Food prices also spiked. Energy prices surged due to diesel, jet fuel, and industrial electric power. Ugly all around.

By Wolf Richter for WOLF STREET.

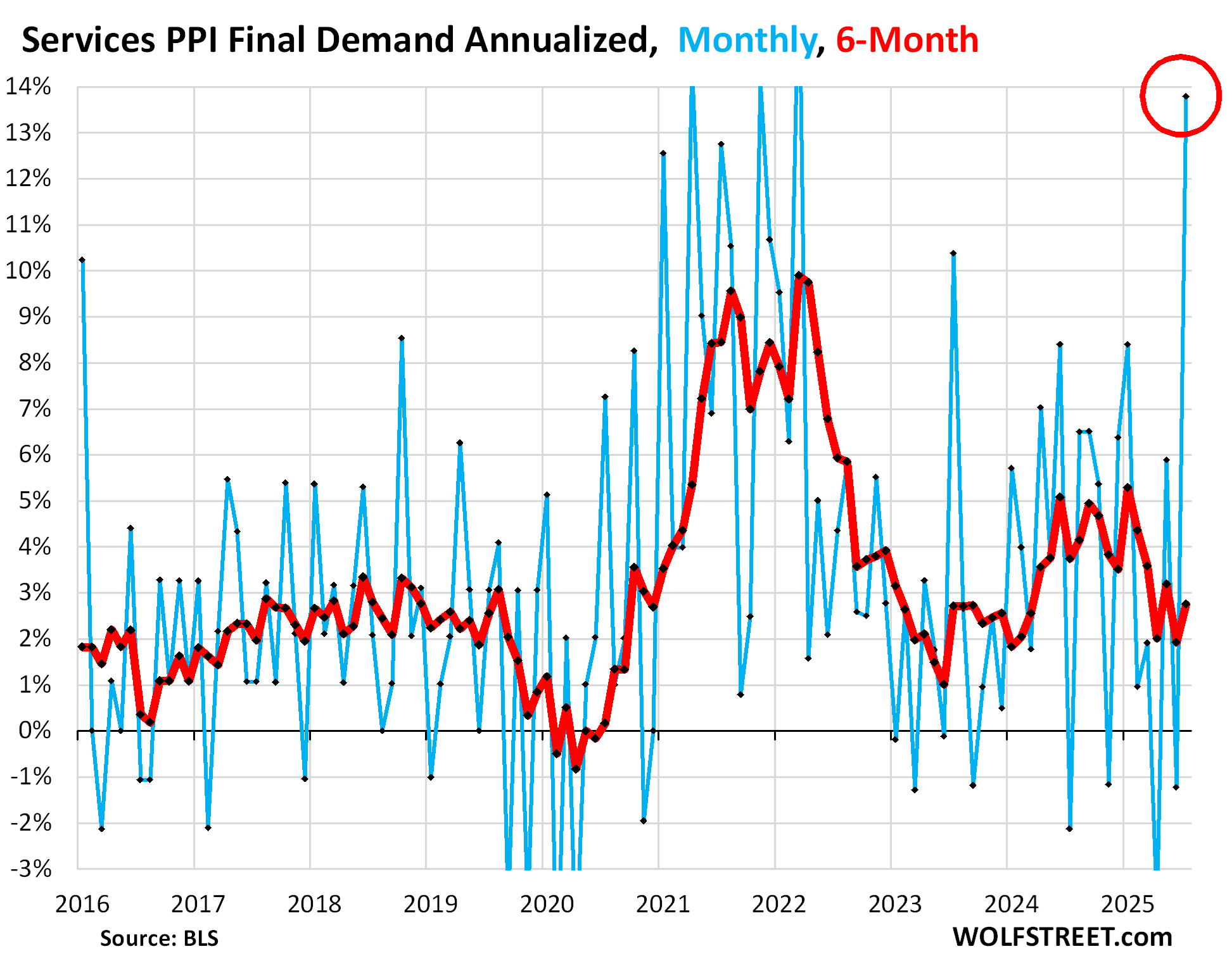

In another inflation shocker – services again! – the Producer Price Index Final Demand for Services exploded by 1.08% in July from June (+13.8% annualized!), the worst since March 2022 when inflation was peaking (blue in the chart). It was broad based: Prices for services less trade, transportation, and warehousing spiked by 0.69% (8.6% annualized), while prices for transportation and warehousing services spiked by 1.01% (12.8% annualized).

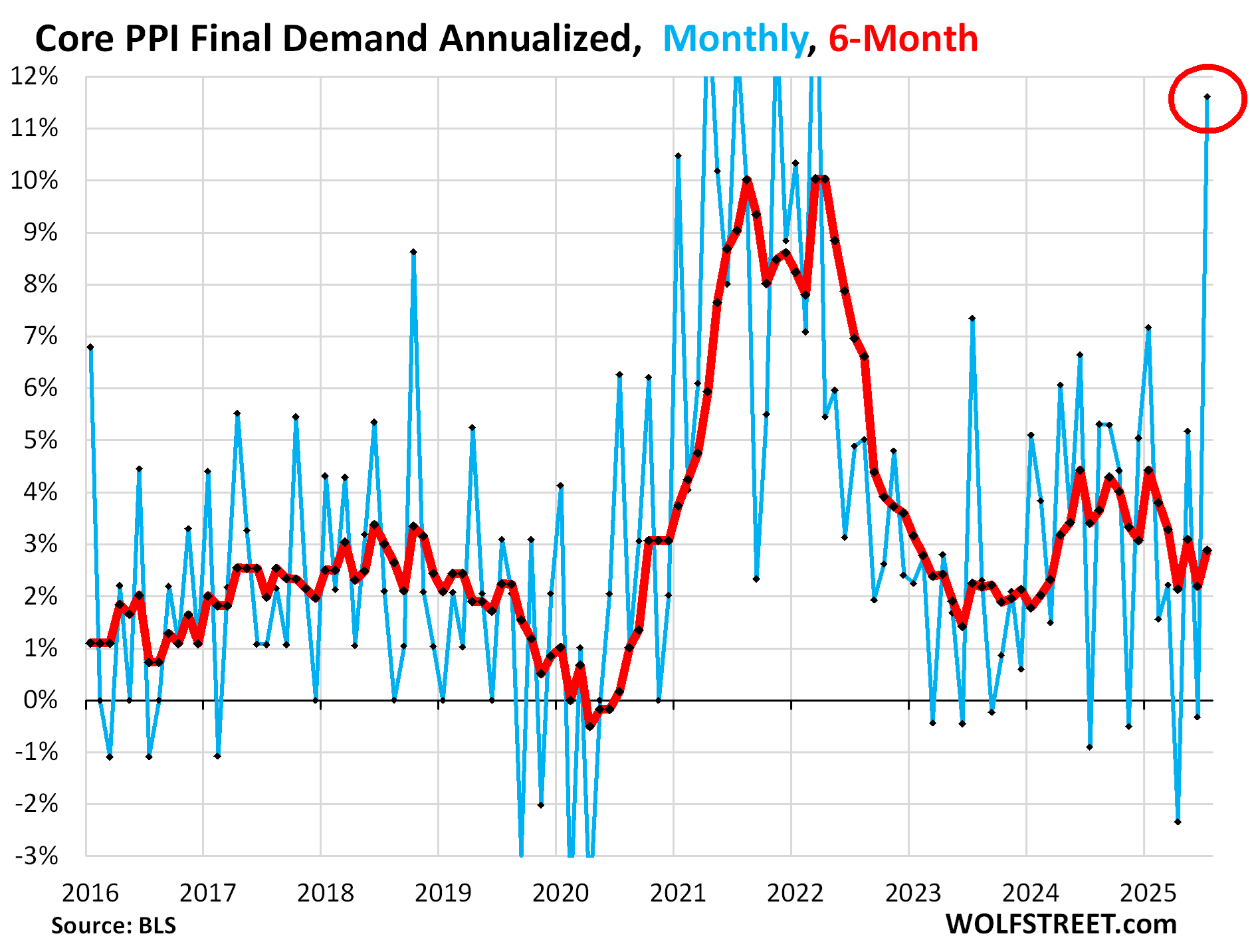

This explosion in services prices caused the “core” PPI Final Demand, which excludes food and energy, to spike by 0.92% month-to-month (+11.6% annualized), the worst since March 2022. And it caused the overall PPI Final Demand to spike by 0.94% (+11.9% annualized), the worst since March 2022, with food prices and energy prices also surging.

The six-month average of core Services PPI, which irons out some of the huge month-to-month zigzags, but also then lags sudden U-turns, accelerated to +2.8% annualized (red in the chart).

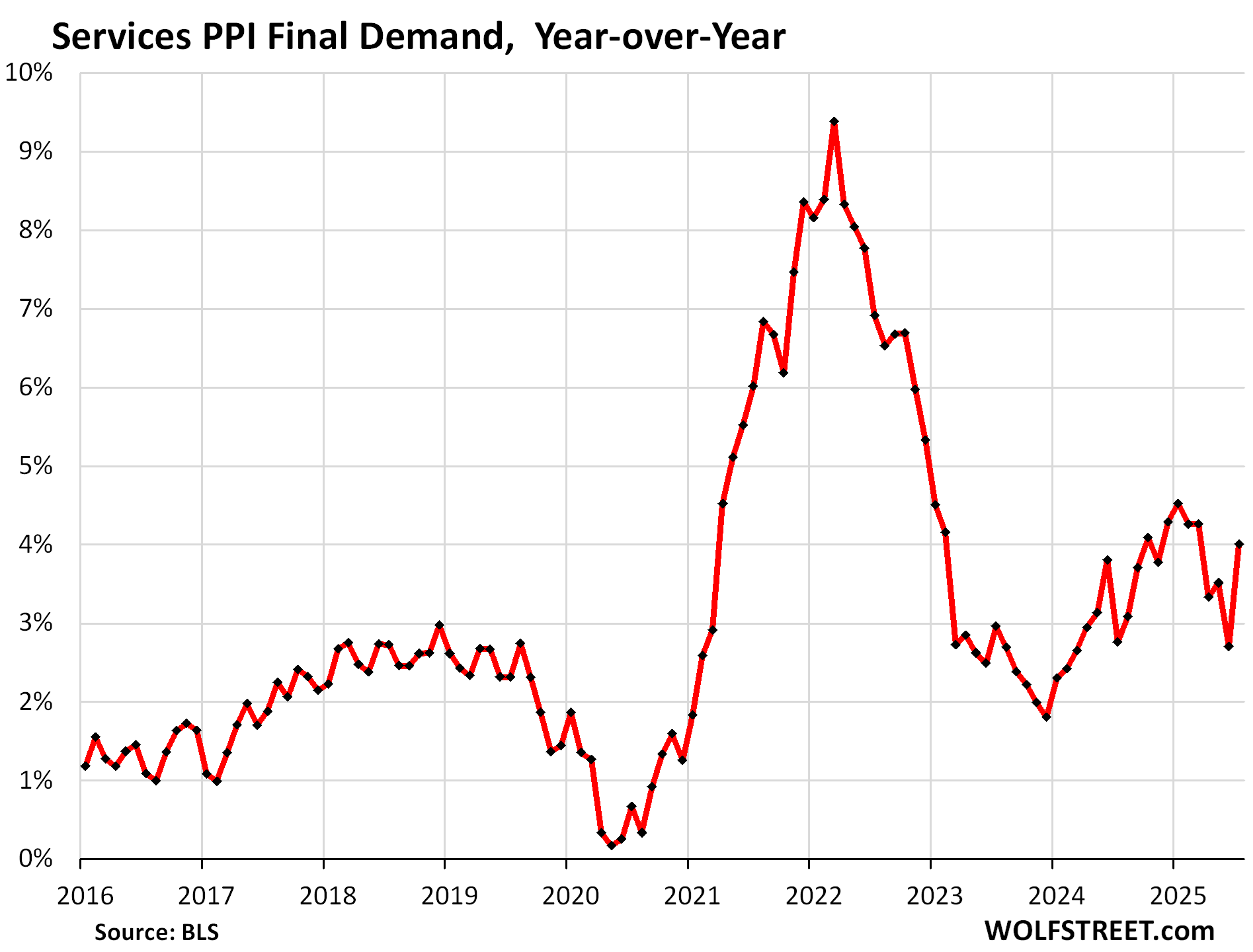

Year-over-year, the core services PPI jumped by 4.0%, a steep acceleration.

Where the new tariffs fit in.

The PPI does not track import prices, and therefore doesn’t directly track the costs of tariffs that companies are paying on imported goods. It tracks prices that companies charge each other, including export prices, and so indirectly, it tracks how companies eat the tariffs or pass them to other companies.

Companies have been paying the tariffs – $28 billion of them in July alone. In their earnings warnings and quarterly reports, consumer-goods companies, such as automakers across the board and companies such as Nike, have already disclosed how much those tariffs are costing them as they have trouble passing them on to consumers because additional price increases would cause sales to fall.

For them, the problem is that they’d already jacked up prices into the sky in 2020 through mid-2022, leading to an extraordinary historic profit explosion. And now they’ve hit consumer resistance.

The tariffs are percolating through the prices that companies charge each other, but have shown up only in small increments in consumer prices, totally overpowered by the renewed surge of inflation in services, which are not tariffed, which often have little price competition, and where consumers do most of their spending. It’s services inflation at the consumer level that is so hard for the Fed to contain, which is why the Fed fears services inflation so much.

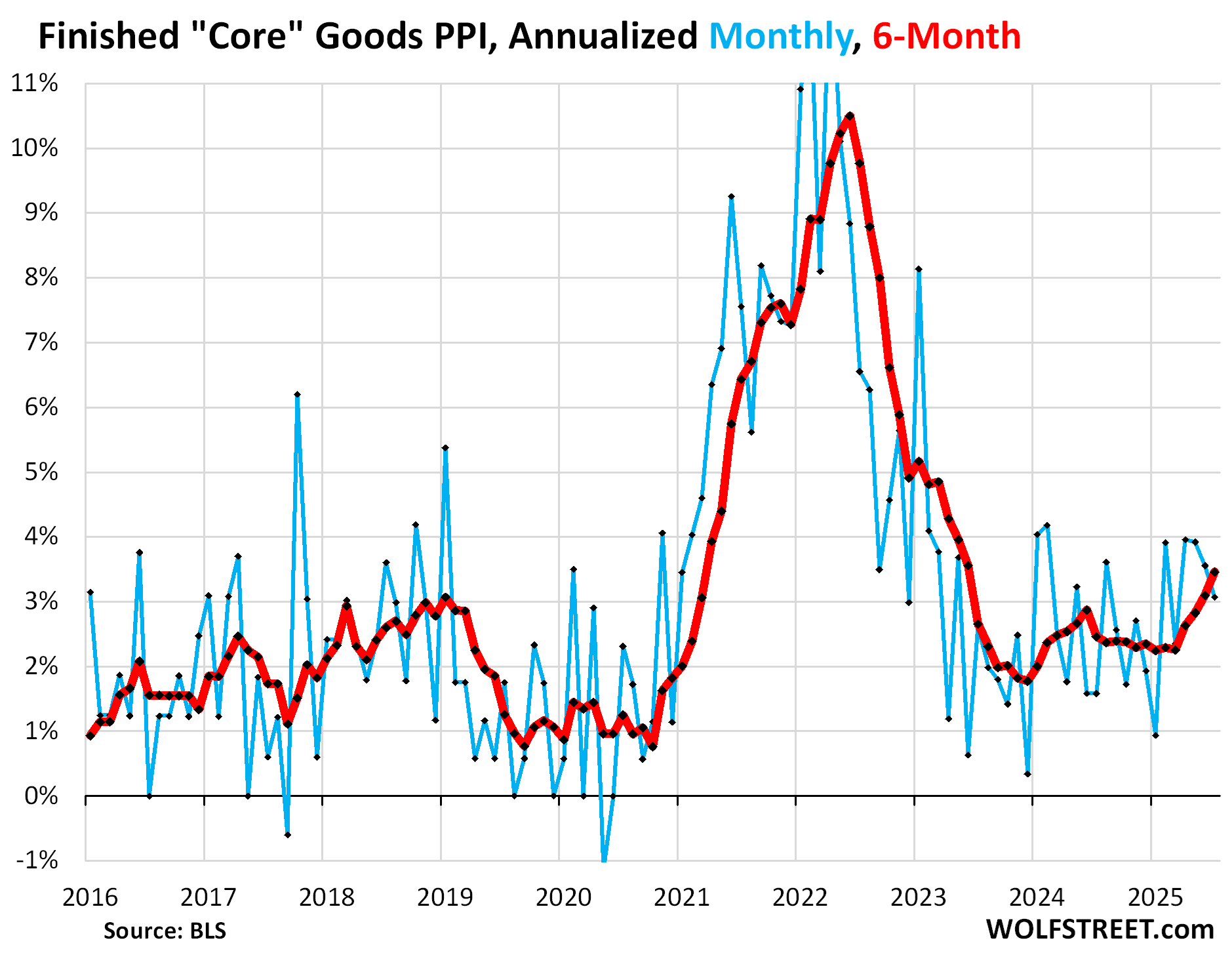

Core goods: plenty of inflation, but not nearly as bad as services.

The PPI for “Finished Core Goods” cooled a little, rising by 3.1% annualized, a deceleration from increases in the 3.6% to 4.0% range in the prior three months. This measure excludes food and energy.

The six-month average continued to accelerate and reached 3.5% annualized in July, the worst since June 2023.

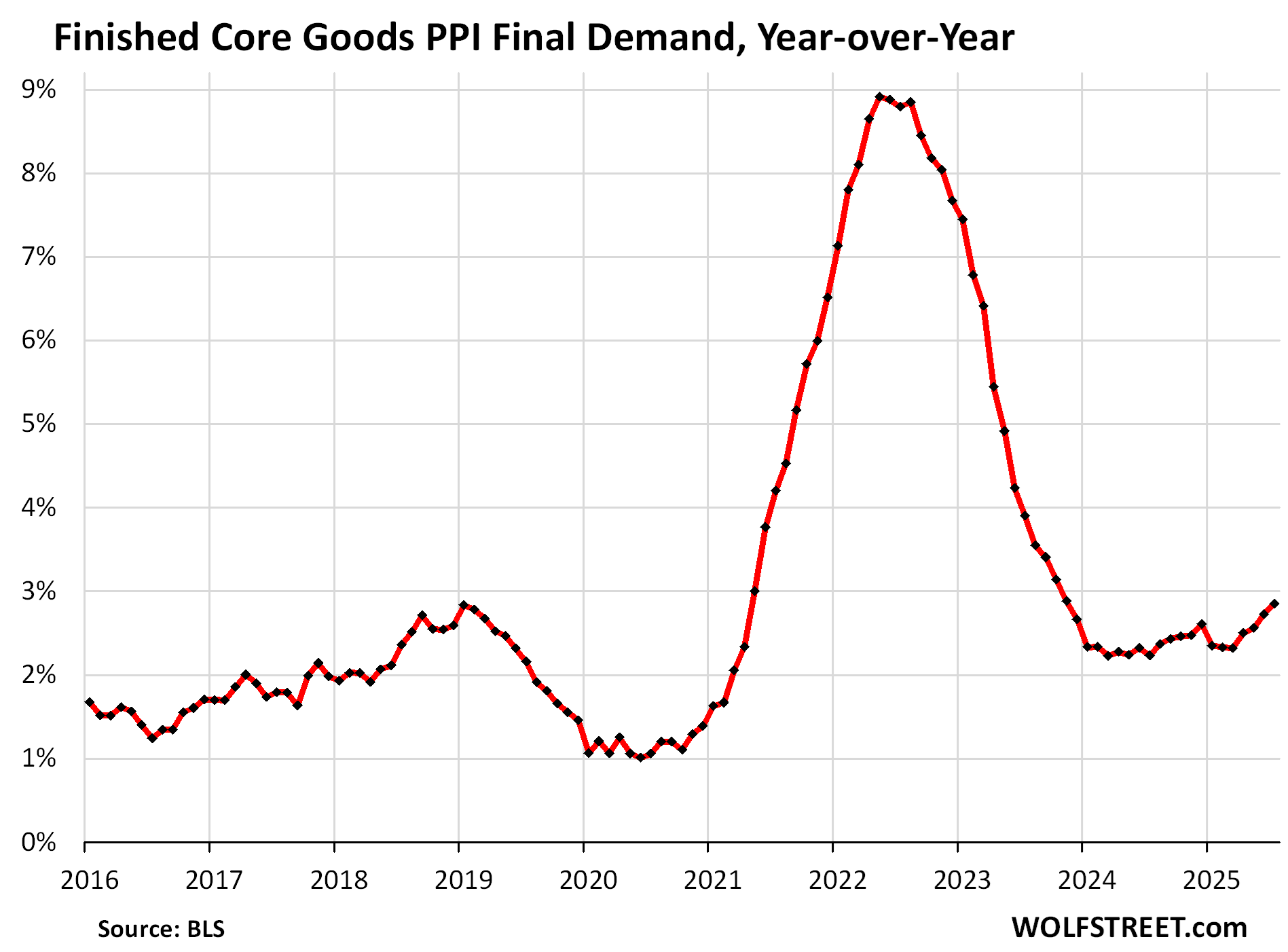

Year-over-year, the PPI for finished core goods accelerated slightly to 2.85%, the worst since June 2023.

“Core PPI Final Demand, which includes all goods and services except food and energy, exploded by 0.92% in July from June (+11.6% annualized), the worst spike since March 2023, driven by the price explosion of the services PPI. The six-month average accelerated to 2.9%.

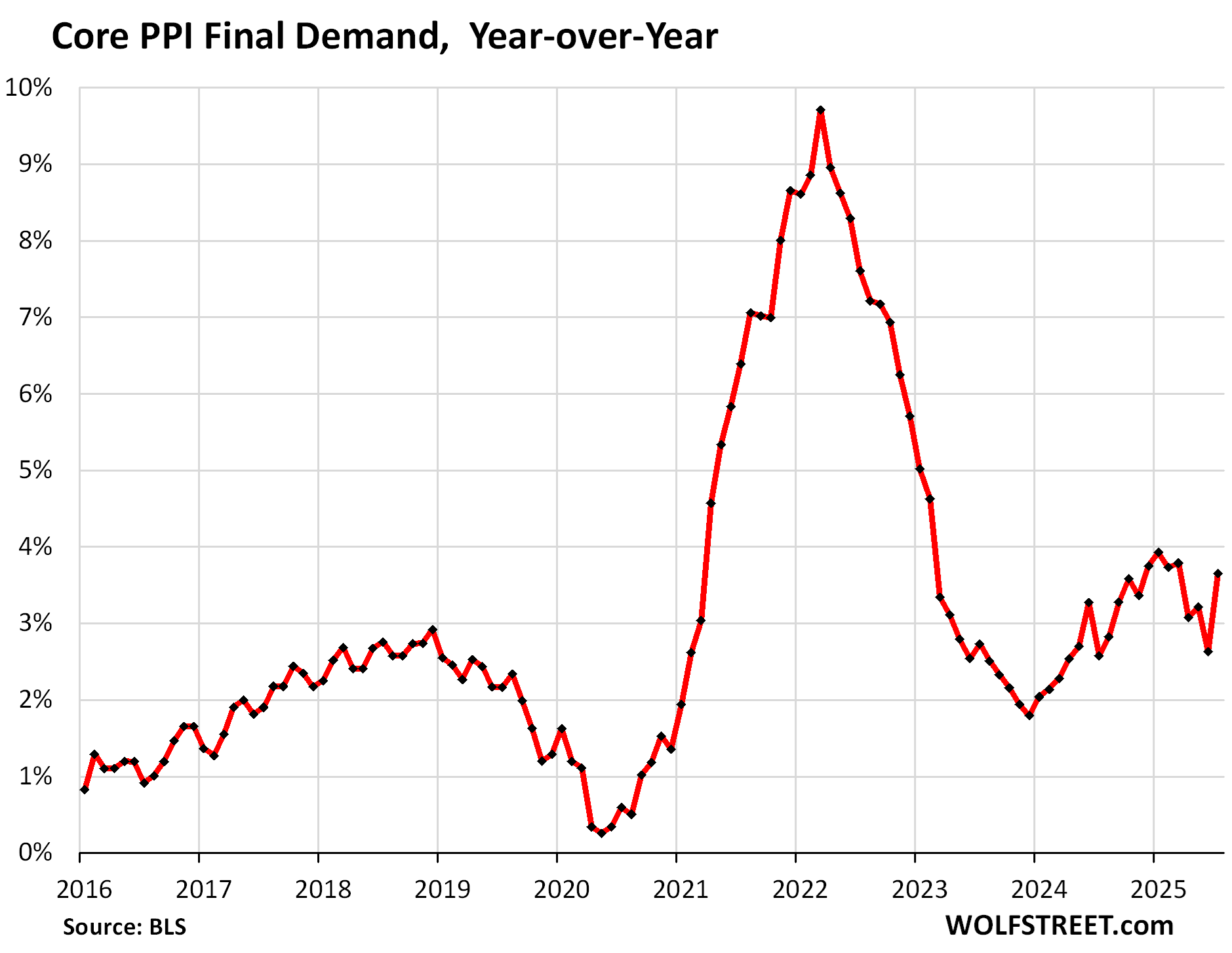

On a year-over-year basis, the core PPI accelerated sharply to +3.7%:

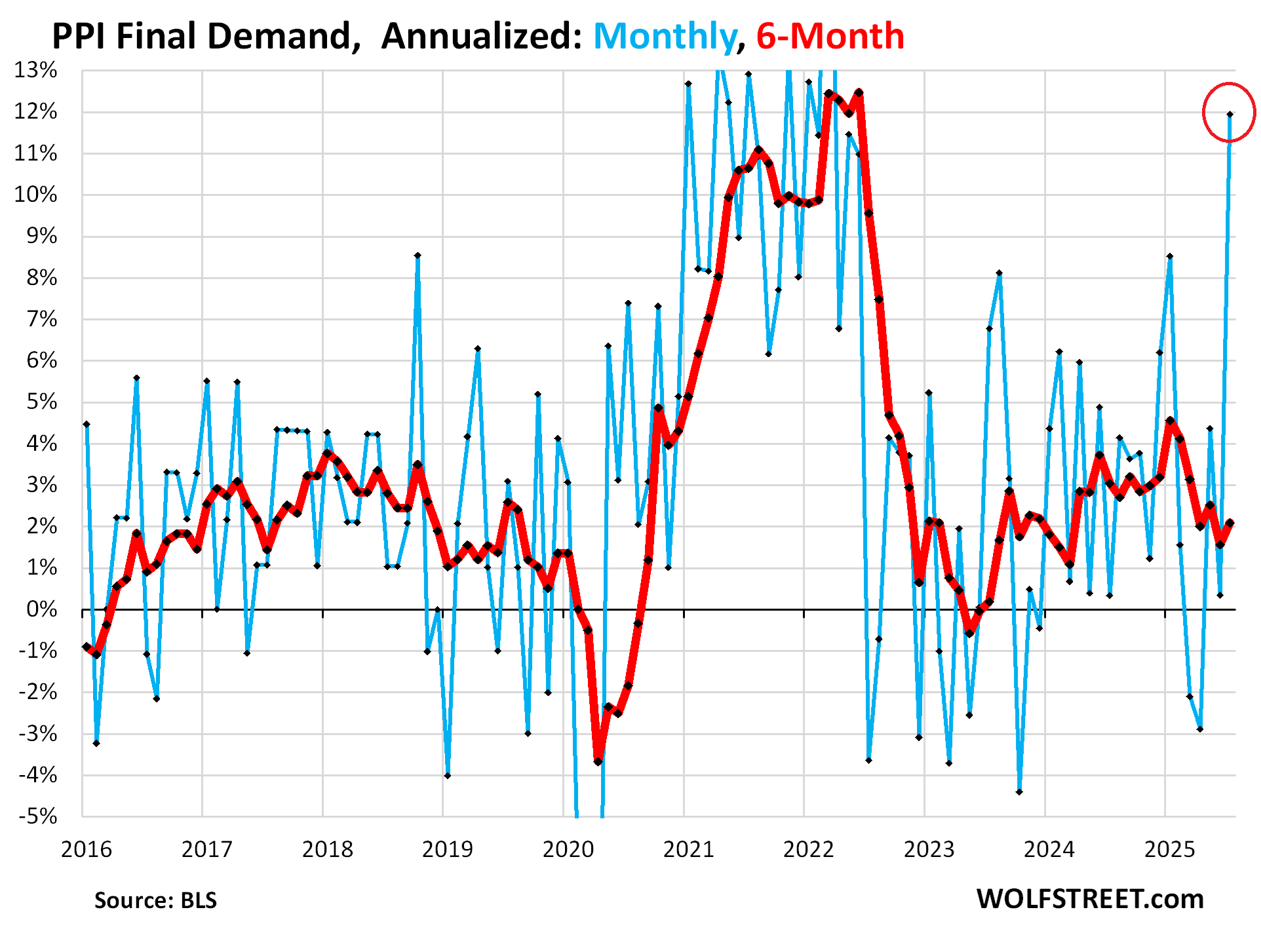

Overall PPI Final Demand exploded by 0.94% (+11.9% annualized), the worst spike since March 2022, fueled by the explosion of the core services PP.

And it was further fueled by the surge in food prices (+1.4% month-over-month).

Energy prices also surged (+0.9% month-over-month) on higher prices for diesel, jet fuel, and industrial electric power, though gasoline prices declined.

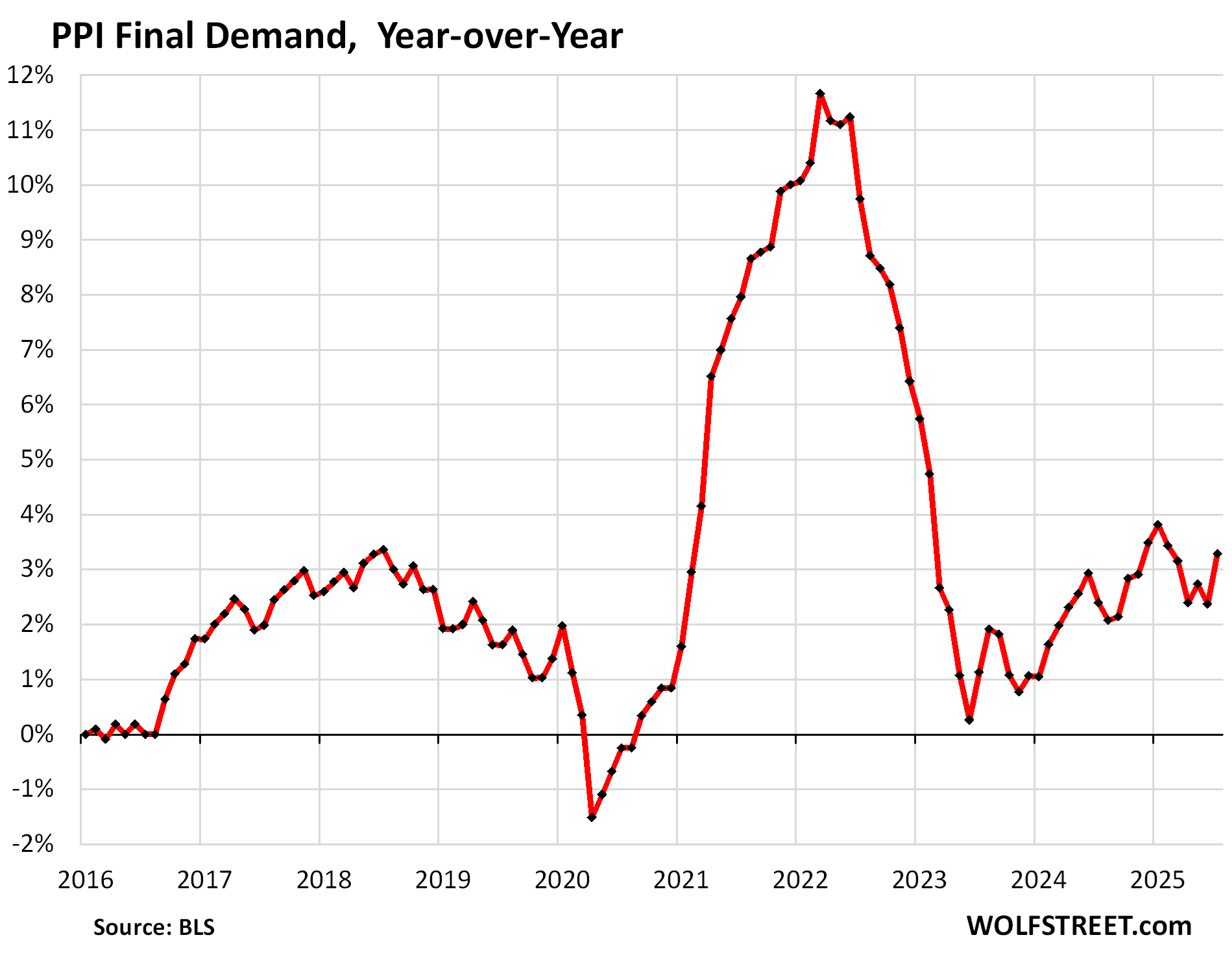

On a year-over-year basis, the PPI Final Demand accelerated to 3.3%, the worst since February.

Note how the acceleration in its uneven manner started in the second half of 2023, with June 2023 having marked the low point at near 0%.

What I expect.

Just by looking at the month-to-month blue lines in these charts, how much they zigzag, I expect further zigzags, big ones too. After a huge spike, we’ve often seen a much smaller increase or even a negative reading, and vice versa.

It’s the sum of those zigs and zags over time that mark inflation at the producer level. So I expect a sharp reversal of the services zig in a month or two. But I also expect the sum of those zigs and zags in the services PPI to trend higher on a six-month basis and on a 12-month basis and drag core PPI and overall PPI with it.

As mentioned, PPI reflects what companies charge other companies – not consumers. Companies paid $28 billion in tariffs in July, and they paid $27 billion in June, and $22 billion in May. Tariffs are a tax, but tax increases are hard to pass on, and tax cuts are never passed on.

But we can see the tariffs percolating through the ecosystem of companies as they’re trying to pass on some of the tariffs to other companies, and these other companies are resisting those price increases.

The far bigger concern here is inflation in services, which are not tariffed, which are a much bigger part of US economic activity, and where roughly two-thirds of consumer spending goes to.

And services inflation at the consumer level, such as tracked by CPI, has been reheating: Two days ago, the core services CPI shot up by 4.5% annualized, the worst in six months. It accounts for 60% of overall CPI. The push came from services other than housing. And today’s explosion of the services PPI is not encouraging, even if the next zag is much smaller.

And one more thing: The PCE price index, a measure of consumer price inflation that the Fed uses for its 2% target, includes some parts of the core services PPI here, such as the category of “portfolio management; securities brokerage, dealing, investment advice, and related services,” which also surged. The July PCE price index will be released on August 29, and it might come in hot due to services inflation, further fueled by the components from the services PPI here.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

May I ask – how do you think this will affect treasury interest rates going forward?

They will head upwards on US Treasuries, both short and long term.

For longer-term considerations, it takes more than a couple of inflation reports. So we have two CPI reports with accelerating services inflation in a row. And we had one PPI report with spiking services inflation. The trends look to be higher, but we need confirmation.

So today, Treasury yields rose modestly. The 10-year yield by about 5 basis points, undoing yesterday’s decline. The 6-month yield by about 3 basis points, also undoing yesterday’s decline.

Yesterday, the media was very successful in misrepresenting the CPI data by their exclusive focus in their headlines on overall CPI, which had been kept down by dropping energy prices, while CPI services and therefore core CPI surged. That surge was worrisome, but the headlines covered it up.

Today, that could no longer be done with the PPI.

For the bond market to seriously react to inflation, we need confirmation. If we get another bad core CPI reading and a bad core PCE reading before the FOMC meeting, and the Fed cuts anyway, long-term yields will like start rising on renewed fears of a lackadaisical Fed in face of surging inflation. The bond market is very nervous about inflation not being contained by the Fed.

Market doesn’t care. Looks like it’s locked in for rate cuts.

The federal funds rates futures market yesterday had a 0% chance for a rate hold and even 2% double cut. After PPI we had a 10% chance of a hold.

It kind of feels like to me the equity shot its load early when cuts started. And now that they bet so much on it, its actually having the reverse effect. The expectation of lower rates might have lead to over-optimism and thus preemptive spending. Which ends up hurting the chances of a cut.

Like why should the fed cut? I hear so many people say they should, but to solve what problem? The stock market sure thinks cuts are coming, but Im not sure why.

I know what you mean. He last cut them around election time, Sept through Dec, 2024. Why? That is the one time I would have to say that he cut to appease the current President and/or the one to be.

If he cuts, I think it is just to show how dumb it is to invite even higher inflation rates back. “Look what you made me do!”

No, it isn’t at all and sank today on yet another set of delusional notions yesterday that rates would go down. They won’t.

Explosive and shocking indeed unless you read WS. I remember reading how inflation has a way of dishing out nasty surprises.

Need to see JP pulling his hair out here.

The stock market is primed for a rug pull.. But it probably won’t happen.

Do you think the tariff increases will be onetime? My guess is a gradual decline in month on month number over next 6 months. And I guess, the difference in CPI an PPI will likely affect corporate profits more, essentially creating more impact on stock prices (lower PE) than bonds.

The other aspect could be decline in dollar (something you may want to cover in article) causing tariff like effect or magnifying it – increasing PPI If dollar strengthens (which seems unlikely) this effect may reverse

Overall – my guess not very bearish for us30y, us10y but a hit on EPS for companies. Who knows – I may be wrong.

July PCE will come in hot, but not as hot as now expected. The sensible commenters on this board will call for no Fed cut in Sept, while the administration will point to the number as good news and refresh its call for urgent rate cuts (to lessen the cost of interest, mind you, not because the economy is weakening).

Sensible people will suggest a significant Federal Funds interest rate hike.

Shout this a thousand times from the rooftops, as it is the real reason for cut pressure: “to lessen the cost of interest.”

(However, I’d replace “interest” with “debt,” as a quibble).

The head of the exec branch is a debt guy.

It will be interesting to see if Trump is going to continue “his inflation is low” and “the Fed needs to reduce rates” rhetoric. Maybe one of his staff will clue him in (I doubt it).

No one on his staff or party has the cajones to disagree with him on anything.

Has anyone seen a group of hypnotized masses since the emperor with no clothes?

Seriously, this is starting to get ridiculous or is it scary?

Listening to NPR on occasion I’m amazed they are even still on the air based on the audacity of their reporters to represent a different P.O.V. other than the Trump mandate.

Uhm how about every fucking administration. I swear you people only wake up every 4 years

The facts have already clued him in and if he ignores that it will, of course, be to his own peril. Facts are facts. Delusions are delusions.

“According to a report from the US Department of Labour (DOL) released on Thursday, the number of US citizens submitting new applications for unemployment insurance fell to 224K for the week ending August 9. The latest print fell short of initial estimates (228K) and was lower than the previous week’s 227K (revised from 226K).

Additionally, Continuing Jobless Claims shrank by 15K to 1.953M for the week ending August 2.”

Where’s the recession?

This is all very exciting. Thank you Wolf.

Line go up!

Can ANYONE please tell me is there ONE GOOD REASON at this time for a rate cut?

Being REALISTIC of course.

Thank you.

I don’t personally think there’s any good reason at all for a rate cut. Those inclined to advocate for it, though, will point to the past 3 months’ slowdown in the employment numbers, which suggest a risk of a broad economic slowdown over the next few months.

This employment slowdown will be argued to justify a rate cut, by people who unfortunately will then soon enough have cause to shed tears while interest rates rocket back up in 2026, as the Fed is forced to respond to what will, by then, be a level of inflation even the administration won’t claim to love.

Thank goodness that, according to the “Main Stream Media”, inflation is only “transitory”.

Just take a look at the Bonds today

The long end yields all spiked big time.

The rest is all noise, IMO

Moves in the 20 year Treasury bond yield tells me pretty much all I need to know about inflation, although yesterday’s action seemed odd (rates went down despite high core CPI number). The stock market is a useless indicator, driven by mad men and MSM.

Today could not be ignored. Also see jobless claims post a bit up above. One Two punch.

So rate cut in Sept then? Cool…

Oh man, it’s going to be a good one for all the firework aiming at Pow Pow if he deviates from rate cut fever dream despite these not so good numbers

Does anyone know what the inflation rate for CPI-E is at this time ? Is this info being published (or even still being collected ? ). I did a google search and could not find anything.

For retirees, the key inflation index is the Consumer Price Index for the Elderly (CPI-E), which is a research price index calculated by the Bureau of Labor Statistics (BLS). The CPI-E specifically reflects the spending patterns of those aged 62 and older. While not used for official government adjustments like Social Security’s COLA, it provides a more realistic measure of inflation for retirees.

I have to wonder if BLS numbers in the future are going to reflect reality, or the wishes of some guy in the White House ?

Statistics will increasingly reflect the White House’s agenda. We’re in Lysenkoism now.

2.9% YoY

You can download the data, including sub-indices, here:

https://www.bls.gov/cpi/research-series/r-cpi-e-home.htm

FRED also has a series on it somewhere.

Meanwhile aspirants to appointment to the Fed outdo each other in their proposed cuts to the Fed’s rate. Marc Zumerlin is a piker here having called for a mere .5 % cut last time. David Zervos blows right past him in this race. Zervos is unable to see his way to Trump’s desired 3% cut ‘but I could certainly get to 2%’ or 4 times Zumerlin’s call.

Is it something in the water?

Just as all of the financial shill sites were penciling in a jumbo rate cut in September…. Any rate cut at all would be a dereliction of duty.

Prices at the grocery store lately are absolutely mind-blowing. And I won’t even get into coffee.

“Over half of the broad-based July increase [in services] is

attributable to margins for final demand trade services, which jumped 2.0 percent (27% annualized). (Trade indexes measure changes in margins received by wholesalers and retailers.)”

Does this mean that wholesalers are passing tariffs on to other companies, even if companies aren’t yet passing those tariffs on to customers?

My gut has been telling me that inflation due to tariffs really wouldn’t start working its way into actual prices paid until Q4 of this year. My gut still tells me that we’re going to see inflation tick up and stay problematic through mid-2026 at the earliest, barring any other shocks from energy or a sudden financial blowup somewhere.

With all that said, and I think that new car sale prices are a good indicator of this, I don’t think companies have much pricing power at the moment. Used car prices are ticking back up (to be expected with fewer used cars available due to the pandemic, combined with the *belief* that used = cheaper), but new car final sale prices seem to have hit a ceiling.

I can’t help but think that a rate cut will be serious fuel to the inflation fire, but it seems that Trump is hellbent on making that happen.

Another anecdote in the services pricing discussion: I run an IT services company out of the midwest. Last month we received three requests for price breaks from long term happy clients who are under some financial strain. In the 27 years I’ve been in this business, this is only the second time we’ve received requests like this (first time being 2009).

In terms of new biz development, our sales team has had to get clever with pricing, and our margins are definitely under pressure. Whereas we typically are able to charge $200 per user/mo., we’re increasingly making consessions to earn new business (no charge for onboarding, discounts for year paid in advance, price reductions into the $165/user range, etc.).

Again, anecdotal. We’re still making reasonable profit, but the challenges are definitely out there.

If you’re still making reasonable profit, what were you making before?

There’s a lot of excessive profit that can still be squeezed out of the economy, in favor of consumers.