But there is a solution to this affordability crisis.

By Wolf Richter for WOLF STREET.

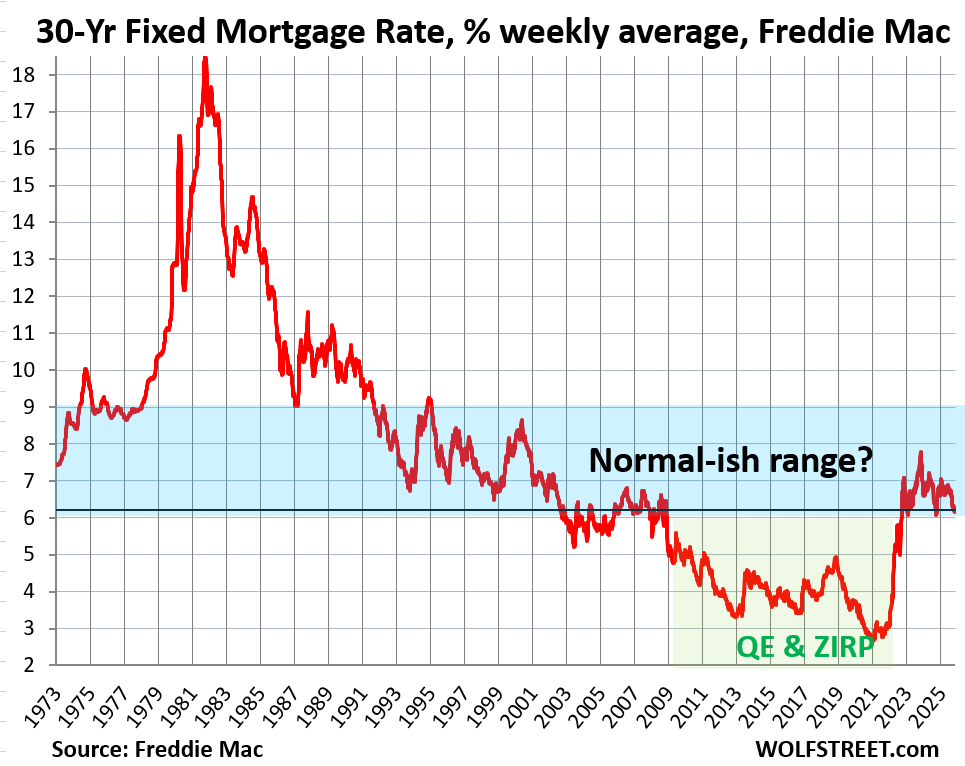

For about the past three months, the average 30-year fixed mortgage rate has been around 6.25%, give or take a few basis points. In the latest reporting week through November 26, it was at 6.23%, according to Freddie Mac data.

While this may seem high to people who have not seen anything beyond the QE era of 2009 through 2022, it’s at the low end of the historical range. There was a 40-year bond bull market from the early 1980s through 2020, during which longer-term yields kept zigzagging lower, and mortgage rates with them. But the final phase of this 40-year bond bull market was driven by QE, starting in 2009, when the Fed bought large amounts of securities, including mortgage-backed securities (MBS). This ended when the worst inflation in 40 years erupted.

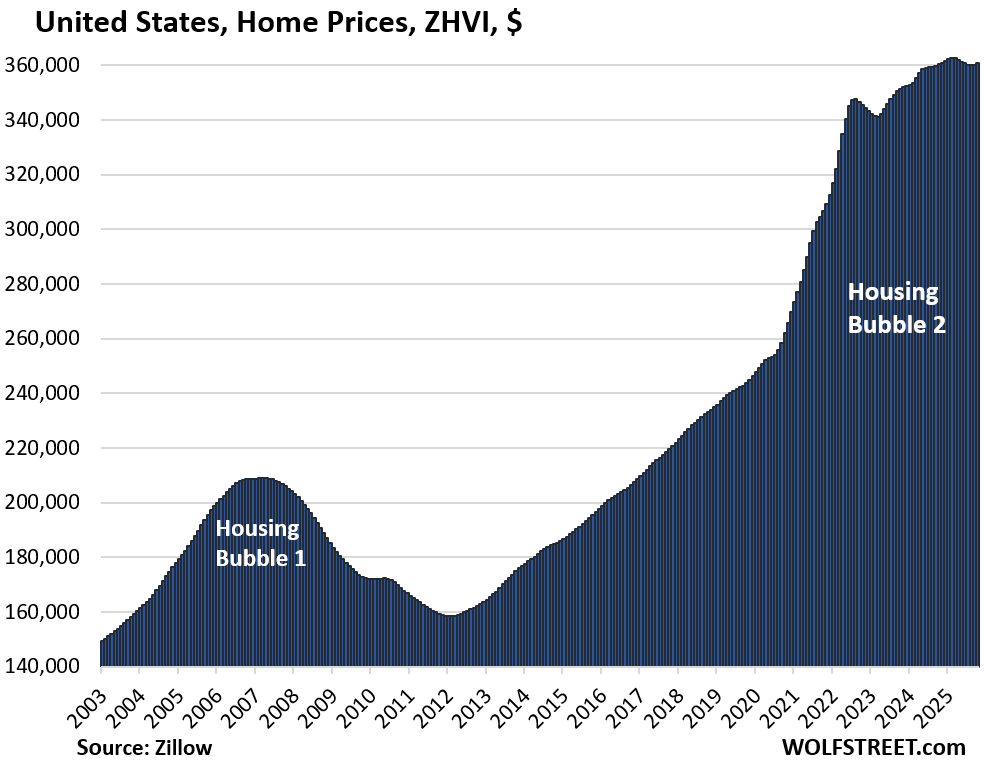

The below 5% average 30-year fixed mortgage rates were an aberration caused by QE – an explicit policy by the Federal Reserve to repress mortgage rates to trigger the biggest bout of home price inflation this country has ever seen. The below 5% mortgage rates started in 2009, and in 2012, home prices began soaring. And then, amid the mega-QE during the pandemic, home prices exploded by 50%, 60%, even 70% in many markets in just two years.

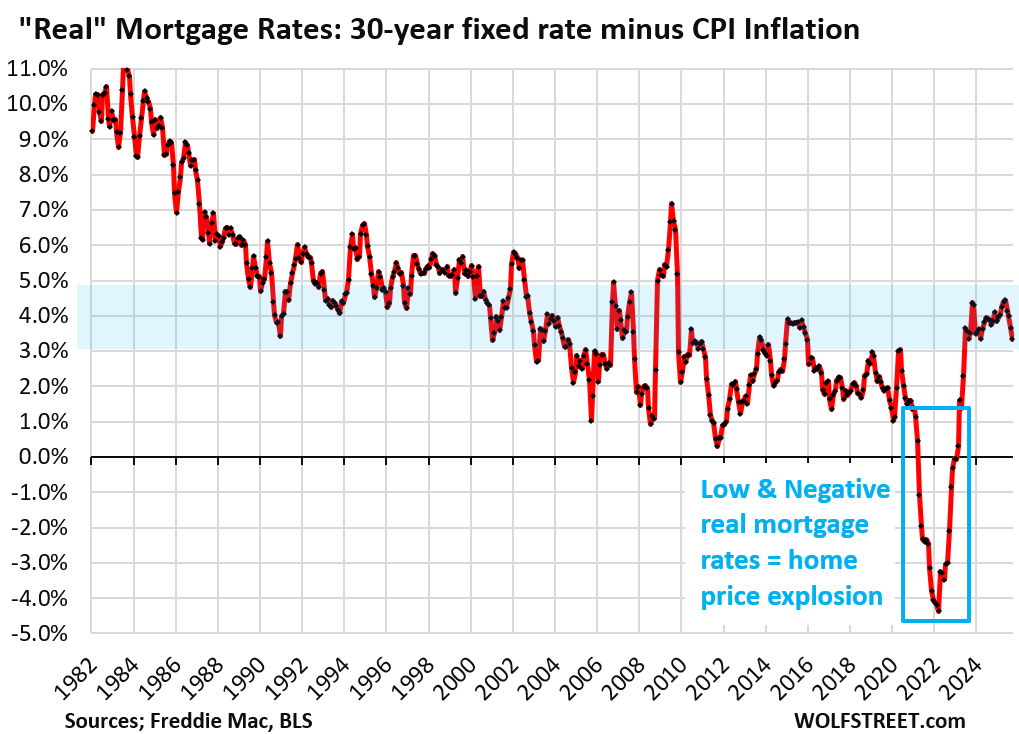

Negative “real” mortgage rates were ultimately the result of the mega-QE from March 2020 through early 2022 – which included the Fed’s purchases of trillions of dollars in MBS – which pushed mortgage rates below 3% even as inflation was spiking.

By the beginning of 2022, inflation was heading toward 9%, and the most reckless Fed ever (as I called it at the time, you can google it) still had its short-term policy interest rates near 0% and was still doing QE to repress mortgage rates.

Mortgage rates were far below the rate of inflation at the time, so negative “real” mortgage rates (mortgage rates minus CPI inflation rates), and that turned out to be better than free money.

FOMO-addled buyers, armed with better-than free money, trampled all over each other, overbid, outbid each other, offered ridiculous amounts “over asking,” bid sight-unseen, waived inspections, etc., and home prices exploded by 50%, 60%, 70% in many markets in just those two years.

Negative real mortgage rates were not normal. They were the result of the most reckless Fed ever. They were an aberration.

Recently, mortgage rates have been in a normal range in relationship to inflation

Now CPI inflation is over 3%, the worst since May 2024, after having accelerated for months. Higher inflation also seems to be the new normal, as the Fed has been cutting its policy rates, and has been discussing further cuts, despite this inflation, and if it continues to cut, it would be an indication that the Fed is going to tolerate higher inflation over the longer term, that it’s comfortable with maybe 3% to 4% inflation. And higher inflation would entail higher bond yields, and therefore higher mortgage rates.

And there is no appetite for QE because it would cause inflation to explode in this already inflationary environment. Americans hate, hate, hate inflation and high prices, and they have a history of voting governments out of office under which that inflation occurred.

What is not in a normal range are home prices. Home prices move very differently in each market – but they soared in most major markets from 2012 to 2019, and then they exploded in most major markets in the two years from mid-2020 to mid-2022.

In a bunch of markets, home prices began sagging in the second half of 2022. In other markets, home prices continued to rise, but at a slower pace.

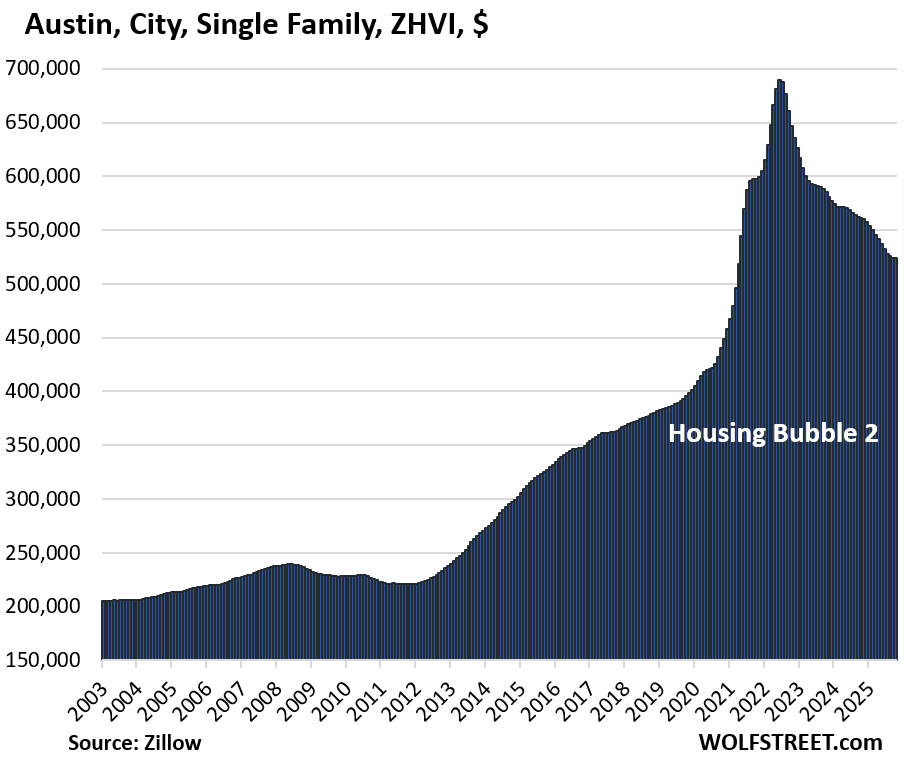

For example, in Austin, TX, prices of mid-tier single-family homes exploded by 64% in the two years from mid-2020 to mid-2022. That is not normal. It’s ridiculous. And from mid-2012 to mid-2022, over those 10 years, home prices exploded by 207%, from $225,000 to $690,000 for mid-tier single-family homes – having more than tripled in 10 years! That’s not normal; it’s ridiculous. Those are the effects of the Fed’s mortgage rate repression.

Since the peak, home prices in Austin have dropped by 24% as the market is in the slow process of repairing the affordability crisis. Undoing the craziness from 2020-2022 is the solution, along with rising wages over the years, not lower mortgage rates.

For example, in Sarasota County, FL, home prices had exploded by 70% in two years from mid-2020 to mid-2022, and by 210% from mid-2012 to mid-2022 (tripled in 10 years).

Home price explosions like this are not normal, they’re a result of years of reckless monetary policies.

The solution to this affordability crisis in Sarasota County is not lower mortgage rates, but unwinding the home price explosion. And the market is working on it; prices have dropped by 16% from the peak:

For example, in Phoenix, AZ, prices of mid-tier single-family homes had exploded by 60% in two years, from mid-2020 to mid-2022; and by 360% over the decade from mid-2012 to mid-2022. The market has since then been slowly working on reducing the massive affordability crisis, and prices are down by 11%.

But in other markets, prices are still rising, though at a slower pace.

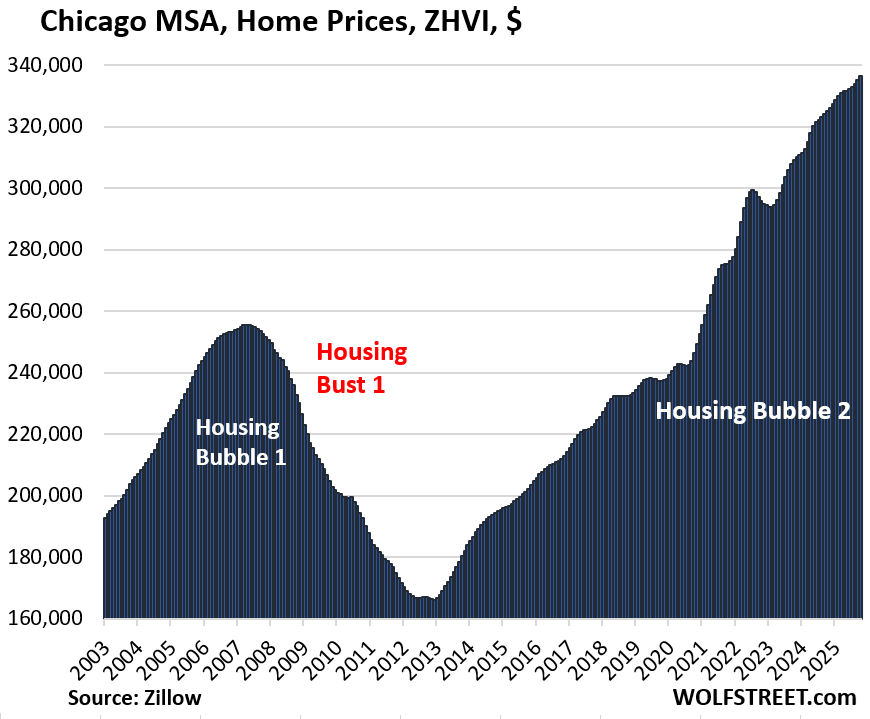

For example in the Chicago-Naperville-Elgin, IL-IN metropolitan statistical area (MSA), prices are up 3.6% from a year ago. From mid-2020 to mid-2022, prices had soared by 23%, and then continued to rise. Over the five-plus years since mid-2020, prices have soared by 38%, as the affordability crisis worsens, and lower mortgage rates would just make the crisis even worse by driving prices up further.

Since mid-2012, prices have doubled.

There are other big metropolitan areas where prices are still rising, including in the Philadelphia metro and the New York City metro.

Home prices in all markets combined also exploded since mid-2020 on top of the already soaring trajectory before the pandemic.

For mid-tier single-family homes and condos, prices have soared by 42% since mid-2020, and by 128% since mid-2012, according to the seasonally adjusted Zillow Home Value Index (ZHVI). Over the past 14 months, the index has essentially flattened out.

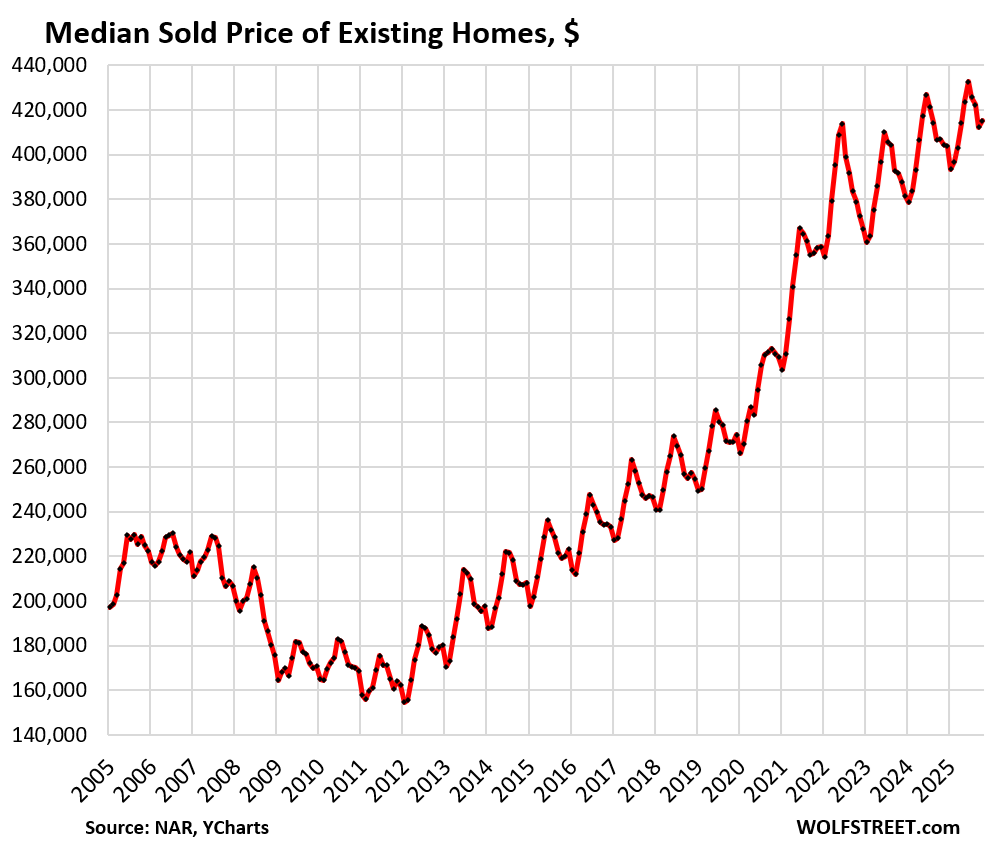

For all single-family homes and condos, as per the not seasonally adjusted median price by the National Association of Realtors, prices from October 2019 to October 2025 exploded by 53%, and since October 2012 by 133%.

This is the median face of the affordability crisis: It’s far worse in some markets, such as Austin, and it’s less bad in other markets, such as Chicago. But in Austin, the market has begun to repair the affordability crisis; in Chicago, it’s still getting worse.

Lower mortgage rates are the problem, not the solution to the affordability crisis. Low mortgage rates have caused the affordability crisis. If mortgage rates were forced back below 4%, with inflation as high as it is, it would cause home prices to rise even further and faster, and make the affordability crisis even worse.

Every adult in the room knows this. But it’s politically incorrect to say it out loud because somehow the industry dogma has to be maintained that home prices can never decline, even after they’d exploded by such crazy amounts.

The solution of the affordability crisis is many years of rising wages and falling home prices that over time would unwind the crazy home price explosion that started in mid-2020.

Mortgage rates that are higher than CPI inflation by a historically normal spread — so currently at around 6.3% — would allow declining market prices and rising wages to find each other over the years, thereby solving the affordability crisis and bringing a modicum of sanity and health back to the housing market.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

On a macro scale I agree with most of the above. I would, however, suggest that both can be true: that the price of homes increased beyond norm in some places. It’s those last 3 words… Yet rates went up for completely different reasons and did so nation wide – all places and for all things.

You nailed it. I started in the mortgage industry in 1978 as a Savings and Loan mortgage loan officer. Today I’m an nmls mortgage broker with my own company. So you could say I’ve seen it all. The one thing I don’t hear mentioned much if ever is the real estate crash of the ’80s. Does history repeat itself? At the peak of that unwinding the states with the worst foreclosures were called the Colt States. Colorado Oklahoma Louisiana and Texas.

The energy states, I can’t believe I ever felt sorry for an oil man. Thousands and thousands and thousands of foreclosures, people walking away from their homes because they were under water, the resolution trust corporation formed to auction them off nationally at fire sale prices. Since there’s been a moratorium on foreclosing in our current times, if the market is ever allowed to try to digest that reality the adjustment of housing prices that would occur would certainly put some more affordable housing on the Street. Add in unemployment rates, even when housing prices are down if you don’t have a job or your credit sucks there’s not a lot you can do. Anyway I liked your analysis. I talk to people everyday who want to know when rates are going to come down below 6%. Right now you can structure a deal in the high fives with some points but otherwise I think they’re going to be waiting a long time. We’ll see.

“I talk to people everyday who want to know when rates are going to come down below 6%.”

When we have a recession, that’s when rates will move materially below 6%. The question is what does the Fed do in terms of MBS?

The recession solution is another one of those taboo topics that nobody wants to talk about. However, it’s the only real long-term solution. Anything else will be window dressing.

we contemplated downsizing our small 2700 SF home to 1800 now that kiddies are gone.

because we still maintain mortgage(about 30% todays value) we’d have to get NEW mortgage and NEW TERM

we have 15 year at 3.35% and about 1/2 way

peeling off principle every month

new loan would lock up into perpetuity and big mortgage as we begin retirement

STAYING PUT until we pay it off – in 7 to 10 years

When fiscal spending regains sanity, that’s when rates will fall below 6%. Recession has nothing to do with interest rates coming down. QE created the false belief that falling rates and recessions were somehow tied together. Argentina has been in a never ending recession, and their interest rates are sky high.

What are your opinions on CLTs (Community Land Trust)? I read an interesting article on it recently, talking about how every politician champions affordable housing but none have a real solution. CLTs on a massive scale could work as a way to decouple real estate speculation from home ownership. Not perfect, but perfect is the enemy of good.

It doesn’t really address what most here focus on as part of the “have” crowd, but could be a way to help with housing affordability for the “have-not” crowd. I see potential for something like this to “pull-down” the top part of the market since it would reduce speculative rent-seeking property investment, via less renter demand.

Don’t you have to pay fair market value for the land then develop it to code for those? Where does the money come to create these trusts. Once you have them, how do you create a sense of ownership to bind maintaining appeal and value to the resident rather than the failure of the “projects” model? Big picture is from 2003-2025 home prices nationally went up 4% on average but income and inflation only went up 2.3%. This is driven by two factors, first the cost to add inventory went up 4.26% on average and second is the outsourcing of manufacturing along with the burden of education costs inhibited M2 and thus money available for income growth. Add in the opening of speculative investment shifting the risk burden of leverage on homes from the lender to the public twice, first via MBS followed by REITS and the pending collapse of the latter and you have the current scenario.

A superb article that defines the issue, an incendiary talisman of change in the offing.

The kids are likely to reinstate their great grandparents WW2 social democracy decisions.

Clear, concise and rational.

Anyone finding fault with this piece should not be allowed near a voting booth.

Thanks Wolfe for your work.

Monetary policy is not *just* about mortgage rates. Much of what Wolfe says here is entirely rational but is reality seen through a soda straw.

you mean the new 10% annual inflation rate like 70’s

here to stay and likely get worse with every 6 month $Trillion new govt debt

Of course it is not, mortgage rates are only a tiny portion of monetary policy.

The question is would YOU lend someone money for 30 years at rates below 6%? Neither would any reasonable investor in today’s inflationary environment.

On the flip side, in the unlikely event that deflation occurs, the risk of default rises.

We’d love to move our current mortgage to new property

it’s 3.35% 15 year

but we won’t pay this off just to get 6% new term loan

we’ll wait til it’s paid off

then we’ll have 100% cash

Agreed, a nice and concise summary of the situation and the various “leadership” stupidities/corruptions that brought the US to this point.

How about we get investors out of the market, check into who owns a lot of these homes…..

Speculation drove the house price bubble as much as low rates. No one with a choice would sell a house whose price was rising so fast as they did through 2022.

There’s now a lot of multiple homeowners, plenty of regular people as well as corps and funds. Mostly legal self-interest, but like every bubble there’s plenty of shenanigans.

In certain markets (NYC/SF looking at you…) it might be pretty worthwhile to have a publicly available database (more easily navigated/analyzed than current ones) to really get a strong, in depth handle on just WTF actually owns RRE in the NYC metro funny farm (how can lower middle class/mc afford to rent, even in distant suburbs? And true for years and years and years, even before present insanity).

Of course (assuming hidden ownership concentraion), there will be an army of paper LLC fronts, named cutouts, etc. Still worth trying though – it is a start).

(I’m sure plenty will say that concentrated ownership in RRE is “impossible” – perhaps, but less so than before

1) 20 years of ZIRP provided massive RRE speculator fuel,

2) AirBNB’ing shifted housing to motel speculating,

3) Realpage made online algorithmic landlord collusion a thing,

4) 4-5 million *additional* illegal aliens were blind-eyed into the US in just 1-3 years

5) China had 3 trillion in USD export proceeds that had been getting ZIRP’ed for 15 years and looking for a new asset class that might yield greater than 1%

And so on.

I’m not saying *nationwide* price collusion is particularly likely (although…China…3 trillion USD…in a RRE market where 80-90% US bank leverage is readily available…, I’m just saying).

1) Having much greater transparency into actual end-ownership of RRE is probably a very worthwhile thing…with relatively few downsides

2) This is particularly true in the worst of the rent-inflation metros, where almost unprecedented 20%-25% hikes in 18 months have to at least raise questions.

The last 5-20 years have been all sorts of ugly, economically, for the US.

It isn’t paranoia to want to get more transparency and empirical data from a financial sector that has been intimately tied to the worst excesses.

Decrease in mortgage rate brings down monthly PMT given everything else unchanged. Because super majority of home buyers are irrational &/or financially illiterate so the sudden increase in demand brought by this perceived lower monthly PMT drives up the home price. This obnoxiously welcomed 50 year mortgage is another disaster in making yet financially illiterate irrational buyers don’t know nor bother to learn. Right now the mortgage rate is not high but normal given 80 years history in mortgage banking. When the world is dominated by insane ones sanity becomes rare commodity.

Blame lies mostly with the congress: the fiscal response of stimulus, PPP, etc was not completely necessary. QE was not responsible for the quick run up of prices; higher disposable incomes were.

Dave,

I personally blame the Federal Reserve.

Then I blame congress.

Then I blame Wall Street.

Frankly, I don’t see any good guys in this movie & it explains the financial pain we are all experiencing.

Shadow stats turned me to the dark side. John Williams taught me to double & triple all FRED data to the negative.

End the Fed.

Nope. That’s not how it works at all.

I agree that the Fed is incompetent as demonstrated by their QE policy as Wolf accurately hypothesized created the housing bubble 2.

Bernanke’s conjectures currently appear to be wrong.

But who knows.

QE was definitely responsible. Disposable income did not rise that fast.

I think a whole bunch of people suddenly had down-payments via PPP. It’s also when the TikTok RE investor craze ignited and people also had a lot of time on their hands to start a new RE business

BS. RTFA.

Let’s not forget the psychological effects of COVID19, where millions of apartment dwellers in large cities were terrified for their lives and wanted to move to the burbs into a SFH. Not to mention the new WFH crowd who could suddenly work from a beach front condo in St Petersburg instead of their flat in Hoboken. Had COVID never happened the Fed might have gone into QT mode much earlier, deficit spending never would have exploded and we would likely be in a much more normal environment.

The Fed and its stupid QE are almost entirely to blame. Look at the chart, prices ran up from 2012, it’s the Fed.

You can all be correct here. QE doesn’t just sit idle, it sloshes throughout the system and becomes disposable income.

Similarly, massive federal deficits become massive corporate profits. (Read Hussman on this.)

Loose money anywhere drives prices up everywhere.

But incomes don’t rise equally… so inequality grows.

Ditto to all, hopefully. Thanks Wolf

I disagree that using the historical norms is the proper basis.

even 7% is cost prohibitive (that’s paying 1/15th the the cost, just to be there. There is no way that can be justified by any means, other than excessively high historical ratres.

Prices exploded by 40-70% in 2 years. That’s NOT normal. That’s crazy. That’s the issue. And prices have started to come down in many markets. They need to come down more, and wages need to come up, and over time, it’ll work out. But the rates are fine.

Lower rates will just make homes EVEN MORE unaffordable because they would cause prices to rise again. That’s the last thing you want.

How can prices come down when cost to build new is so astronomical? Even a modest size builder grade house is approaching $600k in the Midwest.

Costs are irrelevant to prices. Selling prices are determined by the market = willing and able buyers. They don’t care about your costs. This is one of the most fundamental principles. If companies cannot produce below their selling prices, they lose money and eventually go out of business. Happens all the time.

Lennar cut its selling prices, regardless of what you think the costs of building are — all homebuilders are doing that in order to find willing and able buyers for their product.

https://wolfstreet.com/2025/09/19/what-it-takes-to-sell-homes-lennar-cuts-average-selling-price-below-its-2019-level-and-its-home-sales-held-up/

Wolf, I suggest costs may be irrelevant to price in the short term, but if landlords can only find tenants at a loss and builders can only find buyers at a loss, there will be a future drop in supply as capital departs for greener fields.

1. Prices of construction materials have been falling for years, for example lumber prices have plunged from their 2021 and 2022 highs by something like 60%, and steel rebar prices have plunged from their 2022 high by about 30%. Labor costs have gone up.

2. The huge wave of multifamily construction starts from 2013-2023, particularly 2021-2023, has now swamped the market with available units (condos and rentals), putting downward pressure on prices and rents. Lots of apartment landlords have defaulted on their loans, and properties have been sized by lenders or the buyers of those loans. This is part of the CRE meltdown. So the supply is here and still being completed and coming on the market. Multifamily construction starts are still amazingly strong, but have dropped off from those highs in 2021-2023. Since 2013, multifam construction starts have been the highest since the boom in the 1980s.

3. Homebuilders are also still building a large number of houses even where supply is coming out of their ears, such as in the South and West. And we see that in their rising inventories.

4. Why is that? Because it’s the business of these companies to build multifamily housing and single-family housing, and they cannot just stop doing business. So they have to keep building to stay in business. And they’re competing on price (often hidden in large-scale incentives and mortgage-rate buydowns) with homeowners trying to sell their homes. That’s one of the reasons sales of existing homes have plunged, because homebuilders and multifamily are eating their lunch.

5. One thing to keep in mind: All successful producers, from automakers to homebuilders, are always and constantly working on reducing their costs through various methods, including automation (homebuilders use more manufactured components, for example), lower-cost materials, less labor-intensive processes and designs, etc. That has been going on forever and continues. So when raw material costs go up, that doesn’t necessarily mean that the cost of the buildings go up.

The costs to build a new home go up, because the builder can charge more when the market says a house is worth 600k.

A general contractor in the past might have been happy to make 50k out of a project, now expects $75k or $100k. All of his subs take the same point of view.

Where I live, it’s easy to see in the costs of excavation. It’s a small market, but lots of people are moving here. 3 years ago there might have been 50 new houses built in a year, now it’s 100.

The same guy who used to charge $10k to prepare the site and excavate the foundation hole, now charges $25k. Diesel is not much more expensive. His equipment is pretty much the same equipment. The ground hasn’t gotten any harder to dig. It’s supply/demand. Over time, if the demand keeps up, new outfits will move in or one of his operators will decide to leave, buy an old trackhoe and start his own business.

The price increases for materials is a minority component in Building costs. The real explosion has been in subcontractors – plumbing, heating, septic, electritian, drywaller, concrete, painter, trim carpenters.

An even more insidious problem is finding an honest contractor to maintain our techno geopolitical homestead.

I replaced my ac system and the quotes from the firms advertising on tv were 5X more than I overpaid an honest contractor.

So many of them have been chased south of the border that we are at the mercy of the native population.

As homebuilders, we couldn’t agree more. Rates should have NEVER gotten that low. Were we winners in those 2 years? Yes, but it absolutely killed affordability AND the expectations of younger generations, who now think that’s normal.

Our biggest issue is the raw cost of inputs for new homes. We are making LESS per home than we were even before 2021 yet having to charge much more because our costs have exploded by over 50% in the last 10 years. Not good at all and we can’t figure out how that gets corrected.

Historically, 30 year mortgage rates have averaged around 6.5% or so ever since 30 year mortgages were created in the 1930s.

Somewhat surprised they’re cutting again in a couple weeks… Talked tough last meeting but haven’t followed thru and not sure what has changed since then.

Maybe it’s a live meeting but you’d think they would communicate that before blackout.

If they don’t cut popcorn time!

Well, Markets were not expecting it. Then Powell sent his deputy to tell Markets expect a Cut.

FED is catering to Wall St more than all US Citizens who they claim to serve. There are enough jobs out there. White collar job losses we are having are not going to stop by FED doing 25 or 75 BP cut.

People are tired of Inflation. From 2021 till now and FED projects it will hit 2% by 2028. FED’s 2% target is lie.

“Watch what I do and not What I say”

The solution is to prohibit QE by statute. The reason the 10 year is where it is, in my opinion, is because the market believes a resumption of QE is possible (even though there’s no evidence of this). Ban it by statute, and the 10 year will go where it should.

That makes changes to the Fed Funds Rate a lot less imporant.

“The solution is to prohibit QE by statute”

See also “Gold Standard” or any standards at all…

The root cause is the same as it was in Weimar or long before that to the Romans and time immemorial…

– The essential fraud enabled by the “power” to issue fiat money essentially unbacked/unsupported by anything other than the honesty/integrity/ability (ha!) of the government/money issuer.

Sooner or later, almost all governments select monetary fraud (money printing in one fashion or another) over fundamental reform in their economies, societies, or (especially) themselves.

It’s time to cut. Long-term money flows have peaked. There is a “sweet spot”.

The fallacy of monetarist economists like Milton Friedman may only be determined by a crash in asset prices, ie deflation. An assimetric evaluation that ignores, what I consider inflation, an inexplicable increase in asset prices.

What we measure as inflation is a derivative as prices increase in response to the monetary stimulus. According to Wikipedia which sounds right as follows

“A derivative is a mathematical concept that measures how a function changes as its input changes, often represented as the slope of the tangent line to the function’s graph at a given point. It quantifies the instantaneous rate of change of the function with respect to its variable.”

Correct and homes can drop 50% and they probably be still too high or back to normal and 95% home owners will still be ok. The next crisis will be when how’s drop and people used their homes as piggy banks ! Look out

We need a depression/ recession by 2030 to try to normalize some

Of the craziest policies ever

Vincenzo Wrote: “ We need a depression/ recession by 2030 to try to normalize some

Of the craziest policies ever”

We’ve seen though The Fed will always take a crisis (see 2008 and 2020) and overreact. If we did have a massive recession/depression The Fed would probably use QE or ZIRP again.

The FED uses the crisis to appease the American Bankers Association. They used them to remove legal reserves.

We need a depression/ recession by 2030 to try to normalize some

Of the craziest policies ever

I disagree. recession or worse depression falls upon the backs of God’s favorites, the working people.

What we need to do is too increase the marginal tax rate to a level that at least we’re not borrowing money to pay for your extravagance

Canadian here. West coast. Would add, the cost of homeownership has escalated too. Including: property taxes with 8% to 10% increase per year for years, maintenance especially labour which has doubled in rates, utilities and insurance aswell. Other items would include low life span on appliances, car repair if commuting, the increase in rates on renewals; (many were on variable rates, others on 3 to 5 year term. CDN doesnot have 30 year term.)

Awesome article, Wolf

I think what the rest of the nation is seeing is what the reality has been in San Francisco in like almost forever.

Yes, SF home prices are crazy, and they exploded years ago, but they rose a lot less during the pandemic than they did elsewhere.

Well I sold my loft in SOMA in Nov. of 2021. It has lost $200k in value. I am a happy camper.

Thanks Wolf. Artitcle Title says it all.

FED created this House price crisis by doing ZIRP and QE. It will take many many years to undo the damage.

Last 15 years, many boomers and Gen X bought multiple homes. Because of very low rates and multiple refinancing, they don’t have to sell as they can just get by through rental income. Rents have gone up too.

States like CA make this crisis worst by Prop 13.

Sky rocketed Stock evaluations have helped to Real Estate prices still very high.

I think only FOMO buyers who bought post Covid boom, are feeling the pinch if they didn’t intend to keep property for very long. Already high purchase price, cant sell at loss or refinance as they were told “Date the Rates and Marry home” BS.

FED and Treasury are hand in hand to keep 10 yr less than 4.5-5%. Otherwise we should have seen Montague rate 8-10% by now.

But lets see how long they can. One day Bond Market is going to wake up and start pricing for much higher long term inflation.

It is site unseen, not sight-unseen.

“Sight-unseen” is an idiom meaning “without having seen it first.”

Thank you. Exactly my thoughts. Mismanaged conjured pandemic mania collateral damage +gross fiscal incompetence by those who were so busy playing spin that they whipped up social hysteria to a level of mass dysfunction of a rabid dog. The return to sanity is not going to be comfortable or quick but if we see the light of the approaching train receding it we will begin to breath.

Soooo typically people move every 7 years. The smartest thing would have been to let home prices crash. People who bought pre-2020 had plenty of equity. People who bought in 2021/2022 don’t need to sell for awhile. They could have crashed without a crisis. However, for some reason the govt and fed wanted to prevent this and screw a whole generation over.

mm1,

They don’t want home prices to fall because they NEED the inflated values to keep the property taxes high. These taxes support billions in debt acquired and misspent on the local level.

We just voted down an increase in school taxes in my area. They have declining enrollment, because nobody can afford kids anymore, and yet they want more. They have been building a new high school with a campus that looks like a university. You can see the lighting fixture(chandelier) from the road as you drive by. They have a stadium too, why not! I live in a lower middle class area, where families are doubled and tripled up to afford the house.

Last year they passed a road improvement bond issue for over a

$1 BILLION. In the fine print it says this is for 10 miles of road, $100 Million per mile. It was stopped by a lawsuit because you can see it is pure fraud.

You must be in Dublin?

Petunia – “They don’t want home prices to fall because they NEED the inflated values to keep the property taxes high.”

Couldn’t they just change the mill rate? Wouldn’t this get them the same amount of dollars?

For instance, if they need X number of dollars to run a city/cover their debts, but house prices have declined by half, let’s say, then they would just adjust the mill rate upwards to get those same amount of dollars they need.

Solution for declining house prices? Raise the mill rate. They’ve been doing this forever.

The mill rates are capped by a certain percentage, maybe 10% a year increases. Now that they can’t hide the home price decreases, they want to change the assessment schedules to once every few years, this means they can stop the lowering of assessments as home prices fall.

These people are now working for us, it is in your face public corruption.

P.S.

I protested my taxes for 2025 and got the assessment dropped by $40K. However, I don’t know how much lower this will make my tax bill. Maybe not much.

“I live in a lower middle class area, where families are doubled and tripled up to afford the house.”

One can only imagine what the shitter must look like.

“Typically people move every 7 years” is marketing B.S.

There is no typical.

Plenty of people stay out for decades. Especially older ones who value their home equity.

Some need to move for professional or family reasons. But the “every 7 years” meme was propagandized to encourage the unwise to waste money on Realtor fees, and move far more often than they should.

The 7-year figure has been cited for mortgages that get paid off via refis and people selling their home or paying it off with a bonus check or whatever.

The average time before a home sells was cited as 11 years.

But all those figures are pre-3% mortgage figures. Everything has kind of frozen. Refis collapsed and home sales plunged, and that’s been the case for three years, so I assume the averages will be higher now and going forward.

“There is trouble in the forest”

Those crazy Maples and Oaks.

Other factors are left out of this conversation like the down payment issue…. The reason the younger generation spends money on food and experiences is the rational belief they will never be able to buy a home and keep it with 20% down required because jobs are more and more unstable and the ancillary cost of homes is skyrocketing. This is why no one is having kids. It seems in CA the politicians want people to be endless “students” partying in 2 to 5K apartments with a care costing $1,500 with insurance not including gas and maintenance. Now way can the young get married and have kids in a home purchase that supercharges the economy. I bought this ranch with 5K down with a 1K rebate from my real estate agent. Ca does not allow for small inexpensive homes to be build as starter homes for families ending as a downsize of retired people buying the same little house with a fresh remodel. The elephant in this room is the fact that Capitalism as were were trained to believe is not in fact at play. The very first thing I would teach my son is to clearly understand HOW THEY TELL YOU IT IS AND HOW IT REALLY IS…. Wolf really helps us to see the really but all this ignores the reality that tech will dominate all and everything. I am seeing amazing things with dynamic pricing and was able to beat Home Depot on a demolition jack hammer (Cost $269), and Lowe’s (Cost $279), and Wal Mart at $185) all with free shipping or pick up. Same exact model.

Amazon is the worst at doing this as its pricing was way high in the dynamic pricing carousel. This is not Capitalism or Socialism…. So what should we name this system?

We call this system ‘neo-fuedalism’.

Instead of the benefits of owning all the land accruing to a “royal” or “noble” (oligarch) class, the benefits accrue to an ‘executive’ or ‘investor’ (oligarch) class.

Very, very, few billionaires became billionaires with non-stock market earnings.

You can tell when we’ve regressed from capitalism to neo-fuedalism when consumer options and the economy are dominated by a few (almost) monopolies, and the number of key beneficiaries of the economy becomes small enough that they’re all household names.

O. Henry already coined the name for this… Banana Republic

Varoufakis calls it “technofeudalism” — his premise being that the large network entities have captured ordinary industrial producers and consumers alike in rent (economic rent) extraction “fiefs.”

Tack on Cory Doctorow’s “enshittification” whereby these same entities make everyone’s user experiences worse over time and you get what you’re living with.

I’m skeptical that housing costs are what’s driving the young people to not have kids. This phenomena is happening all over the world, even in places with reasonable housing costs. It has been tried to pay people to have kids and that idea fell flat on its face.

I think the only common denominator is screen time. Most of us spend 10-14 hours a day now looking at a screen. My husband is looking at a screen from the minute he gets up in the morning and right up until he turns off the light to go to sleep. Why have kids when you have 24/7 streaming everything you could possibly want?

The world around us is changing at a freaky pace and it is only accelerating.

This is a compelling piece, but I am confused by the chart on real mortgage interest rates. I know that anecdotes are not data, but we bought our house (in the VA suburbs of WDC where we still live) in August 1980 with a 30 year fixed rate of 9%. AI says the 12 month CPI increase for the 12 months beginning August 1980 was 11.2% so despite the high nominal rate of 9% it looks to me like our real interest rate was actually negative even back then. What am I missing?

At the time I didn’t know where else I could get a risk-free 9% nominal rate of return so I paid off the mortgage in 7 years. It was kind of fun, when the first payment came due, you could look at the month-by-month principal reduction for the next 12 months in the amortization schedule that came with the closing papers and then wipe out a year’s worth of future mortgage payments with a relatively small addition to the required monthly payment.

You got a VA rate. They’re a LOT lower than average 30-year fixed mortgage rates. You got 9%, you said. The average 30-year fixed mortgage rate in Aug 1980 was 12.25%, so above the rate of inflation you cited.

Nope! I was never in the service.

My reference to VA was to the Commonwealth of Virginia. This was a conventional 30 year mortgage loan obtained through a conventional mortgage broker from an S&L that later failed.

It is also interesting that a nominal mortgage rate of 12.25% in Aug 1980 would have produced a real interest rate of less than 2%. Your graph starts in 1982 and shows real interest rate data points of 9% and 10% for that year. That is a massive change from the Aug 1980 figure of less than 2% so there must have been huge changes in the mortgage market over that interval.

All in all, our Aug 1980 purchase was very lucky in its timing.

Yes, there were huge gyrations, with inflation spiking like crazy, and mortgage rates somewhat slower to move, and so you got these very wide spreads, and then inflation rates plunged, but mortgage rates were slower to decline, and so the spreads collapsed and even turned negative very briefly, and then it happened all over again. The early 1980s were crazy times in terms of inflation and long-term interest rates. This was also during the terrible double-dip recession, the worst employment crisis since the Great Depression, and the beginnings of another oil bust in the Oil Patch. Thousands of banks collapsed (they were smaller back then as national banks were not allowed). S&Ls (big mortgage lenders) collapsed left and right, and their depositors ultimately got bailed out, but some of their executives went to jail (senior Bush still had balls against Wall Street). Like I said, crazy times. I don’t miss them!

I’ve been patiently watching the market for a price correction. It just hasn’t materialized. Houses are delisted as soon as homeowners realize the asking price is too high. They then choose to wait only to find more houses on the market. This is keeping the housing market from tanking because it’s not a loss in perceived value until it’s sold. Then there are those with actual losses or rising insurance/HOA fees making a home unaffordable. They face tough decisions in the next six months to a year.

Sellers in my neck of the woods (East Bay Nor Cal) are pulling their listings off the market after they havent sold for 60 days and renting them. They refuse to believe their home is worth less than what it is listed for. They may do a couple price drops along the way, but nothing significant. Sorry bro, there may be a sucker that will purchase your sloppily put together tract home for 200k more than what you purchased it for 5 years ago, but it won’t be me. I’ve been following Wolf for way too long to know that is a recipe for disaster.

Home ownership in CA is more of a lifestyle choice than a financial one. But the housing gurus constantly are in your ear fueling the FOMO mantra of, “it’s a great time to buy” knowing damn well it isn’t. When you can rent the same property for $1500-2000 less a month and invest the difference isn’t that a no brainer situation?

Also, optionality value, such as renter’s mobility, is underated. By a lot.

A well-taken point completely missed in the “must-own-house” drone of MM RE propaganda.

I noticed that you used the term sloppily built tract homes.

I was a roofer for 10 years on CA Central Coast. I worked on many tracts in that area. Many of the tract homes built there in the last 20 years are indeed sloppy. Poor overall designs, and poor build quality. Many incur serious issues very quickly, sometimes within months of completion.

The structure of the house is poor, but builders slap granite and fancy “lookin” fixtures to make it look high end, and buyers unfortunately do not know the difference.

They pass inspection somehow though, likely lubed monetarily and politically.

Some of the builds are so bad, they are essentially unrepairable and have multiple homeowners filing class action suits….buyers sold a used Yugo at a new Ferrari price.

Same for the area in CA that I’m watching. My tracking spreadsheet is full of “removed from market” listings. Apparently, these sellers are willing to die on the hill of aspirational pricing. You can read them whining up a storm about mortgage rates “killing the market” in any number of Reddit subs.

They’ll do that for a while, but they’re not going to be able to (or be willing to) hold out indefinitely.

In this peculiar market, I think it’s going to take a recession and stock market downdraft. Because that will shake loose not only newly unemployed people who can’t pay their mortgage, but many second home owners who find the Airbnb and vacation rental markets smacked.

Am expecting this to pick up in 2026. Whether it hits full roll by then remains to be seen, but it’s quite possible.

Nicholas I believe the term for what these “de-lister/re-lister” sellers are doing is referred to as “chasing the market down”. We will see this happen more and more frequently in 2026 and several years to follow.

Won’t “Boomer” demographics bring down house prices? A friend of a friend living in Venice Florida is desperately trying to sell his house so he and his wife can move into an assisted living facility. He’s dropped his price 3 times in the last 3 months.

If he’s desperate, he can give it a price where it sells. That’s a falling market.

Mortgage rates do not operate in a vacuum. Real rates matter, and with inflation running at about 3 percent, a 6 to 7 percent mortgage is not historically extreme. A 6.5 percent nominal rate with 3 percent inflation is basically a 3.5 percent real borrowing cost, which is close to long-term norms. Elevated nominal rates alone are not enough to force home prices down.

The larger reality is that we have almost no distressed sellers, extremely low mobility, and a structural housing shortage that has been building for 15 years. You cannot get a major price correction without forced selling or a surge in inventory, and neither condition is present today.

What we get instead is a correction through time rather than price. The market moves sideways. Nominal prices flatten. Real prices slowly decline as wages rise. Affordability improves gradually in real terms, not through a dramatic drop in listed prices.

The most realistic outlook is a long period of stagnation in home values. Demand is softer, supply is tight, inflation offsets part of the rate shock, and very little moves. This produces a slow, drawn-out correction rather than a collapse.

100% Levi.

The Fed/covid/stimulus created a demand squeeze.

The structural problem remains. Hence prices continuing to rise in some markets. With materials, permitting, and labor costs continuing to rise, I don’t see the structural problem improving any time soon

Housing has fallen every recession. We’re likely to begin on in the 1st QTR.

There is no structural housing shortage.

Houses per capita is highest historically.

A lot of people are hoarding houses in hope that they keep on increasing .

Demographic decline also dont support high home prices .

In my city jn socal I see most homes for sale are vacant in the listing pics.

Jon – “A lot of people are hoarding houses in hope that they keep on increasing.”

Exactly, and that is why the cities that had less price appreciation (in other words, those that are considered cheap and ripe for appreciation) are being bought up. Too many speculators in the game, private equity companies snapping up large percentages of homes that ordinarily would have been sold to ordinary citizens.

And one housing expert said that the wealthy boomers who bought two and three homes, who are now listing but can’t get the high prices they expected, are quickly delisting. She called them “irate delisters”. She said that the only thing keeping them cocky is the gains they are receiving in their stock market portfolios. They are currently delisting because they CAN.

But she said that if the stock market were to decline, these people would be scrambling.

Jon you are correct if you are referencing SoCal’s southernmost city/county. We did a market analysis several years ago and concluded that population growth did not outpace housing units added.

Why would someone invest in housing supply increase if all the building costs are going up and the increase in supply will ultimately drive down home prices? Rapid price swings in housing are untenable. Stretch out the x axis is the plan, as usual.

Assumes the economy remains stable or strong. If not…

Headline: Mortgage Rates Are Not Too High. What’s too High Are Home Prices that Exploded by 40-70% in 2 Years, Creating the “Affordability Crisis”…… ??????

Wolf then goes on to contradict the headline…..Negative real mortgage rates were not normal. They were the result of the most reckless Fed ever. They were an aberration……Home price explosions like this are not normal, they’re a result of years of reckless monetary policies.

The Fed, under Bernanke and his QE and ZIRP sowed the seeds of the Affordability Crisis. It continued through Yellen and Powell. The Fed’s negative real rates were mainly designed to help business and wall street enabling the out of control competition destroying mergers and acquisitions we also suffer from today. Then the Fed spread their gospel worldwide.

And who received a Nobel Prize for this folly? Fill in the blank. Next, a real estate developer and a lackey in control of the Fed. God save us all. Pensioners will once again have their retirements destroyed.

There are so many variables today influencing housing inflation, from tariffs to supply to massive relocation of folks from high priced markets gobbling up and inflating once lower cost housing markets, i.e. Austin promoted by the governments of the destination states. Good luck with any cure beyond a deep recession.

The vacancy rate of homes occupied by owners more than 180 days

per year is up to 1%. It was 2.8% in 2008. Rental vacation rate is 6%. It

was 11% in 2010. Total: 7%. Total vacant homes: 15 million out of US 150 million housing stocks, or about 10%, including not for rent or busted houses. It used to be 18/19 million in 2008. Data centers can collect

Airbnb and VRBO invoices. They should report their inventory in major cities. Vacant homes in Florida, Maine or AZ don’t affect rent or home price in NYC or SF. Airbnb agent’s online invoices include: sale taxes on rental including cleaning fees, guest fees, hotels fees, late charges, whatever. Data centers can prevent agents cheating. Higher taxes can reduce Airbnb and VRBO profit. Less Airbnb, more housing for sale in a dead market. Major cities should convert vacant office building for sale, rent and for the homeless. Less Airbnb, more for Hyatt and the Hilton hotels. A house rental for a family is different than renting 3/4 hotel rooms.

Think of it like this.

When people retire en’ mass their nest eggs are giving them the “buy it” itch

They are then set against other retirees in what some could term “old ppl thunder buy dome”

Costcos hurriedly spring up to hoover their dollars in exchange for carts full of happiness.

Bidding wars for homes where they relocate from a location they love and where their every thought in a day about said location occurs, However it “is too expensive… (add moaning sound)”, yet no place is as good as the place they left, especially where they moved to… Irony?

Then they too must push up the daisies (say some words). And onto the next bubble of wealth transfer/retirement

smells like stagflation to me.

What does?

the home prices. the explosion you outlined. reminds me of 70s. my brother flipped houses after his return from nam. the malaise is real out there from coast to coast. lived all over this country. it’s out of reach for young adults.

That being said great agreed however there’s a load of home sellers that didn’t get the memo and are digging their heals in on bygone era pricing. Buyers resist your broker’s advice to bid within 10% of ask if you do you’ll still be overpaying by 25%-50% in many stressed markets. Do not be an out of touch seller’s exit plan or fund their retirement facility!

What is not to love? I was raised not to be in debt as are my children! I have no need to sell anything as I own everything I have.

My kids will not sell my places as they will be no mortage rentals. Not having debt changes everything. That is the lesson people need to learn!

Debt is not a friend, it is a master.

Banks and rates are not the problem. Foolish expectation and FOMO are the problems.

I’m dreaming of a long recession, just like the ones we used to know.

Merry Xmas.

totally agree. i owned dozens of rental units in 2 and 3 family houses, all debt free. bought in 2011, sold them in 2022. i suspect i will buy some of them back in another 5 years or so. cap rates are looking decent in some places i’m poking around.

People who took on 30 year mortgage at 2 percent are doign great.

If you are financially savvy debt is a great tool to build wealth

Jon – “People who took on 30 year mortgage at 2 percent are doing great.”

People who took on 30 year mortgage at 2 percent got given a gift.

Only if the home does not lose value. Two percent may not look so good if the home loses a quarter of its value.

@Bear Hunter

True and also assuming everything else is going right. The 30-year mortgage with 2 percent interest doesn’t necessary work out very well if circumstances change, a lot of things have to stay right for 30 years for that to be a true benefit especially when the initial home price is too high. 2 percent mortgage on an overpriced principal purchase can still be a high monthly payment.

And if anything goes wrong in those 30 years, a layoff, divorce, get sick, and you’re facing foreclosure or delinquency. Having a 2 percent mortgage rate isn’t some magic shield to protect your finances from disaster if the initial price of the home already too high, it’s a big reason of that 2% mortgages aren’t a good idea either, they just spike the prices and you can’t even benefit from a re-finance down. Already we’re starting to see foreclosure spikes again and even more so delinquency rates go way up. And Americans have so much more debt now and higher prices for things like daycare, healthcare, cars, college, even groceries. And delinquencies on all kinds of debts are going way up in the US, auto repos are near all time high and private credit market is straining. Home-buyers with 2 percent mortgage aren’t immune to this either. Who even knows what’s going on with BNPL debt.

The Fed should be abolished. Price stability indeed.

How would that create ANY ‘price stability’ at all? Please do tell.

Tell me if the US had more stable prices prior to the creation of the Fed than it has after. I already know the answer.

If I were King, I would decree that the 10 year bond never is allowed below 3%. If a person loans money to others for 10 years, they should get at least 3% returns. The “free money” aspect of rates lower than this just causes bubbles and distortions like those in the article, not healthy economic growth. Nobody listens to me though, probably for a good reason.

Airbnb was a sponge that reduce vacant homes in 2008/11. It did a good job. Less Airbnb in Manhattan, LI, Queens, Bklyn, Staten Island and in NJ can reduce home prices and rent in the NY metropolitan area.

Owners collected dividends for years and benefitted from a large unrealized gains. It’s zoomers vs gen X and boomers war chest. They are good for tourists and owners, but not for young New Yorkers.

Reducing their stock is more effective than new construction.

The “drunken sailors” aren’t going to save the housing market.

Feels like if any down turn happens we won’t feel the affects like last time where short selling, getting out from under the mortgage were very common where I am at. There are a lot of people who have low mortgages or house paid off. That really hurt neighborhoods as cash buyers swooped in and turned home ownership neighborhoods into rental ones. Wouldn’t be surprised to see this on a smaller scale though although not clear investors would be rushing in with cash this time.

It doesn’t feel like the exit from this affordability crisis will be neat or clean or painless. Just hope Congress doesn’t go overboard when they likely get elected on solving various affordability issues. That would likely end even worse but at the same time “it’s the economy, stupid” or the perception of the economy that matters. After all, how many people have any interest in Venezuela? I do honestly but I think you average American tunes this out.

Housing price is not in a bubble.

The mortgage rate is not too high.

The problem of housing affordability is inflation.

Wage growth did not catch up with inflation. Years of high inflation determined the housing price, which has to catch up sooner or later. The accumulated inflation over the past 20 years is about 70 to 88%.

If you look at market like Chicago, the overall inflation and the housing price increase matched perfectly. In fact, for some areas of Chicago, the housing price inflation is between 20 to 40% over 20 years. It is very modest.

The question to ask yourself is whether your salary/wage increased 70 to 88% over the past 20 years.

That’s just another way saying the Fed completely failed in it’s duty to maintain some stability in prices as did Congress and elected officials with fiscal policy, and inflation in the US is way too high. Wage growth not going to catch up to that and it’s not clear that it can, there’s so much more global competition in many industries and the US companies can’t just arbitrary raise prices on goods or services or lose market share. Tesla is facing a 2nd straight year of declining sales for example as a different EV maker takes the crown for sales worldwide, it can’t raise prices anymore or it loses even more sales and so revenues and profits are restrained. Even darlings like Nvidia or Palantir are very constrained in how much they can raise prices, they’re already doing circular deals in the AI bubble and the ROI just isn’t there, not to mention now there are more competitors making GPU’s or TPU’s and no moat. Less and less room to raise wages across all kinds of industries.

So wage growth may never really catch up to all this inflation in the USA, unless mass currency debasement and the complete loss of the US dollar as reserve currency. Even when companies can raise wages the incomes for most workers trail those of execs in America. And wage gains even then are very uneven, it’s often easier if you switch jobs but that can carry a lot of risks and problems too when you leave a position where you’ve built up a good track record. Bernanke, Greenspan, Yellen and now Powell have planted the seeds of disaster with ZIRP, QE and loose monetary policy, we needed the discipline of a Volcker and we got a mess instead, foolishly rewarded with a Nobel Prize in economics for ruining the American economy. Something has to give, among other such things is the birth rate in the US plunging even more as young couples can’t afford homes or other costs, and soon the prices themselves will have to fall or Americans won’t be able to afford much of anything.

Housing market is ‘set to face a price correction worse than 2008’ with prices feared to drop by half in MONTHS

Housing analyst Melody Wright predicted the market could face a price correction ‘worse than 2008.’ However people have accused her of fearmongering.

Data showed that 53 percent of US homes have lost value over the past year, the highest level since 2012, when the housing crash finally hit bottom.

Wright warned that this statistic indicates the housing market is set for a price correction worse than the one in 2008 that burst the housing bubble.

‘I think we’re going to correct all the way to a point where household median income matches the home price, the median home price,’ she said.

‘So that is going to be worse than 2008. This could devolve a lot faster than last time.’

She explained that homes have lost value in 2025 since the pandemic era housing market boom because people are not buying at the same rate.

That would be great, but part of me wonders if its just the real estate industry trying to spur people to sell. House prices correcting that much would be a big part of returning to a “golden age”, along with substantially cutting debt/spending and stopping warmongering.

Booking.com, Expedia and Airbnb charge guests and owners.

Airbnb average fee is: 15%-20%, guests pay the most. Booking.com: 15% – 20%, guest pay nothing. Expedia: 15% – 30%. VRBO: 8% -15%. Expedia owns VRBO. Expedia stock (EXPE) is up from $6 in Oct 2008 to $280 in Nov 2025. Booking.com (BKNG): up from $6 in Oct 2002 to $5,840 in July 2025.

NVDA has 24 billon shares o/s. Booking. com: 32 million share o/s.

I’m not sure why high fees like this surprise people.

You’re paying for their platform and customer base. Without their service, you’d have a much harder time finding a counterparty to do business with.

It’s the same reason sales people often are the most highly paid people at companies. Because without them making sales, the company dies.

@Wolf So if you listen to some of the housing podcasts like bigger pockets, they insist that while the short term market may soften price declines are unlikely since we have a long term supply shortage due to under building from 2009-2019 which will prevent any decline.

Also if we do have a long supply issue, why don’t we ban foreign ownership and only allow citizens and green card holders to own homes? With Trumps other protectionist policies I’m not sure why that hasn’t been discussed.

Another solution would only allowing Airbnb’ing of your first and second home. This would leave houses zoned as residential for residential use…

There lots of actual solutions besides 50 yr mortgages or transferable mortgages.

I’m glad to see that there is a lot of new supply recently added and being built in Texas, though I hate how those developers bulldoze every single tree. I don’t know how that is going in other states and regions. Makes sense about the foreign ownership. I saw something about some colleges saying they need a whole lot of foreign students to stay afloat which is total nonsense considering their too expensive tuition and bloated unnecessary costs. Made me wonder, could the real estate industry start saying the same nonsense, that they need more foreign buyers? I sure hope not.

“declines are unlikely since we have a long term supply shortage…”

Do a quick search- there are 15 Million empty homes in the U.S. 15 MILLION.

The “supply shortage” is real estate industry propaganda.

However, the vacation rentals effect has been an issue in some areas with lots of tourists, such Manhattan, San Francisco, etc. We need a long decline in tourisms, including foreign tourist. And hotels need to step up and compete.

I plugged Tourists into your search function and got 119 results over 12 pages. Are you considering a “tourism bashing” exploratory topic in the future? I’m dying for some good laughs this week.

Nice to see Canadians are already on board this idea. Sure a lot of whining about it though below 49, including direct threats from Ambassador Hoekstra.

The relatively small number of investors and businesses who make their money off tourists in tourist-flooded areas whine about a decline in mass-tourism; for the rest of the population, mass-tourism raises costs, including rents and home prices, creates congestion, and produces other issues. They’re just paying the price.

Some tourism is great, if they use purpose-built lodging for tourists. But the gigantic numbers involved in today’s mass-tourism, and their large-scale shift into residential properties, are a real issue for locals. There have been numerous protests against mass-tourism in cities like Barcelona because locals have had it.

Canadians trying to sell, or selling, their homes in the US — if actually true, and I don’t know that — would be highly appreciated; it would help in making housing more affordable in places like Florida and Texas.

I feel like the change in demographics has to fit in here somehow. We have reached peak baby. I know my 20 something kid can afford a condo but isn’t buying probably because of no plans to procreate like many of their peers. Houses used to mean babies but many of my young neighbors are childless. Not sure how it all fits together. I know there isn’t much land to build where I live anymore.

Great point and we’ve absolutely been seeing this too, and the Fed’s reckless monetary policy with ZIRP and QE and then the massive overstimulus from pandemic and PPP fraud is 100% a main contributor to the total collapse in the US birth rates too. The Fed needs to wake up and channel it’s Paul Volcker and realize the monetary looseness just keeps making things worse, and something has to give. Inflation on the top of all the earlier inflation and cost-of-living hits are causing uncalculable damage to Americans of chidlbearing age, so one of the things that’s buckling is Americans ability to form a family at all.

Housing, healthcare, daycare, college, cars, care for seniors, homeowner’s insurance, property taxes, groceries, the cost of everything is pushing ever more outrageous levels. Fed easy money policy would just make this worse, the Fed put and this dumb moral hazard of favoring speculators and investors over the general population has reduced actual buying power and the real economy, all those extra dollars circulating don’t mean actual wealth, it just means all the actual goods and services people need get more expensive. And soon the end of the USD as a reserve currency as each dollar gets more worthless. The Fed should raise interest rates and do more QT as Volcker would do, and fiscal policy to match. This can’t be kicked down the road anymore and just debasing the currency, lowering interest rates and printing more dollars would be yet another example of inflation and money-printing bringing a once great power to ruin. Inflation has ended far more empires and great nations than any war ever has, now the easy money policy ever since Greenspan and Bernanke is leading the United States to the same fate. Only facing things head-on like Volcker can prevent that, it may mean a recession but at worst this would cleanse the malinvestment and insane speculation of the Everything Bubble we’re still in.

Regarding the squeeze on pro-creation, I think you can chalk it up to one item that has many facets: people are in love with themselves. Look around our society: it’s now structured for the almost perfect expression of narcissistic fantasy. Start with social media (part one), since it was the tip of the spear: the user has a well-callibrated, self-engineered market for constant validation. What’s the currency of this market? Attention. How does a rational user of these platforms select for connections (assuming the huge mass of people who are not actual “influencers”)? The amount of attention they get. How does a rational user maintain or attract connections? By doling out the same. It’s a merry-go-round of attention swapping. What to do with someone who doesn’t play by your rules? Zip. The Eastern Front. So… it’s a curated social life with no compromise or conflict… just a desperate need for validation through attention. And the young grew up with that as their social norm from the age of 13. Second comes smart phones. I was a smart guy back in the day. Tested well. Read well. Worked hard. I was respected as a knowledge resource in my social until everyone had a smart phone in their pocket. Well, now, anyone can look up something on the internet that supports their position–no matter how wrong. Adding smart phones to social media (part one), and now anyone can find a “community” of like-minded individuals in a moment to offer aid and comfort. It became almost impossible to have a productive resolution to any argument with most people. Once again, young people have had this as their norm since early adolescence. Third comes social media (part two). The second evolution of social media was all about the rise of influencer. It became a gallery where one could pick their own brightly-lit guru and follow the fads even more obsessively than kids in a junior high school. And what’s more, it became something that people internalized as “real life” and sought to demonstrate, in their own way on social media, their adherence to that lifestyle. Essentially, a lot of people mistook a fantasy-land setup as real life and have tried (and overwhelmingly failed) to remake their lives as such. It’s almost like they didn’t understand that what made the fantasy entertaining and satisfying to them as consumers was the escapism created by this yawning gap between the fantasy and their reality. Broken record here, but young people have had this as their norm since 13. Finally… the “on-demand” everything that makes people feel like “little royalty”. They never having to do anything other than tap a few buttons and have sufficient access to funds (or credit) and anything they want is soon either there or on the way. Instant streaming, Amazon, Uber, Instacart, Uber Eats, etc–everyone waits upon the “little royal” whim. Oh, and dating? Let’s combine social media (parts one and two) with this on-demand function. Presto. You don’t have to worry about being the kind of person that your friends and family would want to introduce to their acquaintances as a potential match (the old method). Nope. As a guy, you just need an attractive online persona and the basic social graces to not screw up the date before she winds up underneath you. Remember… it’s always been like this for the young. And now that you’ve constructed a perfect environment for narcissism to thrive and grow, throw in a huge societal change: women, as a whole, no longer “need a man” for economic reasons. And the widespread acceptance and utilization of reliable “family planning.” So… rationally speaking, if you value your own utility maximization as the highest expression of your existence (and really, who shouldn’t) but you grew up in the above described atmosphere with those things as your norms, is it any wonder that you would have trouble being in a long term relationship or married? And say you cleared that first hurdle and you found your keeper, why would you two then give up your precious DINK (double income, no kids) lifestyle for a lifetime of having to be inconvenienced.

I’m not saying any of the items I listed above are bad things. Intrinsically, they are not. Like guns or alcohol, they’re designed to be effective, but the trick lies in using them responsibly. And one of the best predictors of responsibility–I cannot believe I’m saying this–has a certain level of age and experience. It’s why minors cannot buy guns or alcohol in the US. Thankfully, my age cohort mostly got through college before social media (part one) struck. So… we kinda got the best of everything except the economy. And, even then, some of us did well, there, too.

Perhaps you should consider a Value Added tax, or VAT tax. It might pay down the debt. A US with less debt and a rising GDP from new business coming to the US might be able to do something about housing for the younger generation.

Resume QT, cut rates.

Problems solved.

You’re welcome.

Or even better yet, more QT with rate hikes and fiscal discipline to choke off inflation, ie. do what Volcker would do. Things are just going to continue go downhill economically in the US until the price instability and loose money disaster from COVID and before the pandemic is addressed. Everything else is just doing things at the margins.

Silver at 57+ @ moment,wonder how the cooling system at the CME is doing?

Would be hilarious if “The Chief” from Stocks & Jocks show out of Chicago has been running back-and-forth to Home Depot and Menards to fix (joke!). I will be tuning in tomorrow morning for an update at 6. Whenever he talks about “getting his people into Au and Ag” he means paper / ETFs.

So, the solution entails lots and lots of pain and turmoil. Once the pie is baked, there’s no going back! Once the bubble is inflated, the chaos is unavoidable.

Soft landing which entails slowly deflating home prices and rising wages? Doubtful – that would also cause significant inflation for all goods and services, hammering consumers even harder – possible depression territory.

I’m not hoping for a hard landing, but I think that this Housing FrankenMonster will cause a lot of turmoil before the party is over. Remember – real wealth isn’t destroyed, it only gets transferred from one party to another. But certainly these fantasy valuations are going by the wayside.

.

He’s right. QE and ZIRP made housing prices go crazy. Now mortgage rates are normal and home sellers don’t want to let go of their extra $200k+ in value they don’t really have. If I look at how long it took to work out the last fed induced explosion of a fed induced housing bubble and apply it to this, house prices will bottom in 2026.

I agree with your assessment that this can be fixed with rising wages and falling home prices over many years, but I disagree this would ever happen. Americans are NOT patient, and need bubbles burst before they see the light.

The issue with rising wages is the enormous pressure put on companies to contain costs. It’s not that there isn’t overhead for higher wages, it’s that investors hate increased wages even more than Americans hate inflation and higher prices. A C-Suite that can’t keep wage growth under control is a C-Suite that’s out of a job soon.

Where it all gets interesting is when you factor AI into the equation. All the excitement around AI is hope that it will reduce headcount and make the remaining people super productive – which it may well do. But, the more lackluster performers you push out of the workforce, the fewer people who can afford rents and car payments. Long term, that underclass builds to a size capable of voting themselves a new set of politicians.

That all may happen in time for 2028. The current administration was brought to power on the back of a revolution, so too, will the next administration — but a very different type of revolution.

Austin, Tx, “ home prices exploded by 207%, from $225,000 to $690,000”.

So a cash out refinance can get a drunken sailor maybe $150,000.

They could do that through mid-2022. Since then, they couldn’t do that because the refi would have doubled the mortgage rate and the equity to be cashed out has been evaporating.

Generation of young people are buying Risk trading vehicles instead of homes. Housing market doesn’t wake up to a stop loss waterfall event on Monday morning. It’s going to be interesting to see how many people have stop losses on their crypto etf, we could get a proper crypto crash this morning. We will find out in 60 minutes

BTCUSD -6.71%

There seems to be some support around $80k. If it falls through that it’s in the $60ks. And if it breaks $60k then the next level looks like $30k. One can hope…..

As someone with an accounting and finance background this has been the hardest bubble of all to watch since crypto literally has no actual value – but enough propaganda, hype and this is how you get rich FOMO and every non financially educated gen Z person jumps on board. They literally taught us about this in school the psychology of market bubbles – driven by FOMO.

Crypto is just gambling for young people. Instead of blowing their cash in Las Vegas like their parents, they blow it on Crypto. Same underlying thing going on. At least with Vegas you have a hangover and some compromising photos for your trouble.

I know for sure that there is a huge amount of support at $0, according to my technical analysis. Bitcoin will not fall below $0.

A handful of people paid 2032+ prices in 2022 and the whole market thought that “equity” was real. Prices falling 5% a year with inflation at 3-4% takes care of overvaluation real fast. It’s happening, the market is working itself out.

With the ten year pretty much stuck at 4% mortgages should level out at 5.5-6% based on the historical spread?

Why do think mortgage rates will go down? I got the 10 year hitting 5.3% in 2026. The 10 year has been at 4% plus or minus 150 basis points for less 3% of the days in 2025, I am guessing by looking at the charts I didn’t actually count days and do math. But not many.

Just curious about your thesis. FYI, I got unemployment claims going to 211k plus or minus 1k this week. So that helps explains my thesis. The trend is down with weekly claims.

Thanks :)

Typo~30% not 3% for clarification, :)

thanks Wolf looking forward to your Canadian housing update specifically major metro areas

Thanks

James

“Now CPI inflation is over 3%, the worst since May 2024, after having accelerated for months. Higher inflation also seems to be the new normal, as the Fed has been cutting its policy rates, and has been discussing further cuts, despite this inflation, and if it continues to cut, it would be an indication that the Fed is going to tolerate higher inflation over the longer term, that it’s comfortable with maybe 3% to 4% inflation. ”

This is the most interesting paragraph of this post. Is the unstated FED policy to inflate away the national debt?

“Is the unstated FED policy to inflate away the national debt?”

LOL! Have you been living under a rock for 50+ years? Yes. Moreover, the Fed has no choice if CONgress isn’t going to balance the budget and cover spending with revenue. Duh.

Yes and the Fed is delusional if they think this could work. The fantasy of trying to inflate away the US debt just means costs for government spending also go up with the inflation and the deficit jumps even more, so we’re stuck with an ever higher national debt but with higher inflation and an angrier populous. The US birth rate falls even faster and fertility rates collapse even harder in the states with unaffordable housing and worse inflation, more schools and colleges close. As housing, healthcare and daycare get even more outrageously expensive, more American couples are priced out of starting families, then more American cities and especially rural areas become ghost towns and the rust belt then stretches across the whole country. It’s what the economics classes always teach us, this is how inflation brings down empires and once great countries.

And the US dollar losing reserve currency status even faster that makes inflation even worse and crushes the US economy even worse, and things in America get even more unaffordable. All these dumb distortions in the Everything Bubble, from the housing bubble and AI bubble and cryptocurrency bubble, all resulting from this too. This also just leads to the incumbent parties in power getting demolished in an ever uglier landslides due to anger about the cost-of-living troubles and crisis with things getting even more unaffordable, we got taste of this in the elections in November in 2025. Inflating away the US debt is not going to happen for all kinds of structural reasons. Just attempting it will break the US economy. The QE, ZIRP and COVID stimulus easy money era was always going to create a nasty bill has to be paid, and it can’t be inflated away. Taxing the billionaires more can bring in some more revenue but the deficit just keeps surging more and more even with the tariff revenue. Nor can the date of reckoning postponed much longer.

Pointless ramble. Yes, fiat currencies and reserve status comes and goes, so what? Try to be a useful engine, teach your children well, and hedge accordingly.

I thought that was obvious during QE1. Surprisingly, QE1 didn’t do as much of it as expected because everyone rushed their money to USD since the rest of the world went to shit too.

I know QE is largely derided here for good reason, but QE1 after 2008 was the right play in hindsight. The US was largely on the way down compared to Europe, and came out ahead when comparing US QE to EU austerity. The problem came when QE was then seen as a future solution when it was actually just a lucky draw.

I agree. The purpose of QE is not just to help the housing market, but also businesses and consumers to lessen the effects of a recession. We shouldn’t look at QE from just a housing market perspective. In 2021-2023, housing bubble was collateral damage.