The deficit doubled, as benefit payments spiked in part due to the expansion of Social Security, while income rose only slowly.

By Wolf Richter for WOLF STREET.

The new thing this year for the “Old-Age and Survivors Insurance (OASI) Trust Fund,” commonly called the Social Security Trust Fund, was the Social Security Fairness Act, signed into law on January 5, 2025, by President Biden. It expanded benefits to certain groups of retirees with careers in government, education, and law enforcement that are already covered under public pension plans.

The Act ended the Windfall Elimination Provision and the Government Pension Offset, which had reduced Social Security benefits for certain people who also received a public pension.

Retroactive benefit payments started going out in February 2025, and surged out in March, and benefit payments in March spiked by 13.5% from February, and by 20.2% year-over-year, to $130 billion for just March, a massive record. Those were just the retroactive catch-up payments. The regular monthly benefit payments also increased under the Act.

But the Act did not provide for any additional revenues or other tweaks. In addition, the growth of contributions slowed sharply as the labor market has been growing more slowly. And so, with income barely rising (blue in the chart), and outgo surging (red), the Social Security deficit doubled this fiscal year to $181 billion, according to the Social Security’s fiscal year income and outgo data, released today.

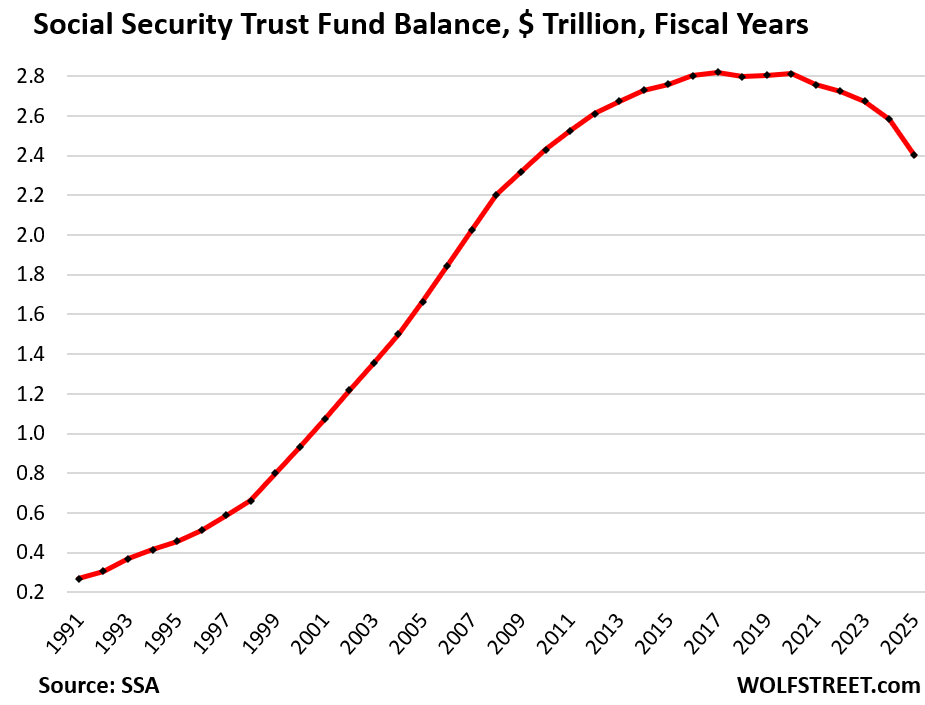

When the total income (blue) was above the total outgo (red), the Trust Fund ran a surplus which caused assets to accumulate and the Trust Fund to grow. When the red line rose above the blue line – this happened for the first time in 2018 – the Trust Fund ran a deficit and its assets shrank.

Congress needs to get serious about tweaking various aspects of Social Security, but this time to improve the financial aspects of the system, and not to make them worse, as it had done in January.

These figures do not include the Disability Insurance Trust Fund, which by law is a separate entity from the OASI Trust Fund, and is not part of this discussion here.

Total outgo (red line in the chart above) spiked by $117.2 billion in the fiscal year through September 30, or by 9.0%, to a record $1.42 trillion.

By category of outgo:

- Benefit payments spiked by $117.4 billion (+9.1%), to $1.41 trillion, attributable to more retirees drawing benefits, including through the Social Security Fairness Act, and to Cost of Living Adjustments (COLAs).

- Administrative expenses fell by $300 million to $4.5 billion (0.19% of the Trust Fund balance, 0.36% of total income).

- Transfer to Railroad Retirement Program rose by $100 million to $6.0 billion

Total income (blue line in the chart above) rose by only $27 billion (+2.3%) in the fiscal year ended September 30, to a record $1.24 trillion.

By category of income:

- Contributions rose by only $21 billion (+1.9%), to $1.12 trillion. The slow increase was due to much slower labor market growth.

- Taxation of benefits rose by $5.1 billion, or by 9.6%, to $58.2 billion.

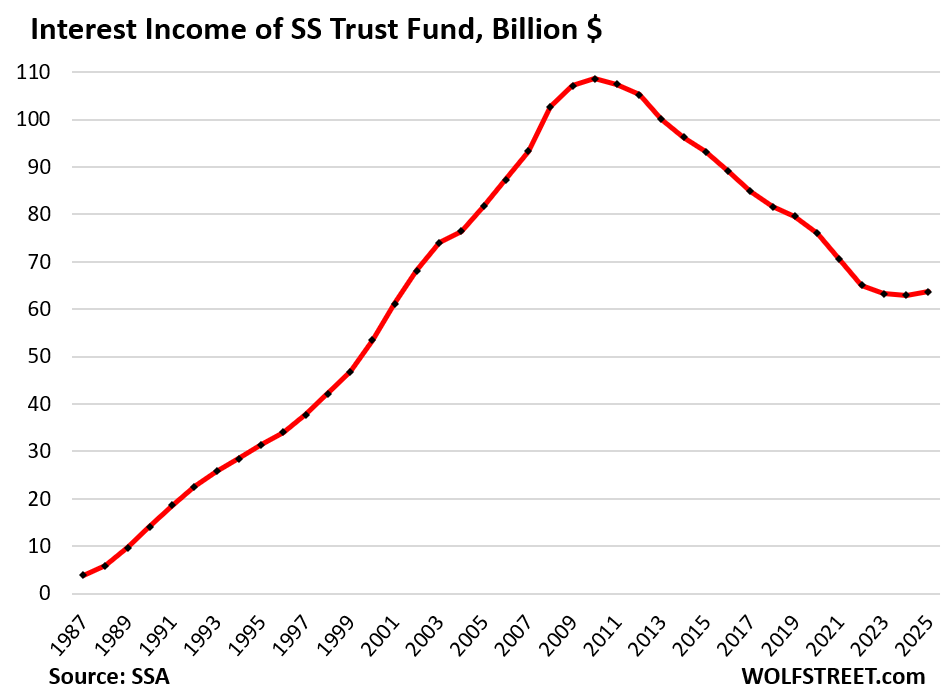

- Interest income from the securities in the Trust Fund ticked up by 1.4% to $63.7 billion, on higher interest rates earned by the Trust Fund’s securities.

This first increase in interest income came after 14 years of declines that ravaged the fund though its balance ballooned through 2017. The Fed’s reckless interest rate repression (QE and ZIRP) from 2008 to 2022 is responsible for the plunge in interest income.

Social Security is not part of the general budget. Its surpluses through 2017 didn’t reduce the general budget deficits; and now its deficits do not increase the general budget deficits. And its surpluses and deficits have no impact on the size of the US debt. The Trust Fund doesn’t have debt and doesn’t borrow funds. It invests funds into US debt. It’s an investor, not a borrower. Cutting benefits will not reduce the general budget deficit nor the debt.

But the system needs to be tweaked in several ways to accommodate demographic changes, just like it was tweaked under Reagan last time.

The Social Security Trust Fund.

With spiking outgo and only slowly rising income, the deficit in the fiscal year doubled to $181 billion, from $91 billion in the prior fiscal year, the biggest deficit yet, and the fifth year in a row of deficits.

Over the past 36 years, 30 years had surpluses, totaling $2.6 trillion, which accumulated in the Trust Fund. Six years had deficits (2018, 2021, 2022, 2023, 2024, and 2025), totaling $429 billion, which reduced the Trust Fund.

The shortage between income and outgo is paid out of the Trust Fund, and in the fiscal year, the Trust Fund balance declined by the amount of the deficit, by $181 billion, or by 7.0%, to $2.40 trillion.

How the Trust Fund invests the $2.4 trillion.

The Trust Fund’s total assets of $2.40 trillion at the end of the fiscal year was split up between $2.23 trillion in interest-bearing special-issue Treasury securities and $172 billion in short-term cash-management securities (“certificates of indebtedness”) at the end of the fiscal year.

Similar to the Treasury I bonds and EE savings bonds that retail investors hold in their accounts at TreasuryDirect, these securities are not traded in the secondary market, and are not subject to the whims of the secondary market; so the value of these securities doesn’t fluctuate with the day-to-day prices in the secondary market.

The Trust Fund gets paid face value when its Treasury securities are redeemed. Day-to-day price fluctuations are irrelevant for the Trust Fund.

Investing in Treasury securities when they’re issued and holding them until maturity is a low-risk conservative investment strategy. But the Fed’s reckless interest rate repression from 2008 to 2022 crushed the cashflow from this investment strategy.

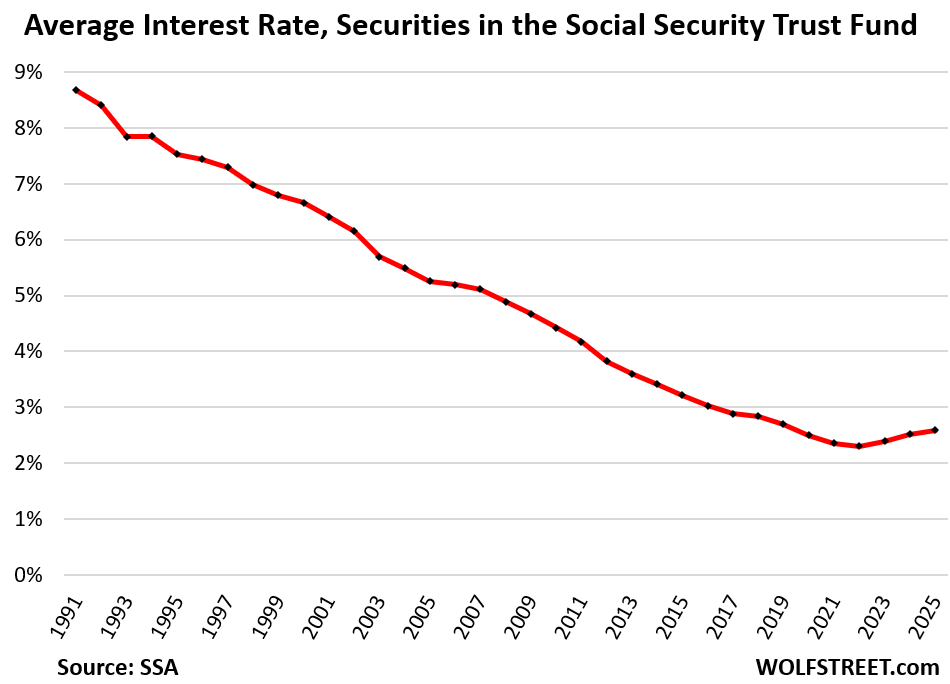

The average interest rate ticks up. The low-interest-rate securities from the QE and ZIRP era are maturing piece by piece and are being replaced with higher-interest rate securities with shorter maturities, which pushed up the average interest rate earned by the Trust Fund to 2.6%, the third year in a row of increases, after several decades of declines, but still woefully low.

For example, this fiscal year: If the Trust Fund had earned an average of 4.1% on its Treasury securities, instead of 2.6%, it would have earned $94 billion in interest income, instead of $64 billion. In the prior fiscal year, the deficit would have been one-third lower. Two fiscal years ago, it would have had a surplus.

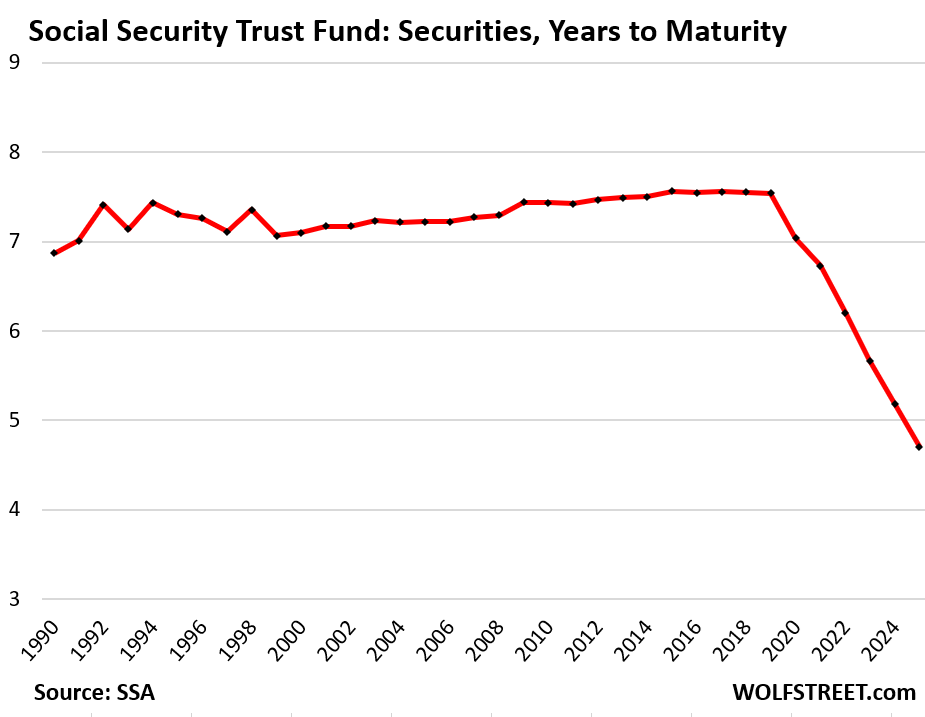

Shifting to shorter-term securities. The average number of years to maturity used to be around 7 to 7.5 years. But in 2020 it began to drop, likely a strategic decision by the SSA to not load up on the 0.5% longer-term securities issued at the time.

In the fiscal year through September, the average years to maturity declined to 4.7 years, the shortest on record.

Tweaking OASI is necessary. Various proposals have been floated in Congress over the years to tweak the system, but they have persistently gone nowhere. The only Act that was actually passed was the Social Security Fairness Act in January, which made the situation worse.

Generally, each proposal tweaks the system in several ways, and each tweak could be relatively small, but combined and over time, they’ll make a difference. It was done before under Reagan when the young boomers were told to retire later, and pay more for longer into the system. These reforms created the surpluses that caused the Trust Fund balance to rise from near nothing in the 1980s to $2.82 trillion by 2017. And it can be done again.

If no changes are made to the plan, if Congress doesn’t get its act together, the Trust Fund will be depleted in the early 2030s, and at that point, without adjustments till then, either the benefits would need to be trimmed to match the Trust Fund’s income on an annual basis, or the general budget would be used to make up the difference.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This is awful Wolf…another thorn in America’s sound, responsible, ethical management systems. Doesn’t Good Judgement ever triumph over Reelection Prospects…ever!!!…PJS

Rarely. Maybe never.

Pete,

Good things and elections can go hand in hand. After all, The New Deal was really about getting the votes, even though it resulted in some good programs. We just need people to be smart enough to vote that way, which is likely a never situation!

People are generally as smart or as dumb as we’ve always been. However, we no longer have a Walter Cronkite to educate us, the electorate.

We have Rachel Maddow, Tucker Carlson, Brian Kilmeade, Joe Rogan etc, so god help us all.

Walter Cronkite et sl didn’t prevent the situation the OASI finds itself in, they helped enable it.

Big government policies can’t compensate for bad parents; they only create more.

We have met the enemy; they are us.

The media has always been propaganda and always will be.

Walter Chronkite was an avowed socialist.

There was a brief era in the 50s-70s when you could say they at least tried to do the right thing.

But it’s looking like that was a rare exception rather than a new norm. And so we return to the “yellow journalism” age of the early 20th century.

Point being, that at least back then one tried to present the news in a calm, more or less objective, manner.

Doesn’t Good Judgement ever triumph over Reelection Prospects…ever!!!”

Not for decade after horrible decade.

And it isn’t that some people weren’t warning about this for decade after horrible decade.

But those in control always had a handy lie, a friendly pre-internet media to distribute the lies and smother debate by ignoring it, and an agends that placed America’s long term economic health towards the bottom of their priorities list.

Interesting connection to your previous post on fed rates. Perhaps some motivation for higher long-term rates is to shore up the Trust Fund a bit.

We could eliminate the income cap and tax all income,e, instead of the first 150k-ish. That would be a dramatic lift.

We could also treat capital gains as income, and apply social security tax to that as well.

Finally, we could also eliminate the congressional pension, converting their current pensions to 401ks, and I bet Social Security would be saved within 10 minutes.

Social Security tax limits are capped because BENEFITS ARE CAPPED at a certain maximum level, and Social Security is NOT A TAX but rather is an insurance based benefit program designed to deliver only a maximum amount of benefits to any recipient.

it was designed as insurance. for living too long. it has morphed into a retirement plan. the cost / benefit is pretty good for lower income folks. has been great for myself. i paid myself a small salary for decades. an IRS agent actually advised me, decades ago. ironic. and true.

Capitalism is at risk with extreme wealth inequality and allowing crony capitalism to flourish . I imagine the SS cap will be taken off or the carry interest that benefits PE and hedge fund will be taken away with the next administration. On another note SPY 641, tomorrow? Wealth inequality will shrink up quickly. The popular vote always will depend on “ It’s the economy, stupid” from 1992 James Carville. Looking for spy 641 tomorrow is a 3.4% drop from now and if that falls than panic!! The levee may break with BTC tomorrow.

As well, due to “bend points”, those who contributed the most typically get substantially smaller benefits per dollar they and their employer contributed than lower income individuals do. Roughly speaking, the first dollar put in yields six times the benefit of the last dollar “contributed” just before the cap (it’s more complicated than that due to uneven income over working careers etc…).

Also, the lowest income recipients of Social Security benefits pay NO income tax on their benefits (even though the half of contributions paid by the employer were never taxed as they were a business expense) while higher income recipients pay federal income tax on up to 85% of their benefits.

It’s a fairly politically progressive system already.

“an insurance based benefit program”

Yes, an insurance program against impoverishment of the elderly. Remember the context coming off the great depression and no one wanted cities filled with begging grannies.

There are many simple tweaks to the funding that can balance the flows:

1) Raise cap on earnings taxable, perhaps taxing the higher tranches of income at lower rates.

2) Change what kinds of income are taxable–expand to investment income.

3) Increase the number of years included in the average wage calculation. Increasing from 35 to 40 makes sense as people live/work longer.

4) Increase the social security tax rate. 6.2% from each of the employer and employee are low compared to international standards. The EU country I live in just raised from 8% to 8.5% to address funding shortfalls. Can be progressive tax based on level of income.

5) Increase returns by moving trust funds to 401k-style program. Bush the younger was an advocate and Singapore successfully runs a system pretty similar to this.

6) Reduce eligibility by eliminating certain claimants, such as spouses and divorced spouses.

7) Reduce eligibility by increasing the required number of contribution years from current 10.

The list goes on but all of these would have a material impact and are not on their face revolutionary.

Another issue is that in 1985 89% of earnings were subject to the SS tax. By 2023 that figure declined to 83%. Adjusting the taxable maximum to 90% of benefits would eliminate 24% of the long range shortfall.

FDR designed SS to have income limits for practical political reasons. He knew the wealthy would attack it as a welfare program if money was taken from them and given to regular working folks. He knew the system would never survive those attacks, so he excluded the very wealthy from contributing to or receiving benefits from SS. And the wealthy probably have even more political power today than they did in the 1930s.

Educated.

I did not realize that Social Security was not part of the general budget.

Probably should have know though !

When the adults were left in the room in the mid 80s, they did a responsible solution for all this stuff, including a tax reform that was essentially a tax increase, and delaying retirement for Gen X and late boomers. Without some of the stupidity that was done regarding benefits, it would remain solvent. The gummint double tax is finally being rectified, as no new plan members were allowed in the old closed systems after 1990 or so.

No adults now, so no solution until this administration is gone and a real accounting shows it benefits most of America. Which requires honest math, not fiction. The two deficits of social security and the us government require a real solution. The last one made 40 years. The next one should as well.

Or into the abyss we go. RED or BLUE we are all in this together, unless Peter Thiel is going to let you into his bunker.

“…so no solution until this administration is gone”

Pretty myopic assertion to something that’s been a problem for decades through multiple administrations. Stop blaming the other side.

Between the citizens united ruling and the money laundering politician self enriching going on from the bottomless taxpayer debt bucket our governmental system is completely broken.

Lindsey Graham just proved that no Bill gets passed without some self enrichment in it. Congress could have increased the penalties for spying on politicians. Instead they just allowed politicians to sue and make money from the illegal activity.

Nothing gets fixed while politicians are elected from deep pockets instead of your and my vote.

I’m confused. We blame the politicians for the lack of problem solving, we blame deep pockets funding political campaigns, HOWEVER, IT IS YOUR VOTE, that elects these politicians. I know I wasn’t paid, so the problem lies with US, THE ELECTORATE. We need to educate ourselves, have introspection, and vote them out for not doing the job! WE, THE PEOPLE , are to blame. We are as greedy and selfish as the people we elect!

It doesn’t matter who you vote for, the Golden Goose is what they all (politicians) are after, regardless of which side of the fence they are on.

Candyman: You took the bait!

The “semantic difference” is actually the REAL difference.

In a Democracy, the “electorate” matters. In a representative republic (like the USA) the electoral college matters.

This actually is fairly irrelevant, because of the process of getting a name on the ballot (bored/ retired people in Iowa seem to have the biggest sway here?).

The BAIT is: YOU, citizen, Have a Voice!

The Fact is: The system deemed long ago that you’re too dumb to decide, BUT for the sake of civility we encourage you to participate in the elephant and donkey show.

(And by “civility” I mean: you will blame, back bite and infight amongst yourselves, rather than uprising against the System).

I have less of a voice in the corporations than corporations have a voice in the politiks.

I won’t even address the gerrymandering, cronyism or the relative “market cap” of the corporate vs. government (and other bedtime stories).

I am sorry, but which side is going to save the social savings program? Is it the Center right Donkeys, or the Reactionary Elephants?

The fund could easily be secured simply by removing the income cap on payroll taxes. Social security payments could also be means tested. After all, millionaires and billionaires probably don’t need these payments.

We could also add a payroll like tax on capital gains since those who own the vast majority of capital don’t have much in the way of taxable income.

But I know, this all smells like socialism which, in the USA, is something only reserved for the wealthy and for large corporations. Anything else risks the American people getting the erroneous impression that government can benefit the common man instead of only the wealthy.

The benefits to the ones who need them least, supported by the ones who can afford it least!

Sounds like our GubMint. Sounds like the adjustment they already made, in that they fully pay folks who already have a true pension?

Today, those folks paid into both, there are very few jobs that are not covered by social security. So, one should not get any benefits of having paid for both for decades? It was meant for those who got RR or public sector benefits and did not pay social security.

That’s the deal made in 1986 that got stale.

The part that is crazy is that it bought decades of relative stability in retirement for everyone.

Ahh well, the rich have won, everyone will just have to move somewhere cheaper to retire…

Not sure I understand your comment. Are you saying public sector employees who don’t pay into SS, but still get public pension, should qualify for SS? I know a few MASS. STATE employees, who do not contribute to SS, and are NOT qualified to receive SS benefits. They receive a state pension. Also, why is everyone so hateful of the wealthy? Aren’t you here to learn how systems work and apply that knowledge to BECOME WEALTHIER? Do you really hate yourself? Are you envious? (Envy, one of seven deadly sins!)

Candyman. Public sector who paid into both were being penalized. Read what I said.

I worked public sector, and had both pension and social security withheld for decades. Understand? Like 20% of my check for years?

Now when I file, I won’t get penalized for it.

@Candyman

The issue that the now-eliminated windfall prevention program (wep) was designed to address is workers who were in public service for the majority of their career (let’s say a 20-year serving member of the military), but who then who additionally work in the private sector for an additional decade or two.

Since social security is very progressive (and much better designed in this sense than many other old age pension systems around the world), if you use the underlying math in this scenario (high income over a short Ss-eligible working career), you will look on paper like a poor person and be rewarded by a relatively large social security payment (a windfall).

I am working with someone in this exact situation now–retired military who makes six-figures and will get both his military pension and a (relatively) large social security check.

I am currently executing a similar strategy by participating in the pension system of many countries, and getting a relatively high yield on my contributions by relying on the progressivity inbuilt in each system.

The impact of WEP elimination will decline over time as most govt jobs now are SS-eligible, but it was a really unjust decision to repeal it and giveaway from the party of the govt to govt workers.

Uhh ?????? Raising the income limits upon the billionaires = taxing those who can’t afford to pay taxes? And giving those funds to you and me = giving to those who need them least? What planet do you live on?

Simple solutions are often not when you apply any amount of thought. If you uncap deductions then it just becomes a tax (which was explicitly against the original principles and is what made it a successful program) the idea is you pay in and you get it back. Your benefits are capped because your deductions are too. A possible solution along the lines of what you say is to create a donut hole- so wages are taxed up to the calculated amount (which changes every year) and then retaxed at 2x that amount with a reduced benefit – from those contributions of perhaps 75%. So you accrue 25% of this group of wages to support the total fund.

OR you could just normalize interest rates and fiscal policy so social security earns a normal rate on the treasuries and then there isn’t a problem for another 30 years…..

Then you’re changing it from an old age insurance program to a welfare program. At least be honest about that.

Government benefits government. You hope government benefits Americans That is what gets them elected, hope.

We could of course do that. But since one’s SS benefits are a (nonlinear) function of one’s contributions, that would create yet more outrage as very wealthy people get million dollar “checks” each month from Social Security.

If we eliminate the feature that contributions and benefits are correlated, it becomes, and becomes correctly viewed as, just a welfare program. Welfare programs are not very politically popular and are subject to “welfare reform” as the political pendulum swings to and fro.

The federal government is not, IMHO, there to help individuals by redistributing wealth – it is there to perform critical national functions such as national security that benefit all and which are not possible for individuals to provide for themselves as they lack the authority or means to do so.

But, if one wants an expanded federal welfare program, it seems dishonest to do it through the Social Security Old Age and Disability Insurance programs which were established for other purposes and have been maintained under that banner for as long as 90 years.

“The only Act that was actually passed was the Social Security Fairness Act in January, which made the situation worse.“

Seems like the “new normal” for legislative action/ especially fiscal and monetary?

“The Fed’s reckless interest rate repression (QE and ZIRP) from 2008 to 2022 is responsible for the plunge in interest income.”

Crush the systems income, then expand the beneficiary pool into gov’t that never paid a dime into the system.

What deep state? What inflation? Anybody who thinks Clowngress will go after the billionaires be trippin’. Those of you in the $2,000,000 – $30,000,000 net worth better find a quick place to hide. Easy pickings.

Another consequence of bailing out the

big banks in 2008 instead of jail time

for them. Basically a wealth transfer from the workers to the bankers which

is still ongoing. And to think Bernanke

got a Nobel prize for his part in the

fiasco.

The average interest rate on the SS Fund’s securities is now less than the rate of inflation. Previous years (before 2020), the SS Fund’s interest rate was much higher than inflation. Looks like the fund will be burning through money a getting a negative real rate of return at least in the short term (few months) and have been the past four years or so.

I do not understand why benefits can’t be cut, particularly for those making >$100k in income per year. Even just a 5% haircut would help the fund. As someone less than 30 years old, I would appreciate being able to someday collect from the fund I’m paying into.

And as someone older than 66 I’d like to be able to at least get out of SS what I already put in. Congress has known for decades that it needed fixing and they kicked the can down the road. If I were a politician I’d likely do the same.

Prior to the change in 1984 oasi was a safety net at less than 3% tax. After 1984 they took an additional 9% of my pay. They’ll claim that the employer paid half but I’ll argue that was the start of decreased pay raises that did not keep up with inflation. By the way 401ks were replacing pensions. Just imagine what my 401k would have done if it had that 9%.

So now in retirement social security is part of my two-legged stool, no pension income.

Through financial planning the Roth account has grown and the income is tax-free. So your attempt to reduce social security income for high income earners (>100k) will not work across the board unless there’s an actual net worth evaluation.

I would argue that social security is a forced retirement 401K/annuity equivalent and therefore should continue to be self-funded by an increase in the social security tax rate phased in slowly maybe 0.2% per year for 10 years

I agree the income cap on SS needs to go. It is not right that the poorer you are, the more you pay into it proportionally.

As a woman who has dual entitlement I got royally screwed. I am entitled to my own benefit or half of my spouses, whichever is more, but woman land up getting a lot less of both their own or their spouses if they retire early. Because I worked I got penalized, both my own benefit and my spousal benefit got reduced even though we contributed more to the system than a couple with a non working spouse. I should be able to switch between the two benefits because together we paid in more, but I only get mine and lose access to my husbands benefit which is higher.

However, my biggest complaint is the number of people who never contributed at all, immigrants right off the boat that collect SSI. I lived next door to a couple whose mom was brought from China to babysit their children and she received SSI while I was denied disabilty when I needed it and had to sell my house because of it. Guess who bought the house, you can’t make this shit up.

“I agree the income cap on SS needs to go. It is not right that the poorer you are, the more you pay into it proportionally.”

Technically, the opposite is true. SS was not supposed to be a welfare program, it was intended to act more like a forced savings program. When you contribute to SS, the contribution benefit is progressive, meaning you get a high replacement rate (90%) for the first portion of earnings, a lower rate (32%) for the middle portion, and the lowest rate (15%) for the highest portion. Everyone who meets the criteria for SS gets a benefit, with the lowest income earners getting a benefit that is proportionately higher (relative to contributions) than higher income earners. The contributions are capped because the benefits are capped.

If the income cap is removed, then SS will function as a welfare program unless the benefit cap is also removed.

ChS,

Lower earners get a higher benefit from the base layer of earnings because there may not be a middle or higher tier for them. Whatever slightly higher benefit they get on the base, it is wiped out by Medicare Part B, which is the same for them as for higher earners(non erma). Part D is mandatory as well, so there’s that cost as well.

Petunia,

“Part D is mandatory as well, so there’s that cost as well.”

No, it’s not mandatory, it’s optional (drug coverage), provided by private insurance companies.

Not even Part B is mandatory; it’s optional. But most people take it.

Part A is free (you already paid for it with your payroll taxes).

SSI is not funded by the Social Security Trust Funds. It is administered by the Social Security Administration for convenience, but the SSA is reimbursed (including administrative expenses) from the general fund. Therefore, that point is irrelevant.

As well, women and men are not treated differently by Social Security except to the extent that a particular heterosexual couple has _decided_ that the male will work and female will not. In that case, the women wins big as she gets the spousal benefit on her husband’s earning record but if her husband had not married anyone, he would have still contributed the same amount but, in the end, his household would end up receiving about 1/3 small benefits than if he had married. Of course, if the couple had decided that the male would not work and the female would, the situation is reversed.

And, since women live longer, they tend to collect benefits for longer than men so take relatively more from the SS trust fund even though contributions are independent of gender.

Where you say “Interest income from the securities in the Trust Fund ticked up by 1.4% to $63.7 trillion”, you mean “billion”. It would be nice if it were trillion.

Not really, as we would be living in the Weimar Republic then…

Want to lose your cushy job as a Congressman? Let Social Security benefits be automatically cut for 10s of millions of elderly voters.

Not only lose their job (if you can call it a job), but they better not be seen in public going forward!

The voters, including the elderly ones, have been unknowingly voting for the possibility of benefit cuts by voting for the Republicans and Democrats who appoint the Fed who carried out the QE that resulted in interest rates on the trust fund bonds being too low to account for inflation. If people don’t want their SS cut, they should be voting for fiscal responsibility, but very few are paying attention to the details.

Getting rid of the windfall elimination provision was idiotic. People with the public pensions exempt from social security often got more than anyone with a SS pension would get. And the “other income” that was adjusted down was usually a part-time job after retirement from the job that had an exempt pension.

It was a gift to people like cops or teachers who picked up part-time jobs in the private sector after retirement.

So your comment and what I’m about to say is why this country is broken and I don’t know what the solution is.

I support president Trump. I’m glad he’s our president. I like what he’s doing. He was wrongly persecuted as were his supporters for many years. I don’t think he’s moving fast enough or putting the right people in positions because we still have a department of education and we still have a corrupt FBI.

Oh by the way I despise the GOP because they’re just the other side of the same uni-party coin. Politicians on both sides of the aisle are there for power and to self enrich.

Just amazing how we can look at the same thing and see the complete opposite.

Redsetter/well said.

“Politicians on both sides of the aisle are there for power and to self enrich”

“I support president Trump. I’m glad he’s our president. I like what he’s doing.”

Just informing you from the other side of the ocean & with no skin in the game: this right there is the problem. These two statements should cause huge cognitive dissonance, but they clearly do not. All politicians are bad, but Trump is good. That’s some proper 1984 doublethink.

If you are really interested in finding a root-cause and a solution, I’d recommend looking up how much $ is spend on political campaigns in different western countries (relative to size). That dissonance that should be there, has been forcefully bashed out of Americans for decades. If some dictator who controls the media does it, we call it propaganda and indoctrination. If a small group of oligarchs do it, we call it superpacks and political advertising.

If government insider trading was used for the trust assets we would all be getting HUGE benefit checks. Wait only politicians can do that.

Richard, look at the very first graph again. How could SS possibly have been bankrupt in 2008? Income exceeded expenses. That’s a surplus—not a bankruptcy. What am I missing?

Richard and others, forgive me. I re-looked at the first two graphs and understand what your point is now. Yes, it seems approximately after 2008, total SS Fund income minus interest income is less than total expenses. So, in other words, the interest income on the SS Fund is what kept the SS Fund in the black since approximately 2008.

With the drop in interest income since 2010-ish, compounded by ZIRP, the SS Fund will be hurting for cash and continue to run an ever-increasing deficit unless something is done.

Social Security was a poorly designed program in that it never imagined the future American demographics or allowed it to be like “insurance,” thus offering no real death benefit (passing on contributions to future generations).

Maybe it is time to revisit the program?

“thus offering no real death benefit”

SS pays “survivor benefits” to spouse and kids when the SS beneficiary dies.

I never thought the Fairness Act would pass as every year I would hear stories that this time it was going to pass. The majority of people didn’t care that we public sector employees were being penalized for having a government pension. I think that the democrats passed the bill with help from some republicans to stick it to incoming president Trump. Now it’s Trumps problem to figure out what to do.

The previous system made some sense actually. Social security is an income replacement program (meaning, it’s supposed to replace a certain portion of one’s total income, going progressively replacing more of one’s lower income than their higher income). As such, it actually made sense to reduce payments for public sector employees with non-FICA earnings.

What they should have done though is instead of lifting the WEP altogether as they did, they should have introduced a computer-based exact calculation that would have taken into account actual not-subject-to FICA lifetime wages when calculating the the income replacement amount for a given retiree such that public sector employees weren’t overly ‘dinged’ by the WEF, but at the same time didn’t receive an overly generous SS benefit because SS wouldn’t be considering their non-subject-to-FICA when figuring out what percentage of their pre-retirement income should be “replaced” by social security benefits.

Alas, it is a death sentence politically speaking for anybody who wants to raise the retirement age or reduce benefits.Our politicians will continue to kick the can down the road until they are forced to do something.

Loved “death sentence.” How true. That’s why you have to disguise whatever tweaks you propose.

Otherwise, more ads of Grandpa and Grandma being pushed over the cliff in their wheelchairs (this time AI generated ads.)

With one major buyer of government debt disappearing as the fund sells off its remaining 2.4 trillion over the next decade, who will step in to buy it? My guess is that new round of QE will arrive before the fund is fully depleted.

SS Trust is down 15% from $2.8T to $2.4T. The high tech sector is booming, but a large portion of the economy is struggling. Aramco extracts NG from unconventional gas field for electricity. Excess oil will further deflate oil price. The RE sector is doing nothing all day. New Immigrants driving trucks competed with traditional shippers. They are hurting them/ killing people. Within a few years AI will spread deflation to other sectors. It will filter unqualified truck drivers and make home prices more affordable. Trillions of new orders and unrealized promises to buy and invest will create a boom in aviation, the ship buildings, the military, healthcare self driving cabs and to other sectors. Demand for highly skilled and skilled workers will rise. The SS Trust might rise to $3.5T/$4T, after further dropping, possibly to $2.2T.

…wtf did I just read?

I see AI services as deflationary, open AI revenue is 13b, deepseek can provide near identical service at 70 to 80% less cost and it’s open source vs proprietary. Chinese are always exporting deflation. AI will displace workers but it’s going to be hard to pay off the debt incurred to hyper scale. Don’t rule out deepseek at keeping the revenue down and gross margins way down. free markets work, we may be biased in the USA to overpay and use the home team but the rest of the world will migrate to China and deep seek derivatives to save money..Bubbles end on good news not bad news! Still expecting future rallies to be sold and downtrend in prices to accelerate Did the unemployment rate tick down in sept? Will weekly unemployment claims be under or near 220k? Perceived liquidity shrinkage.

You guys in the US have a more higher monthly payment pension plan non-government workers than we do in Canada.My husband worked full-time with an a great wage,paycheque 45 years from 20 to 65 and all my husband gets is close to $2,000 a month.This is CPP OAS combined in Canada.

This works out to only $44.44 per month every year he worked and contributed meanwhile most federal and other government workers enjoy a $5,000 to $6,000 a month pension with at most 30 to 35 years work service.They also get very generous benefits and life insurance coverage as well most Canadians do not get.All at taxpayers and Canadians expense.

If it not for myself and my husband making sure saving in our TFSAs,RRSPs,cash accounts we would now have a retirement living with dignity instead of being close to be short every month like many depending on CPP,OAS etc.My husband and I are looked upon as being well off in Canada by many in government and their pals but it took 45 years on my husband’s hard work and 27 years of mine to now be getting a dignified retirement.

This with raising 3 children all on their own now paying and paying taxes,CPP,EI etc. working 50+ hours a week in the private sector.The federal government looks at $40,000 a year in interest from our RRSPs,TFSAs,cash accounts as some big windfall but it is money worked hard,saved since the 80’s and we were responsible,prudent planning unlike many do not.

Just the interest alone being lost every year due to reckless low interest rates,higher inflation policies of the Bank of Canada over the last 28 years is costing us $25,000 a year if you look at average interest rates over the last 45 years.

The federal government of Canada Liberals seem to be the worse always pushing the Canadian dollar down,it costs us today in Canada $1.43 for $1 US dollar,they increase our taxes and make life very more expensive for all Canadians and reward social programs for those that contribute less and less to Canada.

Good luck depending on government to pull anyone out of poverty or having a decent,dignified financial,otherwise life in Canada,elsewhere government keeps pushing their more failed socialist policies and agendas.

It may be time for a wellness check, Jeff. Perhaps a meds adjustment?

Oh, and no politics on this site?

Look how much trouble our so called Government has in dealing with Social Security. Look at all the hate the young pile on the old who collect SS benefits. All the talk of welfare, useless eaters etc. etc….

And then you have people talking happily about UBI and UHI (Universal High Income) as solutions to the “age of abundance” that AI and Robots are about to supposedly unleash. A plan that is 10x or more of the scale of SS.

God told the Jews to observe every 50th year as a jubilee – when debts were forgiven, slaves freed and collateralized property was to be returned. Nobody listened of course…

Walmart E is more important NVDA E !

This is a sobering but essential update. The chart showing the Trust Fund balance beginning its precipitous decline is particularly striking. It makes the abstract “insolvency” date feel very concrete.

The article clearly lays out the math of the problem. My question is about the political and economic mechanics of a solution: When the Trust Fund is depleted and benefits are reliant solely on incoming payroll taxes, leading to an automatic ~23% cut, what is the likely chain of events? Would Congress be forced to authorize Treasury to borrow the difference to make full payments, effectively making the program a direct draw on general revenue, or would they allow the cuts to take effect? It seems we’re heading for a fiscal cliff that forces a binary choice.

To me, the correct solution to SS’ situation would involve a combination of changes to different parameters of the system, such as not to overwhelm any one aspect of it.

So, a combination of a small rise in the tax, say going from 6.2% to 6.5%, coupled with a one time “outsized” bump to the SS wage cap (say something around $30K), coupled with a graduated relatively small rise in the SS retirement age at some far point in the future (say raise the retirement age by one year starting say 15 years from now, spread the year rise over say 5 years), coupled with a modest reduction to benefits to current retirees say by a total of 2.5%, implemented by shaving off 0.5% off of the annual COLA over the course of five years.

Interesting comments and perspectives.

I think SS is one of many programs/institutions that when established, did not/could not foresee the massive changes in our society and around the world.

The hard reality for SS as well as most things economic is that the US has lost it’s preeminence in the world, foremost economically. We are living on borrowed time only because the dollar is so entrenched in world finance. Thus the “ability” to run $ 2T deficits each year with seemingly no consequences.

Well there are consequences, they are just delayed.

Even the SS Trust Fund is somewhat of a questionable structure: Essentially the US government lending to itself.

As China and the BRICS nations continue to expand their foothold on the major resources and means of production of real and important goods, the US will have greater difficulty pushing its dollar influence around the world.

Social Security is/will be the least of our worries. Enjoy it while it lasts.

“Even the SS Trust Fund is somewhat of a questionable structure: Essentially the US government lending to itself.”

That’s conceptually wrong. The Trust Fund’s beneficiaries/contributors, whose money this is, are lending to the US government. Just like I will lend to the government when I buy TIPS at the auction tomorrow.

“most things economic is that the US has lost it’s preeminence in the world, foremost economically. We are living on borrowed time only because the dollar is so entrenched in world finance.”

You hear doomsday thing like this, but it’s really difficult to understand your vision of the future. The US is far better positioned for the future than any other country.

Europe? The country I live in has such an imbalanced pension system that the average pensioner receives higher monthly income than the average worker. The trust fund is set to run out in 2030. No AI in sight. The birth rate is a fraction of the US. The equivalent social security tax is 8.5% vs 6.2% in the US. Talk about a recipe for intergenerational social conflict…

China? Pensions barely exist. My wife’s parents receive $300 USD each per month after full working careers. Parents who invested 30% of their net income in tutoring and basically tortured their kids into elite universities now have recent grads that can’t find a job. Demographic situation is literally catastrophic.

The US isn’t perfect, but we are in such a good position relative to almost everyone else.

Look on the bright side; Most of us will be dead before this can have a detrimental effect on our lifestyle. Good luck to the other 50.000001% of you.

Oops, 49.999999% or the joke falls apart.

Instead of government lending money to itself, should use a portion of the trust fund to invest into American companies providing growth exposure and a rising source of income through dividends. Cap ownership at 2-5% of company value or do equal weight of the S&P 500 so there can be no corporate favoritism. Now everyone participates in the success of our economy

The Wall Street mafia would love nothing more than that to pump up fees and prices further, and they almost succeeded under the Bush administration and Congress at the time, and then the market crashed during the Dotcom Bust, with the Nasdaq down 78% and the S&P 500 down 50%, which shut down the efforts by the Bush administration & Congress to do exactly what you proposed. Imagine the Trust Fund plunging to $1.2 trillion, from $2.4 trillion just because the market crashes. It took the Nasdaq 15 years and lots of money printing to get back to its 2000 high. Meanwhile retirees could only draw half of their Social Security benefits?

These proposals are always made near the peak of a huge bubble (Dotcom Bubble and now) when the Wall Street mafia runs of investors willing to buy this stuff at these ridiculous prices. What for the crypto mafia to push for forcing SS to invest in their crypto scams.