Examples: California, Texas, Florida, Washington, Oregon, Colorado, Arizona. In other states, homes still sell faster than before Covid, such as New York and Georgia (barely).

By Wolf Richter for WOLF STREET.

One way of looking at the housing market is how long a home sits on the market before it sells or before it is pulled off the market when it doesn’t sell. This measure of “median days on the market” shows a mix of two things: How quickly homes sell, and how desperate homeowners are to sell by leaving their home longer on the market before delisting it. In hot markets, homes sell quickly, and if a home doesn’t get any action quickly, it’s pulled off the market quickly.

But now, in many markets, with sales down by 25% to 30% from pre-pandemic times, and with supply high, sales take a long time, and homes that don’t sell don’t get pulled off the market quickly but are allowed to sit longer to attract some interest, before they get pulled.

So here is a sample of states where in September, it took the longest for any September in at least 10 years before a home was sold or was pulled off the market: California, Florida, Texas, Washington, Oregon, Colorado, and Arizona. These are also among the states where supply is high, and where prices have begun to fall, in some cities at substantial rates.

But not all states. For example in Georgia, median days on the market have risen but were back only in the pre-pandemic range.

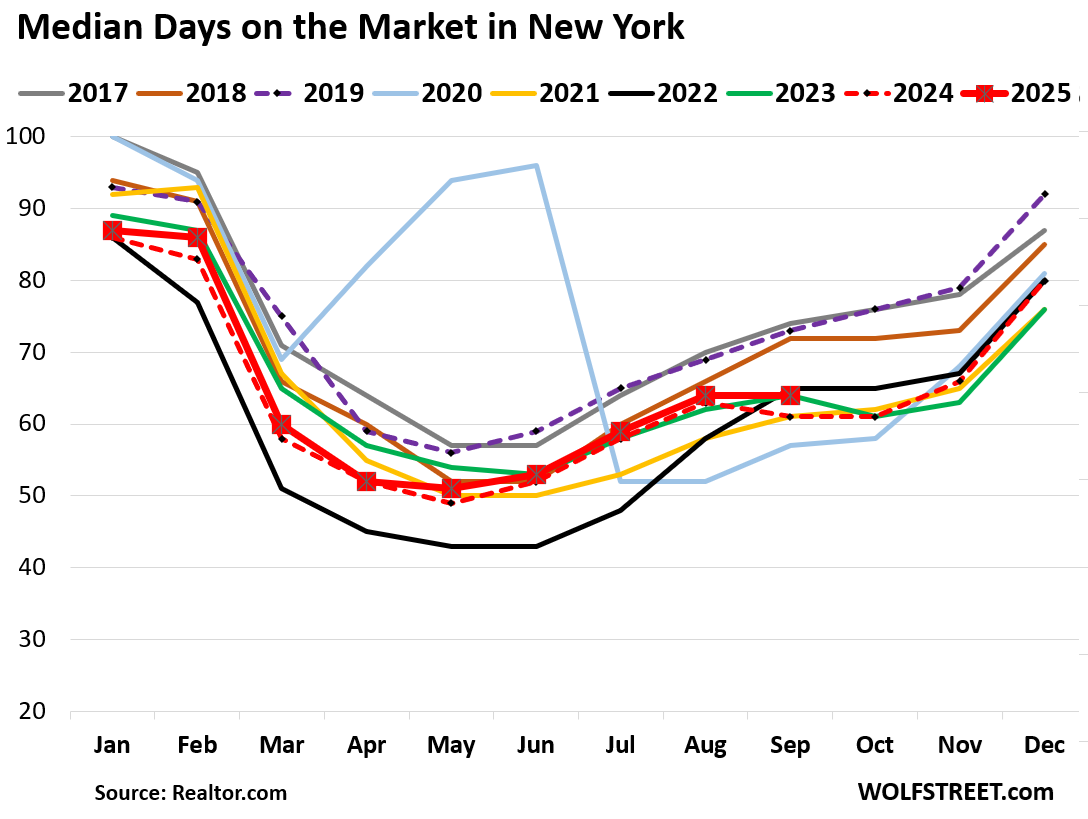

And in New York, they were substantially lower than they had been before the pandemic. New York is one of the states where inventories are still tight, though sales are way down, and prices still rose.

Every housing market is different, and these states span the range.

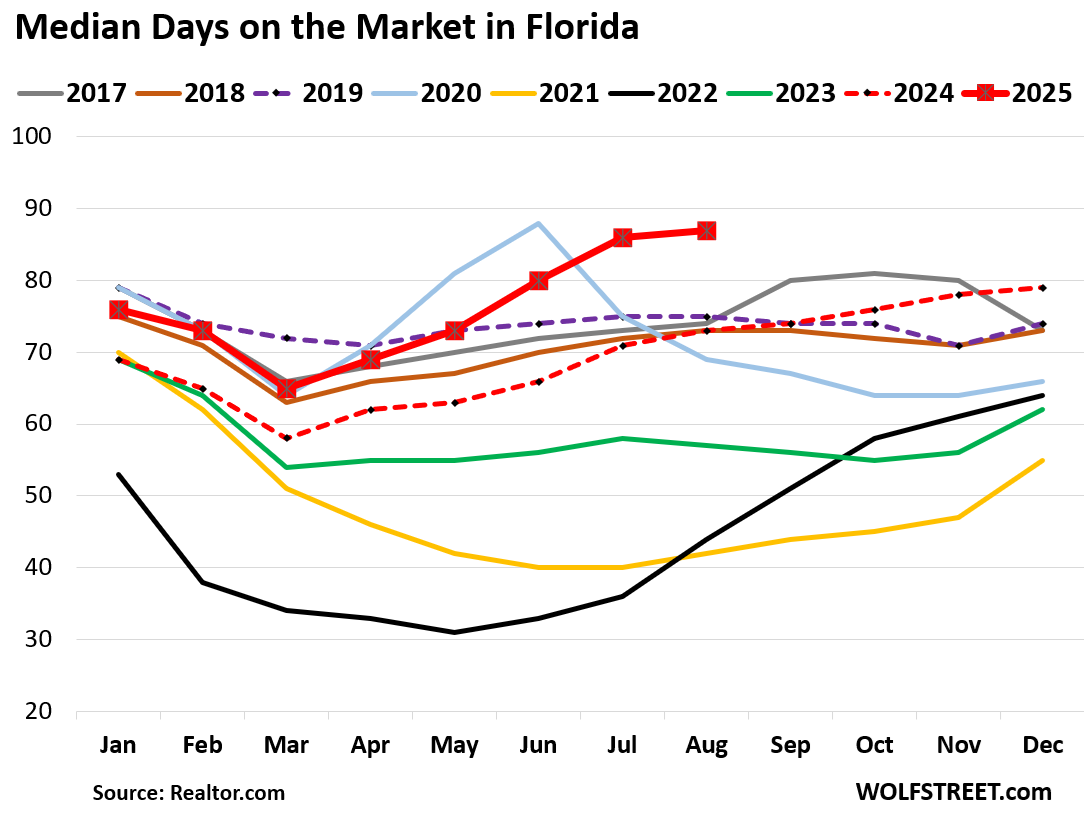

In Florida, the median number of days that a home sat on the market before it was sold or delisted jumped to 87 days, by far the longest for any September in at least a decade, and the second longest in that decade overall, behind only June 2020.

It was 12 days longer than in 2019, 14 days longer than in 2018, and 13 days longer than in 2017, according to data from Realtor.com, which goes back only to 2016 (dotted red line = 2024; dotted purple line = 2019):

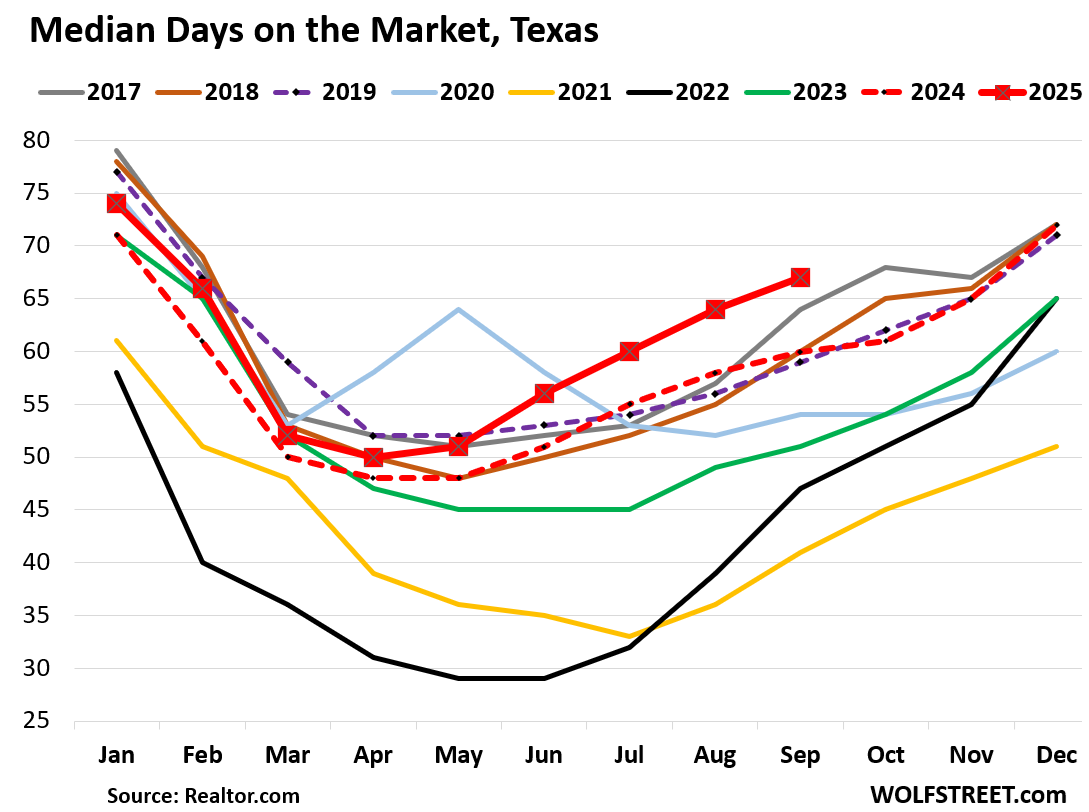

In Texas, the median number of days a home spent on the market jumped to 67 days, by far the longest for any September in at least a decade, 8 days longer than in 2019, 7 days longer than in 2018, and 3 days longer than in 2017:

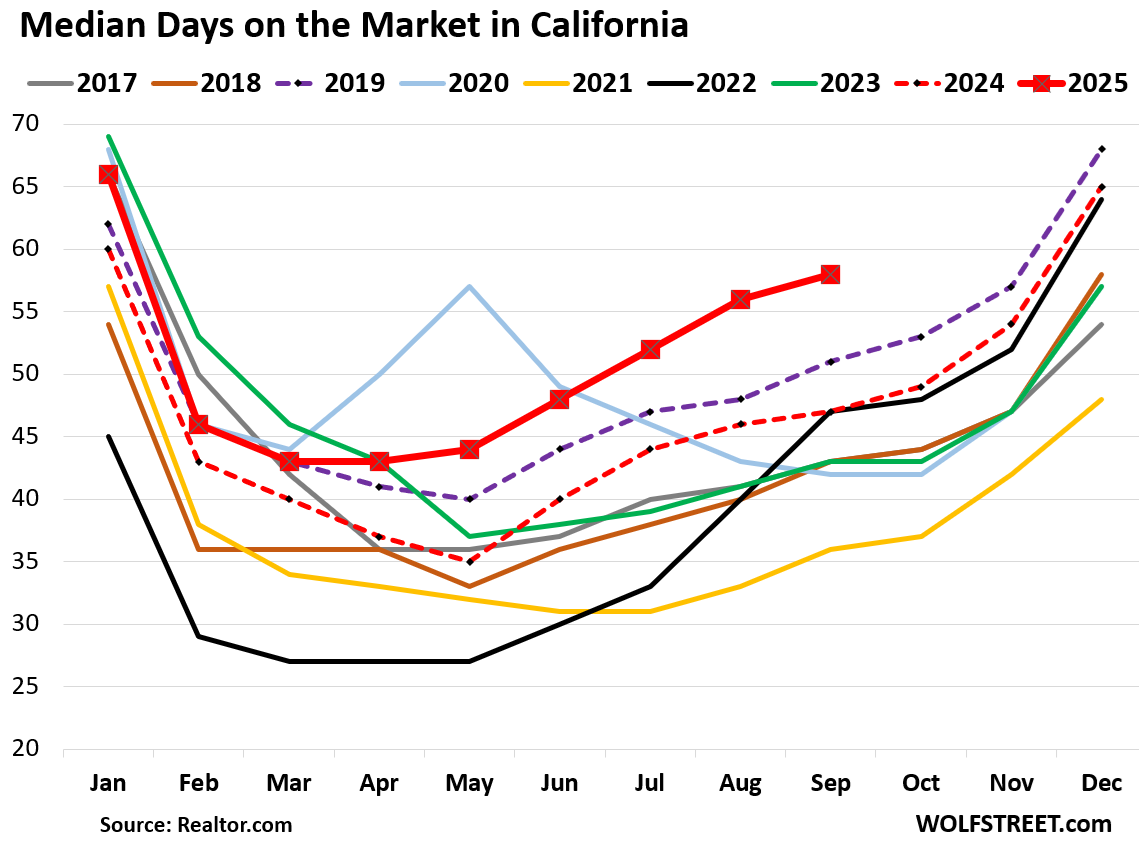

In California, the median number of days that a home spent on the market jumped to 58 days in September, by far the highest for any September over the past decade, 7 days longer than in 2019, and 15 days longer than in 2017 and 2018:

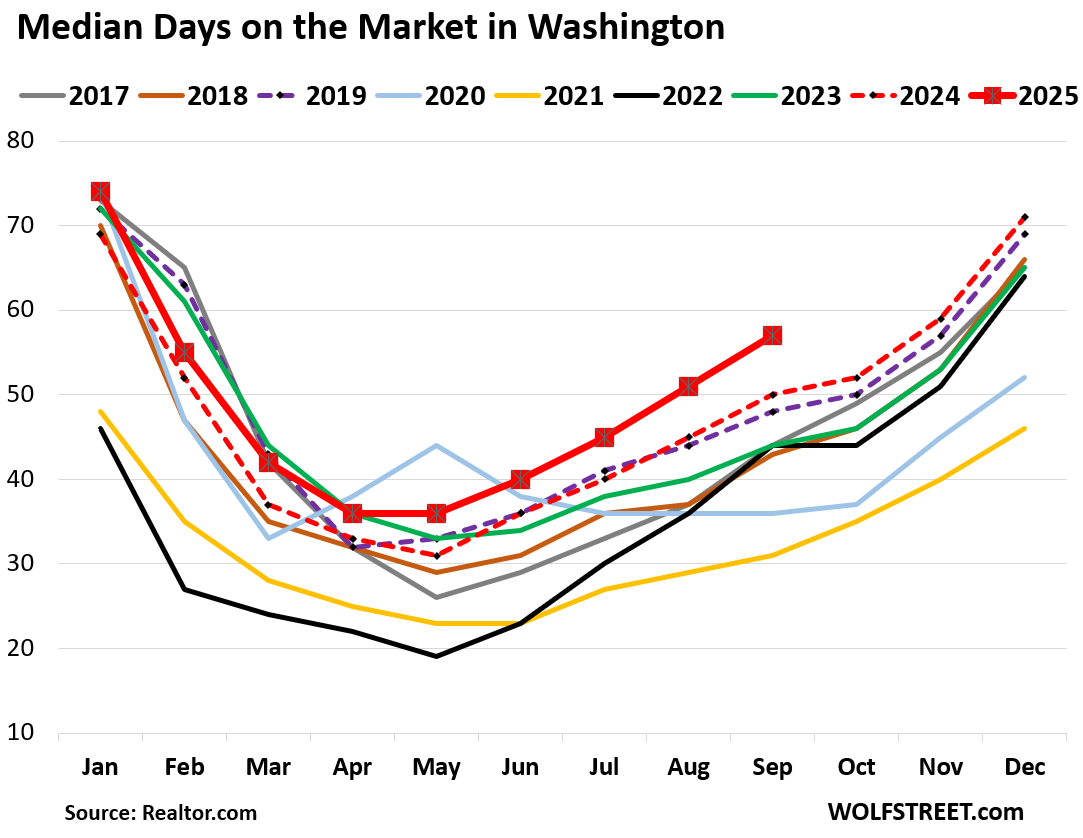

In Washington, homes sat 57 days before selling or getting pulled, by far the highest for any September since at least 2016 – which is as far as the data from Realtor.com goes back. This was 9 days longer than in 2019, 14 days longer than in 2018 and 13 days longer than in 2017

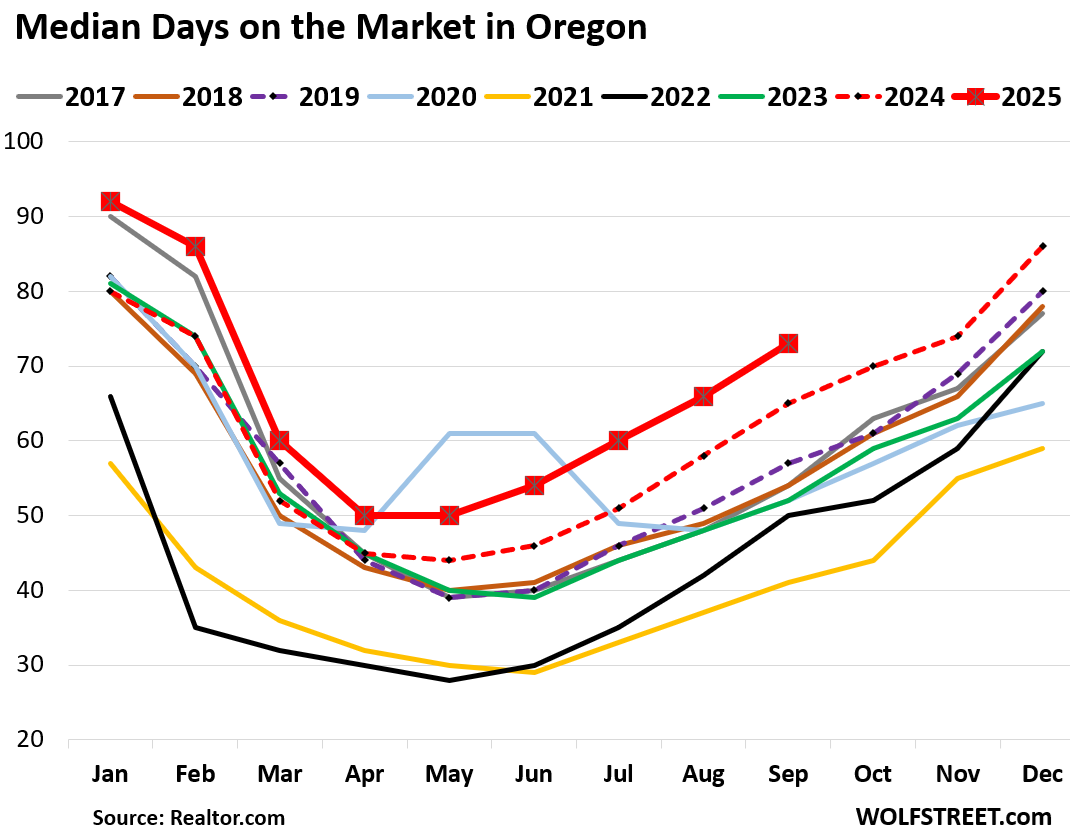

In Oregon, homes sat 73 days on the market in September before selling or getting pulled, 16 days longer than in 2019, and 19 days longer than in 2018 and 2017.

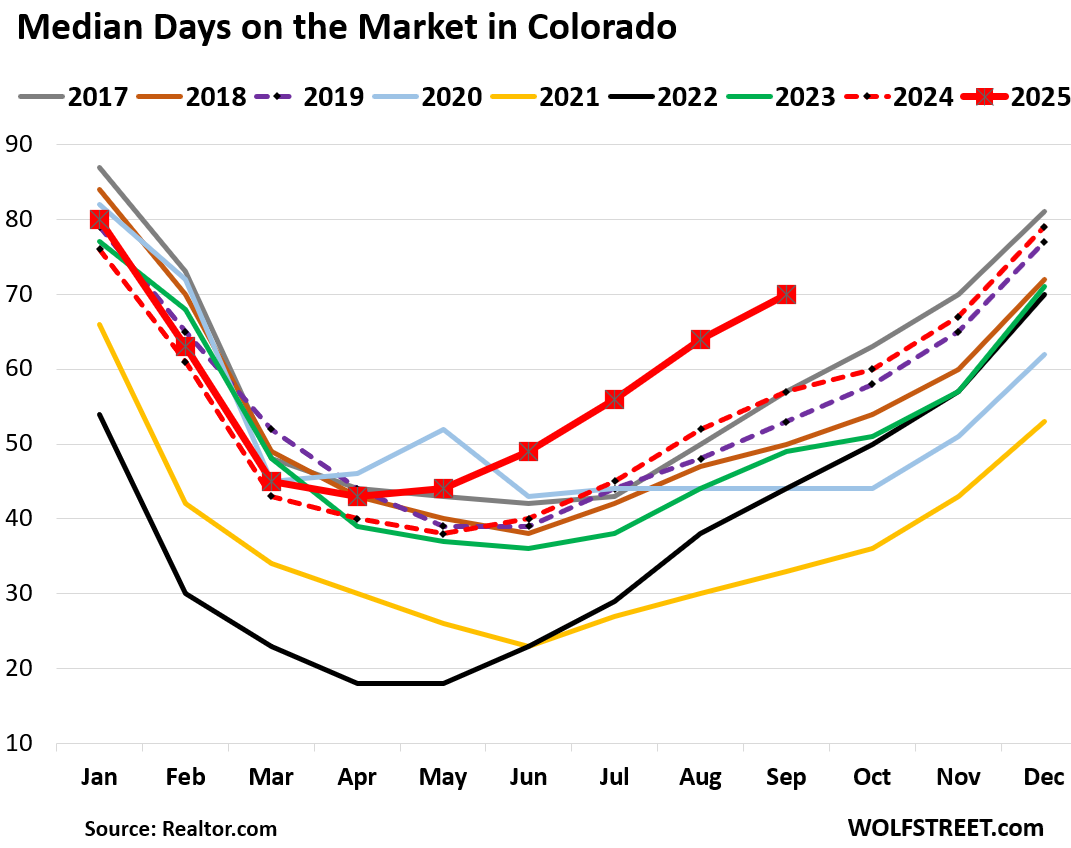

In Colorado, homes lingered 70 days on the market before selling or getting pulled, 17 days longer than in 2019, 20 days longer than in 2018, and 13 days longer than in 2017.

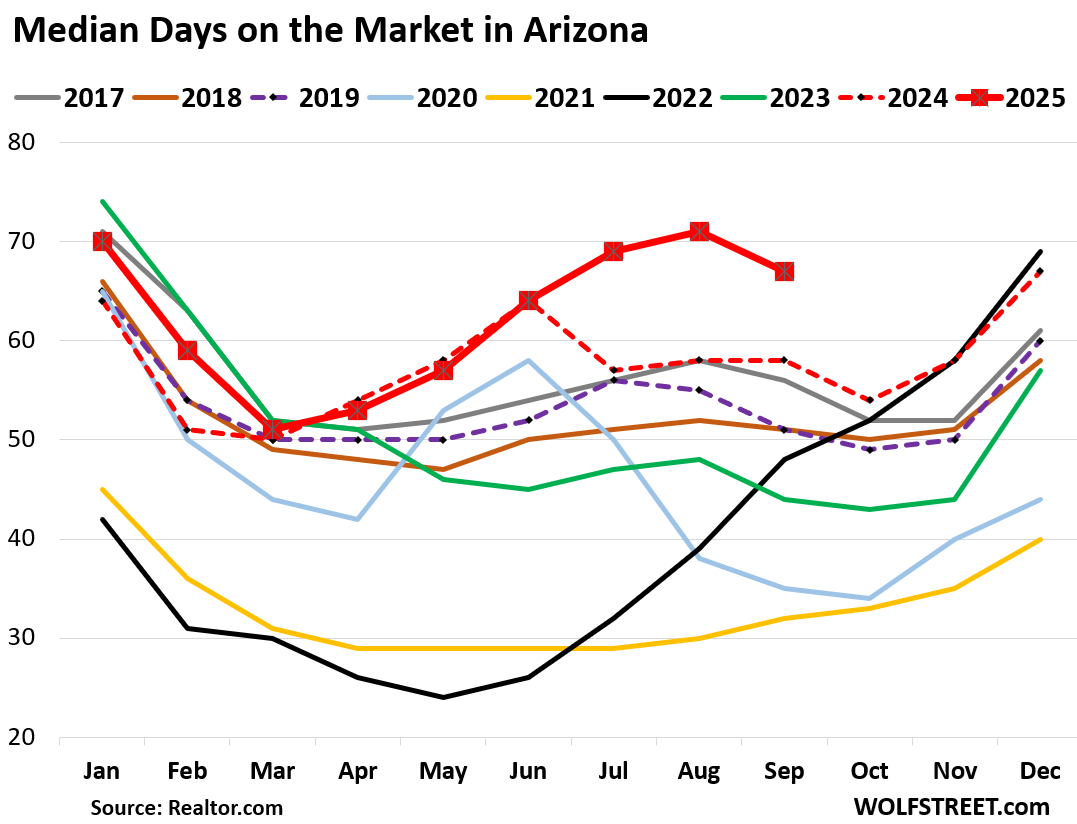

In Arizona, homes sat 67 days on the market, 16 days longer than in 2018 and 2019, and 11 days longer than in 2017:

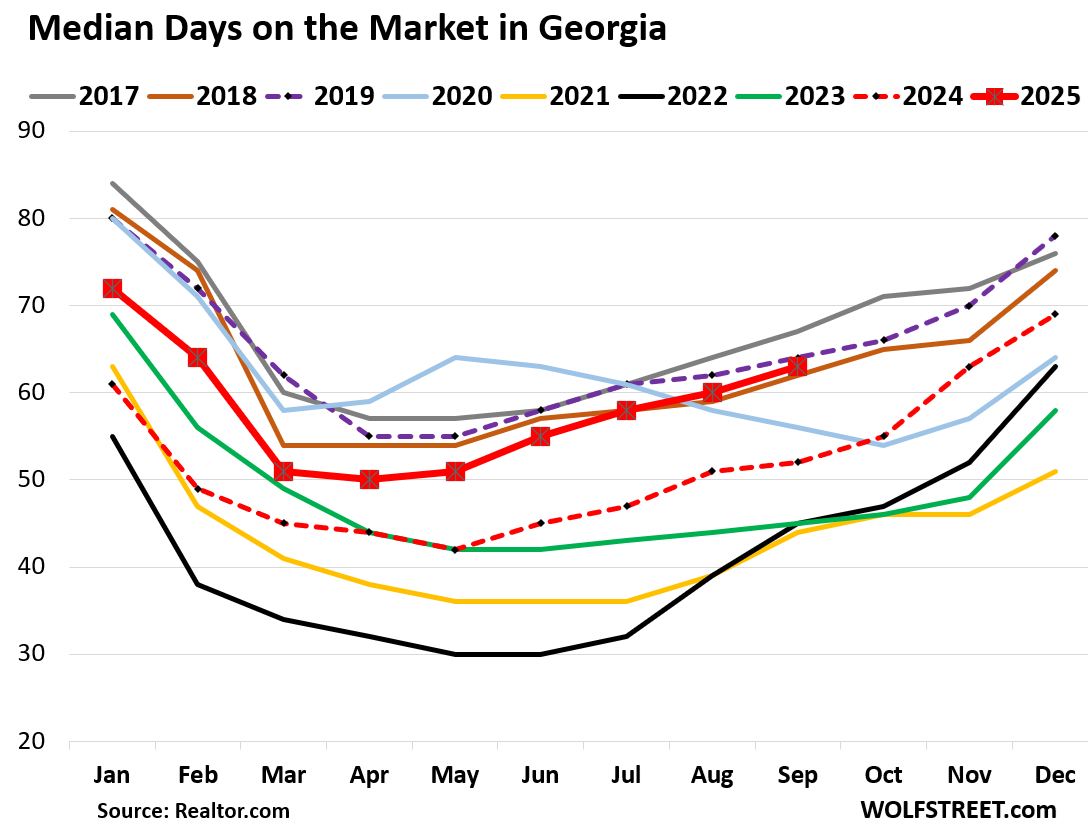

But in Georgia, median days on the market, which rose to 63 days, the third-longest for any September over the past 10 years, was still below the Septembers in 2019 (64 days) and in 2017 (67 days):

And New York is an example at the other end of the range. Days on the market rose to 64 days, up by 3 days from a year ago, but shorter than in the Septembers of 2022 (65 days), 2019 (73 days), 2018 (72 days), and 2017 (74 days). It just always takes a long time to sell a home in New York.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Definitely encouraging to see California # of days are going up. Too bad we can’t see individual markets down to zip code level and if it’s consistent across most markets in SoCal. Hopefully this is the first domino to fall that will eventually lead to some major correction in price.

Likely will only happen when sellers realize they can’t rage quit in selling and hoping for a better day to return…might take a while since employment market still decent and stock market is all time high, these sellers alternative investment can probably support them to rage quit and hang in there just a bit longer…

I still see a ton of houses in SoCal, bought for sub 1million, put in 50k of cheap work, price jacked up 300k a few months later.

Yup, quick search in the Long Beach market, you’ll see plenty of those and people still snatching them up despite reduced volume from the mania back in 2021-2022.

San Diego is weakening a lot from what I see.

Trending down for sure

Thank You W.R.

Have a fantastic weekend ! 🍻

I’m telling ya….. it’s gonna be the ol’ fashioned rug-pull, or tablecloth-pull. Shazam….Kapow!!! Or, as they said on South Park “And… IT’S GONE!!!”

It’s kinda like being struck by lightning. You never know it’s coming, or if you do, t’s only for a quick second and then…BAM!

When everybody ends up running for the exit at the same time, it won’t end well. I’d quietly get up and pretend I’m going for a lemonade and ‘exit stage left’. 😜

A big high five on your compelling description…fun

Creative description….fun twist

It would be nice, but I don’t think the housing market moves this way.

Yup, and prices are still ridiculous, or is the dollar just worthless…or both

Erik

The dollar is getting worthless

I am a REALTOR. Our vacation home in Glendale, AZ (85 miles from out main home in Prescott) took 150 days to sell after 5 price reductions. On a golf course; completely remodeled inside and out; new roof and paint in and out; landscaping all redone and with a brand new putting green. Irrigation rebuilt for the few plants and palms we had growing. All natural grass and hedges removed. New wrought iron view fence on top of block fence; block fence painted. NOTHING WRONG. We still made a profit but wound up getting over $100K less than we would have gotten two years ago. Again, I am a REALTOR. This is a very tough market; sellers must be patient and flexible. Buyers (especially cash buyers) hold all the cards; they can pick and choose carefully and then swoop in with an aggressive (for them) offer.

Yes, the fact that you still made a profit is the big part. Nearly everyone trying to sell, except for those who bought at the peak in 2021 or 2022, still has equity, just not as much as they thought they did.

And since that aspirational price from May 2022 is already set in their minds as what they “deserve,” many are not willing to take a penny less.

That’s why so much is sitting on the market.

Sunk Cost Fallacy

Every downturn always has the same sellers saying they’ll never sell or take less than x.

Fast-forward 3-6 years and there they are sitting back at little to no equity.

People are stupid and think houses aren’t just mass market items readily available to buy and sell.

Still amazed that some of our sold property between 2021 -2023 had such massive gains.

“People are stupid and think houses aren’t just mass market items readily available to buy and sell.”

Amen to that, and thanks to plenty of these stupid people, somehow a $1k to $2k car payment has been normalized as this is the way it is and we should just make it work…

Kinda’ like most crypto.

The thing is, very few people actually realized those gains. The biggest gains, from what I can see, are in markets that became popular during the pandemic for the “work from home” people. What more can you ask for than making a NYC or San Francisco salary and buying a house in Austin, Nashville, Miami, Denver, or somewhere like that where you can get so much more for the money?

The problem is this was all temporary in nature. Work from home jobs now are competitive enough that it’s very tough to make a NYC or SF salary doing it, as the people offering those jobs know they have more demand from applicants.

So the $500,000 house in Nashville in 2019 was $1 million or more in 2022. But you have to remember, the universe of people who could realize those gains fit into 3 main buckets:

1) those who had an extra house to sell. These people made out like bandits.

2) those who were in the process of (or who got the idea after the mania started) to sell their houses in fashionable markets and move to non-fashionable markets. If you had a house in Austin pre-pandemic, you could have sold in 2022 and moved to Omaha and made a lot of money.

3) Those who were severely downsizing. Even if you had to buy the smaller house at peak bubble prices, you came out ahead by selling your bigger one at those prices.

But most people couldn’t realize these gains because they needed their houses to live in. The family in Austin who bought in 2017 couldn’t sell, as they had nowhere else to go. So they couldn’t get out at the top in 2022 before prices dropped 25%.

It’s kind of like the modern stock market. With people believing they can’t lose, there is no selling pressure, only buying pressure. That’s what housing was like in 2021 and 2022.

Now that it’s not, there is kind of a Mexican standoff going on.

Homeowners are emotionally attached to 2 things, their sub 3 or 4% mortgage rate and their huge equity gains, like you said, eventually the equity gain of the silly 2020-2022 market will get lower in the next few years, it’s like buying a stock, its goes up a lot, then you see the profits start to drop, and you have to make a decision when to get out, in real life things change too, job relocations, family stuff, death and divorce, your business needs money or goes under etc., you can’t time that. But there are so many of those people, scary thought if they decide to ditch all at once.

Yes. And that profit is still much higher than value. There needs to be a 2007 style correction before the market returns to true value.

Yes, but it happens slowly.

The wrought iron fence must have cost a bundle given almost no wrought iron is produced, although sometimes they market steel as wrought iron, perhaps as some form of marketing.

“sellers must be patient”

I’d argue the opposite; sellers need to be aggressive with their price cuts to get ahead of the market.

Yes and that’s the reality

I agree

Sellers must haste lest they chase a market going down with time

Despite a hot economy and historically low unemployment rate we have this slow down

Think what may happen in not so hot economy.

Not a tough market, if you price right. And as in your case, the client still made money. Only tough for those who have visions of prices past… And tough for who? What is tough for one side is good for the other. This is still a great market compared to 08 where owners literally walked away from underwater homes… Only recent buyers are underwater and they set themselves up for that, literally buying when prices has already gone up 2x to 3x.

With reference to Washington State, there’s a typo, “ … and 13 days longer than in 2917” should be 2017.

I’m just a very forward-looking guy 🤣

Thanks!

What’s the housing market going to look like “in the year 2525”? LOL

Will man still be alive?

10 Years After. I d love to change the world.

People got arrogant greedy believing there structure and land worth much more than before; much more than they had fixed upon improvement; much more than if the Federal Government Freddie Mac ,Fannie Mae and Powell Zero Interest Rate would allow the next generation and other movers to buy high.

Inflation yes though stupidity needs to allow those who bought into that lose.

… and still in that arrogant price inflated greedy world

My friend just sold his $1.1 million home in Lakewood, CO, after 45 days on market. He dropped the price 50K from initial asking. But still got 40K over the Zillow estimate.

I live in a very desirable area and neighborhood on the Olympic Peninsula. Our neighbors house took 6 months to sell. Overpriced. It’s pending and guessing a cash sale. Out of state buyers ask about , fires. Snow, climate changes. Real estate here is slug cold. Majority of sales are cash. Most common range 400k to 700 k. The plus 1 million still sells if updated and acreage

Used to live outside Sequim and the person that bought my place has tried to sell twice, and currently, 95 days in mkt, going into October.

I have no regrets selling at top!

Prices still have a long way to drop to deflate this bubble. ZIRP and QE inflated it way beyond housing bubble #1.

In my mind I am imagining two Slinky’s sitting at the top of the stairs.. one housing, the other one the stock market…. There is a quantum entanglement between them. If the market Slinky starts to tumble down the stairs the housing Slinky will be pulled along with it. But if the market stays at all time highs the housing bubble won’t deflate as fast because the people with a lot of assets will be less compelled to sell.

But watching the two Slinky’s come tumbling down together will be fun… well because “this time things are different “.

I feel like the economy is stuck in the Twilight Zone. Good is good, bad is good, and up, up, and away.

“What’s good is bad

What’s bad is good

You’ll find out when you reach the top

You’re on the bottom”

Bob Dylan

@BobB

“this time things are different”

Go read the ENTIRE Wikipedia page on the 2008 financial crisis, and you will be shocked at how many similarities exist today to the issues and problems that led to the 2008 crisis

Some have been corrected at the legislative level, but some have not and can not be fixed by policy.

From the John Tuld speech at the end of “Margin Call” he rattles off the years of financial downturns.

1637: Tulip mania Bubble

1797: Panic of 1796–1797

1819: Panic of 1819

1837: Panic of 1837

1857: Panic of 1857

1884: Panic of 1884

1901: Panic of 1901

1907: Panic of 1907

1929: Wall Street Crash of 1929

1937: Recession of 1937–1938

1974: 1973–1974 stock market crash

1987: Black Monday

1992: Black Wednesday

1997: 1997 Asian financial crisis + October 27, 1997, mini-crash

2000: Dot-com bubble

Go watch this video on youtube if interested.

He is right about one thing. We just can’t help ourselves. LOL

Moving in my area. Many sellers are doing BOGO 50% off. Now just need buyers to pair up.

It’s my perception from what i have both read others have written and from what i see on Zillow, that the number of days on-market may be skewed by Listing-delisting-and re-listing again. Clean slate…sold in 30 days, when the actual story may be very different.

Correct. We see this everywhere.

Same with sold “over asking.” Listed three times unsuccessfully, cut the price after each, and then re-listed a fourth time with the lowest price yet, and it sells “over asking,” WOW, the market is hot again, but way below the 1-3 asking prices 🤣

Oldest games in town.

Wolf,

Do you know how many first time home buyers typically buy houses in a year and how numbers have looked over the years? 2024, around 1.1 million houses were purchased by first time buyers but that number was 19% less than previous year. I am wondering how many first time time home buyers have delayed their plans over last 3-4 years and eventually they are going to buy. I believe this number is important. It’s like musical chairs, existing home owners can swap chairs but new chairs needs to be built for first time buyers. Just curious. We may get tsunami of first time buyers and push prices even higher when interest rates drop. Right now it’s double edge sword of high prices and high interest rate but what if interest rates drop?

You’re talking about existing homes – first time buyers of existing homes.

But first-time buyers have switched to NEW homes, and homebuilders have been talking about that, they’re targeting this market very successfully. The monthly mortgage payment on a new home is substantially lower than on an existing home after the mortgage-rate buydowns. Homebuilders are cleaning the homeowners’ clocks. Those first-time buyers of new homes are a huge factor. So you can probably forget your “tsunami of first-time buyers” of existing homes.

This is probably a good thing. Keeps younger buyers away from the temptation to buy a fixer and blow precious time/money (always over budget on both!) on repairs. Better to have a “done” house and focus on career, kids, advanced education, golf handicap, whatever.

I burned my entire 30s on home improvement, and while that was excellent education of a different sort, the actual ROI on it was really poor. We would have been way better off spending more on a nicer (or done) house and enjoyed our lives more.

Just for the record, the NEW house behind us in the saintly part of tamper bay area is still for sale and the price was just dropped another $10K to $1.4M.($405/SF) They started at $1.6M

OTOH, a nicely updated older house down the block just went pending after 3 days for asking price at $522K. ($350/SF)

When will home prices fall to AFFORDABLE levels – when the average number of days on the market is 365? This current housing non-market is for losers. It makes NO SENSE.

Wolf, mortgage rate buy-downs in recent years have been a new source of adjustable rate mortgages. Do you feel as though this is a large enough percentage of home purchases to create problems for the housing market (like in 2008 financial crisis?)

A lot of these buydowns are permanent buydowns.

Thanks Wolf!

Having bought in NYC last year, I am glad that this is the one market where the days on market hasn’t shot up. I felt like the housing prices were irrational, but the reality is that we wanted to move before my son started kindergarten. Fortunately we were in the position to buy something well below our budget for cash.

Humorous delusional listing in my area since July 13 at least: 633 S. Castell, New Braunfels, TX. $355/sq. foot for a 120 year old house with what looks like a rusted roof. I could see it going for half the 889k asking. Calling deep pocket creaky floor lovers!

Duh, since they are way out of price. Only brainwashed idiots have bought houses this millennium. They get less craftsmanship, crap materials for 5 to 10 times the price! Here in Florida they are on TV advertising cutting prices, builderrs are so desperate. Last time they didn’t cut prices. But this time they see the bubble has popped.

All bubles are gonna pop. Gold and Silver are telling the tale. The ponzi Fiat scheme is finished. No way all this debt we’ve created can be payed back.

Hang on your in for a ride. It might be you, Wolf homeless on the street. Don’t think it can’t happen! Think again sucker!