After the debt ceiling, the shutdown: government checking account (TGA) sucks up $700 billion in four months.

By Wolf Richter for WOLF STREET.

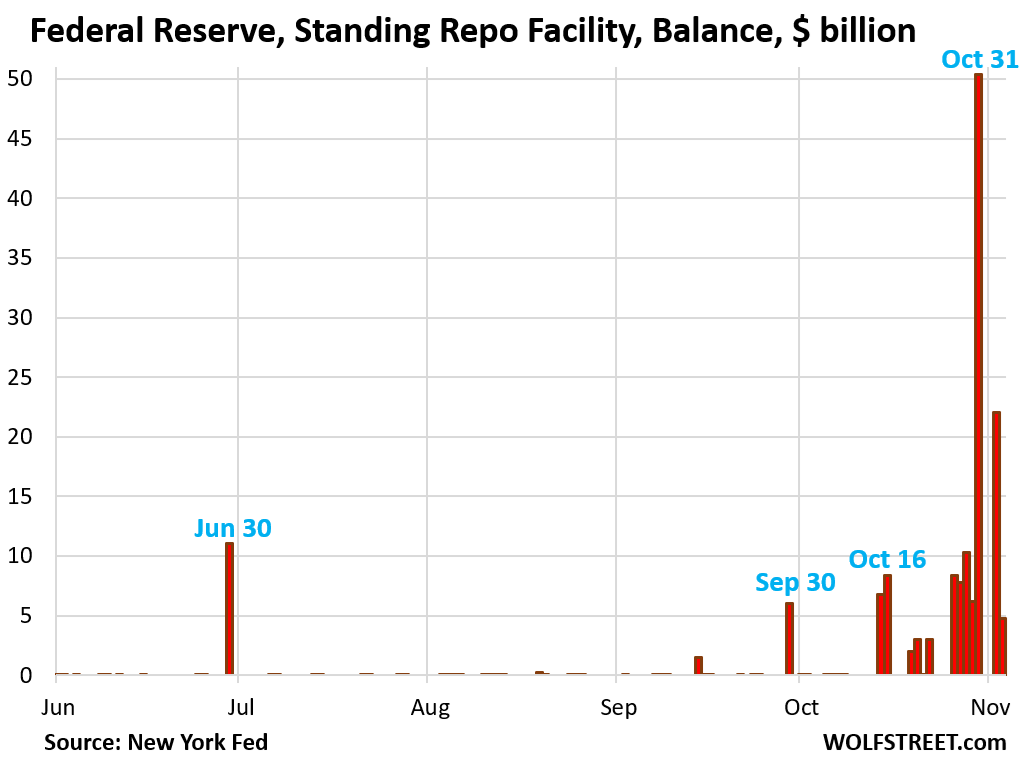

The uptake at the Fed’s Standing Repo Facility (SRF) plunged to $4.8 billion today: $2.8 billion at the morning auction and $2.0 billion at the afternoon auction. The approved counterparties at the SRF are big banks and broker-dealers.

This was down from $22.0 billion on Monday, and from $50.4 billion on Friday, which had been a record of this new facility that the Fed revived in July 2021.

These repos (“overnight repurchase agreements”) will mature on Wednesday, when the Fed gets its $4.8 billion back and the banks get their collateral back. The collateral is Treasury securities and government-guaranteed “agency MBS.” The $50 billion in repos taken on Friday matured on Monday, when the Fed got its $50 billion back and the banks got their collateral back. So that liquidity that these repos provided on Friday got reversed on Monday. Then on Monday, $22 billion in new repos were taken, and that liquidity was reversed today. And today’s $4.8 billion in liquidity will be reversed tomorrow. The total balance outstanding at the SRF is now $4.8 billion.

The purpose of the SRF is to provide liquidity to banks and dealers so that they can lend to the repo market. This is a profitable trade when repo market rates are significantly higher than the Fed’s rate at the SRF (currently 4.0%). And repo market rates have been higher in recent weeks.

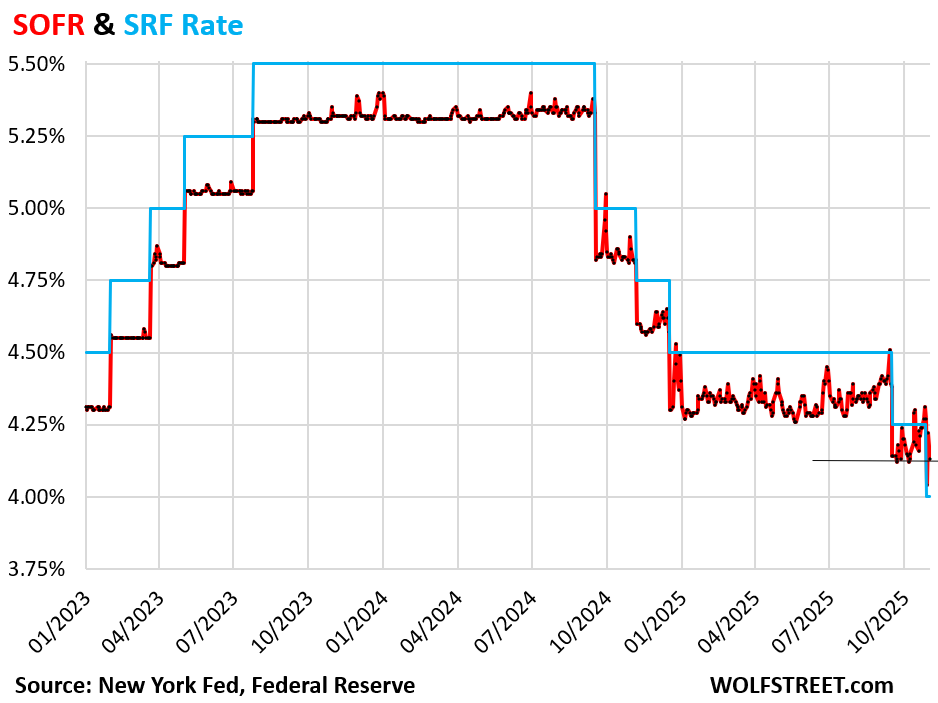

Repo rates. The Secured Overnight Funding Rate (SOFR), which tracks a $3-trillion-a-day segment of the repo market, declined to 4.13% on Monday, from 4.22% on Friday (the NY Fed will release today’s rate tomorrow).

While 4.13% is a drop from Friday, it’s where it was in late September and early October after the September rate cut. But last week there was another rate cut!

The rate at the SRF (blue in the chart below) is now lower than SOFR (red), when normally it is higher. The SRF rate is one of the Fed’s two ceiling rates. When repo market rates go above it, banks are expected to pile into the SRF, grab a bunch of money at the SRF rate, and lend it overnight to the repo market at the higher market rate. That new supply of liquidity brings market rates back down, at which point banks lose interest, and activity at the SRF goes back to sleep.

When repo market rates blew out in September 2019, the Fed did not have the SRF; the Fed had scuttled its repo facility in 2009 under QE.

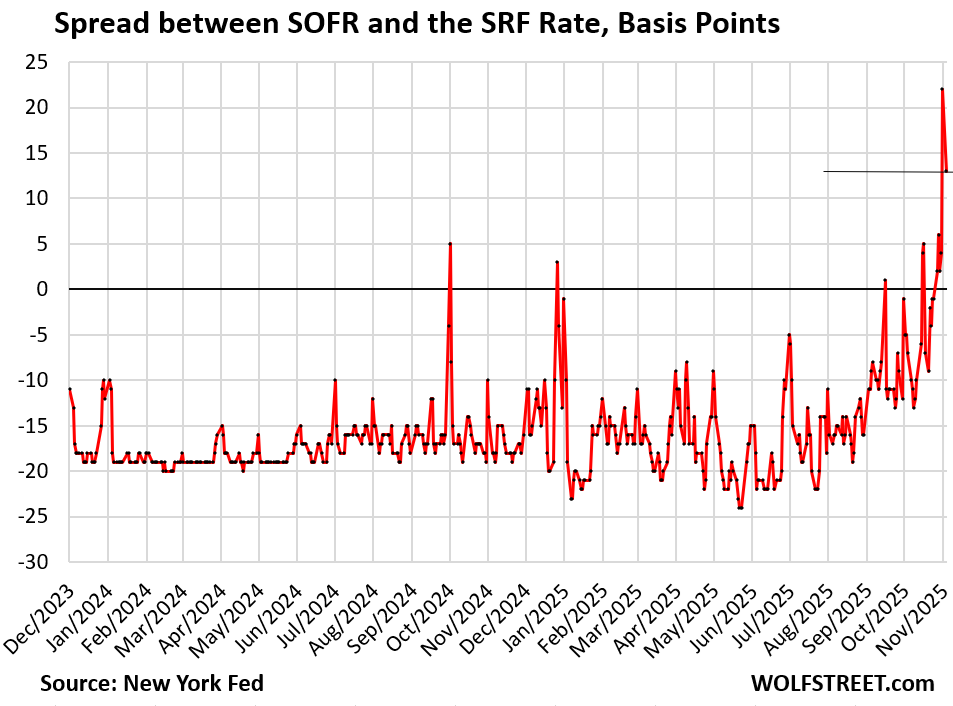

The spread between SOFR and the SRF rate widened on Friday to +22 basis points, the widest in the short life of the new SRF (born July 2021). On Monday, the spread narrowed to +13 basis points, the second widest in its short life.

Normally, the spread is negative, with SOFR below the SRF rate.

Why these liquidity pressures?

Over three years of QT have wrung out a lot of excess liquidity. Now, two major factors came together to put liquidity pressure on the repo market, where large amounts of liquidity have to move around, and yields signal where these amounts need to go, and higher yield help the flow of liquidity to where it is needed. But it takes some time.

1.Month-end, quarter-end, and tax days, and the days surrounding them are pressure points, when massive liquidity flows put pressures on the market and cause SOFR to rise. October 31 was on Friday, which saw the big spike in SOFR to 4.22%.

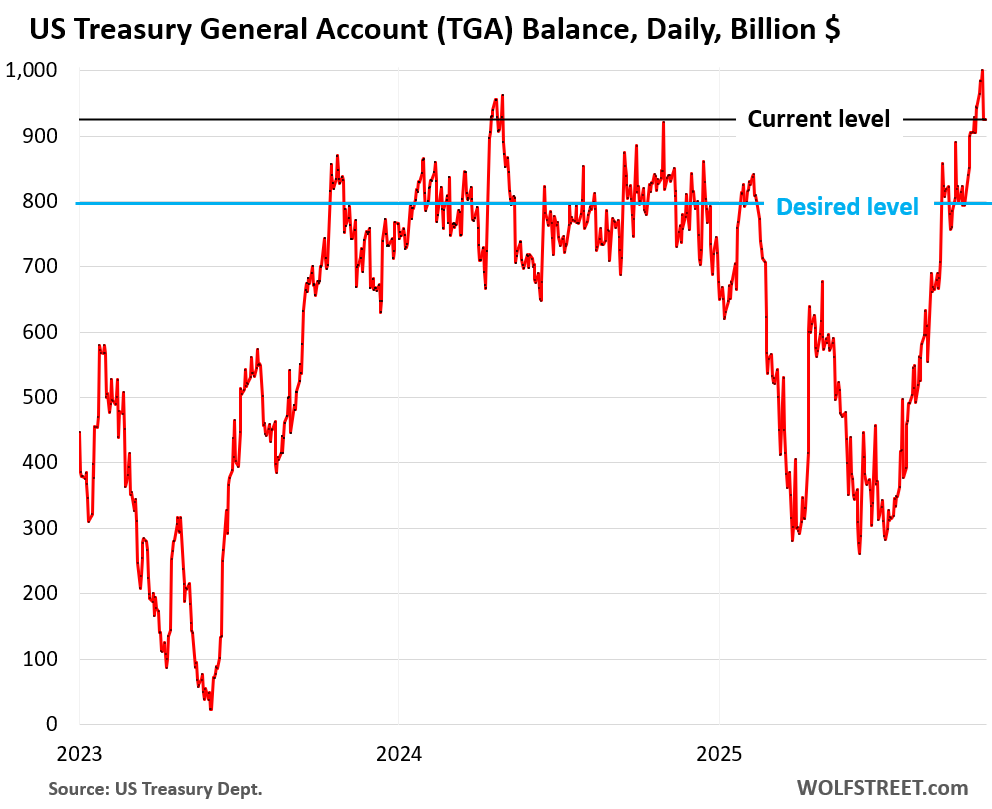

2. The balance in the government’s checking account, the TGA (Treasury General Account) has ballooned over the past three weeks as the government halted paying for some of its operations and salaries due to the shutdown, while still selling Treasury securities and collecting taxes, fees, and tariffs. So cash is still coming in, but the cash outflow has been temporarily slowed, and the checking account balance has ballooned.

The TGA is with the New York Fed. As the TGA balance rises, it removes liquidity from reserves and the market.

On October 30, the TGA balance reached $1 trillion, over $200 billion more than on October 10 before the shutdown began changing the cash flow.

On November 3, the balance dropped to $925 billion, still $125 billion more than on October 10. If the balance continues to decline, it would send this liquidity into reserves and the market.

In the four months between the end of the debt ceiling – when the TGA was down to $300 billion – and October 30, the TGA has sucked up $700 billion in liquidity, part of which came out of banks’ reserves at the Fed.

This type of large and sudden move of liquidity out of the market into the TGA, when liquidity had already tightened up after three years of QT, was the reason the Fed cited when it slowed QT in June to preempt too much pressure on bank reserves, and thereby on the repo market because, when reserves are tight, banks don’t lend their reserves to the repo market, and repo rates surge, which is when the SRF is supposed to kick in. And it did.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I went to Subway yesterday. The $5 footlong is now $16.

If the tariffs are essentially doubling corporate taxes, they will hustle to cut costs and push prices to the limit.

Was that sandwich imported from China? (obviously not because it’s made in front of you by US labor). Was the bread imported? (no, it’s baked on location). Was the labor tariffed? (no the labor is right in front of you and at headquarters and is not tariffed). Were the rent and utilities imported and tariffed? (come on, give it try). Were the transportation and cold-storage costs in the US tariffed? (nope). The cold cuts and cheese? (unlikely, most of this stuff is made in the USA from US beef, pork, and milk). Were the few pieces of greenery imported? Maybe some, others not. So maybe 2 cents in tariffs on four slices of tomatoes and a few morsels of peppers and olives.

So how do you blame a $16 price on a few cents of tariffs – if any? You people are hilarious.

And why did you troll this article on the repo market with your sandwich-tariff hilarity? Trying to start the comments out with a good laugh?

I learned from Google AI recently that California, accounting for 1% of the U.S. farmland, produces something like 75% of the U.S. veggies, fruits, and nuts. Everywhere else they pretty much grow corn, potatoes, and soybeans. And of course Cali is the biggest producer of milk (ahead of Wisconsin). All in all, California produces 8% of the nation’s food supply.

“I learned from Artificial Intelligence “

LMAO

The brainwashing is going well. It is definitely the End of Days

Teacher “Johnny, where is your homework ?”

Johnny “The AI ate it”

There is an entire subset of people that want Trump and tariffs to fail so badly that they forget to apply basic economic principles to what has caused the increased cost on products they’re complaining about. It’s sad when people are rooting for the United States to fail because they don’t like the leader instead of studying economics and hoping this tariff experiment works out as planned. Trump is a tool and he’s getting the job done that should have been done back in the ’80s. The difference is he’s not a politician and he actually said this decades ago unlike the mouthpieces that we elect that are controlled by special interest in the military industrial complex.

It is also why I don’t give a shit about the election results. We need a shakeup on US manufacturing and immigration. It is 100% worth a try.

Rain man, the big “but” is businesses and the U.S. economy don’t work with “hope”. Wolf always supports the check and balances of finance.

It’s a pipedream to think that prior decades of lowered manufacturing of durable goods in the U.S. are going to return faster with blanket tariffs. 60% of the Gross National Product is in services, which have little to do with tariffs on imports. The profit motive of people who rely on manufactured and commodity goods (farm crops) that become less profitable to the U.S. will stagnate production here. The profit motive has been lowered.

Re-tooling Our economy to produce goods that aren’t sold overseas because of counter tariffs is contracting to our economy.

This leader you speak of has done a lot of collateral damage.

The SRF (Sandwich Refinancing Folks) has exploded recently.

This is due to the lack of ATC (Artists Tailoring Chow) resulting from the government shutdown.

The sam-witch you bought was furloughed and bought en masse by the company as an arbitrage opportunity, at pennies on the dollar ($0.50?), and resold at 3X the marketed price.

The sandwich exchange rule means they have to reinvest their profits into an equal or more valuable lunch item in order to mitigate their short term gain taxes.

Expect the $50 inch- along next week (listed in the CPI as a “full monty meatwich” and NOT adjusted for shrinkflation, due to the seasonal effects of cold evenings).

Let’s get it Piled higher and Deeper, eh?

Curious,

The mbs that the fed is dropping off the ledger are presumably holdovers from the last bust. The collateralized value (real world) value of those securities is probably far less then what is booked.

Getting rid of that bad debt off the ballance sheet and turning even a portion of that debt into working capital seems to me it is increasing money supply and growth supportive.

Fed get to claim tightening while at the same time loosening availability to cash and credit.

“The mbs that the fed is dropping off the ledger are presumably holdovers from the last bust….”

No. Most of the MBS that the Fed holds are those that it bought during the 3% mortgage era, from March 2020 through Sep 2022, when it stopped buying MBS. Nearly all the old MBS with higher mortgage rates are gone:

Borrowers refinanced those higher rate mortgages no later than in 2020-2022, and when those old mortgages got paid off, they came out of the mortgage pool, and the principal payment was passed through to MBS holders. So the principal value of the older MBS shrank very quickly.

After the mortgage pool and principal value of the older MBS shrank enough, the GSEs (Fannie, Freddie), and government agency Ginnie Mae, called the MBS at remaining face value and repackaged the few remaining mortgages into new MBS and sold those to investors. This happened at a huge volume during the 3% mortgage era.

All MBS that the Fed holds are guaranteed by the government, and if there are any credit losses, it would be the taxpayer that’s on the hook, not the Fed. The MBS that the Fed holds have essentially the same credit risk as Treasury securities, namely zero.

Why did you buy it???

I believe in strenuous debate about tariffs, but people must call out BS on what Brian posted.

Brian, either you’re ill-informed as to what a tariff is or you’re an ideologue.

Either way, BS on your post – subs are not impacted by tariff such that the price would double.

Honestly you should just stop eating subway. It is gross

I am confused why SOFR would ever go above the upper limit of the FFR if SRF is there to provide better rates?

Do banks rather pay an extra in order to avoid tapping the SRF? Perhaps there is stigma associated with using it?

“Section 11 of the Federal Reserve Act, as amended by section 1103 of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, requires that detailed operational results, including counter-party names, be released two years after each quarterly transaction period.”

And there is no liquidity shortage, there is a trust shortage. Liquidity can be had, just not at the cheap price the banks want.

I expect SFR being tapped more and more, and while we saw a dip in amount today, would not be surprised to see that go back up, ‘until moral improves’ aka QE w/vengeance.

“Do banks rather pay an extra in order to avoid tapping the SRF?”

No, banks LEND to the repo market. Repo market rates jumped because banks didn’t lend their reserves in sufficient amount to the repo market. Banks sit on $23 trillion in cash from depositors, and their $3 trillion in reserves at the Fed are an excess of that. They don’t need to borrow in the repo market. The $7 trillion in money market funds are the other big lenders to the repo market.

I assume they borrow from the repo market because they don’t have collateral to borrow from the SRF?

No, same types of collateral.

I’m also interested in the stigma aspect of banks preferring SOF (private) rather than SRF (Fed) as a lender of reserves (both facilities are based on repo loans). Fred shows SOFRVOL rising and at around 3.2T at the moment, almost linearly rising since 2023/10. While the SRF (Fred: RPONTSYD) had a recent peak and then receded, as is the subject of the current article.

Anyway, the good banks have plenty of reserves, and they clearly are now lending reserves (with secure/USG collateral) to the bad banks at increasing levels, the amount being about 3.2T yesterday. 3.2T is about half the total reserves outstanding at the moment. Not small potatoes, exactly.

Apart from the possible stigma angle, this is an enormous amount of reserves being lent out. Scary that this is necessary (necessary=needed by the weak banks to fill the hole in their reserves).

What is the impact of the tariff proceeds? I thought those inflows went to the TGA. Does it help? And by how much?

I mentioned that in the article. They’re part of the cash inflow into the TGA, along with fees and taxes.

Well, with the Treasury now full, the U.S. government could almost afford to buy a quarter of Nvidia stock. To put the above in perspective, what Nvidia makes in a year, the U.S. government spends in four days. There is a two orders of magnitude mismatch right there, but draw your own conclusions.

This is a great article explaining the dynamics of the Repo rate over the last week or so. Thank you.

Wolf, the SOFR Rate is significantly higher than the Fed Funds Rate currently, if that continues for a longer spans of time, that will be a serious problem .

SOFR was back to 4.0% yesterday, as per the NY Fed this morning. So relax.

4.0% is the upper end of the Fed’s 3.75%-4.0% target for the federal funds rate.

SOFR will drop below 4.0% today, as we’ll learn tomorrow morning.

can’t wait to see $TRILLION jump in funding come end of shutdown

more WORTH LESS fiat $dollars

making things worse for 90%

the vacuums are out for top 1% scooping up excess $$$

just got 20% property tax increase in our bluecoat city

I can take those worthless fiat dollars off your hands.

Wolf…..

I am trying to imagine who is suddenly “caught” and must pay 22 basis ptis over the SRF rate to get back in “balance”.

Are these identities hidden as with the Discount window users?

And is this pure mismanagement or is there a stress in financial system that is being placated by the SRF?

Understood, the SRF is working to tamp down these “spurts”, but are the spurts a signal of stress?

Your thoughts

SOFR was back to 4.0% yesterday, as per the NY Fed this morning. So relax.

Banks LEND to the repo market; they don’t need to borrow in it. Banks borrow at the SRF and LEND to the repo market. That’s what the entire article is about, getting banks to lend more to the repo market as their reserves tighten up.

When repo market rates blew out in Sep 2019, it was because banks didn’t lend enough to it because their reserves were tight, it was Tax Day (corporate estimated taxes, Sep 15), and huge amounts of money flowed through banks’ reserve accounts, and they needed to be able to handle those payments. So they didn’t lend to the repo market when repo market pressures increased, and it got out of control because there was no SRF.

On the other hand, in the spring of 2023, when some regional banks did collapse, there was no sign of that in the repo market because banks don’t need to borrow in the repo market. The repo market wasn’t touched by it.

I know it’s amusing to look for some collapsing bank under every rock. But that’s just not happening here in the repo market.

“I know it’s amusing to look for some collapsing bank under every rock.”

Perhaps I am not being clear. I do not suggest banks are borrowing over the SRF rate…… but who is the typical entity that borrows OVER the SRF rate in the repo market?

Brokerage houses, money market funds. ????

Thanks

The repo market is the cheapest way to borrow for companies. They cannot borrow at the SRF. Only about 30 approved banks can borrow at the SRF.

Simply more confirmation that there really are no consequences and the bad behavior will continue. Remind me, how many “temporary emergency measures” have been instituted by the Fed since Nixon? Repo certainly did not exist.

The heads of several primary dealer banks and investment firms are now openly advising a 15-25% gold position in portfolios. They know that the only way out (barring WWIII) is major currency devaluation.

“several primary dealer banks and investment firms are now openly advising a 15-25% gold position in portfolios.”

That’s because they have had highly leverage bets in place that will make them a lot of money if the price of gold goes up. And then they unwind their highly leveraged bets on gold to take their profit and throw your gold holdings under the bus. Oldest story in town. They ALWAYS do that. Why you falling for it when they hype “gold” and don’t fall for it when they hype their other big leveraged trades?

Personally, I am not “falling” for anything and somehow managed to sell the top in my miners and PM investment positions. Having said that, I still have a very comfortable physical position of the preferred collateral. Sorry Wolf, the only way out is more monetization and devaluation of the Federal reserve note. As yields rise I may take some of this cash back to treasuries, but plenty of good dividend paying companies in the energy/utility space and more than happy to pay my capital gains taxes (it’s less than every other tax I pay).

Yes, I am old enough to have been through this cycle before (twice actually), just doing what the banks do and using to my advantage. Regarding leveraged bets, this will work until there is a failure to deliver of some serious fraud. Sorry Wolf, I think that the western player don’t have the control they use to under Greenspan. Guess we will see.

That should read “or some fraud”. Greenspan was very clear about gold’s role in the monetary system and his fed began the “paper” control game. Risk (trust) is being repriced globally and this isn’t our father’s Fed or congress…

Hedge accordingly.

Update:

SOFR dropped to 4.0% on Tuesday, as per the NY Fed this morning (from 4.13% on Monday, the figure available for the article and 4.22% on Friday).

4.0% is also the SRF rate, so activity at the SRF should to to near zero. And…

SRF had zero activity at today’s morning auction.

This shows that the month-end pressures are over.

Update:

SRF had zero activity in the afternoon auction as well, and the balance is down to zero now.

This wraps up the month-end dynamics in the repo market when it coincided with the TGA balance spiking due to the shutdown.

There’s an interesting pattern in the SOFR & SRF Rate chart: the big spikes in spread are generally timed closely after a Fed policy rate decrease but not after a policy rate increase. Any ideas on the asymmetry?

I get that “all else being equal” doesn’t apply since the Fed balance sheet reduction has been draining liquidity in the background during the same time period as the chart. But I wonder if something else is at play too.

Wolf thanks to you and your easy, straight forward explanations, I can understand this stuff a little more. Much more than I could a few months ago

Given Wolf’s post, I think the biggest unsung influence on repo rates is the US Treasury, the TGA, which—unless the government runs steady budget surpluses— implies one-way upward pressure on repo rates.

That said, since T-bonds have sold off today (and yesterday?), HFT Treasury market-makers will be long futures and short spot, long the basis. (Long futures = long the basis.)

The HFT market-makers collectively dampen, slow, obstruct price volatility because they trade the second derivative (the basis) of the underlying commodity. But they too can be overwhelmed by events, blown out, as they were on March 3, 2020.

When bonds fall in price, the HFTs (which trade 2/3 of daily Trsy volume) end up doing reverse repos with their prime brokers, lending them cash for collateral, supplying banks with cash, temporarily alleviating the upward pressure on repo rates.

It seems like the SRF, as described, is an occasional free lunch for banks. Well, more like a snack.

The US government offered a higher rate of interest to banks than the government set as the rate of interest on its own debt. The banks collected the difference as incentive for participating.

So basically, the government pays the banks a bit extra to create the objective of increasing bank liquidity during times of strain. The banks get a free lunch, the government gets a policy objective met, and the excess paid to banks just gets added to the national debt.

Granted, I’m not being critical here. This might just be the most efficient use of government money to effect economic outcomes ever devised.

By my napkin math, paying the 0.22% SOFR-SRF spread for one day (x 1/365) on $50B cost the government a whopping $301,270. In exchange for that spending, we might have avoided a financial market seizure on Friday which could have impacted GDP by enough to reduce tax revenues by a couple orders of magnitude larger amount.

My math above depends on an assumption I’m not sure about: When a bank uses their treasuries as SRF collateral, does the government collect that day’s treasury interest, or does the bank? If the bank collects the interest, for that day they are essentially earning double the treasury rate and my math above is wrong. In that case, the SRF would have spent ((1/365) x 0.0422 x $50B =) $5.78M. Still indisputably small potatoes in the grand scheme.

However this second scenario doesn’t make sense because SRF lending goes to nearly zero when the SRF rate SOFR, they can free up a ton of liquidity relatively cheaply, by just paying the spread for a day or a week, and work their way out of it. Thus the stigma only makes sense in non-stressful times. In this event, the government would receive the free snack.

Still, it’s impressive how much leverage the government has over bank liquidity thanks to the SRF. The cost of paying that spread is minuscule compared to the political value voters/donors place on the outcome of stable, constantly liquid markets, or the extra taxes generated from uninterrupted economic activity. As an economic lubricant and problem-preventer, it seems comparable to the FDIC – which was among the greatest economic stability promoting programs ever invented.

I do wonder whether the shadow bank, private capital, hedge fund, venture capital, or BDC industries, which comprise a much larger chunk of corporate lending than banks nowadays, are iced out of this facility because they are not regulated banks. What happens when they run into liquidity troubles and have no pawn shop of last resort?