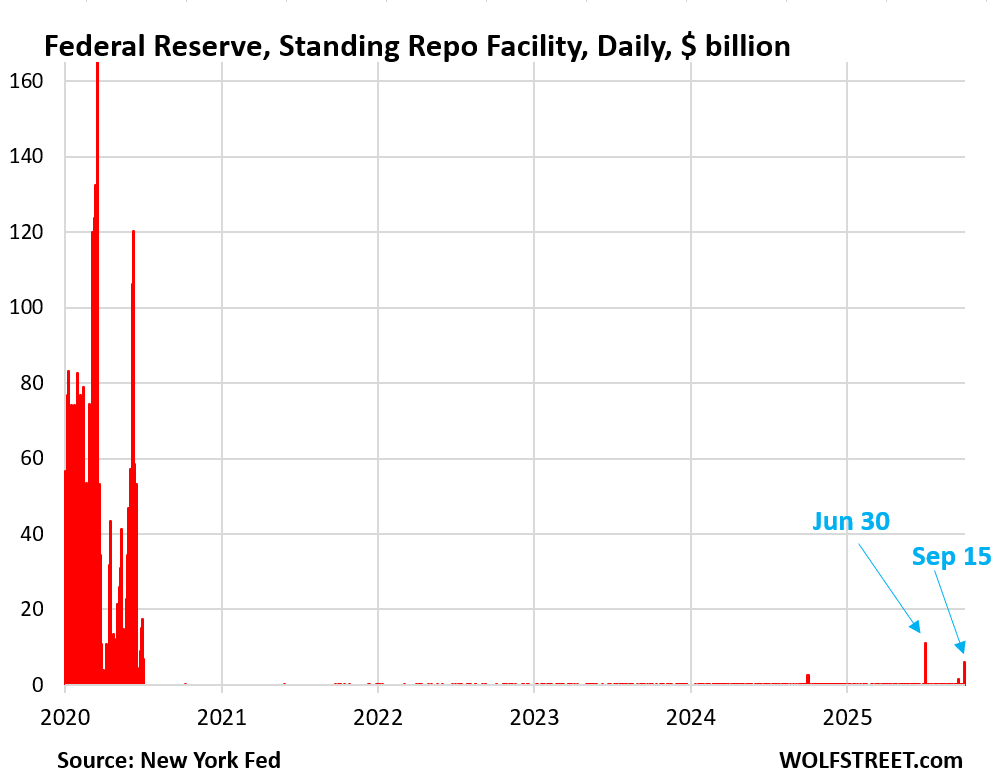

The Standing Repo Facility got a bit of use on Sept. 15 (corporate tax day) amid minor liquidity strains in the repo market.

By Wolf Richter for WOLF STREET.

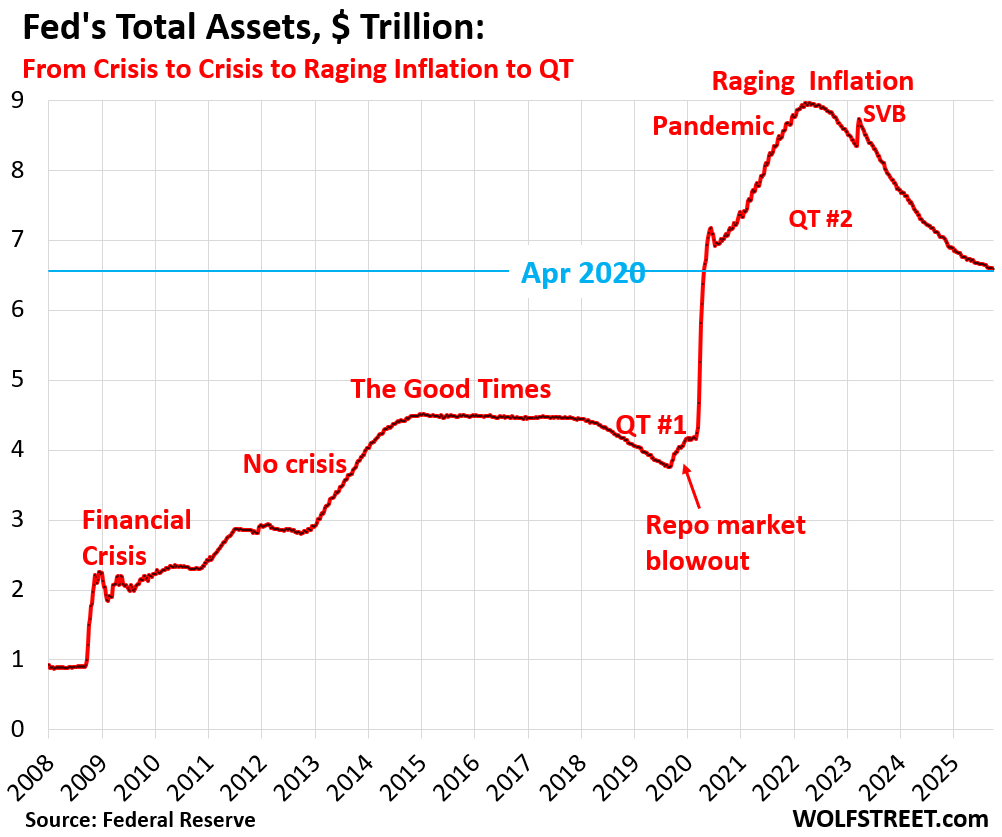

Total assets on the Fed’s balance sheet declined by $15 billion in September, to $6.59 trillion. This $15 billion decline was a mix of $24 billion of declines and $9 billion of increases:

- $24 billion of declines spread over four accounts:

- MBS: -$17 billion

- Treasury securities: -$4 billion

- Unamortized premiums: -$2 billion

- Pandemic-era SPVs: -$1 billion

- $9 billion of increases spread over two accounts:

- Discount Window: +$3 billion

- Accrued interest: +$6 billion

Since the peak of its balance sheet in April 2022, the Fed’s QT has shed $2.38 trillion, or 26.5% of its total assets. In terms of the Pandemic-era QE, the Fed has shed 49.5% of the $4.81 trillion it had piled on from March 2020 through April 2022.

Since the reduced pace of QT began in June 2025, the balance sheet has declined on average per month by $22 billion.

QT assets.

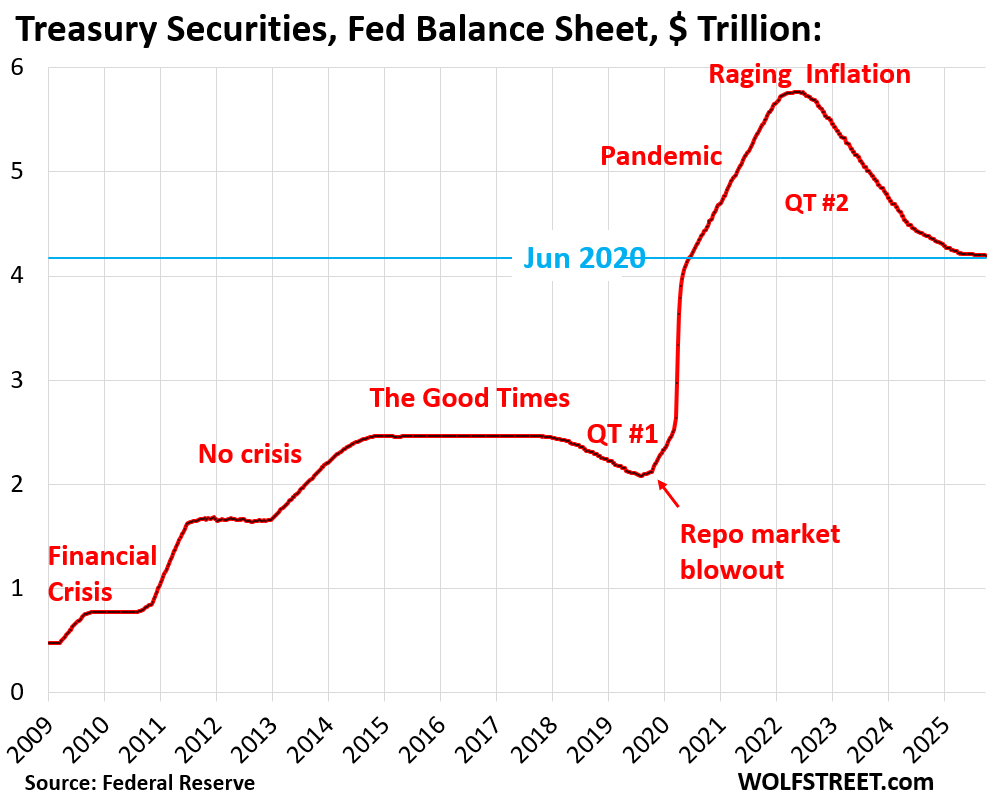

Treasury securities: -$4.4 billion in September, -$1.58 trillion (-27.3%) from peak in June 2022, to $4.20 trillion.

The Fed has now shed 48.2% of the $3.27 trillion in Treasury securities that it piled on during pandemic QE.

The $4.4 billion decline was in line with the $5-billion a month pace of QT for Treasuries. The difference was the inflation protection the Fed earned on its holdings of Treasury Inflation Protected Securities (TIPS), which is added to the principal of the TIPS, instead of being paid in cash.

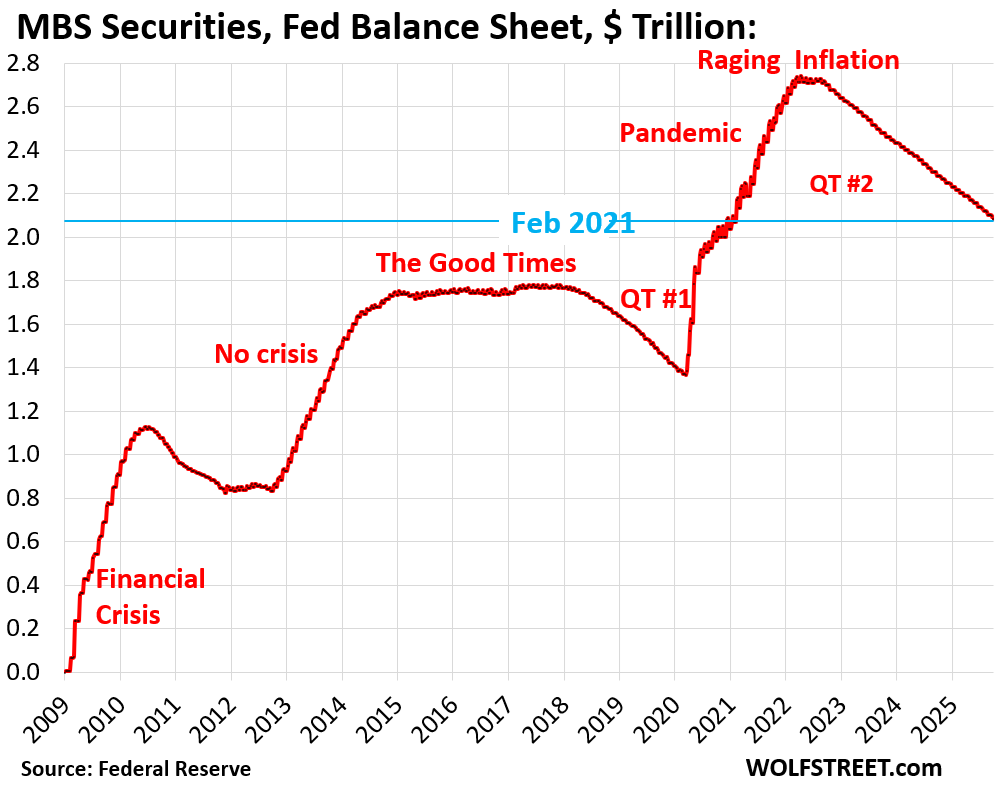

Mortgage-Backed Securities (MBS): -$16.8 billion in September, -$654 billion (-24%) from the peak, to $2.08 trillion, where they’d first been in February 2021.

The Fed has now shed 48% of the $1.37 trillion in MBS that it had added during pandemic QE.

The Fed holds only “agency” MBS that are guaranteed by the government (issued by Fannie Mae, Freddie Mac, Ginnie Mae), where the taxpayer would eat the losses when borrowers default on mortgages.

MBS come off the balance sheet primarily via pass-through principal payments that holders receive when mortgages are paid off (mortgaged homes are sold, mortgages are refinanced) and as mortgage payments are made. But sales of existing homes have plunged and mortgage refinancing has collapsed, and far fewer mortgages got paid off, and passthrough principal payments to MBS holders have slowed to a trickle.

As a result, ever since QT started, MBS have come off the Fed’s balance sheet at a pace that has been mostly in the range of $15-19 billion a month. The MBS runoff is not capped, whatever comes off comes off.

Bank liquidity facilities: a little bit of activity.

- Central Bank Liquidity Swaps ($0.0 billion)

- Standing Repo Facility or SRF ($0.0 billion), but there was some activity on September 15 (corporate tax day).

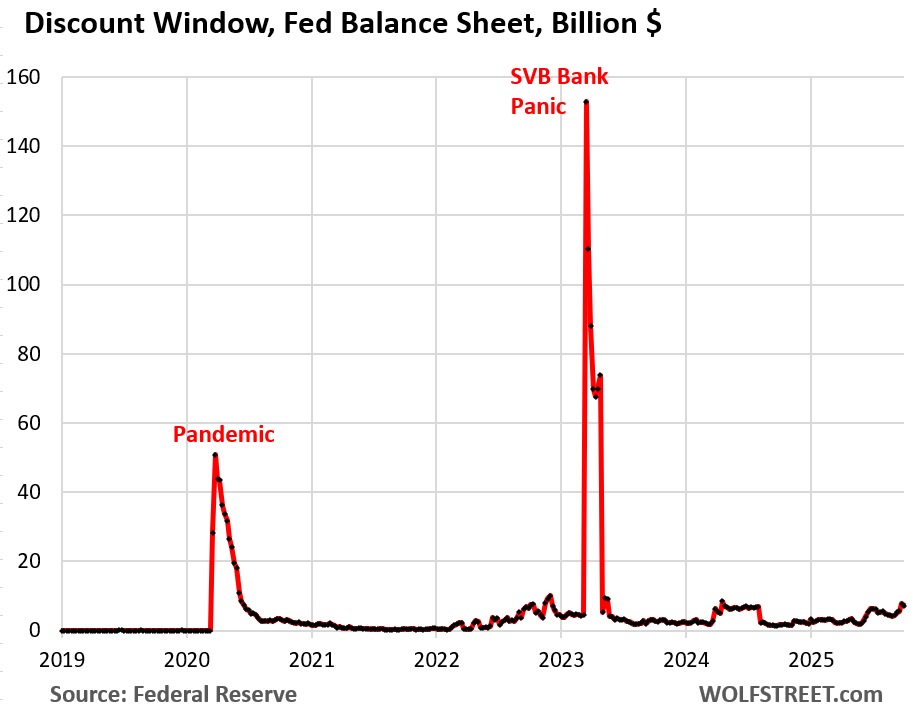

- Discount Window: +2.8 billion to $7.1 billion.

Both of these dates – September 15 and September 30 – entail large liquidity flows that can cause repo market yields to rise now that the Fed’s ON RRP facility, where money markets store excess liquidity, is near zero, after three years of QT.

The SRF: The Fed has been exhorting banks to use its new SRF, implemented in July 2021, to borrow there and to lend to the repo market when yields rise under tax-day or quarter-end pressures. Banks would make money on the spread, and it would keep those yields in check.

The Fed has been improving its SRF in various ways, including recently by offering its counterparties a morning auction, in addition to the afternoon auction.

The SRF’s ability to keep overnight rates in check has been cited in recent discussions as a factor in allowing the Fed to continue to remove liquidity via QT. And so far, it has been working.

But on September 15, just for this one day, $1.5 billion had been drawn on the SRF. On June 30, for one day, $11 billion had been drawn. By the current balance sheet as of the close of business on October 1, the SRF was back to zero.

This is the daily balance of the SRF from the New York Fed. The Fed’s balance sheet is weekly as of Wednesday and doesn’t capture the day-to-day moves in between.

The Discount Window: +$2.8 billion, to $7.2 billion. The Fed has been exhorting banks to use its Discount Window, or at least get set up to use it and pre-position collateral so that they can use it to help manage their daily liquidity needs. There has recently been some uptake.

What else…

“Unamortized premiums”: –$1.9 billion in September, -$125 billion from peak November 2021, to $231 billion.

With these regular accounting entries, the Fed writes off the premium over face value it had to pay for bonds during QE that had been issued earlier with higher coupon interest rates and that had gained value as yields dropped before the Fed bought them. Like all institutional bondholders, the Fed amortizes that premium over the life of the bond.

The leftover PPP loan balance from the pandemic: –$1.3 billion in September to near zero. That was the “PPPLF” in the pandemic era alphabet soup of SPVs, and it’s essentially gone now.

The only remaining pandemic-era SPV is the MSLP, it’s declining steadily and is down to $3.7 billion. All other SPVs have been zeroed out.

“Other assets”: +$6.6 billion to $35.7 billion. This $6.6 billion consisted mostly of accrued interest from bond holdings that the Fed set up as a receivable (an asset) in September, and that will be paid in the near future, at which point the Fed destroys that money, and the balance drops again. This account fluctuates weekly up and down based on these interest payments (the Fed doesn’t have a “cash” account, like companies do; it creates money when it pays for something and destroys money when it gets paid).

This account also includes “bank premises” and other accounts receivables and will always have a balance.

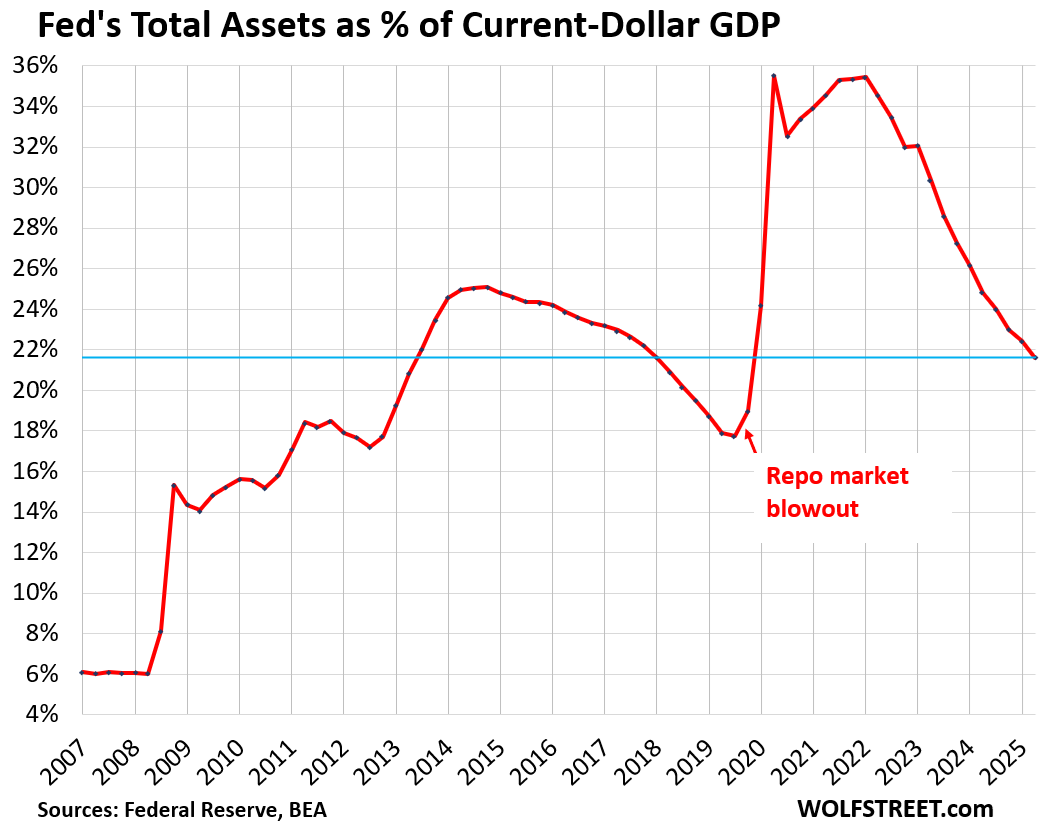

Fed’s balance sheet compared to the size of the economy. The Fed-assets-to-GDP ratio fell to 21.6% in September, where it had first been in Q3 2013 (total assets divided by “current dollar” Q2 GDP).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

God I remember some financial YouTuber using the m2 money supply as some economic red flag and it became clear they didn’t know anything about the Fed.

How is the M2 money supply not a problem? The amount of money available directly impacts the value of that money. M1 money supply directly pushes inflation, and M2 has the potential to become M1 over time, as funds are liquidized to make purchases. It is an indicator of future inflation, that has to be accounted for.

That’s a misconception. Money-market balances, CDs below $100k, and savings accounts — which are all part of the list of accounts in M2 — are investment choices, including for long-term investments, by people who don’t want to risk their money in the stock market and lose 50%. Those balances are like stocks, they are not used for future spending until retirement or hard time or down-payments for a house, no difference between investment choices, whether stocks, CDs, MM funds, T-bills, bonds, whatever.

Other issues with M2, just off the top of my head:

— M2 includes CDs of less than $100k but not CDs of over $100k. So you replace a $150K CD into two $75k CDs, M2 jumps by $150k

— Nearly half of US currency (paper dollars) are held overseas and has zero impact on the US economy. But it’s part of M2. That’s $1.2 trillion that is in M2 that isn’t in the US and has no impact on US spending. And that amount is growing every year because there is demand for paper dollars overseas.

— Inflation itself and economic growth see to it that more dollars are held in transactions accounts as the things they pay for got more expensive, such as a company with a growing number of employees due to sales increases, making higher wages due to wage increases. If over a four-year period, wages rise by 25%, and that company’s employment rises by 25%, its monthly payroll rises by over 50%, and it needs to have 50% more in its payroll account to pay these people. That’s a result of growth by the company and overall inflation wage inflation. Now multiply that by millions of companies. Those higher account balances are effects, not causes.

There are lots of other problems with M2.

This whole concept of M2 is just kind of nonsense. People think that “money supply” is some kind of magic. No, it represents balances in various types of specified bank accounts and MM accounts, plus currency in circulation. There is no magic to it.

This whole concept of M2 is nonsense, including that M2 includes CDs of less than $100k but not CDs over over $100k.

And in addition to all of these excellent points, I’ll repeat what I’ve said in other threads: there’s no consistent correlation between M2 and inflation.

During the highest inflation in modern history (the two peaks above 10% in 1974 and 1980), M2/GDP (i.e. the money supply as a percentage of the economy) was completely flat and much lower than today.

Yeah, even more opaque since Powell destroyed deposit classifications when he eliminated the 6 withdrawal restrictions on savings accounts in April 2020.

This didn’t have the same impact as the “time bomb” in 1981 (the widespread introduction of NOW accounts), which propelled N-gNp to 19.2% in the 1st qtr.

But this now allows the smallest savers to hold any temporary surplus cash in an interest-bearing account which can be shifted at little or no cost, and no loss of accumulated income into demand deposits or currency.

Numbers, do you think there is a correlation between money supply and ASSET inflation?

Put both side by side the past 20 years. It looks that way.

Cause and effect could be the other way around, that high asset prices contribute to increasing the account balances in the included accounts (people take profits for example).

The so called markets are rigged.

Excellent work. I still think the Fed thinks it’s risk mitigation techniques have too few unforeseen consequences.

They imperialized the world into it’s current model, what event are they planning next?? After the past 25 years anything is possible…corporate pro PAGAN da dominate peoples minds…the big lie theory dominated their minds…

I don’t understand any of this lol

Wolf, I think you told this before, but can’t remember the exact number.

What is the lowest balance Fed can have?

My calculation was $5.8 trillion back in March 2024. Fed governor Waller has then said the same thing a few weeks ago. This assumes that the Fed will stick with its “ample reserves” strategy. If it decides it can live with less than “ample reserves,” such as by relying on the SRF to provide liquidity when needed, the balance sheet could drop further.

Here is my calculation from March 2024:

https://wolfstreet.com/2024/03/23/the-feds-liabilities-how-far-can-qt-go-whats-the-lowest-possible-level-of-the-balance-sheet-without-blowing-stuff-up/

Wolf, what’s the status of the Fed’s total reserve assets? Back in March 2024, it was at $3.55 trillion. And you cautioned that the Fed probably can’t reduce below $1.9 trillion because the repo market blew out in 2019. How much of a dent has the Fed made in reducing its reserve assets, if at all?

The 2019 repo blowout wasn’t because reserves became scarce. It was because of nonbank disintermediation that was perpetrated by raising the remuneration rate on bank reserves.

It’s sort of like raising Reg Q ceilings in December 1965.

You’re talking about “reserve balances” (or short, “reserves”), which are a liability on the Fed’s balance sheet (deposits by banks). they just fell below $3 trillion. This is still very high. Not even the Fed knows how low they can go. But they can go lower.

They could probably decline by another $500 billion without problems.

If the SRF is capable of handling repo market squiggles, the Fed could decide that reserves could fall further, and there have been discussions about that.

In 2019, the Fed didn’t have the SRF, and so the repo market didn’t have guardrails, and when liquidity slowed, it blew out. The SRF was created in July 2021 in response to that fiasco and has been improved since then. It will likely not even allow a repo market blowout from forming as banks can borrow at the Fed’s policy rate at the SRF and lend to the repo market when rates rise and pocket the spread. The repo market is secured by collateral (Treasuries or government-guaranteed MBS), so it’s very low risk, but it has a huge volume, so even a small spread can make a lot of money. And that’s what we saw on June 30 and September 15, banks used the SRF to fund repo trades for one day and collect the spread, and repo rates remained relatively calm.

I know this is an assumption, but let’s go with avg $15B a month for argument’s sake. That gives us 4+ years before we get to the theoretical limit.

There are all sorts of things that could happen over that time frame. But the rate of change of total assets curve sure is slowing down.

JPowell is operating in what appears to be very challenging times indeed. I’m sure it wasn’t a cake walk when Volcker was jacking up rates, but nowadays seem much more complex, to say the least.

Haven’t people on the FOMC stated that they want to get rid of MBS completely. If so, wouldn’t that be a problem since there’s over 2.08 trillion of MBS left on the balance sheet? 6.59 trillion minus 2.08 trillion would leave them somewhere at 4.51 trillion. Can they even get rid of all the MBS from the balance sheet now without dropping to low?

So what they said is that they will get rid of all of the MBS, and when QT ends replace them with T-bills, and replace a big portion of the remaining Treasury notes and bonds, when they mature, with T-bills.

They said they will eventually sell MBS outright to speed up the process. So after QT ends, they would continue to get rid of MBS, via passthrough principal payments and outright sales, and replace them with T-bills.

They will also replace maturing notes and bonds with T-bills (minus the QT amount).

As the balance sheet declines slowly under QT, the composition will change, with T-bills becoming an ever larger portion, with MBS getting phased out, and with notes and bonds getting smaller, replaced by T-bills.

When QT ends, they will continue to get rid of MBS and replace them with T-bills, they will continue to replace maturing notes and bonds with T-bills.

They have not specified the exact proportion of T-bills to notes and bonds that they want to achieve. Logan and Waller had some differing views on that. Waller thinks that maybe the proportion should track the proportion of all Treasuries outstanding (total T-bills are at 17% now and heading higher). As T-bills become a bigger part of all Treasuries outstanding (they may be at 30% in two years), the Fed would have more T-bills available to get its proportion to 30% (from near 0% now). Logan thought that T-bills should be a primary position, and notes and bonds a smaller position.

All this would take many years.

About two more years at the $30B/mo. pace. So at Thanksgiving 2027, we can toast whoever is pulling the strings at the time. Assuming there are no reductions in pace or hiccups between now and then.

The Fed has been the greatest enabler of bad behavior the world has ever known. The Fed is an abomination and has facilitated the greatest transfer of wealth the world has ever seen. Taking from the productive (labor) and giving to the 0.1 % (banking and capital).

This is the truth of it. Time to restore equilibrium.

Interesting times.

“The Fed has been the greatest enabler of bad behavior the world has ever known.”

Well said. A racket operating right before our very eyes……

I will always find it funny how the Fed lost the mystical knowledge of the SRF during the 2010s.

Indeed. Now this administration is buying equity in companies that agree to their concessions, straight up bribery while taking ownership of productive capital. Exactly what China and Russia have done for years. So much for fostering competition and capitalism. Communism is all the rage now.

Hedge accordingly.

WB,

I wouldn’t compare what China does to the US. The US believes the market should control all whereas China does not. I honestly consider one of the significant differences, although there are many, is that in China, politicians are not beholden to corporations like here. China is about 50/50 with ownership and even Finland nationalizes about 30%. I would argue, and many would disagree and likely call me names, that more nationalized assets are good for the people in you have something other than lawyers running government. The top level of Chinas government is almost all with engineering background, which does have some drawbacks too, but they are built to solve problems and build stuff. We have just gotten used to thinking we have a great democracy but just doesn’t happen to be working right now. Solid illusion.

WB,

This administration has converted some of the previously agreed to grants (gifts) into equity stakes, that’s all they did. Rather than just giving Intel the money, as Biden had done, they renegotiated that grant (a gift) into an equity stake, same money, but now least the taxpayer gets something, and shareholders got diluted.

Welcome to the world’s largest casino, whose regs and oversight change, as needed, to benefit the house but not the staff.

Thank you Wolf!

Is it BOJ month? :)

I love how your charts show that absurd liquidity injections, for which all dollar holders are now paying, created the speculative asset bubbles that had nothing to do with shortages, assets, productivity, economics or really anything but money printing. So now the trumpsters want to restart manufacturing of goods and services when we have a generation of workers who have ummm never witnessed actual productivity?

Yes, they will probably publish it on Monday.

And the ECB’s quarter-end balance sheet, which includes the gold mark-to-market, also comes out next week (Wed), and I will cover that as well.

Thanks for the information. Continuing to buy Gold.

I haven’t heard anything recently. What is the latest on Freddy and Fannie returning to private enterprises?

They’re arguing over it. There are lots of issues with it, not an easy thing to do, lots of conflicting interests too.

I’d support it if the definitely-not-explicit gov guarantee went away. But Trump previously “Truthed” about that being a feature of any IPO. So that outlook isn’t great.

Yes it would raise interest rates, but it should. You’re asking private investors to accept more default risk on the guarantees.

Why privatize the profits if we’re going to socialize the losses? Same reason equity stakes for capital in companies are better than grants!

But I admit I’m a ‘bitter renter’ who missed the boat on gov policy saying housing will never fail on their watch.

Do you have a link to the guest article from earlier this year that explained why it would be bad for the American taxpayer if they “privatized” those GSE again?

I recall it presenting a persuasive argument and I can’t seem to find it.

Yes, that was a very good article. Everyone should read it:

By Alex J. Pollock & Edward J. Pinto.

https://wolfstreet.com/2025/04/01/not-another-free-lunch-dont-let-fannie-and-freddie-turn-back-into-gses/

I’ve been enjoying the nerd fight between AEI and Vantage Score on credit scoring models.

They recently provided an estimate of how much revenue the GSEs could lose if ‘score shopping is permitted.

Another ‘What do you think’ question. Do you ever look at the US Debt Clock .Org website? Do you think the moving numbers have any bases in reality?

No. It’s just an algo. And it’s made to look fun, like a slot machine in Las Vegas. And it’s way off.

Debt doesn’t work that way. Debt grows on days when new bonds are sold, and it falls on days when old bonds mature and are paid off. It doesn’t go second by second, but day by day. And on days when no bonds are sold and no bonds mature, the debt doesn’t change at all. But the Debt Clock never stops.

In terms of the US debt, the Treasury Department publishes the actual debt outstanding every day. All you have to do is look at it. That’s the real number.

Thanks, awesome answer!!

MW: Dow industrials surge 440 points as U.S. stock-market indexes seek to put six-session win streaks on the board

SPX +0.47%

DJIA +0.95%

COMP +0.22%

For the first time in a long time, the stock market is starting to terrify me.

I don’t care about my portfolio or my 401K, as I don’t need that for a while. What I care about is listening to tons of people, from colleagues, to friends, saying “Keep investing in the indexes, as, even if there’s a decline, it’s guaranteed to be higher in 2 years.”

This mentality is what’s driving all investment. Almost NOBODY thinks a long-term drawdown, like Japan after 1989 or the U.S. after 2000, is possible. Therefore, the idea of considering risk is out the window, and just buying indexes always makes sense. Regardless of what you hear about stocks being “forward looking,” there is no metric that shows these stocks at a reasonable valuation. P/E of 31. Schiller PE of over 40. Record prices to sales revenue. Warren Buffett indicator of 221%. Everything is priced for double digit growth, year in and year out.

I wouldn’t care if a protracted bear market only affected large investors and institutions. But it seems now that the economy, from the top 1-2% who spend a disproportionate share of the money, down to those who are investing on Robinhood, is entirely dependent on the wealth effect from these stocks.

Something happens to break people’s confidence in “stonks only go up,” and the decline could be catastrophic for society.

What’s the solution?

One more data point, dividend yield is nearly at the record lows of 2000 (1.2%). Every raw numerical indicator looks very similar to the 1998-1999 period.

Hopefully, the AI hype that is driving this is real enough to drive earnings higher. But one earnings miss or one big world event similar to 9/11 (telling the world it’s ok to unilaterally bomb things whenever we want is not exactly setting the best example) and it could look a lot like 2001.

I don’t think higher earnings are coming for quite a long time. The thing is, most AI spending seems to be by the Mag7, who are just using their profits that SHOULD be dividends. But investors don’t seem to care at the moment, that their profits are being wasted on this.

Except earnings have grown 30% in a little over 2 years, so they are coming. They’re just not rising as fast as the market itself. Now whether the expected earnings will eventually come, well, that’s the big question. Lots of reasons to be skeptical.

Yes, they’ve grown, but I’m skeptical that the growth had anything to do with the AI investment.

The issue is that a P/E of 40 means that type of growth is projected forever. I’ve been astounded that the big tech companies can grow earnings the way they have, but at some point, isn’t there a limit based on the actual economy around them?

For people stuck in 401K, I’d say hedge with protective put ‘insurance’ strategy on an outside account, mimicking the holdings in the 401k. Hard to find 401K choices with US Treasury money market.

Thats the solution. One match to light the fire. Could be violent downs and violent up rallies on the downside much like dotcom era where the naysayers kept saying this is a temporary dip. Problem is the hyperscalers driving this AI bubble have nearly unlimited ammo with $500B war chest to keep going until they decide to stop the music. May need another DeepSeek moment that is more real than hype, i.e. where costs come down and the Infra build and vast spending on GPUs and data centers and even electricity plummet. Then we’ll have the standard shake out.

People are being uncareful about risk, agreed, but while the fed is draining money, the govt is still providing a lot of fuel and perpetuating an illusion of normalcy, easy money by washing huge amounts of money over the country with 1-2 trillion in deficit spending that a large amount of these investors or gamblers are unaware and dont understand the implications of, so it’s both parties of Congress, the Administrations, and the Fed (shouldnt have done money printing rate suppression to begin with) over a long period of time, whose job is to be fiscally responsible, at most fault.

Yeah, it blew out Elliott Wave Theory’s top.

I’m not that familiar with it. What happened?

Invest in gold.

Wolf: you might like

https://macroeconomicpolicynexus.substack.com/p/from-floors-to-ceilings-the-feds

Yes, they’ve been talking about it. Williams too made reference to it. The new SRF is a game changer for them. It allows them to control money market rates with much lower reserve balances. Logan has pointed out very proudly how it did that on the few days when there was some uptake. Logan, having run the SOMA portfolio and trading desk at the NY Fed, understands the technical issues probably better than anyone else at the FOMC.

We still haven’t seen anything crop up about it in the minutes. So we’ll probably get more speeches on this topic.

At the current pace of QT (slow), they can just let QT run for years and very gradually ease into it. They don’t even have to make an announcement per se. Just let reserves drain slowly and watch how the SRF deals with money market squiggles.

They have the explicit support from Bessent to do this. One of the Fed chair candidates, Warsh (former Fed governor) has come out strongly in favor of it too.

There are huge benefits for the Fed’s profitability (and remittances to the Treasury) for running down its assets and reserve balances.

The other thing they’re going to do for sure is shift their assets from notes and bonds and MBS to T-bills. But they need $3 trillion of T-bills to replace $3 trillion of notes, bonds, and MBS, and there aren’t enough T-bills out there to do this. So Treasury is ramping up issuance of T-bills and keep issuance of notes and bonds steady, so the Fed can start shedding its long-term securities, which the market will have to absorb. But all this stuff is in slow motion.

Logan also gave a big speech on shifting the Fed’s target range from the largely irrelevant federal funds rate to one of the repo rate indexes. She proposed the “tri-party general collateral rate” (TGCR), which she said is “cleaner” than SOFR as it tracks a subset of the repo market.

https://www.dallasfed.org/news/speeches/logan/2025/lkl250925

Great link. Logan was born when the markets were topping.

The FED’s still pegging rates, over a 24-hour time horizon rather than restricting reserves over 24 months.

Could you clear this up for some of us….

If the SRF is where, as you say, banks can borrow and lend…..then there can be both repurchase and reverse repurchases going on at this facility, correct? And the rate structure the Fed implements controls what exactly goes on, yes?

So the SRF is where banks can either put up collateral and take cash, or they can give cash and take securities …… but it is usually one or the other, never both going on? right? (depending on the rates the Fed sets)

Thanks

Your 1st sentence: no, that’s not correct. The counterparties at the SRF can only “borrow” from the SRF (they cannot lend to it). To lend to the Fed, banks use their reserve accounts (just leave the cash in their reserve accounts at the Fed and earn interest). They can also lend to the Fed via the ON RRP facility, but it pays a lower rate than reserves.

Your 2nd sentence: the rates that the Fed charges for borrowing from the SRF and Discount Window and that it pays for reserves and ON RRPs are part of the 5 policy rates that the Fed sets during its FOMC rate-setting meetings. Read this, it gives you the 5 rates after the first paragraph:

https://wolfstreet.com/2025/09/17/this-fed-meeting-must-have-been-a-circus/

Your 2nd paragraph doesn’t make sense; it’s based on the wrong assumption in your 1st sentence.

“The SRF: The Fed has been exhorting banks to use its new SRF, implemented in July 2021, to borrow there and to lend to the repo market”

I guess I misunderstood your above statement i which you use both borrow and lend

Yes, to borrow from the SRF and then to lend these funds to the repo market, and make money on the spread.

Hmmm. So if the Fed still has ~3% to cut fast during a recession, and the MBS rolloff increases to $30-35B a month at the same time because of said recession as people have to move, dump houses, whatever, then the Fed could also BUY $30-35B of T-Bills at 0.5% and not technically be doing QE as the balance sheet would not actually be increasing?

The Fed could also start selling MBS outright — it has talked about that. The current cap is $35 billion. If the roll-off exceeds $35 billion, the Fed would replace the excess with T-bills. MBS roll-offs have never reached that cap. The Fed could reach that cap by selling about $15-20 billion in MBS a month on top of the $15-20 billion that roll off to get to the $35 billion.

The Fed is currently replacing all but $5 billion a month in maturing Treasury notes and bonds with roughly the same notes and bonds. When it switches to T-bills, it would replace maturing notes and bonds with T-bills. As QT continues, and the balance sheet declines, the process of shifting to T-bills and getting rid of MBS would go on. And when QT ends, the process of shifting to T-bills and getting rid of MBS would also continue.

It would take many years. There aren’t even enough T-bills out there now to do that.

The FED paused rate hikes too soon, was way too anxious to cut, and tapered QT way too soon. The entire system is awash in massive liquidity as the biggest credit/everything bubble in history rages on. This whole thing is disgustingly sickening.

Nah, the real problem was raising them too late. They were right to stop where they did, they just should lower any further from here.

What about the Fed’s “Deferred Assets”? I don’t see those listed on their balance sheet, although there is a footnote about it.

The last I read they were losing 5 to 11 Billion / month on Interest payments. That almost wipes out the 15 Billion of QT.

They’re “liabilities” listed under “Other liabilities and capital,” on the liability side of the balance sheet (here we’re discussing the asset side of the balance sheet). This amount is negative (a negative liability). Normally, this is the account where the Fed tracks the remittances that it sends to the Treasury (so normally a positive liability). Since the Fed is losing money, it’s not sending any remittances, but it’s tracking its losses in this account, like an amount that it is owed by the Treasury, and when it starts making money again, the profits will go against that account until it’s no longer negative and all the losses have been wiped out by profits, and when it turns positive, the Fed will start sending those positive amounts to the Treasury as remittances (so back to normal then).

There is approximately a trillion$ in leverage that jacks up the S&P, which is higher than when Lehman Brothers collapsed. And how much does the Fed balance sheet impact the stock markets?

Wolf,

I know the Fed purchased junk bond during the 2019 QE efforts. I know this because I was on the other side shorting junk bonds and thought my ship had finally come in, only to find that the Fed did a rug pull on me…. It was reckless but they managed to stabilize even that mispriced market and assure junk bond investors that there is a Fed put. Have all those junk securities been sold? I think they also purchased even non-agency mortgages too.

Yes, it sold all of its corporate bonds and bond ETFs by Nov 2021 and made $513 million on those trades:

https://wolfstreet.com/2021/11/19/after-fueling-corporate-bond-junk-bond-rally-to-lowest-yields-ever-fed-ends-bailout-spv-with-513-million-profit-sends-90-to-us-treasury/

Thank you Wolf for reporting on QT.

Your one of the few who report on it & I look forward to the articles.

I imagine Wall Street hates QT with a passion & can’t wait for QE & bailouts for billionaires.

I have long ago designated WSJ, FT, & CNBC as propaganda & read my news from you. So your on my top 5 reading/hero lists.

I’d be curious who your hero list ?

Me, its… Michael pento, Wolf Street, zerohedge, melody wright, John Rubino, & of course Lacy Hunt…

I’m your biggest fan.

Thank you!!