American consumers are doing OK on their auto loans.

By Wolf Richter for WOLF STREET.

Every time a specialized privately-owned subprime auto dealer-lender implodes – which happens periodically in this high-risk-high-profit business – the headlines are full with, Oh Deary, the American Consumer is cracking, tapped out, stressed out, and in free-fall, or whatever. Some even put into the headlines some nonsense about surging delinquency rates. And the latest collapse of an auto dealer-lender, that of Tricolor Holdings, is no exception.

The debris of Tricolor, a privately owned AI-powered fintech used-vehicle-dealer-lender with 60 stores, is now being picked through in a Texas bankruptcy court, amid a mushroom cloud of fraud allegations by lenders from all directions, after they’d closed their eyes for years in order to not see what they should have seen but didn’t want to see because they were lusting after the high interest rates and fees. So now, part of that money has vanished.

But don’t cry for the lenders. They knew that Tricolor largely lent recklessly to illegal immigrants with no driver’s license and no credit rating (so they weren’t even subprime), which Tricolor marketed as “social lending.”

Social lending has been promoted for over two decades by the federal government through the Community Reinvestment Act (CRA) and the Community Development Financial Institutions (CDFI) Act. In 2019, the Treasury Department certified Tricolor as a CDFI, granting it a federal endorsement as a “socially responsible” lender.

It’s hard to imagine a more intensely reeking cesspool than Tricolor – a bankruptcy trustee said that the initial reports “indicated potentially systemic levels of fraud” – and it’s hard to imagine more reckless banks, lenders, and investors who eagerly closed their eyes to these shenanigans because they were chasing yield and they didn’t want reality to get in the way – typical behavior at the peak of a credit bubble. But it has zero to do with the cracking or whatever American consumer.

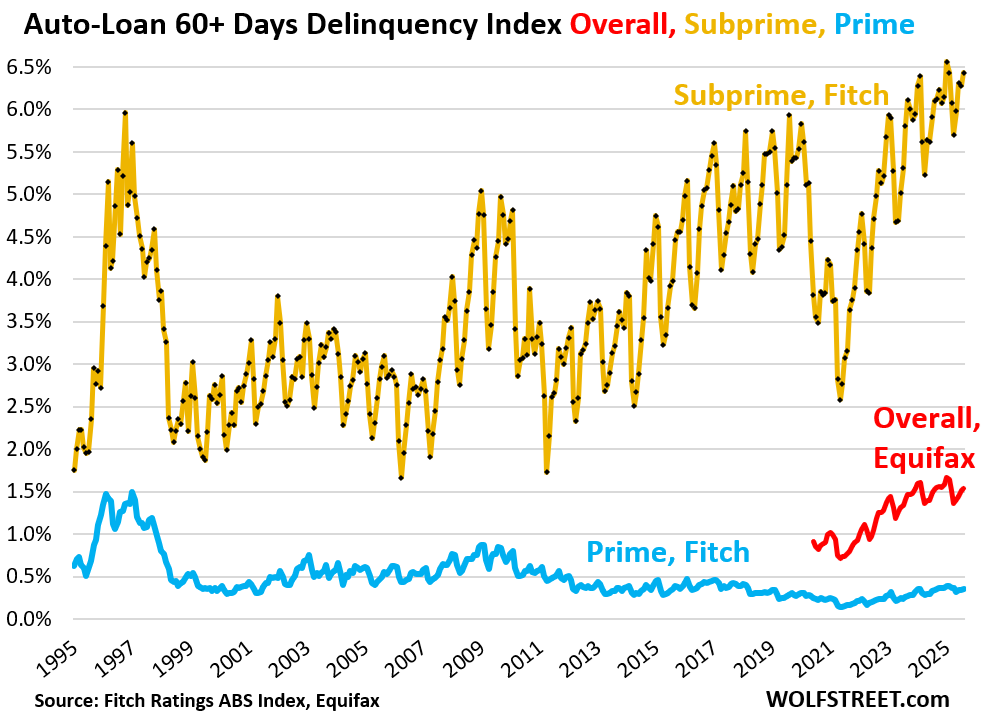

Consumers and their auto loans are doing OK.

All auto loans and leases, including subprime, had a 60-plus-day delinquency rate of 1.54% in August, about the same as a year ago, according to Equifax. The seasonal high was in January at 1.66%. Available monthly data from Equifax only goes back to July 2020, the absolute low of the free money era and lacks the pre-pandemic normal years (red in the chart below).

Prime-rated auto loans had a 60-day delinquency rate of 0.35% in August, roughly the same as a year ago, a little higher than in the free-money era, a hair lower than in 2017 and 2018, according to data from Fitch which rates auto-loan ABS. During the Great Recession, it peaked at 0.9%. In the mid-1990s, when auto-loan securitization was still new and was handled by cowboys, it peaked at 1.5% (blue in the chart).

Subprime means bad credit – a history of being late in paying obligations and not paying them at all. It does not mean low income. The young dentist in over his head is a classic example of higher-income subprime. They’ll get it worked out eventually. Low-income people often cannot borrow at all, and if they can borrow, the amounts are small.

But an outfit like Tricolor – and other specialized subprime dealer-lender chains that have collapsed, such as two in 2023 that I covered here – can lend recklessly, and these securitized auto loans blow up and drive the subprime delinquency rate.

Subprime auto lending is a small part of auto lending, done mostly by specialized lenders and specialized dealer-lenders, and is limited mostly to older used vehicles.

Fitch’s subprime 60-day-plus delinquency rate rose to 6.43% in August along seasonal patterns. The seasonal peak was in January at 6.56%, an all-time high. Compared to August a year ago, the delinquency rate was 33 basis points higher (gold in the chart).

Tricolor was a AI fintech star in Texas.

In 2023, the Dallas tech media still gushed:

“Tricolor, the largest used vehicle retailer to the Hispanic market in the US, has secured a new patent for its innovative AI tool called Automás. The tool lets customers self-select and finance vehicles, generating offers for different models and financing terms with machine learning. A unique feature of Automás is that it empowers customers to customize their own financing terms within the parameters of the system-generated offer.

“Tricolor said the new tool, U.S. Patent No. 11,574,362, leverages data across the company’s integrated platform to give historically marginalized consumers the power of self-selection when choosing and financing a vehicle from Tricolor.”

The funding for these deals.

Big used-vehicle-dealer-lenders obtain financing for the inventory of vehicles and for the auto loans they originate in three phases:

Floorplan line of credit, under which each vehicle, identified by its VIN, serves as collateral for a portion of the loan. The purchase of the vehicle is funded through the floorplan, and when the vehicle is sold, that portion of the loan is paid off.

Warehouse line of credit, under which the auto loans extended to vehicle buyers are temporarily funded by banks. In other words, funds from the warehouse line of credit are used to pay off the floorplan when the vehicle is sold. The collateral is each loan, collateralized by that vehicle.

Securitization, through which auto loans that had been temporarily funded through a warehouse line of credit are packaged into Asset-Backed Securities (ABS) and sold to institutional investors around the globe. The proceeds from the sale of the securities pay off the warehouse line of credit for those vehicles. These ABS are backed by auto loans that are collateralized by the vehicles.

And they’re all now alleging all kinds of sordid stuff. These three types of lenders to Tricolor, and a federal government investigation, have formed a mushroom cloud of fraud allegations. Tricolor allegedly pledged the same vehicles as collateral for multiple loans from multiple lenders, misrepresented the credit quality of the borrowers, understated the risks of the loans, etc., etc., and money has vanished.

But the last securitization occurred in June, $217 million, three months before Tricolor’s collapse, when everyone involved was still trying to close their eyes as hard as they could. A unit of Tricolor was also the servicer of the securitization; borrowers are supposed to send their payments to this unit of Tricolor, which is then supposed to forward the passthrough principal payments and interest to the ABS holders.

S&P Global rated the six slices of the $217 million Tricolor Auto Securitization Trust 2025-2. The four top-rated slices were all “investment grade” and amounted to $189 million, or 87%, of that securitization (my cheat sheet for corporate bond credit ratings by ratings agency):

- ‘AA’: $131 million

- ‘A’: $27 million

- ‘A-‘: $14 million

- ‘BBB’: $17 million.

The four slices were rated “investment grade” on the theory that the two lower-rated slices, representing 13% of the securitization, would eat the first losses, after the credit support measures built into the offering were used up, and that this would be enough to protect the investment-grade slices from losses when the borrowers – mostly illegal immigrants – failed to make their payments and failed to return the vehicle.

On September 12, two days after Tricolor had filed for liquidation in bankruptcy court, S&P Global put the bonds on “CreditWatch with negative implications.”

Tricolor was a creature of alleged fraud, taking advantage of willfully blind lenders and investors in the midst of a huge credit bubble when greed had turned their brains to mush. And it has nothing to do with American consumers and their auto loans.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This is a dynamite piece, Wolf. I’m a corporate bankruptcy professional focused on CRE; the tide is washing out and providing a good view of random trash and dead bodies. It’s getting exciting! ZIRP and Covid Era Stimulus Squared fostered spectacularly profligate lending. (Good thing rates would never go up. 🙄). Of course, it’s always other people’s money getting thrown to the dogs. Some lender might lose his bonus or his job and get nasty things said about him in court. Big deal. The money is somebody’s ephemeral pension.

Are you a lawyer or do you work for a special services?

The issue is not so much subprime borrowers but subprime lenders.

“not so much subprime borrowers but subprime lenders.”

Nice one.

1) The true obscenity is that intentionally crappy underwriting is pretty simply a case of “adverse selection” – a topic fairly heavily covered in sophmore Econ 201. It ain’t like such dangers were “impossible to predict.”

2) Especially…since exactly the same dynamics (intentionally crappy risk underwriting) blew up the world rather dramatically by 2008. Same crap, different flavoring – less than 10-15 declining years later.

3) More or less all of this can be laid at the doorstep of ZIRP – whose creation of yield starvation intentionally motivates half-educated institutional investors to take on more and more risk in the service of trying to fund corrupt/moron “promises” to their “beneficiaries” – themselves willingly blind for decades.

4) And ZIRP itself is a function of the real-economy collapse of America’s intentional competitiveness over the last 25 years – an inescapable fact that escapist DC would do anything (ZIRP) rather than admit/address.

FYI: BlackRock put $90mn behind Tricolor in 2021, touting it as one of the asset manager’s first commitments in its “impact opportunities” strategy and for its use of artificial intelligence.

I’m betting a box of milk bones, that BlackRock was behind the patent process from the beginning , and they’ll probably mysteriously end up with that super valuable asset — that provided to be so critical in stealing cash ….

See also:

Creditors of PrimaLend, which provides financing to auto dealerships that cater to subprime borrowers, are weighing pushing the firm into bankruptcy after going unpaid for months, and as the industry reels from the recent downfall of Tricolor Holdings. Holders of the company’s $75 million bond due in 2028 are working with lawyers…

When money changes hands, signatures are required. Time for signatories to assume debts or occupy the cell. Until people are actually jailed – nothing will change.

Perfect

yea dont hold your breath. Animal spirits and all.

I wonder where all the money went from multiple financing of the same assets?

Yes, lots of people are wondering about that. It went somewhere.

They better start warming up the printing presses for the next $10 Trillion bailout of all the AAA investments out there in the wild. Just Sam Altman’s shenanigans are going to need a trilly or two.

I learned a new word: “trilly”. Love it!

What about Carmax ?

They’re not a dealer-lender, and they don’t target subprime.

But Car-Mart targets subprime and is a dealer-lender. They’re publicly traded [CRMT], and their stock today hit a new 10-year low.

I wrote about it back when they ran into trouble in December 2023, and it has become part of my Imploded Stocks.

https://wolfstreet.com/2023/12/06/subprime-comes-home-to-roost-for-specialized-auto-dealers-lenders-their-investors-car-mart-was-next-to-confess/

You may be too sanguine. How do we account for the additional allowances for losses that KMX made in their last 10-Q? They were being too aggressive previously? Just a blip? We’ll know soon enough as AN, CVNA and other lenders release their quarterly results.

What I said is:

“They’re not a dealer-lender, and they don’t target subprime.”

That is also true for CNVA and AN.

No one said that the car business is easy these days, but these dealers don’t carry the note, and they don’t sell to unrated buyers, such as illegal immigrants. They’re in a business that Tricolor chose not to be in.

Back in late July/ early August of 2007, the very first two subprime mortgage hedge funds blew up, both with Bear Stearns.

This event occurred < 2 weeks from my closing the sale of my business. I had been glued to the housing insanity for almost two years by then, and was well aware it was going to blow and take the economy either way it. I was practically praying every day my buyers did not disappear. (They did not).

I like to remind a few friends that “eventually and imminently are not the same words”.

I’ve long believed we could not turn a blind eye to housing, as I’ve long believed we could not turn a blind eye to the excesses and euphoria of our present markets.

While the reported numbers still look good, beneath the surface there are lots of troubles in housing, employment, commercial real estate, etc. But… the credit has kept flowing to paper everything over.

I’m personally of the belief you cannot have a strong economy with a lackluster housing market. Too many jobs both within housing and beyond (manufactures of housing related goods) are dependent upon it. And we all know housing is not doing every well.

My belief is that eventually this is all going to blow up spectacularly, just as we had in 08/09. Is it imminent? That part I don’t know.

Those two Bear Stearns funds were the first warning shots. I’m treating this current episode of Tricolor, First Brands, AND the “spill over” into Jeffries, regional banks, and others with the same sense of caution.

There is nothing systemic about specialized subprime auto dealers. They’re only a minuscule part of total auto sales. Regular dealers don’t do that. I have covered imploding subprime dealer-lenders since at least 2018, and the world hasn’t ended yet. They just do that. It’s a regular occurrence. It’s a slimy risky business, and these dealers implode, often overnight.

It’s nonsense to compare this to the mortgage crisis.

And in terms of mortgages, most of them now guaranteed by the government, and low-down-payment subprime mortgages are insured by the FHA. Banks have nothing to do with that. So you can forget that too.

Wolf,

With regards to your mortgage comment, and how they’re guaranteed by the government, I should ask:

Could the feds try to bail on that obligation if it comes down to that?

I’m pretty sure they will bail on those obligations in some way or another, if only to prevent a bond market crisis. They may try to do so for political points, force losses onto investors instead of the government.

If that happens, then what?

The guarantee is to investors of these MBS, not to borrowers.

You can obviously imagine all kinds of stuff, and the human brain loves to do that, but I’m not spending my time on that.

That would be tantamount to defaulting on U.S. treasuries. You want to see chaos in the bond market? That would cause it.

Is it nonsense to suggest that the investors who closed their eyes to Tricolor’s problems likely closed their eyes to other companies’ issues as well?

While the subprime auto loans might not be systemic, could the investors who invested in them have made enough mistakes in other places that those mistakes will become systemic eventually?

That was outright systemic fraud — where lenders thought their loans were collateralized, and then there is no collateral. People can go to jail for this. That’s not a common feature. Risky lending is.

In addition, total C&I loans for all banks combined are only $2.6 trillion. That’s half of what CRE loans are. Residential mortgages amount to $13 trillion, but the majority are government guaranteed.

I am with you. There was a reduced amount of diligence being applied in a chase for yield, and auto loans are one manifestation of a systemic problem. Jamie Dimon’s cockroaches are not done revealing themselves in the auto sector, and it will waterfall down eventually from subprime.

But there could be something systemic about the way banks were willing to finance a company like this.

remember how JPMorgan got defrauded when it purchased the startup Frank for $175 million, and there was essentially nothing there and the users were fake? Fraud happens all the time.

I don’t remember if links are allowed but I thought some of the auto related data in this FICO insights report was interesting.

https://www.fico.com/en/latest-thinking/market-research/fico-score-credit-insights-fall-2025-edition

Don’t bet on seeing anything like that again.

Mar 2000 – Mar 2009 was the great depression.

Lost decade in equities, 13-15 years, depends on how you count.

Millions lost their homes, millions more lost work.

Minus the 2 big buildings in NYC and the subsequent GWOT.

Remember, jobless recovery then ZIRP?

They called it a recession twice, but it lasted 15 yrs.

Don’t be Doomer Dano,

unless you live in Detroit,

then it’s ok.

The collapse of the real estate market, especially condos, in Toronto is already at 1990 levels.

Motorcity_Madman

Good lordy.

The recession during the dotcom bust lasted until Nov 2001.

The “jobless recovery” was in 2002 through Oct 2023.

Then from October 2023 through Dec 2007, 7.6 million nonfarm payroll jobs were created, nearly 2 million on average per year, which is pretty good.

In December 2007, the Great Recession began, and nonfarm employment began to decline in January 2008.

So there was a pretty good recovery in those years between late 2003 and late 2007.

So your statement “Mar 2000 – Mar 2009 was the great depression” is BS that you used for the purpose of ZIRP mongering.

Post-2003, a huge share of the jobs recovery was construction and other real estate related.

Are you talking about the Cboe ad at the bottom of the page? Does it do something funny?

So my technical terminology may not be precise but………

When the site loaded with the ad popup bar it would keep running connections to a series of web addresses that would not finalize and, even with the add bar closed out of. I’m not sure if that makes sense nut it’s pretty simple to observe when it happens on some websites. It’s all good. We live in a mass surveillance police state so we can’t be too concerned about what’s going on with our communications networks.

Perhaps the morass was started by the socialist politicians who created ‘social spending’ in an attempt to buy voters. The resulting money tree was heavily fruited with dollars, just waiting for the multitude of pickers to collect the taxpayers money, expecting that government support would appear when the tree was looking rather empty. Perhaps this should be looked upon as simply another type of business enterprise, distribution of cash from the clever to the gullible? By the way, I wonder how George Soros is doing?

I think a lot of the current morass, was superheated by Bush ll —

During the George W. Bush administration, social spending on homeownership was a key part of his “ownership society” agenda.

Obviously, what followed was the TARP ACT and $800* Billion, that paved the way for the current morass with deficit close to $40 Trillion.

God bless Trump for doing so much to reduce that,

It’s a shame that S&P Global gets to take a fee for rating Tricolor’s ABS “investment grade” and isn’t held responsible when it implodes.

1. Then think about whats in the “less than” investment grade high yielding corporate bonds.

2. You have to put kids through college like Harvard. Bankers kids.

3. In the “Big Short” movie, a lady temporarily blinded by cataract surgery is rating the bonds.

4. Rating agencies have the best 1st amendment free speech lawyers. The ratings are free speech.

5. If the ratings are higher, they can get away with lesser yields. Ask the Government.

“How many credit default swaps do you own?”

Great scene, great film.

Re: The proceeds from the sale of the securities pay off the warehouse line of credit for those vehicles. These ABS are backed by auto loans that are collateralized by the vehicles…

From my Google Bro:

Some holders of Tricolor’s asset-backed bonds received interest payments in September 2025, but those funds were later “clawed back” by the custodian bank. This happened because the trustee overseeing the bonds did not disburse the necessary funds, a direct result of the bankruptcy and fraud allegations.

After Tricolor’s September 2025 bankruptcy, it was discovered that about 40% of 70,000 active loans had vehicle identification numbers (VINs) that were identical to at least one other loan. This indicates a major data irregularity or outright fraud.

The bankruptcy has frozen the collateral—approximately 100,000 loan accounts and 10,000 vehicles. A third-party servicer, Vervent Inc., was appointed to take control of collections, but the investigation into the validity of the collateral is ongoing.

The value of Tricolor’s ABS, particularly lower-ranking bonds, has plummeted. For example, some tranches of a $217 million ABS sold in June 2025 were fetching as little as 12 cents on the dollar by late September. This indicates that the market has little confidence that these creditors will be able to recover their initial investment.

I wonder what else AI underwriters have planned for making finance more efficient?

“Social lending” used to be called loan sharks.

LOL at “social lending”. They packaged turd sandwiched ABS from worst possible buyers and sold them off as solid investments all with the stamped approval from the people at S&P and the Treasury. There is a reason Buy Here Pay here lots exists and why Repomen carry guns. Apparently none of the people involved have actually been in the car business, otherwise they would have known better.

“none of the people involved have actually been in the car business”

That’s not entirely 100% true…

One of the two co-founders served time in the hoosegow for selling stolen cars.

The other co-founder was forced out of a prior used-car company over accounting irregularities

… AND LARGE AMERICAN BANKS STILL FINANCED THEM AND TOOK THEIR WORD AT FACE VALUE.

That’s the scandal, not Tricolor itself. It implies the banks are easily ripped off by fake paperwork.

Yes. I don’t feel sorry for the creditors at all. They acted like they wanted this outcome. Greed turns brains to mush.

“Consensual Hallucination”

– W.R.

“Greed turns brains to mush.”

Correct, BUT it only gets worse when the government REWARDS such bad behavior. Long past time to let management, owners and the shareholders suffer real consequences.

‘One of the two co-founders served time in the hoosegow for selling stolen cars.’

Holy Sh&t! Didn’t that disqualify them from running a large company?

Did it have a listing on an exchange? Was this disclosed?

There are yellow flags and red flags: a criminal record is a red flare.

Not sure if it was known at the time of the founding, but it was reported some years ago, but it didn’t matter to the lenders. They just closed their eyes because the interest rates were juicy.

I was referring to the people at S&P and the Treasury. Which I know is a sweeping generalization. A car subprime dealer/lender is a risky proposition. Apparently they were ignorant of the risks or willfully negligent in assessing the risk.

A quote from Jamie Diamon to a question on bank supervision and regulation during JP Morgan’s recent third quarter earnings call

“So, we had the Silicon Valley Bank blow up, because they’re so focused on governance, they forgot to focus on interest rate exposure. And they

are making changes now, like what is actually real risk banks are bearing as opposed to the woke signaling of what a bank should be doing all

the time. “

Let that be a lesson for you, son. There are people, maybe some day like you, who are obsessed with making money and conmen who know how to take advantage of that.

Most people are interested in acquiring more assets or more power, and money is a handy yardstick for measuring and obtaining both. Obsessions with money is why most of us are reading Wolf’s blog, but being highly interested in how systems work, velocity, flow, goes-intas and goes-outas, is not the same as being obsessed with making more money without providing even value in exchange.

The obsession of something (a lot of somethings) for very little is what drives people into the arms of conmen. Unrealistic returns, big wins from small bets…we love those stories (see also crypto, lotteries, and other scams) and those drive additional investment (see also casinos, OpenAI, etc.)

Prime auto loans are doing well. Sub prime is appears to be all time worst.

Wonder what the ratio of sub prime to prime loans have been over last 20 years.

If the ratio has increased over time then the overall consumer situation may be worse than thought.

Almost no new vehicle loans are subprime, which is why subprime auto lending doesn’t really matter to the economy (new vehicle sales go into GDP, used vehicles sales don’t since they just shuffle around an existing product).

Of used vehicle sales, only 37% had ANY financing and 63% were cash deals.

Of those 37% of used vehicles that had financing, only 15% were subprime.

So subprime is a very small specialized part of auto lending.

Experian data as of Q2.

Private credit mangers got paid already from closing transactions. It’s easy to take huge risks with other people’s money! When you find one moth in your home eating your sweaters there is always an infestation, same as cockroaches. Credit bubbles are impossible to pick a top, but maybe we are post peak, let’s see what the evidence has to say. Isolated Problematic news or infestation. Seasonally the stock market peaked Oct 11 2007, before the pain trade happened for Americans. Maybe October 2025?

Nah, everything’s fine with the $50k price tag of cars. Doing well as this site tell us.

Could be another reason cities and states seem to be looking into transit seriously. Maybe they’re getting ready for the blowback/blowup of all this.

You’re citing the AVERAGE transaction price. It was pushed higher in September because people bought lots of high-end EVs because the incentives expired at the end of the month. That figure has been turned into braindead clickbait headlines by morons for morons to spread around the internet.

There are plenty of new vehicles you can buy for less than half that price, including new Toyota Corollas for less than $23,000 MSRP.

I had to map out a network diag ram to trace the thought process (not my area of expertise) – but – that’s as a clear and succinct an answer (your article) Wolf. Thnx.

Didn’t say most people. And most people aren’t conned.

Is the AI mania at a top. The big boys are crying about a bubble that’s going to bust. Is the competition for AI control so hot that the dollars flying out of their coffers are making them sweat and cry.

Comes a point when a billion there and a billion here going out and not much coming back starts to hurt.

But now it’s like a gamble, card game, who is going to fold first. They will fold when it shows up in someone’s earnings and the stock tanks.