He who panicked first panicked best.

By Wolf Richter for WOLF STREET.

There’s so little demand at current prices, and so many homes sitting on the market, that sellers are pulling them off the market “in frustration,” a phrase realtor.com used to describe the situation in a blog post. Others aren’t putting their homes on the market but are hoping for better days or whatever. The issue is that prices have shot up to such ridiculous levels that they’re now way too high, and the buyers willing to pay those too-high prices have already bought, and now demand has vanished at those prices, though there would be plenty of demand at much lower prices.

Home-sellers that sold in 2024 and in 2023 at near peak prices got out the door with their money. He who panics first panics best. Since then, prices have drifted lower, and condo prices in many markets are now plunging – see price charts at the bottom for Fort Myers and Saint Petersburg.

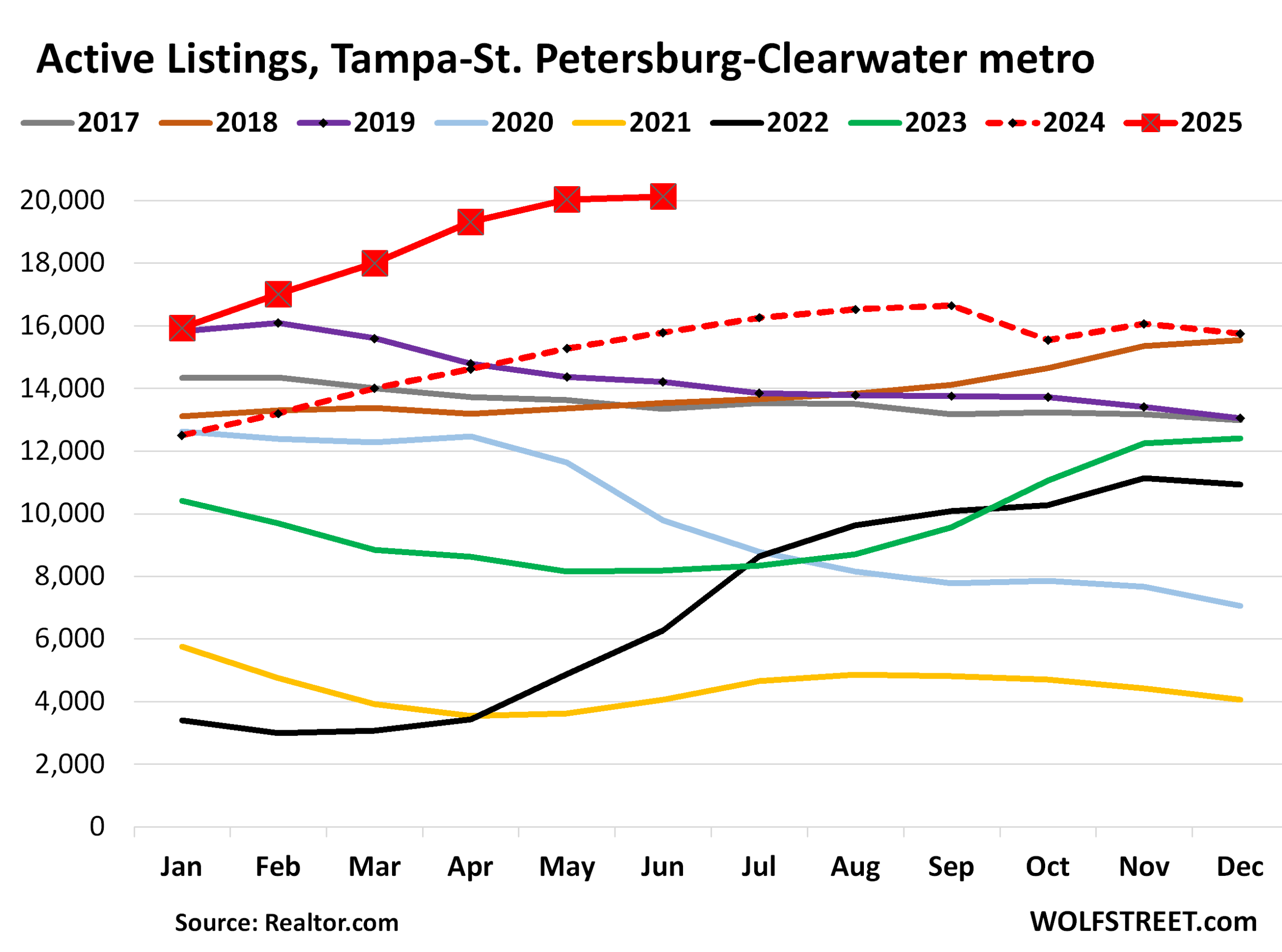

In the Tampa-Saint Petersburg-Clearwater metro, active listings jumped by 28% in June from the already multi-year high levels in June last year, to 20,128 homes, the highest in the data from realtor.com. That dataset goes back to 2016. Compared to June 2019, inventory was up by 42%; compared to June 2018, by 49%; compared to June 2017, by 51% — massive inventories, at a time when sales have plunged.

Inventories in 2021 (yellow line at the bottom) and in early 2022 (black line at the bottom) were as close to zero as they could possibly get – not because homebuilders hadn’t built enough homes, and not because there was a “housing shortage” or whatever, but because there was an extra-special buying-frenzy, driven by the Fed’s reckless monetary policies, where people, who’d just bought a home and moved into it, held on to their now vacant home, instead of putting it on the market, in order to ride the enormous price spike up all the way since money was nearly free.

Those who have sold their vacant homes by now came out way ahead. Those that bought them, not so much. And those that haven’t sold them yet, well, they’re facing an entirely different market with plenty of demand, but at lower prices.

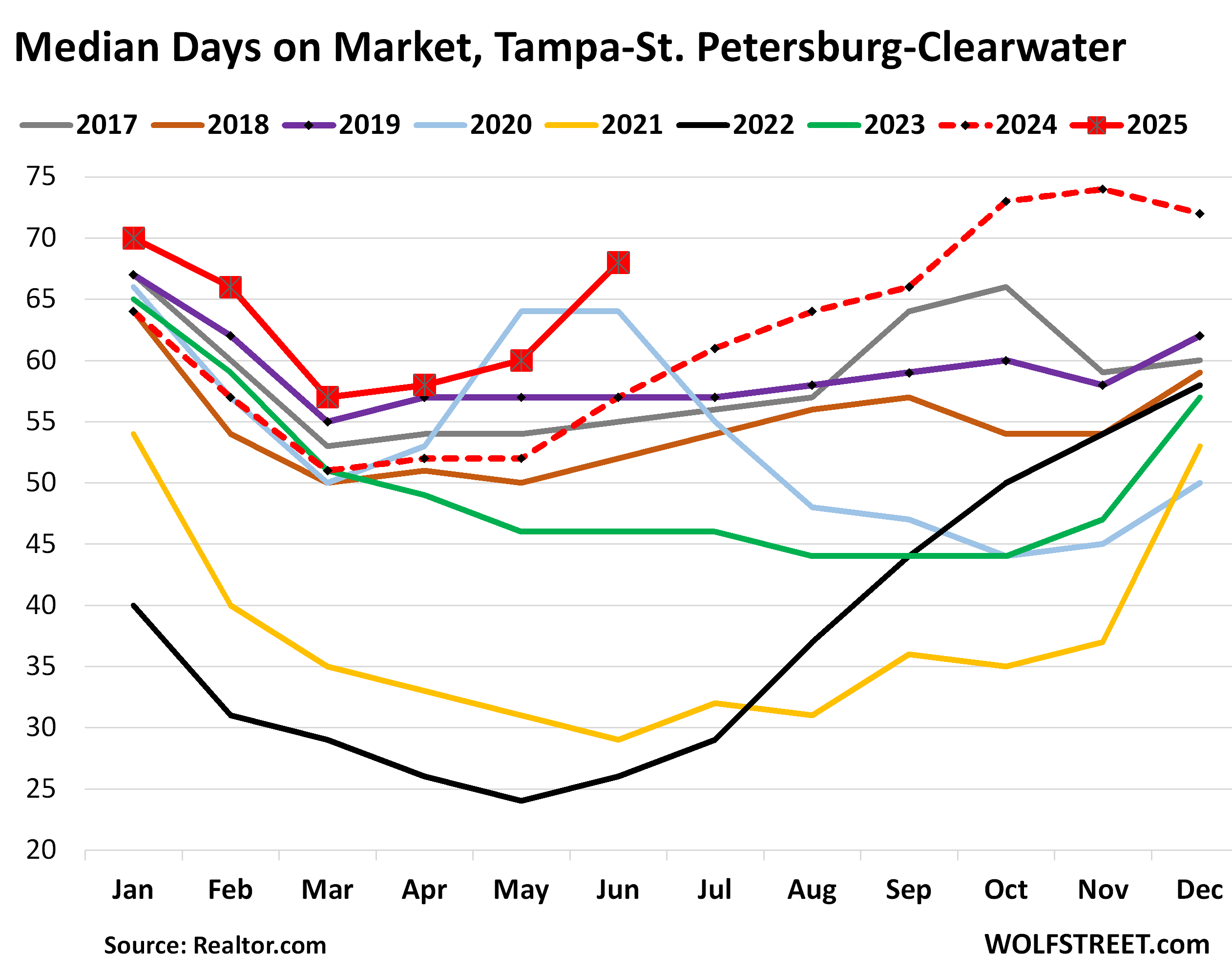

The median number of days homes sat on the market before they got pulled off the market or before they sold spiked to 68 days, the highest for any in June in the data from realtor.com, which goes back to 2016, up from 57 days in June 2024:

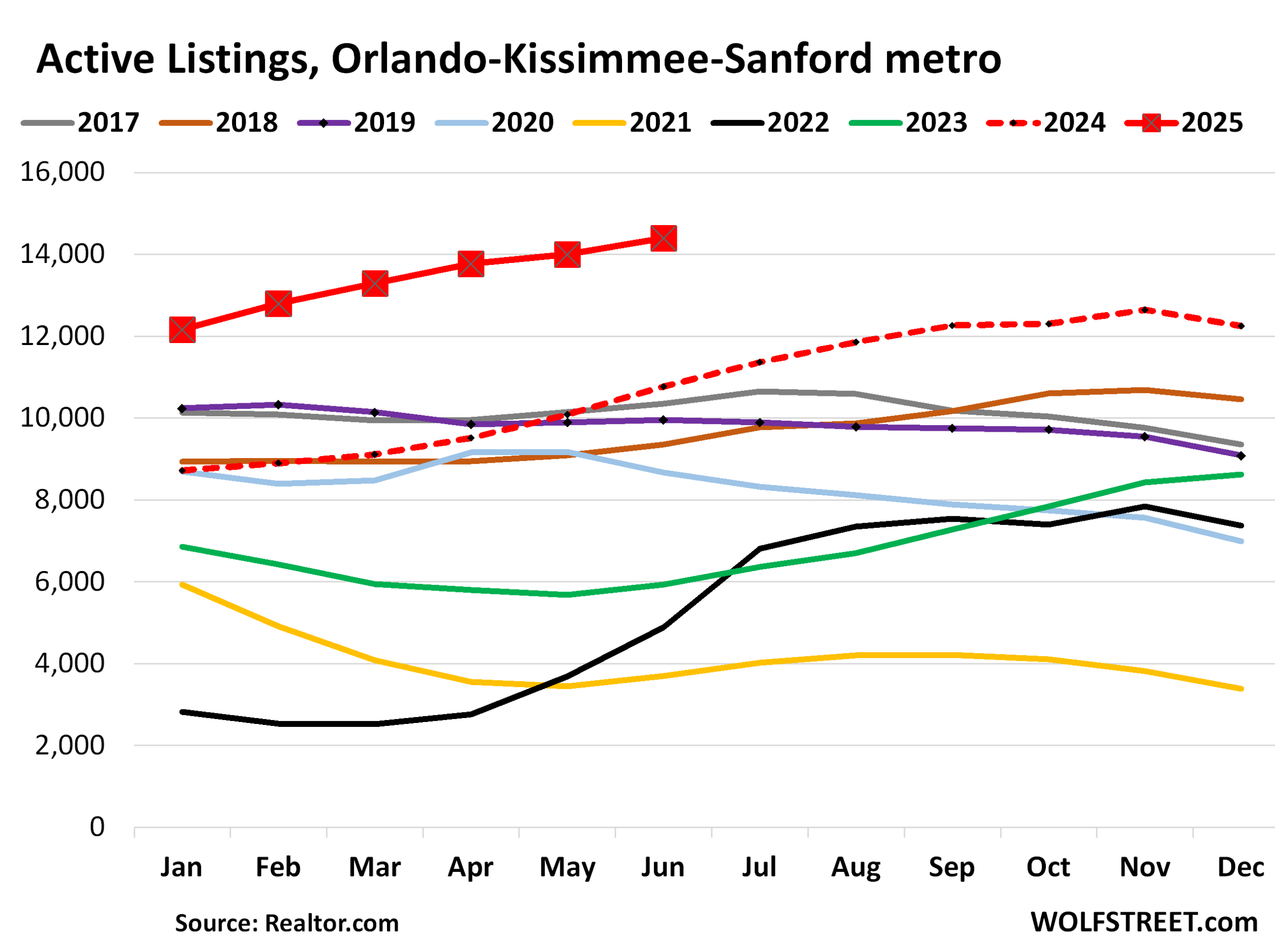

In the Orlando-Kissimmee-Sanford metro, active listings jumped by 34% year-over-year in June, to 14,391 homes, by far the highest in the data from realtor.com which goes back to 2016.

Compared to June 2019, inventory was up by 45%; compared to June 2018, by 54%; compared to June 2017, by 39%.

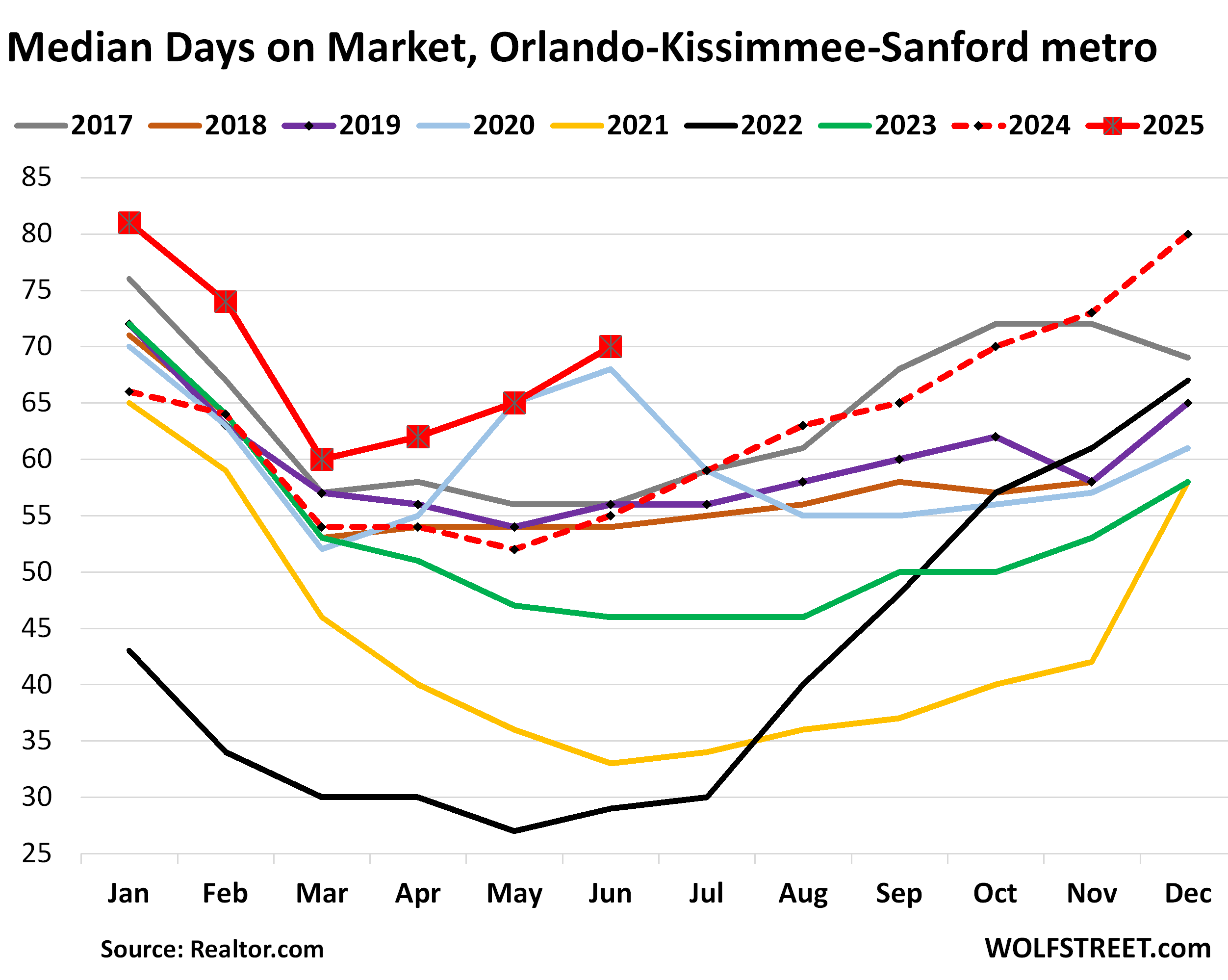

Homes sat on the market for 70 days before they got pulled off the market or were sold, the highest for any in June in the data from realtor.com, which goes back to 2016, up from 55 days in June 2024 and up from the 54-56 range for the Junes in 2017-2019:

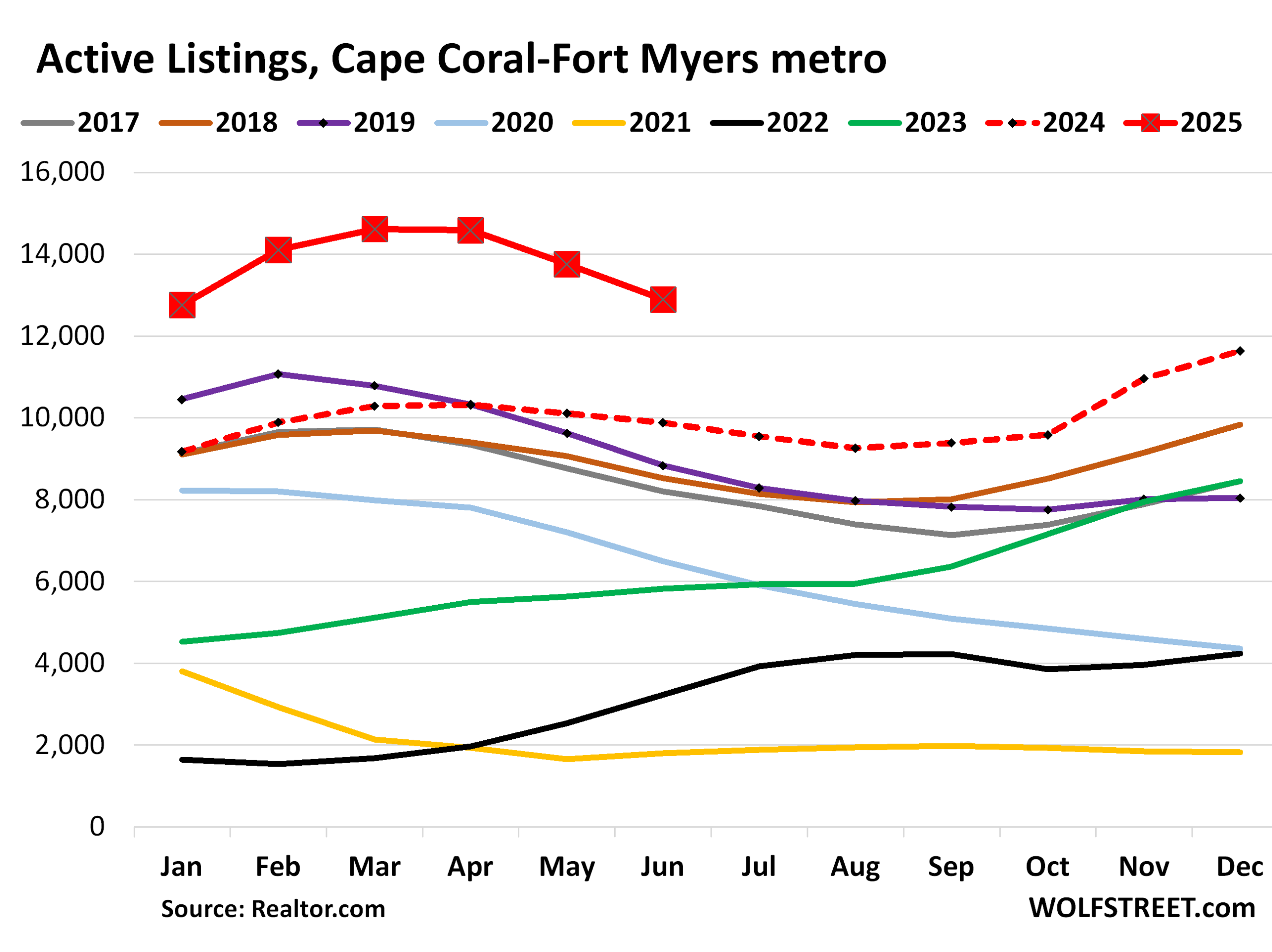

In the Cape Coral-Fort Myers metro, active listings jumped by 30% year-over-year, to 12,892 homes, the highest June in the data from realtor.com.

Compared to June 2019, inventory was up by 46%; compared to June 2018, by 52%; compared to June 2017, by 57%.

Days on the market jumped to 95 days, up from 79 days a year ago, matching June 2020, and both were the highest since the data from realtor.com.

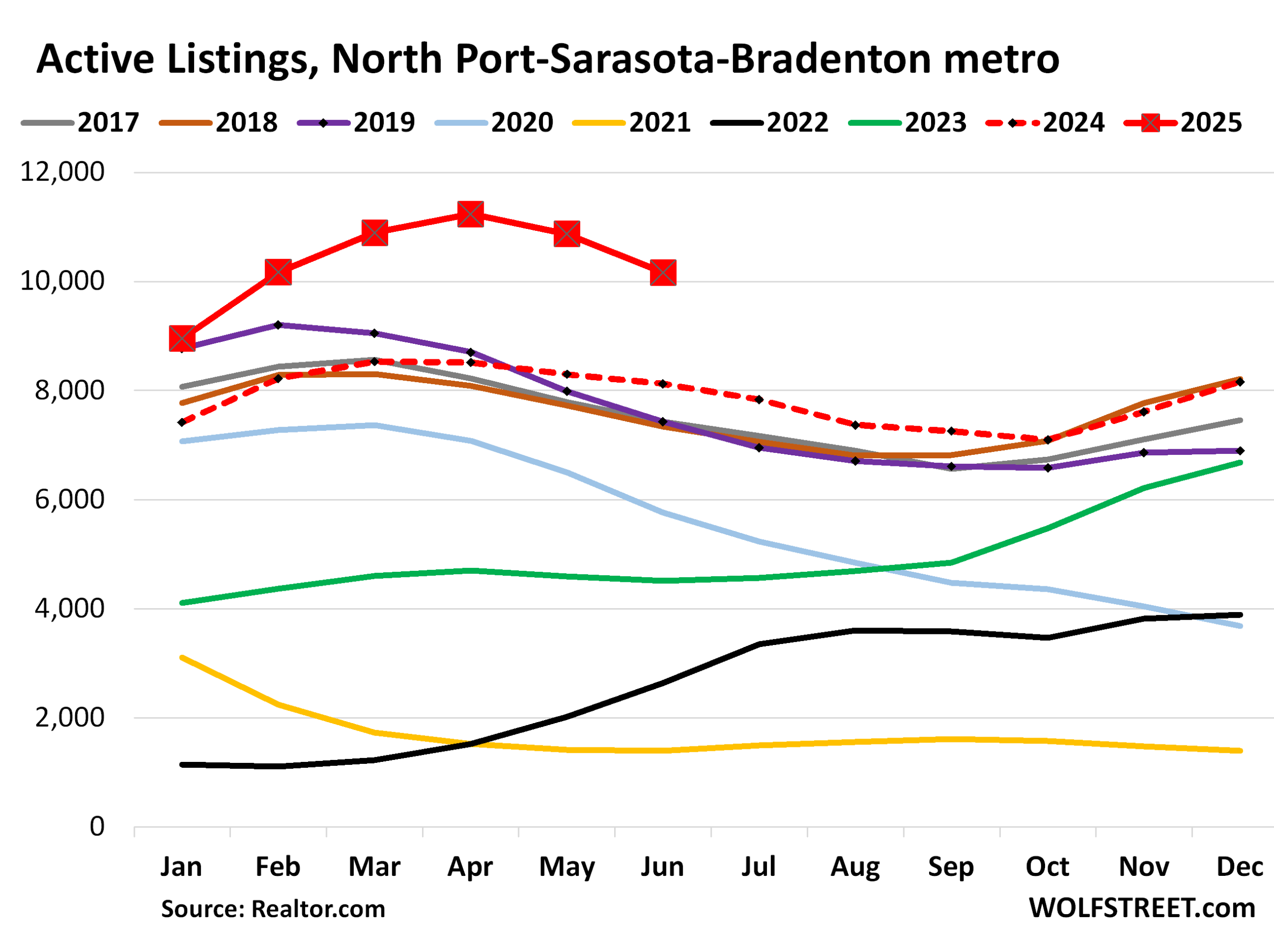

In the North Port-Sarasota-Bradenton metro, active listings rose by 25% from June last year, which had already been the highest June in the data from realtor.com going back to 2016; to an even higher 10,163 homes.

Compared to the Junes in 2017-2019, inventory was up by 37-38%. Days on the market rose to 77 days, from 65 a year ago.

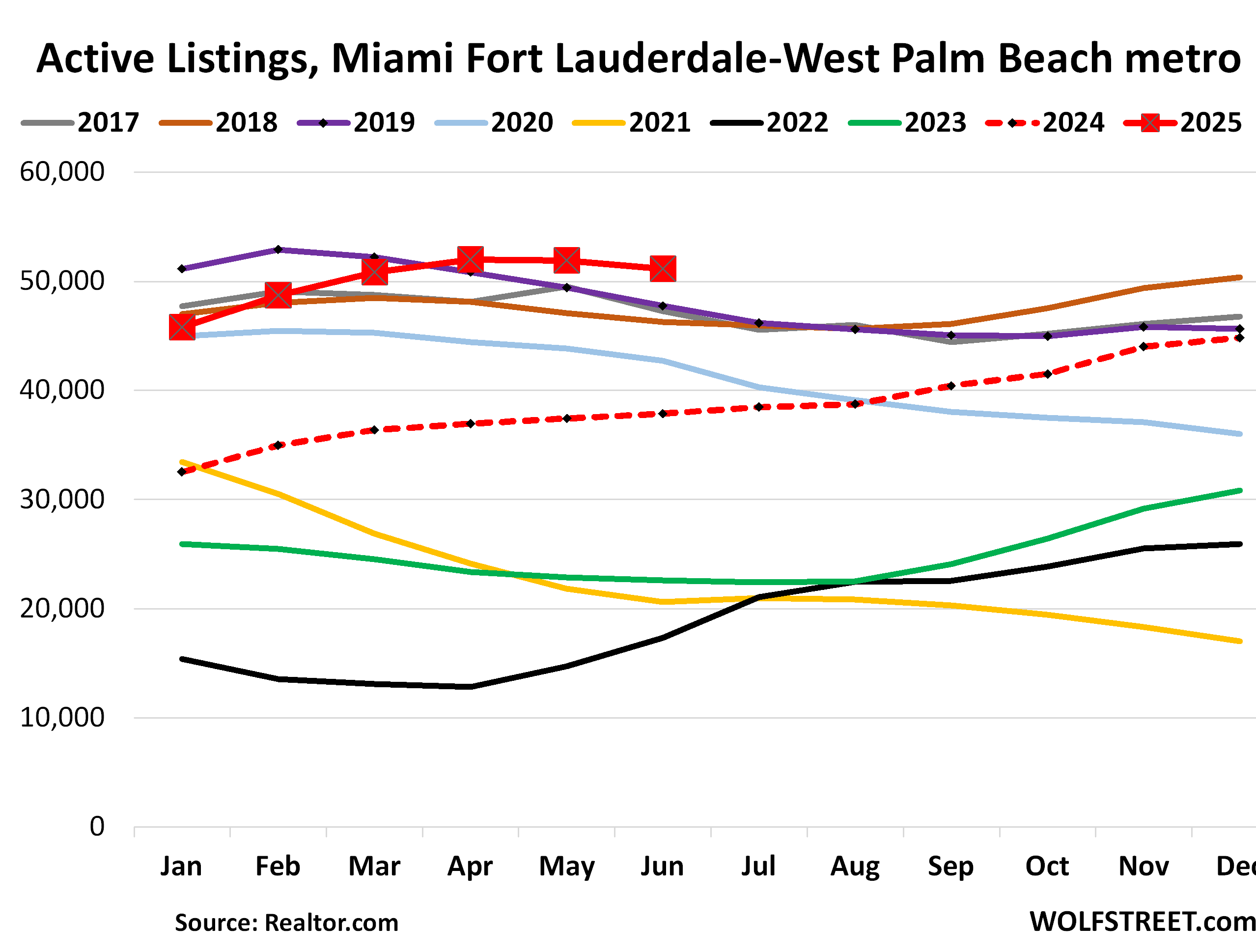

In the Miami-Fort Lauderdale-West Palm Beach metro, active listings jumped by 35% year-over-year in May, to 51,139 homes, the highest June in the dataset from realtor.com, which goes back to 2016.

Compared to the Junes in 2017-2019, inventory was up by 7-10%. Days on the market jumped to 83 days, from 68 days a year ago:

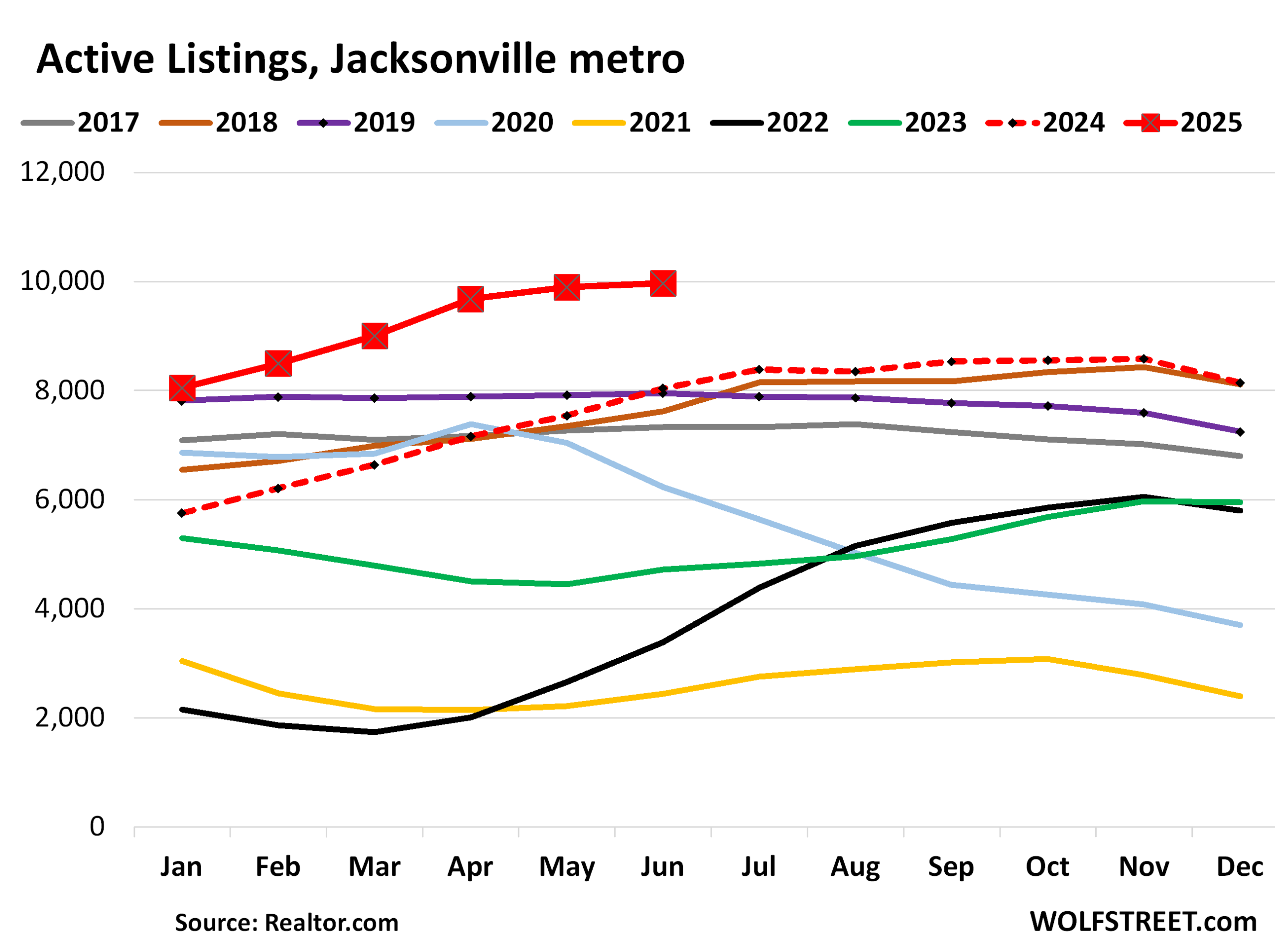

In the Jacksonville metro, active listings jumped by 24% year-over-year, to 9,965 homes, the highest in the data from realtor.com.

Compared to June 2019, inventory was up by 25%; compared to June 2018, by 31%; compared to June 2017, by 36%.

Days on the market jumped to 67 days, from 55 days a year ago, and from the range of 57-60 days in 2017-2019.

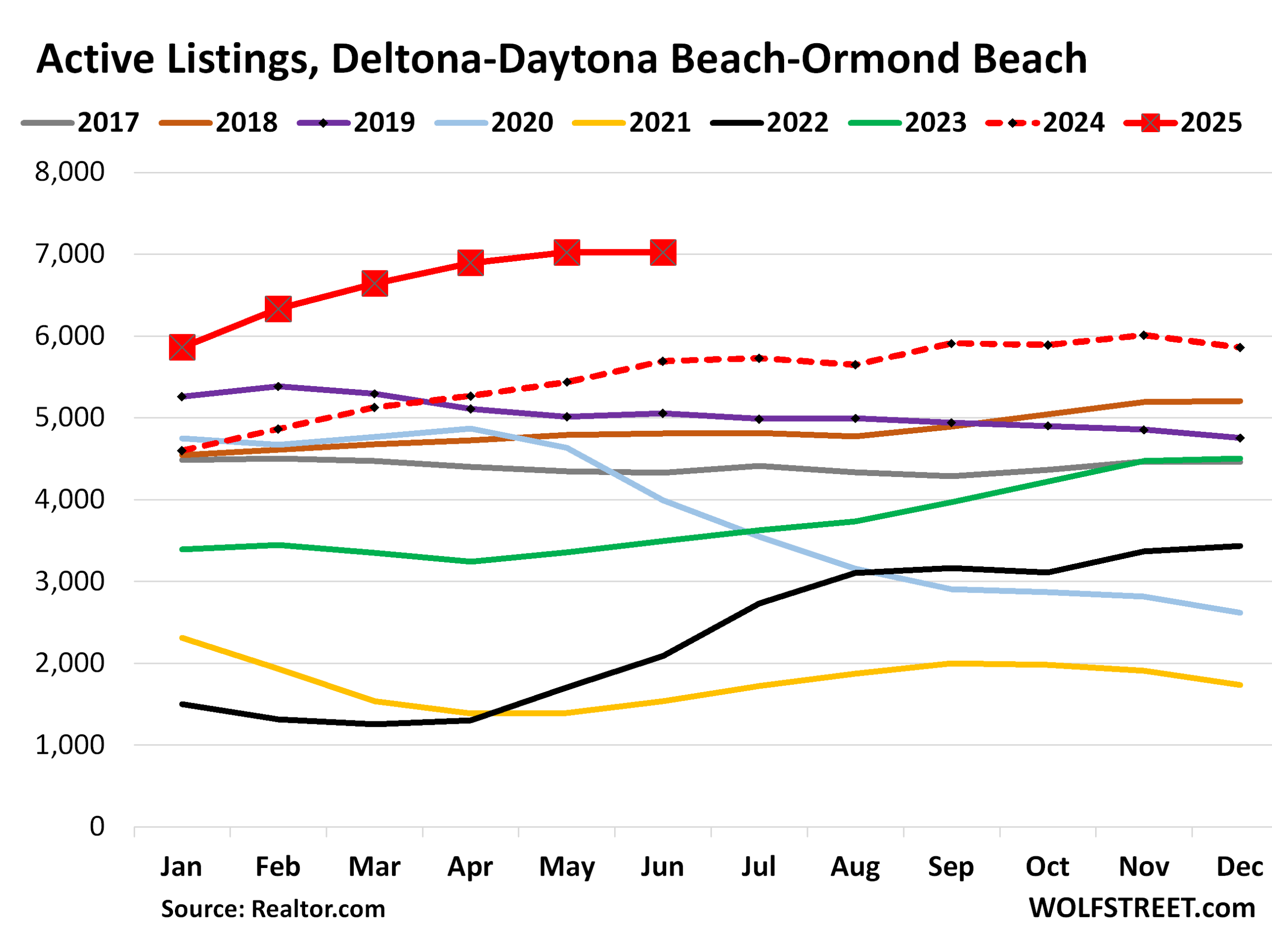

In the Deltona-Daytona Beach-Ormond Beach metro, active listings rose by 23% year-over-year to 7,021 homes, the highest in the dataset from realtor.com.

Compared to June 2019, inventory was up by 39%; compared to June 2018, by 46%; compared to June 2017, by 62%.

Days on the market jumped to 79 days, up from 66 days a year ago. In the data that goes back to 2016, only June 2020 was higher. In the Junes of 2017-2019, the range was 63-70 days.

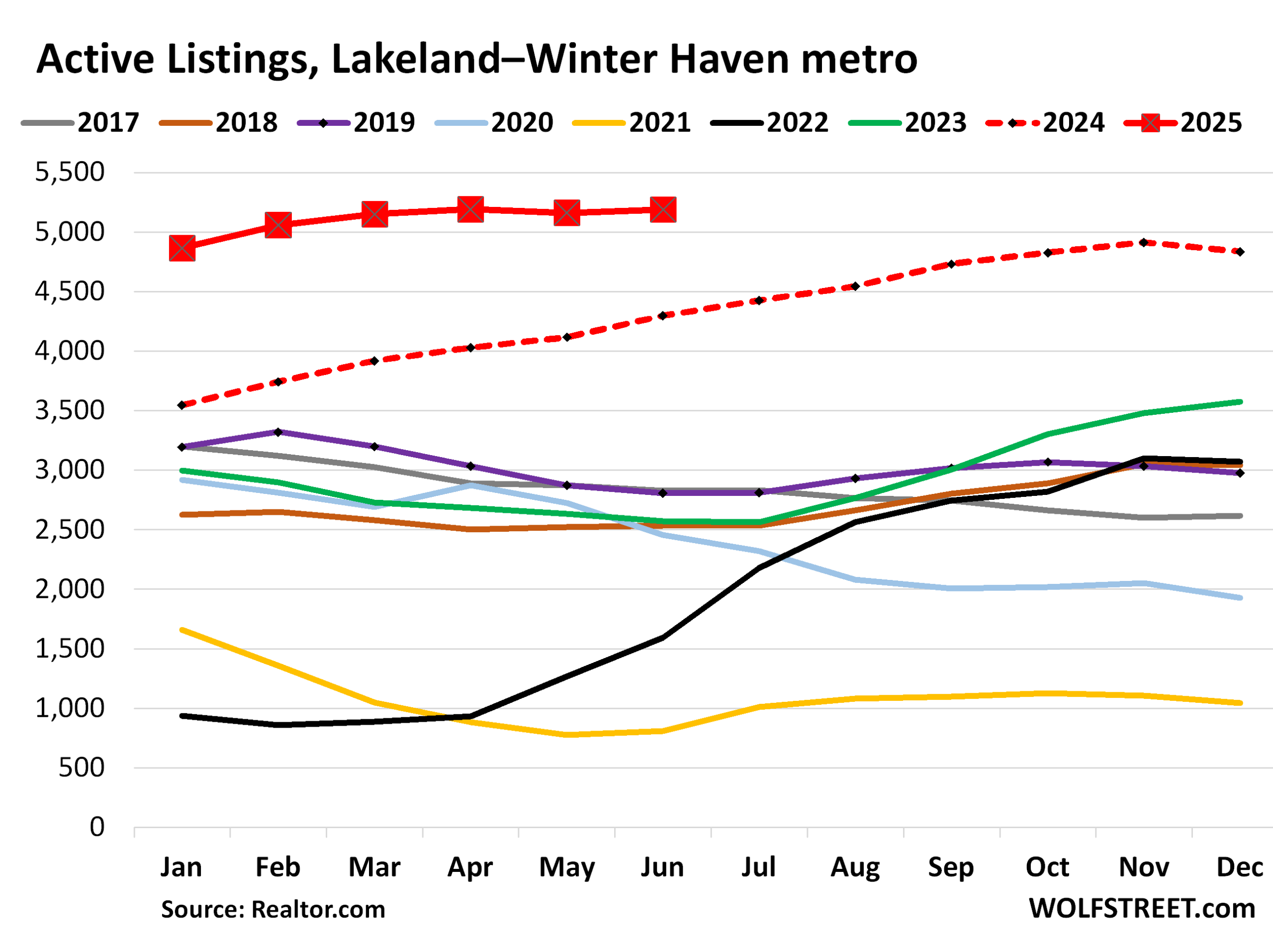

In the Lakeland-Winter Haven metro, active listings rose by 21% from the already extreme levels last June, to 5,189 listings, the most in this dataset that goes back to 2016.

Inventory has more than doubled compared to June 2018, and was up by 85% from the Junes in 2017 and 2019.

Anything can be sold if the price is right (low enough). But where is that?

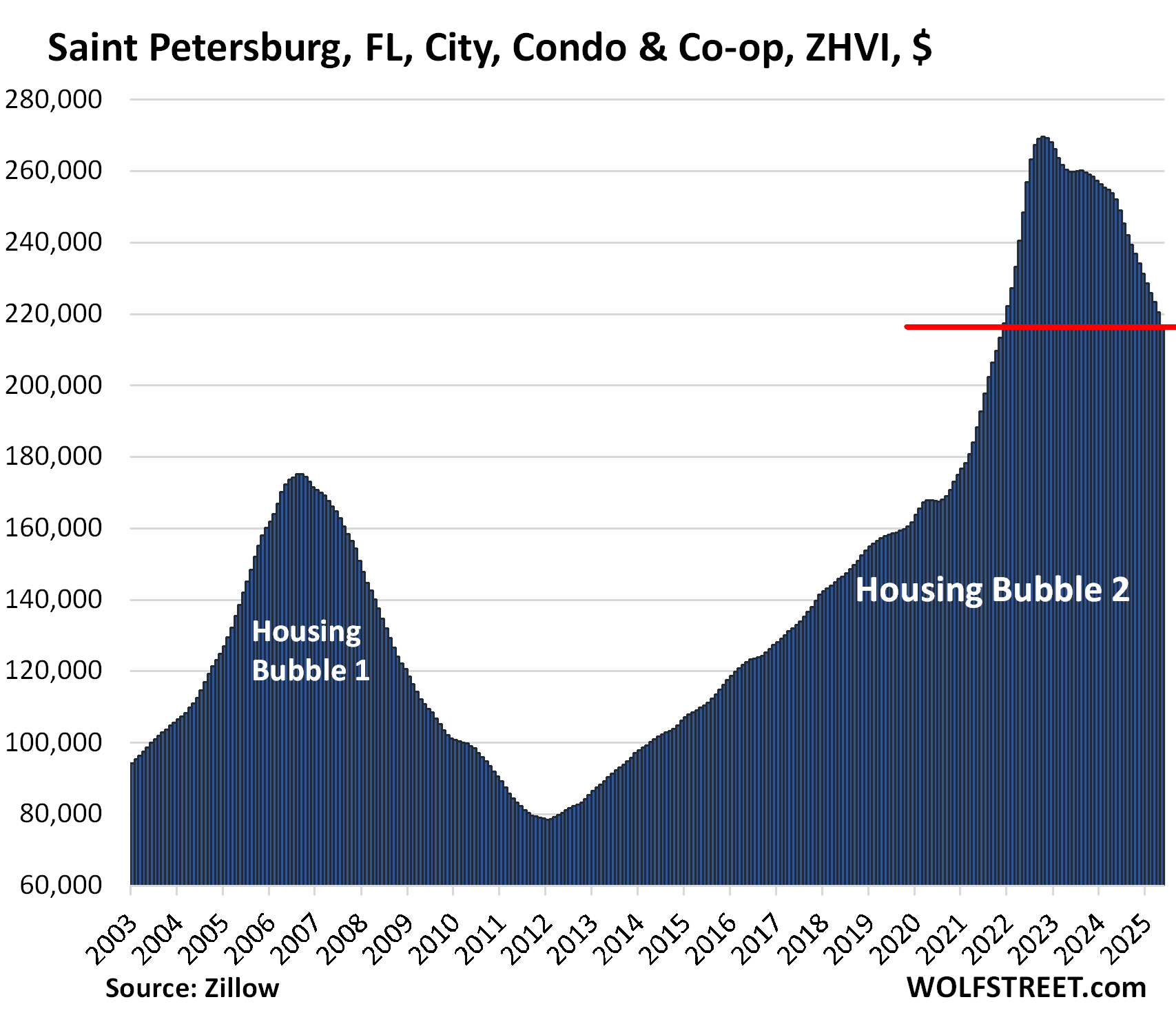

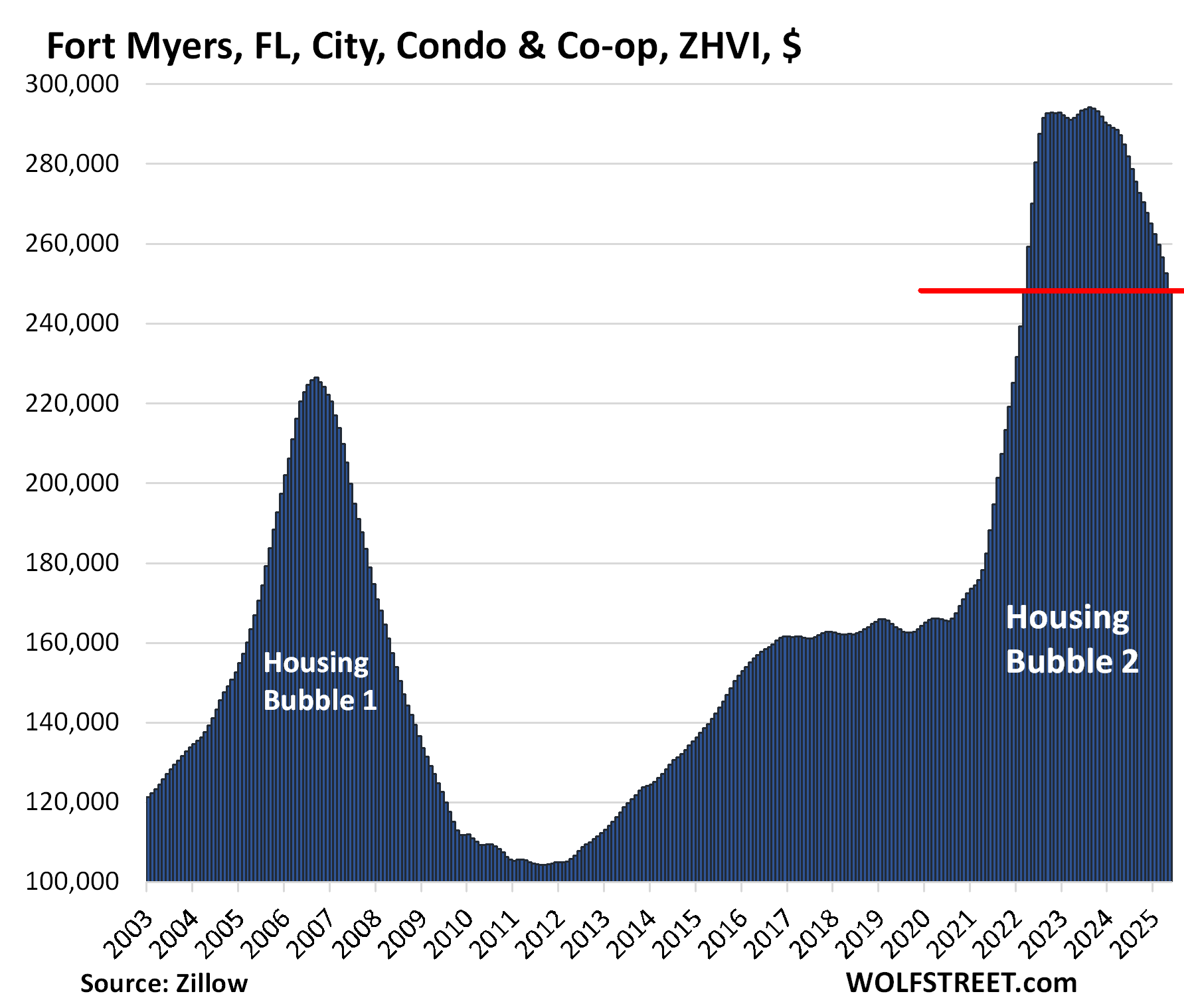

After a historic price explosion came the market’s search for reality. But where is that reality? For example, Saint Petersburg and Fort Myers. Both feature among the 20 bigger cities where condo prices already dropped by 10% to 23%.

In Saint Petersburg, condo prices have plunged by 20% through May, from the peak in October 2022, and are back where they’d been in October 2021, unwinding about one-third of the 100% price explosion since 2017.

In Fort Myers, condo prices have plunged by 16% since July 2022 after one of the craziest and silliest home-price explosions ever. There is a reality somewhere, and the market is trying to find it:

And in case you missed it: Inventories of Homes for Sale in Big California Markets Jump to Highest in Years, Days on the Market Soar, Demand Withered.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I saw a nice townhouse for sale locally in Sarasota FL for $379K. Just one small problem: HOA fees are $895…….PER MONTH!

My son wants to move closer to work in Ave Maria. Unfortunately the HOA fees are about $800 a month there too.

Are we the only family without a money tree in the backyard? How is this normalized? (I blame the New Yorkers coming over from the East coast of FL).

Yes! Whether it’s NY or California, they always ruin everything.

Really? I think it’s more likely private equity that ruins everything.

BP……Agree and just getting bigger and stronger. Most of the ridiculous wealth gap money is in PE…..good luck unravelling who owns what……the ultra rich don’t like that…….and now they have their second lower class wrecker in….as if pulling off Fin Crisis without any problems wasn’t enough.

Legacy condos 3+ stories and 30> y/o on the water have screwed themselves. It’s a corrosive environment and the owners are reaping all those years of waiving reserves in their budgets, kicking the can down the road, until it’s the size of a pop top (anyone remember them). They are all grasshoppers, not ants, and have the gall to ask for “relief” from the state in the form of no interest loans. The idiots in the legislature have reacted, as they always do, with ridiculous mandates to keep reserves. Why not require full disclosure of all condo financials, budgets, and minutes of meetings? The market can figure out what condos are “worth.” You can do due diligence on stocks, you can find out more about a $10,000 car than you can on a $800k condo. Disgusting. The most opaque “asset” you can buy.

This is exciting but kind of terrifying at the same time.

So many empty boxes, so many delusional sellers with dollar signs in their eyes, so much propaganda, so much herd behavior.

If and when we actually get the spectacular, secular implosion of the residential housing market we’ve all been waiting for, the unified screams for another gargantuan bailout will be deafening.

Tens of millions of bagholders and Chicken Littles becrying the end of the global economy as we know it because of a simple 40% drawdown in bubble valuations…all demanding Big Daddy Government to socialize their losses, or armageddon shall commence.

The “millions of bag holders” eat their losses. The 10’s of big banks get bailed out.

75% of all residential first mortgages (and a large amount of second home mortgages) are backed by Fannie, Freddy, or a GSE. How in the world did that happen? /s

I hope we learned from 2008. The subsequent asset bubble blown by the Fed with QE was the worst policy blunder of my lifetime, for sure. We are looking at 2 decades of extreme price distortion thanks to Bernanke’s Folly. Let’s please never do that again.

QE brought extreme price distortion and a market that can’t be broken (until it finally cracks).

I’m convinced nothing will kill this market. It just keeps going up with no basis in reality.

You are completely right, but I’m afraid we as a society have learned absolutely nothing, except to double and triple down on those failed policies, as david just suggested.

https://www.isi.edu/news/69838/cleanroom-course-offers-a-gateway-to-microelectronics-careers/

Here’s your upbeat “better jobs coming” in Hi-Tech, Wolf.

But I DO realize you just run your Biz and dial in clientele………just call it FYI

Thanks for letting me post a bit and especially share stuff with Dustoff…..I’m invalid pretty much, and it’s something to do…….

Wolf’s adult day care center! Don’t get mad…I HAVE and DO learn a lot and this is as good a place to watch things go to hell in the economic and sociology sense as any.

Like I said, only social media…..hell I even bank at the bank and pay bills with mail…..mostly study from what and where and how we got here….just want to “Know” as much as I can.

Thanks for putting up Bacon stuff…might help someone think better.

Guess there is always hope….but shit……..seems pretty bad times…..

Sorry again for attitude….life WILL go on no matter if mankind does or not…….

Guess you didn’t read 2 week (some may even do all 6 and be head “fry cook”) “Fast Food” level jobs/pay training like I did……there’s a reason they do this stuff where a slave class is maintained…robots can’t do it all…these guys won’t know shit except they will get carpel tunnel from repetitive motions and take home survival wage…will never own anything…..never be debt free…..IF two or more people work in an apartment.

Yeah, some may advance…..to equiv of McDonalds shift mgr (or even shop mgr?) or even move up corp ladder a bit….but how many do at a Fast Food place?

That’s like Rubio/Cruz saying just learn to weld and forget all else….we’ll deal wit it…

You ever welded….it’s nasty…..art to it, but 8 hrs a day? Same damned things usually over and over?

Some guys used to get their OWN little 1 man shops, and with lots of certs and a good rep could get by pretty well doing custom stuff……but few still do.

1st 2 weeks allows you to clean and push carts around inside the clean room.

And live in packed dorms like Fox-Conn girls did in China…..at first.

But what about here?

This is beginning to look like a giant game of Musical Chairs. At some point the music is going to stop playing and people will have to take real losses.

People=corporations right?

Or does that only work in one direction…

Everyone see the problem now?

WB – …I’m afraid it does, and I do, as they have the citizen’s right of ‘free speech’, but not the obligation to being drafted…

may we all find a better day.

As my friends in BC say, when they can face capital punishment THEN they are people….or the draft……

I saw where the contractors are going to start fixing a LOT more military gear they make…(someone instructed Trump and the stupid ex talk show jerk)……nothing new…maybe some pork, too….but the very poor and a few macho types are all that enlist…..not too smart or just poorly public school educated…don’t learn well…..still good for most combat arms….mostly infantry. We are pretty good at running small contained wars/killing now, anyway.

Had a buddy that fixed helicopters in Thailand for a contractor…he was smart…after his two years….one fixing them in country…..said nothing but Hash, good scotch, and plenty women……using GOOD PAY……had great times…maybe 2 years.

Retired auto mechanic now.

A town in my area had a ballot issue that would have allowed LLCs and businesses to vote in the general elections.

It was heartily defeated. I think people have ALWAYS seen the problem, but the SCOTUS is no democracy. No one is above lobbying

Remember when that was the worst SCOTUS ruling ever? I’m glad the Democrats passed legislation to remedy that abomination. Rather than wait until it benefited them – as it does now that they receive the majority of corporate support – and make no effort to change it. /s

So since the Republicans have both houses of Congress, the Executive and an ideologically biased Supreme Court that favors whatever the general Republican leadership wants, they will surely fix this and undo Citizens United, right? Because if this is something that predominantly benefits the Democrats then this would be an easy win. I would love to see the Republicans actually vote to get money out of politics, but we both know that will never happen lmao.

Just look at the ideological leanings of the Justices who supported Citizens United. Not to mention how Mitch McConnell praised it.

Mirage, Citizens United is gold, pure gold for all of the string-pullers in “the Uniparty” along with the consultants and lobbyists at the trough.

Neither the Elephants nor the Donkeys are ever letting that golden shower end. EVER.

Corporations ate actually associations of people…

kra – … a REALLY-funny/true typo(?)…

may we all find a better day.

Dustoff,

Good catch. Take care.

If they’re refusing to sell they’re not sellers and they’re not in the market.

I wouldn’t necessarily say that. A lot of them are definitely “If someone is willing to pay me peak 2022 pricing for my house, I’ll sell so that I can take the profit and buy a similarly overpriced house that I have my eye on” people.

But they’re not actually intending on selling. Hopefully at some point, these people permanently take their lists down so that what’s left on the market actually represents people who are sellers at today’s prices.

Lmao. Keep thinking that way. Bagholder

I wonder what influence Georgia Congresswoman Marjorie Taylor Green’s House bill might have on the residential real estate market if it were to somehow get signed in to law?? Would it perhaps influence sellers to reduce prices knowing they’re not going to take a capital gains hit on the sale of their primary residence…for those who own homes that have appreciated over the years??

https://greene.house.gov/news/documentsingle.aspx?DocumentID=1125

There was some conversation in comments section of another WS RE article about “House Humping”, coined by a flaming bird.

Subsequently found a RE ad from 1925 for Frederick, MD, written in olde-timey language:

“THERE IS A DIFFERENCE between the man who applies his rent toward the purchase of a home and the man who pays for a home, but never owns one.

“Which, after all, is not so much a difference in men, as a difference in vision and determination…”

It goes on melodramatically, and painfully written, for many long paragraphs. I guess realtors really are to blame for at least the last 100 years?

Yup house humping and I didn’t come up with that term, check around doctor housing bubble and when it was active, you see that term used a lot.

Realtors are not alone to blame, give a bigger blame to the FED instead, below statement is why and why so many have the utmost contempt for who’s in charge there now.

“not because homebuilders hadn’t built enough homes, and not because there was a “housing shortage” or whatever, but because there was an extra-special buying-frenzy, driven by the Fed’s reckless monetary policies”

Yes and what happened 4 years later?

Sales price in Miami Beach is 10-30% below ask. At least I paid 30% below ask for a house I’m renting out right now to a couple that moved down from Maryland.

If you want to sell a vacation home, I estimate you will pay 25 percent of any profits in real estate fees, moving costs, federal gains and state taxes on any profit you make. Here is the point, you can not afford to move, what is left is no enough to buy nearly what you had. We need the old 1031 tax break reinstituted for homeowners. This would help us all to move around the USA, and no hold on to our unused homes.

The $500,000 exemption, for couples, was supposed to replace the 1031 for residential, and for most people, they’re better off.

Finally seeing signs of a letup in NW NJ. 4 new builds in a neighborhood just got cut from 789 to 689, most used homes now taking price cuts.

As Wolf has pointed out, on several occasions, and backed with data. Greenspan’s move to keep rates low set the stage for housing crisis #1 and to some extent the great financial FRAUD (call it what it really was already). The Fed continues to be the greatest enabler of bad behavior, mostly by congress. No surprise their charter is never in question.

It home ownership going away for the majority of the population? I have seen first hand how the average person takes care of a rental property.

Interesting times.

Renters run the gamut.

On the low end, I heard of a young couple who started a dog rescue operation in a rented home. They had six anxious dogs in there, peeing all over the carpets and gnawing on the woodwork for three months before the landlord found out. Home was trashed.

i remodeled & took care of 4 rental properties in so cal for well over 20 years (not mine), lived in one of them for 20yrs.. the places either got trashed or only needed cleaning and touch up, not much in between. had maybe 4 good tenants, 8 or 10 times units needed full paint/floors/ holes in walls, stuff destroyed, drama, legal issues.. conclusion, fully 2/3 of people suck as renters/ neighbors …

…perhaps another indicator of the nation’s social fabric’s unravelling (…Clinton’s admin’s economic policies, and I think even W., perceived this with his own, anemic public efforts at expanding an ‘ownership society’, though the percentage that actually devolved to ‘the people’ appears inverted…).

may we all find a better day.

When dumb down public is purposely designed, follow who benefits from this nonsense, it is very clear why middle class is squeezed. History always repeats itself just not in exact presentation. Human behavior is driven by factors that can be explained bio-logically not logically. No wonder majority will do what actually harm them in the long run or even in the short term. Such irrational behavior from all groups realtors & buyers alike are enabled & encouraged because ultimately the higher housing prices means higher mortgage so the more borrowed the merrier for … true free market factors into irrational behavior but will be punished when it is wrong … this is why the greatest generation is the ones who saw as children the 1929 great depression or personally experienced as teenagers … they are dying … less & less will remember … are we in true free market? Housing market since 2020 reveals a lot beyond supply/demand in housing market, beyond the concept disposable income & allocation of such & income … & not even pure consumer psychology …

Wolf, minor typo, paragraph under the first chart, says “where buyers held on to their vacant homes”, probably should be “sellers”

…or not. I see what you meant now. Sorry!

Thanks. That “buyer” was actually correct but the whole sentence was badly phrased. This is the new version: “…where people, who’d just bought a home and moved into it, held on to their now vacant home, instead of putting it on the market…”

As Wolf points out especially during the free money days about vacant homes and lack of inventory vs a home shortage media realtor hype .

I live in east Texas and have a married neighbor that is 73 and has a condo in Destin Fl. He wants to sell after buying a 200k Class B Sprinter camper in 2024. He travels to the beach 6 times a year for a week (6 weeks total) Had plenty of money but not extravagant (no kids two spouses)

He wants to sell but has not listed because of lack of sales . He is waiting for interest rates to drop . He should look at the data Wolf publishes and realize that we are in a normal Mtg Rate environment .

His HOA dues are 1000 a month . No idea what his insurance and monthly costs are plus commuter costs to go there 42 nights.

Possible scenario

(Low price sale today ) 250k he wants 400k

2000 a month holding costs

Unrealized interest cost 12 k invested in a 10 year tbill

36 k holding costs annualized

Something around 750 USD a night 42 nights

Lots of money floating around for retirees

I don’t man, two spouses sound extravagant…

No kidding. 200k for a used sprinter is insane.

Before I retired, one of my co-workers and his wife were looking at getting a motor-home, as they did a lot of traveling around the US every year during their vacations, typically 3-4 weeks a year.

We did a cost benefit analysis (we are both engineers), and it was more expensive than just renting a very nice hotel room every night (150-200$). The only way it worked economically was if they lived in it full time or traveled an insane amount every year.

I know several people who have bought motor homes after retirement, and after 2-3 years realize they are not using it enough to justify it. They then sell at a big loss (those suckers depreciate fast).

I know a couple who bought a motor home shortly after they sold their house. I think it was one of the contributing factors to their divorce.

A couple friends of mine work in RV repair and they don’t recommend buying one unless you’re able to do all the maintenance and repairs yourself. The repair bills run in the tens of thousands and it’s going to be in the shop for weeks to months because they’re so far behind. People who were living in the RV end up spending all their money on a hotel room while waiting.

The shop generally won’t take anything more than 10 years old because you can’t get parts for it. They’re built like crap – it’s all 1x wood framing and particleboard, screwed together, that you then take and vibrate down the road for thousands of miles.

One repair they have a few cases of right now is people towing them at too high a speed on the shitty stock tires. The tire shreds and goes right through the laminated plywood wheel well and destroys the whole kitchen. The other common ones are roof leaks, sometimes from being torn by tree branches, and people hitting poles at gas stations.

Very nice take on RVs —- lol!

He should have been first to panic sell. He’s going to get crushed.

That camper will depreciate faster than the condo

Happy 7,11 or is it 9, 11? Good article, since I live on the sandbar, many homes are for sale in area…if you’re locked in, your locked in, 70 percent of outstanding lines are 5 percent and under…big number…

Here is Sam Diego county the prices are so high that unless you can afford 1.2 million and up for a basic 1300-1600 sq ft home you are out of luck. We are in Oceanside and prices have doubled since 2020. We could not buy our townhome now that we bought in 2021. I am starting to see listings that were bought 1-2 years ago and they are riding the market down. Listing at or below what they paid. On the other hand I am still seeing places that sell over asking. We want to move but are not willing to have an 8k mortgage per month. The whole market is depressing.

“…that sell over asking” is a phrase that should never even be looked at or mentioned because it’s just BS: You put your home on the market for $1.5 million and can’t sell. So you cut the price to $1.4 million and can’t sell, so you delist it, then a month later relist it at $1.3 million and can’t sell. then you delist it again and try to rent it out, but can’t get in rent what you want and so you delist it from the rental market and relist it for sale at $1.2 million. After a month, you sell for $1.21 million, and then everyone hypes the sale as “over asking.” That’s how that works. No one should ever pay any attention to that RE hype BS. People, media outlets, and brokers that pitch that “over asking” are trying to pollute your brain.

The on-off-on the market discussion got me thinking about “rental” listing for houses that are also for sale: house behind me is divorce sale, they are asking top dollar from 2002 (gotta pay those lawyers!). It sits for a couple of months. Gets pulled and relisted at “lower” price of like $25K less, nowhere where it could “move” (they need to reduce by 250K). Been doing this for 6 months.

Last week it was listed for sale AND for rent – and the rent was a stupid amount, like $2500 over comps in the area. Quick query to my favorite AI said that this could be for tax reasons: putting it on rental market is not serious at the high price and they don’t expect real renters, but since it is now a “rental property”, the monthly maintenance costs can now be written off for taxes while they also have it on the market hoping for the all-cash buyer who has no clue of the current market. Does anyone have any idea if this is true because I don’t trust AI output.

Likely not true. Real estate tax losses can not offset wage income. So unless they have income from other passive sources, those losses just accrue.

True but this is still RE’s game and probably will forver be. We could be in the middle of 2008 now, and you’ll still see flyers from them advertising over asking. Case in point, just got a flyer yesteday from a RE agent listing a specific house in Garden Grove, sold for over asking.

Utter digust when I see flyers like that, at least my paper shredder got a good workout from the cardstock used

👍 the 1st thing I go through for any listing is the price history section. If bought before Jan 2020, I go to picture section. If not, move to next home. “Burn baby burn” is what I say when realtors try to push a home @ open house that clearly was bought by speculator. This type of BS happened in 2005-2008. Only realtors & realtor association were not punished so they are doing the same now.

They’re trying to put one “over” on you.

… A wise man once said…. He who panicked first, panicked best. HA! That’s is what the will say someday about the US Dollar.

“If you’re the first one out of the door -it’s not panicking.”

– Margin Call

I’m nowhere near Florida but a huge wave of inventory hit the markets this year and almost none of it has sold. Market says prices are way too high. The funny thing is that my ‘hood is the only place around here where anything has sold, but it’s a small and quiet enclave – and the sellers have had to drop prices at least 50K to move.

It’s hurricane season in Florida. I wonder what the market will look like after the next major storm hits the area? You could see people walking away from their property and handing the keys to the lender.

Hasn’t happened in the last 200-years.

A lot of that happened in 1926 in Florida and that is less than 100 years ago.

Tons of folx with large deposits on new construction walked away and bought similar for half price in last FL crash when prices fell way more than deposit.

Personally inspected two ”ranchers” on canal with sailboat water to gulf asking $900K each in ’06 when auctioned with no reserve in ’09. They fetched $225K.

My bid was going to be their sale price in 1998, $78K.

FL is one hurricane from being uninsurable.

How many are just rolling the dice on insurance coverage? And what if you are insured but half the people in your community are not and will not rebuild? What is your property worth next to vacant lots?

This was my instant reaction to this article — who would choose to buy in a state that is becoming increasingly uninsurable?

What could happen is another 1900 Galvenston hurricane to hit Florida. We’re due. Water temperatures are 4 deg above normal. Who in their right mind would insure properties in low lying areas in Florida. Insurance companies that do will all go bankrupt and not be able to pay out claims. Homeowners will be left with nothing but unpaid mortgage debt.

We sold our “forever” home in 2023.

Not because of panic. But because I could no longer walk up and down the stairs.

We downsized to a Condo that is around half the size of the BUT is all on one level.

Then again, we never have considered our “housing” as investments. They are shelter to us.

I consider my home as an investment – but as a reverse annuity. I understand an annuity as an investment one can purchase that guarantees a fixed income in return. My house is the opposite: in exchange for purchasing my home, I have a fixed housing cost. If it happens to appreciate, that would be nice.

In my sordid youth, I thought of real estate as an investment that could appreciate. I ended up taking a loss on it after I sold it after 5 years. Lesson learned.

Price fixes everything.

“…after one of the craziest and silliest home-price explosions ever.”

As silly as this house price explosion was, this “crypto” explosion is exponentially more stupid. At least you can live in your grotesquely overpriced house. You can’t live in your paper wallet of imaginary digits…..

Dude if I can’t put physical cash in it, its probably not even a real wallet.

Based on the action in Bubble 1, prices for condos in St Pete need to halve from peak to trough. That would put the bottom at about $130,000.

I own a community bank. We do not get bailouts. The largest banks should not get bailouts. The government shouldn’t bailout the homeowners either. The FED should not use the situation in this post to lower rates, or any other action. The market will eventually correct this situation. Let the losses fall where they may

You will never get Powell’s job.

CB,

Still think the Market is a diety, huh? Then show it some respect and capitalize it’s name.

His hands ARE still generally invisible, though….mostly by choice.

…good’un, NBay. Best!

may we all find a better day.

After the last market crash in 2009 a lot of Canadians rushed in to buy homes and condos. Prices were right and exchange rates were favorable. Now with all the politcal rhetoric, and prices and rates where they are… Canadians are staying far, far away from investing. I’m assuming a large portion of the listings are Canadians.

That was one of the last waves of retirees from Canada. Now most of the baby boomers in Canada are retired already.

So, they are going to enjoy the winters in Canada?

I suspect these folk are all talk no action.

I personally know several sellers (in both Florida and Texas). That’s anecdotal, I know, but it’s also real.

Apparently airplanes still fly to other sunny destinations NOT in the US, eh?

I am fairly well connected with successful people across Canada, and many or most are either pulling out of property investment in the USA or seriously thinking about it. It’s not just about Trump’s rhetoric, but a slew of reasons that are piling up. They aren’t abandoning the USA completely, they are just taking their money out.

“give a bigger blame to the FED instead, below statement is why and why so many have the utmost contempt for who’s in charge there now.”

The Fed and its ZIRP spawn were the indispensable actors in Bubble 1, Bubble 2 and so on.

I’m sure the Fed would make the excuse that “We can only influence interest rates – if people use ZIRP to speculate on existing assets instead of using ZIRP to create *new* assets (creating both additional labor demand and product supply) there is absolutely *nothing* we can do about it”

Which of course ignores about ten bazillion regulatory strictures the Fed and the G put on essentially every kind of economic activity – but if the TBTF banks want to pimp housing bubbles at ratios that would have been considered insane pre-2003…the Fed can’t do nuttin’ – except create inflation to bail the banks out after the Bubbles inevitably (at this point, *definitionally*…) blow up in their faces.

All this could have been seen by 2000-f’ing 4…but the Fed has spent the last 21 years telling us how lucky we are to have them centrally mis-managing the economy for us and empowering the compulsive, pathological spending habits of the G.

When you buy in Florida (at rip off prices) you get an added bonus at NO EXTRA charge! The occasional alligators that show up on your front step or back patio come at no additional charge.

HOWEVER, if you’re not careful, they may end up costing you an arm and/or a leg.

Or a dog…

Kudlow is acting like the Fed, Powell is the bad guy with the Fed sitting on 1.1 trillion in unrealized losses after directly buying Treasury debt and mbs…so much misdirection and theater like they all aren’t on the same page behind closed doors…amazing really like they speak in tongues…and this renovation contract..and paying interest on bank reserves…what, they can’t wait until May next year…

There are 12 members of the FOMC which makes all interest rate policy decisions and Jerome Powell is just one of those 12 people who have unanimously agreed not to lower their short term interest rates.,

Kudlow needs to go back on opiates and alcohol like when he worked for Reagan.

Some talked to my financial advisor this morning and he said rates are likely coming down in the next 6 months (this was discussion regarding duration I wanted to buy on tbills). But if rates drop in a likely inflationary environment between tariffs are govt spending is it likely that the long end of the yield curve goes up? And mortgage rates increase? Like there’s no data to support cutting right now, if anything the data says we’re pretty close to the neutral rate as is.

Why pay someone to guess for you?

Many years ago I got a call from a New York broker begging for my business. I gave him a small amount to prove his worth. He lost 40% in two months on what he called a conservative options strategy. Then he had the rocks to ask for more of my money.

My phone’s autocorrect is terrible but hopefully that makes sense

No love for Tallanasty metro? :(

I covered the eight biggest metros by population in Florida. There are lots of smaller metros. Tallahassee metro is way down in the list.

Special request Wolf to please add Naples, FL in an upcoming survey. I think it’s not included in the Ft Myers data. Thanks

That metro is too small to be included here. But Naples is included in some of my home price articles:

https://wolfstreet.com/2025/04/22/in-15-bigger-cities-condo-prices-already-10-to-22-5-are-in-florida-with-accelerating-drops-absurdity-comes-unglued/

I live in the Sarasota area, having moved from Denver in late 2021. The prices peaked in the summer of 2022 and have been slowly falling ever since. Homes are still selling when the price is right (that’s a tautology).

I traded one very overpriced home in Denver for another overpriced home in Sarasota. You can still get more house for your money here than in Denver, and falling prices may mean lower property taxes. When I bought in Sarasota, I knew that we were in a bubble (homes were selling in a couple of days with multiple bids etc), but I was not willing to rent for years waiting for the prices to fall back to more affordable levels.

A home is a place to live, not a great investment. Falling prices will help the young. This is not a catastrophe for them.

Rents in Sarasota have not really dropped, $1400 for a basic 1 bedroom apartment is the floor. There is a lot more inventory for sale, but much of it is near busy roads, those always have high turnover. Stock market is still at all time high so that keeps Florida going as well. To me this is just a adjustment of the 2020-2030 real estate growth rate, initial big burst and then a slight decline.

Thanks for sharing the good information.