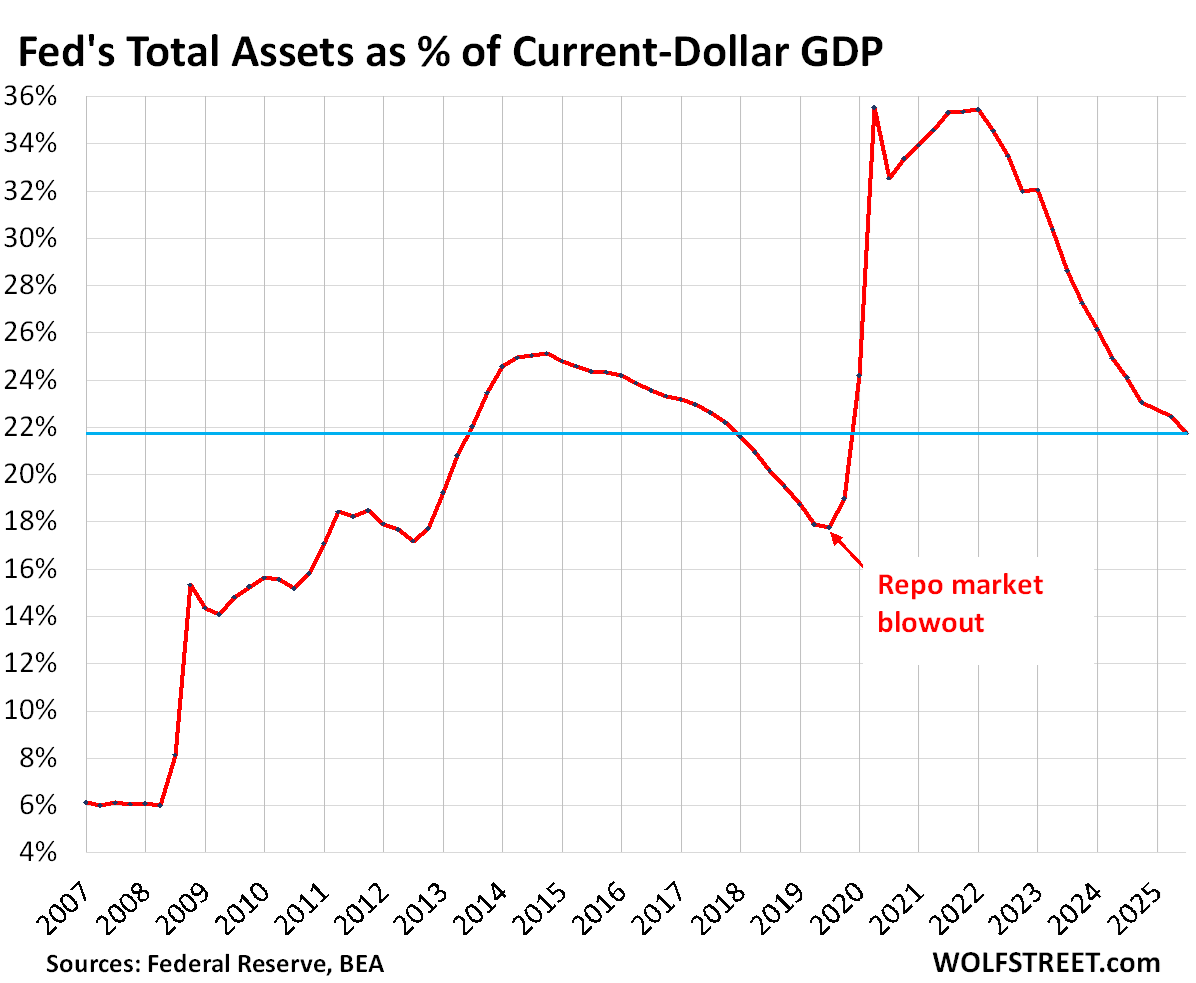

Compared to the size of the economy, the Fed’s assets are now down to 21.8% of GDP, where they’d first been in 2013.

By Wolf Richter for WOLF STREET.

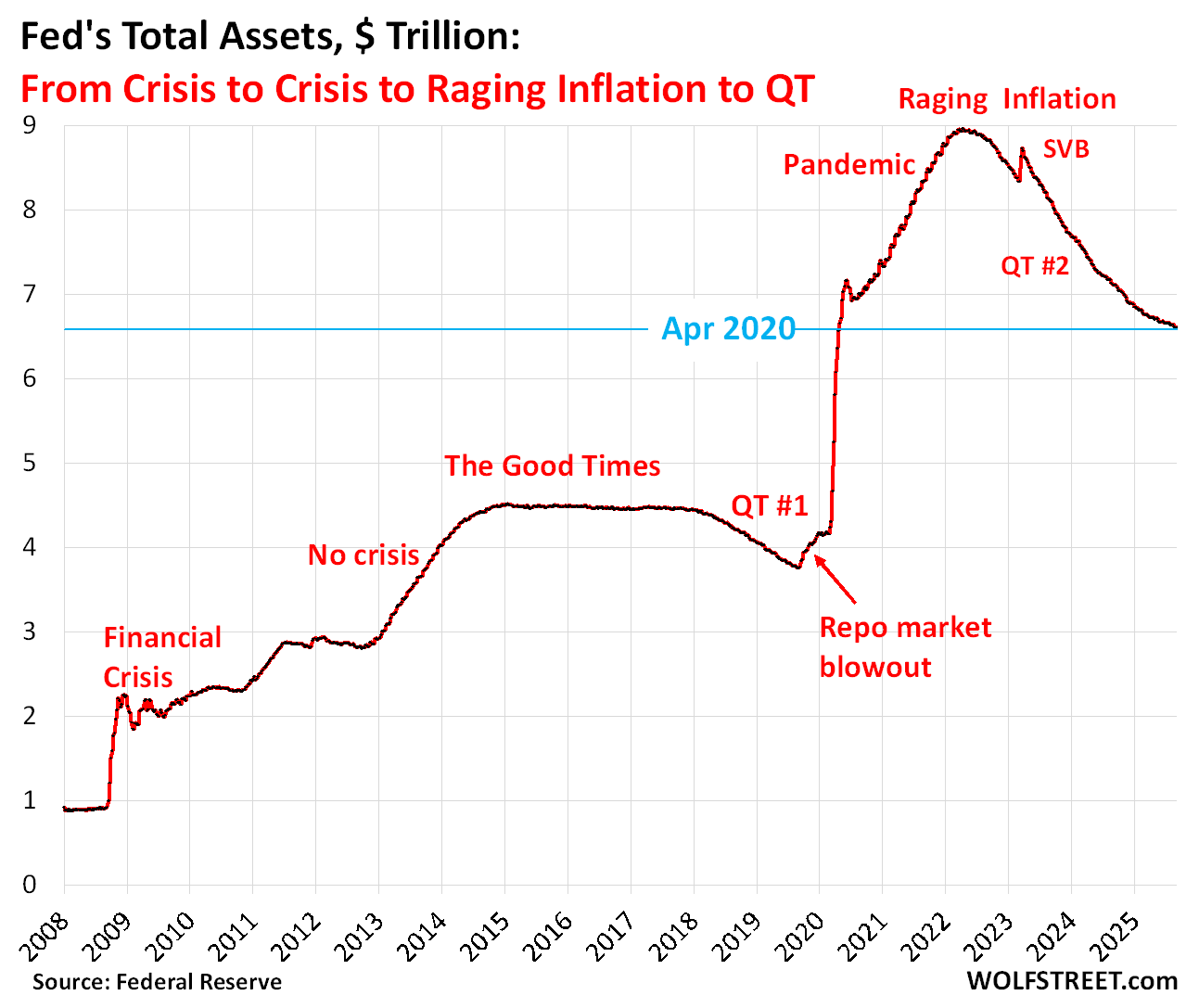

Total assets on the Fed’s balance sheet dropped by $39 billion in August, to $6.60 trillion, the lowest since April 2020, according to the Fed’s weekly balance sheet today.

Since peak-balance sheet in April 2022, the Fed’s QT has shed $2.36 trillion, or 26.4% of its total assets.

In terms of the Pandemic-era QE, the Fed has shed 49.2% of the $4.81 trillion in assets it had piled on from March 2020 through April 2022.

QT assets.

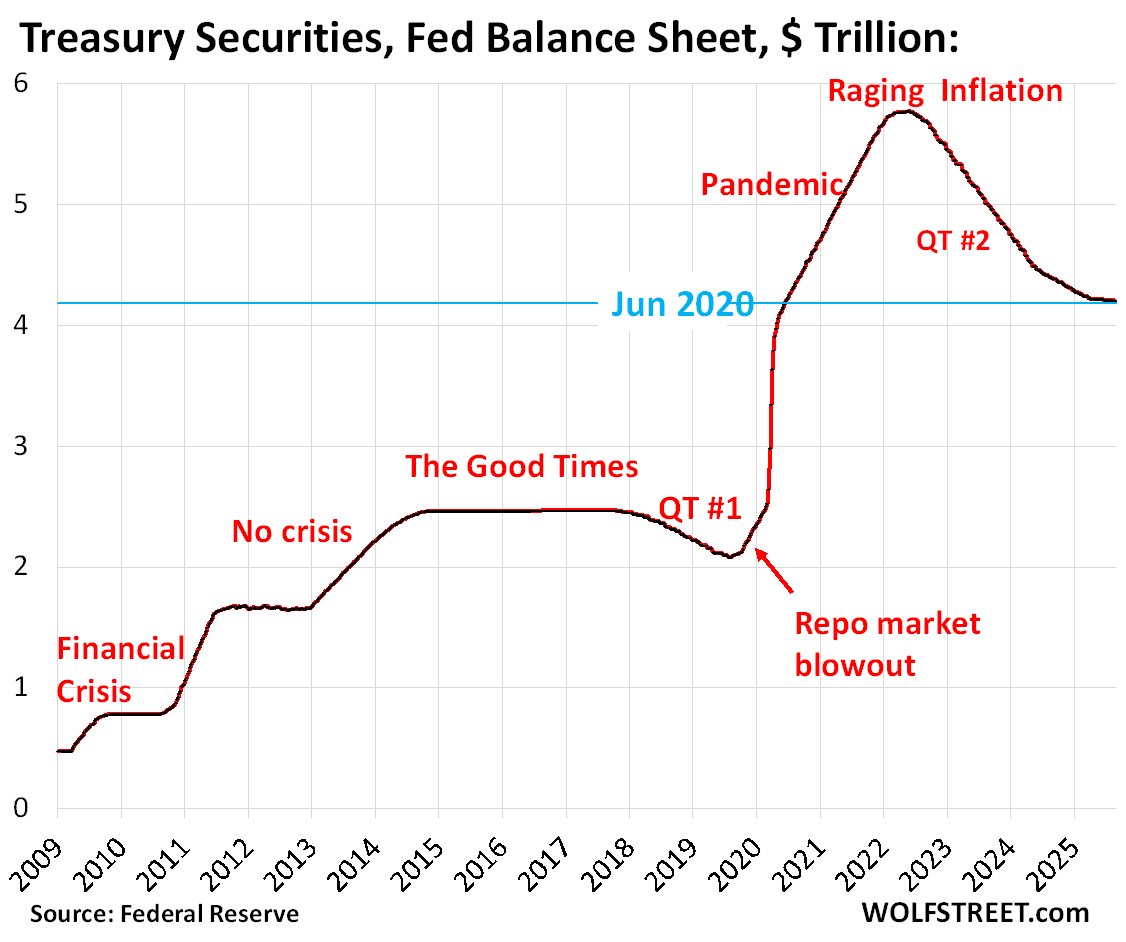

Treasury securities: -$3.7 billion in August, -$1.57 trillion from peak in June 2022 (-27.2%), to $4.20 trillion, the lowest since June 2020.

During pandemic QE, the Fed had piled on $3.27 trillion in Treasury securities. It has now shed 48.1% of that.

The $3.7 billion decline was in line with the reduced pace of QT for Treasuries of $5 billion a month. The difference was the inflation protection the Fed earned on its holdings of Treasury Inflation Protected Securities (TIPS), which is added to the principal of the TIPS, instead of being paid in cash.

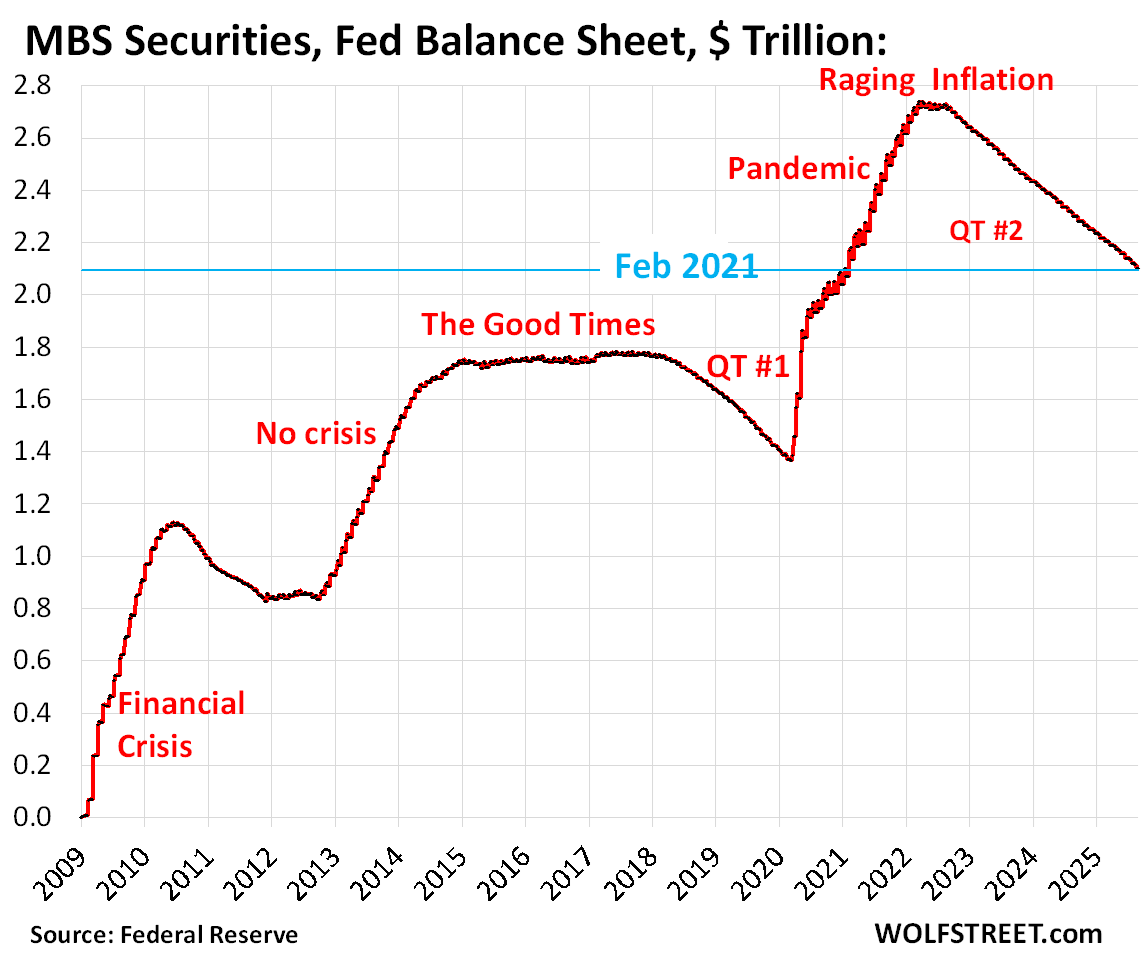

Mortgage-Backed Securities (MBS): -$17.8 billion in August, -$637 billion from the peak, to $2.10 trillion, where they’d first been in February 2021.

The Fed has shed 23% of its MBS since the peak in April 2022, and 46% of the $1.37 trillion in MBS that it had added during pandemic QE.

The Fed holds only “agency” MBS that are guaranteed by the government (issued by Fannie Mae, Freddie Mac, Ginnie Mae), where the taxpayer would eat the losses when borrowers default on mortgages.

MBS come off the balance sheet primarily via pass-through principal payments that holders receive when mortgages are paid off (mortgaged homes are sold, mortgages are refinanced) and as mortgage payments are made. But sales of existing homes have plunged and mortgage refinancing has collapsed, and far fewer mortgages got paid off, and passthrough principal payments to MBS holders have slowed to a trickle.

This plunge in sales of existing homes and in mortgage payoffs just finished its third year.

As a result, ever since QT started, MBS have come off the Fed’s balance sheet at a pace that has been mostly in the range of $15-19 billion a month.

The MBS runoff is not capped, whatever comes off comes off and goodbye. But that’s all that the mortgage market has delivered over the past three years.

If pass-through principal payments become a torrent again during a refi boom, the MBS balance drops by the entire amount of the pass-through principal payments, but any amount above $35 billion a month would be replaced with Treasury securities, according to the Fed’s revised formula. In that case, QT from MBS and Treasuries combined would reach $40 billion a month under the current QT regime.

Bank liquidity facilities:

There was little activity in August. The Fed has been pushing banks to practice using these facilities with “small value exercises,” or at least get set up to use them and pre-position collateral – which apparently quite a few banks have not yet done – so that they could use them quickly.

- Central Bank Liquidity Swaps ($0.0 billion)

- Standing Repo Facility, or SRF ($0.0 billion).

- Discount Window: $4.4 billion, down by $482 million from a month ago. During the SVB panic, the balance had spiked to $153 billion.

Fed’s balance sheet compared to the size of the economy. The Fed-assets-to-GDP ratio fell to 21.8%, the lowest since Q4 2019, and back where it had first been in Q3 2013 (total assets divided by “current dollar” Q2 GDP).

What else contributed to the $39 billion decline in assets?

The balance sheet declined in total by $39 billion in August. But Treasury securities declined by only $3.7 billion, MBS by $17.8 billion, and the Discount Window by $0.5 billion, for a combined decline of $22 billion.

Another $17 billion of the $39 billion decline came from declines in these three accounts:

Leftover pandemic loan programs declined by $221 million. The two remaining accounts are the PPP liquidity facility and the MSLP, that continue to wind down gradually. Combined, their remaining balance is down to $5.7 billion.

“Other assets” fell by $14.6 billion. This consisted mostly of accrued interest from bond holdings that the Fed had set up as a receivable (an asset) previously, and that it was paid in August. When the Fed receives interest payments, it destroys that money and it comes off the balance sheet, and the account declines by that amount (the Fed doesn’t have a “cash” account, like companies do; it creates money when it pays for something and destroys money when it gets paid).

This account also includes “bank premises,” which have been in the news recently, and other accounts receivables and will always have some balance.

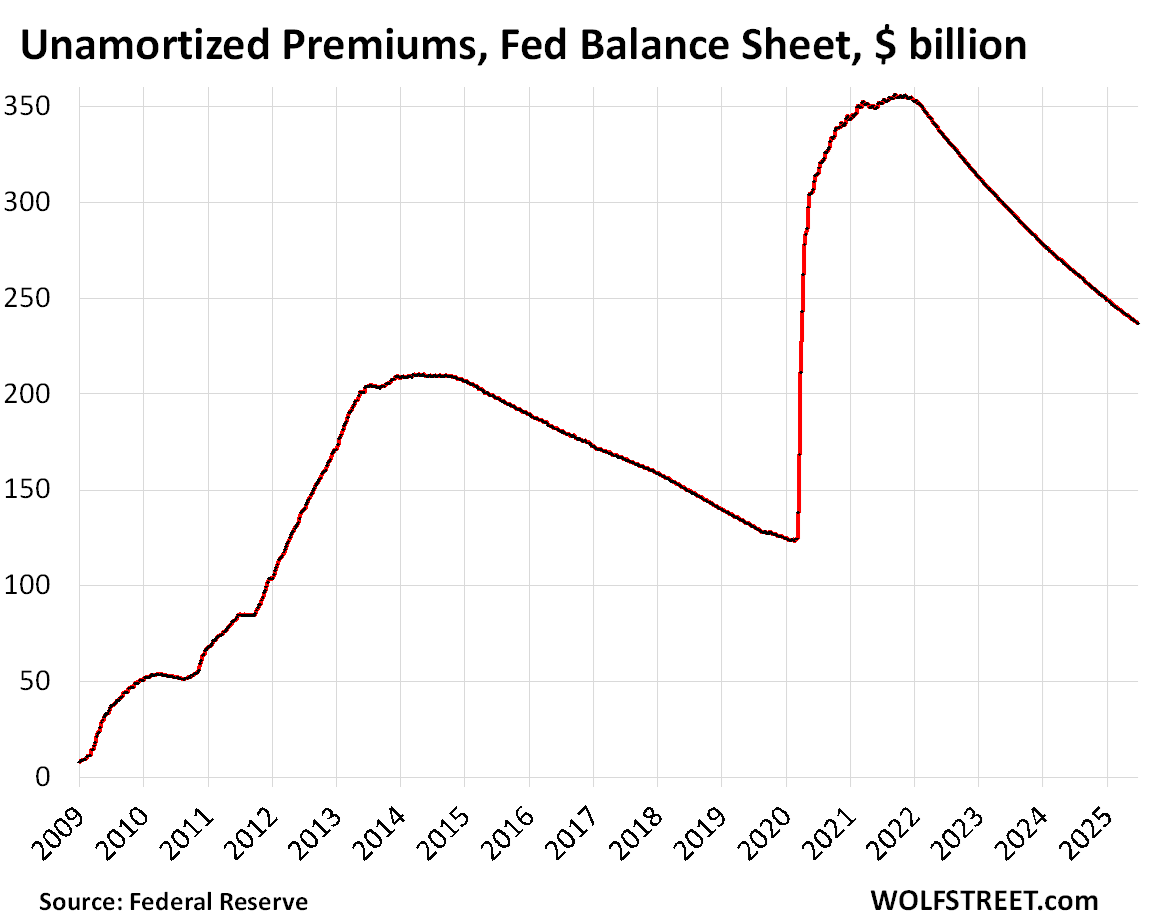

“Unamortized premiums” fell by $1.9 billion. These are regular accounting entries with which the Fed writes off the premium over face value it had to pay for bonds during QE that had been issued earlier with higher coupon interest rates and that had gained value as yields dropped before the Fed bought them. Like all institutional bondholders, the Fed amortizes that premium over the life of the bond. The remaining balance of unamortized premiums is down to $232 billion, from $356 billion at the peak in November 2021:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf – very helpful. Particularly this at the end:

“Other assets” fell by $14.6 billion. This consisted mostly of accrued interest from bond holdings that the Fed had set up as a receivable (an asset) previously, and that it was paid in August. When the Fed receives interest payments, it destroys that money and it comes off the balance sheet, and the account declines by that amount (the Fed doesn’t have a “cash” account, like companies do; it creates money when it pays for something and destroys money when it gets paid).”

I have always wondered what happened to the money the Fed receives on interest payments and repayment of principle on its government securities portfolio. “Poof“ it just disappears. This makes sense, but it’s difficult for we normal folks to understand.

Thank you

Wolf,

Thank you for those timely updates.

$39 Billion was good surprise. Was expecting around $20-22 Billion.

Even with slow QT (assuming they continue beyond May 2026), FED should be on path to healthy balance sheet.

ON RRPs almost vanished. Soon I think liquidity will start come off from Reserves.

On MBS balances, I am thinking even if Home Owners dont sell, the roll off amounts will increase. As time passes, interest components will be lower and higher amounts will go to Principal. So FED will be paid higher. It will be very slow and gradual. But still over period, it will be significant.

IF FED starts selling MBS then thats different story.

Logically I don’t dispute the point being made here about it ramping up over time. However, two counter thoughts.

1 as a pandemic mortgage holder myself. When looking at an amortization table at the time. Roughly a year into the loan I would already pay more against the principle than the interest. So I wonder if that effect would even by all that pronounced at this point. Especially as we get further down the track with other loans taking place recently if this principal pay down is becoming a bit muted.

2 With all the Helocs and home equity seconds for pandemic of loan holders in general that could also be masking the principle pay down effect.

3. If 10 year and prime rates press lower it could really be an synergistic way to wind down MBS quickly. I suspect that is why the current administration is really pressing the fed to lower rates(in order to force the fed to buy treasuries from MBS runoff over the monthly cap.)

I understand pandemic mortgage have much lower rates. They are already 3-4 years old. Even with lower rates, principle will keep going up. It will be minor amounts but still it will have snowball effect over few years.

FED stopped buying MBS now. Yes, there could be some masking effects but again my point was :EVEN IF” current Owners dont sell. MSM keep telling how people are locked in and all. Lot of MSM BS. Sure. There is incentive. But usually People’s life/situation changes in 7-8 years. They sell and move on. Very limited people settle and keep staying in same place for very long time.

It will take some time for FED to get out of MBS unless they sell. When long term rates already under pressure, now if FED starts offloading MBS, it will further shoot up Mortgage rates.

I really doubt current Administration is really aware of what they are thinking and strategy. Pushing FED to drop rates is only going to have boomerang effect. We already saw it with last 100 BP cuts. Long term rates including Mortgage went up 100 BP.

Rein-in inflation and bringing down debt are sure ways to bring down long term rates. QE can do it. But it will just push the problem to future with much worst effects.

Haven’t you heard? Bessent says we’re in a housing emergency. I’m thinking the next shoe to drop is an increase in the cap gains exemption…maybe up to $1,000,000.

Bessent was talking about how to add new housing supply (ease constraints to build new homes, remove tariffs on construction materials, etc.), and lowering transaction costs and fees. It was all about adding more new supply to bring costs for buyers down.

Waiono, somehow every “emergency” results in a giveaway to teh rich.

“Waiono, somehow every “emergency” results in a giveaway to teh rich.”

exactly. I put nothing past Trump.

Out of curiosity, leading into the GFC, who were the primary original consumers of subprime loans that lenders eventually wrapped into MBSs for Fanny and Freddy?

I must admit as an extreme skeptic of the Fed generally, these GDP adjusted figures are very encouraging, we are well on the way to more normal monetary policy.

But Congress simply must act to preclude the Fed from future QE, and explicitly banning MBS purchase by the Fed, or at the very least, limiting QE in GDP terms to less than 10% of GDP, otherwise the Fed will simply replay this stupid playbook the next time a recession occurs, which is inevitable.

Ok, Happy 1 gets my vote for Comment of the Day. Well stated!

P.S. While my heart and head hopes and prays that Congress gets responsible thus precluding the need for future Fed QE and replaying this stupid playbook, the skeptic in me assumes that Congress won’t. When push come to shove, Congress won’t act until a crisis is upon us and then, it’ll be money printing and QE time again at the Fed. Besides, what’s politics for if not for the brinkmanship?

“Congress simply must act to preclude the Fed from future QE”

Doesn’t this violate the principle of Fed independence? Not that I’m a fan of QE but…

Fed gets its directives from congress, its independents is how it chooses to enact policy to support said directives. This has always been the way.

Fed independence is a myth. Show me the Fed Chairman since Clinton that wasn’t the evil spawn of Wall St.

Fed is independent and free in the sense of setting monetary policy within the boundaries of their mandate and the law. Congress writes the law. The recent discussions on fed independence relates to the public and private pressure excerted by the executive branch on the monetary policy itself. Trump isn’t interested in laws, he’s interested in strong-arming his (perceived) opponents into doing what (he thinks) benefits him.

After decades of enabling bad behavior and white collar crime, The Fed is “trying” to do the right thing. LMFAO.

No surprise the price of gold is exploding. As the saying goes “Full Faith and Credit”

Interesting times.

How is the price of gold different from any of the other laughably absurd and inane speculative bubbles?

With each “emergency” the Fed becomes more of a factor, more powerful.

Before 2009 the balance sheet was well below 10% of GDP, now it is roughly twice as large at 21%.

All of this goes to show that the current asset bubble has nothing to do with the Fed balance sheet or with M2 or whatever people say. It is pure mania, driven by future expectations of what the government (Congress and the Fed) will do, not what they’re currently doing.

Gold and silver prices are telling you something here. Listen to them.

What they are telling you and everyone is that they are in a manic bubble.

Lol, very few people except perennial gold bugs listen to the precious metals.

Gold is in the bubble bath with AI stocks and shtcoins.

Assuming constant MBS roll-offs of $15-19 billion per month, that gives an estimated range of 11.5 to 9 years, respectively before the Fed no longer holds any MBS.

It’ll likely be sooner based on what Wolf writes about if more homeowners refinance or take out mortgages relative to current rates of doing so. I don’t know how to feel about this other than I’m glad the Fed is removing MBS from its balance sheet.

Glad we are exiting this unprecedented charade.

“Mortgage-Backed Securities (MBS): -$17.8 billion in August, -$637 billion from the peak, to $2.10 trillion, where they’d first been in February 2021.”

Looks like March or April when the MBS balance will finally fall below $2T. That will be nice from a psychological standpoint. As you’ve written about many times here the housing market is severely broken and will take a long time to heal without more Fed meddling.

When will the stock market feel the pinch of lower liquidity? It was said that ample liquidity from the QE has pumped up the market since 2013. Now that the balance sheet has retreated to 2013 level in terms of percentage of nominal GDP, the over valued stock market, real estate market, and gold should come down a bit, right?

Wolf. Yesterday at 10:40 am you answered a question and commented on how to get long term rates down. I thought your answer was perfect. You questioned how moronic long term bond investors accept such low rates today.

I cannot fathom extending a bank investment portfolio in these times. The politicians and CRE players all begging for lower interest rates in a self serving analysis. But for the country?

Anyway, looking at market reaction to today’s jobs report does suggest economy is slowing, and bond investors recognize that a FED FUNDS rate cut is coming, but this will only add gas to the inflation fire.

Can you do your best to explain why people buying 10 year bond (or extending duration) with this inflation?

If I had to guess, I’d say investors believe that a slowing economy will cause inflation to go away, and thus, the 10 year at 4.08% or whatever it is now will be more appealing.

I don’t think they’re considering either a) the possibility that this jobs report is not that bad, and thus won’t really slow inflation, or b) that the jobs market is getting bad, but that inflation will persist anyway (stagflation). There’s probably a c) I’m not considering.

Yep. Stagflation is real. Why does FED want negative real interest rates again and again?

Classically, you have to choose where to put your money that gives the greatest yield (regardless of inflation). You can choose stocks, which average 10%/yr but have a large variation and often goes negative. You can choose bonds, which average 5% and have less variation and rarely go negative. You can choose t-bills, which average 3-4% and are even less variable. Or you can choose hard cash which always gives 0%.

There is almost never any reason to choose cash among these, unless you absolutely positively can’t lose the money (but you’ll still lose value from inflation). There are only a very few periods of time when short-term bonds outperform long-term, namely 1967-1969, 1972-1975, 1978-1982, 2004-2006 and 2021-2024, all periods of sudden large increases in the Fed Funds rate.

Side note: inflation alone doesn’t do this, as you can see if you look at the WW2 years when there was a burst of inflation, but there was no increase in 10-year treasury yield, because the Fed actually capped interest rates by buying a lot of Treasuries (sound familiar?). By 1947, the Fed owned 90% of all t-bills!

When the economy looks like it’s about to struggle, people guess that stock returns will turn negative and then choose bonds/t-bills instead because at least they will give positive returns, unlike cash which gives 0%.

Countrybanker

I don’t understand why anyone buys cryptos except to sell to the bigger fool later for more money. Bonds, stocks, all this stuff now trades on that basis. Long-term bonds gain value when long-term yields drop. So you can look at it as a crypto-like bet to sell those bonds at lower yields and higher prices to a greater fool down the road. And hedge funds can turn this into a leveraged bet that can make or lose lots of money. That’s my story, and I’m sticking to it.

There is still way too much liquidity out there, and until that gets burned off, rational fundamental thinking is just not taking place.

“And hedge funds can turn this into a leveraged bet that can make or lose lots of money. That’s my story, and I’m sticking to it.”

Essentially that was the point of my derivatives post that vanished. Wall St. has fought against regulating derivatives since Clinton was Pres and every Pres since has followed the same script.

You may be right, and this might be an explanation for the fact that an inverted yield curve didn’t lead to recession this time. If hedge funds and/or other investors can develop a leveraged bet that distorts the signal that bond yields usually give, then there’s no need for them to demand more yield for longer terms (as is traditionally the case).

Shouldn’t the supposed genius fund managers/investors recognize that no one individual monthly report ever tells us all that much?

Aren’t there always revisions on these after the fact anyhow (in either direction, independent of the party in power?)

Wouldn’t taking a breath, and looking for the trend over time be more useful?

Shouldn’t we really be asking why these blips of data move the markets as much as they do? Isn’t that an indictment of the investor class that they are constantly reacting to minutia and not doing a deep dive on fundamentals of the stocks they are buying?

These numbers here are not from some kind of survey but are figures from the Fed’s balance sheet, they’re accounting figures, and not estimates, and they do NOT get revised. RTGDFA before you post BS.

Why is the fact that the Fed’s bs is “only” 21% of GDP good news? It was less than 10% before fin crisis when QE became a solution for a problem it wasn’t meant for.

Why don’t more people question why the Fed still own over $6.5 TRILLION in bond securities or the fact that they are sitting on over $1 trillion on mkt to mkt losses still today on that portfolio that much of was bought at historically low yields – next time don’t do that since it played a major role in the inflation that these supposed experts thought was temporary.

It’s basic Econ 101 that if you increase M2 by nearly 40% in two years time in the world’s largest economy, you’re going to create inflation.

Let’s avoid that mistake again as we head into another recession in the year ahead – yes lower rates, hopefully not below 2%, but enough of excessive money printing, which I guess gold is also telling mkt.

You are so absolutely right, Brad. No way we should have BS where it is. No reason why it shouldn’t be back at pre-emergency (Covid) levels (which were still unjustifiably high) except that the top 0.1% can enjoy excessively inflated assets.

Use real GDP, not nominal.

There are two options:

1. nominal balance sheet divided by nominal GDP.

2. inflation-adjusted balance sheet divided by inflation-adjusted (“real”) GDP.

They both will produce exactly the same ratio. Duh.

I use #1 because that’s the standard way that everyone uses.

Only obliterating idiots divide a nominal dollar figure by an inflation-adjusted dollar figure.

When it’s $6.6 Trillion, $39B is chump change.

Coffee shop money.

As one poster said above, Bessent said that a housing emergency may be declared. Wolf, do you have a couple extra bunks to take in a couple of homeless from the San Fran streets?

“Wolf, is my breakfast ready!?” 😂😂😂😂😂

Not to worry – you’ll get a monthly stipend of $500 per bunk mate.