. But it does have consequences.

Why is having the top reserve currency important for the US?

Foreign central banks buying USD-denominated assets, such as Treasury securities, helps push up prices and push down yields of those assets. Being the dominant reserve currency had the effect of helping the US borrow more cheaply to fund its huge twin deficits – the trade deficit and the budget deficit – and thereby has enabled the US to run those huge twin deficits for decades. At some point, this continued decline as a reserve currency, as it reduces demand for USD debt, would make the trade deficit and the budget deficit more difficult to sustain.

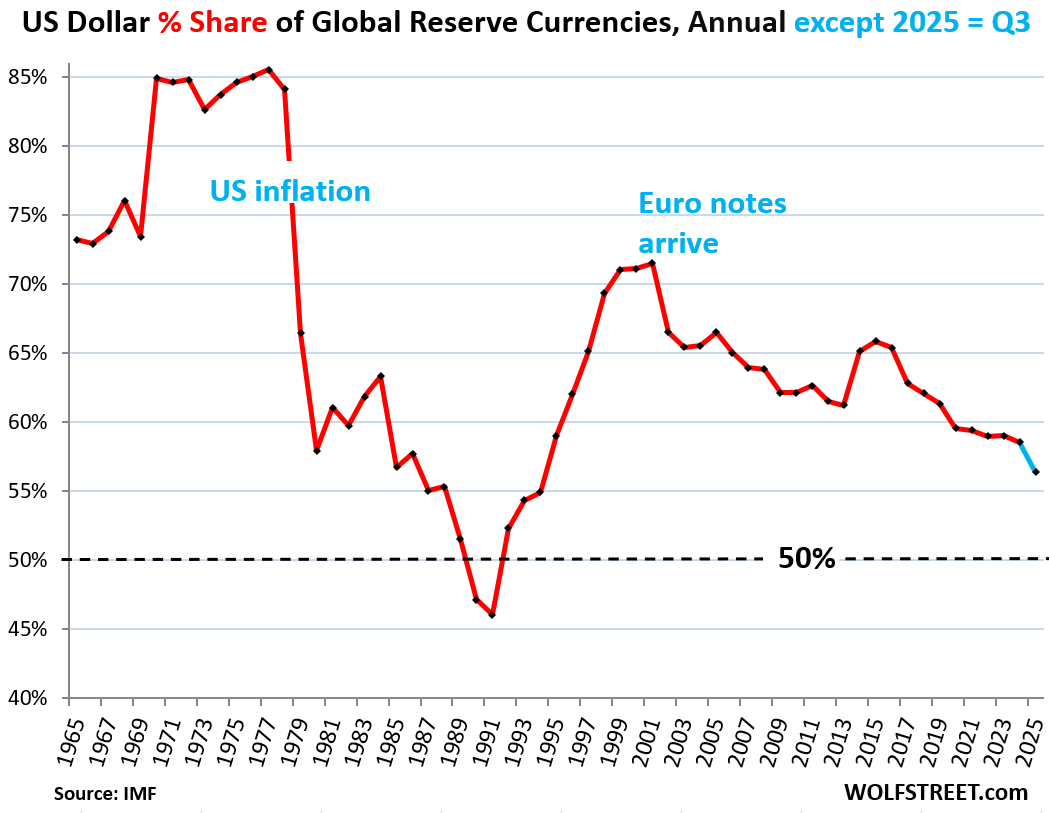

The dollar’s share had already been below 50% before, in 1990 and 1991, after a long plunge from the peak in 1977 (share of 85.5%). This plunge accompanied a deep crisis in the US with sky-high inflation and interest rates, and four recessions over those years, including the nasty double-dip recession. Central banks lost confidence in the Fed’s willingness or ability to do what it takes to get this inflation under control that had washed over the US in three ever larger waves.

The dotted line in the chart below indicates the 50%-share. The dollar’s share bottomed out at 46% in 1991, by which time the Fed had brought inflation under control, and soon, central banks began loading up on dollar-assets.

Then came the euro, which turned into the next set-back for the dollar, but not nearly as much as European politicians had promised when pushing the euro through the system; they were talking about parity with the dollar. That talk ended with the Euro Debt Crisis that began in 2009.

Then, over the past 10 years, came dozens of smaller “non-traditional reserve currencies,” as the IMF calls them.

The chart shows the dollar’s share at the end of each year, except 2025 where it shows the share in Q3:

But they didn’t actually dump USD-denominated securities.

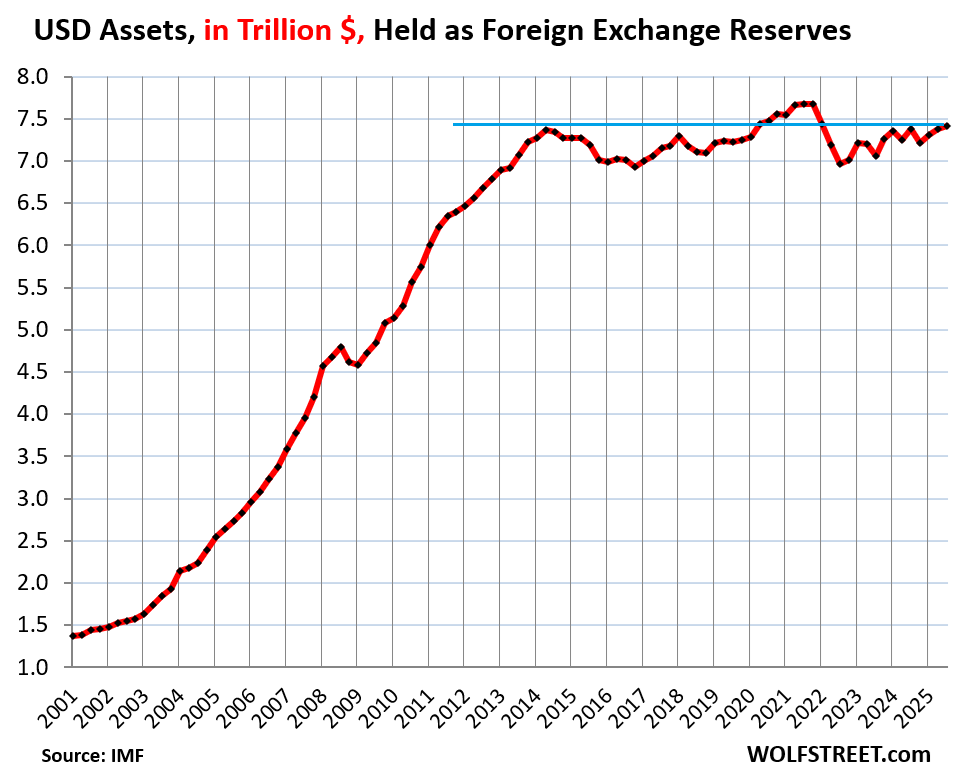

Foreign central banks increased their holdings of USD-denominated assets by a hair in Q3 to $7.4 trillion, the third increase in a row.

Since mid-2014, despite some sharp ups and downs, their holdings of USD-assets have remained essentially flat.

So, what has caused the percentage share of USD assets to decline over the years is the growth of foreign exchange reserves denominated in other currencies, particularly many smaller currencies, as central banks have been diversifying their growing pile of foreign exchange assets.

The chart below shows foreign central banks’ holdings of USD-denominated assets – US Treasury securities, US MBS, US agency securities, US corporate bonds, etc. – in trillions of dollars:

The top foreign exchange reserves by currency.

Central banks’ holdings of foreign exchange reserves in all currencies, and expressed in USD, rose to $13.0 trillion in Q3.

Top holdings, expressed in USD:

- USD assets: $7.41 trillion

- Euro assets (EUR): $2.65 trillion

- Yen assets (YEN): $0.76 trillion

- British pound assets (GBP): $0.58 trillion

- Canadian dollar assets (CAD): $0.35 trillion

- Australian dollar assets (AUD): $0.27 trillion

- Chinese renminbi (RMB) assets: $0.25 trillion

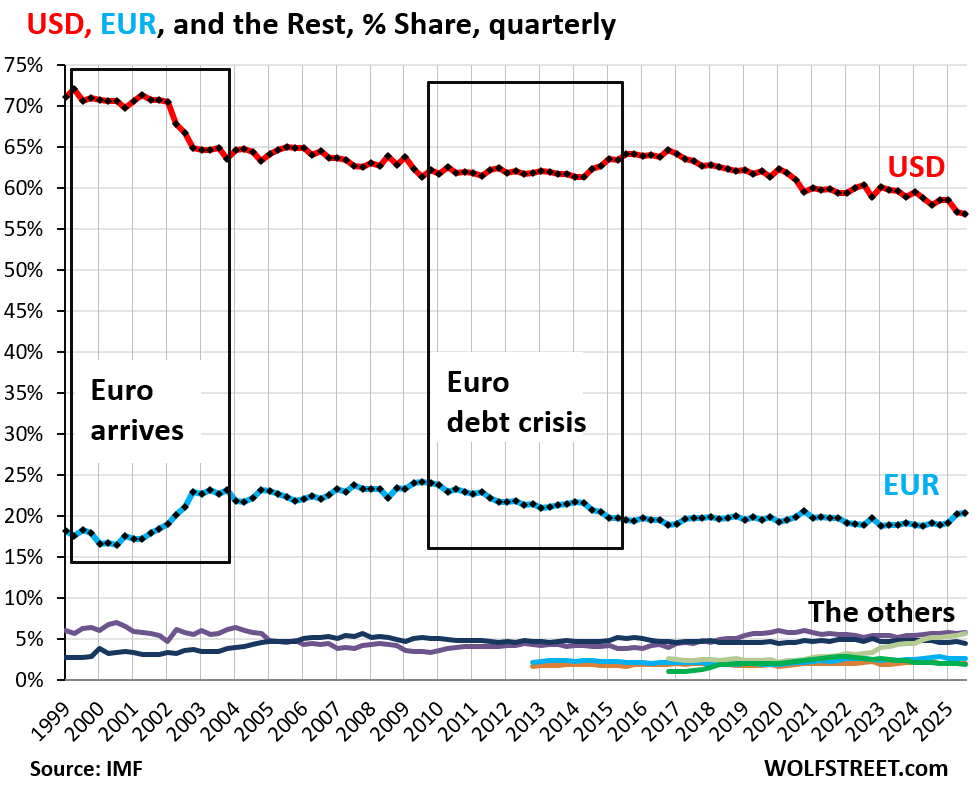

The euro’s share, #2, has been around 20% since 2015. Before the Euro Debt Crisis, it was on an upward trajectory and had already risen to nearly 25%.

The rest of the reserve currencies are the colorful spaghetti at the bottom of the chart (more in a moment). Combined, they have gained share over the years, at the expense of the dollar, while the euro’s share has remained roughly stable since 2015.

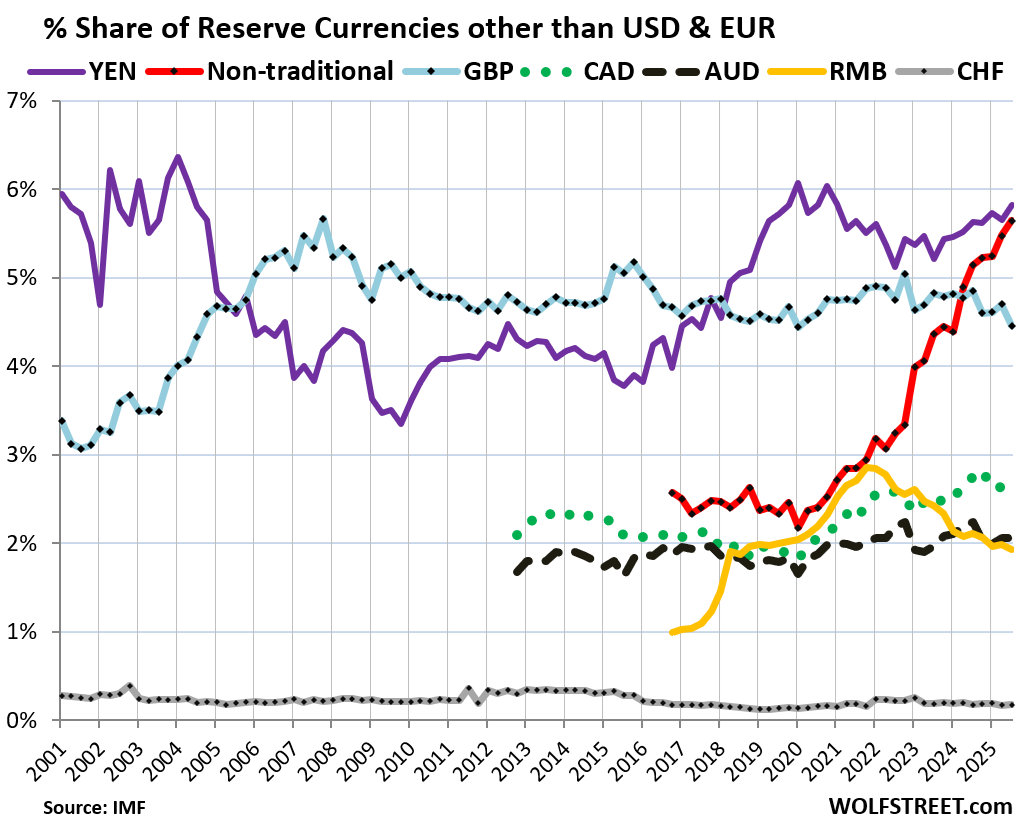

The rise of the “non-traditional” reserve currencies.

The chart below takes a magnifying glass to the colorful spaghetti at the bottom of the chart above.

The soaring red line shows the combined surge of assets denominated in dozens of smaller “nontraditional reserve currencies,” as the IMF calls them. Combined, they reached a share of 5.6%, just below the yen-denominated assets (5.8%).

But the share of the RMB (yellow) has been declining since Q1 2022, and its share is now back where it had been in 2019, amid ongoing capital controls, convertibility issues, and a slew of other issues.

In other words, the USD and the RMB both have given up share to the “non-traditional reserve currencies” as other central banks have been diversifying away from assets denominated in USD and RMB.

In case you missed my update on a slightly less ugly situation: US Government Interest Payments to Tax Receipts, Average Interest Rate on the Debt, and Debt-to-GDP Ratio in Q3 2025

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Waiting for the cliff! There is no way to stop this train. We could if we stopped using the dollar as a weapon and balanced our budget! Zero chance of that.

Would not bet on this trend to continue forever. Once word spreads on stablecoins and on how to purchase those dollars in shitty 3rd world countries using only your mobile, escaping the local depreciating currencies, the dollar will probably even strengthen in relative terms.

You’re getting things confused. “Foreign exchange reserves” — the topic of this article — are holdings exclusively by central banks and are not related to what people do with their local currencies and how they exchange them in everyday life.

IMHO – it’s surprising that this measure was lower in 1993-1994. I would have thought this measure was lowest since WWII.

MS,

It’s not surprising to me because I lived through the mid-1970s through the 1980s in college and grad school with various jobs along the way, and then starting my career. And I remember what it was like: sky-high inflation, sky-high interest rates, tens of thousands of banks and S&Ls collapsed, big repeated waves of unemployment topping out at over 10% and staying over 7% for many years. It was very hard to find a job. These were tough times for someone to start out in. The US was in a crisis. It eventually got fixed or fixed itself, and the 1990s were much better.

Brilliant

Just wanted to say thanks for these charts Wolf, one of clearest presentations I’ve seen on it and clarifies a lot of things I used to be confused about on the reserves topic

Buying stable coins is like buying MSTR instead of buying bitcoin for people who believe in crypto. Instead of buying stable coin it’s safer to buy directly US T bills that backs the coin. Poor people around the world don’t have extra money, the people with extra money around the world are already in dollar denominated assets. Money is liquid it flows; stable coins are way to generate fees for the coin creator and NBFI, and sell or offload risk to the buyer. Genius act fallout will ask for a taxpayer bailout in 27, at least that is my running assumption. I am not a hater of new technology just recognize a casino when I see one.

I am focused on the Wolf paragraph

They added a little to their holdings. But they added more assets denominated in other currencies, particularly a gaggle of smaller currencies whose combined share has surged, while central banks’ holdings of USD-denominated assets haven’t changed much for a decade, and so the percentage share of those USD assets continued to decline.

The underlying currency of the world’s commerce, that rapacious beast that manifests itself in full view of denial is the Uncle Sam based dollar system.

It reversed in the 90s. Why can’t it reverse again?

Because there were no challenge in 1990s but now it is challenged by China and BRICS both in monetory term and technological term.

The 1990s saw a “resolution” to the previous decades’ fiscal and monetary failures.

It was (unfortunately) a short-lived success. One presidential administration in our lifetimes presented a balanced federal budget (and created surplus).

See Wolf’s previous article and the trajectories of: 1. Interest payments to tax receipts, 2. Debt to GDP.

Debt:GDP rolled over in the 90s, which I assume influenced the turnaround of Central Banks’ attitude toward the USD.

That’s exactly why the world lost trust in the dollar. Successive administrations have weaponised it against other nations. Even against its allies. Eventually how do you think these countries will respond? Trump started the tarrifs in the assumption that the world would bow to US’ whims because everyone desperately need the US. Well, no one’s scared of the Big Bad Wolf anymore and now there’s the BRICS countries. They’re already doing most of their trade in their own currencies. They’re not interested in acquiring US dollars.

It doesn’t make any difference at all to the US or the US dollar what currencies companies use to pay for stuff, whether it’s cross border or local. No one cares what currency a company in China uses to buy stuff from a company in Brazil or Russia. It just doesn’t matter. They spell the currency out in their sales agreement, and that’s it.

It DOES make a difference if foreign central banks shed their USD assets (topic of this article).

The BRICS currencies, except for the Chinese RMB, have all plunged or collapsed against the USD. If a company wants to get paid in one of those currencies, fine.

Wolf, why on earth would many foreign central banks invest so much currency these days in non currencies such as gold and even silver these days since we are talking about currencies of central banks here.

I think it makes a big difference. To the extent the dollar is the trade dollar, many central banks settle their exchanges of foreign currencies in dollar vehicles that they can use for many other exchanges with other nations that also need US dollars, especially when the petrodollar was running strong. That is what made the dollar the global trade currency. This creates huge demand for dollar-denominated bonds in banks that run those exchanges.

Based on that, I predicted the dollar would take a huge hit this year due to tariffs diminishing its entire reason for existence as a “trade currency.” Less trade equals less need for a trade currency. As a result, we see central banks no longer increasing their hold on US dollars but increasing their holds on many other currencies.

More directly, though, to the extent that companies in other nations trade with US companies, they have to write checks or debits that adjust the amount paid by the exchange rate with their local bank. As those banks exchange directly with the US centra bank or through their own central banks, they almost always do so by trading US-denominated bonds (especially Treasuries) to make their exchanges. The central banks of those locales particularly do a lot of that kind of trading:

While it is completely true that companies trade using their local currency. The fact that US products are sold in US dollars means currency exchanges are necessary through those companies’ local central bank that processes the checks or debits of those local companies. The company trades in its local currency, but ultimately its local central bank exchanges those currencies for US dollars to complete the transactions for their member banks, and they do this, not one check at a time, but by moving dollars in huge bundles—typically dollar-denominated bonds, most often US Treasury bonds from time to time.

When there is far less trade with the US in those countries, there is far less need for those huge dollar containers (dollar-denominated bonds), so central banks stop purchasing as many of those and may even, as you show in your article here, switch to purchasing bonds in other national currencies where more local trade is happening. So, even if their holdings in US bonds went up by a lot less than usual this year, we see a move to holdings in other currencies becoming more involved in international trade. I suspect we will see this move go from a diminishing of purchases of US Treasuries to a lowering of existing holdings in US Treasuries as banks become more convinced that the world of trade has permanently shifted under tariffs. Right now, all of that is still in considerable flux.

When other countries ran trade surplus with us they reinvested their extra USD here making the USA the world piggy back. Our US exceptionalism was the result of easy access to capital to take risk. Those trends may all be changing with current changes under way. Our military will always give us an edge in receiving capital but that may also be changing. For instance, Germany is getting self sufficient and will probably buy less US dollar denominated instruments. Tis the season for change ; Nikkei 225, peaked on December 29, 1989, hitting an all-time intraday high of around 38,957.44. It took until Feb 22 2024 to regain that high.

Well there is that rather than the obvious solution which is the public option access to medicare level insurance. Perhaps a scale that charges more if you are one of the fortunate few wealthy rather than our current work horse the working family.

DXY is in a trading range since July 1st low @96.4. When trillions of foreign promises actually pour in the dollar will rise. If SPX turns down DXY will rise. The dollar might fall only if we lose a major war.

I agree with you, DXY 50DMA is 99.13 above its 200 DMA of 99.06. Everything is interconnected and it’s all setting up for the perfect storm. If DXY gets above 102 it’s a good time to diversify 105 would be an overshoot of the 104 target. I like the traditional commodity currency, Canada kiwi and Australia, Norway. When or if the DXY reaches those levels I would be a buyer of commodities currency or their short term bonds. The USD or DXY looks like a safe place to be and of course the Yen, but the yen has implied risk if central banks other than Japan make a coordinated action to prevent the Yen from appreciating as a PUT to global risk selling. Our Inflation should rise and unemployment should fall. Government Puts will be sly. If the $2000 stimuli check get issued in 26 will 9 million defaulted student loan people make a 2k payment? Probably not. :) but they should!

Those 9 million people would be wiser to spend $2k on increasing their skills and employability (especially learning how to work with AI and build workflows) so they can increase their earning power and pay back their loans.

AI = Atrocious Idiocy

Saw an article elsewhere the other day that more and more people of all ages are successfully including student loan debt in their bankruptcy. Something needs to be fixed to push college prices down.

One must never neglect the very old regularity, the Santa Claus rally.

Personally, given the nose bleed valuations for risky assets, for me the correct strategy is T bill and chill.

I can’t calculate a scenario in which the current monetary conditions don’t end up in a roaring inflation episode

Asset prices are the avatar of inflation created by the excess issuance of the controlling commercial currency. It is not hard to find mathematical evidence that the increase in asset prices leads the increase in rental cost for that asset by six months or more. The increase in cost continues past the peak in asset prices which decline unable to sustain the price of hope previously assumed but have reevaluated and currently embrace the improbable, that the magic is codified within the most powerful human emotion. Even though the simplest love love love more love

Interesting article! Wolf, what happens to the graphs when the vertical axis is in Euros?

1. The euro didn’t exist before 1999. The long-term chart (chart #2) goes back to 1965.

2. The US dollar is still the reference currency, and so all global things, when expressed in a common currency, are expressed in US dollars. So you can get the GDP of Japan in YEN and in USD, but not in EUR. Get used to it.

Hello Wolf, thank you for producing this series on reserve currencies. I was wondering if you had any more detail on the specific currencies within “non-traditional reserve currencies?”

Anecdotally, I have heard that the Qatari Riyal has begun to play a significant role across West Asia and East Africa in terms of exchange, though I do not know if that would have any bearing on what currencies central governments keep in their reserves.

The IMF does not disclose detailed data on the dozens of currencies in the “non-traditional” category. The Chinese RMB was part of that basket until the IMF pulled it out in 2016 and gave it its own category that we can see now.

Note that the share of these dozens of currencies combined is 5.6%, so each currency alone has a minuscule share, but all combined, they account for 5.6%. If you add the RMB back into this group, the percentage rises to 7.6%. So as a group, it would be #3, but spread over dozens of countries.

The non-traditional currencies group was composed in part by the currencies of other OECD countries, according to an IMF article in 2022 (it didn’t give per-currency share and details either).

So looking at the OECD countries whose currencies are not broken out separately here, that would be the European countries that are not part of the Eurozone (Czechia, Denmark, Hungary, Iceland, Norway, Poland, Sweden), Mexico, Costa Rica, Chile, Colombia, Turkey, Israel, South Korea, and New Zealand.

The other part of the currencies was often based on trade relationships and currency pegs. Here is a quote from the article:

“For example, Namibia holds a large share of its reserves in South African rand due to its peg to that currency and trade relations with South Africa. Kazakhstan and Kyrgyz Republic hold Russian rubles due to their close trade relationships with Russia.”

Thank you for the explanation. I do wish the IMF would provide more detail on the smaller currencies. The quote you pulled out at the end is suggestive, and I am tempted to use it to spin a narrative about the rise of bilateral trade settlement in local currencies at the expense of USD.

Either way, it will be interesting to see whether these trends hold through the latter half of the decade.

1. Bilateral trade agreements have existed long before the big ones were negotiated. Neighboring countries always had trade agreements. But trade agreements are about tariffs and various customers regulations, not currencies. Trade agreements don’t dictate currencies. Companies that trade with each other can use whatever currencies they agree to use. And they have always traded in their local currencies, nothing to do with the USD.

2. The USD has never been used in trade between Namibia and South Africa. Or really anywhere in Africa. They use regional currencies, such as the West African CFA franc and Central African CFA franc. Or they use local currencies.

3. What’s relatively new are these huge global trade agreements, but even these huge global trade agreements don’t specify which currency has to be used.

4. Companies can pay for any purchase with any currency as long as the seller agrees to take it. This is part of the sales contract. If an African mining company sells minerals to a a company in the US, it’s going to gladly get paid in USD. If it sells it to a company in Germany, it’s going to gladly get paid in EUR.

5. Trading in USD is very different from “reserve currency” and has no impact on the USD. It doesn’t make any difference to the US whether a German company pays in EUR or USD for LNG from Qatar.

Are you sure about this statement?

“It doesn’t make any difference to the US whether a German company pays in EUR or USD for LNG from Qatar.”

Yes, I’m sure about it. That’s just payments.

What does make a difference is if German entities sell their USD securities to buy euro securities.

And what does make a difference is if the German company buys the LNG from Qatar instead of from a US LNG exporter. But the currencies used to pay for the LNG make no difference for the US.

I suggest that the latter half of the next 3 years is unlikely to look anything like the last 18 years.

AI is never capable of replacing the collective genius that programmed a machine that is never able too understand one word of what it took mankind a quarter of a million years to invent

What about the Indian Rupee?

What happened to BRIC’S impact on these numbers? I thought the plan was for them to become the new top dog and it seems like they are barely a blip.

Correct. The biggest letter in BRICS is the C, China, and the RMB’s share has been skidding for years, see last chart. The R, ruble, is a trash currency, and no one wants to hold assets denominated in it; it has collapsed against the USD. The I, Indian rupee, is down 50% over the past decade against the USD, steady as she goes.

Please can you summarize what’s going on ?

Why did you exclude gold?

This is just tiring.

1. Gold is NOT a currency and therefor not a foreign exchange asset.

2. This article is about “foreign exchange CURRENCIES” that central banks hold.

3. Gold does not figure into any of these numbers since it’s not a a currency and not a foreign exchange asset.

4. Gold is a “reserve asset,” and so you might want to see the share of gold as a percent of total “reserve assets.” But that’s a separate topic and has zero business being here.

I’m glad you asked because I didn’t want to get slapped by the teacher.

Baaaaaaah

No mention of Gold? Is that included in the redline of “non-traditional reserve currencies”

This is just tiring.

1. Gold is NOT a currency and therefor not a foreign exchange asset.

2. This article is about “foreign exchange CURRENCIES” that central banks hold.

3. Gold does not figure into any of these numbers since it’s not a a currency and not a foreign exchange asset.

4. Gold is a “reserve asset,” and so you might want to see the share of gold as a percent of total “reserve assets.” But that’s a separate topic and has zero business being here.

Gold leads to madness!

So shiny!

Haha

Then madness for me it shall be as I laugh looking at me stacks!

The premier conductor of electricity but too expensive supplanted by copper which was much more abundant than the much more scarce silver.

The computer I bought to run my AI models in 2004 had gold bus connections.

It still took umpteen hours for the model to reach a solution within the two std dev window that the model was able predict the outcome that it was trained to predict.

And the output was a prediction of the future based on the patterns of the past

“Gold leads to madness!

So shiny!

Haha”

Or sadness, Wah! I sold my gold in 2022 😒

Reserve currencies are a subset of reserve assets…though nowadays with Bitcoin and Gold so liquid they are becoming quasi-currencies. Drug and Weapons cartels are major enterprises who routinely settle transactions using these quasi-currencies.

The exact reason why all of the financial provisions in the Patriot Act are obsolete. Would-be terrorists can just send each other Bitcoin or numerous other cryptos and avoid the banks altogether. But no matter who is in the White house or Congress they STILL continue to extend that knee-jerk reaction known as the Patriot Act that requires your bank to spy on you

I think that bitcoin is a worthless token without support.

Gold has exceeded its utility and will equilibrate the tension between bid and ask at a much lower price.

But what do I know, nothing. In fact I have been so wrong for so long that even my wife is comfortable in wagering against my prediction,

Its not that hard to trace where the dislocation occurred

“Big change coming (very important)

• New IRS rules will require Form 1099-DA (Digital Assets) reporting

• Expected to roll out starting tax year 2025 (filed in 2026)

• Will eventually make crypto reporting closer to stock reporting”

Gold is a ‘tier one asset’ for the Bank of International Settlements.

Bitcoin is not rated and is unlikely to be rated.

Bob Triffin to the white courtesy phone…..Bob Triffin…

Same as Krypto that’s not what we’re analyzing here correct?

Initial hypothesis on rise of “non-traditional” reserve currencies…

Historically (pretty darn historically) the USD was a decent bastion of stability/store of value when compared to the vast majority of currencies around the world (whose issuing governments were not particularly shy about running the old currency printin’ press when their fiscal/trade balance management “policies” failed – a not uncommon event.)

But those days are long gone for the US, with its own deranged fiscal/trade imbalances and no honest fixes remotely in sight. Enter USD quantitative easing/money printin’.

So if you are a saver/international trade participant these days you are much more equally likely to get diluted/screwed by the USD as your own/bilateral trade currencies – so why go to the trouble/cost of interposing the USD in there?

Result – less reason to hold the USD around the world.

Agree with that. It’s not that the U.S. is really any worse than the other big currencies, as the central banks of Japan, England and the EU did equally stupid things before and during COVID. So the U.S. may still be the cleanest dirty shirt, but the cleanliness gap between it and the other dirty shirts is less than it used to be.

The U.S. has shown that it’s not willing to reduce spending, and is not willing to increase taxes. The only way out then is borrowing and inflation.

Hence, less reason to hold it and more diversification.

Cut spending or increase taxes.

Heck we have a fit if an attempt is made to clean up the fraud.

I dont agree. The last thing that China wants or the defective Euro wants i s to be the reserve currency

A thankless chore if there ever was one.

The USA is stuck with it v

Why? Europe would love the Euro to be the major reserve currency, it increases your number of buyers. Or are you saying that that causes your culture to become less financially disciplined?

It looks like dollar holdings are just fine……but in reality…..the purchasing power of dollars held by the banks since 2014 have declined by 37%.

Since the banks want to hold approximately the same percent of total gdp they have added other currencies to make up for the dollar.

So what looks stable is actually a huge drop in dollar holdings not only as a percent but more importantly how much it buys……which will continue as long as the deficits do…….good luck with that.

How much has the purchasing power of Euros or pounds held by the banks declined since 2014?

Have patience pls with my post, or tear me a new one.

Will the requirements of the genius act for stable coins to be backed by certain securities and US dollars support the future funding of the twin deficits and the US dollar.

And do you think there be any change in relationship to the US dollar and foreign reserves being held by others.

Is the exercise a move away from dependence on foreigners buying securities to support US debt and if so do you think it will work.

For me this is the most scary article. Trend is most scary if it is showing consistency. If new Fed chairman decides to fulfill wishes of his boss instead of what is good for inflation or US$ then we are up for a ride. Time will tell but historical evidence pointed by Wolf is not a good news.

We want foreign central banks to buy our dollar. Debt was fraction in 1999 and in 1980 compared to what we have right now. This is not good.

AR,to you and all here,what do folks believe is a solution to this problem of debt/is there one that could work besides total reset?

I have thought about this as our country and other countries debts keep rising,wonder if we are at the point of no return excepting a whole new start….,and the insanity that brings.

I will say I never signed a iou ect. on this insanity of borrowing,do not feel my mere existence requires me to accept this monetary bill(though may have to deal with the consequences).

A modest proposal: For starters, every federal agency (including military) gets 5% less, but unlike with DOGE, cuts are not micromanaged from the top for political reasons, and agencies must figure out how to accomplish their missions with less. Next, taxpayers all pay 5% more than they are presently paying. Net recipients of transfer payments (welfare etc.) take a 5% haircut. We keep the tariffs except some of the more punitive levels. We let Wolf figure out what they should be. All of this is done without malice. We all need to do with less.

I agree we need to survive with less and for most not a hardship,perhaps exempt those whom it would be,but,do not feel even that is nearly enough if we are serious about paying the debts owed,guess anything though as a start would help as it is figured out.

Yes we really do need to take steps toward using less. NOW!

And add 5% for everybody above a certain income

This is Merica…

It’s Faster horses…

Younger women…

Older whiskey…

More money

Spending cuts of 20% or higher across the board is what is needed and your approach of simply setting a percentage is the best.

Yes we really do need to take steps toward using less. NOW!

And add 5% for everybody above a certain income

I would vote for this. Make it 10%

5 or 10 % Take action NOW!

10% doesn’t cut it

10% cuts in expenditures would create a big budget surplus in theory. In practice, huge sudden cuts like that will send various shocks through the economy and mess up the economy and throw it into a tailspin that would cause tax revenues to plunge and create even bigger deficits. The budget issue has to be approached slowly and carefully. The way out is big economic growth (which will cause tax revenues to grow), moderate inflation (which will cause tax revenues to grow), and some budget discipline, such as increasing the budget at a slower rate than inflation for several years (which will represent budget cuts after inflation).

Instead of one big beautiful (gag) cut, how about a 1% cut in year 1. Then for the next 5 years, 0.5% cuts. Then the next 5 years after that, 0.25% cuts. Slow and steady, planned in advance. The debt “ceiling” would actually be a ceiling and not a floor as previous commenters have noted.

A blind, across the board, percentage cut would be the… impractical. You wouldn’t cut medical expenses by the same percent as dining out and neither should you tell kids on snap to eat less by the same percent that the Navy spends on toilet seats — pardon the hyperbole. Instead of everyone paying more in taxes, how about simply closing all of the egregious loopholes. Finally, instead of keeping the tariffs, why don’t we just shoot ourselves in the foot and tell our spouse, “yes, that outfit does make you look fat.”

Good point. It would need to be more tailored than what I said for this very reason. What I would like to avoid is changes perceived as hyperpartisan, which would provoke a backlash and overcorrection. I would like to get away from perceptions of bad faith from each political faction towards the other. We’ve gotten ourselves into a pickle, and we need to calmly figure out how to get ourselves out. Perhaps Wolf’s idea is better. I figure it would piss off fewer constituents than mine.

Practical, sensible proposal. Now all we need is for voters to stop falling for immodest and/or malicious politicians.

“Managed recession” is the solution. The Fed should regulate credit creation to keep annual GDP growth in the 1% range for a five year period. That would slowly squeeze out many zombie corporations through five years of a steady rate of bankruptcies.

I’d like to clarify my thinking here. “Economic growth” is measured as “GDP growth”, which is primarily new debt/loan creation, especially in the current hyper-financialized world. The goods/services produced with that new debt today are not commensurate to what they were in the 1940s, back when the USA last produced a similar debt-to-GDP ratio. Nowadays, debt is mostly borrowed from Peter to pay Paul, in the form of rolling over existing debt, or stock buybacks. Unlike the 1940s, when there were “real” goods and services produced that subsequently lowered the debt-to-GDP ratio, most of the 2026 “economic product” produced is inflation, borne by the lenders/bagholders. It’s true that the debt-to-GDP ratio is “stuck” at the moment, due to the extrordinarily high rate of debt creation right now (creating GDP growth). But when that firehose rate of lending ebbs, debt-to-GDP has nowhere to go but up, as lenders in “the market” get tired of being treated as bag holders rather than as respected business partners. We are already seeing a 10% drop in the proportion of Treasuries bought by “indirect” buyers (aka foreign central banks) at US Treasury autions, and that proportion is likely to fall further going forward.

Simplifying everything I just said, you can’t solve a debt problem by printing more debt, without a commensurate amount of real world goods and services produced (aka “real growth”). Even more simply said, hyperinflation is the end result of current US policy actions.

The “managed recession” approach I propose would indeed cause some pain, but could actually result in a better outcome in the end.

People who throw around “hyperinflation” applied to the US context have no idea what hyperinflation actually is. FYI: 5% or 10% or 15% a year is NOT hyperinflation.

I agree! What I was referring to is the “end game” of current US policy actions. They aren’t designing the system to increase “real” economic growth anymore. They are designing the system to hide all the new ways that the system is increasing the leverage ratios throughout the economy. There’s only one way that ends.

Possibly the monster we are looking at the next 10 years to 2035:

“ annual (government) outlays rising from about $7 trillion to over $10 trillion. “

“ • A commonly cited component economists focus on — debt held by the public — is projected to rise to around $52 trillion by the end of fiscal 2035 in some analyses. ”

Being the world’s reserve currency was initially a huge boon for the US. It was one of the primary reasons why the post WWII period of the 1950’s and part of the 60’s was such a sweet spot in our economic history.

However, as we know, being the reserve currency of the world is much like doing drugs. The addiction tears at the body and soul of the country. As other countries step up to compete, America has gotten hooked on running annual $2T deficits that the rest of the world has been paying for.

No major country in their right mind would want to repeat the reserve currency mistakes of Bretton Woods. The world will end up with a basket of currencies and gold as the new reserve asset for all. This will be fairer and have less downside.

Unfortunately for the US, this will mean we will have to live within our means.

I think you have the chicken and egg backwards. The 1950s and 1960s success was due to the U.S. having a virtual monopoly on manufacturing, as Europe was left destroyed by WW2 and the current manufacturing powerhouses of South and East Asia were not developed yet.

It was those factors that led to the U.S. dollar being adopted as the reserve currency. In other words, the USD as the world reserve currency was the symptom, not the cause, of our post-war success.

Thanks for your comment, you are right.

These were both the reason for such enormous economic advantage. And in reality the reserve currency annointment wouldn’t have occured without the circumstances at the end of WWII.

However, as you know, there was an alternate plan put forth by Keynes called the Bancor which was the basket of currencies and gold. While a better long term plan (for the world in my opinion), it would have struggled to work properly in the first couple decades after WWII because of all the weak economies.

In many ways, the US reserve dollar just had to happen after WWII, at least for a period of time. I think what we are seeing now is that it isn’t working for a number of other accomplished nations and certainly has fostered in the US a dependency on debt to run the country.

The shifting and sharing of world power is a story as old as time.

Bretton Woods was replaced by currency float and FOREX which allows the free market to set currency exchange rates. Gold is less than 1% of global assets and is not a currency of any sort.

Where do you people get this storyline from? American Monopoly on what? Europe had a big problem with food and resources in the beginning, but their factories were back to work the moment bombs stopped falling. Unwinding the mess of the German railyards took a little while, but they were producing consumer goods in no time. England was a bankrupt but that didn’t keep them from manufacturing their own products. They were even the first country to successfully put a jet airliner in the skies…albeit with the typical built-in problems that always surface in that endeavor. Japan’s steel industry was intact and rapidly undermined American products…our cutlery factories began shifting offshore and were totally wrecked in less than two decades. We lost practically every basic industry needed for daily work and survival in exchange for a bunch of electronic games. And China did us in because of our own foolish lawyer-led politico traitors who can’t figure out what underlies an actual base for all the other bloated crap. We won’t even go into all the people who got a lift up aquiring our used but still functional products…not that any of that helped our factories to produce any more to export anything…all because we throw shit out before we need to ensuring that the whole damn country goes deeper into debt which is always transferred to the national black hole. Now, please show us this giant mountain of American made products that were sold brand new to foreign countries under our so-called “Monopoly”, and then open up all of those domestic landfills and look at the volumes of imported junk that’s in them.

Europe rebuilt quickly after WWII due to very liberal funding from the Marshall Plan and the US.

That’s total B.S.! Military Authority had them back to work long before that government goon get rich quick scheme. The war was over…they would have pulled themselves out slowly but surely. Ugly? Sure. More might starve? Certainly. But that’s the cost that must come when you go around trying to murder the rest of the planet. Still, they would have climbed back up with or without us. We were just using them to stave off the freaking Soviets while letting stinking internal spies sell atomic destruction to yet another group of wacko’s.

Back to work the minute the bombs stopped?

The road back was lead by VW, but it was a long hard slog.

The factory at Wolfsburg fell in the Brit sector.

AI overview: British Army Major Ivan Hirst was the officer responsible for reviving Volkswagen after World War II. As Senior Resident Officer, he rehabilitated the bombed-out Wolfsburg factory, secured crucial military orders for the Beetle, and set the company on the path to becoming a global automotive manufacturer between 1945 and 1949.

Some detail: the place was surrounded by craters. The floor was flooded and workers had to wade for weeks. The first work was repairing VW’s for use by Brits. Pay was a bag of groceries a week.

Then came permission to assemble with parts on hand.

Meanwhile the Brits were cut off lend lease jeeps and were looking for a cheap solution. VW? A test was ordered. A corporal driving with a sergeant were told to take one out and kill it. With lots of craters this looked easy. They came back later, bruised and said ‘we can’t kill it’ ( Torsion bars, not spring suspension)

So the Brits ordered 10, 000. But first they let anyone who wanted to buy VW kick the tires. All the Brits looked. Ford looked. No one interested. Air cooled Engine in the back?

So is the rest history? No. Production was halted frequently by lack of raw material. It wasn’t until 4 years after the bombs stopped that things were running well enough to hand over.

When Hirst left they wanted to give him a Beetle but Army regs forbade this so they gave him a scale model.

Gold is a tiny little miniscule asset of no financial relevance at all.

Get your head out of the sand Beach Dude. I’m no gold bug. I won’t be around when the future folks need it to do all their space cadet junk, so I can’t say what it should be valued at now. But we wouldn’t be communicating here without metals, period. A shovel is real. Gold extracted and refined is real. Both can be used to build an economy, basic or advanced. All your valuations of dirt, stick shacks, phoney promises to pay, and contracts yet to be fulfilled amount to little more than the weight of air and a rushing wind to carry a fire. If this pile of nothing comes tumbling down there will still be someone who will pay gold to someone else to operate that damn shovel to grow food on the dirt field where your abandoned skyscrapers once stood. Get it? The electricity seizes up and no more finished metals can be had. Suddenly those ounces and tools become something and all of your fake economy is gone. No oil. No gas. No turbines. No jets. No computers. Wooosh. And no Wolf to tell you it’s all gonna work out. Remember that other guy who spread false hope? “Ooh, look out. Here come the waves of Allied Bombers to liberate Frankfurt and Berlin from the burden of having to get up in the morning.” Buy into the lies all you want. “Hedge accordingly.” China ain’t growin’ grass under their feet.

BuySome:

If I am not mistaken, it seems as though you are saying that gold is the only real asset and nothing else would exist or have worth without it ??

While I do believe that gold has value, and is currently doing quite well, I think many very real and productive things would exist without it. Someone can still drill an oil well, cut trees into lumber, or plant corn absent gold.

Gold may have value, but I believe you are overstating its intrinsic necessity.

I am not a gold hater either, and do believe it is useful in diversifying a portfolio.

Really? The market cap of gold is $32T which is more than the market caps of Nvidia, silver, Apple, Google, Microsoft, Amazon, Bitcoin, Meta, Broadcom, Tesla, and TSMC combined. It is a massive asset with massive financial relevance.

Wrong. All gold ever mined is less than 200,000 metric tonnes and is worth around 1% of all global assets making it totally and completely financially irrelevant with about 70% of it in jewelry.

Gold is not a currency but as a reserve has just overtaken US $ securities in the world’s other central banks for the first time since 1996. It was always a ‘tier one asset’ for the Bank of International Settlements in the meantime. Meaning it can be used to settle any country to country debt.

Living within our means could be traumatic for some but it is unarguably needed

Canadian dollar as a percentage of foreign currency reserve went up a bit from 2020 to 2023, and looks like it went down a bit this year.

The CAD to USD went up by a cent last week, not bad lol

And gold premiums are high in Canada: people are paying at least C$7500 for a legit ounce of gold and C$160 for an ounce of silver. And a fractional piece of gold is like buying it for C$10,000 an ounce. Tulip mania.

And Canada has weak laws against crime and self defence that jewellery stores are helpless when mobs of juvenile thieves storm the glass displays with hammers in order to loot the gold.

And there’s scandals of counterfeit gold being packaged as if it was from the Canadian mint. I’ll keep my “worthless fiat” for now.

“Since mid-2014, despite some sharp ups and downs, their holdings of USD-assets have remained essentially flat.“

Root cause? Did something happen in 2014 where central bankers decided that they needed more diversification?

I sold a 50 oz J and M silver bar in Canada about 2 months ago. The price was the same as the US price, adjusted for the currency at 72 cents C per US$. Needless to say I wish I’d waited 2 weeks or so, but the prices of gold and silver traded worldwide, adjusted for the currency, don’t vary per country.

PS: forgot, There was a 5 % commission but I assume the US buyer also does this.

All those asset freezes/seizures along with drunken inflation in last few years eventually got old to whomever had some trust left in USD.

I guess I’m the hoser ehhh? I went to sell some silver rounds on 12/23/25 and the LCS offered me $5 back of spot. I didn’t need the money so I walked out. Maybe I’m not a hoser afterall.

Doesn’t the surge in gold buying play a role in this; meaning changing dollars for gold?

This is just tiring.

1. Gold is NOT a currency and therefor not a foreign exchange asset.

2. This article is about “foreign exchange CURRENCIES” that central banks hold.

3. Gold does not figure into any of these numbers since it’s not a a currency and not a foreign exchange asset.

4. Gold is a “reserve asset,” and so you might want to see the share of gold as a percent of total “reserve assets.” But that’s a separate topic and has zero business being here.

Wolf, seeing the decline of central banks purchasing U.S. debt, is this along with the U.S. Treasury (prior) QT, leading to why the 10 yr treasury refuses to break below 4%; keeping 30 yr mortgage rates 6%+; hence locking up trillions in home equity, which ripples through the economy and GDP?

Is the reversal of this trend the key to lowering 10 yr treasury yields?

Folks can expect the US 10-year yield to keep rising significantly.

I agree and have no idea how to “get the 10-yr yield down.” I see a long term uptrend underway.

I did see a commenter mention how “yields are going down.” I’m not sure which ones, besides the 3-month or whatever.

The US, under Trump, spend less on poor people all over the world. The

UK and other Europeans are doing the same. Both the US and the

Europeans spend on their poor people, rearm, invest in the US and

rejuvenate their deflated industries. UT after distribution on falling

Xmas vol is bs. The weak hands can beat the strong hands.

Tell me, how did it go wrong? Gradually and then suddenly.

A 2024 IMF working paper states this about “non-traditional currencies”

“Rather, it has been accompanied by a rise in the share of what we have called nontraditional reserve currencies, including the Australian dollar, Canadian dollar, Chinese renminbi, South Korean won, Singaporean dollar, and the Nordic currencies.”

So yes, it’s actual currencies and not the speculation that’s being mentioned constantly on this message board.

The FOREX is the largest single exchange in the world with currency pairing and it is about nothing other than SPECULATION with wild swings.

Wolf, I still think you should publish an article about the dollar as a percent of RESERVE ASSETS, with gold included, and see what the numbers show.

In know, gold bugs care about that. But it doesn’t have any impact on anything. If a central bank buys gold, someone else has to sell it. Gold just changes hands. And the guy who sold it has to do something with those dollars, such as buy Treasury securities…

But all the hype about gold — even here in the comments — drives up the price of gold. It’s hype-driven, and I’m not going to participate in that hype.

And I would also have to list all the big central banks that have NOT been adding any gold at all for years, including the Fed, the ECB, the BOJ, the BOE, the BOC, and many others.

Firstly, thank for you the article. However as the subject of gold has entered the conversation – earlier you described the Dollar as a reference currency. Yet the Dollar floats. The whole subject was a ‘subject’ surrounding the Jamaica Accord in ’76 and was (purposely) not defined.

Add Triffin’s Paradox.

The absence of a real value peg prohibits price discovery (and leads to hot money flows that fail to produce real returns).

Bretton Woods failed in 1958. The London Gold Fix was an effort to prop it up and it was disbanded in ’68. The logical consequences were subject to math. What has gone on since ’71 has been one form of fraud after another.

Call me crazy – but I think we may be moving to a Bancor style clearing unit that will be backed by gold, particularly when you look at things like Project Aurum from the BIS – the world is actively looking for an off ramp from the Dollar (and we should be too).

Gold floats too, and more crazily than the dollar. No one in their right mind is going to allow a metal to strangle an economy just so that gold bugs are happy.

Gold is a speculative risk asset.

Bitcoin is a speculative risk asset.

The two are often mentioned together these days.

Both are insanely volatile; even more than the politicians?!?

I believe most people (including financial types and even economists?) have no idea what a currency IS?

Maybe include a definition of a currency in a future article?

“USD-denominated foreign exchange reserves”

Don’t some foreign central banks hold some actual reserves at the Fed, as opposed to US govt bonds, stocks (Swiss central bank holds some), etc etc?

1. Foreign central banks do not have access to the Fed’s reserve accounts system. And foreign exchange reserves are about central banks’ holdings, not commercial bank holdings.

2. Foreign central banks hold about $350 billion in reverse repos at the Fed that these central banks report as part of their USD holdings on their balance sheets and that are part of foreign exchange reserves.

3. Foreign commercial banks do not have access the Fed’s reserve accounts system. Only US incorporated and regulated entities, including those of foreign banks, have access to reserve accounts where they can put a portion of the cash from their US deposits. But that’s completely outside of foreign exchange reserves.

Wow! Those posts and even the comments under them are so good quality. Thanks, Wolf!

As of 2024-2025, gold’s share of global central bank reserves is around 20%, making it the second-largest reserve asset after the U.S. dollar (around 46%) and surpassing the Euro (16%). This reflects a significant increase from previous decades, driven by central bank diversification away from dollar-denominated assets due to geopolitical risks, sanctions, and inflation concerns, with major buying by countries like China, India, and Turkey.

Central banks only hold around 35,000 metric tonnes of gold and that has changed very little from the 32,000 they held 10 years ago. The Federal Reserve owns no gold, but the US Treasury is by far the largest holder of gold in the world with around 8,000 metric tonnes which they carry on the books at $42.42 per ounce.

Every time we had a financial calamity it looks like the reserve holdings dropped. It’s dropped about the same this year as it did in 08

allegedly

Actually it’s driven by the increase in the gold price.

Wolf…..I love your site and the great insight into the US economy. While others have called for a recession over the past couple years you consistently provide your view and stats describing a strong economy.,,,,,and correctly so. Bravo! I add the following comments as diversification of your views simply as a basis for others to think about.

No challenge to your view is submitted just other ideas.

No one in their right mind would run a trade deficit of over 1.2 trillion dollars or a government deficit over 2 trillion dollars…..in good times…….even the fed calls it unsustainable. How will we address these issues….no one even talks about it.

Gold is not being hyped……..very little US buying…..very little leverage. Very few people in the US own gold or silver.

The price of gold reflects the depreciation of the dollar, not only in terms of its purchasing ability but the credibility of the government which issues it. Unfortunately both are in decline.

Internationally our government recently stole 300 billion dollars from the Russians and two or three oil tankers from Venezuela. These are acts of a pirate state, not the world’s trusted arbiter. Both these actions, and others have destabilized our standing internationally among states which are neutral observers. Calls to take over Canada, Greenland etc add to the ill feeling. Yes, our bedrock allies continue to support us finanacially. The ECB etc is not buying gold. However Germany, Italy etc hold some of the largest gold reserves in the world….and they are not selling into the higher price.

I love the US. I served in our armed forces. I benefit from its economy every day. I voted for Trump. However we have a problem and to ignore it is to be very foolish.

Do I know the solution. No.

I hope AI and Quantum among others provides the solution however hopes are not a way to plan your future.

Even JP Morgan’s chief investment officer is now suggesting its clients go to an allocation of 60% equity, 20% fixed and 20% gold rather than the traditional 60/40 mix. This is not a pack of wild speculators talking….this is JP Morgan.

As the third world has emerged its citizens are buying gold. They now have a much greater ability to do so. China recently allowed its insurance companies to allocate 10% of their reserves to gold. Gold is now considered a tier one asset. Shorting gold (which used to hold the price down) has now become more difficult due to the new trading rules requiring shorts to hold a larger portion of the metal.

Bottom line……I have no idea where we are headed……but the US may need a course change that may alter the position of the dollar substantially.

I hope not….but having some insurance is prudence….not hype.

Some central banks, most are not allies of the US, are buying gold at the rate of over 1000 tons per year. Considering the world mines approximately 3500 tons per year this is serious demand. A decade ago central banks were net sellers. It takes a decade or more to open a new gold mine. The central banks that are buyers represent economies that are growing faster than the US and therefore have far greater resources than just a few years ago.

Will the dollar collapse…..highly unlikely……could the US go on to a greater level of leadership….yes…….but do things look shaky right now and look like the US may have to accept being an equal with others in a new world order that does not allow us to print dollars out the wazoo…..yes and the chance of it happening appears to be greater than the other paths. Which is a big change.

Good start far damn shore ff:

How some ever, neither gold nor silver nor anything other than bullets or shotgun shells will be worth a brass farthing IF and only IF and when the poop really hits the paddle…

And to be sure, community is the only real ”hedge” against anything short of the total collapse of law and order, and to think otherwise is to be both naive and very ignorant.

My only suggestion to anyone and everyone, including the Zucks and Bezz type folx is to get down with your neighbors and if that doesn’t work for you, GO to where the neighbors DO work for YOU and your family.

GOOD LUCK and God Bless ALL on Wolf’s Wonder, THE best place on the web to learn SO much about reality of the vast and clearly mostly unknown ”financial” world!!

Very well said. Thank you.

Merry Christmas and Happy New Years to all and especially our host. Wolf Richter.

👌👍💵💰👌👍

Gold prices don;’t reflect anything except massive mindless speculation. IF your thesis about the US were true then oil would be in the hundreds of dollars per barrel but in reality it is sunk down to around $56 and keeps heading lower.

We are now net oil exporters, plus spewing out tons of LNG. Oil shortages will not happen outside of political disasters (well, guess we could just say when), and the price of oil is awfully close to the cost of production. We also produce tons of gold, and ever more from the decades of accumulation in America’s jewelry boxes.

This is simply a discussion about how long we will stay atop the world of finance and trade. And gold is a security blanket for a lot of people, because it can always be sold for something, unlike beanie babies (bitcoin….). Now, Wolf above was talking about being young in the 80s and living through the Reagan shock therapy. It sucked, and only ended when the last big tax reform was done- and it was a whopping tax increase, and the last big social security reform was done. Now, given how stuck our political class is, the crisis will go even farther this time.

Ready? If your timeline extends to T+20 then you should be doing it now, if much shorter, Play Louis XIV, and hope your heirs can survive it. Your comfy seat totally influences your commentary. Now talk to teh youth of today- all they see is crappy jobs that don’t pay enough to afford a middle class lifestyle, and rich paying pennies on the dollar in taxes while telling them to suck it up. They will burn this place down because they have no flipping stake in your wealth or your world.

Off the soapbox to clean the carpets.

It’s weird everyone wants to talk about precious metal when wolf’s article is about USD reserve status. JPM wants to unload gold and silver before the correction happens, hence their clients should buy! Gold is cooked its at target. Silver price to Gold price ratio is nearing or the place where global institutions have sold silver. Silver is abundant in the earth, miners will mine more or industry will find alternatives to using silver if prices stayed up. If the price of oil went up people would drill more, production would rise, if silver and gold stayed up miners would produce more from the earth, we would have giant new mines the size the Kennecott Copper Mine that is viable from space. GDX miners historically haven’t been that profitable compared to other sectors in the past 50 years, I know they have doubled this year. Silver and gold are not rare in the earth, osmium, iridium, palladium, ruthenium, rhodium, tellurium, and rhenium are hard to find. Those true rare metals are what you want to invest in, wars will be fought for them. Whatever quantum chips require will be the new it material.

Tellurium; the new “old” business for my non-skiing ski town.

Day 4 of a historic strike here!

Business as UN-usual!

In a debt based fiat system, all countries will (have to) inflate their money supply some. But obviously, when that inflation gets out of hand, that country’s currency gets greatly devalued and its citizens suffer the effects of large price increases as well as myriad economic impacts.

With the US, dollars are everywhere in the world. I don’t think anyone really nows how many dollars (mostly digital) exist worldwide. Even the Eurodollar system which creates dollar denominated loans outside of the US seems opaque.

All said, the US has an exorbitant privelage of being able to print/inflate the dollar in many cases without immediate and/or direct impact to prices at home. This inflation of the currency is not captured in Federal Reserve or Treasury statistics. Much of it is very likely linked to military spending abroad (which is significant) as well as strategic commodity purchases (e.g., the Strategic Petroleum Reserve SPR).

What is the basis for this theory? The Pentagon has been unable (e.g., won’t) produce auditable financial records; a startling fact that was first uncovered and publicly announced by Donald Rumsfeld under Bush II. That revelation was quickly suppressed and while Congress “appears” to be concerned, nothing material has resulted.

The SPR periodically gets drained for various BS economic reasons (last one was Biden to lower gas prices). When the SPR is refilled and oil is bought from other countries, who would know if that electronic purchase with dollars was created out of thin air? Again, these incidents of creating digital dollars out of thin air, I believe have to be associated with military/national security items the facts of which could then be protected/suppressed by national security clearances required of those involved.

If I am correct on this conjecture, it is also likely that other major countries suspect this is also been happening. It may be one of the reasons the Saudi’s have been selling oil to China and denominated in yuan. That act alone screams rebellion in our existing petrodollar system of which the US Government could advantage itself by making some oil purchases with digital keystrokes.

You all may think these ideas are extreme and crazy. Having studied a variety of subtle economic issues over the past decade or two, it seems perfectly logical that the US would be doing this as their financial system no longer can supply the real wealth it is used to.

Real wealth comes from productivity, innovation and increases in standards of living. And while technology has been a large driver of that in recent years, I would submit that an inordinate amount of our technology in the US has been used for unproductive or zero productive uses (e.g., entertainment, recreation, BS socialization, unnecessary electronic crap in cars, etc.). The list is huge if you step back and think about it carefully.

Thanks for the opportunity to comment.

There is no such thing as the ‘petro dollar’ and never has been. All of 27 or so major commodities are denominated in US Dollars globally and that has been the case for a very long time. Oil is just one of those commodities and only amounts to around 5% of global trade transactions. Oil is now down significantly to around $56 per barrel.

What has propped up the exchange value of the U.S. dollar is the decrease in E-$s.

Times have changed. Basel III’s LCR, and Sheila Bair’s assessment fees on foreign deposits, changed the landscape of FBO regulations. It helped make E-$ borrowing more expensive, less competitive with domestic banks (the exact opposite of the original impetus that made E-$ borrowing less expensive, when E-$ banks were not subject to interest rate ceilings, reserve requirements, or FDIC insurance premiums).

All prudential reserve banking systems have heretofore “come a cropper”. The E-$ market is following that historical precedent.

Considering the transition from LIBOR to SOFR, the decline in DXY seems to have accelerated.

You have a flair, sir.

It’s a reason I’m a repeat customer.

Wolf – in fairness, this is representational of arguments in ’76. The DXY is a closed loop and means something until it doesn’t. Correct me if I’m am wrong here, the DXY is used as an assessment of dollar strength and thus implied value as based on 6 (FED? Tres?) chosen currencies. One of those currencies (Yen) has been a liquidity injector for 20 yrs and may be on the brink of pivoting.

(follow up) What other means or measures does the US employ to justify / assess the value the dollar on the world stage?

Thank you again

Whatever. But I posted the chart IN REPLY TO SPENCER’s COMMENT: “Considering the transition from LIBOR to SOFR, the decline in DXY seems to have accelerated.”

The transition to SOFR was completed in June 2023. Where is that accelerating decline of the DXY since June 2023 that spencer referred to? There isn’t.

One more unwarranted Fed cut should do it……..

Like someone asked…

“If you cut rates with unemployment under 5%, all time highs in stocks, metals, services, insurance, medical care, and near all time highs in real estate.”

When do you raise rates?

Lotta noise in this thread but back to the article –

I’m taking some of it with a grain of salt. Reserve-currency status clearly helps the U.S., and a sustained drop in reserve demand would make things harder at the margin.

Where this overreaches is in treating today’s decline like past confidence crises. Unlike the late-1970s/early-1990s period, this looks like gradual diversification and valuation effects, not a loss of trust in the Fed or U.S. institutions. Dollar holdings still remain high, Treasuries are still the deepest and most liquid market, and recent GDP growth has been solid while inflation has cooled and all parts moving in the right direction for 2026 and beyond- Thanks to POTUS 47

Bottom line: valid long-term caution, but this is portfolio rebalancing—not a dollar confidence shock at all.

“Reserve-currency status clearly helps the U.S….”

Is that true? Once you have obtained a dominant reserve currency status and your currency issuance is all over the place, isn’t there more downside than potential upside?

Maybe reserve currency status is like debt leverage, which can accelerate matters in either direction.

In late 2023, 1 dollar was equal to 1 Swiss Franc. It has lost 21 cents to the Franc since then. Would it be better to convert your USD cash reserves to CHF? Switzerland has a great GDP/dept ratio unlike the U.S. and it has consistently been known as a safe haven currency. If more wars pop off and as the political situation in the US keeps growing more volatile, the CHF will likely remain the most stable fiat.

God forbid if some burglars were to break in your house they definitely will grab ALL dollars, gold, or silver they discover but it’s possible they would view your francs as junk souvenirs and not even take them. They’re not exactly what the average burglar is seeking, thus making them safer than USD in that scenario as well.

Exchange rates on currency pairs on FOREX all swing wildly and it is a vast speculative market with over $8 trillion in transactions daily. The US dollar is now rapidly increasing in value against many other pairings.

May be increasing short term against some but my point here shouldn’t be overlooked: From 1956-2024, the Swiss franc lost about 78.4% of its purchasing power, while the U.S. dollar lost about 91.6%. CHF has proven over 75yrs that it fights inflation better than USD. If physically holding fiat is something that someone chooses to do with a portion of their net worth, CHF is the best currency to hold. And being that it has a 1000 denomination it takes less space to store as well.

The Swiss National Bank has an $855 bn balance sheet. It owns $167bn of US equities, with over $42bn in 5 companies. (Source: swissinfo .ch).

I could just as easily hold the same 5 tech companies… I am sure I already do in my 401k.

DJT pushing for rates equal to or UNDER inflation rates will further push the dollar out of the reserve currency spot

then what of inflation?

A President pushing rates around is a bad look

“A President pushing rates around is a bad look”

Look at the dates of QE and QT efforts.

It has been political for decades, largess has been used as a carrot and a stick. Currently, it is print the money or face large scale unrest (bang bang). Miran was express in Mar a Logo – they intend to devalue the Dollar.

The ‘problem’ is the value of the Dollar has been destroyed, and the Dollar is the WRC.

While we’re on the subject – one of core arguments against the Dollar is the free ride. The US is only responsible for @ 12% of world Trade in Dollars and yet it is @ 88% responsible for FX transaction volume. (International Banker 1.2.24).

Thanks Wolf. This, admittedly, may be a dumb question, but could US citizens/institutions replace foreign demand to keep US borrowing costs low? I realize they could likely get higher yield elsewhere, but US citizens also benefit from government spending (if spent wisely at least).

That’s kind of what has been happening. Foreigners have increased their holdings but much more slowly than the new supply coming on the market, and the difference was picked up by American investors. This has been going on for a few years. Over the past three years, the Fed has unloaded $1.6 trillion in Treasuries that American investors also picked up.

if you’re not that savvy w.r.t global assets, reserves, etc… how

sensible is it … or not… to buy something like

DODLX (Dodge and Cox Global Bond fund) or

LCORX (Leuthold Core Investment) ? Both are mutual funds,

Dodge and Cox has been around a long time, for what that’s

worth.

How knowledgeable do you think the fund managers are

compared to individual investors such as those found at

this site ?

Why is the Chinese currency at only 2%? Why isn’t it almost equal to the USD as a reserve currency in the 21st century?

Couldn’t China simply demand that anyone who buys from them (the entire world) use RMB? (Making it a de facto major currency?)

I mentioned some of the reasons in the article:

“…amid ongoing capital controls, convertibility issues, and a slew of other issues.”