Companies don’t just suddenly drop everything to stew in their own juices.

By Wolf Richter for WOLF STREET.

Look, the job market hasn’t cratered yet, and doesn’t look like it’s on a path to cratering, despite whatever is happening to federal government jobs and despite all the moaning and groaning in the media and social media about the cracks in the economy, the tariffs, the recession, or whatever. Companies are still doing what they’re supposed to do: taking care of business and chasing after opportunities. They don’t just suddenly drop everything to stew in their own juices.

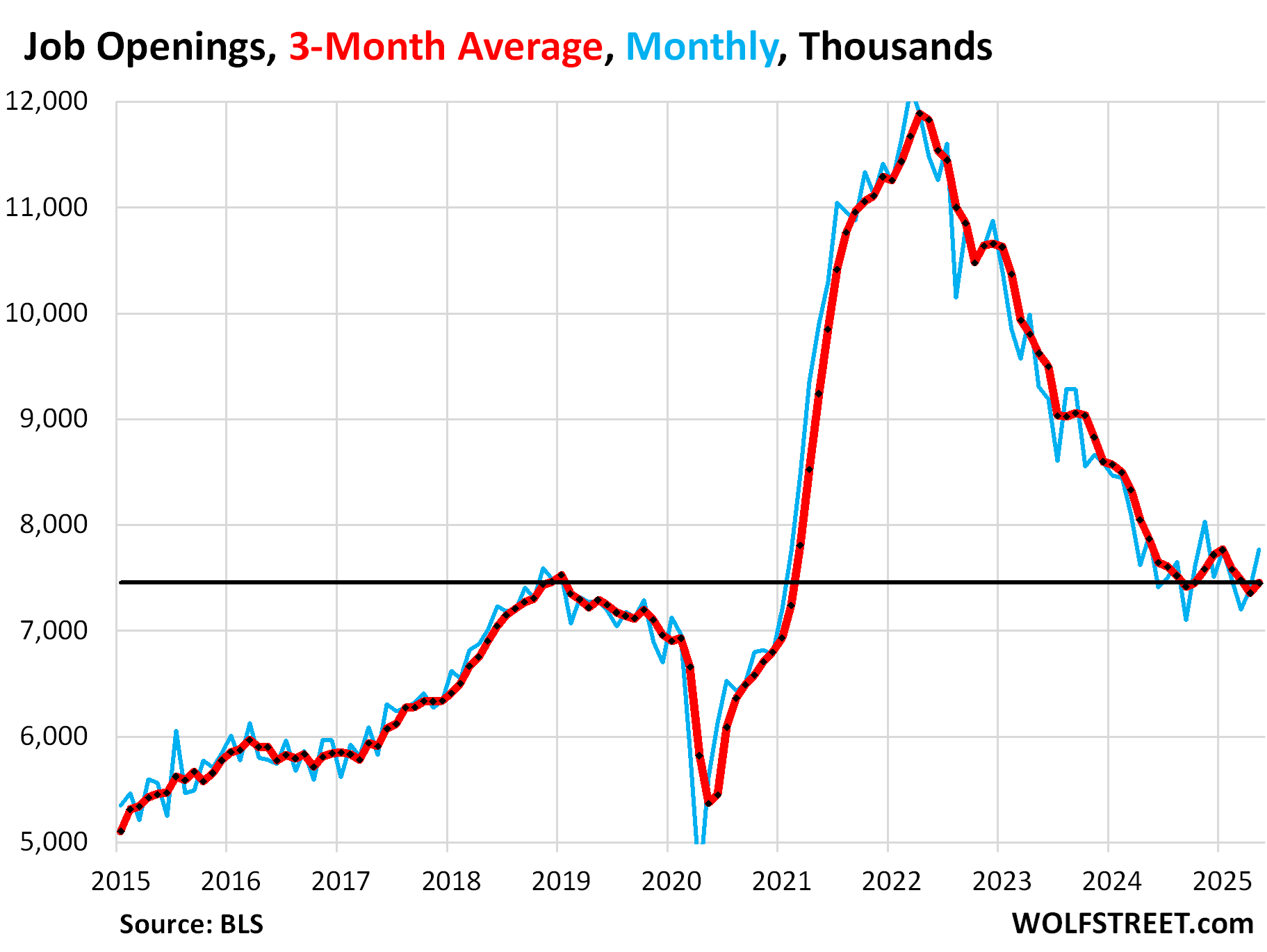

Job openings jumped by 374,000 in May from April, to 7.77 million, seasonally adjusted, the highest since November 2024, and the second highest since May 2024, and well above the high of the pre-pandemic Good Times (blue in the chart), according to today’s Job Openings and Labor Turnover Survey (JOLTS) by the Bureau of Labor Statistics, based on surveys of about 21,000 work locations, and not on online job postings (fake or otherwise).

The three-month average, which irons out the month-to-month squiggles and revisions, rose by 96,000 openings in May from April to 7.45 million, right where it had been at the peak of the pre-pandemic Good Times, showcasing a solid labor market, but without the excesses of the labor shortages in 2021-2022 (red in the chart).

Most of these job openings are a result of workers having quit or having been fired, and leaving vacancies behind (more in a moment). Only a small portion of these openings represent newly created job openings.

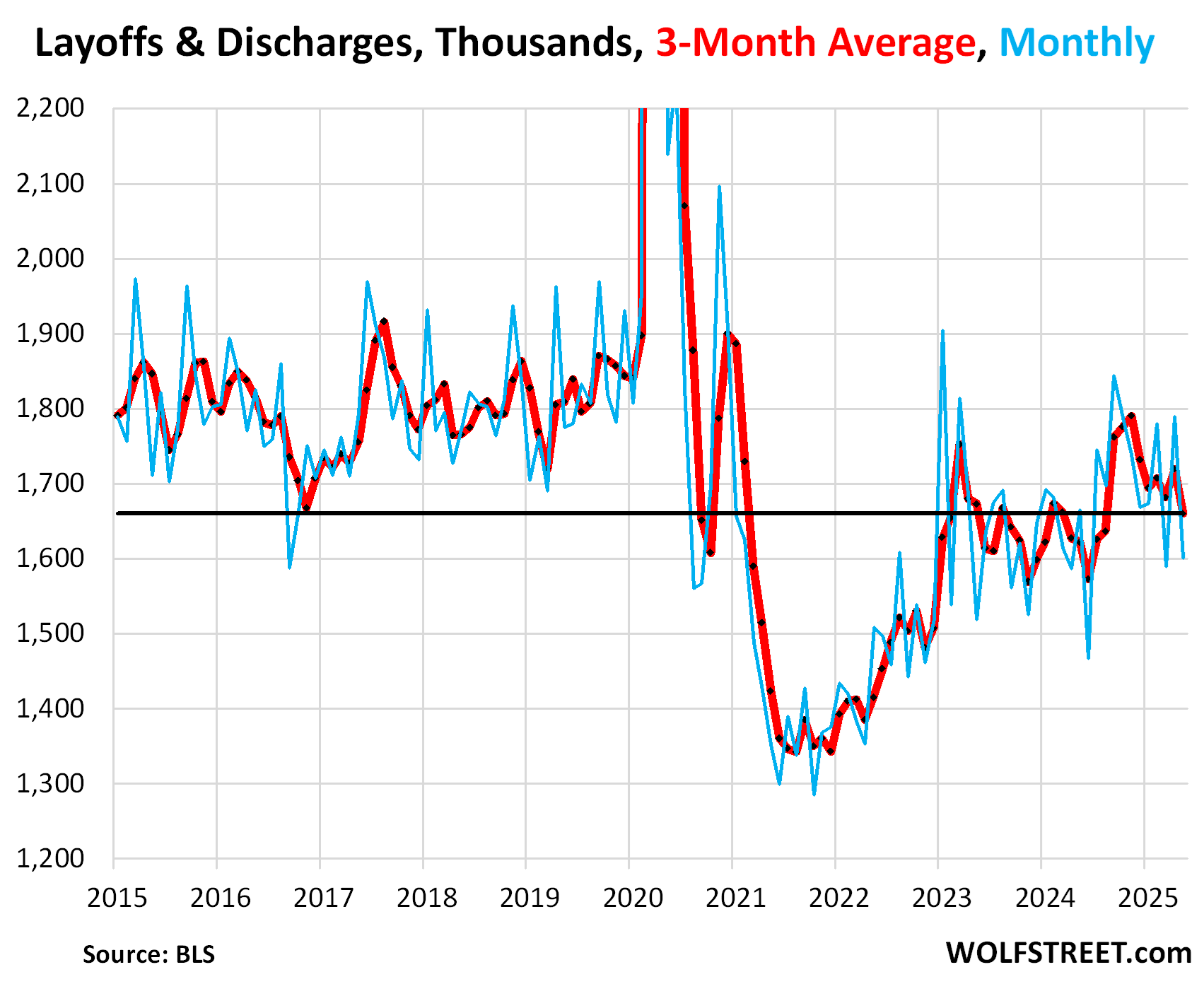

Layoffs and discharges fell by 188,000 in May from April, to 1.60 million, seasonally adjusted.

The three-month average fell by 60,000 to 1.66 million, the lowest since August 2024, and below the pre-pandemic Good Times low. The labor shortages are over, and companies are no longer clinging to whoever they could cling to, but this is a solid labor market.

These are workers who got fired with or without cause – a common feature of the US labor market – and workers who got laid off for economic reasons.

Excluded are retirements, deaths, etc.; they’re included in the small category of “other separations.” Also excluded are people who quit voluntarily to take a better job elsewhere; they’re included in “quits.”

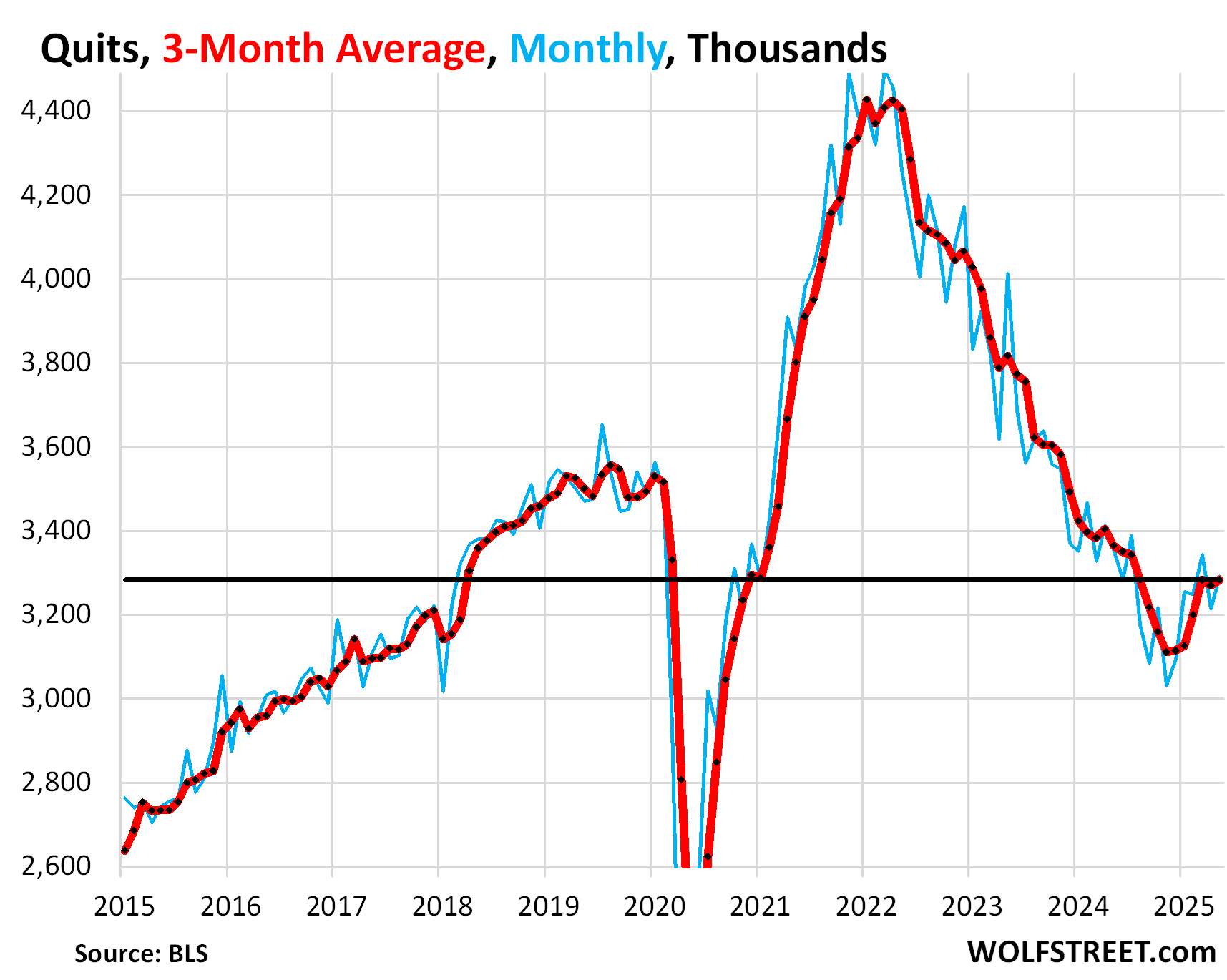

Quits rose by 78,000 workers in May from April, seasonally adjusted, to 3.10 million. These workers voluntarily quit their jobs such as to take a better job somewhere else. They do not include retirements, deaths, etc.

The three-month average ticked up by 14,000 to 3.28 million quits, roughly the same as in March. Both were the highest since August last year.

A high rate of quits is a sign of churn in the labor market. It means workers are unhappy where they are, and are confident they can find some greener grass elsewhere, or already have a new job lined up.

This still relatively low rate of quits, after the huge churn in 2021 and 2022, means that workers have found some greener grass elsewhere and that employers successfully scared workers into staying put with mass-layoff announcements starting in mid-2022.

Fewer quits means fewer job vacancies left behind, and fewer people that need to be hired to fill those vacancies. Job openings and hires are in part a function of quits.

Note the low point in quits towards the end of last year.

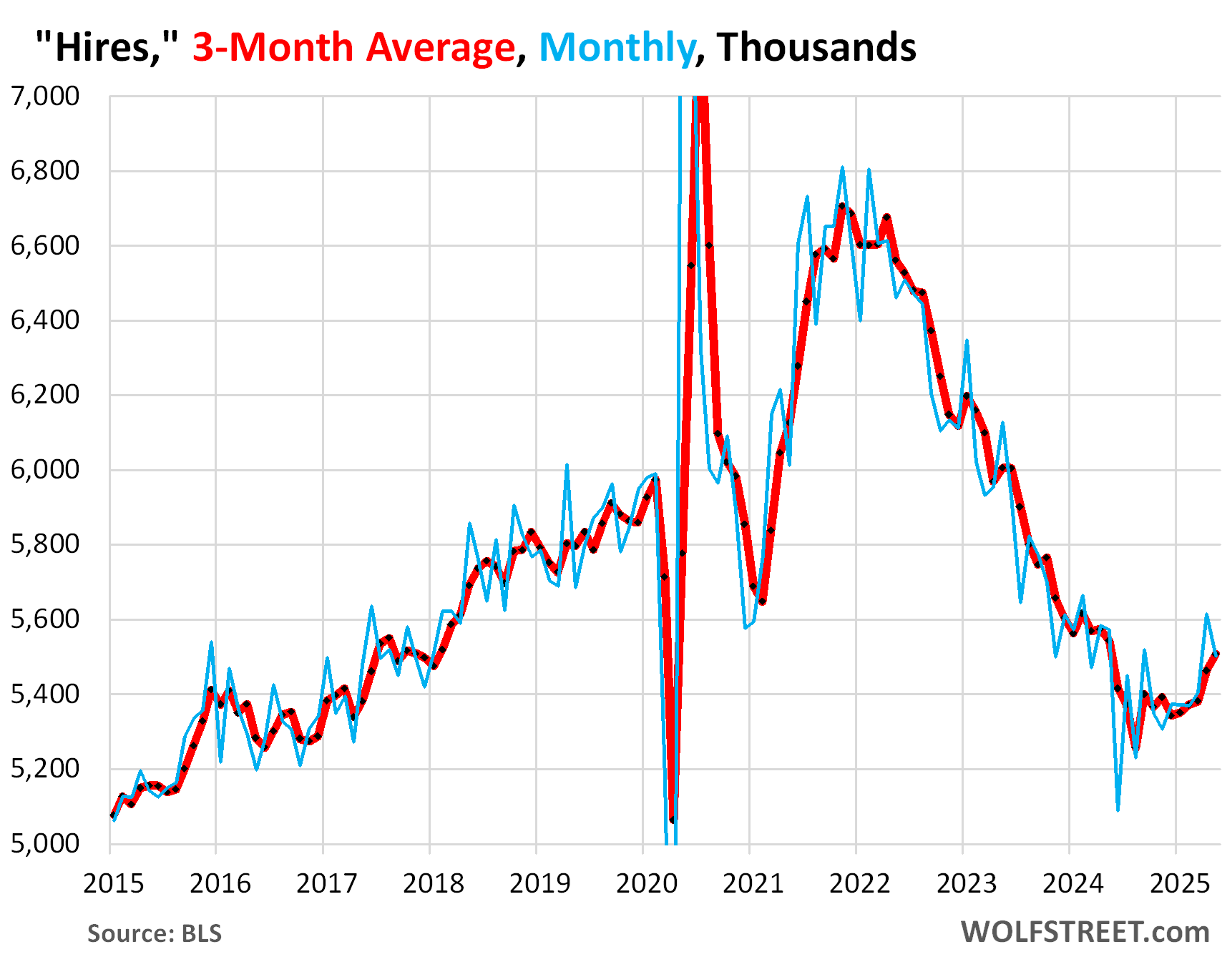

Hires declined by 112,000 in May from the spike in April, seasonally adjusted, which had been the largest hiring spree since February 2024. The total number of workers hired in May, at 5.50 million, was the second highest since September 2024.

The three-month average, jumped by 81,000 in May from April, to 5.51 million hires, the highest since May 2024, and the fifth month in a row of increases.

Most of these hires replaced workers who’d quit their jobs or who were discharged or laid off for whatever reasons. Only a small portion were hired to fill new jobs.

Fewer quits and fewer discharges mean fewer hires are necessary to fill the job openings left behind.

What we’re seeing here in these underlying data of the labor market is a solid and dynamic labor market, but without the immense and costly churn in 2021 and 2022, when people quit left and right to go after better jobs, when the whole labor market was reshuffled in a span of two years. What we’re looking at today are not the dynamics of a labor market headed for a recession; and so that recession stays on the back burner.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Quits and hires turning up. Hmm, might suggest some bidding going on for dependable staff. This can be a challenge, especially in areas where the cost of simply living is consuming all of the person’s income. Not sure how you would parse that out. Regardless, considering the complete dereliction of their duties/responsibilities by CONgress. I am becoming more convinced that America is choose the path of Argentina and not fiscal responsibility. So, yeah, I expect everyone to be employed, in potentially numerous roles as the second wave of inflation hits. Not “technically” a recession, but not good either. Might explain Powell’s actions as of late.

Inflation is above the desired 2% target rate, and the labor market is still in decent shape. Then I guess there’s no need to lower rates? Maybe even the opposite?

And no rate cuts…poor wall street!

I’m just super thankful you have a recession in the back burner, and not off the stovetop.

The recession crockpot slow cooker has been abused for several years, and everyone tired of the same old regurgitation of revised noisy data, that gets juiced up from nominal fiscal and monetary magic. Gross!

Nonetheless, the Fed kitchen is still serving updates:

The Atlanta Fed GDPNow growth estimate for Q2 comes in at 2.5% vs 2.9% last.

The data was revised up today.

I never understood people who live in this country who root for a recession while the blue team is in power just to own the libs just like I don’t understand people who root for a recession when the orange team is in power because [insert whatever they’re upset about today]

Just stay out of bonds, and buy assets. Keep some cash handy, a bit coin or two, a few quality stocks. Life is good.

Stocks take the stairs up and the elevator down. Shorting is so lucrative that people cheer for good reasons to go short

Dow ends up 400 points, S&P 500 and Nasdaq slip from record highs as Senate passes Trump’s big bill

It’s not just about the labor market. It’s about the tariffs and they’re worse than Smoot Hawley. It takes time for that to work it’s way into the economy. There’s steel and aluminum in lots of products like Pepsi and Coke. We know port workers are going to be in trouble. We know dealerships will shut down. We know farmers are going broke because countries are retaliating by not buying our crops. We know Trump’s not supplying weapons to Ukraine. Later this year or early next year the recession starts because of the lunatic in charge of America.

Tarrifs will shut down the earth as we know it huh? My pepsi can will be unaffordable. What ever will I do? Should I switch to tap water now before I declare bankruptcy, or just throw my hands up and be part of the coming Armageddon?

“Top economists predict tarriffs will LITERALLY cause Earth to stop spinning on its axis.”

Well this is why We have wind turbines on the Altamont Pass,

Their thrust helps push the earth round and round ! 😀

Lots of room for companies to absorb the tariff increases (as Wolf has shown repeatedly) until they can reshore manufacturing. And for many items, the impact is negligable. Using your example, the cost of the aluminum in an aluminum can is about 1.4 cents (if you trust Google). Raise it 10%, and the cost increase for a six pack of Coke is less than a penny. Now, for autos, the cost can be substantial, but again, many auto companies have plenty of room to cut (I just had to pay MSRP for a new Lexus). But there, buy US steel and build the car in the US, and voila – no need to worry about tariffs on steel. And that is the whole point of the tariffs – reward reshoring, and raise money from those companies that refuse to do so.

For many manufacturers (and tech companies), energy costs are a huge factor. Trump’s energy plans will have their biggest impact there: tariffs will reward reshoring, and lower energy/electricity costs will help keep manufacturing costs reasonable (particularly as compared to the renewable energy plans that the Dems have/would impose).

😂

I’m wondering how that post made it past Wolf’s hammer.

I guess he knew “we all” needed a good laugh?

“We know Trump’s not supplying weapons to Ukraine.”

I picked this one because it was the easiest to research:

5/1/25 WASHINGTON DC – On Wednesday, the Trump administration informed Congress of its intention to green-light the export of defense-related products to Ukraine through direct commercial sales (DCS) of $50 million or more, Kyiv Post has learned from diplomatic sources.

“I’m wondering how that post made it past Wolf’s hammer”

I was busy writing this article, LOL:

“Tariff Cash Is Rolling In: June’s Record Take Spikes by $20.5 Billion Year-over-Year”

“Businesses have been paying them out of their huge profits and have not been able to pass them on to consumers so far.”

Do yourself a favor and Stop watching the MSM it is polluting your mind.

Stopped reading when you brought up Coke and Pepsi.

They will SAY they have to increase their prices because of “muh tariffs on Aluminum”

But check out how much a soda can weighs and the cost of Aluminum, and how much a tariff on Aluminum will actually cost compared to the price increases they’ve rammed through the past few years

It’s overpriced, and it’s bad for you. Used to be cheap and bad for you. The price increases after Covid have helped me cut out the bad habit.

“We know”? “We” don’t even know how many of the tariffs will be in place in 10 days. And there are other forces at work that are probably much more stimulator, a massive permanent tax cut looks likely, massive regulatory cuts, and an unleashed energy industry. I’m not an economist, but those forces are likely to put far more money in people’s pockets than the tariffs will take away. Of course deficit spending will have its own costs, due in their own time, but don’t say we “know”, because we don’t, or we would all be as rich as Buffet.

“Excluded are retirements, deaths, etc.; they’re included in the small category of “other separations.”

Really? There are an estimated 4.1 million retirements a year in the US, so that would be about 340,000 a month.

LOL, compared to 3.1 MILLION monthly Quits?

And your figure is exaggerated. Total “other separations,” which includes retirements and deaths, was only 302,000 on average over the past 12 months.

It’s hard to have a recession when deficits are 5-7% of GDP. The bad news takes the quiet form of systematic risk and rising debt/GDP ratio, while employment stays normal.

The Big Beautiful Bill will kick the can a little farther down the road.

It’s hard to own treasury bonds when debt keeps rising and nobody cares.

@Bobber Absolutely. I keep wondering when the hammer is going to fall… while benefiting in the short term. My children won’t need to worry about buying a house, because I’ll form a real estate LLC, buy one for them, and rent it to them while deducting interest, taxes, and maintenance expense. Life is good… if you have money! I don’t plan on being around when the bill comes due. (Darkly sarcastic humor)

This. Totally agree.

If happier workers are more productive, I wonder if the churn during 2021-2022 is turning out to be a solid investment in the people hired and trained in the past few years. I wonder if worker productivity has gone up.

It’d be interesting to see amount of people in the labor force as a ratio to Gdp pre-pandemic and year 2024.

Yes, it seems there is some of that. During the churn, productivity plunged, as you’d expect, as so many people have to constantly get their feet on the ground. But then, starting in mid-2022, after they settled in and learned the ropes in their new jobs, productivity surged.

Wow, 3 great new articles for July 1. My cup runneth over !!!

I read an interesting book called the “Rise of Carry” – a book whose premise is that various kinds of carry trade now dominate the Global Markets and Economy to the degree it has captured the Central Banks.

The book suggests that Carry Trade Regime is characterized by steady gains punctuated by big but temporary crashes.

The author makes the interesting comment that in the carry regime, the crash in the equity markets IS THE RECESSION and while the regime lasts we may see some disconnect between equity performance and real economy performance.

July 1st – “Recession is on the back burner.”

July 2nd – Microsoft lays off 9,000 employees.

My rose tinted glasses just fell off. Is it SHTF time, or not yet?

LOL, Microsoft has been conduction layoffs since mid-2022, some bigger than this, including 10,000 in 2023, and still no recession. Get used to it. It’s Microsoft, not the economy. Cisco announces layoffs EVERY summer, and has for decades. Etc. etc. They’re just getting rid of the deadwood, cleaning out underperforming divisions, and now maybe cleaning out people refusing to RTO.

tech in general has been shedding jobs since mid-2022, after the huge hiring binge they went through, replacing humans with AI, etc. And still no recession:

https://wolfstreet.com/2025/05/21/as-tech-jobs-plunge-in-san-francisco-silicon-valley-housing-reacts-condo-prices-drop-back-to-2015-single-family-home-prices-back-to-2018/

In today’s news, Tesla sales are going down the toilet, down 13.5% from the second quarter last year. Circling the drain?

They actually rose quarter to quarter, as all auto sales do in Q2, and the year-over-year decline was the same as in Q1.

What’s funny is the collapse of the sales of its “other models” (Model S, Model X, and Cybertruck). They plunged by 50% year-over-year. Sales are back where they’d been in Q2 2020. They’re going to hell. The Cybertruck must have turned into an incredibly expensive dud for Tesla.

I wonder what kind of jobs these are (7.7mm job openings?) Are these door-dash like jobs?? The math doesn’t add up (median salary $43k vs home prices). something has to give….

homes sales are WAY down, tourism in Las Vegas is way down, sales of Teslas are way down (-13%) more will follow

By the time unemployment spikes something already broke.

the openings are across the board, some higher some lower.