A Los Angeles tower, FEMA headquarters in Washington, 100-year-old tower in Manhattan join list; some delinquent loans were “cured,” including by transfer to a custodial receiver and extend and pretend, and came off the list.

By Wolf Richter for WOLF STREET.

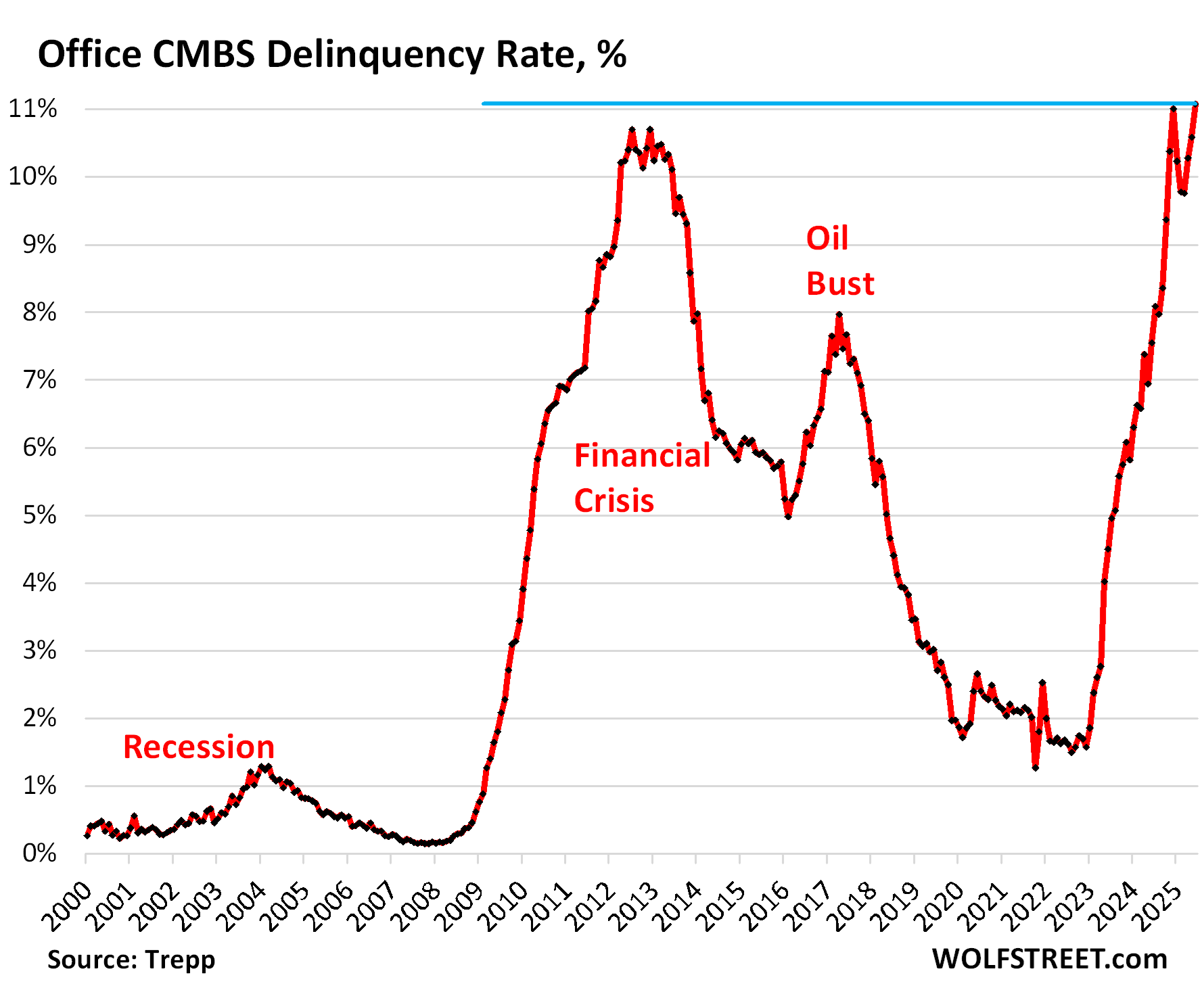

The delinquency rate of office mortgages that have been securitized into commercial mortgage-backed securities (CMBS) spiked to 11.1% in June, a new all-time high, re-blowing past even the Financial Crisis meltdown high, and squeaking past the December 2024 high, according to data by Trepp , which tracks and analyzes CMBS.

Since the beginning of 2023, the delinquency rate for office CMBS has exploded by 9.5 percentage points. And so the depression in the office sector of commercial real estate drags on, despite well over a year of pronouncements that “the worst is behind us.”

The last three months were a majestic relapse from February and March when the delinquency rate seemed to be on the mend.

A total of $156 billion of office loans have been securitized, Trepp said. The CMBS were sold to institutional investors, such as bond funds, insurers, etc. Banks are off the hook here.

In June, $1.8 billion of these CMBS office loans became newly delinquent, including the three discussed below, while $1 billion of delinquent office loans were “cured” and came off the list, including the three discussed below, one of which was “cured” when a court transferred the property into receiver, and another was “cured” by extend and pretend. It’s ugly out there.

The delinquent balance rose by $800 million – the difference between the newly delinquent loans ($1.8 billion) and the “cured” loans ($1 billion).

The top three June additions to the “delinquent” balance:

1 Cal Plaza, Los Angeles: $300 million, foreclosure. The 42-story 1-million square-foot 1980s office tower, formerly known as One California Plaza, was purchased in 2017 by a partnership between Rising Realty Partners and Colony Northstar.

The tower was financed with a 3.8% fixed-rate interest-only mortgage of $300 million that was then sliced into three pieces and securitized: An A-note of $86 million and a B-note of $164 million comprise the single-asset CMBS, CSMC 2017-CALI. The third piece, an A-note of $50 million, makes up 6.97% of the CMBS, CSAIL 2017-CX10, which is part of CMBX 11, according to an earlier note by Trepp.

At the time of securitization in 2017, the collateral was valued at $459 million. By March this year, the collateral value had been slashed by 74%, to $121 million according to Special Servicer notes. The loan, which matured in November, has not been paid off and is now in foreclosure, according to Trepp.

75 Broad Street, New York City: $176 million, 30 days delinquent. The 34-story nearly 100-year-old tower in Lower Manhattan was acquired by JEMB Realty in 1999 and renovated in 2017, according to JEMB. In 2017, it borrowed $176 million against the tower, at 4.077%. At the time, the tower was appraised at $403 million.

“This is the rebirth of a true original, a shining example of JEMB Realty’s expertise in value-enhancing properties so as to attain their full potential while remaining on top of ever-evolving trends and needs in office-using industries,” JEMB says.

The loan was sliced into three pieces and securitized: The AA1 piece of $59 million and the AB piece of $84 million are sole assets in the CMBS, NCMS 2017-75B. The AA2 piece of $33 million makes up 4.95% of UBSCM 2017-C1, according to Trepp.

JEMB failed to make interest payments, the 30-day grace period came and went, and in June, the loan was deemed 30 days delinquent.

Federal Center Plaza, Washington, DC: $130 million, maturity default. The property consists of two adjoining eight-story class-B office buildings of about 725,000 square feet combined.

About 71% of the space is leased by the US government: FEMA leases 64.7% of the space which serves as its headquarters; that lease expires in 2027; and USAID leases 6.5%, and that lease expires in six months.

The property was appraised at $309 million when the loan was issued. In February 2023, before the DOGE chaos snowed upon government-leased buildings, the appraised value was cut to $237 million. Earlier this year, KBRE estimated that the collateral had a liquidation value of $122 million.

The loan came due in February and has not been paid off. After the forbearance period, it became delinquent. The loan makes up 56.5% of the remaining collateral behind COMM 2013-CR6.

The top three delinquent loans that were “cured” and came off the list:

Selig portfolio, Seattle, $220 million, cured by transfer to a “custodial receiver.” The office empire of Seattle’s “office king” Martin Selig, once counting 30 buildings in downtown Seattle, has been unraveling in recent months in large chunks. The latest hit came in June, when the court transferred a 9-office building portfolio to a custodial receiver, after Selig had defaulted on the debt.

That transfer to a custodial receiver took the loan off the delinquency list and “cured” that delinquency.

1000 Wilshire Boulevard, Los Angeles, $128 million, cured by “performing maturity balloon.” The loan went into maturity default in March 2025, when the borrower, an entity of Cerberus Capital Management, failed to pay off the loan. Apparently, some a deal has been reached. Trepp said that the loan is now listed as “performing maturity balloon” and is no longer considered delinquent.

393-401 Fifth Avenue, New York City, $94.8 million, cured by extend and pretend. The landlord (the Chetrit Organization) had failed to pay off the loan when it matured in January 2025. A deal has now been reached between them and the special servicer to extend the loan from the original maturity date for 18 months to July 2026, according to Trepp. Extend and pretend in all its glory.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Just wait till AI and UBI (Universal Basic Income) get going.

Will office buildings be worth the demolition costs? Unlikely in most cases, unless someone is paid a large subsidy to demolish or convert as most are totally uneconomic conversion to residential propositions, the majority will just be vandalised and decay.

Why was all of this vast amount of excessive and unwanted commercial office space ever built in the first place? If it was just moronic stupid speculation in an attempt to pump up asset values from the get go, is there any real issue in just letting the speculators now take 100% of the losses as it sits increasingly vacant?

Who’s to say it was excess / speculative? This very much looks like a direct result of remote work.

Obviously, nearly all of this building was purely speculative as there were no tenants to lease all of this absurdly overpriced space. It looks a lot to me like the Japanese attempted takeover of CRE in Los Angeles and over in Hawaii back in 1989. Idiot speculators just never learn.

is it possible you missing the nuance that these buildings were leased for decades (or perhaps even 100 years) before being sold, and then several more years after that?

Yes the buyers speculated wrong, but claiming these were empty buildings with no one interested in leasing them back in 2017 is silly.

Virtually all societies drive in the rear view mirror. Add America’s penchant for unbridled capitalism (aka, greed), and you have your answer.

Give this another 2 decades and the issue will no longer be investor losses. These babies will end up abandoned to the public to handle takedown expenses. Or more likely, left standing, windowless hulks. A beautiful sight.

You just can’t help wondering how bad it will get.

Wait until people start realizing real estate funds advertised as safe havens with stable returns are not so safe after all. There’s a lot to be lost here, especially for the people that have their pension funds continue investing after retirement date (pension funds often advise to pivot to ‘safer’ investments running up-to and after your retirement date).

Perhaps something like David wrote about?

The Halloween Jack is a real cool cat

And he lives on top of Manhattan Chase

The elevator’s broke, so he slides down a rope

Onto the street below, oh Tarzan, go man go

Meet his little hussy with his ghost town approach

Her face is sans feature, but she wears a Dali brooch

Sweetly reminiscent, something mother used to bake

Wrecked up and paralysed, Diamond Dogs are stabilised

These loans were probably issued during the covenant light period engendered by the QE mindset. In that case the public would probably be called upon to subsidize the malfeasance. Then again, maybe not.

Hey Wolf,

What about the Columbia Center. That was built by Selig in 1983. It’s been sold a few times. The latest owner is Gaw Capital (Chinese company). I wonder if they are in difficulty. The building has many vacancies.

Is this really any different than the residential home debacle that started in 2007? Why do you lenders and investors believe that things will continue the way they are at the time loan is given?

The real question now is whether or not we are going to allow deflation and overleveraged idiots to actually go bankrupt or will every day Americans be forced to bail out these entities again.

I think that was a rhetorical question, right?

Oh the great joys of other people’s money and the ability of Wall Street to create excesses and then to slice and dice mortgages and then sell the pieces on to yield needy institutions who forgot the lessons of the sub prime mortgage and junk mortgage disaster of the 2009 onward.

Which entity is responsible for payments for the Federal Center Plaza loan?

The SPV (single purpose vehicle) borrower. When commercial mortgage deals like this are set up, the sponsor, being the “owner” of the building, sells the property into an SPV LLC, which the sponsor owns. The mortgage loans are now for 100% of the value, but for say 80%. So let’s say the building was appraised at $200 million at the time of origination. The SPV borrows $160 million from the mortgage lender and buys the building from the sponsor. The sponsor is thus contributing $40 million in equity capital into the SPV. Note that this loan is non-recourse, so if the SPV borrower defaults, the lender’s only recourse is to the building itself, and not to the sponsor.

Shortly after the loan was originated, it was sold into a securitization trust. That trust then, with the help of underwriters, sold bonds to investors, backed by that loan, and others it was pooled with.

The sponsor still acts as the “manager” of the building, and signs leases, collects rents, and so on. It takes those rent payments and pays its mortgage with it. Now that the mortgage is owned by the securitization trust, the sponsor takes those rents and pays them to the servicer of the securitization. The trustee then takes those payments and divvies them up, making the payments to the bondholders.

The problem here is that nearly 2/3rds of the space is leased to FEMA, and the lease expires in 2027. While FEMA of course isn’t going to default, unless it signs a new lease, no lender will take the risk to refinance the loan at maturity. If they had, and refinanced the old loan under a new 7 or 10 year term, the lease would end in the middle of the loan, and if the space stays vacant, there would be no tenant paying rent that would be used to pay back the new mortgage. That’s why it’s in maturity default.

Even if FEMA does renew, let’s say they do so at half the rate they were paying before. That means that the new loan will be smaller, and likely not big enough to pay off the balloon payment on the old loan that just matured.

Since the sponsor only has $40 million into the project (the original $200 million – $160 million), if the building is only worth $122 million now. So it’s not going to pay more to keep the building. It’s better off writing off the $40 million and letting the owner of the mortgage (the securitization trust) foreclose and take the building. Which is likely what’s going to happen. The problem is the bondholders will take losses, as there won’t be enough in liquidation value to pay off the remaining loan.

Thanks for posting that, the details about how the sausage is made.

” Note that this loan is non-recourse, so if the SPV borrower defaults, the lender’s only recourse is to the building itself, and not to the sponsor.”

Theoretically these investors are sophisticated enough to know the risks they signed up for.

E.g., If you are enticed into buying a mortgage bond because you believe the fed gov’t is a great tenant, then you are shouldering the risk that the fed gov’t will change its mind and shut down that department.

Sounds like the system working as designed.

The collateral is in the process of being transferred to the lenders (special servicer representing the CMBS holders). They’ll own the collateral and the loan. It’s their baby now.

Thank you Wolf Richter for reporting the facts. Most CMBS mortgages flawed. Brokers submitted and Bankers approved CMBS loans without proper underwriting. They were motivated by high fees payable to real estate brokers and Bankers. Bankers knew they could sell the loans after 90 days to Investment Banker “packagers” of large loan pools for sale to pension funds in the secondary market. Loan amounts on many were even increased enough so banks could prepary first three months monthly mortgage payments to escape their first 90 day default liability to repurchase them. All parties were motivated by excessive loan fees and lack of proper underwriting.

I watched it happen as mortage company operated successfully for 32 years (1982-2014) without a single foreclosure, I refused financing involving government leases containing options to early cancellation.

Profit motivated Bankers invented “Fair Value” instead of “Fair Market Value” to increase loan amounts and approved loans without visiting the properties! I wrote letters about this practice in 2004 to the Appraisal Institute (member since 1969) and the American Bankers Association objecting to the unethical practices and received no reply. After ten years of “extend and pretend are facing up to results.

I believe The Senate Banking Committee was also party to this charade.

The risk of investing in a long term risky asset. Betting on a vision of the future.

Promoted by deficit spending whereby the expense will be covered by the profits when the investment pays off.

Where would we be without gambling ?

So sad, so sad.

Has the % of office loans securitized into CMBS increased over time?

Wondering if office bankruptcies are higher in this cycle than previous, or if instead they’re more visible because a greater % end up in the CMBS data.

For example, was a significantly lesser % of office loans securitized during the 2004 recession, making that CMBS delinquency rate look much smaller than it was?

Wolf – What % of GDP do the delinquent loans account for compared to the housing crisis in ’07? I believe the current level of risk is significantly lower than the last time around.

The big problem loans that threatened to take down the banks during the Financial Crisis where the residential mortgages. That amount far exceeded CRE mortgages. Within CRE mortgages, Office mortgages are less than 20% of total CRE. The biggest part of CRE mortgages are multifamily mortgages (now over half are guaranteed by the government). Even in total, CRE mortgages were never big enough to take down the financial system, and CMBS were always held by investors, not banks.

Isn’t part of the bust driven from the trend to work from home?

The oil bust was because monetary flows, the volume and velocity of money fell by 80 percent causing the price of oil to trough in Jan 2016 by 70 percent during the same period (as predicted)

Zero to do with money flow. The oil bust was due to the rapid surge of oil production in the US that triggered oversupply, as demand for gasoline stagnated. Natural gas went through that a few years earlier. The immensely prolific production from fracking crushed prices. In recent years, the booming exports of US crude oil and petroleum products, and increased use by the US petrochemical industry have provided an outlet for this production:

These articles have charts that go back to the 1980s:

https://wolfstreet.com/2025/03/04/u-s-production-exports-of-crude-oil-petroleum-products-hit-new-record-in-2024-imports-dipped-further-spr-refilling-halted-in-february/

https://wolfstreet.com/2025/03/02/drill-baby-drill-for-20-years-us-natural-gas-production-and-exports-via-lng-pipeline-rose-to-new-records-in-2024/

Maybe, just maybe, we’re arriving at the point where CMBS will start to be a drag on the economy or at least a real omen of what lies ahead.

Doubtful. These are over levered idiots who bought office space when even before COVID the trend was wfh and less office space need per person anyways

We are not prepared for what lies ahead but we are a resilient people.

IF one examines the basic structure of our economy, at the granular level, they would find the source of our wealth, the everyday people.

After so many years of “rewards” the market has a nasty way of reminding all of the “risk” side of the risk/reward equation….. But in the long term lower rents will help new businesses and spur innovation. Just sucks to be holding the ball when the market inevitably turns….

“But in the long term lower rents will help new businesses and spur innovation.”

IMO, that type of thinking is what leads people to invest in REITS.

Go on X and find the video of the robot giving women haircuts. Stylists will go the way of musicians. The hair salon market is over $50 billion in the US.

We will need far, far less commercial space in the US going forward. Now, I do have a buggy whip investment coming up and it’s opening to a few select individuals who want to passively net 15% annually. Trust me, this IS the next big thing!

I disagree. I suggest that the robot is unable to gossip which is why one of significant impulses that induce people to go to the human barber in the first place.

Robots are a necessary evolution that are here too stay.

1000 Wilshire is old, in DTLA and has lost a major tenant. Good luck with that Cerberus!

DM: Del Monte files for bankruptcy after 138 years on shelves

An American grocery staple just went bankrupt.

Del Monte Foods, the 138-year-old company behind some of America’s most recognizable pantry staples, has filed for Chapter 11 bankruptcy protection.

For decades, the company has produced canned fruits and vegetables for American grocery consumers. The food producer filed for bankruptcy protection late Tuesday night.

Del Monte said it plans to sell itself as part of an agreement with key lenders and will continue normal operations during the process.

To keep things running, Del Monte secured $912.5 million in financing.

Del Monte’s portfolio extends beyond canned corn and peaches — it also shelves household names like College Inn, known for soup broth, and Joyba’s bubble tea.

Womp womp. Make better business decisions

It died when it was taken private by KKR. They stripped off the assets and sold it to some Filipino company.

There is no point in talking about the funeral of a long dead company.

Del Monte, like Hostess, makes great products and it will be bought for below value in bankruptcy and will rise again strongly supported by consumers like me who want their quality products.

Looks like they were touched by private equity (KKR) back in 2010, similar to Joann Fabrics. Loading a company up with debt makes it fragile.

Wow, a household brand name failing. A schocker.

Further concentrating an already concentrated, oligopoly. Competitive pricing doesn’t have a chance. The President will fix it as soon as he is done tending the mop up. As Mitch said, They’ll get over it.

It reminds me of that famous movie scene where the human turd was floating in the public pool.

‘before the DOGE chaos snowed upon government-leased buildings’

This may be the one of the smaller impacts of the DOGE chaos, as the sector was already in its largest downturn. Kind of a cherry on top of the CMBS.

Every one will have a fave of the DOGE debacle. Mine is firing a bunch of nuke safety guys, then being unable to quickly find all of them when they were wanted back pronto.

In what universe would a sentient human bring in clueless 20 year olds too solve any sort of problem beyond they’re sex life. The whole DOGE thing is weird, a premonition of the damage that can be done by a senile 80 year old.

This is partially the reason for mandatory RTO. If workers don’t return to their cubicles, the office space is not necessary. Commercial real estate pays a disproportionate percentage of local taxes. If it collapses, it is the first in a series of dominos that will fall.

Unlike Walmart which guts the local business community and pays a pittance in property taxes.

Walmart shoppers include union members. There is no accounting for stupid.

The social democrat in NY’s mayor race is being smeared as being a commy by the very crowd with contracts with the CCP ( Chinese Communist Party) to offshore American manufacturing.

No, it isn’t.

If you’re like most companies, commercial real estate is an expense, not a revenue stream. Why, exactly, should a company throw more money into expenses than they have to?

No, the real reason for mandatory RTO is simple: most workers intend on doing the minimum possible (which is understandable) to get paid and not get in trouble/fired. WFH allowed them to do even less without getting in trouble which cancelled out gains from not paying for CRE.

BLOATED BIG BAD BILL FACES REPUBLICAN REBELLION…

HOUSE THREATENS TO SINK IT…

Dream on. One way or another this will pass. Most of their ability to get re-elected relies on it. If Murkowski voted for it with getting some grease thrown her way then that will happen for others

There will BE NO CHANCE WHATSOEVER FOR REPUBLICANS TO GET RE-ELECTED if they pass this atrocious and horrendous piece of grossly irresponsible bloated evil and moronic hogslop as they’ll be voted out of office in droves and will lose control of Congress.

Eh. Each party does this

LoL, securitizing spread the risk, so that more entities take the (L)osses. So we trudge on. As predicted with the spread of work from home. The real irony is so much work is wasted, so allowing more efficient workers to spend less time should be a net positive, yet we think it is a negative. In short, this return to office stuff is bs, because deliverables are all that ultimately matters. The fact that some people can maintain two full time remote jobs really means that the two jobs are not really full time.

AI is the illusion of reality that the workplace is very inefficient for office work, and still needs to be rationalized. I would note that in most cases the bureaucracy is half the problem. So much inefficiency exists due to friction built into large organizations.

And now with full service payroll and benefits available from outsourcing, work from home, and no need for the office infrastructure, a lot of intellectual property places are going to go offshore to the lowest cost places. Further erosion of tax bases is the future.

How do I tax an entity that hires me from Ireland, with my domicile in a low tax country that gets my work and integrates it in 14 countries, then actually produces a final product in Vietnam that is sold worldwide? In short, taxes are going to very difficult for intellectual work, and the modern world is going to rely on W2 workers. Another great example is the 1099 scam of cutouts in contracting, with temporary entities that never file any taxes, with no real responsible parties after the funds pass through to “workers”. How do you tax a software gaming company based overseas that takes payments through a third party also overseas? The money flows out of your country, but how do you get it taxed? In short, governments are going to have to rethink how the entire system is going to work.

So many leaks, so property and goods are going to be primary sources of taxes in the future.

“…new research appears to indicate a rise in gored-oxen mortality. In other news, the Empire has decided to end support for the Wall of Hadrian and the occupation of Brittania…”.

may we all find a better day.

“LoL, securitizing spread the risk, ” – I think securitizing makes the actual cash engine opaque to the buyer, and presents him with only predicted rates of return, putting dollar signs in his eyes.

exactly

These delinquencies are bullish for bulldozers and demolition — and to think, this is just the tip of the iceberg —with titanic still in London.

“According to CoStar, office conversions are reshaping the US real estate landscape in 2025. For the first time since at least 2000, more office space will be removed through conversion or demolition than added through new construction”

Maybe the demolition business will stimulate GDP — probably not.

@Citizen AllenM Secritizing loans does not just “spread the risk” it gives the risk to people who know what they are doing. The guys buying the “first loss” “B-Pieces’ know they will take losses just like the VC guys know many or even “most” investments will be worth $0 down the road.

@SoCalBeachDude Office is built where there is demand for new office space. In the 1960’s most people worked in offices in downtown LA, SD & SF. In the 80’s they built lots of new offices in Century City (like the one in the TV show LA Law), UTC (that Sam Zell bought for haff price in the 90’s) and the Peninsula (like the Oracle Campus on the site of the Marine World theme park) since there was a change in where people wanted to work it was not “just moronic stupid speculation in an attempt to pump up asset values from the get go”…

The vast overbuilding of office CRE was nothing but moronic and very stupid speculation from day one.

I’m sure there are some individuals that take losses in these REITS and securitizations…BUT the majority that take the hit are going to be small fish way down the food chain. Like common stockholders in a bankruptcy. They never saw it coming.

The big boys take their cut at the start and are non-recourse thereafter.

LoL, “knows what they are doing…”

There will be no return of equity, so risk was absolute.

In other words, just another bezzle of the system.

It is simply another symptom of an economy that has asset problems. Tranching it out just slices and dices the risk into smaller portions- but a 5% zero valuation on a pool of risks still drops the value of the pool to 95% at a stroke, and because these are illiquid, there is no exit.

Cockroach investing. Just light your money on fire.

Top Collateralized Loan Obligation (CLO) Managers (by Assets Under Management as of 31 March 2025):

Golub Capital: Ranked first with $43.5 billion in CLO AUM.

Blackstone: Ranked second with $41.8 billion in CLO AUM.

Carlyle Group: A major player, previously ranked as the largest CLO manager globally.

CIFC Asset Management: Significant CLO AUM.

CSAM: High CLO AUM

A regular who’s who of who destroys companies and values.

DC office vacancy rate reported at 20.9 percent, on DC news radio. City by city rates might vary.

I think the residential real estate market seems to be like that, fracturing into different markets. The big underlying factors affected all, but the northeast seems to be quite different than southeast and west.

How about the FBI building in DC which is slated to be abandoned? What will happen to that ugly building after all the employees move to the Ronald Reagan building which use to house the USAID which was just abolished. And the HUD building which is slated for abandonment because it is falling apart.

Stablecoins are setting the stage for the next financial meltdown