Loan balances remained flat for a year despite higher unit sales, an unusual situation. Two reasons: prices and cash deals.

By Wolf Richter for WOLF STREET.

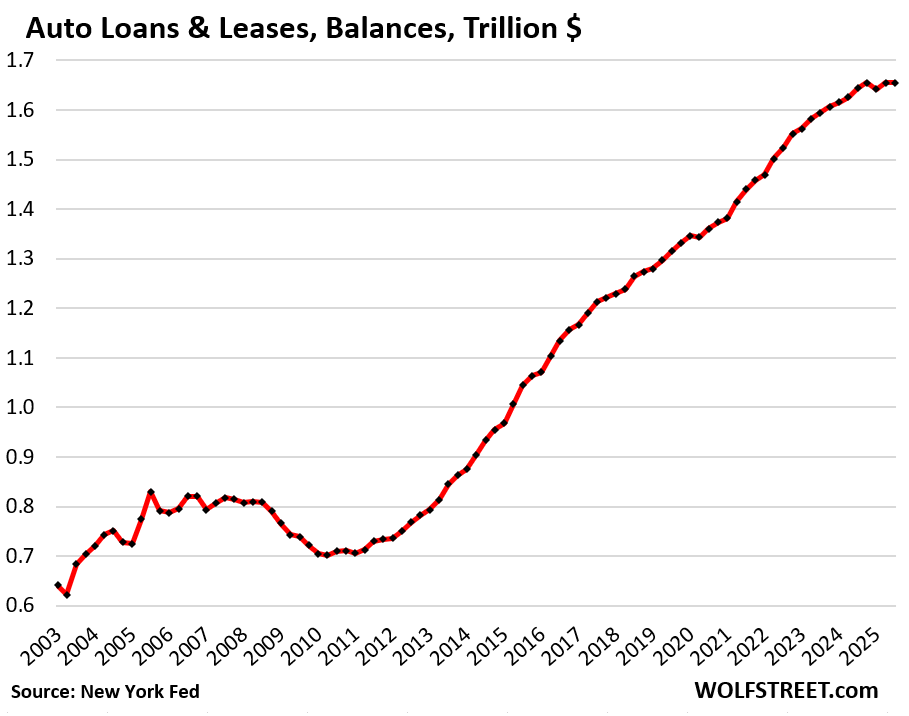

Despite higher unit sales of new and used vehicles in 2025, total balances of auto loans and leases in Q3 remained at $1.66 trillion, essentially unchanged for an entire year, according to data from the New York Fed, based on Equifax credit report data.

There are two big factors for this unusual situation of flat auto loan balances for a year despite higher unit sales volume:

More cash deals: A larger portion of used-vehicle buyers paid cash rather than finance amid higher interest rates for used vehicles. The portion of cash deals rose to 63% in 2025, from 61% in 2024, 59% in 2023, and 58% in 2022, according to Experian. The portion of new-vehicle cash deals has remained roughly unchanged at about 20%, amid subsidized leases and interest rates that have captured a big portion of the automakers’ incentives.

Lower prices: Prices for new and used vehicles combined have barely risen year-over-year and are down from their peaks in 2022 – new vehicles by a hair, and used vehicles by 19%, which has been giving some serious heartburn to big used vehicle dealers, such as CarMax.

The burden of auto loans and leases: Debt-to-income ratio.

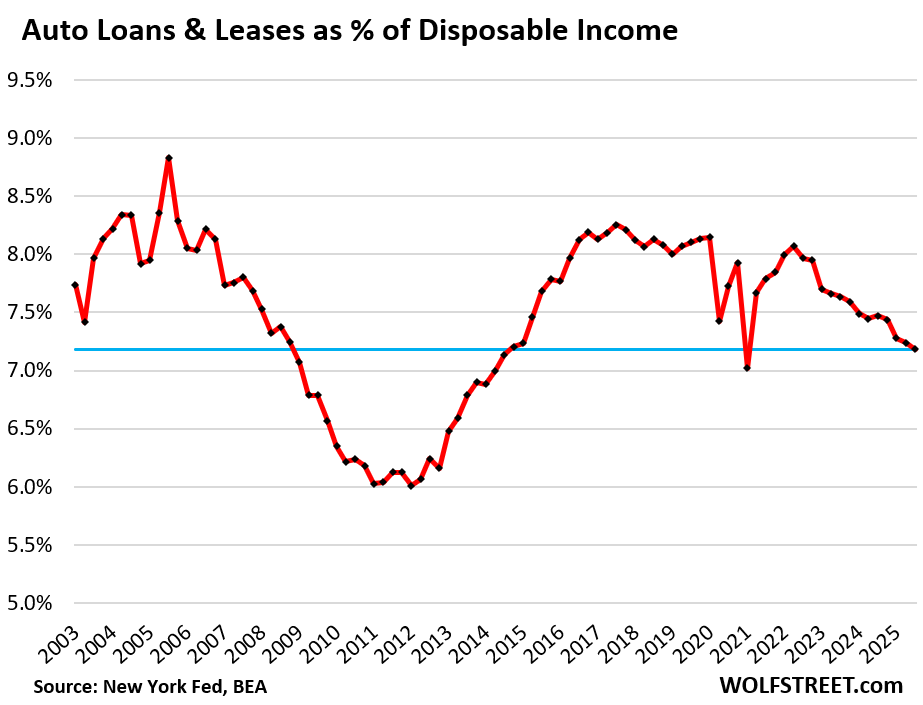

The burden of these auto loans and leases on households can be tracked with the auto-loan-to-disposable-income ratio. This accounts for more people and households, higher employment, and higher incomes.

Disposable income, released by the Bureau of Economic Analysis, represents an after-payroll-tax cashflow from all income sources but excludes capital gains: Household income from after-tax wages & salaries, plus income from interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc. It roughly represents cash flow after payroll taxes that is available to spend on the costs of living and debt service.

Due to the government shutdown, the BEA has not yet released disposable income for September. To get Q3 disposable income, we can use the data for July and August and estimate September based on average growth year-to-date.

The auto-loan-to-disposable income ratio in Q3 declined to 7.2%, on flat loan balances and higher disposable income.

The stimulus distortions in Q2 2020 and in Q1 2021 caused disposable income to jump, thereby pushing down the ratio. Now the burden is in the middle of the 22-year range:

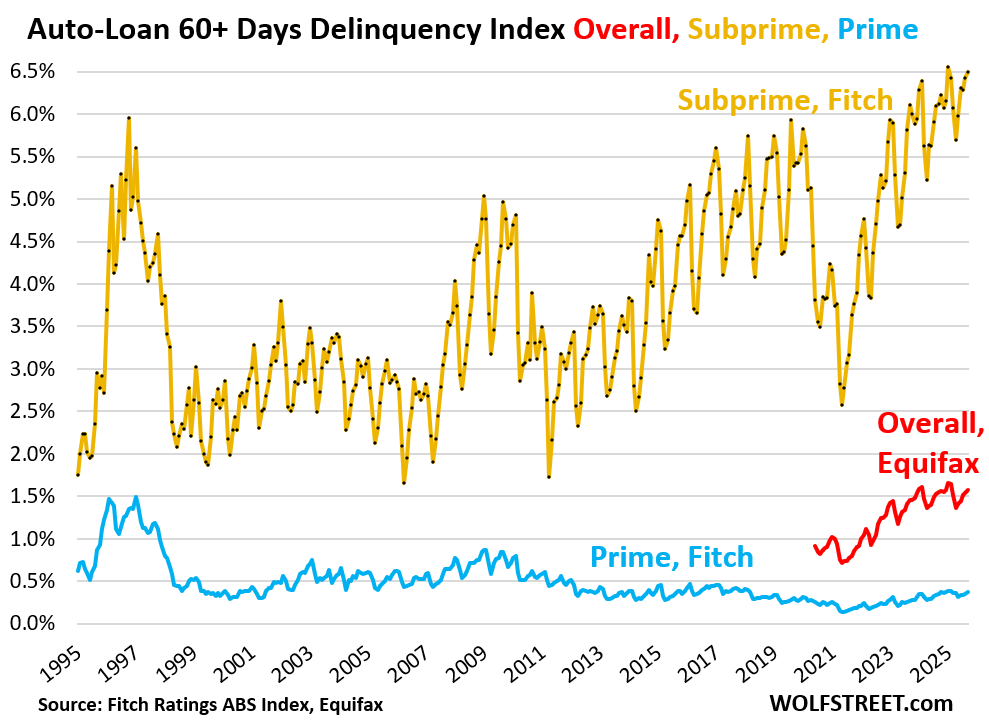

Serious delinquency rates: total, prime, and subprime.

Of the auto loans and leases originated in Q3, 15% were subprime rated (below 620 FICO score) at the time of origination, according to the NY Fed’s Equifax data.

Of the outstanding balance of auto loans and leases (the $1.66 trillion), also 15% were subprime rated at origination, according to Experian data.

Subprime gets a lot of press in the crisis media, but is only a small part of auto lending (15%), and an even smaller part of auto sales, as 20% of new vehicles and over 60% of used vehicles are sold without any financing at all.

For all auto loans and leases, including subprime, the 60-plus-day delinquency rate was 1.57% at the end of September, roughly unchanged from a year ago, according to Equifax. Delinquency rates are very seasonal. Unfortunately the publicly available monthly data from Equifax only goes back to the pandemic, and values from the prepandemic normal years are not available (red in the chart below).

For prime-rated auto loans, the 60-plus day delinquency rate ticked up to 0.37% at the end of September, according to Fitch, which rates asset-backed securities (ABS) backed by auto loans. The recent high was 0.39% in January and February. Even during the Great Recession, the prime delinquency rate maxed out at only 0.9% (blue in the chart).

Prime-rated auto loans have a credit score of 660 or higher at origination. Some specific loan pools of ABS rated by Fitch have no loans rated below 700. The top end of the credit-score scale is 850.

Subprime means “bad credit,” not low income. “Bad credit” is a result of being late in paying obligations, or not paying them at all. It does not mean “low income,” though the crisis media constantly equate subprime with low-income.

Low-income people have trouble getting loans, and if they can get loans, balances are relatively small. But the young high-income high-debt dentist into it over his head is a classic example of high-income subprime (he’ll get it cleaned up, but until then, if he gets a new loan, it’s a subprime loan).

An entire industry has sprung up selling at very high prices and lending at very high interest rates to subprime-rated customers, a high-profit-high-risk business. These companies range from specialized auto-dealer-lenders (which tend to implode periodically) to Wall Street firms that securitize these subprime-rated auto loans into ABS and sell them to institutional investors around the globe that used to like them during the era of ZIRP due to their higher yields.

The subprime 60-day-plus delinquency rate rose to 6.50% in September, the highest rate for any September, up from 6.12% a year ago, according to Fitch. The seasonal peak was in January at 6.56%, the still reigning all-time high (gold in the chart).

In case you missed it:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Overall the American consumer is killing it. Stock market at all time highs that at all time Lowe’s I could see this going on for at least 5 or 10 years until the next recession. That would also help for incomes to catch up to home values and keep the real estate bubble from popping. So all in all this looks like excellent news and I’m really glad to be fully invested in America.

our son is doing killing business

$100,000 kitchen remodels – booked out to April 2026

at 27 he’s handling 3 crews to make sure they don’t screw up

That’s awesome One of the best ways to become rich in America is to profit from all the lazy people who aren’t willing to do the work themselves.

“Lazy” is a pretty unfair characterization. The modern economy is built around specialization or labor and collective endeavor. A group of specialists can accomplish much more than a single non-specialist could ever accomplish.

In the next year or two, I am probably going to hire a contractor to redo a couple bathrooms, my kitchen and repaint. I am a middle-aged banker. I would need to be constantly on Youtube to learn how to do any of this. I don’t have the licenses needed to secure the required permits. It would take me years to do this while a contractor would have six workers do this in six weeks.

On the other hand, if the contractor needs to expand, he would come to the bank with his accountant. There is no way a contractor could organize the depositor public to lend him the money directly and have the arrangement properly documented.

AGREE, like totally dudes and dudettes with Paul!!

Back in the day, waaayy back in the 1980s, I could tell most clients with total certainty that unless they made LESS than $12.50 per hour, they were much better off paying me $50 per hour to do their skilled construction work.

And to be sure, I would invite them to do the ”basic” manual labor part, for which my employees contributed, if they wished to do so, and several did, and most of those who did hired me over and over to remodel and rehab and restore their homes and commercial facilities when they saw the clear cost advantages of hiring skilled specialists…

Ultimately, the producers/builders are the real creditors, not the banks. It seems like the world forgets this and goes to war from time to time.

Most people hiring joedidee’s son to do a $100K kitchen remodel are not “lazy” they are smart enough to realize that buying all the tools to make custom cabinets and learning how to remodel a kitchen so they can do it one time is not the best use of their time.

Good for them. Prob for new buyers, not those who were fine with their pink bathrooms, avocado green appliances and long paid-off mortgages the past 60 years all the way to their graves. Not lazy, just from a by-gone era.

Is it an automated robot kitchen?

Kitchens come from IKEA

They’re all sawdust, vinyl and maybe a smooth stone surface.

100k is insane

If you mean that the top 10% are doing near 50% of consumption then the 10% is really “killling it.” But this share of spending is up from circa 30% ish, so the economy has never been so tied to financial markets, which obviously the 10% own and increasingly it seems as if it might really be down to one stock Nvidia, given its linkages across the AI ecosphere.

That stat is headline BS

I was remembering the proposed “K-shaped recovery” from the pandemic.

I think it’s kinda been happening… maybe more “E” (sideways W?) or whatever shape.

I’m doing fine (always been in the middle). The wealthiest people seem to LOVE the economy (buying overpriced “assets” with cash!)…

Meanwhile the bottom of the middle (and, everyone below) seems to be just trying to stay afloat? I guess it’s the American definition of a “lower middle class”/ aka paycheck to paycheck class.

The blame usually goes to them, often with the accusation of laziness or stupidity et al.

Pretty much agree…NYC (albeit NYC) didn’t just vote in a Democratic Socialist because a majority of people are “crushing it” financially – rather the opposite (they are being crushed – primarily due to the rent explosion).

Meh .. his constituents were largely trust fund kids with art degrees, paying $5000+ for a 1 bedroom in Brooklyn. Votes for him were more performative than anything.

That democrat socialist is a millionaire who has never worked a real job in his life

Paul,as a contractor I am happy to see folks hiring others.

First off though,usually on own home one can pull permits/be GC,that said,do not have the time and or want to learn the skill set then by all means hire a contractor.

You do not know good contractors talk to family/friends/co-workers ect.,good word of mouth is the best advertising for us and also gives you folks to at least consider,best of luck with your home improvements!

NVIDIA is kind of where ALL of the tech spending is atm.

So yeah we do kinda live and die by NVIDIA

If they ever crumble, oh boy. Put your depends on

This nonsense again? The stock market at all-time highs doesn’t benefit the bottom 40% at all, and of the top 60%, it only really strongly benefits probably the top 10-20%.

The initial posters do kinda sound like bots or parody accounts…

To be fair, the media doesn’t help constantly discussing the “American stock market” as though it’s our past time, like baseball.

Agree with T-305

“Permanent High Plateau!!!”

At least that is what my shoeshine boy told me this morning…

You’re going to surprised and a greatly disappointed when this things pops. Most consumers are not killing it and they’re stretched financially and over levered. The stock market is on fumes as valuations are insanely stretched. For example the Shiller PE ratio LT average is about 17 to 18, right now we’re over 40. These levels are close to what we saw in 2000 (internet bubble). As for real estate they say the best cure for high prices are high prices. Be careful this is not going to end well.

I am sure 15 year auto loans will help.

As you can tell from the article, they don’t need help.

True, I was talking more the future users of 15 year loans.

If they want a permanent payment, they would do a two- or three-year lease and get a new car every two or three years, while payments continue, no?

Leases are very popular among people who like getting a new vehicle every two or three years, and don’t want to hassle with repairs and many maintenance items, such as new tires (unless they drive a lot), brakes, and other maintenance items that they might encounter after a few years.

@Wolf Richter

The people who would consider a 15 year car loan don’t have a choice. They’re underwater in their current vehicle and rolling their trade-in debt into their next vehicle. The only way they can afford the now $50k principal on an Altima they’re buying is with 15 year loan and lower monthly payment.

Once a consumer is in this debt trap, it’s hard to escape.

Yes, they would have been better off with a lease in the first place. But that’s the past and consumers often fall into this trap when their financed vehicle has a fatal issue outside the warranty window. Nissans with bad CVT transmissions, for example.

In the grand scheme of things, this phenomena isn’t endemic. But it’s happening.

They don’t HAVE to trade. They can just drive their car for a few more years, and the underwater part goes away naturally.

But people WANT a nicer newer vehicle, which is why they trade.

@Dan it has never been easier for a consumer to make extra cash with the ability to sell stuff online and gig jobs.

AptInvestor,

You left out OnlyFans as a way for renters to make the 30% hiked rent…

@cas127 we have not had any 30% rent increases in CA for a long time with statewide rent control capping increases at a maz of CPI + 5% (8% this year) unless a local law (like in SF and Santa Monica) has a lower amount.

15 year car notes are nothing new. People have been using them for years to “afford” a Lamborghini.

Wolf

I am happy for a payroll tax definition since you clearly define in your detailed description of what disposable income represents.

You can not control the data sources and detailed definitions are needed . Thanks for the details.

All taxes withheld from wages and salaries by employers, including federal, state & local income tax withholding, FICA (Social Security and Medicare), FUTA (Federal Unemployment Tax Act), SUTA, and SDI, and for self-employed, the taxes they estimate and pay quarterly.

I watch the shorts from “Benzs and Bowties” on Youtube. It shows the deals being negotiated by a Mercedes Benz sales manager. many of the buyers are terrible credits (and still want Mercedes). Two years ago the channel was all about getting people approved for $1,000+ lease payments. Today it is all about finding work arounds to get people with $10,000+ negative equity positions into new cars with ‘lease cash’ incentives and EV tax credits. The automakers are still able to move the new units for the time being, but if normal depreciation ever returns, there are certain vehicles like the Mercedes GLB that the banks and OEMs will have to take a wash on with lease turn ins.

Mercedes forces dealers to buy most lease returns by tying that ratio into performance metrics needed to hit top bonus levels. Dealers end up taking a bath on the individual units, but hope to make the money back elsewhere. The rest of the turds get sent to auction where the dealers can fight it out for inventory. I’m sure other manufacturers have similar strategies. They know how to protect themselves from large losses.

While subprime might not mean low income, you can’t deny that so many of these shady subprime lending used car dealers setup in low income neighborhoods. They follow the repossess and sell again model. They’ll get more in interest over 2 years than the car is even worth.

That’s a small portion of subprime lending. And it’s not true. Used car dealers set up where used-car dealers set up.

Do NOT confuse these large dealer-chains in the article with the tiny note lots that some guy owns.

I wonder how the number of used cars hitting the market has been affected by companies like Uber and Lyft. I remember when I used to travel it would almost always involve renting a car, as it was that or an expensive taxi or unfamiliar or non existent public transit. Can’t remember last time I actually rented now. Obviously a lot of miles put on Uber/Lyft drivers cars but they don’t turn them every few years necessarily.

Panic grips Wall Street as the ‘Warren Buffett of tech’ quietly offloads ALL stock in world’s biggest company

The move has rattled traders already spooked by a growing chorus of warnings about the overheated stock market.

Masayoshi Son, one of tech’s most–watched investors, is making a gigantic bet – and it’s sending shivers through Wall Street.

The Japanese billionaire and SoftBank founder quietly sold off all his Nvidia shares and most of his stake in T-Mobile last month, unloading roughly $15billion worth of stock in total.

The move by Son – dubbed the Warren Buffett of tech investment – has rattled traders already spooked by a growing chorus of warnings about the overheated AI market.

Among the skeptics is Michael Burry, the Big Short investor who predicted the 2008 financial crash. Last week, it emerged he has now made a huge bet that Nvidia’s share price will fall.

By midday Tuesday, the tech-heavy Nasdaq was down 0.8 percent, while Nvidia’s stock slid more than 3 percent. Both recovered in the afternoon, but are still down significantly from a week ago when Burry’s bet was revealed.

It reverses some of Monday’s gains on optimism that the end of the government shutdown would help boost American spending.

Son’s sale is being read as a warning sign that the AI boom – the same one that has powered record stock gains for companies including Nvidia, Microsoft, and Palantir – might finally be wobbling.

Nasdaq down 0.2%. Not looking like “panic” to me just yet.

Eh. It either will or won’t. Big guys like that make dumb bets all the time. Michael Burry did a ton of research into the subprime market and even he had to get lucky for that kind of meltdown to occur.

Now people think he is a guru.

Time in market, not timing the market is what makes sustainable wealth