The beginning of the 4th year of demand destruction in the resale market after the price explosion from mid-2020 to mid-2022.

By Wolf Richter for WOLF STREET.

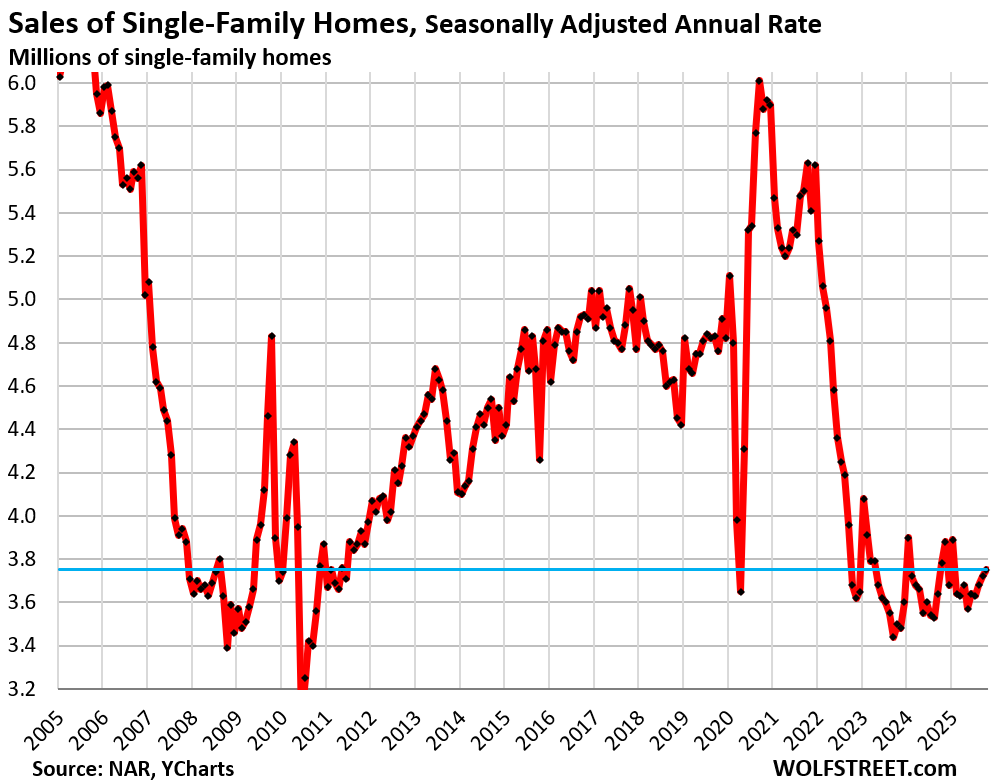

Sales of single-family homes that closed in November rose seasonally adjusted by 0.8% from October, but were down year-over-year by 0.8%, and by 22% from November 2019. At an annual rate of 3.75 million, sales were at Housing Bust levels.

Welcome to the beginning of the fourth year in a row that sales of existing single-family homes have wobbled along crushed levels (historical data from YCharts):

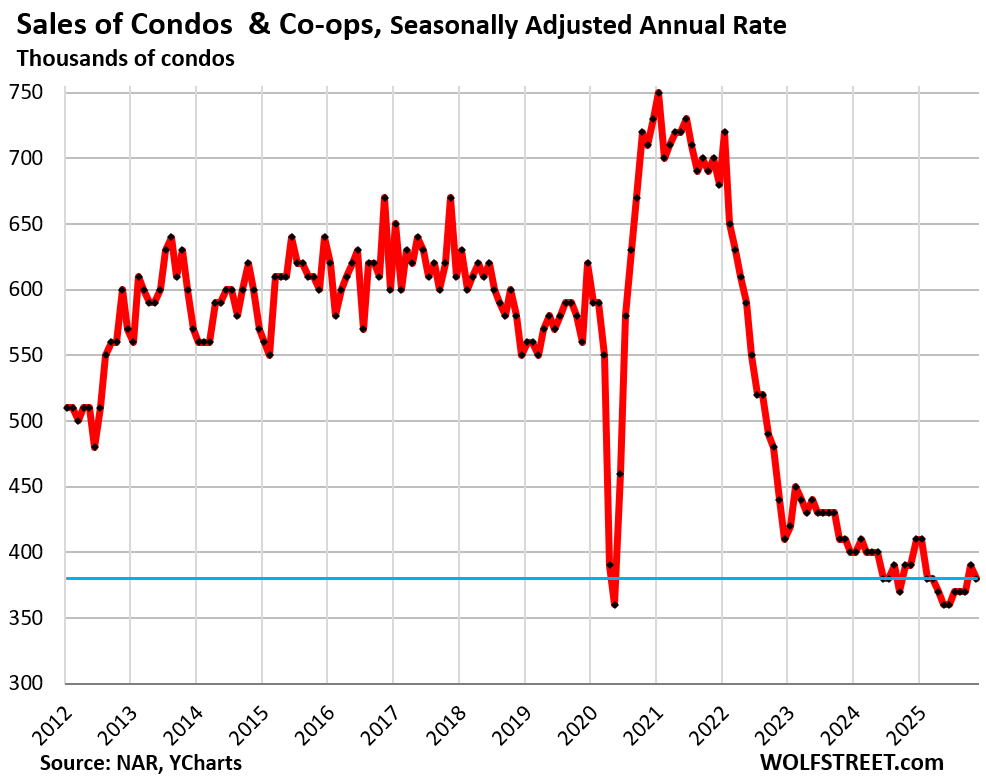

Sales of condos and co-ops fell seasonally adjusted, both, month-to-month (-2.6%) and year-over-year (-2.6%), to an annual rate of 380,000, according to the National Association of Realtors today.

Compared to November 2019, condo sales were down by 32%. NAR’s data on condos goes back only to October 2011, and within that time frame, sales have been wobbling along record lows for over three years (historical data from YCharts).

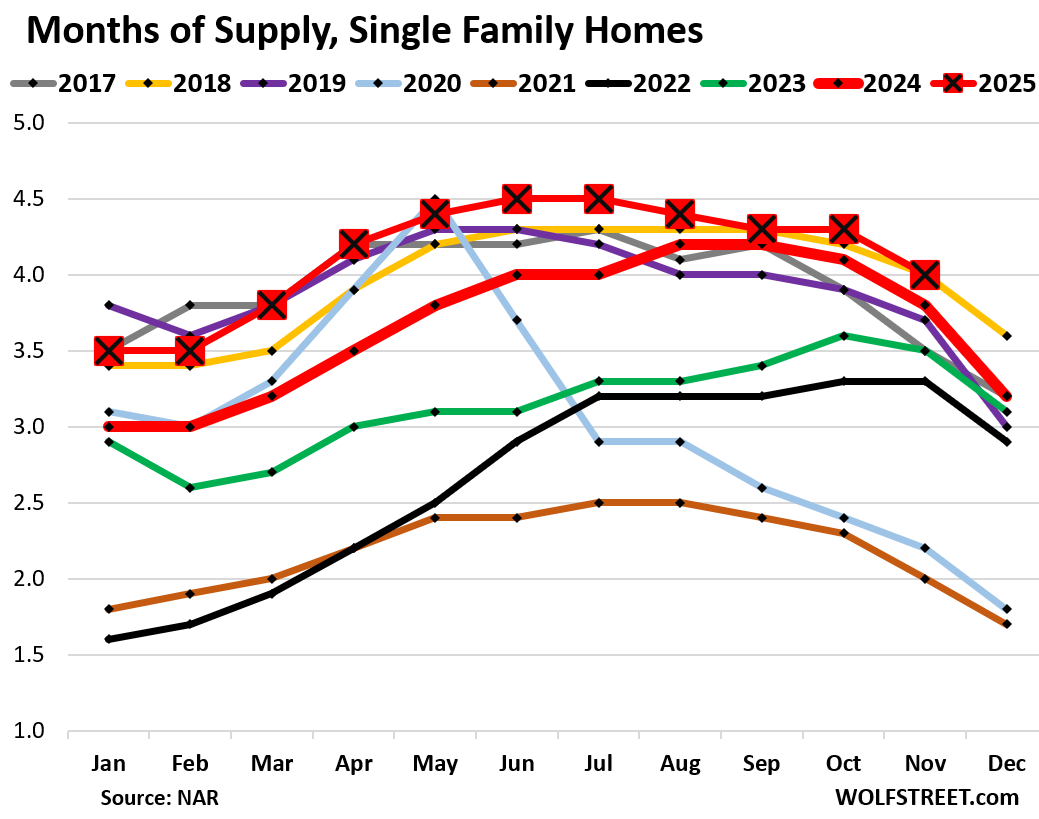

Most supply in years.

Supply of single-family homes dipped along seasonal patterns to 4.0 months (red line with big squares in the chart below), the highest for any November since 2018 (also 4.0 months, yellow line). Back in November 2018, mortgage rates had surged to 5% and were starting to shake up the housing market.

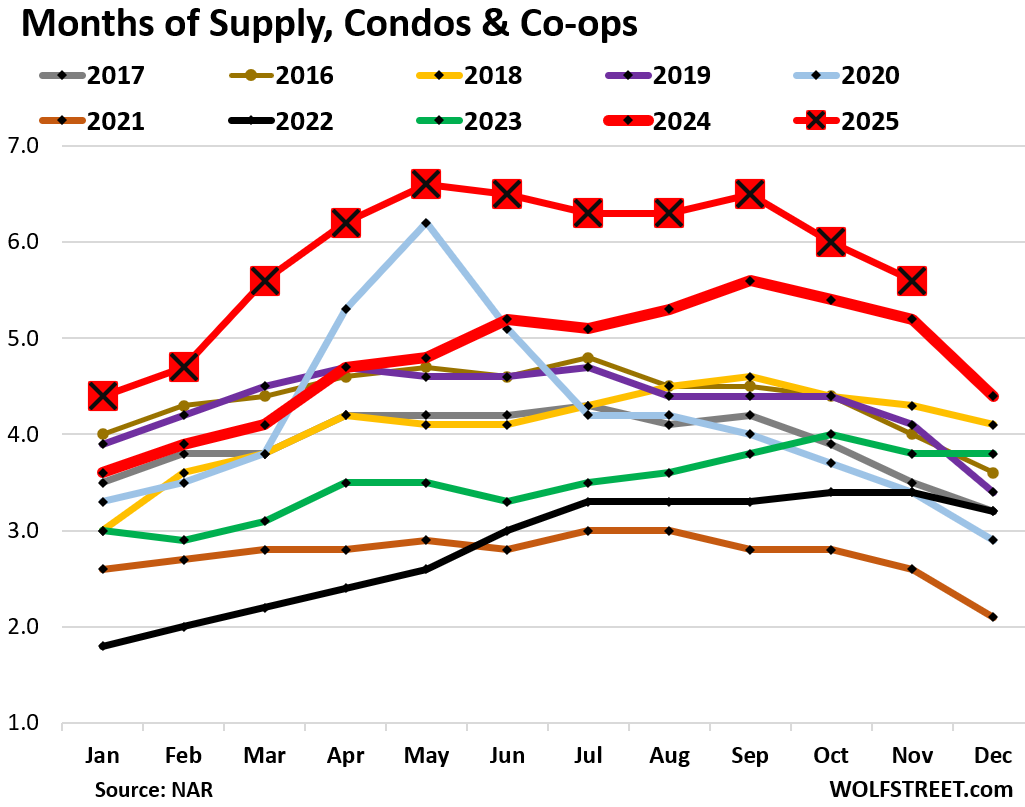

Supply of condos declined seasonally to 5.6 months, the highest for any November since November 2011 during the Housing Bust. Compared to November 2019, supply was up by 37%.

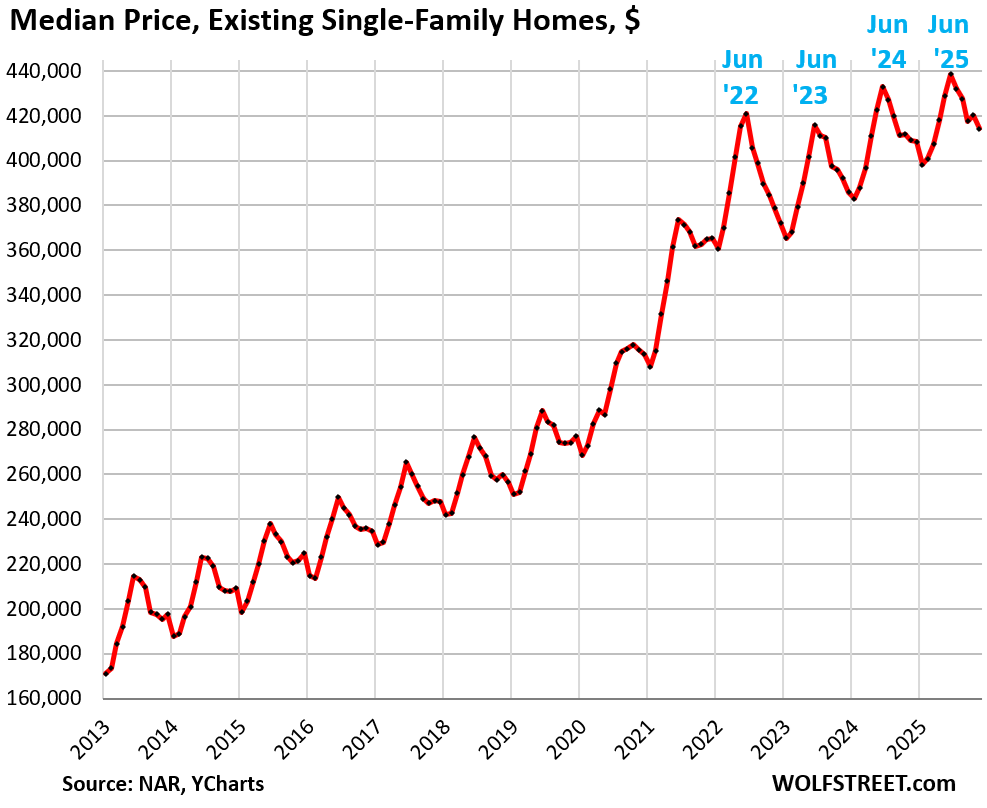

The national median price of single-family homes fell by 1.4% in November from October along seasonal patterns, to $414,300, reducing the year-over-year gain to 1.2%.

This national median price of single-family homes had exploded by 47% from June 2020 through June 2025, most of it during the two years of mid-2020 to mid-2022.

June marks the seasonal high each year. January or February marks the seasonal low each year. The index is not seasonally adjusted. The seasonal zigzag is a result of shifts in the mix of what is on the market and sells, which shifts the median price up or down.

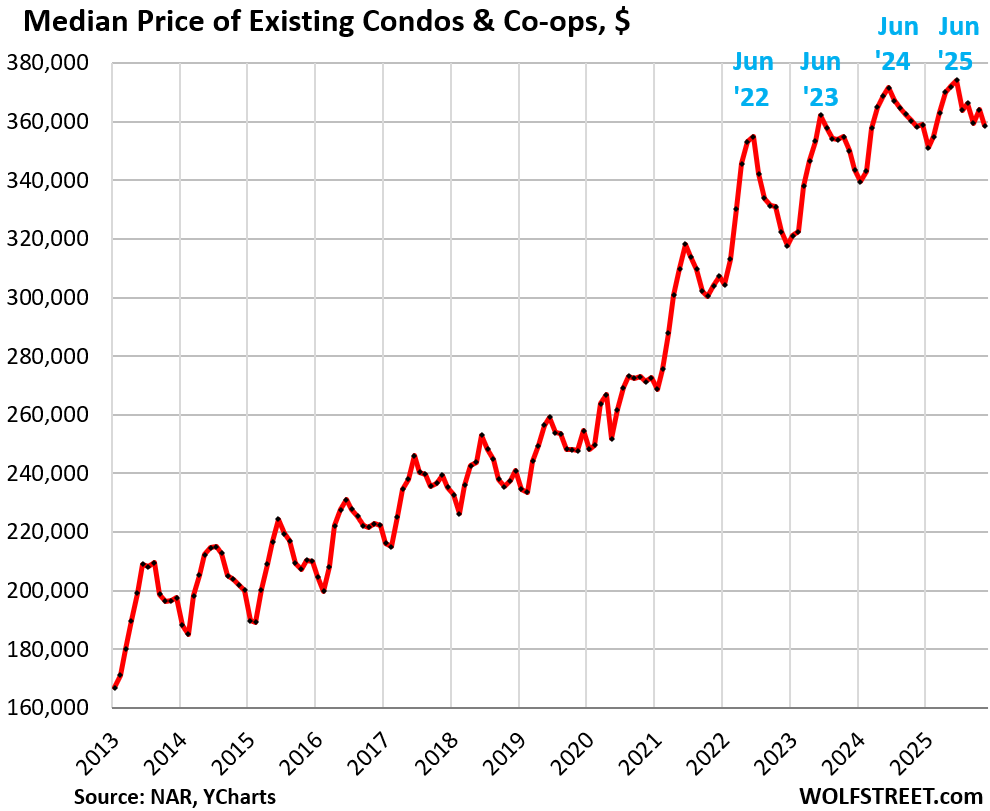

The national median price of condos and co-ops dropped 1.5% in November from October, and by 1.5% year-over-year, to $358,600.

This national median price of condos and co-ops had exploded by 43% from mid-2020 through mid-2025, most of it during the two years of mid-2020 to mid-2022.

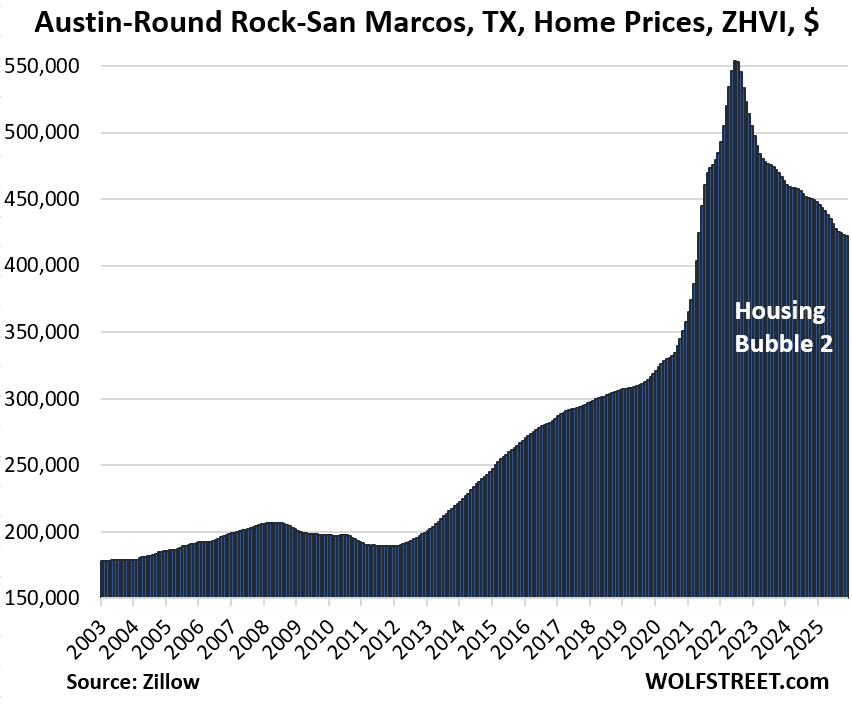

But price dynamics differ in individual markets.

The national median price is meaningless for specific markets. In some markets, home prices have fallen substantially, including by 24% in the Austin-Round Rock-San Marcos metro, the biggest drop in our lineup of 33 large and expensive housing markets. The drop so far has backed out only about half of the 74% price explosion from January 2020 through June 2022:

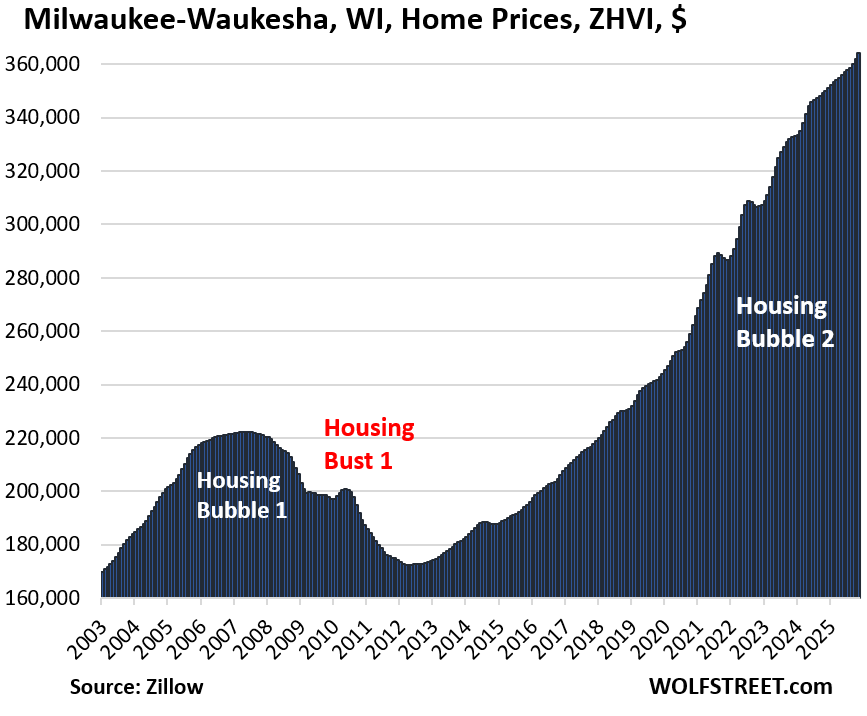

Conversely, the Milwaukee-Waukesha metro is the market with the biggest year-over-year gain (+4.1%) in our lineup of 33 large and expensive housing markets:

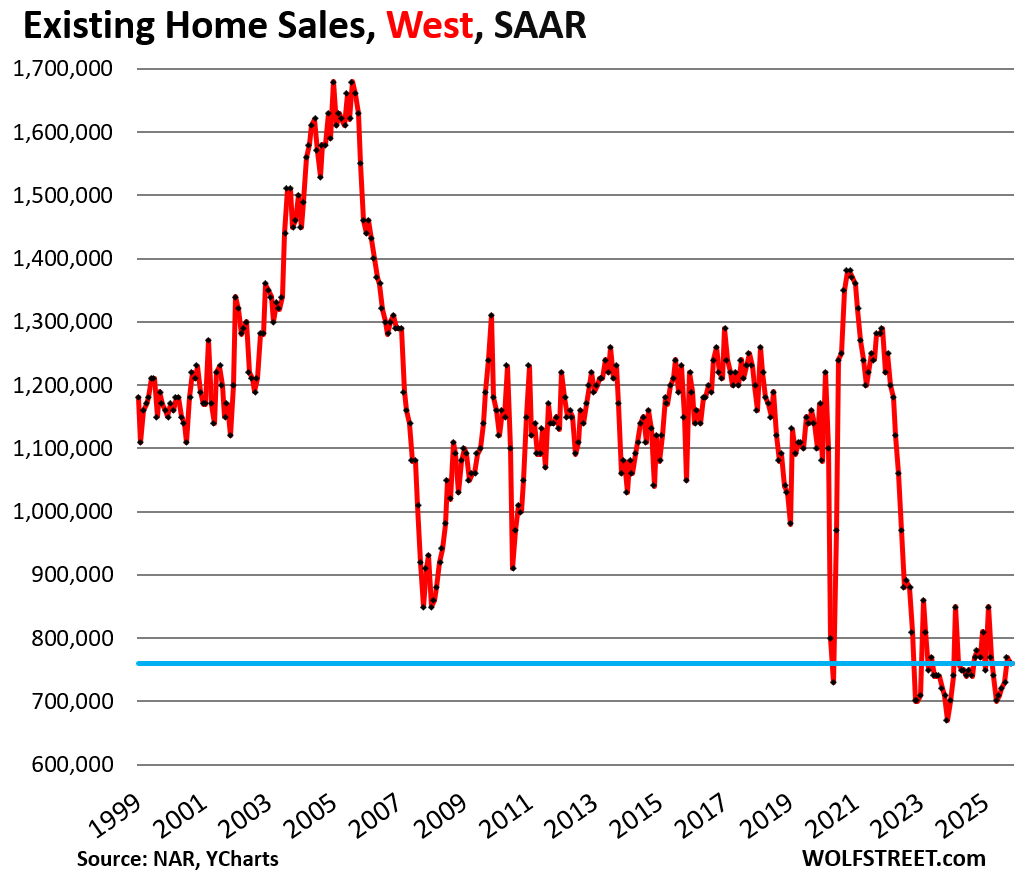

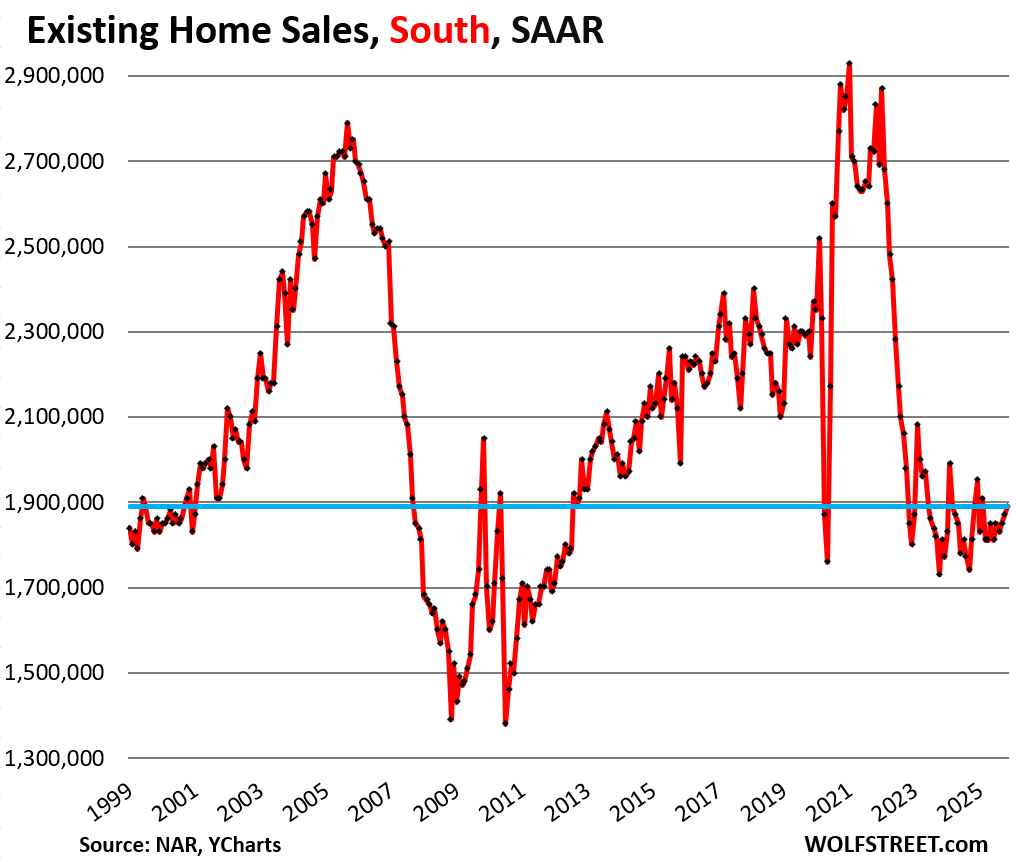

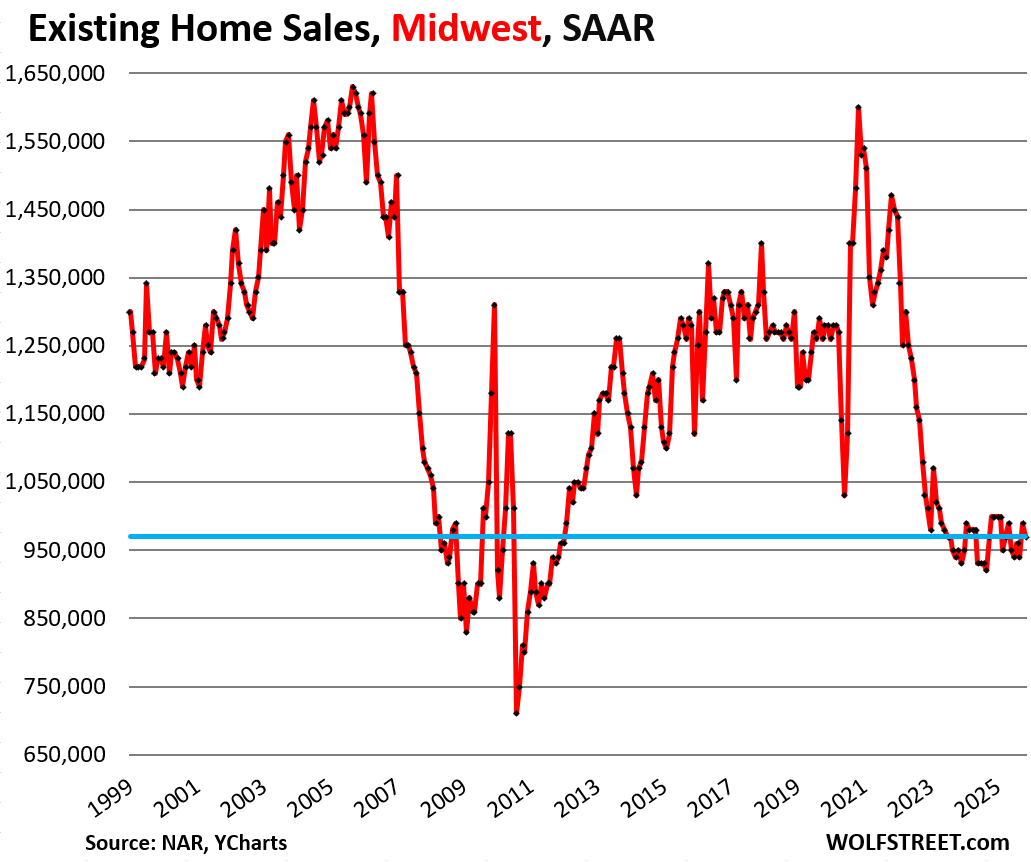

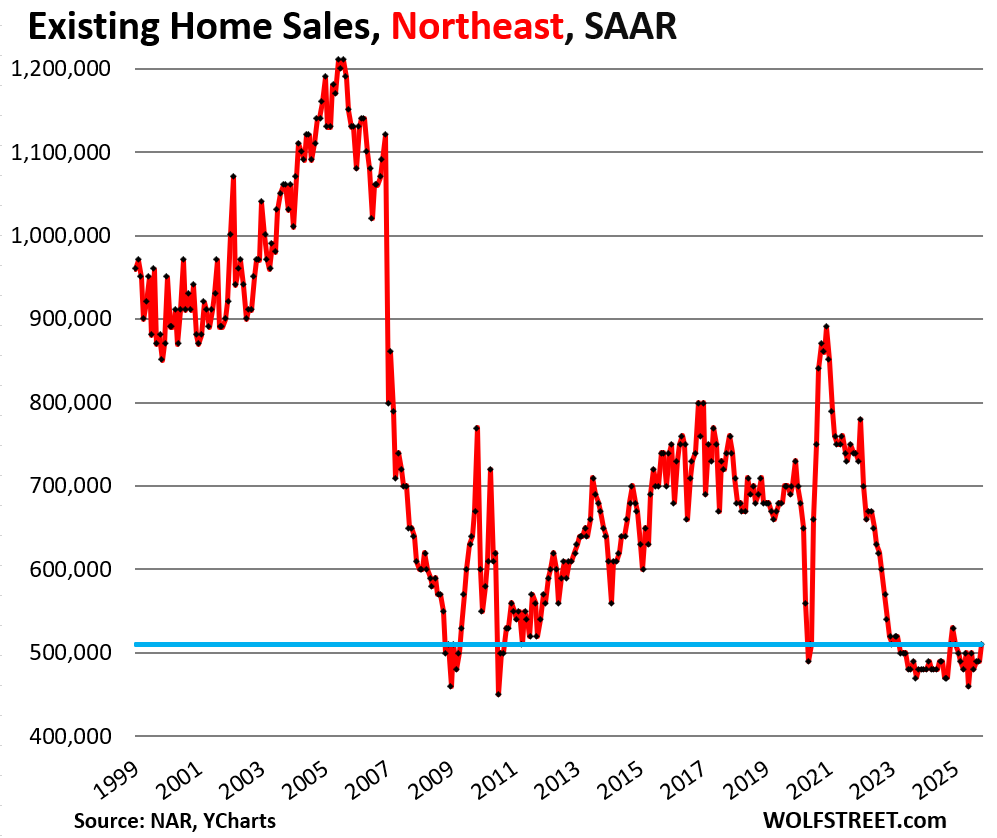

Demand destruction by region.

The charts below show the seasonally adjusted annual rate of sales (SAAR) in the four Census Regions of the US. A map of the four regions is at the top of the comments below.

In the West, the seasonally adjusted annual rate of sales remained at 760,000 homes in November compared to the prior month, and was down by 1.3% year-over-year, by 31% from November 2019, and by 27% from November 2018.

In the South, the seasonally adjusted annual rate of sales rose from the prior month to 1.89 million in November, but was unchanged from a year ago, and down by 16% from 2019 and by 13% from 2018.

In the Midwest, the seasonally adjusted annual rate of sales fell from the prior month to 970,000 in November, down by 3.0% year-over-year, by 24% from 2019, and by 23% from 2018:

In the Northeast, the seasonally adjusted annual rate of sales rose from the prior month to 510,000 homes in November, unchanged from a year ago, and down by 27% from 2019 and by 28% from 2018.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Here is a map of the four Census regions of the US:

Great article like so much of what Wolf publishes. In a world of mostly self dealing when it comes to financial “experts” and “analists”, Wolf seems to actually provide an insight based on an unbiased observation of the facts.

I agree that Wolf’s analysis is a standard by which I am able to judge my own reaction against.

Of course, I am a proponent of the hypothesis that what they’re frantically selling, is the basic decency of the American people. The place that I grew up and live in.

I’m so provincial that I think the basis of the argument has something to do with the general welfare which increasingly is becoming less defined as the courts waffle from the operating doctrine.

Why are prices still going up in some markets

Some markets are still relatively cheap. Prices there surged too, but from low levels and are still low compared to high-priced areas. I keep thinking about my former hometown Tulsa, which had been through three decades of a housing depression. Obviously, incomes are a lot lower too in those areas, with far fewer opportunities. Cities like Tulsa were so desperate that they paid working-from-home people to move there if they brought their jobs with them (with some success). But it seems from some sporadic reporting that not everyone who made that move is particularly happy with it. It goes something like this: “Sure, housing costs a lot less than in San Diego, but…”

Wisconsin’s economy is supposedly still in expansion. I guess that coupled with relatively low unemployment has allowed it to continue….for now. That said, I sure as hell am not buying. 😉

Well Wisconsin is a fell weather state whose employment profile pre-swaged the ensuing state of the manufacturing economy of yor.

Before the USG helped certain corporations export our manufacturing base to China.

A classic, economic Shakespeare plot that lays bare the motive.

If only we lived in a free market-based economy the shrew and patient among us could benefit from what in a rational and non-manipulated market would be a good opportunity in a few years or so.

But since we live in a world in which all asset charts must always go up by any means necessary (see Wolf’s last article) we will see manipulations and schemes* to keep this economic flaming box of turds barreling down the road.

The result?

Inflation out the wazoo!!!

* free government downpayment assistance, FFR bullied down to 1% (or lower), stimulus checks, 50 year mortgages, etc.

Just plug your nose and buy Palantir at 150x revenue.

Their CEO actually said in a news article once that their stock price is just street cred.

Like it has zero correlation to their company.

Which is kind of funny

In Lynch’s day it was research good products your family and co workers are buying.

Now it’s buy stocks cuz someone on the net told you to.

“If only we lived in a free market-based economy the shrew and patient among us could benefit from what in a rational and non-manipulated market would be a good opportunity in a few years or so.”

I would point out that the entire concept that you site in your words about the market only applies to the wealthiest contingent.

Most Americans live the reality of a beneficial capitalism put in place in the 1930 through 1960 time period

The cost of living, the affordability quotient, the normalization of violence.

The housing market in lock down is the end result of the Government and Federal Reserve policy manipulating the natural interest rates and money markets

Interest rates on nearly everything is set by the US Treasury markets which are the largest free capital markets in the world. What they set in market auctions are the ‘natural interest rates.’

SoCal,

“Interest rates on nearly everything is set by the US Treasury markets which are the largest free capital markets in the world.”

On the off chance you aren’t joking…

What exactly do you think QE and ZIRP *were* if not “direct action” by the G,

1) To artificially lower interest rates,

2) By printing incrementally unbacked “money”

3) Used to then buy new issue Treasury bonds (grossly facilitating the deficits/debt)

4) At ultra low interest rates no remotely rational private actor would ever accept for an already hugely indebted nation (circa 2011)

5) With an eye towards artificially inflating asset values (via semi-informed utilization of traditional DCF and NPV calculations)

6) To create a (ultimately, phantom) wealth effect,

7) To try and resuscitate the cratering/moribund US economy, without…

8) Doing any, you know, actual frigging fundamental reform in the US.

Want to go on about the splendor of the “pure” US Treasury markets?

9) QE and ZIRP live on in those “ample reserves” (in the trillions) at the Fed that the US economy/banking system apparently can no longer survive without.

10) Compare the Fed balance sheet (read, cumulative US debt monetized) in 2025 with that of 2002.

But is it. I happen too suspect that the entire rate curve, especially the long term is artificially depressed by the obese Fed yield curve structure.

There are two charts of SF Wolf, where one was supposed to be condos and coops.

Yes, thanks!

Just kick the television hard. This stuff tends to right itself eventually. And now, another episode of Keeping up with the CarCrashians.

Keep up with the times!

The new thing is VanderDump Rules

I think the election pretty much showed Duck Dynasty has made a strong comeback in the Reality TV World.

Your very first phrase – “Single-Family Home Prices Barely up YoY” is all we need to know that there is MASSIVE manipulation going on.

Home prices should be falling like a rock, instead we have price levitation that would make a master magician jealous.

(And yes, I do read many of your articles. I’m aware that prices are falling by minor amounts in some areas).

We are at the apex of the biggest asset price bubble in the history of mankind. The idea that house prices will crash when there is this much money sloshing around is laughable.

Well, for the record I agree with both of your assertions that the Fed money sloshing around will provide a subsidized liquidity to the so called market, the asset holders,

designed to prevent a decline in asset prices.

The MASSIVE manipulation is homeowners attempting to maximize the income they receive from the sale of their home.

Don’t forget about all the cities & towns reinforcing these insane bubble prices via increasing assessments.

All that those assessments are is an attempt to match current margins of housing purchases using comparables.

I like to think of as legalized larceny. The price of housing doubled because of QE and that price increase was not considered inflation.

I have several times proffered my hypothesis that asset price increases are the native cause of inflation.

We define inflation as a derivative of the price increase while at the same time we define deflation as a price collapse.

Economics is a political science without the benefit of a universal speed of light metric

The first chart that shows volume of sales, show we are at “bust levels” for 3 years now.

But the same chart show that in the Great Recession, after 3 years of low volume of sales, that the volume rebounded.

Based on the Great Recession, volume of sales should be rebounding soon. If consumers start to fear inflation, that could be a big motivator to jump in a buy sooner, rather than later.

IMHO, the USD dilution from the coming Debt Crisis (which will result in devaluation of the USD by at least 90%, of not 999%, will result in huge prices increases in everything.

Homeowners with below 4% mortgages are doing everything they can to not have to sell their home, so they won’t have to buy another one with a 6-7% mortgage. This keeps them off the market, both as sellers and as buyers, and they have been very slow to return to the market (“lock-in effect”), which is one of the reasons why demand/sales are so low. I document the progress of them returning to the market here quarterly:

https://wolfstreet.com/2025/09/29/the-lock-in-effect-and-mortgage-rates-update-on-unwinding-a-phenomenon-that-wrecked-the-housing-market/

Now they are talking about “portable” mortgages where these lucky beneficiaries of the FED’s FU*KERY can buy a new house and transfer the old low-rate mortgage to the new house, but the young person who buys their old house has to pay the current high rate – you know, just another screw job to the young. Kind of like Prop 13 where olds have low taxes but the young families bear the high tax burden. Burn it all down. It’s fu*king broken.

They cannot make old mortgages portable because of the collateral issues and the fact that these mortgages are in MBS, and the contracts cannot be changed. They’re talking about creating new types of mortgages that will be portable. I posted an article with a discussion about this here:

https://wolfstreet.com/2025/12/10/ceo-of-ice-on-making-mortgages-portable-assumable-in-the-era-of-mbs-and-on-ai-at-ice-and-its-impact-on-hiring/

Thank God, Wolf. It seems that every single program and idea benefits the already benefited. I am getting PTSD from it.

The notion of portability of mortgages is utter nonsense as any long term loans need to relate most to the credit worthiness of the current buyers which changes whenever houses are sold.

Focus on the mountain rather than the shiny object. The problem caused by the over priced housing market does not lie in the travails of a tiny sliver when compared to the deluge of potential transactions that are infeasible because the asset price has become excessively high.

Yeah, prices came down much more in 3 years during the housing bust than in the most recent episode. As many people have said, this is most likely going to be resolved by 7-10 years of slight price decreases than by 3 years of steep ones.

Agreed. It should have deflated by now, but our govt propped up the stock market and economy to avoid the recession that would have caused the correction. It’s not crashing with a stock market at all time highs and ultra low unemployment.

I’ve now heard multiple well educated people in their early 30s say things like the tech bubble is a joke, the govt would never let the stock market crash. In business school one professor would say the telltale sign of a bubble is retail investors thinking they’re experts – I’ve met so many people in their early 30s who are all real estate investors, day traders, or the worst crypto investors. They’re all saying the same things and getting rich though…. the amount of risk and leverage they’re taking on is phenomenal, but it’s seems to be working, maybe they’re right, maybe this time is different

No. It’s not different this time at all. PE multiples for stocks matter now as much as they did heading into 1929.

40% of the companies in Russel 2000 are losing money, that is an all time high. Case Shiller CAPE is the second highest ever!, are they telling the truth with earnings? The yen crashed over 1% yesterday and that gave the algo some buying power on the largest quad witching day ever with 7.1 Trillion of notional value trading. With that much money at stake maybe they can move the yen market for 1 day. The big yen move was head scratcher IMO after BOJ raised rates, Rubber bands get stretched than they snap back. I am not sure if the trading algorithm knew the inflation number was bogus, its program to react to input hence the 10 year was bought and gave an assist for equity rally. Smart money knows, retail not so smart in the long run.

“If consumers start to fear inflation, that could be a big motivator to jump in a buy sooner, rather than later.”

That’s funny. How can buyers jump in when they can’t afford the house? As Wolf notes, on a national basis, home prices rose 1.2% YoY. Affordability remains out of reach for the majority of people wanting to buy who are below 55 years old.

A 1.2% increase of single family home prices in the face of 2.8% or whatever annual inflation means housing price got cheaper and a 1.5% decrease in condo prices added to 2.8% inflation is a 4.3% net loss. It like Earnest Hemingway said when he fictionally ask how you got poor, and then answers: “Slowly, at first; and then all at once.”

I live in the Northeast; and looking at the sales volume in the 1999-2005 years compared to now is incredible to see. Hard to believe there was that much volume of sales at one point.

Not sure too what you are attesting. Unless what your saying is that our young people are so hopeless that they are spending money because the rationality of saving becomes negative

luckily they’re vigorous and horny

The Federal Reserve didn’t “make a mistake” — it detonated a housing bomb. Near-zero interest rates were not some noble emergency tool; they were an open invitation to speculation, leverage, and greed. Anyone with a freshman-level understanding of economics knew that 2% money would blow a massive asset bubble. They did it anyway.

Then they poured gasoline on it by letting hedge funds and private equity storm the single-family housing market — crowding out real families with cheap institutional capital. That never should have been allowed. Single-family homes are not trading desks, and houses are not derivatives.

The result? Prices disconnected from reality, buyers panicking during COVID, and people overpaying for homes that weeks earlier couldn’t meet asking price. The Fed claims it couldn’t see this coming. That’s nonsense. This was the inevitable outcome of reckless policy and moral hazard.

Now, after inflating the bubble, they slam rates higher and pretend they’re firefighters instead of the arsonists. Regular people are left holding the bag while Wall Street walks away with the gains. That’s not bad luck. That’s policy failure — and accountability has been nowhere to be found.

“That never should have been allowed.”

What’s your solution? Regulate real estate market so that families aren’t allowed to accept free-market bids from corporations?

How would you convince Americans they should be forced to discount the biggest asset they own?

“How would you convince Americans they should be forced to discount the biggest asset they own?”

Personally I don’t need any convincing that my house should be worth wayyyyy less than its current assessed value – I agree 100%.

My city’s assessing department is the one you need to convince.

No, the basic problem is the Fed – meaning the very existence of that institution. Give the government a weapon which enables it to reward its donors and supporters, and the government will use that weapon in its own self interest every single time. If you really want a free market with less regulation, let’s start by eliminating the Fed. Will we experience pain through asset booms and busts – sure we will – but the alternative, crony capitalism system which is enabled by the unholy combination of Fed/Gov has got to go.

What should be regulated is the amount of OTHER PEOPLE’S MONEY that can be loaned against an asset such as a house. If any party wants to buy a $10,000 house for $1,000,000,000,000 then that should not be regulated at all.

One solution is to end depreciation for rental properties. It is an absurd notion that one can depreciate an appreciating property and then only have to recapture 20% when sold. That one change would, I imagine, create a substantial shift of home ownership from rental to primary residence.

The fact of the matter is that all real estate depreciates.

Yes, buildings do, and eventually are torn down. But the land normally does not — unless it was a former nuclear waste dump. In tax and other accounting, you only depreciate the value of the building. You don’t get to depreciate the value of the land.

We don’t have Ayn Rand’s laissez faire capitalism. We necessarily have regulated capitalism.

The “administered” prices (oligopoly, monopsony, and monopoly elements) would not be the “asked” prices, were they not “validated” by M*Vt (money Xs velocity), i.e., “validated” by the world’s Central Banks

Imagine managing your investments in a command economy.

It could be done at the local level by taxing second homes and rental homes through the roof. Many states don’t tax second homes higher. Every chamber of commerce and real estate lobby blocks every attempt to make those investors pay more. Sales tax on airbnb, the destroyer of desirable towns, could also be increased.

In Utah, rental landlords get a property tax exemption that is the same as owner occupants–it’s called “primary occupancy” to obfuscate. And they get to depreciate everything. What’s not to love?

I’m not saying most renters make great homeowners, but the prices would come down if higher property taxes cut into profits.

Seniors get special property tax exemptions in many states, in some regardless of income. How is that fair to the young?

Of course the top 5-10% don’t care about property taxes as much, but the airbnb speculators and older potential downsizers do. Corporations with narrower profits due to overhead would.

As an old guy 69 years old the Texas increase of prop tax deduction for those over 65 are a slight increase in the homestead exemption and then a freeze on the assessed value from 65 forward.

Since I’m not working and my fixed income does not keep up with inflation rapid increases in homes can cause seniors to become priced out of their homes if the prop tax freeze was not in place.

This freeze has other consequences since my 35 year old used home would sell for much less per sq ft making a downsizing move difficult since a new home would not benefit me from a prop tax freeze . I’m basically prop tax frozen from selling.

Exactly. Not being able to see this coming is like firing a gun in celebration into a crowd and being shocked, just SHOCKED, that an innocent bystander was hit.

Right besides the very obvious lessons from any basic monetary policy class (part of any bachelor of economics curriculum). This was all over the news. Things that could have been done:

1. Raise interest rates to 1-2% early instead of holding them at zero. The economy did not need zero percent rates. The govt gave COVID loans and payroll loans and froze mortgages

2. Ban foreign ownership of US homes if there’s actually a shortage

3. Ban Airbnb’ing homes that are not a primary residence, i.e. if something is zoned residential, it should not be used as a commercial hotel

The truth is they’re stupid or they wanted this outcome. I’m not sure which is worse. They screwed a whole generation and created massive wealth inequality.

Clearly the government was incapable of handling a perceived pandemic followed by work from home from private sector and low rate mtgs artificially suppressed by FRB an experimental cure for an unknown illness with dire consequences.

Followed that by a disruption in energy to the EU and the world with Russia and Ukraine . The world experienced inflation not just USA and USA industry margins skyrocketed which is their job to charge as much as the world will pay . I don’t want more regulations but less.

I don’t want the government to restrict sales to foreign investment rather I want the opposite. STR can be a big boost to the travel experience and have been in existence for as long as homes have been . No room at the inn no problem bed down in my manger. Internet concept of STR just made the process easier . Yes taxation and city zoning can take care of occupation and parking 🅿️ but don’t restrict access to sales to STR.

What is the motivation for posting AI generated comments on a free finance blog?

Giveaways:

– the emdashes

– the following sentence structure: “the topic wasn’t this….its that.” For example where it says “that’s not bad luck — it’s policy failure.”

It also does that on the first paragraph.

Standard AI hallmarks from beginning to end.

Why?

The markets would have crashed, you’d been dirt poor.

And still complaining about it!

Lol

While I agree with much of your analysis of the historical fraud imposed. Mostly I mourn the loss of the precious innocence that allows validation that …….

Forgot to ad- END THE FED. If a central bank must exist at all, it should be limited to true emergencies — yet it usually creates the emergency. Artificially low rates aren’t stabilization; they’re market manipulation.

A free market would produce a real interest rate based on actual savings, risk, and time — not a committee guessing with broken models

Lol. Part of the reason major crises and crashes happen about every 80 years is that we eventually forget why we put in place certain fixes, and what happens when they go away.

I’m not eager to return to a world with financial panics every decade (as was the case in the 1860-1910 period).

There is NEVER any single interest rate in any economy, and the array of rates are based on DURATION and RISK and are established by the largest bond market in the world in the US, namely the US Treasuries market which is the epitome of free markets.

The FED is run by the bankers it serves. The Lobbyists virtually control the House Committee on Financial Services & the U.S. Senate Committee on Banking, Housing, and Urban Affairs.

While your argument is hypothetical, the enactment of the QE policy on its own is sufficient evidence that the Fed has an alternative agenda contrary to the concept of the public good.

A concept my dad who was shot in the face by a German sniper while driving a tank destroyer, union representative, and an all around good guy with a heart bigger than himself.

In the US about 40% of the population live in towns with less than 50K people and about 27% in rural areas with less than 5K. The rest live in large and small cities. In Italy and in Germany the situation is about the same. In France, Austria, Croatia, eastern Europe and Russia more people live in small towns and in rural areas. The situation is inversed in China, India and a few cities in South east Asia.

Existing Home Sales Bubble #2 existed in the south and the midwest. Both deflated. There was no Bubble #2 in the northeast and the west. Both decayed.

If a wolf man wants to sell his house (or den) for $2 Million, should ‘The Great Housing Authority’ be able to tell him his house is only worth $300k?

Then why should ‘The Great Money Authority “‘ control interest rates? It’s the price banks ‘sell’ money or credit. Why should THEY decide? It also affects how much interest you make on your savings.

Juat for the record – I think most homes in San Fran should sell in the $300K range. But that’s just me. Maybe I’ll put my application in for ‘The Great Housing Authority’. 🥸. 🏠

The Federal Reserve is a result of the fact that banks want to lend against assets, which drive up asset prices. As those asset prices increase, banks gain confidence and reduce interest rates, spiking speculative behavior, which increase prices further. Eventually prices jump far higher than is sustainable and the asset prices collapse, causing the banks to collapse, causing interest rates to soar, causing the economy to collapse, causing millions of innocent people to lose their livelihoods, causing socialism.

By manipulating rates lower during a banking panic, the Federal Reserve can help stabilize the banking system and minimize the negative economic impact on the population. How it goes about that effort, and for how long, is the key question.

Yes, but when you do this, you need to withdraw the stimulus after it’s stable.

That’s the part that they failed miserably at in 2021 and early 2022.

Any and all banks lend against assets as collateral for all securitized loans and charge very high interest rates of 25% to 35% on loans that are not securitized such as credit cards. Those principles have nothing whatsoever to do with the Federal Reserve and are universal principles of money lending and banking that go back thousands of years,

What causes prices to go up on assets is manic speculation by bidders not justified by the returns (if any) on those assets. Some commodities such as metals simply have no return whatsoever other than capital appreciation as they have no earnings power.

Credit card interest rates now are higher than 1980s In the 80s when the 10 year UST bonds yielded 16% credit cards % rates peaked at 18%. Wolf how did this happen? why is no one talking about this spread?

1. Most states got rid of their usury laws that applied to credit cards (many capped rates at 18%)

2. Most people don’t use credit cards to borrow – they use them as payment method and pay them off every month and never pay interest. High interest rates discourage borrowing. The total interest-bearing credit card debt outstanding is small… something like $600 billion, out of $18 TRILLION in total consumer debt. The credit card balances that are reported monthly and quarterly are statement balances before the charges are paid off.

Essentially I agree with what I think you are saying is that the relevant statistic is affordability which translates roughly into the tension between income versus expenses.

The one thing I am curious about is this last summer while traveling through one of Colorados mountain towns I met an executive from a real estate development company and I met a land speculator – the guy who does the demographic research to tell developers where to build. The developer told me that housing was like turning a tanker ship, that once it gets headed in a certain direction it’s hard to stop, but the turning is slow. He said if you can hold on until next summer there will be a lot on sale. He said probably 5-7% declines for Denver with no economic weakness, more if unemployment rises and the stock market drops. Larger % decreases in the mountain towns with the exception of Eagle/Vail/Beaver Creek because of the direct flights from the east coast. The land speculator separately said they’re not recommending anywhere in Colorado for development in the next 5 years and also that the demographics indicate 0 to slightly negative price appreciation over the next 5 years.

I hope they’re right.

What I will say is like any market, things are worth what people are willing to pay for them and the realtors are very good at scaring people with buy now before it doubles again propaganda so this could get propped up forever. I mean look at Bitcoin, logic and fundamentals are no longer what drives markets

Based on my research, NAR’s definition aligns with the Census Bureau, considering some attached homes like townhouses as single-family if they have ground-to-roof walls and their own entrance, but they often appear in specific “condo/co-op” categories in detailed breakdowns.

Townhomes in the Florida panhandle have dropped around 20% from all time high prices set in 2022, such as in my HOA they are selling for $260,000 and were selling for $325,000 in spring 2022.

On the east end of Panama City Beach, the rents are around 2021 levels for a 3 bedroom, 2.5 bath, +1 car garage townhome units.

My townhome HOA in Panama City Beach has lowered the HOA regular assessment by about 8% from 2025 to 2026, and the regular assessment has increased about 5% since 2013 with no special assessment.

The HOA decided to take a +$500,000 loan instead of issue a special assessment for Hurricane Michael repairs (i.e., insurance deductible to replace roofs, clear damage trees, etc) and for delayed projects like a new sidewalk for an entrance so the school age kids can use to walk to bus stop.

I wonder how falling prices will affect municipal governments and their budgets. I have a couple comments above alluding to this.

I live in New Hampshire, which is known as a low/no tax state. But we have much higher property taxes relative to other states. The philosophy here is that land owners are primarily responsible for funding government.

Prices have been sticky but I feel like we’re about to see some real declines. I was chatting with one of my city’s assessing people a few weeks ago, and she said they’re likely done with re-assessments for the next few years because they don’t think prices will keep going up.

“I wonder how falling prices will affect municipal governments and their budgets.”

Yes, that’s already a big problem with owners of office buildings and multifamily buildings filing for massive reductions in assessments. This is putting another big dent into the San Francisco budget, for example, where office buildings are selling at 60-70% discounts from prior transactions, and landlords here have been filing to have their assessments cut by half or more.

>50% assessment reduction….What a boon for the landlords who haven’t lost much rent revenue, and aren’t concerned about their buildings’ values.

Lots of these landlords lost their buildings. They’re goners. Investors that bought those buildings from lenders for 70% off are at the forefront here; and landlords that kept their buildings, often with high vacancy rates, are asking for lower assessments based on the transaction prices now happening. The vacancy rate in SF is still over 30%.

I think that there is a lot more too it than that. The American market is overpriced. Reminds me of 1971 when I was advised by my high school adviser that I should join the marines in their adventure in southeast Asia,

Sigh. Perhaps our govt will have to be financially responsible??? One of my first jobs out of college for my first degree was auditing school districts and a few other govt agencies. The amount of money, waste and inefficiency was phenomenal, especially when compared to similar private businesses, non profits and one Indian tribal govt. They govt can take the hit without it impacting the services it provides, they’d just have to cut jobs related to unnecessary bureaucracy.

I know that I am on record saying that AI is this generations snake oil.

For a while I toyed with the expansion of AI as autistic intelligence.

Sort,am a Hampster resident working in Mass.,have seen some very modest drops and some more realistic pricing.

As for property taxes,really depends on town,was very interested in a property recently till saw the property taxes and moved on.

The taxes I see in Mass. many times even worse and they have income/sales tax also.

There’s an interesting article in the NY Times, titled “These Young Adults Make Good Money. But Life, They Say, Is Unaffordable.”

The fact is, many, many people are unhappy with today’s economy. And it doesn’t matter why, and it doesn’t matter whether you think they’re objectively wrong. Telling them how great they have it is not going to make them feel better when essentials, like housing and child care, are increasingly out of reach.

Biden/Harris learned that in 2024, and Trump is learning it now.

Yeah propaganda only goes so far….

Wealth is relative making $100k a year was good when houses cost $200k and cars cost $20k.

$100k when a house costs $600k and a car cost $50k doesn’t go very far.

It will be interesting to see how this plays out. Both parties will do anything to win. The right action is to allow a recession and the bubbles to deflate. What is likely is free money/buying votes. Student loan forgiveness, sizeable first time home buyer credits, sending out checks

Govt’s historic role as trusted information source under threat…

Numbers fudged?

Data wiped?

Facts fabricated?

MAG: There’s a 92% Chance Trump Is Making It Up…

May I make a suggestion. Buy a lot with trees and sawmill, and build a home. The sawmill and lot cost maybe 20k. You will learn a lot, It is not that hard, and you will be very proud of yourself when you finish it. If you do a good job you will make $ also

You just opted out of the American rat race. You can do it on weekends and holidays.

As if opting out is not the healthy choice.

However, I have yet too meet a friend that didn’t remind me of someone I knew that was a bastard

Where do you live while building the house? I imagine it takes more than a single day.

I do my own car repairs, and a frequent challenge is getting a ride to the parts store when my car is partly disassembled.

FYI: Wells Wilder’s Reverse Point Wave Signal, also in Edward and McGee’s Technical Analysis of Stock Trends, has an 83 percent historical chance of proving correct. Daneric’s Elliott Wave theory is also pointing down.

We’ll see if the FED counters.

Well there is no need to respond to make believe or unsubstantiated claims

The Elliot wave is a concept that is promoted continuously without a whiff of validation let alone the only metric correlated with the stock price

Love is the only thing that can break your heart

I was standing in my driveway in Algonquin IL when FED ex delivered Robert Prechter’s sell signal for Black Monday the Tuesday before.

Yeah, the analysis is convoluted but works in retrospect. And it’s foolish to use one signal. There are multiple signals at inflection points.

These charts don’t tell the whole story.

I live in San Diego and homes that had deferred maintenance and still had the original 40 year fixtures were going for $400K over asking. Homes in the same neighborhood that have full gut remodels are selling for less than these same houses sold for at the peak of the stupidity in 2022.

So while homes are still selling for close to the 2022-2024 price, the home you get for your money is way more. I can now buy a home for $1.5M that would have sold for $2.0M a few years ago. Lots of homes in my neighborhood are now selling for a few hundred K under list as sellers realize the party is over.

Side note: Went to an open house yesterday of a flip down the street from me and you could feel the desperation from the agent. Nice enough home but $400K over priced and they haven’t figured out that 60 days on the market means you’re priced too high.

Just wait until the AI bubble burst and the stock market comes back to reality.

“$400K over priced and they haven’t figured out that 60 days on the market means you’re priced too high”

Something is only worth what someone else is willing to pay for it.

Amazing how few people seem to grasp this concept.

I wonder what OER says about the value of homes based on ROi. With corporations net sellers of the single family rental and not buying condos their business model is for neighborhood ownership where they control maintenance and rental prices . Much more efficient.