Boom-Bust, Boom-Bust?

By Wolf Richter for WOLF STREET.

Condo prices have shown that they’re subject to huge booms and busts. Here we’re going to look at bigger cities where prices of mid-tier condos have dropped below where they had been about 20 years ago at their respective peaks during Housing Bubble 1. There are not many among the bigger cities we’re tracking, but there are some.

The other day, we discussed the 23 Bigger Cities where Condo Prices Dropped by 12% to 28% through September. Prices in most of those 23 cities were still well above their highs of Housing Bubble 1. But in a few, they weren’t, and they’re back under the limelight here.

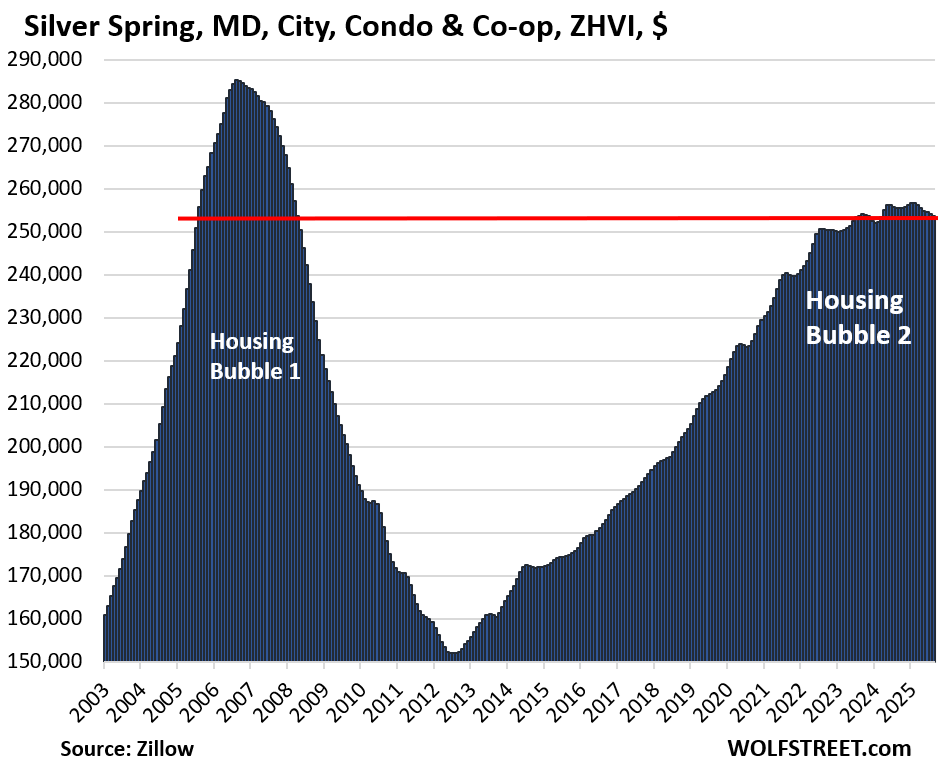

Silver Spring, MD: Prices of mid-tier condos in September 2025 were 11% below the peak in August 2006 and were back to where they had first been in August 2005, over 20 years ago. This city in the Washington DC metro had a gigantic condo bubble from January 2003 through August 2006, when prices of mid-tier condos exploded by 78%, before collapsing and giving up more than the entire gain by mid-2012. Then it started all over again, but more slowly.

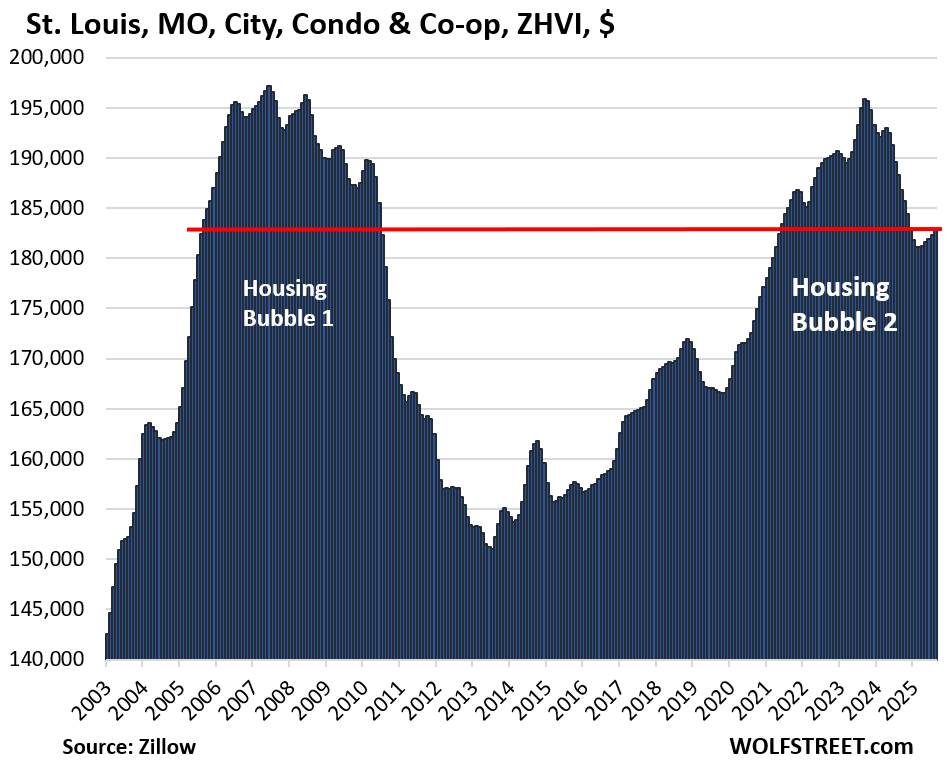

St. Louis, MO: Prices of mid-tier condos in September 2025 were 7% below July 2007, and were back where they had first been in September 2005.

Methodology and data: These prices here are seasonally adjusted three-month averages of “mid-tier” condos and co-ops in “cities” from the Zillow Home Value Index (ZHVI), which is based on millions of data points in Zillow’s “Database of All Homes,” including from public records (tax data), MLS, brokerages, local Realtor Associations, real-estate agents, and households across the US. It includes pricing data for off-market deals and for-sale-by-owner deals. These are not median prices.

Some of the bigger cities might not be included here. The ZVHI for condos does not have data going back to 2003 for all cities, though it has more recent data on them. And so any of these cities with incomplete data, whose prices might have dropped below Housing Bubble 1 peaks, would not be included here.

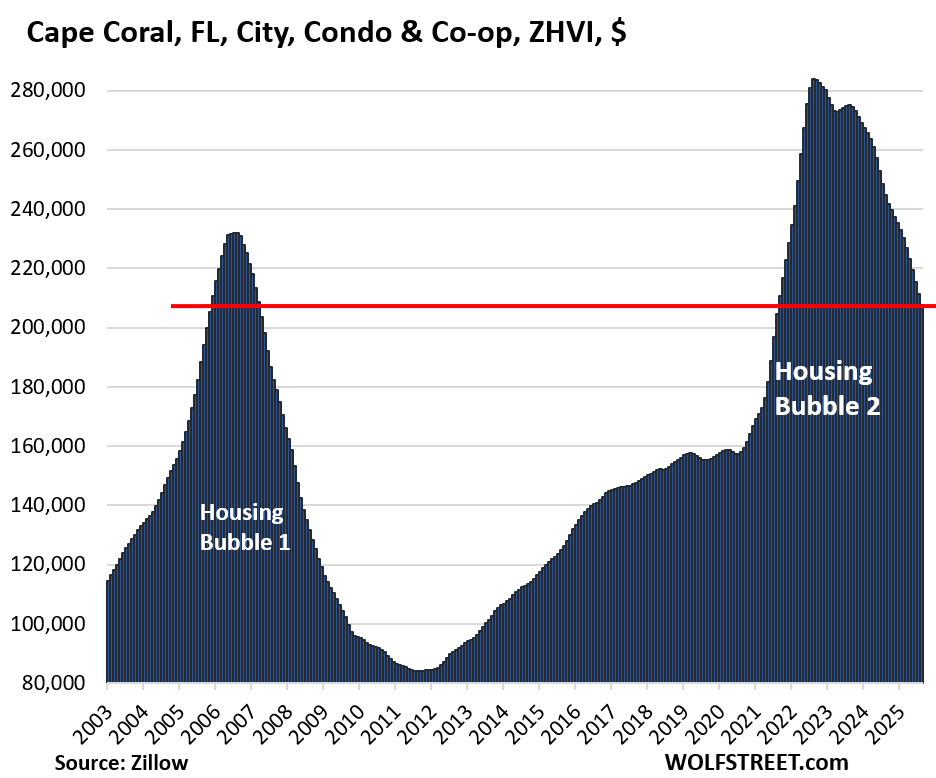

Cape Coral, FL: Prices of mid-tier condos in September plunged back to where they had first been in November 2005, and were 12% below the July 2006 peak of Housing Bubble 1. Epic Boom-Bust, Boom-Bust.

Prices have plunged by 28% from their peak in July 2022 and by 16% year-over-year.

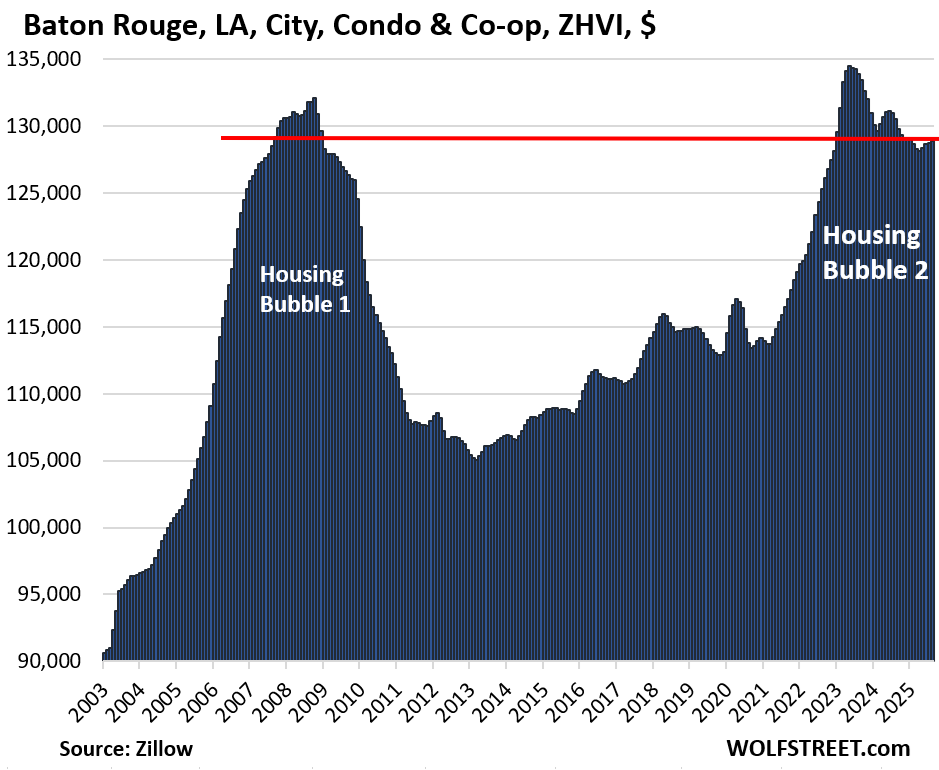

Baton Rouge, LA: Prices of mid-tier condos in September 2025 were 3% below the September 2008 peak during Housing Bubble 1 and were back where they’d first been in August 2007.

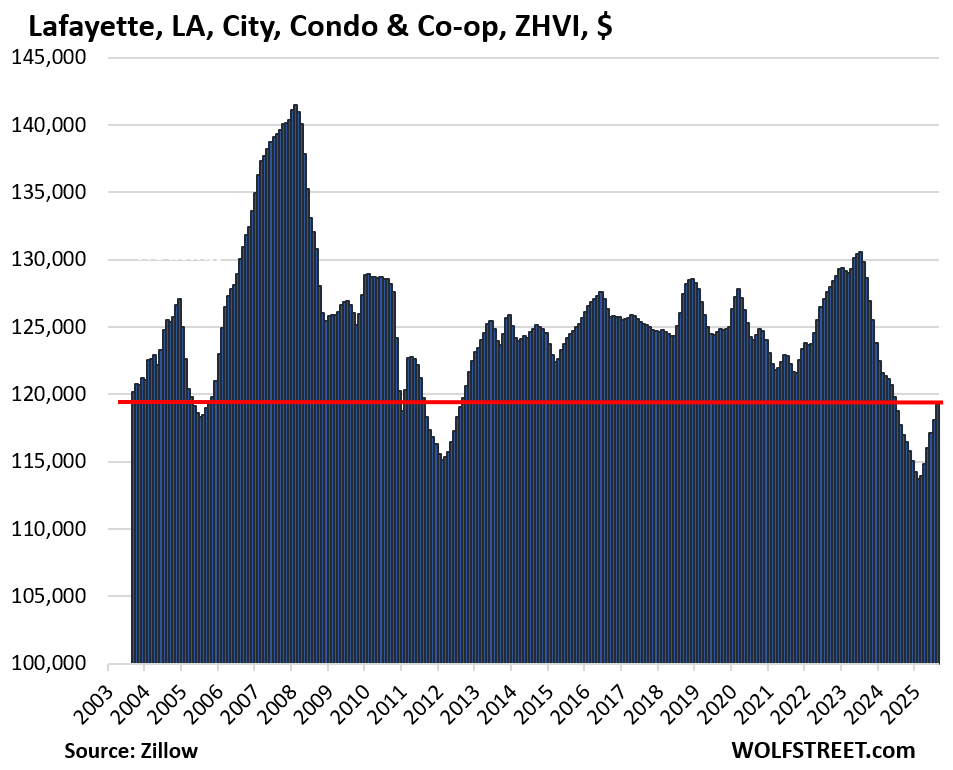

Lafayette, LA: This isn’t a bubble market, though it made a valiant effort in 2006. Prices of mid-tier condos in September 2025 were 15% below their peak in January 2008, and were below where they’d been in September 2003, the extent of the ZHVI condo data. Most of the 22 years in between, prices had been higher than in September 2025.

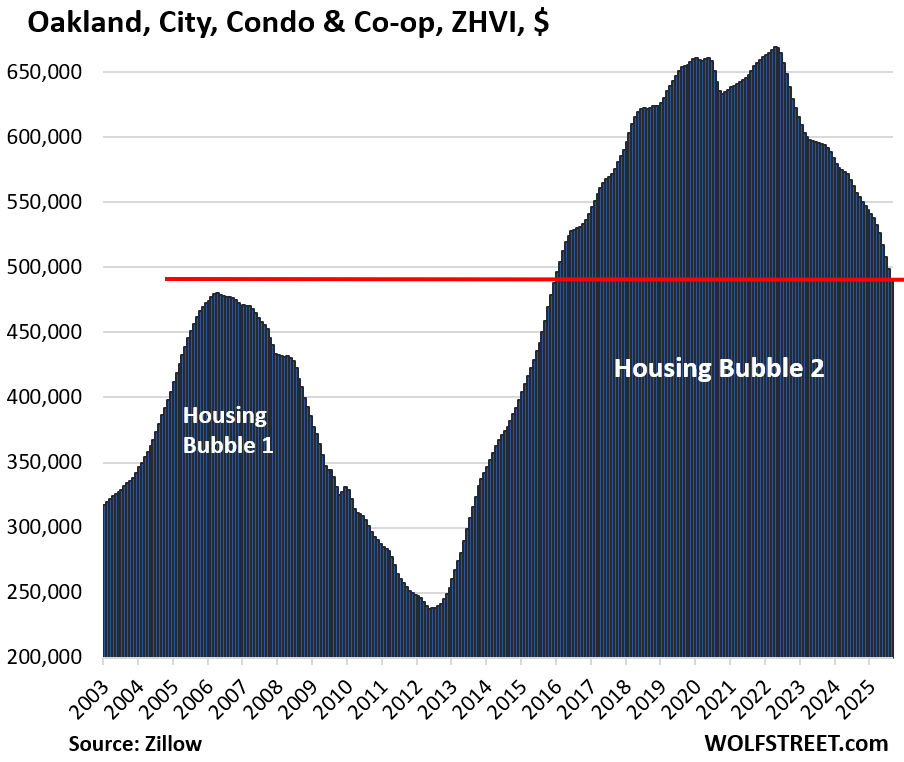

Oakland, CA, is almost there. Prices of mid-tier condos are just 0.6% above their April 2006 peak during Housing Bubble 1.

Prices have plunged by 28% from their peak in May 2022 to the lowest level since December 2015. Despite the plunge, these mid-tier condos are still the most expensive on this list, more than twice as costly as those in Ft. Myers, FL, below.

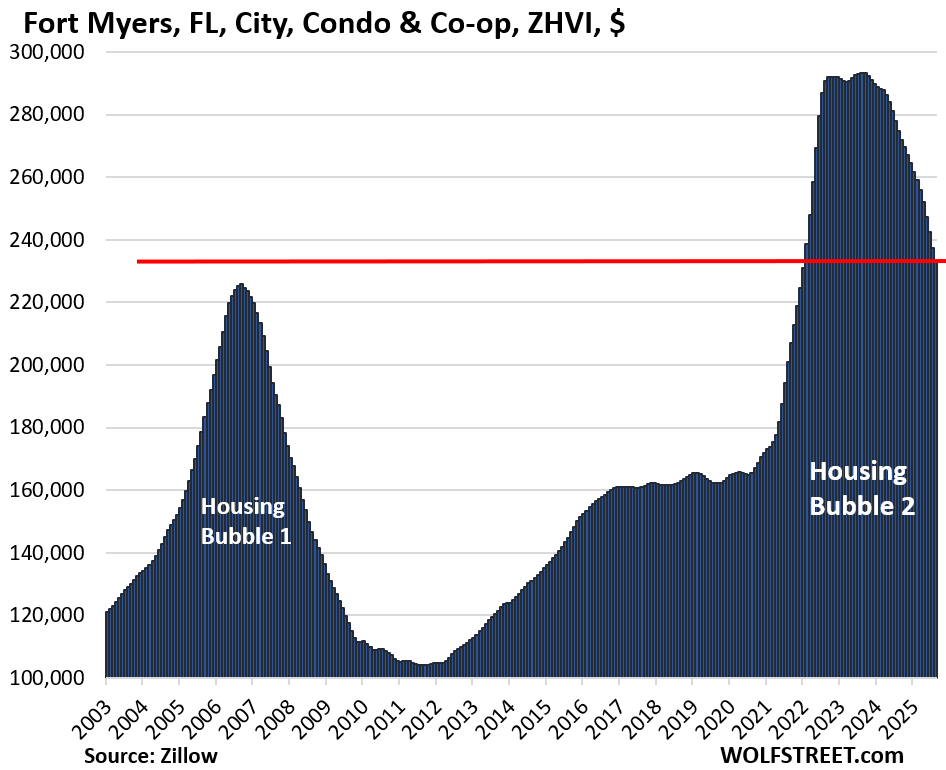

Fort Myers, FL, is almost there, with condo prices just 1.4% above the September 2006 peak during Housing Bubble 1. Prices have plunged by 21% from their peak in July 2022 and by 16% year-over-year.

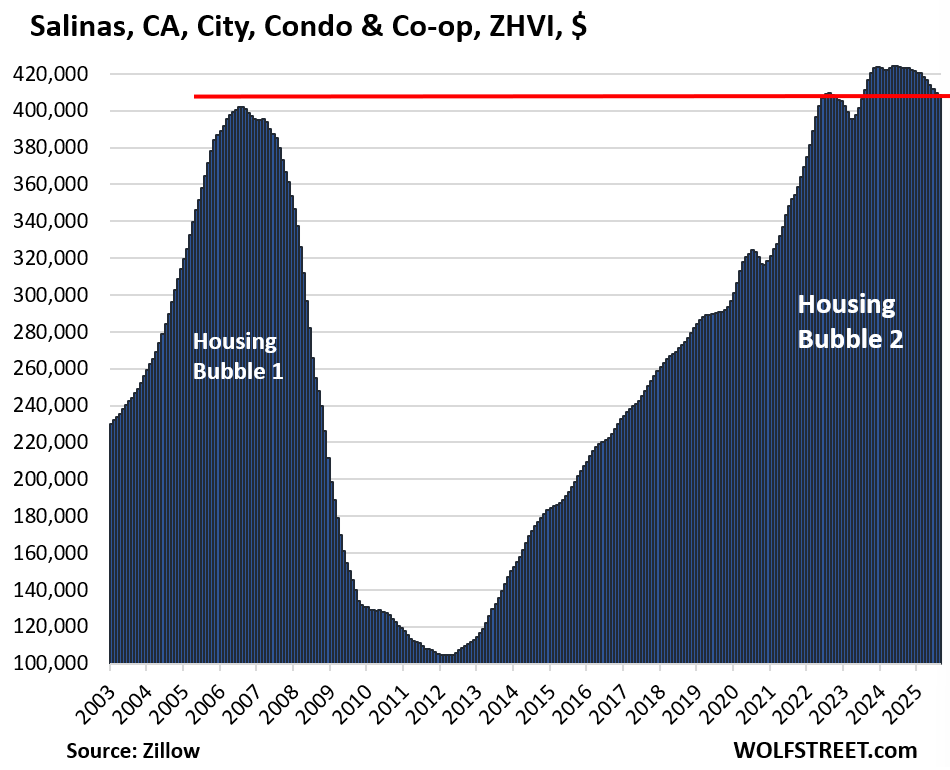

Salinas, CA, is almost there. Prices in September 2025 were just 1.5% higher than at the August 2006 Housing Bubble 1 peak, after which prices collapsed by 75% in six years, after which prices quadrupled again in 10 years.

The city is the county seat of Monterey County – which is largely rural, but also includes the cities Monterey and Carmel-by-the-Sea where some ultra-expensive homes are located, such as along 17-Mile Drive.

Note that the mid-tier condos in Salinas are the second-most expensive on this list, behind Oakland, and almost twice as expensive as in Cape Coral, FL.

And in case you missed it: Falling Mortgage Rates further Reduce Demand in the Housing Market (Not so Paradoxically)

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Boom-Bust, Boom-Bust” I remember once upon a time there was show on RT America that had the same name as well ..the amount of loonies as guests on that show talking about economic collapse definitely give Zerohedge a run for its money..actually some of them might have been the same doomer crowds running in the same circle.

And yet, here we are reading about “Boom-bust”

on Wolf Street…

Apparentl, Doomers occasionally get it right. They just refuse to grasp the concept of timing being important.

Mongoose

nah, they don’t do that, they’re just early to the show b/c they see it before everyone else does.

Bust really does happen sometimes.

But probably won’t be as bad this time because the looming debt crisis in which intelligent people will avoid Treasury bonds like the plague, will cause huge inflationary pressures, keeping prices relatively higher than the depths of the Great Reession.

If people avoid Treasury bonds like the plague it will send rates up which will not be good for housing.

Just a question

Suppose the Fed cuts once this week, once later this year and 50 basis points next year

That will place short term rates close to 3% .

Will money currently invested in short term

Treasuries stay in short term paper or will

some of this money gravitate towards longer term Treasuries ?

It will be MUCH worse. That $8 trillion of debt in 2008 is now heading up over $40 trillion, LOL.

I remember whenever there was a great price on a condo or townhome, the appeal quickly faded when you saw the HOA fees, rules, and assessments. Buying a condo during hot services inflation seems like a bit of a blank check for assessments, fees, and fines. No thanks.

I hear your point but that can easily happen with property taxes too on non-condos

Yes but taxes aren’t HOA are they? Most stuff an HOA does are things you can do your self.

I live in an urban area where we actually get to vote next week on how much to raise our own property taxes: a little or a lot. The default is a little; we have to vote to pass a proposition to make it a lot. One of the quirks of Texas state law.

The HOA fees are very small for my SFH but I’ve never been asked to vote on the tiny increases. I assume HOA fee increases for condos are equally non-democratic. So from this narrow view a SFH gets the win over a condo in my city.

Up here in Canada over the years condo fees have ramped up considerably so if you include them in the cost of ownership they have pushed against price.

Have condo fees in the USA gone up over the last 20 years as well? I would expect so simply from inflation but I don’t know….

I bought my 1b1b + Den condo in summer 2016. Monthly HOA due $835. Sold it last summer. Monthly HOA due $1,450. 😬 Not much appreciation due to lack of demand because of this HOA due. I bought it as so close to airport & I travel a lot. Would not do it again. No control over HOA dues means cost of homeownership become unpredictable. 🤨

Yes, especially in Florida, as the HOAs are responsible for hurricane insurance (which has gone up dramatically) and the post-Surfside collapse repairs that are now mandated.

The dirty secret of the “free state of Florida” is that it is unsustainable without government intervention.

That intervention is Citizens Insurance. It’s a state funded backstop when private insurers pull out after a busier than normal hurricane season.

It’s doesn’t have to be that much busier and the frequeny will only increase as the years go on. The insurers that return in each cycle seem smaller than those that left.

David,

Condo fees (Homeowner Association Fees, or HOA here) include homeowner’s insurance. So in addition to inflation in maintenance and repair costs, staffing costs at the property, and utilities to the extent provided by the property, there is homeowner’s insurance, which has spiked in some areas. So for lots of properties, HOA fees have gone up faster than inflation.

The line items I mentioned that go into HOA fees also have gone up for owners of single-family homes: homeowner’s insurance, utilities, maintenance and repair (including lawn care).

In other words, the carrying costs of a home, even without mortgage, whether condo or single-family, have gone up in general. The difference is that HOA fees hit every month, not in big lumpsums (such as a new roof or AC for owners of a SFH).

And that HOA fees, insurance, and local county, city taxes are variable costs and in general never go the opposite direction or if they do not for long. It is perhaps a function of the once-in-a-lifetime sub 3% mortgage rates contrasting with other costs which are not fixed and rising with inflation that people are saying, “hey what’s going on here!” lol

Monthly HOA fees in Florida condos were relatively suppressed until the collapse of the condo building in Surfside Florida . That disaster changed everything .As a result the state passed a law. required all buildings older than 30 years old or over 3 stories high to undergo

a certified inspection . A number of condo

buildings , which had neglected needed repairs for years , were hit with huge one time HOA assessments to cover these costs . Some condo associations chose to wrap this huge one time assessment in future monthly HOA fees while others chose to directly assess individual condo owners for this huge HOA assessment all at a once . At the same time fewer insurance companies have chosen to remain in the Florida property insurance market . due to huge payouts resulting from previous storms .

In the mid 90s I worked as an Actuary in the state of Florida for a Florida based P&C Company and got to see first hand how the state Insurance Commissioner held down rate increases for the state for years when compared to other coastal states. So I am not surprised in the least with the magnitude of insurance premium increases which have only be exacerbated by high costs to rebuild and building in more storm/flood prone areas of the state. The HOA situation is also not surprising. But the cumulative affect is a significant increase in variable costs for owning property in Florida.

Great points Wolf on home ownership as well. I thought ACs were owned by the condo owner .

As far as single family home ownership.

I have replaced just this year

HVAC 4 ton 10K

Roof 40K

Broken Windows 6K

Pool plaster 40K

Different homes different sizes different choices. So costs vary a great

So my total maintenance cost for 2025 YTD is 96K

Insurance 6K

Prop Taxes 10K

Total 112K

Texas market with a home valued at 900K for replacement costs.

Wow, that’s a stiff maintenance bill for one year!

“I thought ACs were owned by the condo owner .”

Yes (and no). The condo I owned in Tulsa had its own heat pump on my balcony and I owned it. But later in the Washington DC area, I rented a condo, and that tower had central head and AC (lousy). But probably all newer buildings have individual HVAC units.

/agree condo fees at least in GTA are insane and going up all the time. I really don’t see the value in owning a box in the sky paying $800 for condo fees on a 2 bedroom. Even new product fees start around $4-500 for studios! Lots of projects getting cancelled too.

Thanks wolf

What is going on in Lafayette LA? I didn’t know there was a single market that didn’t have a big runup during covid.

Just realized that was only condos maybe SFH are different.

Lafayette got hit by a hurricane about 5 years ago and is still recovering. I drove by there right after and it was a mess. You can still find stories about homeowners still battling the insurance company over repairs.

8:20 AM 10/27/2025

Dow 47,410.20 +203.08 0.43%

S&P 500 6,851.93 +60.24 0.89%

Nasdaq 23,561.37 +356.50 1.54%

VIX 16.03 -0.34 -2.08%

Gold 3,987.80 -150.00 -3.63%

Oil 61.97 +0.47 0.76%

This is all good news. Prices will move down to a level that attracts buyers; or vice versa. I just pray that the government (Fed,state,local) stay out of this natural and normal correction. Let the market clear.

One downside of hyper leveraging, is that government is so affected by it. For instance, government does not believe it can let poorly managed banks fail, so banks provide huge leverage on the housing market on the way up, but government interferes on way down. Debt needs to default, creditors need to suffer pain, they need to fail. Pain from defaults is what incentivizes them to be prudent.

Also, the City and counties get HOOKED on high valuations and do not lower their levies when real estate is appreciating. They cannot find ways to spend less when values decrease.

The US economy needs more market consequences

I just can not imagine a world in which they don’t try to bail out the market, stop foreclosures etc.

Agreed.

The biggest issue are municipal governments though, not creditors so much. Creditors won’t feel much pain if prices come down slowly as they have been. Not a lot of people would be willing to walk away if they’re underwater only by a thousand dollars as compared to $100,000 or more. Creditors can only start feeling pain if prices fall dramatically, which could happen but hasn’t yet. And even if they do much of the MBS are guaranteed by the federal government at present. I could see the feds going back on that due to budget/debt issues, but that is something they’d have to actually do.

But the municipal governments? They have massively overspent the windfall property taxes from the bubble. They could have paid off all their existing debt but public-sector unions have guaranteed all the influx has gone into wages and benefits for them. Municipal budgets are so screwed that even a simple pause in housing price increases will wreck their budgets. Thanks to the bubble property taxes are a very contentious issue and the movement to get rid of it completely is strong, and so most property tax rate increases can’t happen.

Only two ways out for cities:

1. Go bankrupt.

2. Go to their state legislatures and beg them to ban public sector unions, then immediately cut wages/benefits by half and fire half their workers.

Given that cities are Democrat, I highly doubt most of them will go for option 2. So if you own municipal bonds get ready to get screwed.

This is not always the case.

Here the municipalities are not spending the windfall, and have millions of dollars in rainy day funds. One municipality has been putting away ten percent of their budget each year. Eventually they are going to have to do something with it, but not all munis are irresponsible.

Hey Cb, your comment, ”The US economy needs more market consequences.”

Is SO correct!!!

And WE, in this case the workers and savers who are going to be screwed once again by lowering rates on our savings are going to pay for the crazy moves by the FRB and the paid political puppets to save the financial crooks who have stolen most of the value of our savings, etc., etc…

I really have no idea why any sane and rational person would support the FED,,, other than the banksters whom the fed has protected for over a hundred years to the completely clear detriment of the workers and savers..

Time and enough to get rid of the FRB, a completely owned operation of the banksters.

People blaming the fed and government for housing prices is all fine and dandy, and of course low interest rates are a [small] part of the problem. But the biggest part of what ran up home prices for housing bubble #2 is increasing wealth inequality. Housing and real estate of all types is an asset, and the ultra-rich and merely wealthy suck up all assets like a hoover. Falling prices recently is just indicative of housing being a weaker investment than it has been previously, and all the rich throwing money at AI nonsense these days. Look at the percentage of all cash purchases, it was a shocking 35% in 2023 after shooting up during the pandemic when wealth flowed one direction. Now it’s dropping again, and shockingly (/s) housing prices are falling.

If house prices approach a level where regular people can afford it again (and once the AI bubble has burst and the remnants of those investments need a new home), housing will all get hoovered up again by the ultra-rich. They buy it directly, they buy it for family members (I know, my neighbors all had their houses bought for them with cash by their parents and rich siblings), and they buy it through businesses. And they own the debt that ensues when regular people are forced to take out massive mortgages if they want to participate. So they profit from both sides of the equation.

Their housing can sit empty (I know, many houses where I live sit empty), it can be rented, it can be AirBnB’d. Wealthy people and private equity do not care. They also do not take care of the real estate they own.

Housing prices will never revert to [and remain at] historical affordable standards until wealth inequality is dealt with.

It’s understandable why economists avoid this topic of discussion, it sounds anti-capitalist. But it’s getting increasingly hard to ignore the elephant in the room, and needs some common-sense solutions.

The fact that a large part of the country yearns for a period in time when the top marginal tax rate was 91% should tell people something about what needs to happen.

You are clueless.

Private equity definitely takes care of its assets until it sells them at high valuations to raise capital to deploy elsewhere.

Ditto for rich folks–at least those who intend to stay rich.

Hence the term “smart money”.

The entire premise of this comment defies reality.

The top 10% account for 49% of consumption .

The top 10% account for 93% of stock ownership .

I read a recent article stating that an income of around $250,000 was required for a middle class lifestyle in Hawaii.

The very richest control a large % of assets .

I believe in capitalism but the US does enjoy capitalism , but is a system where the richest write the laws that affect them , where the richest get huge government contracts and where the richest get huge government subsidies .

Rcohn – and, may I add, do not serve militarily in numbers proportional to the protection of their societal wealth (…the advent of AI-drone slaughterbots perhaps weakening this observation…).

may we all find a better day.

Right on brother,,,

NOT since the days when Wild Bill convinced many of the oligarchy to either join, the OSS or others to fight in WW2 have the rich folks ventured to put their sons and daughters at risk.

At that time, clearly, if was either join or quickly learn to speak German or Japanese.

WEB Griffin tells us all we need to know about that era in his earlier works…

Have heard a lot of conflicting and different stats on that esp the proportion of consumption by the high 10% of earners, they’re varied a lot on the exact number maybe because is hard to measure and so many different ways to measure it, it’s not like we have a single uniform payment system in the US or a “tracker” that labels and counts purchases based on someone’s wealth level, so it’s always going to be a lot of estimates and guesswork. It is disproportionate high and it does reflect problems with America’s unstable middle class and inequality extremes but the claim of consumption by the 10% being half sounds like click-bait headline and some figures seem to say otherwise.

And it really doesn’t make sense either. A billionaire can’t buy 200 expensive Michelin star restaurant dinners or get 200 fancy haircuts a day to make up for a relative loss of spending power by a growing struggling middle class or working poor who can’t. And even if they have much higher luxury spending in other ways it’s not going to make up for less spending by huge majorities seeing their savings and affordability going down from inflation and living costs. This is why Econ 101 teaches us it’s best to have broad spending by working poor and middle classes with good spending power instead of concentrate wealth into hands of fewer and fewer ultra-rich families like a feudal system, that’s the structure for 3rd world countries after all. So while the 10% may spend disproportionate it’s doubtful that high, maybe half that. (which is of course still a huge disproportion) For the working poor and middle class in America there’s been both increasing income and higher debt levels, And for student loans and auto loans, more delinquency. (who knows about buy now and pay later) All the same, seems like a weak argument for a rate cut the pivot-mongers are constantly calling for–we have 3% CPI inflation and 3.1% core, and if inequality and job loss to structural issues (or tariffs) a rate cut would no nothing to help that while make inflation even worse.

Your comment about spending power is only true if the economy needs more consumption.

I can tell you just by looking at the trade deficit that consumption is not a thing that America needs more of. What we need are investments (more factories, more transport infrastructure, etc.), which means money will be funneled upwards to the rich until the investment demands are met.

This is happening slower than it should because of welfare though. And welfare also double-squeezes workers because they’re taxed to pay for it. And most of the people who get most of the welfare aren’t working – I know this because most of the welfare money is spent on Social Security and Medicare, not to mention all the entitled people now making social media posts about never having worked for decades until SNAP began to require community service or a full time job.

If you want less income inequality these investments have to be done, and the only way you can accelerate these investments getting done is to crush welfare. And once that’s done then income inequality can (and must!) start to fall. But only then.

A free investment market would remove these wealth distortions fairly quickly. Unfortunately, the wealth disparities and distortions can remain for decades when governments suppress interest rates and maintain ample liquidity regimes that promote inflation of asset prices.

What would happen if the Government said it would cap the debt-to-GDP ratio or abandon the use of QE in the future? We’d have an asset price leveler event followed by decades of strong sustainable growth that is better dispersed throughout the population. The public needs that, but it would destroy political careers that rely on wealth concentration and avoidance of recession.

@jack basically agreed with you here, I don’t like this hyper-focussing on consumption in America and the way overconsumption not only clutters neighborhoods and hurts the environment, but also just seems to damage so many people’s minds and basic financial literacy, I see this in friends and family all the time. I’ve even had successful close friends with good careers and families start drowning in debt and wind up in trouble because they couldn’t resist signing up for that +$80K shiny new truck they’ don’t need and put on a 72 or 84 month payment plan, and the shiniest new iphone (that’s not even as good as the working one they already have) or theme park trip with a $4K resort stay. And then suddenly they’re maxxing out credit cards and using buy now pay later and going deeper in debt, it’s like a disease and even worse, this overconsumption too fuels the inflation makes things even more expensive for the rest of us too. Part of why cars cost so much (leave alone homes), is so many FOMO buyers delude themselves into look at only the monthly cost instead of total cost and how much more a 72-month financing costs, so this consumption mania makes everything worse.

And agreed on the better investment part, just so the long as the investment is wise and better allocated than what we have right now with the AI bubble. It’s such a disaster of poorly allocated assets it’s sucking out hundreds of billions of dollars in resources better used in the rest of the US economy, all for terrible ROI and noisy, power and water guzzling data centers that ruin towns and drive up utilities hundreds or thousands of dollars a year for residents and businesses already stressed by cost of living and their dollar losing buying power. And for all this, we’re getting massive low quality AI slop and bots that’s choking off the useful parts of the Internet like weeds, basically mass plagiarizing from authors and artists, hallucinating so bad it’s messing up data streams, getting worse training on their own AI slop and now basically ruining education. It can certainly be useful for some things with specific applications but as always, the financial squawkers and Silicon Valley hyped it way beyond what it could do and now we’re in a massive bubble fueled by probably the biggest malinvestment in history, making even dot com bubble look tame.

The vast majority of those cash purchases are small mom and pop landlords who have no idea what they’re doing and will sell as soon as it becomes obvious how little cash flow rental real estate actually produces at these prices.

Robert Banks,

“But the biggest part of what ran up home prices for housing bubble #2 is increasing wealth inequality. Housing and real estate of all types is an asset, and the ultra-rich and merely wealthy suck up all assets like a hoover.”

65% of households own their own home = regular people.

“The fact that a large part of the country yearns for a period in time when the top marginal tax rate was 91% should tell people something about what needs to happen.”

Why not a 100% tax rate? It’s only 900bps higher /s

The only thing it tells me is that a large part of the country is stupid.

@Robert Banks what percentage of the $120K Condos in Lafayette, LA do you think are purchased by the “ultra-rich and merely wealthy”?

Do you actually “know” that any of the vacant homes near you are owned by “Wealthy people and private equity”? I have never heard of private equity letting homes sit empty and wealthy people typically only do it when they are not actively using the property or the owners are fighting over what to do with it.

The way to tell would be look at the tax records and see if one of the big equity buy out companies owns any of those properties. Here are just some of the names to look for. Many have been bought and resold by private equity companies.

Invitation Homes

American Homes 4 Rent

Invitation Homes 2

Tricon Residential

Opendoor

CoreVest Finance

It would be interesting to know which SFH are below 20 year price.

I assume this is in nominal dollars vs real dollars. Inflation adjusted dollars that’s a big loss!!