There was an extra-special spectacle in Q1 among the Swiss franc, Australian dollar, British pound, and Japanese yen.

By Wolf Richter for WOLF STREET.

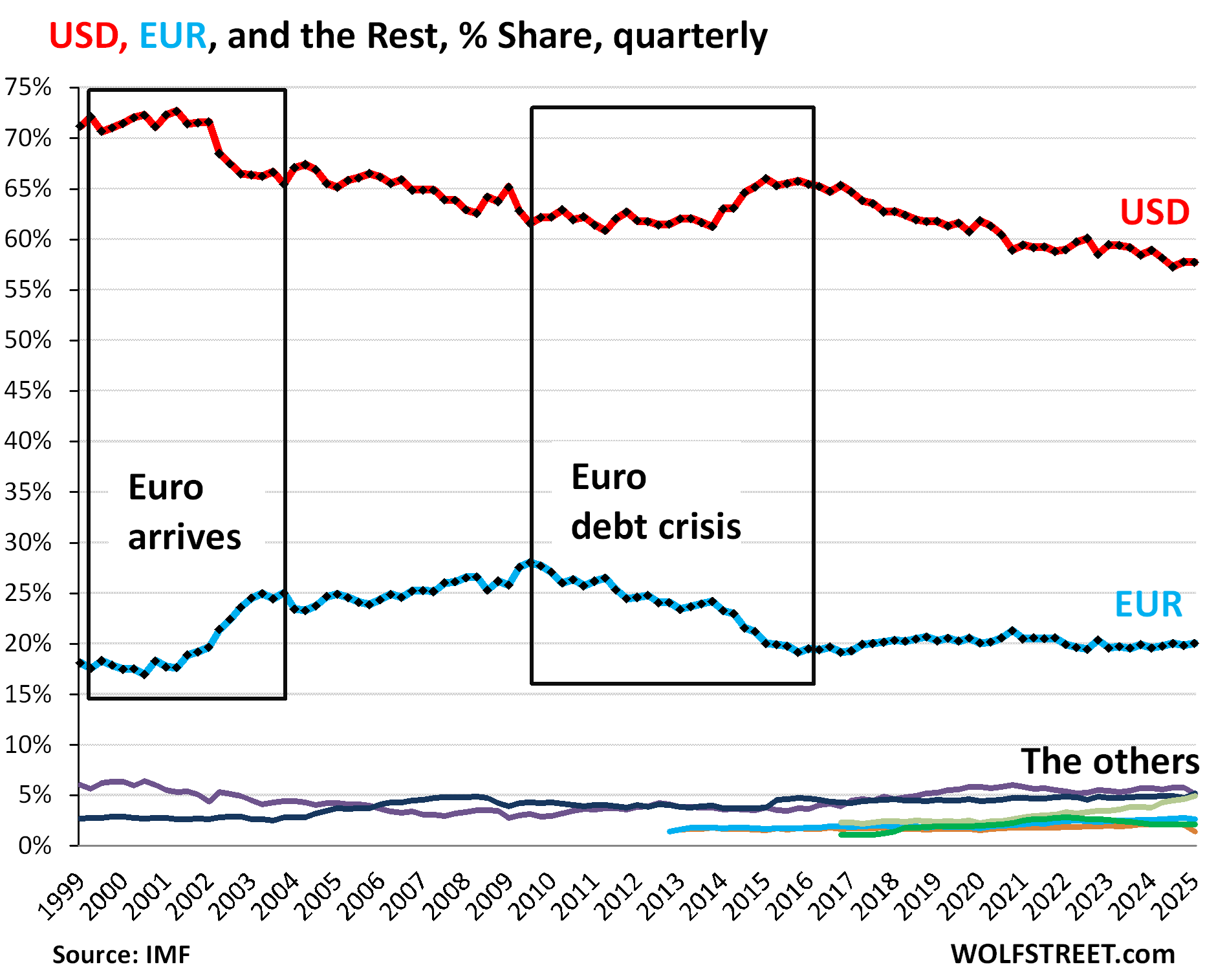

The dollar’s status as dominant foreign exchange-reserve currency has been diminishing for years as central banks have been diversifying to other currencies and over the past three years massively into gold. The decline of the dollar has been slow and halting, a couple of steps forward, one step back, sometimes bigger steps, other times smaller steps, and it remains by far the dominant global reserve currency. But the long-term trend is clear – and this has significant long-term consequences for the US.

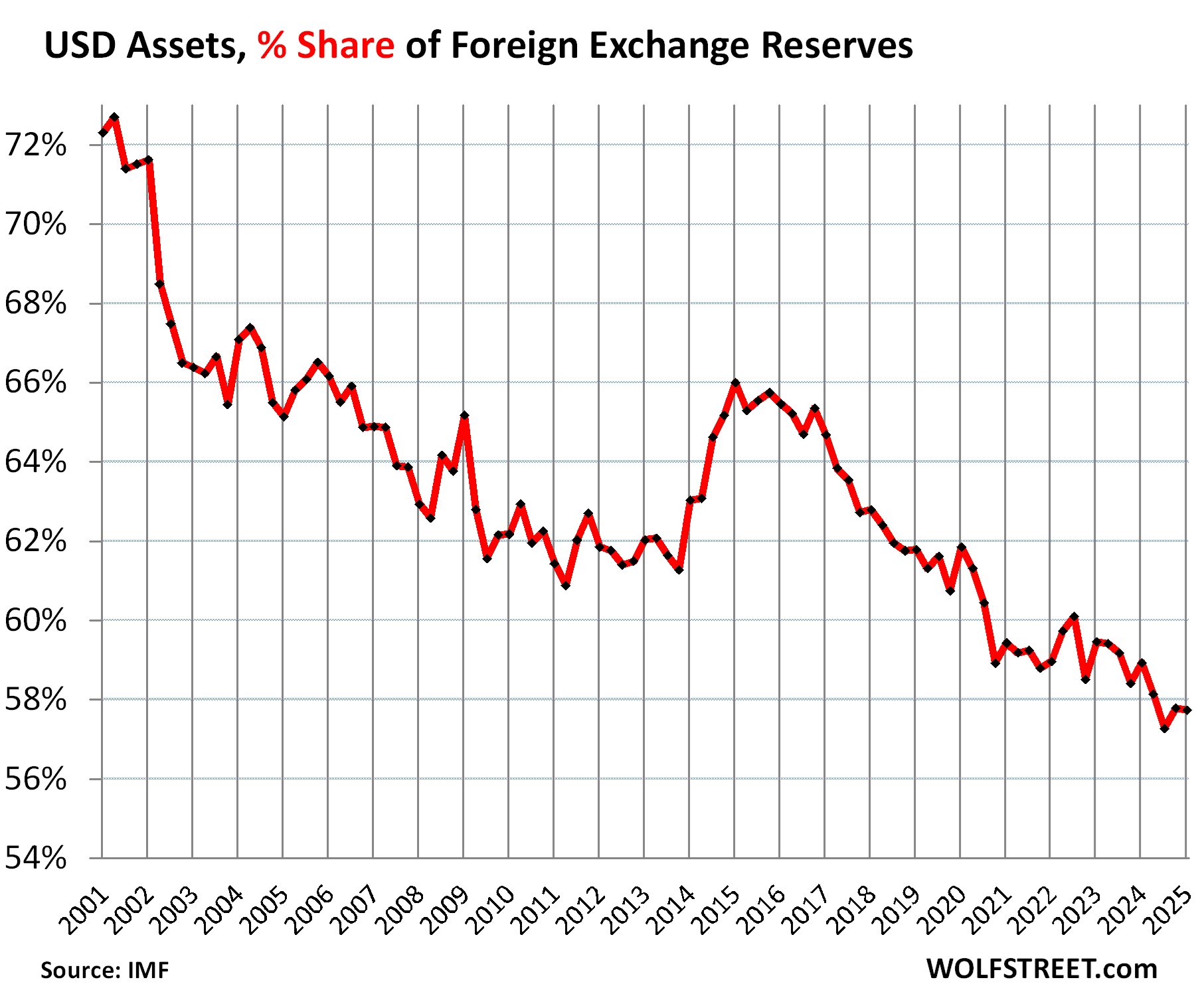

The share of USD-denominated foreign exchange reserves declined to 57.7% of total foreign exchange reserves in Q1, according to IMF’s data today. In Q3 2024, the dollar’s share had dropped to a 30-year low.

The hump starting in 2014 was a result of the Euro Debt Crisis when central banks briefly diversified away from euro securities back into USD securities.

USD-denominated foreign exchange reserves include US Treasury securities, US agency securities, MBS, corporate bonds, and other USD-denominated assets held by central banks other than the Fed.

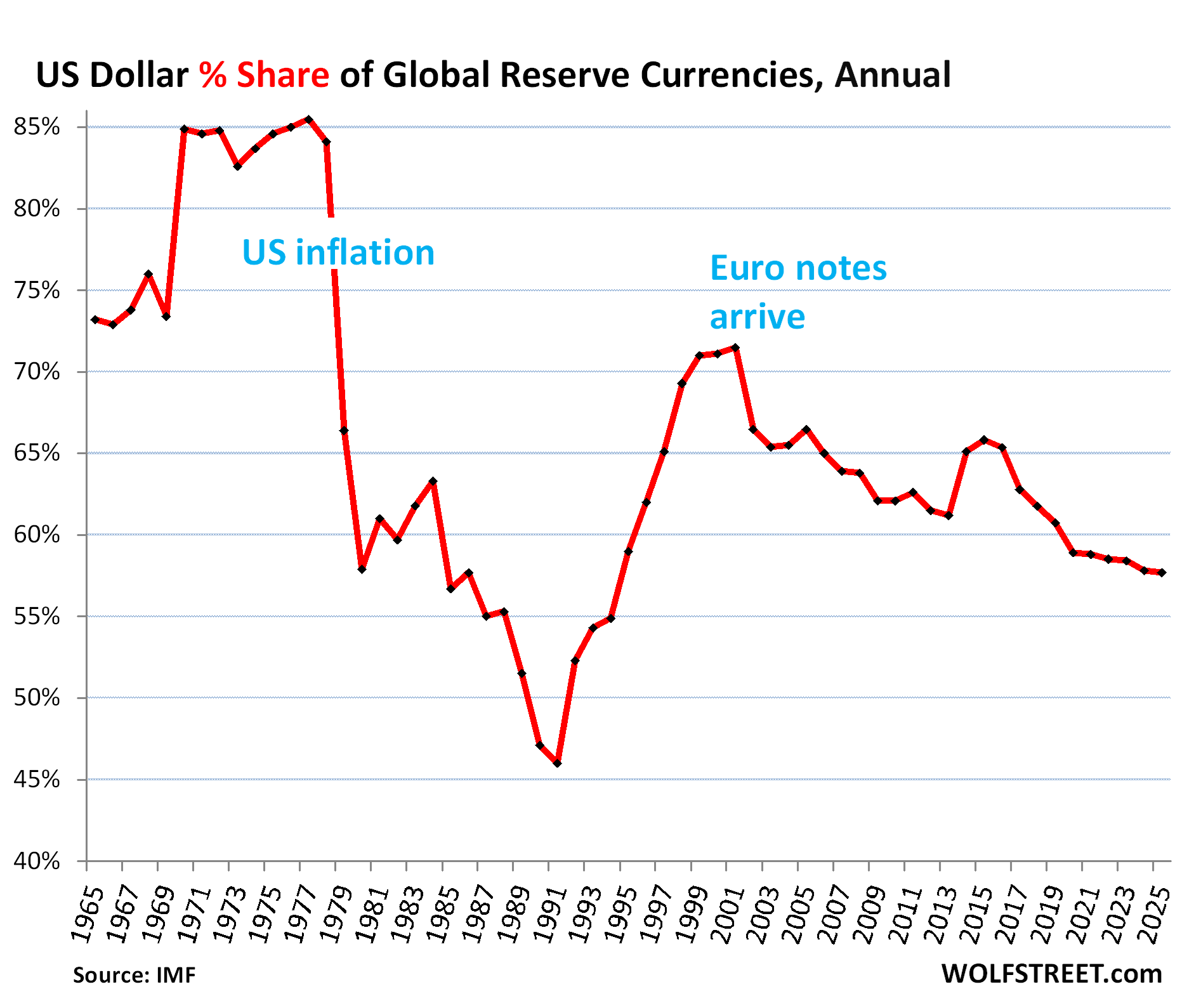

The dollar’s share had plunged to 46% in 1991. At the time, inflation had exploded in the US, and eventually the world lost confidence in the Fed’s ability or willingness to get this inflation under control, and they sought refuge for their foreign exchange reserves somewhere else.

But after inflation had been brought under control, central banks started switching back to dollar-assets, until the arrival of the euro – the first plausible alternative to the dollar until that concept was nixed by the Euro Debt Crisis.

This six-decade chart shows the dollar’s share at the end of each year except 2025 = Q1.

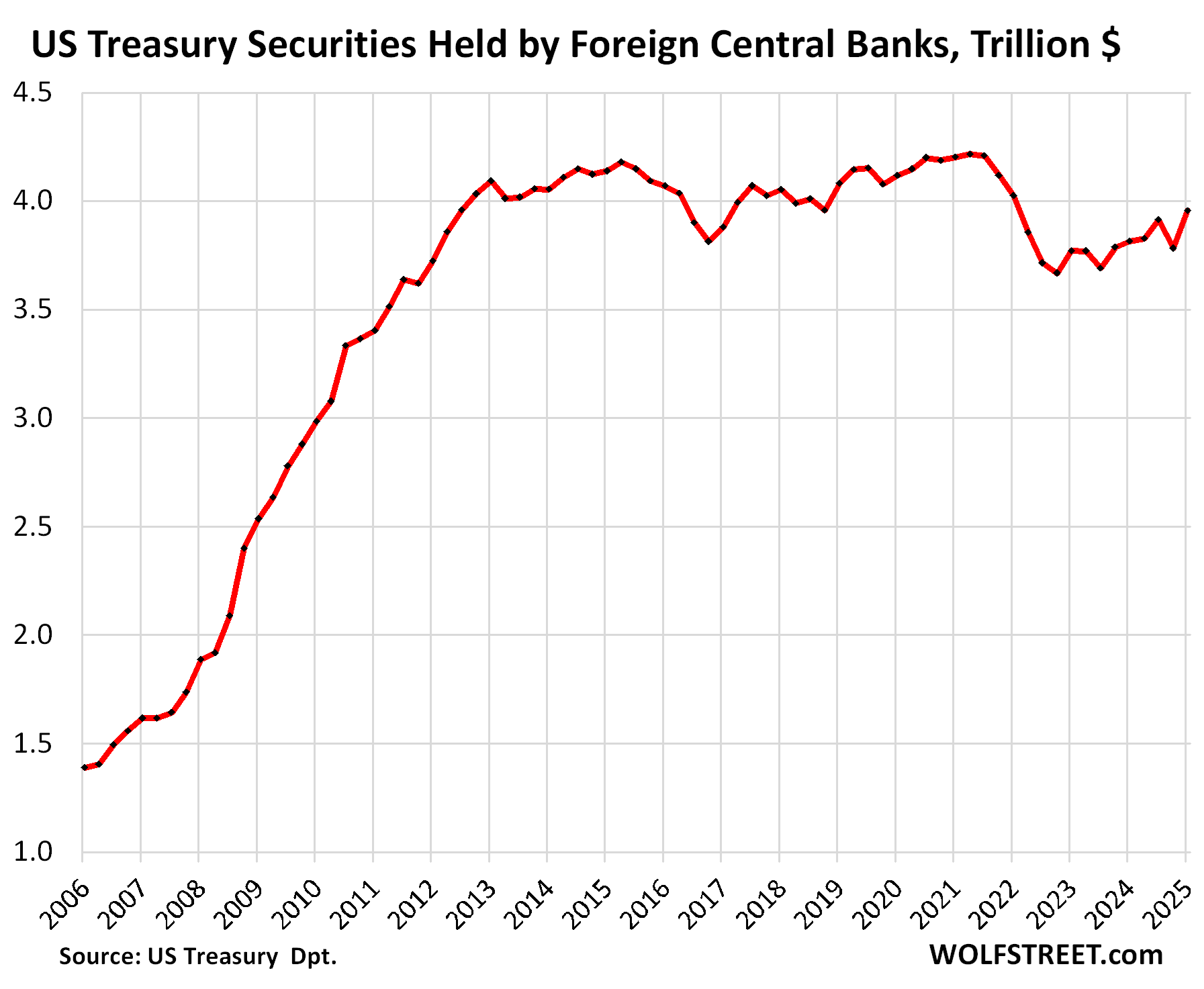

But they didn’t dump US Treasury securities, they just added more other stuff.

In Q1 this year, their holdings of Treasury securities rose to $3.96 trillion, the highest since Q1 2022, but below the high in 2021, and essentially unchanged from 12 years ago, according to the Treasury Department’s data on foreign holders.

These are holdings of Treasury securities, as reported by the Treasury Department, while the USD-denominated foreign exchange reserves reported by the IMF include all USD-denominated securities, from Treasuries to corporate bonds. [Here is our discussion on who overall held US Treasury securities: Who Held or Bought the Huge US Government Debt].

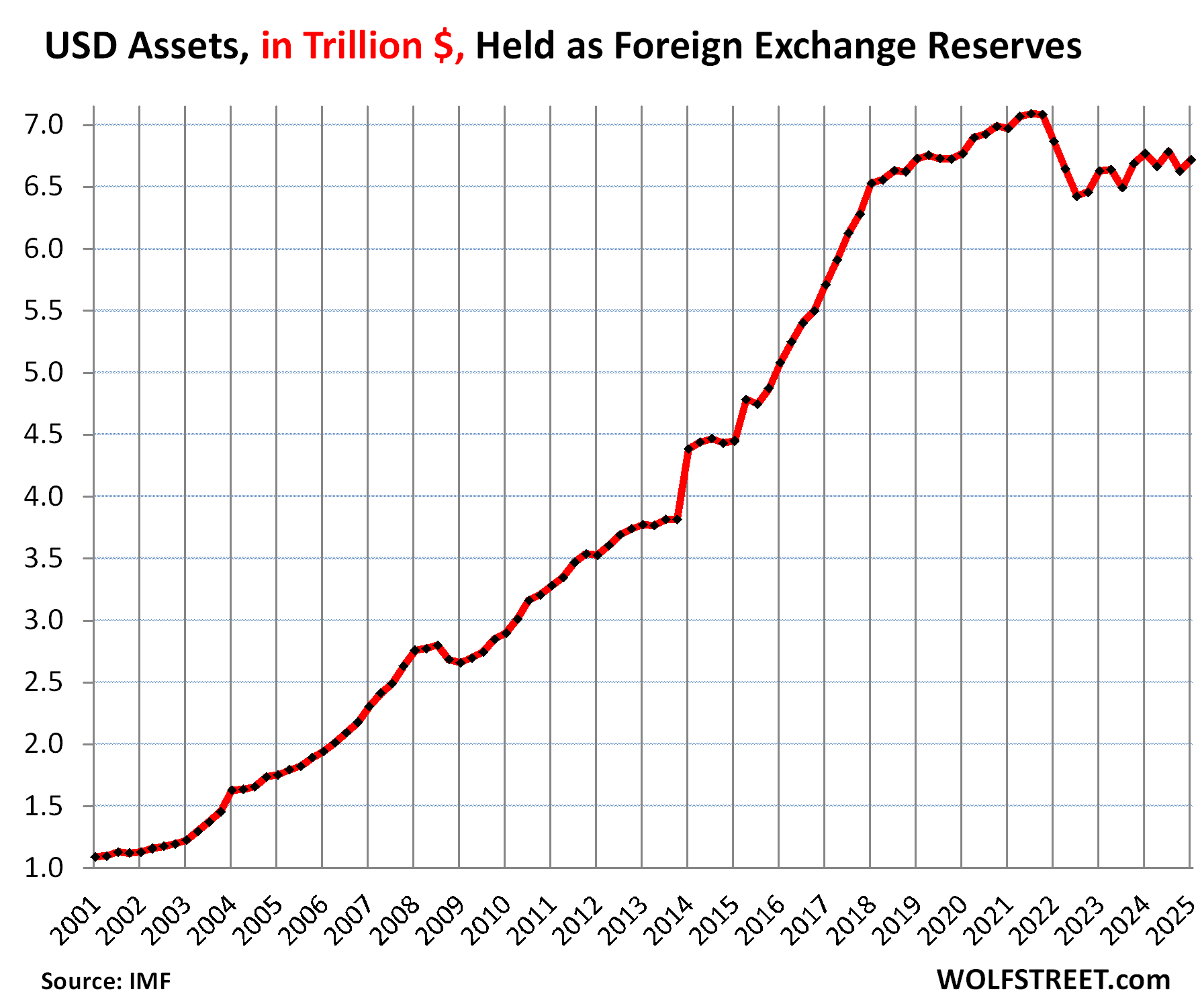

Total holdings of USD-denominated assets as foreign exchange reserves – so US Treasuries, agency securities, MBS, corporate bonds, etc. – rose in Q1 to $6.72 trillion but remain below the high in 2021 of $7.1 trillion and are about level with Q1 2019.

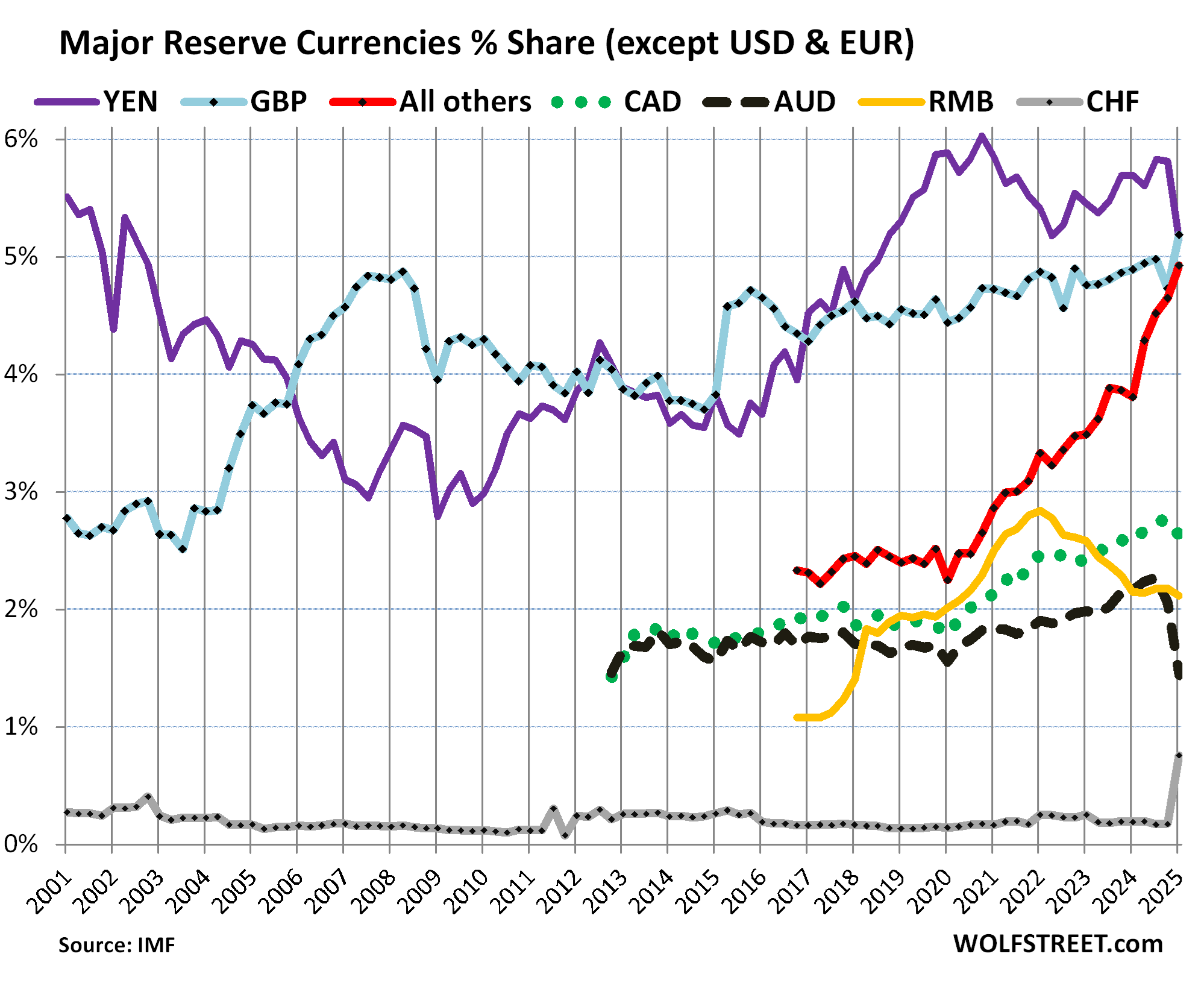

The other reserve currencies.

The euro’s share, #2, ticked up to 20.1%. It has been around 20% for years (blue in the chart below).

The other currencies are the colorful tangle at the bottom of the chart. More on those in a moment. Combined, they have been gaining share over the years, at the expense of the dollar, while the euro’s share has remained roughly stable since 2015.

The colorful tangle at the bottom under the microscope.

Q1 provided an extra-special spectacle there in that tangle at the bottom of the above chart that we now look at under the microscope:

- Spiked: Swiss francs (CHF, gray), pound sterling (GBP, light blue), “other currencies” (red)

- Plunged: Australian dollars (AUD, black dotted), Japanese yen (YEN, purple), Canadian dollars (CAD, green dotted).

This massive shift among these smaller foreign exchange reserves may have had something to do with the huge global shifts of gold in Q1, including massive imports of gold into the US largely from Switzerland. These unprecedented massive imports of gold into the US that blew up the Atlanta Fed’s GDPNow may have also entailed or paralleled large-scale shifts in foreign-currency assets held by central banks.

The category “other currencies” (red in the chart above) is a basket of “nontraditional reserve currencies,” as the IMF calls them, whose combined share has been surging since 2020. That’s really where the action has been, spread across many small reserve currencies.

China is the second largest economy in the world, but the renminbi plays only a small role as a reserve currency. And it has lost ground against the USD and other currencies since 2022, as central banks have not been enamored with RMB-denominated assets for a variety of reasons, including capital controls, convertibility issues, and other issues.

Far behind the USD and the EUR, the largest currencies by share (chart above):

- British pound, 5.2% (GBP, blue).

- Japanese yen, 5.1% (YEN, purple).

- “All other currencies” combined, 4.9% (red).

- Canadian dollar, 2.6% (green dotted).

- Australian dollar, 1.4% (black dotted), down from 2.1% in Q4.

- Chinese renminbi, 2.1% (red).

- Swiss franc, 0.8% (gray), up from 0.2% in Q4.

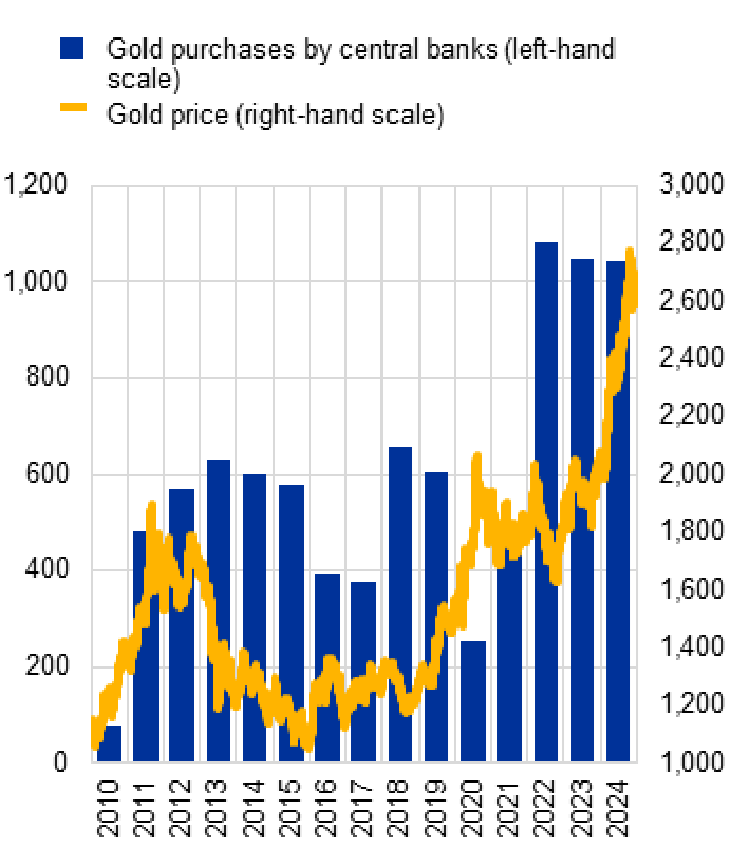

The diversification into gold.

Gold bullion is not a “foreign exchange reserve” asset of central banks, and is not included in the data above. But both, gold and “foreign exchange reserves,” are “reserve assets” that central banks hold.

In 2011, central banks started rebuilding their gold holdings, after having spent decades unloading them. Then in 2022, 2023, and 2024, they suddenly bought gold at a record pace, over 1,000 tonnes of gold per year, double the average of the prior 10 years. And the price of gold spiked from this dramatic buying pressure.

These purchases of over 1,000 tonnes of gold per year for three years in a row pushed up total gold holdings by central banks to 36,000 tonnes, close to the all-time high of 38,000 tonnes in 1965 during the Bretton Woods era, according to an ECB report, citing data from the World Gold Council.

The chart from the ECB shows purchases in tonnes per year (blue columns, left scale) and the price of gold through 2024 (yellow line, right scale, $ per troy ounce):

The ECB’s report adds:

“With the price of gold reaching new highs, the share of gold in global foreign reserves at market prices, at 20%, surpassed the share of the euro (16%).

“Survey data suggest that two-thirds of central banks invested in gold for purposes of diversification, while two-fifths did so as protection against geopolitical risk.

“The share of gold in total official foreign reserves – comprising foreign exchange and gold holdings – increased to 20% at the end of 2024, surpassing that of euro, on the back of historically high gold prices and purchases.

“Surveys suggest that hedging motivated by economic and geopolitical factors played a role in these historically large purchases of gold, notably in emerging and developing economies.

“Countries that are geopolitically distant from the West have been active diversifiers into gold.”

Why is the dollar’s status as global reserve currency important?

Central banks other than the Fed have purchased $6.7 trillion in dollar-denominated financial assets, largely US Treasury securities. This money flow into the US has helped the US fund its twin deficits – the huge trade deficit and the even huger budget deficit – and thereby has enabled the US to incur those two deficits.

The dollar status as the dominant reserve currency has been crucial for the US, it has enabled the US to live beyond its means. As that dominance declines slowly — two steps forward, one step back — all kinds of risks pile up ever so slowly, including the sustainability of the government deficits and the debt.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, The Fed, unlike many central banks, owns zero gold. It has thus misssed the big gold rally. Do you know if the Fed can legally own gold now? It couldn’t after the Gold Reserve Act of 1934, but that act’s provisions were mostly repealed in 1974. I have tried without success to get the Fed to answer the question whether it could buy and hold gold now, if it wanted to. Maybe you know the answer? All the best, Alex

1. The Gold Reserve Act of 1934 required the Fed to transfer ownership of its gold to the Department of the Treasury. In return, the Treasury issued gold certificates to the Fed for the amount of gold transferred at what was back then the statutory price for gold held by the Treasury. Fed’s gold certificates are still priced at $42.22 per troy ounce (in total $11.04 billion book value on the Fed’s balance sheet, or about $850 billion market value if the Fed could cash them in, which it can’t).

2. The Fed is in charge of monetary policy (interest rates) and the stability of the banking system, and gold is irrelevant to the Fed for those purposes. I know that gold bugs would love for the Fed to print trillions of USD to buy gold with them, so you have the combo of money printing and gold buying by the Fed, and gold bugs have serial climaxes over that illusion because it would blow the price of gold out the wazoo, and the gold bugs would get rich, but it’s just nonsense for the Fed to do that, and everyone knows it. I don’t understand why this keeps coming up.

3. If you want the Fed to print money to buy gold, you need to talk to your congressman and tell them to change the law.

Isn’t that what the Lummis Bitcoin bill does? Revalue the gold certificates from $42.22 to current market value.

I think she intends to bring this a vote in August.

Under this bill, the gain on the price of gold would all go to the Treasury, not to the Fed.

You’re right that the Fed’s gold certificates cannot ever be worth more than $11 billion–they convey no interest in gold’s market price, as was carefully designed in 1934. I am not asking whether the Fed SHOULD own gold, but whether under current law it is able to. Thought you might know, I don’t. The Fed was required to own gold in 1913. Forbidden in 1934. Most Depression era gold restraints were removed in 1974. What is the legal situation now? Would it take a new law for the Fed again to own gold? Or not? By the way, really nice essay on the dollar and international reserves.

The FED and Treasury both are probably utterly committed to never admitting to any monetary role for GOLD.

They are 100% committed to USD and it’s current role. How could they not be. I don’t believe that the BITCOIN bill has any chance of passage. The GENIUS act is in reconciliation because that is viewed as safe for USD with a plan/hope to have it be a platform for supporting US debt.

It may become necessary sometime in the future to “back” USD with some asset. It wont we gold. It might possibly be BitCoin if Treasury and FED feel they can tame it.

Looking at a recent heatmap of where BitCoin mining is not concentrated, I was surprised that the US and Europe are now the big centers. It used to be China and there is still a significant presence there, but it’s share seems to be declining.

The US credit card is still ours and looks to remain usable for the next several years. Given the velocity of events today, who can reliably look much further out than 5 years.

The real unknown is our seeming obsession with forcing Russia and China into a corner where war seems to them to be the only way out.

@danf51: Bitcoin is like owning gold without the gold.

Regarding Russia and China, your comment assumes that defending oneself against aggression from X is somehow “forcing” X. That’s only true in the sense of trying to force them to stop their aggression.

Interesting. I’ve always believed, for many meny decades now, that the Federal Reserve Bank of NY had a big pile of gold in their vault, right under Liberty Street. Of course JP Morgan Chase is on the other side of the road and they share the vault..

Maybe that’s just from the movies. John McClain and all.

That gold belongs to the US Treasury and others. The New York Fed just acts as the custodian of it.

I’ve known people who have worked at the Fed who have gotten to go down there. You have to wear special shoes, because each bar weighs 28 pounds and would break your toes if one was dropped on you without protection.

“Of course JP Morgan Chase is on the other side of the road and they share the vault..”

From the St. Louis Fed site: “”So is the Fed private or public? The answer is both. While the Board of Governors is an independent government agency, the Federal Reserve Banks are set up like private corporations … Member banks also elect six of the nine members of each Reserve Bank’s board of directors.”

I was part of a small private tour of the NY Fed gold vault in, probably, summer 2004. It was arranged by a Fed employee. Garage-sized compartments there, most with chain-link front “garage doors” and the gold visible behind it. Over each garage hung a sign with the owning nation’s name. A few large scales throughout and shoe coverings made of steel next to the scales.

Is that what they mean by gold ropes?

Gold being a tier 1 asset, as classified by Basel III, can be used as collateral for banks when trading etc. That being said China(the Yuan) currently on probation with the IMF is an ongoing concern and China has been a net buyer of gold. All the gold they mine stays in China. It is presumed that China may be working towards the Yuan becoming backed “fractionally” by gold. Keep in mind that China has reduced its U.S. Treasury holdings from over $1 Trillion to around $750 Billion. The U.S. needs a new buyer to step up and buy U.S. Treasuries and hopefully it won’t be the Fed. Future interest rates will be the deciding factor. Also keep in mind that there are other countries who owe debt denominated in US $ dollars and can only repay that debt in $ dollars. In other words they can’t repay that debt in their own currencies.

Let’s say you’re Russia and you need to buy computer hardware, chips munitions, etc. and due to sanctions cannot use your own currency, then you need to find an alternative such as oil, gold, or have someone such as China buy it for you using their U.S. $ dollar reserves.

Try this: the USA owns the gold.

I am surprised at least one commenter isn’t having a fit over this news: Central banks loading up on shiny rocks?

Then somewhere there will be the guys wondering why not Bitcoin.

You explain things so well.

20 percent of the S&P 500 value is 3 stocks…the other 497 make up the 80 percent…the fiscal insanity continues until the day of reckoning comes…the corporately controlled media cheers it all on the past 30 years…if they can sanction your holdings anytime in dollar assets, physical gold in your vaults is good and selfish

.

Literally have heard this since 1812

I doubt you have heard anything since 1812.

Woooosh

instead of 25k or 50k rainy day savings fund, this family has 50k to 75k in gold, platinum and palladium.

started buying gold in 2013 around $1200/oz and now it is about $3300/oz. Did we do better than putting it in the bank? (It is easily sold to major online vendors or even the local coin store 12 min drive).

I don’t need a mexican to mow my lawn nor gooish bankster to profit on my savings. very liberating.

I would love to have those assets. one pal bought a big stash of gold quite awhile back, and I applaud his move. But there is always the question of transaction costs, transacting in that stuff daily, especially under conditions of societal stress. You think?

Which 3?

Those assertions are absolutely false and laughably ridiculous.

What percent of revenue, profits and growth are in those 3 stocks?

Total market cap S&P500: $52.5 T

Per Chat GPT:

NVIDIA (~$3.97 T; ~7.3%–7.5% of the S&P 500) – the largest component

2. Microsoft (~$3.74 T; ~7.0%)

3. Apple (~$3.15 T; ~5.8%)

4. Amazon.com (~$2.36 T; ~3.9%)

5. Alphabet (~$2.14 T; ~3.6% including both classes)

6. Meta Platforms (~$1.84 T; ~3.0%)

7. Broadcom (~$1.31 T; ~2.45%)

8. Berkshire Hathaway (~$1.03 T; ~1.7%) ()

9. Tesla (~$953 B; ~1.76%) ()

10. JPMorgan Chase (~$787 B; ~1.54%) ()

Together, these ten firms account for roughly 38% of the total S&P 500’s market cap.

SO, the top 3 do amount to approximately 10/50 trillion (or 20%?)

I like DATA. This is why I like Wolfstreet.

The stupidity involved in the Nvidia bubble is breathtaking.

The entire history of computing more or less consists of ever more clever algorithms *reducing* the demands on (and need for) computing hardware.

And yet Nvidia (“key” hardware engine of the most brute force driven hype cycle in computing history) is allegedly worth $4 trillion just 2 years after the hype cycle began.

(So much for the wisdom of bottomless CAPEX “investment” – MS/FB/Apple – relative to returning excess corporate cash to shareholders)

And only a few months after a Chinese company illustrated how software advances can basically neuter “unavoidable” hardware “demands”.

Greatest valuation bubble in history meets greatest computer chip hype cycle in history.

Right, well it’s been in “bubble” territory for a decade.

I remember a former coworker lamenting that he had missed the boat on it… in 2015.

I am still not on board. Meanwhile, many people have reaped a reward. I feel the same about BTC. I had $1000 when it was $200/coin. I looked into it and it seemed “too complicated” to invest in at the time (I had no investing experience or brokerage account etc.).

At a new ATH this AM, I would be thrilled to own 5 of them. Even if they’re inherently worthless. Ehh, I guess I will just keep going to work.

Let assume :-

Company A data center using Deepseek have installed less powerful Nvidia AI chips

Company B data center using Deepseek have installed with the latest most powerful Nvidia AI chips.

Which one will perform better ?

Which customer will use AI to carry out work, company A or company B ?

Surely must be company B if you want better performance and higher accuracy results.

Conclusion :

Almost all AI training models need most powerful AI chips.

At the moment Nvidia produced the most power AI chips with Taiwan TSMC help using the most advanced semicon chip 3nm node.

So the whole world need Nvidia AI chips to improve performance and accuracy.

China has recently issued some long term bonds to the international market. It will continue to do so over time to increase supply of RMB denominated assets. Maybe this will allow RMB to be used more as a reserve currency.

Not even a little bit.

SoCal,

Why?

Perhaps not due to bond issuance but in the end, doesn’t the nation with the greatest productive capacity become empowered to more-or-less dictate the currency in which it will allow its national exports to be made?

No Yuan in hand = No Chinese exports (2030)

And don’t all countries *want* that currency to be their own – which they can print at will. See, USA.

China uses capital controls in part because it doesn’t want its currency being accumulated elsewhere. By definition for other countries (or for that matter private actors) to accumulate your currency, you must run deficits and pile up debts — it’s an inescapable accounting identity.

As a full time worry wart, my concern is the perception or practice of debasing a currency on one hand, while on the other hand, suggesting various assets have stable value.

This entire debate or observation that the dollar is declining as a reserve currency is predicted on hyping alternative forms of speculation — which is in itself destabilizing.

The commoditization of central bank holdings is becoming a game of speculation and hedge funding — especially with US Treasury so keen to connect itself to *hitcoins and ponzi graft money laundering —- the immediacy of chasing a trend, whether gold or crypto, is far more alluring than actually managing the deficit, to generate long term stability.

With that casino model in mind, the destabilization of the dollar does present global geopolitical dynamics, where various countries will want to diversify away from our mismanaged chaos, and hedge their exposure —- gold is a classic relic to chase, but, I always look at gold (or bitcoin) like inflation —- the cure for high prices, is higher prices.

If everyone continues to chase overvalued assets to ultra extreme bubble limits, this markets will increasingly be illiquid — and held by fewer and fewer entities and less and less profitable to hold — because, ultimately these are Ponzi schemes that eventually blow up.

Yes, there is an exquisite system keeping the US dollar “money-good,” entwined with an insured banking system, that is for that reason bankruptcy-remote. All kinds of substitute claims on other assets, physical, digital or otherwise, including credits in an everyday consumer fintech scheme of whatever kind, in a liquidity/supply crash, fall into legal bankruptcy estates with all kinds of sudden and durable barriers, friction and costs to accessing them, if at all. But I worry that the current administration’s heedlessness to this, and its pumping of “alternatives” with no public information (in fact conflicted interests at play), endangers the most sound and smoothly liquid parts of the whole system. At a certain concentration, might these destabilize the whole credit and commerce system?

…and the scrutiny of the effects of an apparently-unlimited utilization of the ‘do-over’ (and its part in generating ‘different’ outcomes) in the endless-rearing of our child of a species, continues…

may we all find a better day.

Isn’t it curious how foreign buyers are loading up on real estate in places like Athens, Portugal, Amsterdam, Southern Spain, Vancouver, Los Angeles, Seattle, etc. at the same time their central banks are reducing the percentage of their USD and Euro assets? At the same time they’re buying gold?

It’s exactly what would happen if they were to predict inflation in the high-debt Western democracies. And some of those central banks are in the Western democracies!

Do you see any correlation between debt/GDP and the most popular recent reserve currencies?

Gold (priced in USD) appreciated by 24% since start of 2025, so 20% figure that Europen Central bank report quotes must be now 25%.

Wouldn’t it be one step forward, two steps back? Two steps forward and one step back, you’re still making progress.

On the path to no longer being the dominant reserve currency — that’s the direction, and it’s two steps forward and one step back in that direction, see chart number 1.

You and I may not like that, but that’s the direction.

The primary industry that is affected very adversely by the manic and beyond senseless speculation in gold is the jewelry industry which is very substantial in the US, China, India, Thailand, and other places. Gold is now prohibitively priced to use in most jewelry where it was long used and it has just become another massively inflated commodity which enormous room to fall in price as real demand for it dries up.

Spoken like a person with no gold, sadly.

Spoken like a person with no clue, more precisely. I went shopping for the wife just the other day. The jewelry stores have the same selection they always do. The big shift there is lab grown diamonds.

In places like India and China, they just shift to a lower weight alloy, buy shorter chains. Or just buy a few links at a time. They don’t ever stop buying gold.

No, jewelry stores have very little gold jewelry available at all these days. Yes, there is a shift away from mined diamond to labor grown diamonds which are just very boring clear gem stones. JTV is the largest jewelry in the US.

I have some both in numismatics and jewelry and I have no interest at all in bullion of any kind and so little interest in numismatics that I never look at any I have. Gold used artfully in fine jewelry can be attractive and that is its own real true purpose.

If I told you to forget home insurance but buy gold instead with the premium money, when the PP fire came through you’d be very happy. One of my inlaws bought his home there in the it’s. He was one of the 1800 who had insurance canceled 3 months before the fire. Gold is great insurance. He lost everything.

Gold isn’t covered by homeowner or dwelling insurance except for jewelry and certain numismatic coins listed on a separate Valuable Personal Articles endorsement while bullion is never covered at all. I would suggest that you always maintain proper and appropriate insurance levels on all residential property and not engage in speculation in metal with wildly volatile and unstable price levels.

Okay, please explain this for the stupid folks. Gold is great insurance, but your brother-in-law lost everything… So he recovered a molten pile of gold after his house burned down?

It doesn’t make sense because what I pay for insurance over two or three lifetimes will never be enough to build a house.

He bought in the 60’s. His insurance company canceled his policy 3 months before the fire turned his home into ash. Over 1,800 home policies were canceled.

Now IF he had never paid home insurance, and used the money to buy gold…see?

Paper is just paper. Even melted gold retains it’s value. In his case, 60 years of insurance company promises were hollow

BTW, insurance rates are insane in California. Not to mention that many areas are now uninsurable.

” because what I pay for insurance over two or three lifetimes will never be enough to build a house.”

This is actually an interesting question.

Leaving aside the outliers (hurricane Florida, hale Texas, and everything California) I was struck by how (relatively) affordable home insurance is in the US – annual premiums perhaps 1-1.5% of current home values.

(I’m a long time renter – so I only occasionally research the home insurance market)

*But*

Just because your home insurance premiums go *out* to “insure” your “$400k” house…actually clawing anywhere near $400k out of an insurance company might be much harder than it looks.

(In which case, how much “insurance” are you really getting for the very real premiums you paid).

Insurers have many exclusions/claim requirements/process steps/impeding personnel/haggling lawyers all in place to make claiming “full home value” a much iffier proposition than may be commonly thought.

It isn’t that you won’t get *something* paid on a claim – but on a net basis, after an extended period of time, the amount paid out may diverge markedly from what the insured thought he was going to get.

Given the nature of insurance (very regular premium flows in, fairly rare compensation claims paid out) the insurers can profit mightily if they manage to shave 10-20% off the notional amount of “coverage”.

It isn’t an accident that insurers have many steps/personnel in the claims process.

While paying premiums *in* is painless…but microscopically policed post hoc.

correct Cas

we’ve seen it over and over here in Hawaii

They have a million reasons why you shouldn’t get paid

The ultimate one is when they just leave the State

You can always switch from gold to a much cheaper platinum. Has great durability and is perceived by many as more valuable and original than gold.

Silver is also an option.

You can only blame currency debasement.

Platinum ha;s ALWAYS been a much rarer and usually a much more expensive metal than much more common gold. The prices of all metals has nothing whatsoever to do with any ‘currency debasement’ and all metals have no financial relevance whatsoever. They are just commodities – and nothing more.

LoL, “real demand for gold”. It ain’t 1999, duuude.

Cheney kicked this off with “Deficits don’t matter, reward the base(me).”

Jewelry is burning fast. Just wait until the antique dealers pull their crap and send it to the propane gods.

The only real question is if we decide to bring on the pain and reset with the current dollar, or we decide, eff it, reward the base.

Base wins, we lose.

Just keep that in mind. The world you knew is gone, and we are into a new world.

Now, what shape that takes, is yet to be determined.

Jewelry demand, lol. Signet Jewelers all time high was 2015. Every kiss begins with K.

No one told you when to run, you missed the starting gun….

Signet is a very low end jeweler and there is becoming practically no gold jewelry available today for anyone due to the manic speculation in the gold bullion market which is both stupid and destructive.

I do not know where you shop in the hood, Every jewelry store and pawn shop I visit, has a nice selection of gold in most price ranges.

myrrh precious

TACO in charge will only make it sooner and more painfull.

Open markets did more to raise the standard of living for average people, than made in america ever did.

As an average person of an average family for generations including the various immigrants who have joined the family over the last five generations that I know of, I totally disagree BH.

What recent decades of USA being open while other countries, all or almost all others, had tariffs on USA goods, and most still do, ”average people” have suffered an increasingly faster decline of real economic situation while the oligarchy has become even more vastly rich.

Only real difference between oligarchy of USA and other countries is that anyone can join in USA.

You are making the assumption that foreign tariffs on US goods are a primary reason for the bifurcation of wealth and income in the USA. That might have some merit, but I would bet that long-term labor, tax and industrial development policies had a far more devastating impact.

For good or ill, tariffs are a part of “long-term labor, tax and industrial development policies…” No, low, or high tariffs impact all of those things and create winners and losers in the process.

I was upper middle class as a kid in the 1980s and 1990s. We now live in borderline poverty, with abject financial stress, and it has nothing to do with budgeting, avocado toast or coffee. It has everything to do with our groceries, rent and electricity costing 70% of our income and we live in the hood.

That’s been the experience in my family.

but making billionaire richer will solve it I am sure , I guess the trickle down just meant getting pissed on . lets elect an even crazier repub lican to finish us off. . I really wonder who is on the list both sides of the aisle and the clinton and trump are all over it.

People need to stop thinking that their is a simple magical solution to this mess. They need to stop thinking we can get rid of all “entitlements” when those who would lose the most have spent their entire working lives paying for their parents, and now it is their turn.

They need to stop thinking that any solution that doesn’t recognize reality is going to fail, like huge federal budget deficits have a simple solution. Raise and enforce taxes. Further, stop the effing grift of the people by the rich. Universal cheaper healthcare funded by taxes. Assets need to be taxed, instead of allowed to grow to the moon. The one percent own far more than they will ever need, and are taxed less than a working person. Everything else is lies and bs. Houses should get a low occupied tax regime. One person living there, lower tax rate. Otherwise, inwestments pay the more than workers. Crapital gains should be taxed at more than working, not less.

In short, people who work are more important than rentiers. And let the AI enforce and make it fair. Get rid of most of the tax loopholes and preferences. Stop the lies, because we are drowning in them and delusion.

And immigration is the same, and trade is ultimately the same. There is productive cooperation, or there is subsidies and illusions. Nothing is entirely pure, but accepting the overall system needs reform is the first step, and recognizing everyone must pay to make far larger gains in efficiency.

The current system will fail in less than 20 years at this rate, and if more disasters like the BBB come through, it will go faster.Anyone going to fix Medicare and Social Security again with a bipartisan commission?

So, contemplate that if you want to flee. I understand that impulse, but to where? The entire world that takes dollars is now tied together with dollars and euros, and nothing else is available beyond commodities that don’t rot.

I hope your gold is safe in Switzerland, and your house in Dubrovnik is nice.

Or your finca in Cuba doesn’t get confiscated. Or Costa Rica, or Vancouver Canada.

You forgot about a wealth tax. Communists are always good for a little doom porn.

Inflation is the ultimate wealth tax. When you can’t pay the property taxes, because the number is astronomical, oh well. No rule of law means no wealth. Hitler had backers who thought they bought access to contracts. Those Mefo bonds ended up bombed into dust. Unless you got out in time. Ask a Russian oligarch how much money is worth when there are windows everywhere. Or the Alibaba dude.

Stop with ancient shibboleths and open your eyes.

Gold is a reboot insurance, or the ability to not starve.

Assets are already being politically taxed.

Worry about whether you have a buyer for what you need to sell, not what it’s worth in coupons today.

As I pointed out in a recent comment, that 20 plus percent in commodity metals since J20 ain’t growth in end user demand.

You don’t like my conclusions about the system of the world, just wait, it’s gonna get worse.

”It’s the best of times, it’s the worst of times.” ,,,

Each has always been truth for some, and always will be, as in, there is always an ”angle.”

Right now the challenge is to make our USA system more fair for all, instead of the socialism for the rich and the poor and to hell with the middle, especially the middle workers who get up in the morning and go and make and do instead of manipulate and financialize.

WE, in this ALL of USA people, will do it or go down the same drain as almost all former ”societies” that have allowed the oligarchy to continue to enrich without regard to equal rewards for those who make and do…

IMVHO, USA not yet at the extremes of the last few millennia, but getting closer far damn shore.

Spoken like a true follower of Karl Marx ( or, that clown running for mayor of NYC ).

The cult of infinite wealth and growth will find it’s limits. Look at how poor workers are in comparison to where they were decades ago.

Capitalism is great, as a winner. I just understand that trees don’t grow to scrape the lunar regolith.

That last article on California real estate showed stagnation and death of assets. And you just call me a marxist. Ridiculous.

LoL, the kids will vote for socialism, because they don’t believe in your gods of capitalism. Because they see no chance to get what you got handed to you in comparison.

So, they will fix things after the boomers, the way they see fit. The flailing for solutions by our “leadership” is obvious… Stablecoins to prop up the dollar disaster?

LoL.

Fly you fools.

The kids will vote for socialism because they are taught about the “evils of capitalism ” and, listen to fools that talk about “fairness” in the system in which they are brought up ( or, I might say “unfairness” ) having never experienced the “other” systems ( such as the approach you espouse ). People only get “handed” success in those other systems. You sound like someone that demonstrated in the 60s and then landed a teaching career at the U in political economics or some such other endeavor. With capitalism anyone can become a “winner”! Certainly sound like a Marxist to me.

johnbarrt, it’s hilarious that you think the kids need to be “taught about ‘the evils of capitalism.’”

They’re LIVING them thanks to the best part of 50 years of neoliberal “because markets.”

There’s a reason The Gilded Age (not to mention the Ancien Regime before it) ended — wake up!

You lost me at taxing unrealized gains.

How about ever realizing gains?

Warren Buffet told you the class war was over, and his class won. Just read what he wrote, and he is the ultimate winning capitalist. He points out the system is rigged, and states plainly, change the system.

Now, this year nonpandemic! budget deficit is $1.4 trillion, with next year going to be $1.7 trillion. Social Security’s Trust Funds will be empty by 2034.

Like a big cliff for the lemmings? It’s coming faster, not slower.

Seriously this isn’t 1970 “personal responsibility no handouts” vibe anymore. Nowadays there’s no viable system to be “personally responsible” within, and those who argue there is, grew up in an era when buying a house only required showing up to the shop in some slacks and a button down shirt.

For me, the big question is how long can our era of “easy money” last.

History paints a not pretty picture of how these periods end.

The exponential growth of government and private debt is reaching ($37,000 billion.) and appears to be unstoppable.

“What fools these mortals be!”

Learn to use inflation to you advantage.

To be effectively competitive in foreign markets, requires that we sell lower unit costs and higher quality products. This means concentrating on production, innovation, and product quality. It means giving workers a financial stake in increased productivity (share in profits, etc.).

No. It all depends on what the product is. For the US most of the exports are low-end commodities and high-value added good such as planes. The first thing is to know your market for what you are trying to sell. There is no general rule that applies to all markets at all.

Thanks Wolf. Yours was a masterpiece. I enjoyed reading every bit of it. I did not know the Fed is not allowed to hold gold reserves. Can you answer Alex’s question?

“Slight” risk only in the hopes and wishes of those with their heads in the sand in USA and rest of the world who have not been following the degradation of US Navy and other USA forces in Pacific.

China could and likely will just keep on with the gradual take over of the South China Sea and similar for a few more months, and while respecting Philippines temporarily, continue as did Japan prior to WW2.

To consider otherwise is to repeat the hopes of Pacific nations exactly as at that period.

Thank you for your efforts, Wolf. The last article showing how the real estate market is slowing down in California, because the price of houses is too damned high compared to buyer’s income. Solution of pulling houses off the market. Instead of just selling and moving the property. Dead assets paying property taxes and insurance, or renting at a loss versus other inwestments like mediocre treasuries. Houses are done, no meat left for buyers, so the glut will solve the problem through much lower prices. We are 200 basis points away from a totally dead housing market . Just run the math on a 9% 30 year mortgage.

Those will be the biggest losers. The market doesn’t care what your emotional inwestment is, but what a willing buyer will pay. In today’s coupons. Find the market, and sell fast.

Inventory gets stale in real estate, so realize that you need to be in front of the buyers, or get the flippers. Moral of real estate- there are two markets- retail who live in it, and those who sell to them after solving the obvious problems- and getting paid for it.

Real Estate will ALWAYS be for sale and it doesn’t matter to most people how long any house is up for sale. The right buyer for every property will always come around eventually. You sound like a flipper realtor.

Anything will sell if the price is low enough.

NewsWeek: Oil Drilling in US Plummets Under Trump Despite ‘Drill, Baby, Drill’ Promise…

Drillers cut back because the price of oil has collapsed by 40% once again because there’s a glut.

Oil extraction in the Permian is STILL limited by natural gas offtake capacity.

Greenspan made several telling comments about gold. It is and has remained the world’s preferred collateral and reserve currency among the “elite” and central banks. Greenspan had commented on using the gold price as a bellwether for interest rate policy. If the spot price was increasing he knew monetary policy was too loose and visa versa. Things will get very interesting should everyone trading contracts in the metals market suddenly demand physical delivery. Personally I am amazed that commodity trading in general has gone on as long as it has operating as it has. Gold aside, many of these commodities are things every society needs just to maintain their current standard of living, et alone grow.

LOL, his interest rate policy of holding rates too low for too long created the housing bubble that then blew up and caused the mortgage crisis which helped cause the Financial Crisis. I cannot believe how people come up with this stuff.

Exactly my point. Yes, the Fed has been the greatest enabler of BAD BEHAVIOR that the world has known. Maybe it’s time to end their charter. Can’t have it both ways Wolf.

Well, gold remains the preferred collateral, and now officially a “tier one” asset. Gold has, in fact, been revalued overnight by governments, including the U.S. Seems to happen every time a country is abusing the reserve currency status.

Personally, monetary roles aside, I think the whole precious metal commodity complex could get interesting if the corporations/people holding the contracts demand delivery. After all, many of these metals are required simply to maintain the standard of living we enjoy. Think energy generation, electrical grid and numerous other technical applications.

In the very big picture, when examining debt, or wondering why the dollar is being destroyed —- it’s important to realize that someone or various entities, profit from contracts — connected to budget deficits.

Tax payers are providing profit for someone — and that helps explain why deficits don’t matter to a political system that benefits from stealing tax payer funds.

Debt is profitable — and more so now than ever — it’s a perpetual enrichment machine that feeds government contracts.

One can almost understand why DOGE had magnetic universal support — but then, faceplant as the budget and deficit exploded:

“”ICE will now have 13 times its current fiscal budget for detention, which is already operating at a historic high, on top of the funding in ICE’s annual budget that Congress sets each year.”

President Dwight D. Eisenhower’s Farewell Address (1961)

“This conjunction of an immense military establishment and a large arms industry is new in the American experience. . . .Yet we must not fail to comprehend its grave implications. . . . In the councils of government, we must guard against the acquisition of unwarranted influence, whether sought or unsought, by the military-industrial complex. The potential for the disastrous rise of misplaced power exists and will persist.“

I guess no one understood how the government was going to wage war on the dollar?

I think that concern about this issue is vastly overblown. What currency actually COMPETES with the USD as an alternative to be the global reserve currency? We talk about the U.S. dollar declining from 72% at the height of the internet bubble to 59% now… but the Euro has been stuck at 20 to 25% for that entire time period. Absolutely no one wants to hold large sums of the Chinese currency because of all the games that the CCP plays with it.

So what else is there to hold that substitutes for the USD… the Yen, Pound, and/or Swiss Franc? Not a single one of those is capable of being a “GLOBAL Reserve Currency” and everyone knows it. To the extent that the USD has “lost ground” to them (a point or two for each over the past decade)… it has more to do with local conditions (BREXIT, Yen collapse) than central banks actually planning to substitute them for their USD holdings. Combine that with those same Central Banks needing to shore up their assets with Gold and you account for almost the entire loss of the USD’s share since 2016.

PS: Don’t forget the part that politics plays in all of this. As much criticism as the U.S. Federal Reserve comes in for… it is amazing how Americans look at foreigners as apolitical sophisticates with their fingers on the pulse of the global economy… instead of the same political hack economists that we despise in this country. It is hardly an accident that the USD share as a global currency turns downwards every time the Americans elect a conservative government. Should we really expect different from Socialist central bankers in Socialist governments?

“…is that Maytag guy EVER gonna get here? Those shirts in the hamper are getting pretty fragrant…”.

may we all find a better day.

“Purchases” of gold by central banks or any other entity need to be defined. Are they physical bullion delivered and stored locally? Or are they IOUs from a bullion bank, futures contracts on the COMEX, or shares of the SPDR gold “trust” ETF?

Missing the point! The world is changing and will not need one world reserve currancy. Soon we will be able to trade, in many ways faster than we can think. Add to that, much of the world does not trust us or our dollar. Hate might be a better word.

Tariffs protect the weak, just like king dollar protects the banksters.

All the chatter on us gold, just shows a lack of understanding. ANY law can be changed and the price of gold does not matter. It is just what you can get for anything when you go to sell.

If we repriced our gold at 10k an ounce, we would still be broke and need to borrow every year!

How low can we sink, TACO just announced more tariffs on Brasil as he thinks they are not treating one of his friends right!

Good one!

Good one Wolfstreet!

Thank you!!! Just saw that in my inbox!

US do not have to worry about pushing debts to US$50 trillion by 2030.

As long as those new billions printed are used to finance rebuild of some very old American infrastructure and cut military spending by 50%. Build high speed railway systems, hydropower dams, etc.

Debt = $20 trillion > Dow = 21000

Debt = $30 trilliion > Dow = 30000

Debt = $50 trillion > Dow = 50000

U.S. government owns oil and gas resources on and offshore worth $128 trillion, roughly eight times the national debt of the country (2013: Oil price = $101 per barrel )

( or $75 trillion @ $60 per barrel )

Some of this is a reaction around the world to the US increasing addiction to sanctions (their use has exploded over the course of this century) — countries (along with some notoriously rich private actors) are taking out a little insurance should the time come when their $USD assets get frozen or seized. Pile the erratic implementation of the new US tariff regime (and I say this as someone who is NOT at all reflexively opposed to tariffs as an important part of a cogent industrial policy) and you have further incentive for countries to give themselves optionality.

The larger pattern here is that the US is increasingly isolating itself. Whether or not this is for good or ill for US citizens depends a great deal upon the domestic policy of the US; whether or not it’s for good or ill for citizens of other countries depends a great deal upon the international arrangements they create in response, along with alterations in their own domestic affairs — it’s the third great transition of my lifetime, coming as it does after the Nixon Shock and the collapse of Bretton Woods, and the fall of the Soviet Union resulting in the end of the Cold War ushering in a brief period of unipolar US dominance. I am reminded of the Chinese curse: “may you live in interesting times …”

The gain in the Japanese Yen vs the U.S. dollar likely results from the unwinding of cash-and-carry arbitrage when yen loans were at near zero. Steps: borrow yen, sell yen and buy dollars, invest dollars at higher interest rates. Selling yen and buying dollars increases the value of the dollar. As U.S.-Japanese interest rates converge, the reverse happens. Dollars are sold, and Yen is purchased. Thus the selling dollars drops the price of dollars. No market participant is making a bet on the long-term viability of either economy. They see a short term arbitrage opportunity. People have got to stop using Karl Marx as a guide to economic reality.

So what is USD share with gold (and platinum) thrown in?