Boom-Bust, Boom-Bust?

By Wolf Richter for WOLF STREET.

Condo prices have shown that they’re subject to huge booms and busts. Here we’re going to look at bigger cities where prices of mid-tier condos have dropped below where they had been about 20 years ago at their respective peaks during Housing Bubble 1. There are not many among the bigger cities we’re tracking, but there are some.

The other day, we discussed the 23 Bigger Cities where Condo Prices Dropped by 12% to 28% through September. Prices in most of those 23 cities were still well above their highs of Housing Bubble 1. But in a few, they weren’t, and they’re back under the limelight here.

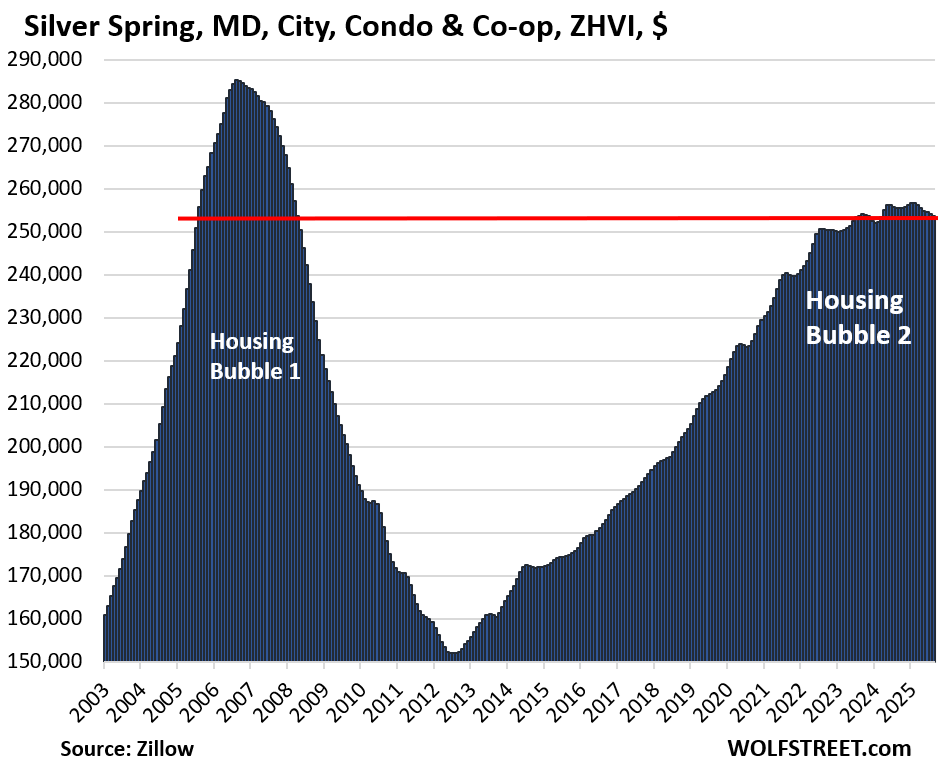

Silver Spring, MD: Prices of mid-tier condos in September 2025 were 11% below the peak in August 2006 and were back to where they had first been in August 2005, over 20 years ago. This city in the Washington DC metro had a gigantic condo bubble from January 2003 through August 2006, when prices of mid-tier condos exploded by 78%, before collapsing and giving up more than the entire gain by mid-2012. Then it started all over again, but more slowly.

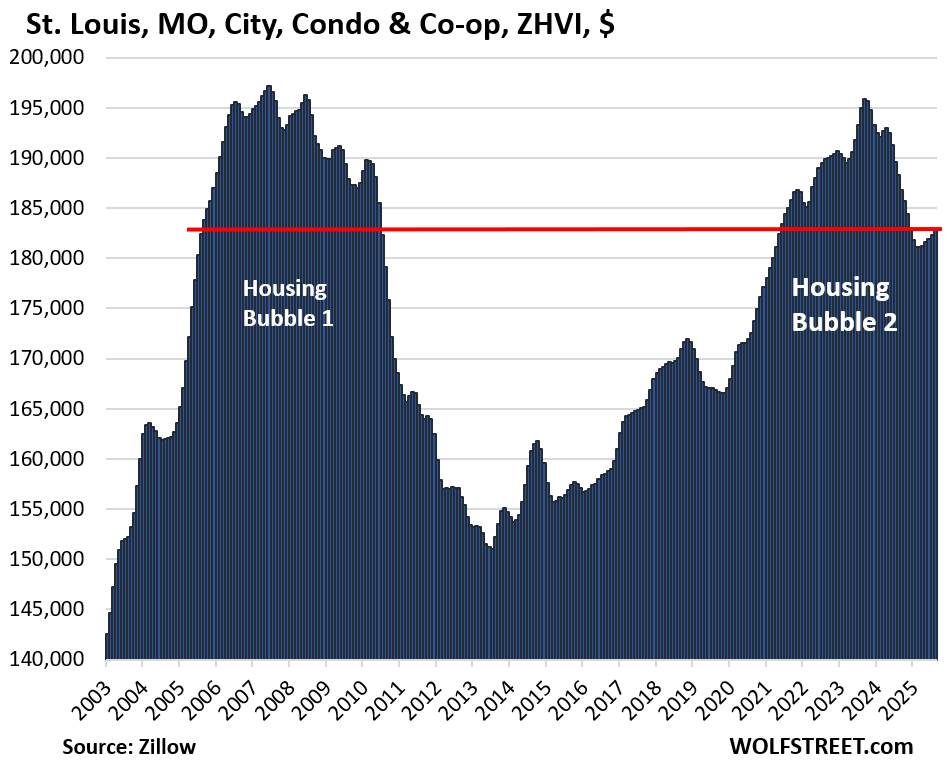

St. Louis, MO: Prices of mid-tier condos in September 2025 were 7% below July 2007, and were back where they had first been in September 2005.

Methodology and data: These prices here are seasonally adjusted three-month averages of “mid-tier” condos and co-ops in “cities” from the Zillow Home Value Index (ZHVI), which is based on millions of data points in Zillow’s “Database of All Homes,” including from public records (tax data), MLS, brokerages, local Realtor Associations, real-estate agents, and households across the US. It includes pricing data for off-market deals and for-sale-by-owner deals. These are not median prices.

Some of the bigger cities might not be included here. The ZVHI for condos does not have data going back to 2003 for all cities, though it has more recent data on them. And so any of these cities with incomplete data, whose prices might have dropped below Housing Bubble 1 peaks, would not be included here.

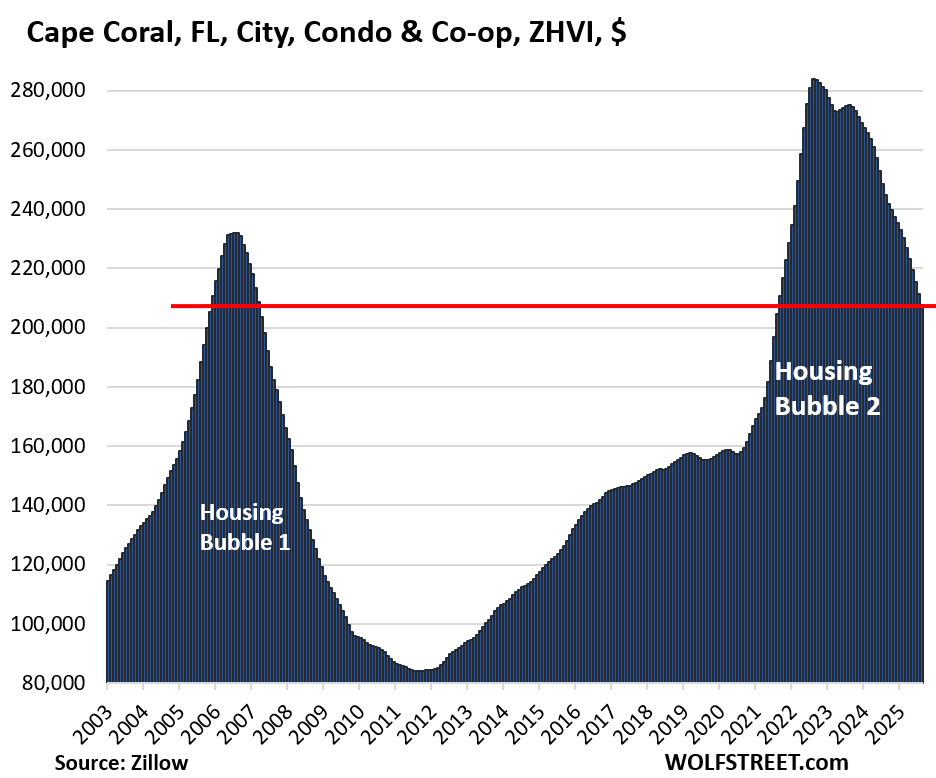

Cape Coral, FL: Prices of mid-tier condos in September plunged back to where they had first been in November 2005, and were 12% below the July 2006 peak of Housing Bubble 1. Epic Boom-Bust, Boom-Bust.

Prices have plunged by 28% from their peak in July 2022 and by 16% year-over-year.

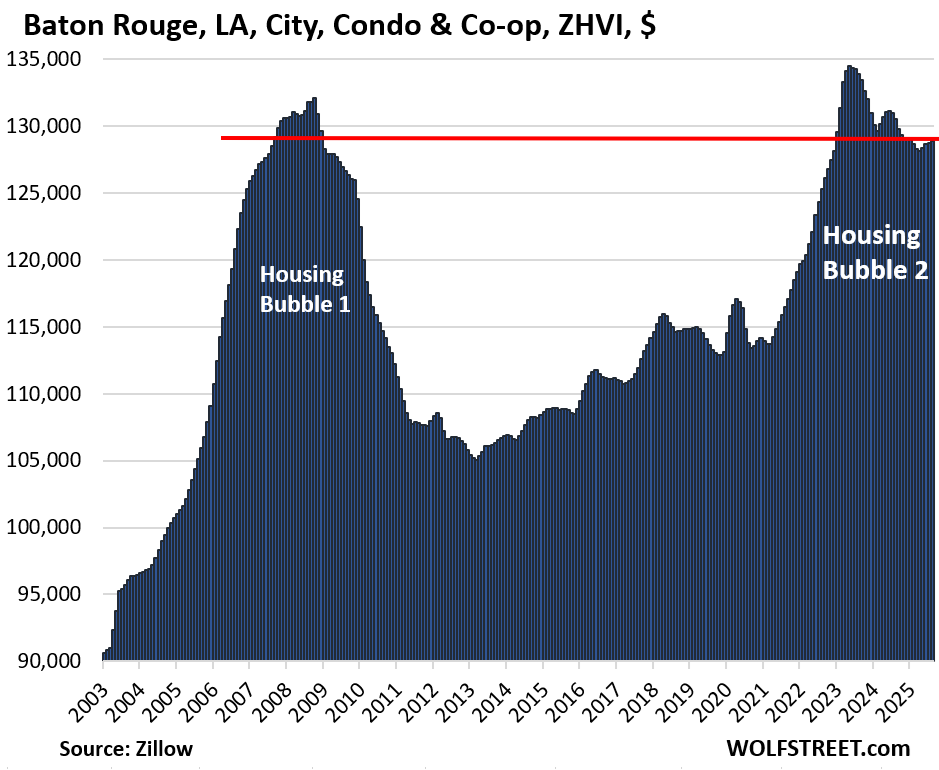

Baton Rouge, LA: Prices of mid-tier condos in September 2025 were 3% below the September 2008 peak during Housing Bubble 1 and were back where they’d first been in August 2007.

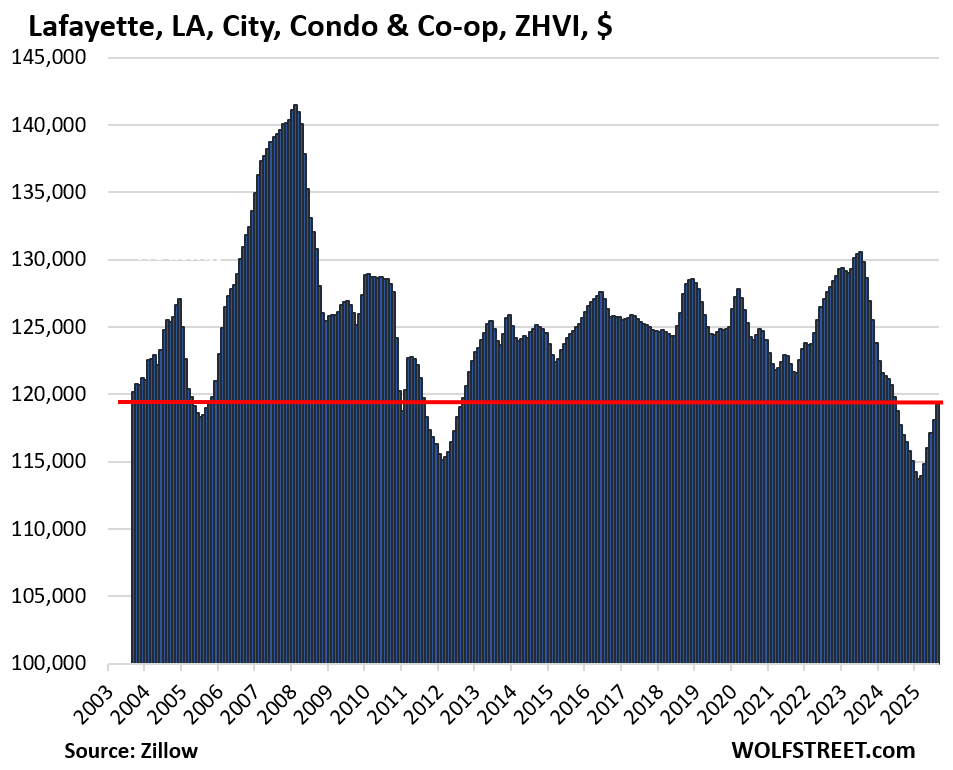

Lafayette, LA: This isn’t a bubble market, though it made a valiant effort in 2006. Prices of mid-tier condos in September 2025 were 15% below their peak in January 2008, and were below where they’d been in September 2003, the extent of the ZHVI condo data. Most of the 22 years in between, prices had been higher than in September 2025.

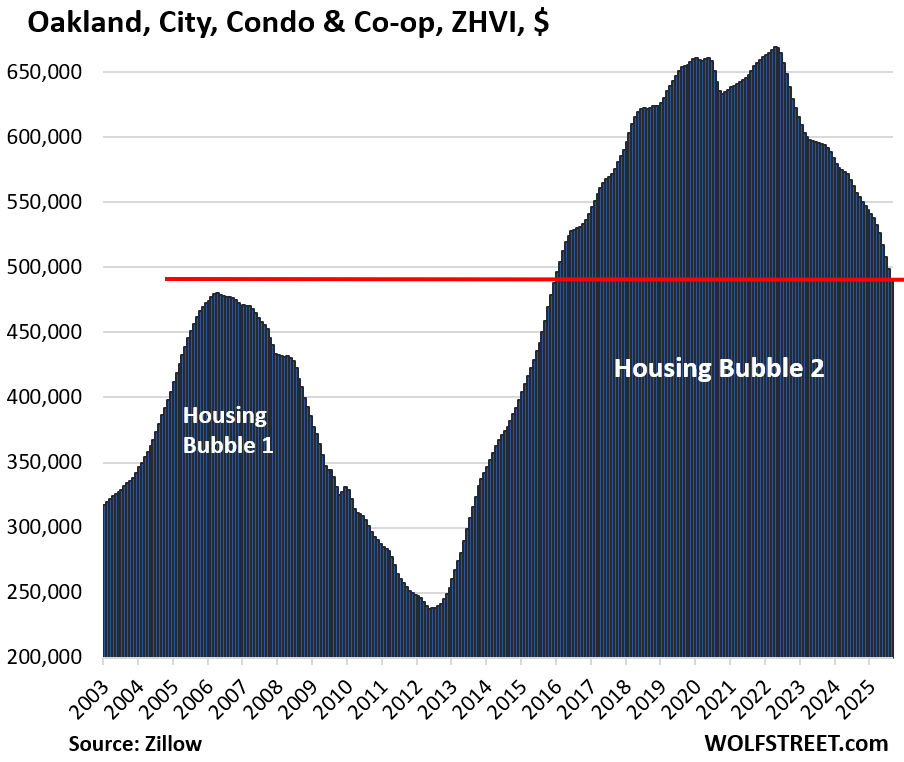

Oakland, CA, is almost there. Prices of mid-tier condos are just 0.6% above their April 2006 peak during Housing Bubble 1.

Prices have plunged by 28% from their peak in May 2022 to the lowest level since December 2015. Despite the plunge, these mid-tier condos are still the most expensive on this list, more than twice as costly as those in Ft. Myers, FL, below.

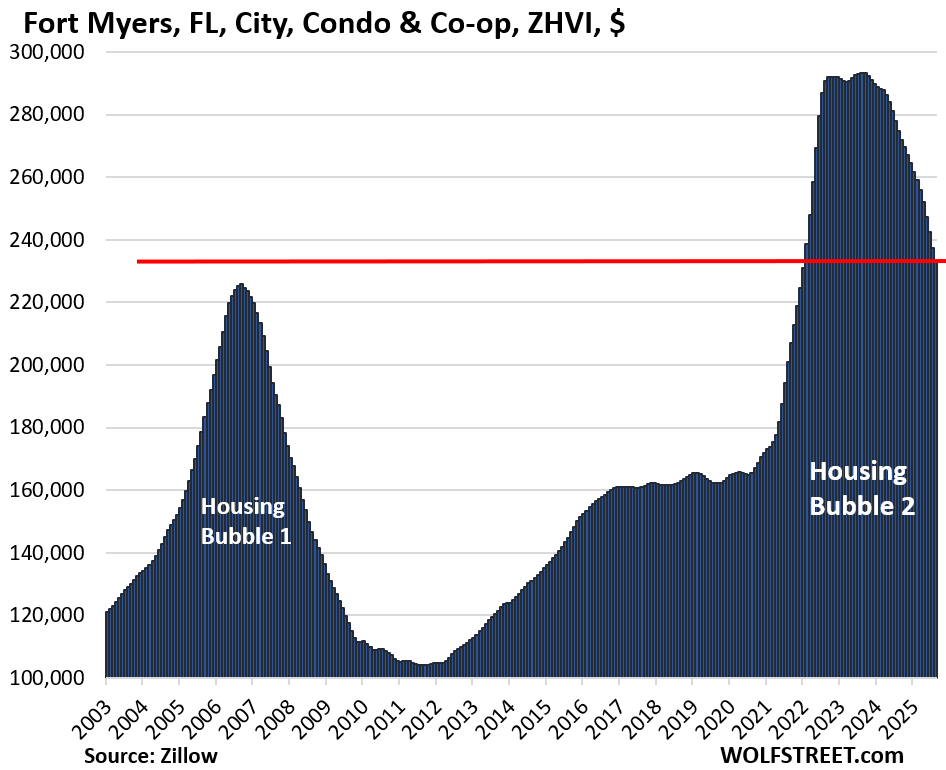

Fort Myers, FL, is almost there, with condo prices just 1.4% above the September 2006 peak during Housing Bubble 1. Prices have plunged by 21% from their peak in July 2022 and by 16% year-over-year.

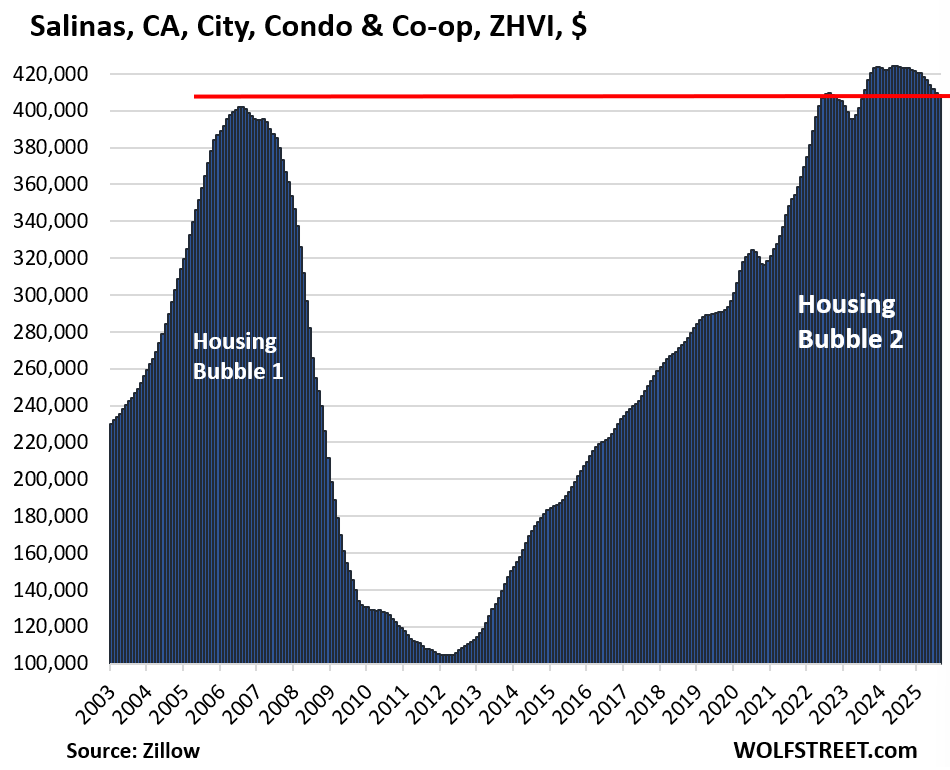

Salinas, CA, is almost there. Prices in September 2025 were just 1.5% higher than at the August 2006 Housing Bubble 1 peak, after which prices collapsed by 75% in six years, after which prices quadrupled again in 10 years.

The city is the county seat of Monterey County – which is largely rural, but also includes the cities Monterey and Carmel-by-the-Sea where some ultra-expensive homes are located, such as along 17-Mile Drive.

Note that the mid-tier condos in Salinas are the second-most expensive on this list, behind Oakland, and almost twice as expensive as in Cape Coral, FL.

And in case you missed it: Falling Mortgage Rates further Reduce Demand in the Housing Market (Not so Paradoxically)

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Boom-Bust, Boom-Bust” I remember once upon a time there was show on RT America that had the same name as well ..the amount of loonies as guests on that show talking about economic collapse definitely give Zerohedge a run for its money..actually some of them might have been the same doomer crowds running in the same circle.

And yet, here we are reading about “Boom-bust”

on Wolf Street…

Apparentl, Doomers occasionally get it right. They just refuse to grasp the concept of timing being important.

Mongoose

Bust really does happen sometimes.

But probably won’t be as bad this time because the looming debt crisis in which intelligent people will avoid Treasury bonds like the plague, will cause huge inflationary pressures, keeping prices relatively higher than the depths of the Great Reession.

If people avoid Treasury bonds like the plague it will send rates up which will not be good for housing.

Just a question

Suppose the Fed cuts once this week, once later this year and 50 basis points next year

That will place short term rates close to 3% .

Will money currently invested in short term

Treasuries stay in short term paper or will

some of this money gravitate towards longer term Treasuries ?

I remember whenever there was a great price on a condo or townhome, the appeal quickly faded when you saw the HOA fees, rules, and assessments. Buying a condo during hot services inflation seems like a bit of a blank check for assessments, fees, and fines. No thanks.

I hear your point but that can easily happen with property taxes too on non-condos

Up here in Canada over the years condo fees have ramped up considerably so if you include them in the cost of ownership they have pushed against price.

Have condo fees in the USA gone up over the last 20 years as well? I would expect so simply from inflation but I don’t know….

I bought my 1b1b + Den condo in summer 2016. Monthly HOA due $835. Sold it last summer. Monthly HOA due $1,450. 😬 Not much appreciation due to lack of demand because of this HOA due. I bought it as so close to airport & I travel a lot. Would not do it again. No control over HOA dues means cost of homeownership become unpredictable. 🤨

Yes, especially in Florida, as the HOAs are responsible for hurricane insurance (which has gone up dramatically) and the post-Surfside collapse repairs that are now mandated.

David,

Condo fees (Homeowner Association Fees, or HOA here) include homeowner’s insurance. So in addition to inflation in maintenance and repair costs, staffing costs at the property, and utilities to the extent provided by the property, there is homeowner’s insurance, which has spiked in some areas. So for lots of properties, HOA fees have gone up faster than inflation.

The line items I mentioned that go into HOA fees also have gone up for owners of single-family homes: homeowner’s insurance, utilities, maintenance and repair (including lawn care).

In other words, the carrying costs of a home, even without mortgage, whether condo or single-family, have gone up in general. The difference is that HOA fees hit every month, not in big lumpsums (such as a new roof or AC for owners of a SFH).

And that HOA fees, insurance, and local county, city taxes are variable costs and in general never go the opposite direction or if they do not for long. It is perhaps a function of the once-in-a-lifetime sub 3% mortgage rates contrasting with other costs which are not fixed and rising with inflation that people are saying, “hey what’s going on here!” lol

Monthly HOA fees in Florida condos were relatively suppressed until the collapse of the condo building in Surfside Florida . That disaster changed everything .As a result the state passed a law. required all buildings older than 30 years old or over 3 stories high to undergo

a certified inspection . A number of condo

buildings , which had neglected needed repairs for years , were hit with huge one time HOA assessments to cover these costs . Some condo associations chose to wrap this huge one time assessment in future monthly HOA fees while others chose to directly assess individual condo owners for this huge HOA assessment all at a once . At the same time fewer insurance companies have chosen to remain in the Florida property insurance market . due to huge payouts resulting from previous storms .

In the mid 90s I worked as an Actuary in the state of Florida for a Florida based P&C Company and got to see first hand how the state Insurance Commissioner held down rate increases for the state for years when compared to other coastal states. So I am not surprised in the least with the magnitude of insurance premium increases which have only be exacerbated by high costs to rebuild and building in more storm/flood prone areas of the state. The HOA situation is also not surprising. But the cumulative affect is a significant increase in variable costs for owning property in Florida.

Thanks wolf

What is going on in Lafayette LA? I didn’t know there was a single market that didn’t have a big runup during covid.

Just realized that was only condos maybe SFH are different.

This is all good news. Prices will move down to a level that attracts buyers; or vice versa. I just pray that the government (Fed,state,local) stay out of this natural and normal correction. Let the market clear.

One downside of hyper leveraging, is that government is so affected by it. For instance, government does not believe it can let poorly managed banks fail, so banks provide huge leverage on the housing market on the way up, but government interferes on way down. Debt needs to default, creditors need to suffer pain, they need to fail. Pain from defaults is what incentivizes them to be prudent.

Also, the City and counties get HOOKED on high valuations and do not lower their levies when real estate is appreciating. They cannot find ways to spend less when values decrease.

The US economy needs more market consequences

I just can not imagine a world in which they don’t try to bail out the market, stop foreclosures etc.

People blaming the fed and government for housing prices is all fine and dandy, and of course low interest rates are a [small] part of the problem. But the biggest part of what ran up home prices for housing bubble #2 is increasing wealth inequality. Housing and real estate of all types is an asset, and the ultra-rich and merely wealthy suck up all assets like a hoover. Falling prices recently is just indicative of housing being a weaker investment than it has been previously, and all the rich throwing money at AI nonsense these days. Look at the percentage of all cash purchases, it was a shocking 35% in 2023 after shooting up during the pandemic when wealth flowed one direction. Now it’s dropping again, and shockingly (/s) housing prices are falling.

If house prices approach a level where regular people can afford it again (and once the AI bubble has burst and the remnants of those investments need a new home), housing will all get hoovered up again by the ultra-rich. They buy it directly, they buy it for family members (I know, my neighbors all had their houses bought for them with cash by their parents and rich siblings), and they buy it through businesses. And they own the debt that ensues when regular people are forced to take out massive mortgages if they want to participate. So they profit from both sides of the equation.

Their housing can sit empty (I know, many houses where I live sit empty), it can be rented, it can be AirBnB’d. Wealthy people and private equity do not care. They also do not take care of the real estate they own.

Housing prices will never revert to [and remain at] historical affordable standards until wealth inequality is dealt with.

It’s understandable why economists avoid this topic of discussion, it sounds anti-capitalist. But it’s getting increasingly hard to ignore the elephant in the room, and needs some common-sense solutions.

The fact that a large part of the country yearns for a period in time when the top marginal tax rate was 91% should tell people something about what needs to happen.

The top 10% account for 49% of consumption .

The top 10% account for 93% of stock ownership .

I read a recent article stating that an income of around $250,000 was required for a middle class lifestyle in Hawaii.

The very richest control a large % of assets .

I believe in capitalism but the US does enjoy capitalism , but is a system where the richest write the laws that affect them , where the richest get huge government contracts and where the richest get huge government subsidies .

The vast majority of those cash purchases are small mom and pop landlords who have no idea what they’re doing and will sell as soon as it becomes obvious how little cash flow rental real estate actually produces at these prices.

@Robert Banks what percentage of the $120K Condos in Lafayette, LA do you think are purchased by the “ultra-rich and merely wealthy”?

Do you actually “know” that any of the vacant homes near you are owned by “Wealthy people and private equity”? I have never heard of private equity letting homes sit empty and wealthy people typically only do it when they are not actively using the property or the owners are fighting over what to do with it.

The way to tell would be look at the tax records and see if one of the big equity buy out companies owns any of those properties. Here are just some of the names to look for. Many have been bought and resold by private equity companies.

Invitation Homes

American Homes 4 Rent

Invitation Homes 2

Tricon Residential

Opendoor

CoreVest Finance