Household money-market funds surged, large CDs also surged. But small CDs are the hot money; they flee when yields drop.

By Wolf Richter for WOLF STREET.

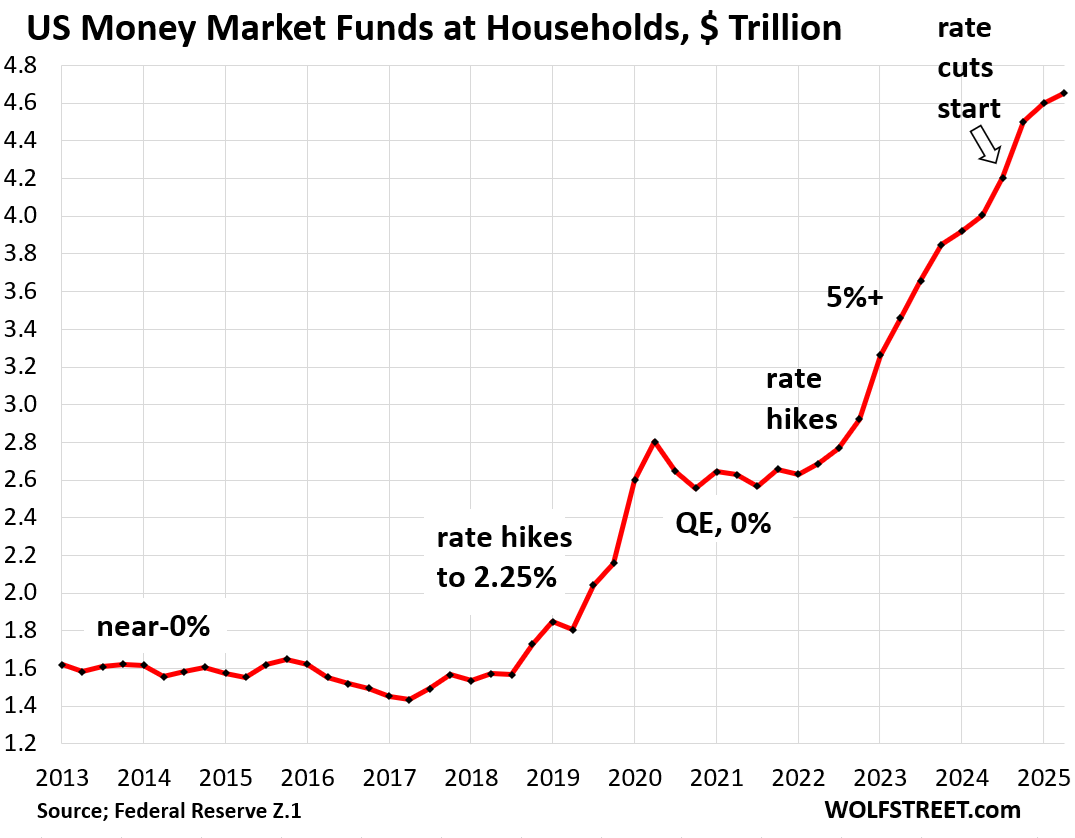

Despite the Fed’s rate cuts of 100 basis points in 2024, and therefore lower yields on money market funds, households continued to pile their cash into them. Banks have lowered the rates they pay on CDs, and holders of small CDs, always the hot money, have started to cash out. But balances of large CDs continue to grow. On net, their huge pile of interest-earning cash grew further.

Balances in money-market funds held by households rose by another $55 billion in Q2 from the prior quarter, and by $650 billion year-over-year, to a record $4.65 trillion, according to the Fed’s quarterly Z1 Financial Accounts yesterday. Since Q1 2022, when the Fed started hiking its policy rates, balances have surged by $2.02 trillion.

These money market fund (MMF) balances include retail MMFs that households buy directly from their broker or bank, and institutional MMFs that households have indirectly through their employers, trustees, and fiduciaries who buy those funds on behalf of their clients, employees, or owners.

MMFs invest in safe short-term instruments, such as in Treasury securities with less than one year to run (anything from a 1-month T-bill to a 30-year Treasury bond that matures in a few months), in high-grade commercial paper, in high-grade asset-backed commercial paper, in repos in the repo market, and in repos with the Fed (ON RRPs).

The Fed’s five rates form a floor and ceiling for short-term market yields, such as the gigantic repo market, to which MMFs are big lenders.

Short-term Treasury yields track the Fed’s policy rates expected in the near future. The three-month Treasury yield dropped in recent days and is at 4.03% currently, fully pricing in one 25-basis point rate cut next week, whereby the Fed would bring its five policy rates down to 4.0% at the low end and to 4.25% at the high end.

Many MMFs still have a yield above 4%. But yields of many Treasury money market funds have fallen below 4%.

But when Q2 ended on June 30, the 3-month Treasury yield was still 4.34%. And so the household MMF holdings of $4.65 trillion at the end of Q2 were still earning the yields prevalent at the time, roughly 30 basis points higher than today.

All these yields are still positive in inflation-adjusted terms: CPI inflation – in another nasty surprise that inflation tends to dish up – rose to 2.9% for August.

If the Fed cuts short-term rates aggressively while inflation continues to accelerate, it won’t take long before real yields on MMFs turn negative.

Falling yields, and especially negative real yields, would suggest that households yank their money out. But as we saw in 2020, nominal yields plunged to near-0%, and by early 2022, real yields were around negative 7% and falling further, and household MMF holdings barely dipped.

But when yields rose sharply later in 2022 and through mid-2023, MMF balances exploded and they continue to surge though yields have backed off by over 100 basis points.

So it will be interesting to see how far yields would have to fall before aggrieved households begin to drain those MMFs. And as we saw, it might not make a big dent.

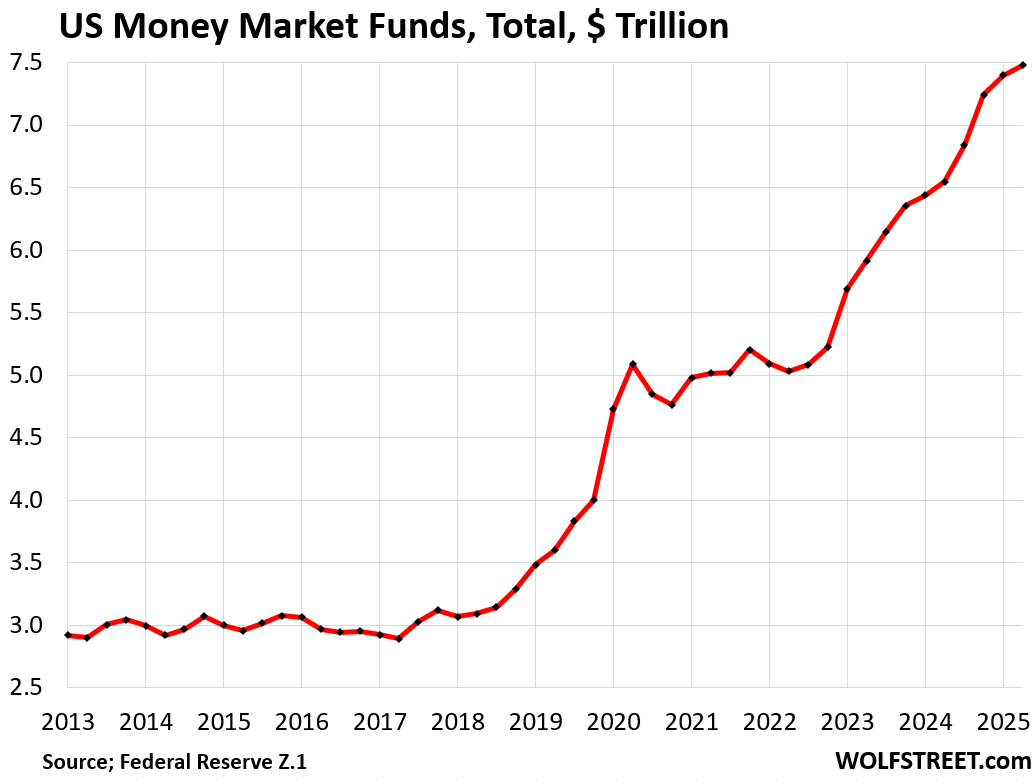

Total MMFs (those held by households and institutions) rose by $83 billion in Q2 from Q1, and by $933 billion year-over-year, to $7.48 trillion. Since Q1 2022, balances have ballooned by $2.39 trillion.

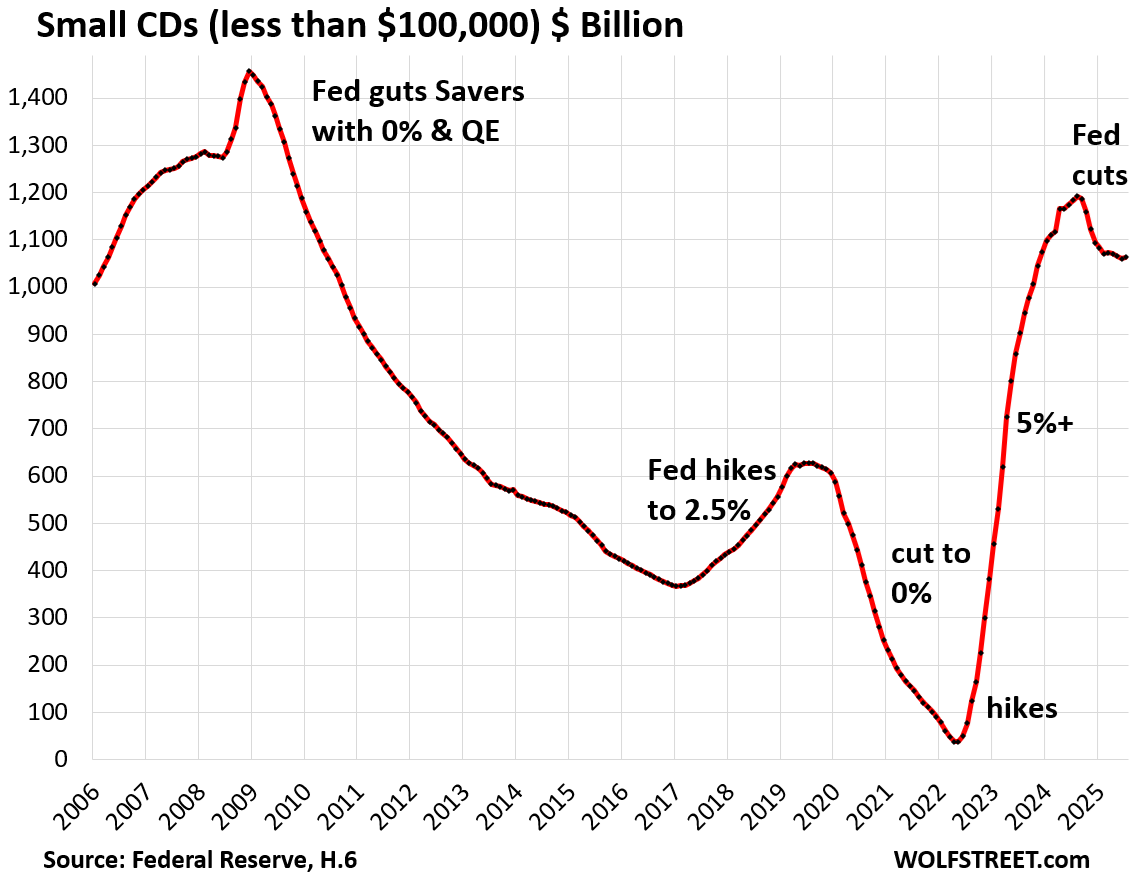

Small Time-Deposits (CDs of less than $100,000) react fairly quickly and strongly to interest rates offered by banks. They’re not “sticky” at all. They’re the hot money.

In July, balances ticked up a hair from June to $1.06 trillion, according to the Fed’s latest Money Stock Measures. But that was down by $129 billion from just before the Fed began cutting its policy rates in mid-September 2024.

In the time frame of Q2, small CDs fell by $13 billion quarter-over-quarter and by $114 billion year-over-year.

As soon as the Fed started cutting rates in mid-September, which caused banks to cut the interest rates they offered on CDs, balances began to fall.

Balances fall gradually as holders don’t reinvest the proceeds from maturing CDs. Some CDs have short terms, such as 3 months or 7 months, others go out further, 2 years, 5 years, and longer. So it takes a while for balances to drop, as we can see in the chart below.

When the Fed gutted savers’ cash flow from savings in 2008, they began cashing out, and by mid-2022, small CDs had nearly vanished. But note, when the Fed started hiking its policy rates, balances of small CDs exploded from near-zero in April 2022 to $1.19 trillion in August 2024. The hot money!

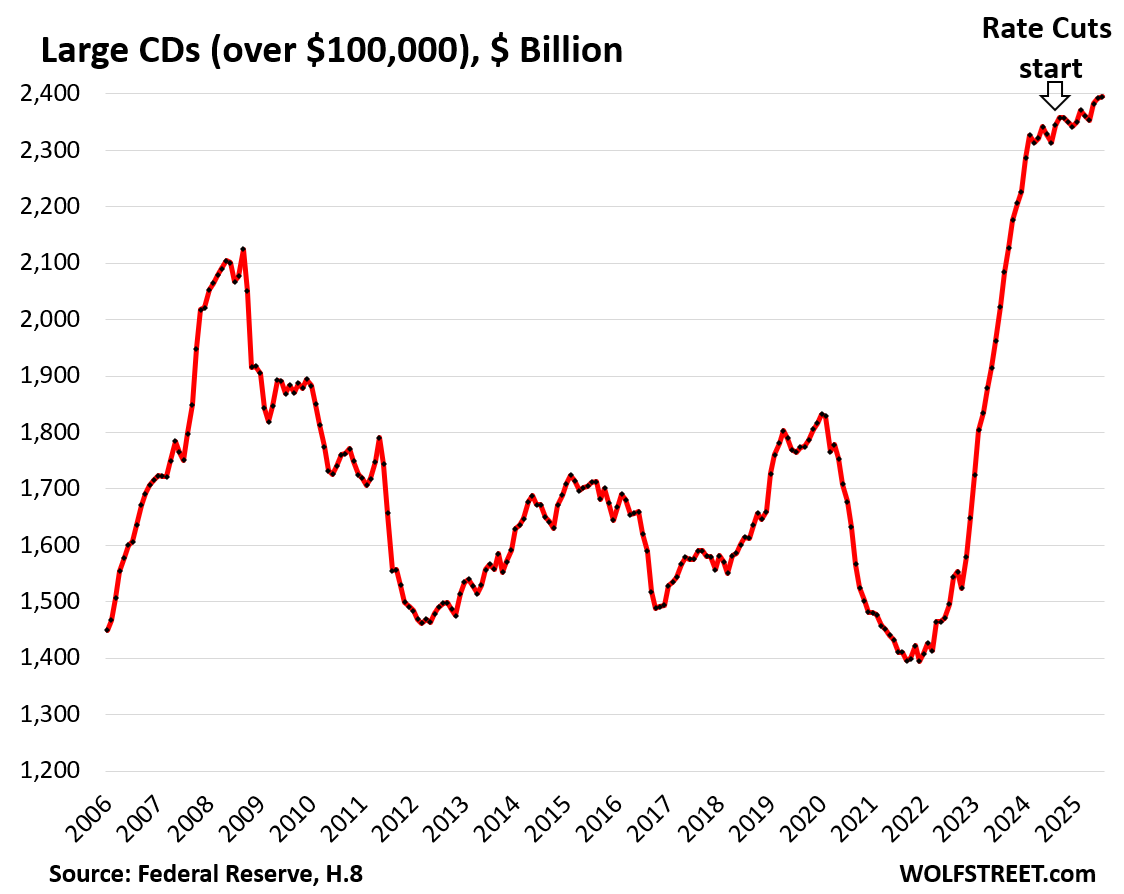

But Large Time-Deposits (CDs of $100,000 or more) continued to inch from record to record, and in July reached $2.40 trillion, up by $82 billion from a year ago, according to the Fed’s monthly banking data.

In the time frame of Q2, large CDs rose by $32 billion QoQ, and by $82 billion YoY.

Since March 2022, when the rate hikes began, large time-deposits have surged by $982 billion.

So, with…

- Household MMFs +$55 billion QoQ and +$650 billion YoY, and

- Small CDs -$13 billion QoQ and -$114 billion YoY, and

- Large CDs +$32 billion QoQ and +$82 +billion YoY

these piles of interest-earning cash combined increased by $74 QoQ and by $618 billion YoY, to a record $8.11 trillion.

In addition, many Americans hold high-yield savings accounts, but they’re not included here.

In addition, many Americans hold T-bills directly, either in their brokerage accounts or in their accounts at the government’s TreasuryDirect, and they’re also not included here.

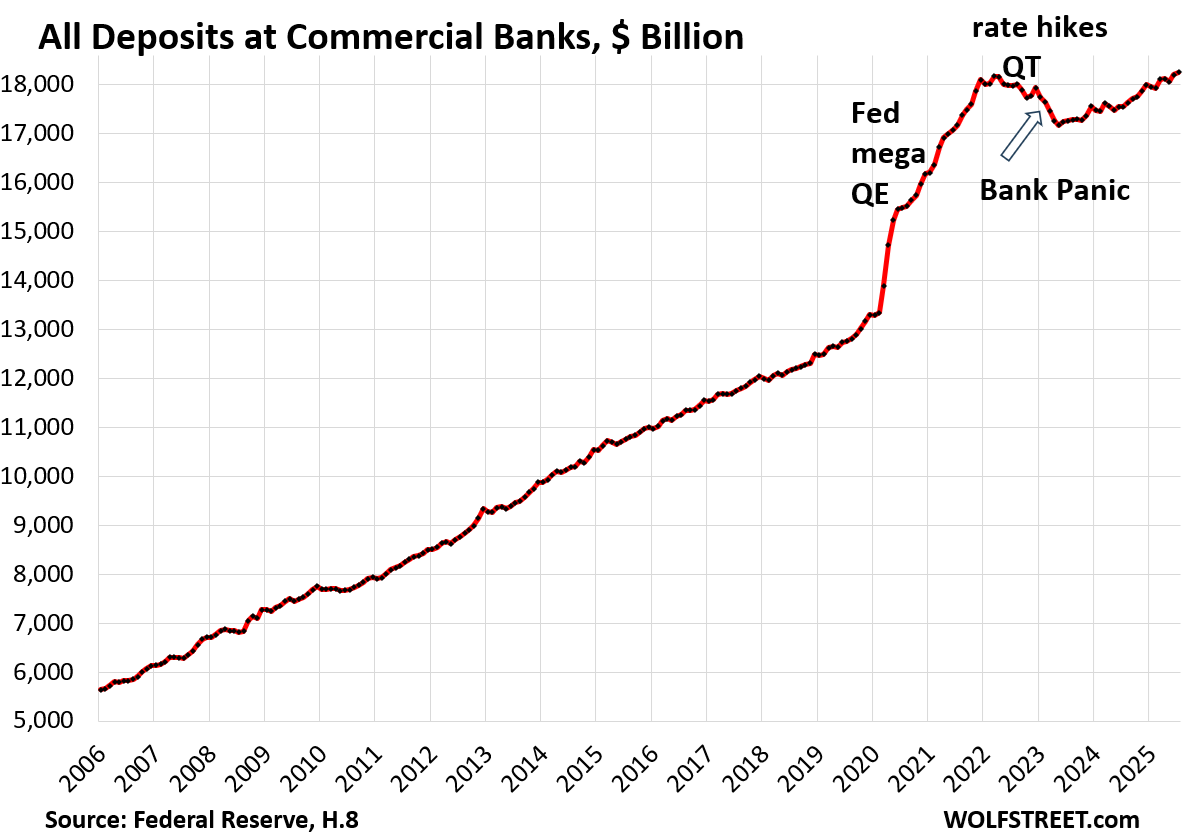

CDs are only a small part of total bank deposits. Total deposits at commercial banks rose to $18.3 trillion in July, back where they’d been before the rate hikes and QT. Balances had dropped by nearly $1 trillion in the first half of 2023 during the bank panic that caused three regional banks to collapse. But the FDIC made all depositors whole, the dust settled, and deposits started coming back.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

MW: As Fed nears highly anticipated rate cut, the market ‘really hinges’ on 10-year Treasury yield

So far, the idea of a lower ST rate has caused mortgage rates to drop. Lenders must think a rate cut is appropriate at this time, even though inflation is still running well above target for the 5th year in a row.

This result makes little sense to me. I sense bondholder complacency.

A year ago, mortgage rates dropped until the day of the 50-basis point rate cut. Then on the day of the rate cut, they rose, and they kept rising until they’d risen by over 100 basis points, while the Fed cut 100 basis points.

We discussed this here in the comments at the time, live, as we were watching it develop on the day of the rate cut. It was interesting.

Unless the bond buyers think that the reduced new jobs means that inflation will die on its own (making the reduced yields more palatable), and that longer-term stagflation isn’t a possibility.

I think there is sort of a feedback cycle going on. Higher stock prices push conservative investors more heavily into bonds, which reduces rates and leads to even higher stock prices.

It might end with a whisper when valuations receive attention and momentum sputters, or bond investors smell the rot.

Are there any Mortgage originators that keep the loans they create on their own balance sheets ? I suspect mostly they sell them off ASAP and just retain the servicing business.

Given that reality what forces really set the Mortgage rate ? Would it be what the Federal agencies are willing to pay, what the demand is for CDO’s and MBS. I don’t know. It’s a mystery to me.

If I were a bank would I be willing to keep 30 year paper on my own Balance Sheet for 6% ?

Most mortgages (aside from so-called jumbo loans) get sold to the government agencies like Fannie Mae, who then package them up as mortgage backed securities and sell them to the Bond market. The bond market compares what those MBS bonds yield compared to treasuries. Generally they’ll compare to the yield on the 10 year treasuries, because most mortgages last about 10 years on average (people usually move way before the 30 years are up).

If the MBS offers less yield than the treasuries, the market would rather buy treasuries. Thus banks know that they must offer a slight premium to the 10 year Treasury to get the market to buy their loans, so they in turn price their mortgages in order to profitably offer that yield.

In that way, market effects on the price of 10 year Treasuries (be it Fed action, inflation expectations, “flight to safety”, etc) gets transmitted to market effects on mortgage rates.

Hope that makes sense.

What the Fed does with respect to rates is becoming more irrelevant. Risk is being repriced globally, things change slowly then “all at once”. As central banks and sovereigns around the world replace treasury holdings with physical collateral (mostly gold) we all know where this is heading, eventually.

Hedge accordingly.

Wolf, if the federal funds rate go lower, let’s just say zero for the moment, and those in MMFs move to buy Notes instead of Bills, doesn’t that also force the Treasury to finance it’s debt with Notes?

No, MMF must cannot do that. They cannot buy anything that matures in more than one year, and their weighted average maturity must be 60 days or less. Those two are what makes MMFs safe. They’re regulatory requirements.

The question was whether the treasury would be forced to issue notes.

I.e. if the Fed offers negative real rates on the low duration end, can they fill all the orders they hope to fill? Or will demand move further up the yield curve?

Wolf Man…

My money in the bank earning maybe 4%….Let’s look a little further…

Beginning of year $1000. End of year $1040 (more or less). My pile of cash at end of year

= BIGGER! Yay!!! Well, uh, no.

That larger pile of cash at year’s end will buy less goods and services that it did on Jan 1st. More pieces of ‘paper’, less purchasing power.

I’m almost finished with my book, ‘Banking for Dummies’.

The idea of yield is to be larger than inflation = positive “real” yield. CPI inflation = 2.9%. Yields over 4% = positive “real” yield. If inflation goes to 3.5% and the Fed cuts to 3.0%, then the “real” yield will be negative.

Read the article. It explains that.

With stocks, you can lose 50% due to market value decline over three years and lose another chunk due to inflation. So a loss of maybe 60% or more. Or you could make more.

That’s “risk.” A nearly risk-free asset, like a MMF, has a smaller potential return, than an asset where you can lose 100% of your principal.

And tax on the yield makes it a harder choice, for anyone earning enough to pay income tax.

After tax the 4% yield is ~3%. So right now we’re all just breaking even. Real yield will be negative soon.

All income is taxed eventually. Why is this brought up ONLY with fixed-income investments? Because it’s easier to figure than taxes on your labor, stock gains, etc.? What kind of bullshit is this argument?

What you should bring up in this discussion is RISK. That’s what is different between these investments, not taxation (in fact, some fixed income investments, such as munis and Treasuries have tax advantages that other investments don’t have).

You can’t let taxes be the tail wagging the dog. This is how you get people buying a home that can’t afford because the mortgage is deductible.

I was just stating that Money Market accounts aren’t beating inflation.

With regards to taxes interest income is ordinary income. Qualified dividends and long term capital gains are taxes at lower rates.

I’m not arguing the risk associated with investments. Just that my interest income isn’t making me richer. It’s just keeping up with inflation and soon by leaving it sitting in a money market it will be losing to inflation.

1. You don’t pay state income taxes on Treasuries and Treasury money market funds at all, and you don’t pay federal income taxes on munis.

2. When the S&P 500 declines 50% and the Nasdaq 78% as it did during the dotcom bust in 2000-2002, or by 50% again in 2008-2009, you’re not beating inflation either. Took the Nasdaq 15 years and lots of money printing to get back to its 2000 high. That’s “risk.”

I’m really worried that so many people think that the concept of risk doesn’t exist anymore.

For a musical version of real yield going negative there is the Nigerian pop song video in English: “I go chop your dollar” by Nkem Owoh; available on YouTube.

Lyrics: “I go chop your dollar,” “…make your money disappear…”

I know all to well with my Lehmon Brothers bonds highest on the debt scale but cents on the dollar when a bank of that size fails .

Still don’t know why Lehmon Brothers was not bailed out in 2008.

“Still don’t know why Lehman Brothers was not bailed out in 2008.”

I still don’t know why ANY of these gangster organizations were bailed out.

Bailing out executive jobs and bonuses, executive pension plans, stockholders, bondholders etc. was just nuts and created the moral-hazard monsters we have now.

Why should ANY private org like Lehman’s be “bailed out”?

Just to give their lenders and investors a risk-free guaranteed return at the taxpayers expense?

What makes Lehman’s investors more special than everyone else?

As usual MSM claims to say 7.5 Trillions sitting on sidelines so Stocks will only go up. Complete BS. Now ON RRP have almost vanished. All those Money market funds are invested into Short term/medium term. So its not like that cash is lying around where people can buy stocks.

If those funds money invested into Stocks, Treasury and Bond markets yields will go up in order to entice the investors. Someone has to buy Govt Debt.

Sure those high balances are having wealth effects specially retirees who have piles of cash. Even at 4.3% they are enjoying their new revenue stream. This revenue stream was killed by FED for 15 years.

The “money on the sidelines” is the funniest BS ever, and it refuses to die though we have driven wooden stakes through its heart many times here.

It is absurdity to the extreme because it makes the assumption that the individual who is high or medium risk adverse chasing interest rate returns will suddenly wake up one day and say, “You know. I should take my MM money earning 4.5% and now invest directly into high risk equities at an all time high because my monthly interest return dropped by .5%.” I remember when this same group of individuals were chasing 0.25% CDs and bank MMs in 2010. However, it does make for a good sound bite for equity pumpers to make the argument that the party will keep rolling. The mountain of cash these cash hoarders are holding onto needs to be “…put to work! How dare people attempt to get a moderate or even small return on their money with lower risk!” It took several years for a lot of these slow moving individuals to wake up and just move their money from almost zero bank interest accounts to higher dividend MM accounts. I don’t see the scenario of them now reacting to a a drop from 4.25% to 4% return or even 3.5%.

The dishonest use of the language is intentional. It’s not just “money on the sidelines.” Even “put to work” is dishonest, as it implies that the money will be used to finance capital investment by companies. That’s only true for IPOs and existing companies that are issuing new shares to raise money.

Most of the “market” is just algos trading the same shares back and forth. That’s not “putting anything to work” in the sense that it’s being described.

…which puts the capital gains rationale to shame. When passive investors trade existing securities again and again, nothing is invested in the real economy. It’s the original purchase of equipment, bldg, and jobs that matters. I’d much rather see an investment credit than a capital gains rate preference. It’s another government handout, largely to the wrong folks.

Bobber, that’s an interesting point I hadn’t thought of.

It’s actually a consequence of bigtech and other companies getting such a stranglehold on the market. They don’t need new investment, in fact, they can buy back their shares with their cash hoard.

I am confused. I thought my money in short term t-bills is considered the “money on the sidelines”.

You are right, that’s “money on the sidelines”. Warren Buffet does the same thing.

@Gabriel, you have it right, that’s money on the side lines, just like Warren Buffet has a bunch of Berkshire Hathaway’s money sitting in T-Bills.

You need to distinguish between individuals and everyone in aggregate. An individual can have “money on the sidelines” for himself. However, in aggregate there is no money on the sidelines because every financial instrument (cash, stocks, bonds, etc.) must be owned by someone at every point in time until the instrument either matures or is retired. Financial instruments can be traded, but they retain the form in which they were created until maturity or retirement.

I dont think your Money in T-Bills is Money on sidelines. Neither Warren Buffets’s T-Bills investment.

They are invested in Bond market. Short term but its invested in Debt markets. Govt is borrowing your money. If you take out that money, someone else needs to buy that Govt Debt. so its like transfer between two types of assets.

Post Covid, FED printed so much, there was no place for Money Market funds to invest without pushing T-bills yields negative. So they parked in FED ON RRP facility and earned minimal interest. That balance went to 2.2 Trillions. I will say that was money on sidelines. Not invested anywhere just lying in ON RRP.

Now ON RRP balances have almost 0 ( < 50 billions). So we dont have so called "on the side" money what Wall St is claiming.

But can we talk about the effect of the aggregate of groups of holders? There are two very distinct groups: banks which can create credit and non-banks who can not.

What happens if the latter group sells T-Bills to invest the proceeds in the stock market? Some here argue that the yields rise till there is a balance in attractiveness, but with T-Bills that is only partially true. Because if yields would rise above the FEDs discount rate, a bank would buy the short term T-Bill and then pledge it as collateral for borrowing from the FED and pocket the rate difference. So the effect would be a growth in money supply. Or am I getting this plumbing wrong?

Yuan- the disconnect is in your description of the banks. The bank will not buy a t-bill when the expectation is for the rate to keep going higher, or else they will lose money. For example, if they buy a t-bill for $100 with 5% yield and then the yield goes to 6% the bill’s price will be lower, meaning they must take a loss on their bond holdings. This is what caused Silicon Valley Bank and First Republic to go bankrupt: investors realized their assets were less than the losses on their bonds they bought during ZIRP whose prices were cratering as interest rates rose.

You could argue that these are short term bills so they would just hold to maturity and not have to take a haircut. Sure, but if tons of banks did this, and the short term interest rates stayed flat while long term rates rose, then soon *other* investors would dump their short term bills and move to longer term notes. In economist speak, if the yield curve steepens too much, people will lengthen the maturity of their holdings to get more yield.

Lots of things affect the yield curve, but the Treasury market is so vast that no single player (aside from the Fed and the Treasury Dept) can “force” it to change much by just buying or selling bonds. They would have to be trading in the trillions to even make a dent.

“and it refuses to die” that’s the problem and also the big question. Will this mindset die or will it thrive –

Yep for every buyer there is a seller net gain of zero

Just in case anyone misunderstood.

As I said in my comments “Complete BS”, I was calling the MSM theory BS.

MSM may not be coming here and get educated. My point was to show the contradiction in how MSM reports and Wolf Reports.

Reality is MSM promotes “Money on sidelines” BS so much. e.g. Listen to many CNBC bulls and you will hear it. You wont believe how many people believe that and keep buying stocks at record high prices.

They use sidelines as a pejorative as if all those investors are unhappy with their investment and just waiting to dump it, rather than assuming that every investor in any asset has decided their own risk/reward goals and has chosen the appropriate investment for their goals.

What’s funny is that it’s clear that there’s also money “in the sidelines” in the stock market: people who are nervous about the valuations who would love to get out once other investments (aka bonds) have a high enough yield, which they’re slowly getting to.

It’s just a way to insult bond investors and shame them into moving into the stock market, since stock shills tend to pay CNBC more than bond shills.

Let them make their “money on the sidelines” wishful thinking comedy

All the better for those of us who staring at the line-go-up, waiting for a sanity check in the stock market.

If rates keep dropping but inflation stays where it is or goes higher I think there will be some yield chasing. Earning 3% is 2.25% after tax and losing against inflation. So we could see a portion of this move into stocks. Will it likely move into high risk stocks, no, but I could see it move to dividend stocks with a long history of increasing dividends.

Similarly if the real estate decline picks up and people decide to sell vacant properties, if they still have equity that money needs to go somewhere.

Not saying 3.75% would the line but anything below 3% is kinda pointless to stash money in, although better than a checking account I guess.

Wolf, what is the ratio between people investing mostly in the stock market and those mostly in interest bearing instruments at the moment? Not an easy thing to estimate, but is it high, medium or low as a percentage and has this changed significantly? If 10% are in interest ones instead of only 5% does that really mean much?

Short term CDs flee to where?

The system is awash with liquidity….still. And the Fed seeks a reason to cut….

The dollar index chart doesnt look so good.

rate cuts have nothing to do with liquidity. But QT reduces this liquidity, and the Fed is doing QT.

I thought QT stopped or the balance sheet really couldnt go any lower?

Do you EVER read any articles here? Or do you just goof off in the comments?

So read this article before you comment again:

https://wolfstreet.com/2025/09/04/fed-balance-sheet-qt-39-billion-in-august-2-36-trillion-from-peak-to-6-60-trillion/

My guess would be stable dividend stocks unless the money needs to be used in 12 months or less

In my experience this money is really not interested in risk assets of any kind.

Wealth transfer is probably the most notable things here.

Most of this money won’t directly enter the economy until it’s used by heirs if at all.

Certainly not a bullish indicator for risk now… MAYBE later

You think the rich just stash all their money in money markets to pass down to their heirs? In my experience that’s not how the rich or ultra rich invest

If that’s the case why didn’t people put all their savings in money markets in 2018 and 2019?

Money is in money markets because of yield. If interest rates drop significantly I would expect a large portion of this money (assuming it’s not going to be spent in the next 12 months) to be allocated elsewhere.

Isnt that the idea that Bernanke pushed, that the problem was a world wide surplus of savings (liquidity) which justified rates near 0 or even negative.

The talking heads are forever talking about liquidity but trying to get a handle on what it is and the proper measurement never seems easy.

Most of the money on the sidelines i’ve seen was in San Pedro among sodden sailors.

Wolf, lots of talk about money supply, interest, and inflation. But what really makes up the ‘money supply’? Yes, I know it is the money stock and circulation of that money stock, but what about the Bitcoins, Stable coins, gold, silver, etc. Perhaps the term money supply should be redefined to include these other monies. This might help to explain how much inflation we, in my opinion, are going to get.

Whether it’s CDs or stocks or whatever, it’s almost impossible not to make out like a bandit right now. “Just dump everything into the market” continues to work, for the time being. Friends and coworkers (mostly Millenials and Gen Z) are all banking on the fed put to backstop any material setbacks and keep the bubble going.

God forbid the job market actually begins to fall apart, pretty much everyone expects both a fiscal and monetary response that will send things back to astronomical levels (checks to households, deficit spending, slashing interest rates to zero, etc). BTFD to eternity and beyond.

It all works until it doesn’t. Find me a short ETF that’s a bundle of BNPL services for when it all eventually comes apart.

Yep. And I’m sure when the job market does begin to fall apart, there will be pressure from the media and others for Congress and the Fed to “do something.” The real concern would be losing the confidence of foreigners in the U.S. dollar. If your policy ever time there is a recession is to print your way out of it, why would anyone want to hold dollars?

The COVID response can be dismissed as a one-time thing, but if that becomes a model, I can see the beginning of the end of the reserve currency.

The fed is panicking and cutting with unemployment at 4.3%, still below historical norms and their year end target. I’m skeptical they’ll let unemployment rise…

The COVID response was similar to the financial crisis bailouts. Pretty straightforward Keynesianism. Except Keynes thought there should be high taxes during good times to pay for the bad times bailouts. That part hasn’t been done.

In terms of kind, yes, but not even close in terms of degree.

The amount of “free money” that was handed out during the 2009 ARRA pales in comparison to what was handed out during COVID and after.

People below 50 investing in their retirement accounts won’t be touching it for decades. The momentary behavior of markets is irrelevant.

Zero Hedge has probably cost people more money at this point than any combination of market crashes.

And if we end up with a Japan situation, it could be down for 3 decades.

And they could send the debt to astronomical levels where they talk about managing 50 trillion.

Except the billionaires that own this government (and previous ones) *want* job losses. It keeps their own employees scared and willing to work for less money.

What gets their panties in a bunch is when *assets* decline, since they own most of those assets. So as long as the recession just causes job losses, they’ll be fine. No bailouts necessary. But if the stock market goes down 10%, you’ll see wailing worse than a toddler’s screaming for big daddy govt to bail out these rugged capitalists.

Are there many people who don’t think that the “Fed’s” playbook has already become the de facto backstop for anything bad that could ever happen… …the QE and fiscal response to COVID “worked”… and proved to an entire generation (and maybe me too) that you can have money without working and nothing bad really happens… (except maybe that I never got any money, personally). The business cycle has been repealed and anything that looks contractionary is really just the Fed not doing its’ job.

The Fed is now in the business cycle preventing business….

Sure, it “worked” by confiscating the value of 25% of dollars out there. The real question is whether the bond markets will accept that in the future or start dumping them, causing yields to blow out.

Right now, the bond market believes the COVID was a one-time thing.

Dealing with the bank is such an inconvenience. Then add into how insultingly low the interest rate is on their savings account; I would never keep more than $100k with any bank.

It’s just easier to buy a 6 month bill on Treasury Direct. A few clicks of the mouse & its done.

Cut the middle man out.

Deposit insurance shouldn’t be greater than 100K with the exception of payroll accounts.

Wolf, as always I appreciate your analysis. It helps the financially inept like myself understand these things.

We have a savings account earning 3.8%, which remains shocking to me because the Savings rate at a much larger institution in 3.7% less than that. It has been a long time since I remember those kinds of rates being that relatively high.

Re: “ If the Fed cuts short-term rates aggressively while inflation continues to accelerate, it won’t take long before real yields on MMFs turn negative.”

That’s my focus, in how to plan ahead — in my mind, it’s not a matter of “if”, but rather, how soon — and what to do. Not many choices really …

In a semi-related head scratching situation that adds to my anxiety:

Magnificent 7 market cap: ~$19.95 trillion.

US aprox GDP $31.27 trillion

It’s like the services-based economy is rapidly mutating into an AI economy — that’s happened almost overnight and it’s terrifying imho.

Adjusting a money mkt fund to a new alien world doesn’t seems problematic.

A lot of the energy buildout requires massive loans, so it’s totally confusing as to how this transformation collides with Treasury debt???

It sucks when you are coming to the last of your 4%+ rungs on your ladder and all the new rungs for sale are less than 4%. The payouts end up in MMF which is still paying just over 4%, but I don’t see that lasting much longer. Maybe only until the FOMC meeting.

I do think the reduction in interest paid from CDs and MMF below 4% will have a psychological effect on many “savers” when inflation is running around 3% in the government numbers or higher if you don’t believe the government numbers.

Not sure where those funds will go. I know I will leave some funds in the MMF for emergencies, but I not excited to take risks on overpriced equities or other investments. I am sure there are many other people who are thinking the same thing.

Feeling the squeeze.

Maybe I will try buying some Magic Computer Coins. /s

“Not sure where those funds will go.”

This is forced behavior. You are now supposed to go out and buy the richest PE ratios in history….

There used to be a constructed balance between stock returns and interest bearing securities. Portfolio managers would be certain to have a nice mix of both. Now it is balls to the wall……stocks, and make sure its the Mag 7

The mag7 to me feels like it’s a powder keg waiting to go off. Everyone is convinced that they can just keep growing every year, without regard to the economy around them.

That is doubly true ever since it became a big AI circle-fest.

All it’ll take is a few bad earnings reports and I can see that causing a rush to the door.

I don’t watch a lot of television or streaming. Watched a football game the other day and experientially, it seemed as if every ad for any business touted some form of AI. I don’t know if this is the path of the future or just some gimmick to sucker people. Either way it was like, I get it, you along with every other person has an AI thing that makes you so much better than the competition.

My last two brokered CDs that have matured, I’ve put into 3.8 & 3.6% 3-year, call-protected CDs. I’m not one for trying to predict recessions, but this Sept feels eerily close to what I remember back in Sept 2007.

I’m selling out of small positions in JOBY, ACHR & UEC to take some profits in my IRA. My portfolio is very conservatively positioned for the time being. If the market still has legs, I’m not going to make much money, but I’ve 97% shielded from any sort of market sell off.

My one misstep was selling OKLO & SMR to take some really nice profits back in April as the Trump tariffs approached. These weren’t big positions, so I should have stayed with them. I’ll definitely put money back in them, PLTR and several others, if the market rolls over from a recession.

I wonder when Andruil will go public? That one will be huge.

If you happen to be fortunate enough to not want income… I have to admit I went long on numerous munis a couple of months ago.

Wolf takes issue that people (above) bring up the

fact that even though you have more pieces of toilet paper at year end, you’re really spinning your wheels, maybe even GOING BACKWARD.

“What you should bring up in this discussion is RISK.” In my mind, toilet paper is pretty risky, no matter how big the pile of paper. 🤔🤫

“4%! 4%! Come get your 4%!”

wait till the S&P 500 declines 50% and the Nasdaq 78% as it did during the dotcom bust, and both declined by 50% in 2008-2009. Took the Nasdaq 15 years and lots of money printing to get back to its 2000 high. That’s thinking about “risk.” I’m really worried that so many people are no longer thinking about risk, or have never thought about risk, or think that risk doesn’t exist anymore.

If you think there is no risk in risk-assets, such as stocks, you’re overpaying for them.

That’s also true for people buying non-investment grade bonds at low yields, as you’ve written about recently.

People truly do believe that it’s different now, and that the stock market will never be “let” to decline.

We have taught them well. Just a few more interventions should anything bad happen in the future here….and it will essentially be factual haha. :)

…and, as everyone is suddenly becoming aware, the Magnificent Seven has contributed more to the S&P 500 gains over the last decade than all other 493 stocks in the index combined. And when market concentration like this exists – particularly if driven by a single economic factor (the ‘promise’ of artificial intelligence) it doesn’t take much to upset the apple cart.

I think some folks are conflating risk with opportunity cost.

I.e. you park your $$ in a 1-year Treasury at 4%, but over that year inflation averages 5% and the S&P is up by 8% – in that scenario you’re down 1-4% depending on how you look at it.

Perhaps this is the inflationary mindset: losing a few % to inflation is a greater concern than a double-digit drawdown from a market correction.

As crazy as a 50% drop in S&P sounds, it would only take us to right before COVID in Jan 2020 if I recall correctly. I still DCA into S&P500 and my MMF only goes up due to reinvesting monthly dividends/interest…not adding more since it’s more of an emergency fund thing for me.

What will be most interesting going forward is if we do get more QT like Bessent would like and no more QE. It will be a good day when MBS is $0 on the H.4.1 sheet. Hopefully that happens, but if we get QE again I won’t be surprised.

Is there such a thing as a chart on “excess reserves” held by banks on account at the Fed? (also earning interest)

There used to be “Excess reserves” and “required reserves” back when the Fed imposed a minimum reserve requirement on banks. In 2020, the Fed reduced the reserve requirement to 0%, and so now all reserves are just “reserves” and are combined. It pays interest on all of them.

The chart is current. This article explains the relation between reserves, ON RRPs, and the Fed’s overall balance sheet, and how far QT could go on:

https://wolfstreet.com/2025/02/06/the-feds-qt-could-go-on-for-a-lot-longer-the-tools-are-in-place-incl-the-revived-standing-repo-facility/

This move into short term debt instruments will continue. The Real estate marked is dead, going from a recession into a depression. The stock market is way overvalued and going nowhere from here on. So the only place to park your money is in CDs, MM funds, ST Muni funds, & ST Treasuries. It’s not worth the risk just to get a point or two in extra yield. Only the suckers that follow CNBC and other main stream media outlets are doing that. On the business network, the guest Charlie Gasperino said his UBER driver was asking his advise for a hot tip so he could cash in on the stock market rise. That’s when you know things are topping out.

Another sign of a potential top out is the Treasury blaming the Fed for decades of QE. They might be positioning for hard times ahead. The blame game has started.

It’s a lot like putting all home loan debt into ARMs. As soon as they adjust upwards the whole debt bomb explodes into a series of default and most all of it is severely affected with no choice but much higher interest. That is why you don’t finance long term things ever with short term debt and it looks like the markets and people will have to learn that again the hard way.

Small CDs exchanged for MMMFs increase the supply of loanable funds, but not the supply of new money (a velocity relationship).

The rise to 2.5 percent policy rates in small CDs obviously slowed N-gDp.

Loans/investments = deposits. An increase in interest bearing deposits depletes noninterest bearing deposits dollar for dollar. C-19 increased DDs relative to TDs. It’s simple stock vs. flow. It raised N-gDp. It has raised interest rates.

Personal Saving Rate (PSAVERT) is @ 4.4%. Savings are insufficient to hold rates down.

Yes, though I’m not sure what the rate would have to be to hold down long-term bond yields. Might have to be astronomical. Because… personal savings = total consumer income (everything from wages to rental and farm income) minus total consumer spending. So its income that was not spent on consumer goods and services. But it doesn’t mean that amount was put into a savings account or other bank account or bonds. Much of the “savings” is put into the principal portion of mortgage payments, into 401ks, into other retirement accounts, stocks in brokerage accounts, cryptos etc. and that portion is not readily available for spending (which is what money supply tries to measure), and is also not available to buy longer-term bonds.

MW: Why the Fed’s first rate cut in 9 months could derail the stock-market rally — and how investors can prepare

MW: Fed governor Cook reportedly declared second residence as vacation home, contrary to Trump claim

I’m getting 3.95% on my 1 year CDs at my local credit union. Why should I jump into that casino on Wall Street which is corrupt from top to bottom just to try to make a quick buck. Same goes for corrupt banks like Wells Fargo, BOA, Citicorp, Chase etc.

Speaking of making interest on your money, how’s this – a major website just released a story saying that an Investopedia study recently released says that in 2025, the American Dream’ costs $5.04 million, up from

$4.4 million last year and $3.4 million in 2023!

So, the cost of the ‘American Dream’ has gone up just over 48% in two years, according to Investopedia.

Crazy! Where can I find returns like that?

Are we all toast? Wolf?

Where can you buy the “American Dream?” Since when are they selling dreams? Is that a new meme? Like selling farts once was? Is it on the blockchain and AI powered?

Coffees are the new eggs — U.S. consumers paid nearly 21% more for coffee in August than a year earlier, a significant jump that is the largest annual increase since 1997.

Coffee is an excellent example of corporations not eating tariffs, but instead, passing the tariff tax directly to consumers — who are also watching monthly income from money mkts decline.

“Coffee is an excellent example of corporations not eating tariffs…”

Goofball. Coffee prices have been spiking for FOUR years. Since January 2020, the CPI for coffee has spiked by 46%. You just slept through it, and now you wake up?

Commodity prices of coffee spiked by 300% from late 2020 through February 2025, before tariffs were even in effect. I cannot believe this anti-tariff bullshit people concoct.

https://wolfstreet.com/2025/09/11/cpi-inflation-dishes-up-another-nasty-surprise-as-it-tends-to-do/

Just make your coffee at home, it’ll cost a fraction of what it does from Dunks or Starbucks.

Even buying Dunks beans at the grocery store, a pot of coffee costs me <$1.

I used to get takeout coffee every day; with brewing at home it now costs less than it ever has in my life.

Small sample but my personal experience.

Starbucks 12oz ground package….from 8.99 to 14.99 in one week

Checked the other brands and there were similar price hikes.

Is this an example of inventory run out and tariffs kicking in on prices of new supply? Will we see this throughout the economy?

The cost of tariffs is $0.45 per pound currently — see my comment below. The rest is Corporate America eating your lunch and the four-year-long price spike of commodity coffee: the cost of a pound of green coffee beans more than quadrupled, from $0.95 in 2020 to $4.25 now.

” Corporate America eating your lunch”

Still should show up in CPI and PCE numbers regardless

Record Corn and Soybean crops should bring beef prices down in a few months……

“Corporate American is eating your lunch” is for sure is showing up in CPI, which is why I gave you the CPI for coffee in a chart (see above and in my CPI articles).

Last week I paid $21 for a 40oz bag of whole bean Pike Place Roast at BJs.

Ouch!

Re: “Commodity prices of coffee spiked by 300% from late 2020 through February 2025”

Perhaps, while enjoying an expensive cup of coffee, we can mutually conclude that tariffs won’t be helpful in lowering the price of a mocha next year? I further assume the cost of a future mocha will nudge consumer sentiment lower, but maybe everyone is content?

over 90% of the price of the mocha purchased in a cafe is non-import related and not tariffed. You’re paying for the cost of roasting, packaging, distribution, profits everywhere, executive compensation packages, executive pension plans, health insurance, wages all the way along, transportation, rents, property insurance, toilet paper, etc., all in the US. Only the cost of the green coffee beans imported in bulk by the roasters is tariffed. And that may only about to $0.03 to $0.06 per cup, see below.

Only Brazilian coffee is tariffed by 50%. No US drinker needs Brazilian coffee, let Brazil sell it to other countries. Coffee is grown in 70 countries, including in Latin America, Africa, and Southeast Asia, and even in the US (Hawaii, California, and Puerto Rico).

Tariffs on Colombian coffee are only 10% on the cost of imported green coffee beans. If a pound of green coffee beans costs $4.25, tariffs would add $0.42 to the cost. But you’re paying maybe $10 a pound when you buy at a Safeway, and most of that goes to Safeway. You might get 15-30 cups out of a pound of coffee, so the cost of tariffs would be about $0.03 to $0.06 per cup, IF the tariffs get pass on.

People need to quit spreading stupid BS about tariffs here.

I just received 120 Kirkland coffee pods from Amazon. $70. About .58 a 14 oz cup. It was $6 more than the previous order.

My favorite coffee was large cup from McDonald’s for a $1.

How much is that now? Anybody know?

Kirkland whole bean 3 lbs. Colombian Supremo $19.99 walk-in (I didn’t check online).

With pods, you just get ripped off.

Does it matter if it was tariffs or just more coorporate greed if I have to pay more for the things I need.

The last thing America needs is more money for their goverment to waste.

There are endless places to park cash. Why would anyone loan it at 4-5 percent and pray to break even?

Every one of those trillions of dollars is a low-stakes bet that the return on short term debt will turn out to be higher than other assets like stocks.