Mortgage rates, QT, yield spreads, inflation, and a bond market that is not to be trifled with.

By Wolf Richter for WOLF STREET.

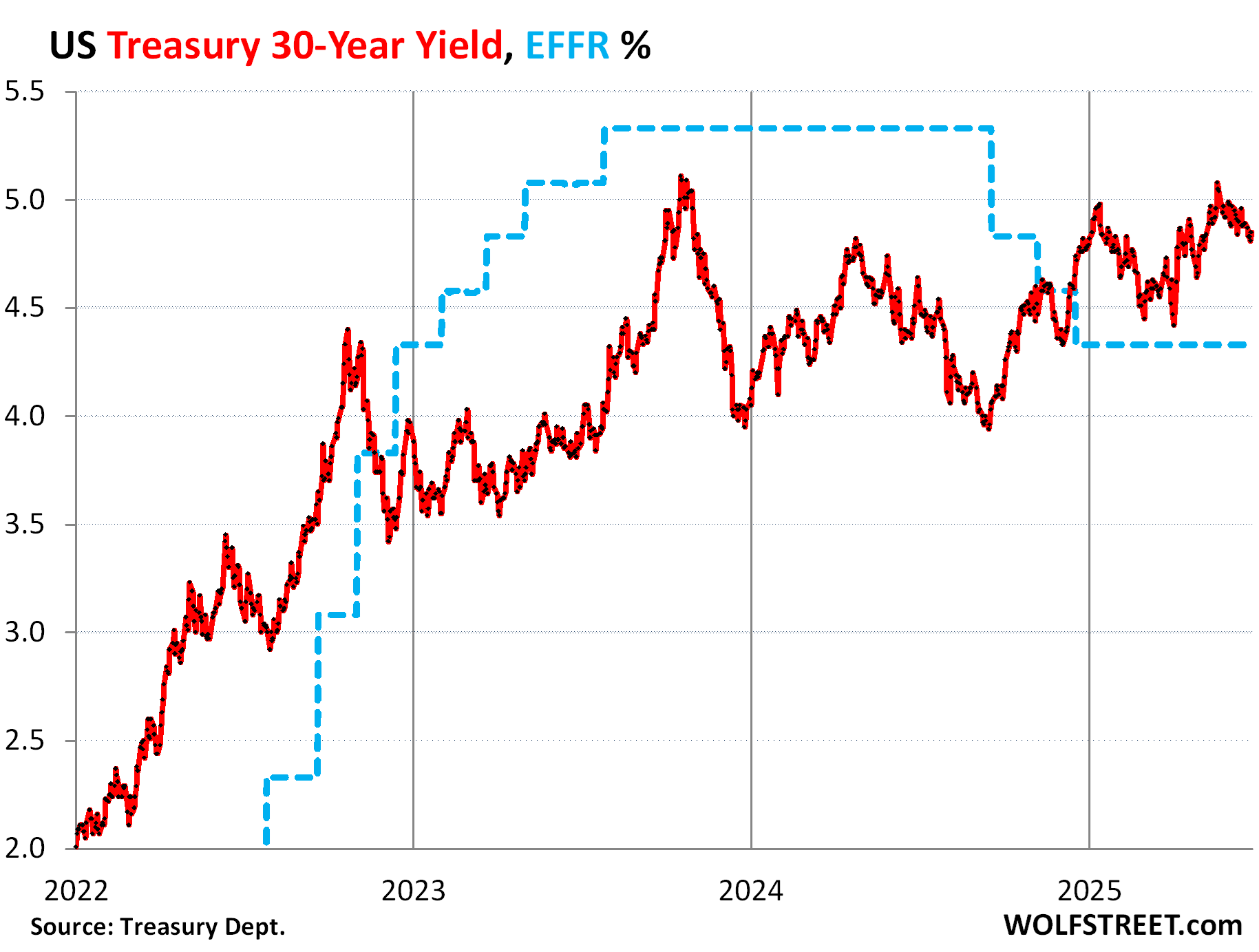

The 30-year Treasury yield, which ended Friday at 4.83%, has been showing a pattern that’s not exactly according to plan, and not even the April turmoil in the bond market knocked it off that pattern:

The 30-year yield has been zigzagging higher since the low point in mid-September 2024, just before the Fed cut its policy rates by 50 basis points. The recent dip is in line with the zigzag pattern higher.

The 30-year yield is now 52 basis points above the effective federal funds rate (EFFR), which the Fed targets with its monetary policy rates (blue).

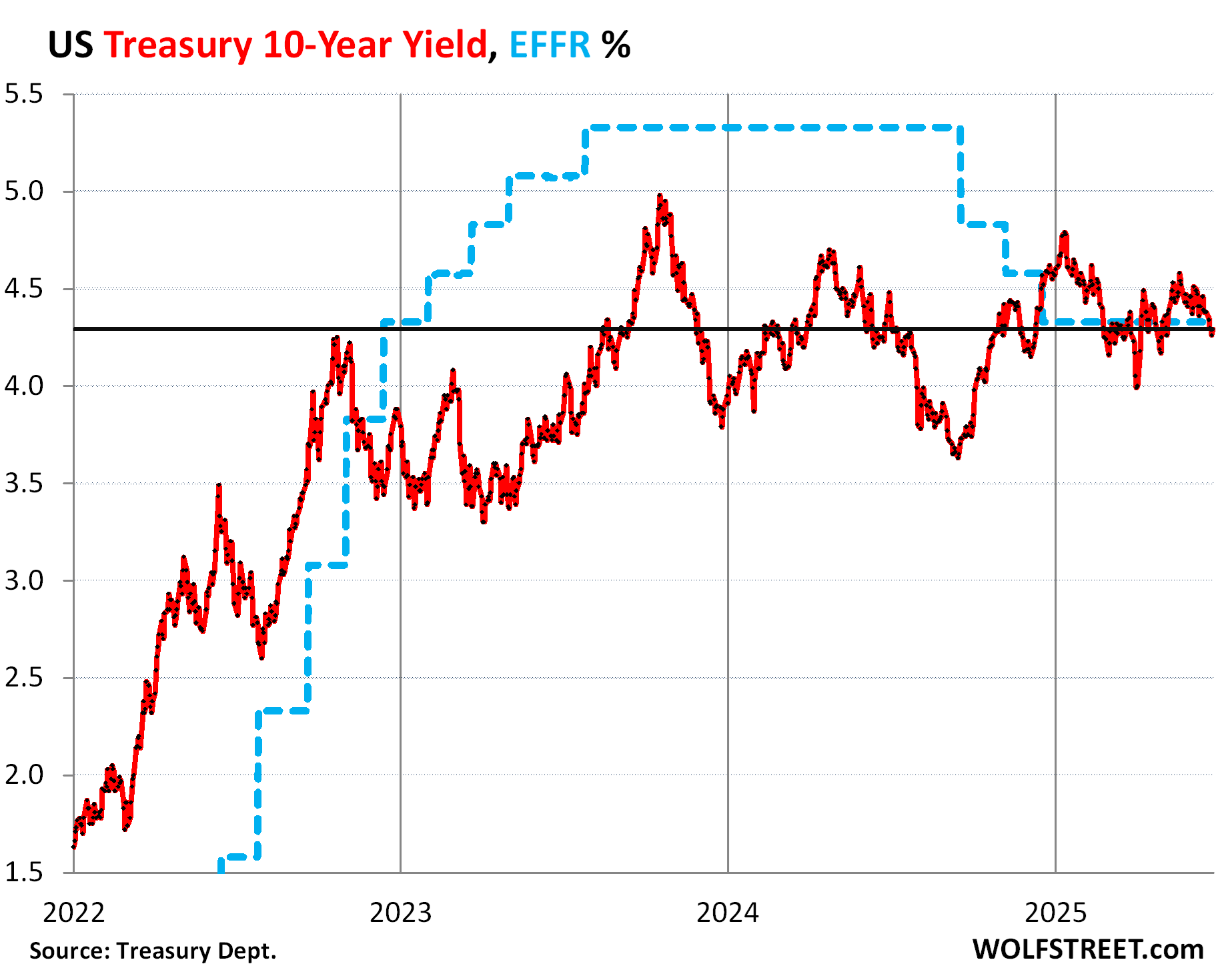

By contrast, the 10-year Treasury yield has this year zigzagged along a flat line, and on Friday, at 4.29%, was right back where it had been in November 25, and is now below the EFFR (4.33%).

The spread between the 10-year and 30-year Treasury yields has widened to 56 basis points, the widest spread since October 2021, except for the wild gyrations on April 2 Liberation Day. This means that at the long end, the yield curve has substantially steepened.

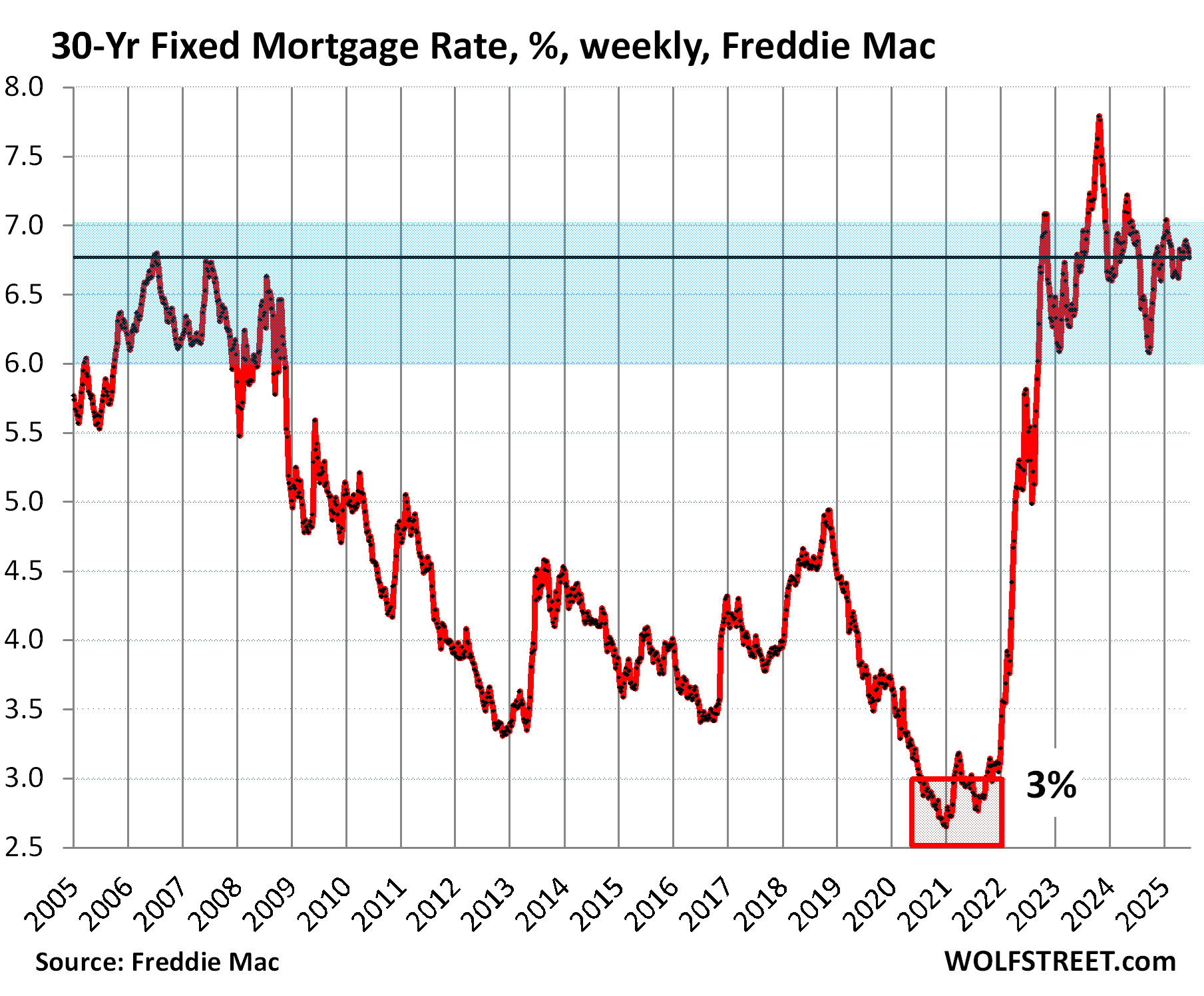

The 30-year fixed mortgage rate tracks the 10-year Treasury yield but is higher. The amount by which it is higher – the spread – varies. That spread has also widened and is very wide by historical standards.

These spreads get our attention because it’s via spreads that the market expresses its worries and fears.

The spread between the 10-year Treasury yield and mortgage rates.

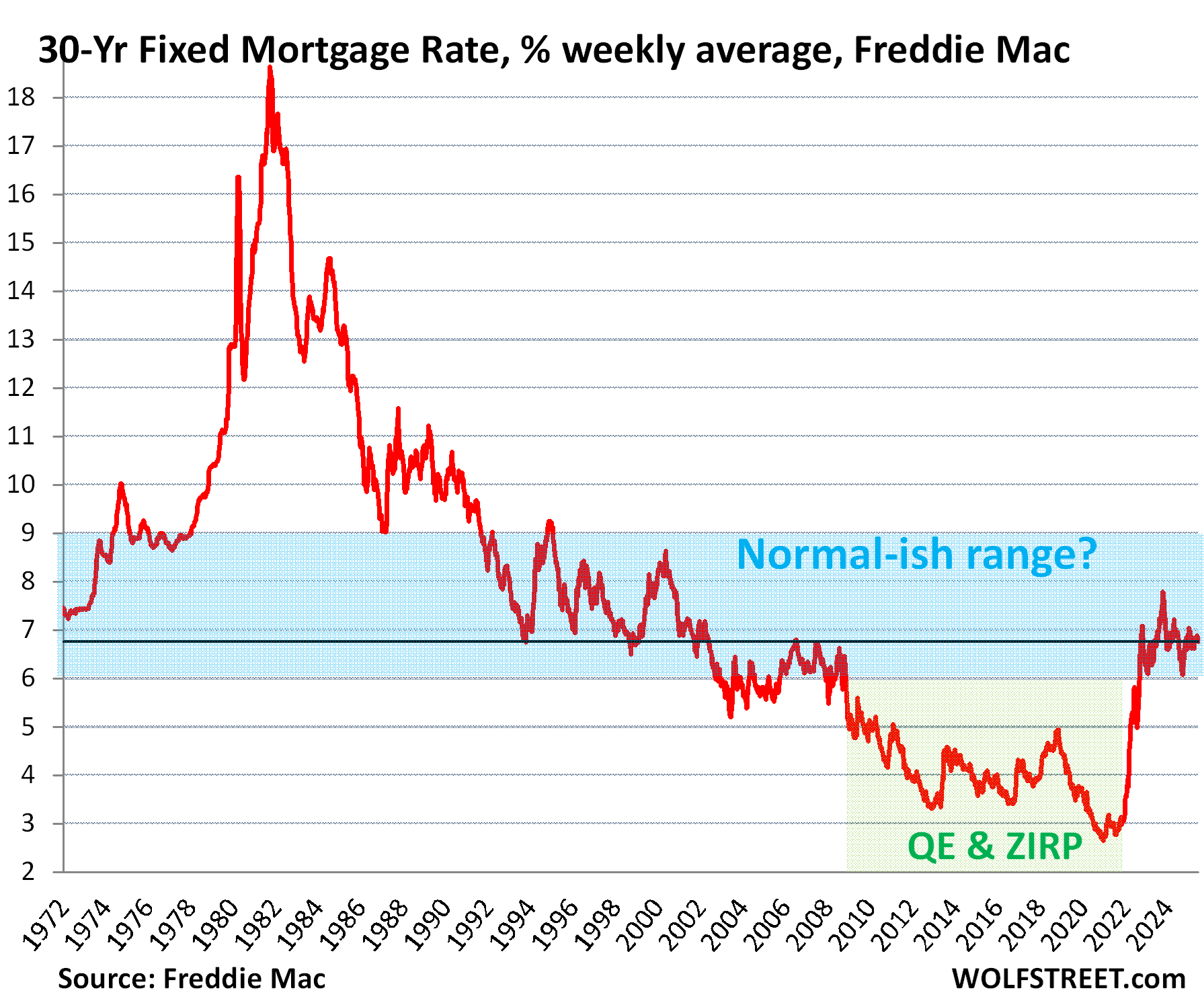

The average 30-year fixed mortgage rate dipped to 6.77%, according to Freddie Mac’s weekly measure on Thursday, which covered the period of Thursday June 19 through Wednesday June 25. It has been in this 6.5% to 7.0% range since October last year.

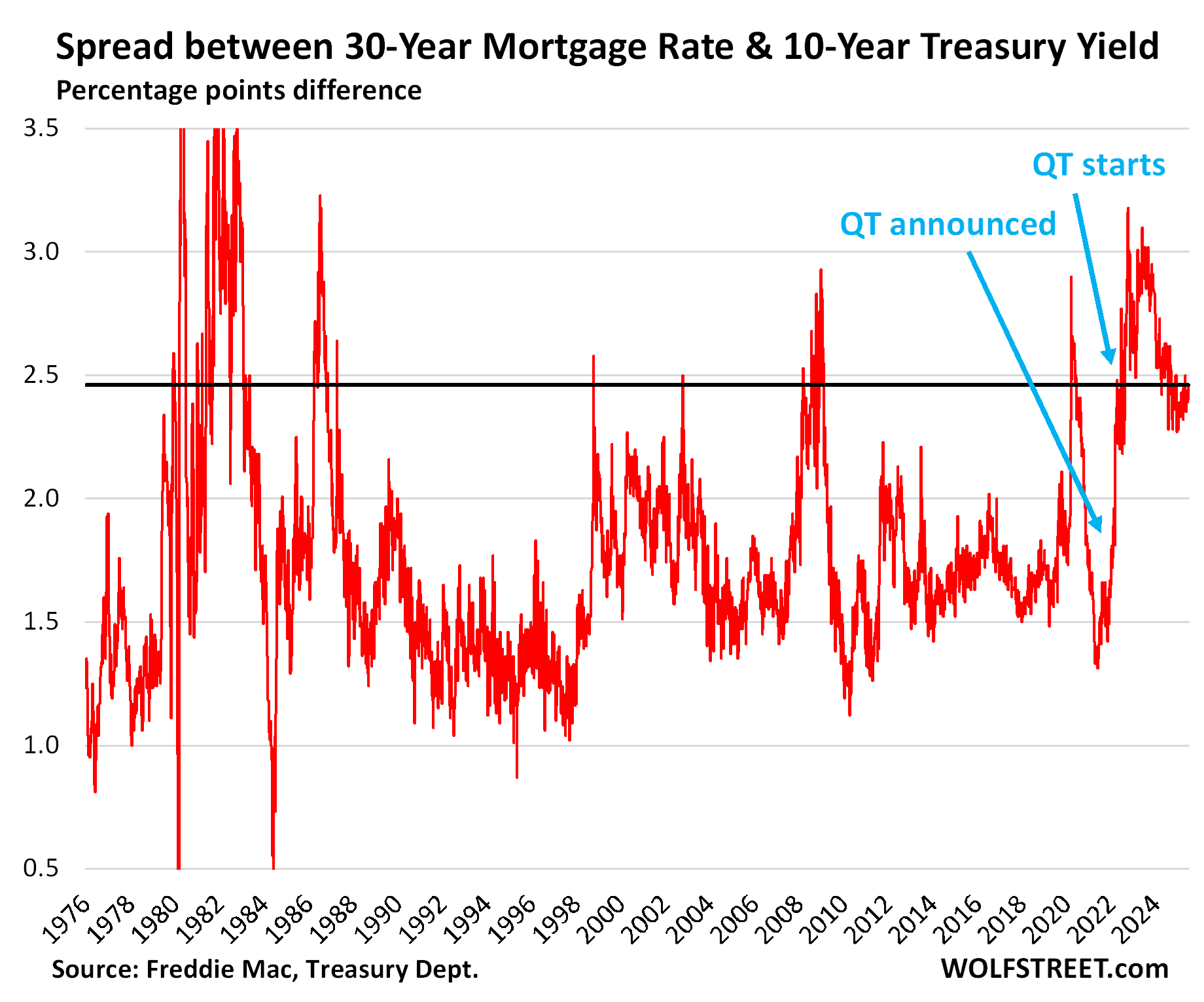

But the average 10-year Treasury yield over the same Thursday through Wednesday period was 4.31%, and the spread between them widened to 2.46 percentage points, having widened in each of the past three weeks.

During QE, the Fed bought MBS to narrow the spread between Treasury yields and mortgage rates, and also to push down long-term yields in general, and thereby repress mortgage rates, and eventually they fell below 3%.

Then in early 2022, the Fed began detailing the upcoming QT, including the QT for MBS, and the spread widened in anticipation ( the “announcement effect”). The Fed then started shedding MBS during QT in mid-2022, and the spread widened further.

Over this period, mortgage rates rose faster than the 10-year Treasury yield, and the spread widened substantially, and in September 2022, the spread widened past 3.0 percentage points, the widest since 1986. Then the spread started to narrow. But this year, the spread has widened again, including over the past three weeks.

Over the past five decades, there were not many years when the spread was this wide.

Between July 1981 and July 1982, the average 30-year fixed mortgage rate was above 17%, and briefly above 18%. This was the era of the nasty Double-Dip Recession, where the second recession entailed the worst unemployment crisis since the Great Depression.

And mortgage rates were above 10% for nearly the entire 12 years between November 1978 and November 1990.

The culprit were three massive waves of inflation that caused a revolt in the bond market, and years later, long-term Treasury yields and mortgage rates remained relatively high even as inflation was subsiding to tolerable levels.

The average 30-year fixed mortgage rate didn’t drop to 5% until the Fed started QE in 2009, which included the large-scale purchases of MBS, which helped push down mortgage rates as part of the Fed’s scheme of interest-rate repression and asset-price inflation.

But then in 2021, inflation began to rage and put an end to it.

The Fed’s QT and the spread. The Fed has shed $2.3 trillion in securities from its balance sheet through QT so far. Two months ago, it slowed the Treasury QT to just $5 billion a month. But it continues shedding MBS at whatever pace they come off the balance sheet, mostly through passthrough principal payments as mortgage payoffs (sales or refis) and principal portions of mortgage payments are forwarded to the holders of MBS, such as the Fed.

MBS have been coming off the balance sheet at a rate of about $15 billion to $18 billion a month. If the pass-through principal payments accelerate, for example if refis and home sales accelerate, then MBS come off the balance sheet at a faster pace.

The Fed has said many times in its official announcements that it plans to get rid of all its MBS. It stepped away from the MBS market in September 2022, and that market has been on its own ever since. This was when the spread between mortgage rates and the 10-year Treasury yield widened to 3 percentage points.

To replace the amounts of Treasury securities that mature in excess of $5 billion a month, the Fed buys Treasuries at auctions. For example, if $35 billion in Treasuries on the Fed’s balance sheet mature in one month, the Fed gets $35 billion in cash, and then re-invests $30 billion at the Treasury auctions. The remaining $5 billion roll off the balance sheet, which reduces its holdings by $5 billion that month.

This asymmetry of having stepped away from the MBS market, and thereby leaving mortgage rates entirely up to the market, while still meddling in the Treasury market, has contributed to the widening of the spread between the 10-year Treasury yield and mortgage rates.

If the Fed does what it said many times it would do – letting the MBS come off the balance sheet entirely – these wider spreads, and thereby relatively higher mortgage rates, are likely to continue for years to come

The bond market is not to be trifled with. It will be under a lot of pressure for years because it has to absorb the huge amount of new issuance of Treasury debt that the deficits will require. The debt will continue to balloon at a mindboggling rate, and all that new debt needs to find buyers.

But inflation spooks the bond market, and a dovish Fed spooks the bond market even more if inflation is re-accelerating. Investors want to be compensated with higher yields for the expected higher future inflation.

This is why the 10-year Treasury yields soared by 100 basis points even as the Fed cut by 100 basis points in September-December 2024. The Fed learned a lesson and started talking hawkish and went on wait-and-see strike, to tamp down on these surging long-term bond yields because they really matter for the economy, for the corporate bond market, for the housing market, for long-term corporate investment, etc.

During the 40-year bond bull-market, the 10-year Treasury yield meandered down from 16% in 1981 to 0.5% in mid-2020. In late 2020, inflation broke out and raged in 2021 and 2022. Inflation has now cooled substantially but continues to fester.

What the bond market now wants is a vigilant Fed that brings inflation down further and keeps it down, which is what it would take to bring long-term yields and mortgage rates down. If inflation begins to accelerate again, as the Fed cuts rates, then all bets are off on long-term yields and mortgage rates.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Trump wants a 1 percent rate…how is that even possible without another event as the graph shows…

1% EFFR, 10% inflation, 10% 10-year Treasury yield, 12% mortgage rates?

Bond market says: Make my day! Been there, done that.

Just wait until upcoming deregulation measures influence the SPR, which should reduce capital required to hold against US Treasuries. Unless MBS are included, count on another bout of widening.

Wolf,

Which indicator moves mortgage rate? Fed interest rate or 10 year yield?

If this holds true and many economists are predicting similar outcome then can someone tell our president not to push Feds to lower interest rate? Is this something we are going to find out in 2026 when interest rate is 3-3.25 and 10 year yield goes to 6%?

We can’t afford another massive change in EFFR. Debt needs to be serviced, but mistakes were made in the last cycle. Debt should have been rolled into longer bonds when our last downturn occurred. The drunken sailors keep spending.

The culprit were three massive waves of inflation that caused a revolt in the bond market

PLEASE call it what it really is

MASSIVE DEVALUATION of fiat $dollar – real erosion in buying power of fiat $dollar

now worth less than .01 penny 1972 dollar

Re: “ What the bond market now wants is a vigilant Fed that brings inflation down further and keeps it down…”

That’s the tricky part, especially with more debt being added to deficit. Although I’m redundant, the added treasury issuance and expanding deficit are kinda the perfect recipe for maintaining elevated long yields.

I ran a fast chart and it’s interesting how the 30y – 10y treasury spread has just converged with the mortgage spread you cover here. That treasury spread had been well below the mortgage spread for past three years — so not sure what voodoo is afoot in that relationship??? It’s kinda strange, but, seems to circle back to inflation expectations and servicing more debt??

I actually mentioned the 10-year to 30-year spread… the 30-year yield is a big deal in this article. The wide spread caused the yield curve to steepen at the long end, and I also mentioned that. It’s a pretty big deal, this whole thing at the long end.

I think we are looking at higher interest rates for a while. Inflationary deleveraging is the likely path we are headed. The 40 year bond bull market is dead and we might see a bond bear market for a long while. 40 years? Maybe.

The Fed’s job in this scenario is to orchestrate an orderly rise in interest rates. I hope they can achieve this, but I am doubtful.

That’s why I said a while ago that the government will eventually reach a fork in the road where it can protect the stock market or it can protect the bond market, but it won’t be able to do both.

The “retail” Mortgage rate is composed of two spreads; the spread between the retail (consumer) rate and the MBS rate, and the spread between the MBS rate and the T10yr.

The first is driven by competition between mortgage originators (Rocket, etc) as well as fees and costs paid to Fannie Mae, etc. This spread was as tight as 55bps, but is not over 100bps.

The second is driven by the level of Implied Volatility (MOVE Index) as well as the shape of the Yield Curve. This is the spread I focus upon and is not at 130bps, vs its historical average of 75bps.

The Curve is still flattish, and Vols are still high, and when they normalize, this spread will also revert to normal.

This is why newly-issued MBS at 5.65% is a better investment than IG corporate bonds at closer to 4.95%.

hb

Boomers unloading houses: a crowded trade. Alas, I am one of them. I got my percs, now I expect to pay a price. Any thoughts by more informed minds on the future of this?

It’s probably better to sell now than to wait for the market to decline further, with implosions in price marking the long-term trendline.

Disturbing and problematic, with a big helping of ennui thrown in, the decline in housing prices will only continue over the next decade; there is no relief in sight.

Whip Inflation Now!!

No Instant Miracles (seen when the WIN button was upside down)

You can’t add $2.8 trillion to the national debt (with the big fat pork budget bill) and expect the cost of borrowing to go down. I’m a fiscal conservative… I guess I don’t get a political party to vote for.

You make sense!

Over the past several decades, we’ve been “painting ourselves into a corner”; slowly at first and then all of a sudden. The debt overhang can no longer be ignored.

We are in for some very painful times. More strong, but “controlled” inflation is in the cards. Powell and the Fed know this. They orchestrated the COVID inflation impulse but want to keep it “tamped” until the next wave and are waiting to see what develops with tariffs.

In the meantime, as mentioned above, the economy seems to be doing pretty well with the $2 Trillion deficit spending our leaders support.

This too can continue on for a few more years, barring some exogenous shock, of which there are many possibilities in an increasingly fractious world.

Meanwhile, enjoy your morning cup of Joe.

At two seperate dinner parties over the past year, discussions happened to turn to “stupid high interest rates” and “mortgage rates are crazy”. Being the idiot I am and with weakness of self control, I couldn’t help but chime in and remind the group that today’s interest rates aren’t high, that in fact, they’re normal-ish.

It’s now been several months since the last party. We’re still waiting for our next invitation.

Needles to say, my wife was not pleased.

My goal in life is to never go to a dinner party again.

I stopped going to party quite some time back and found my peace ✌️

Thanks for this advice. In a situation like this, I’ll just ask them to pass the wine.

That’s because these types of “dinner parties” are likely full of people who have lots of stocks. I think these types of parties are full of people who know that on some level, permanent plateau of high stock prices requires low interest rates. If the “new normal” is 4-5%, eventually stocks will fall, or at least level out for a decade or more.

Anyone who owns stocks can sell them all tomorrow for cash. Not so for a house.

Sort of. Any one person who owns stock can sell them all tomorrow for cash. But what has kept prices high is a lack of selling pressure, which basically means that it’s a collective desire to hold, and not sell, that keeps prices high. So if any large number decided to start dumping, which is what happened after the Liberation Day tariffs, prices would start plummeting.

Next invite, stay home and send the wife alone…

You’ll have domestic bliss…

lol…

Next time just send the wife to the party…

The Fed doesn’t control government spending that’s causing inflation. Just returning to per capita, inflation adjusted spending levels of 2019 would whip inflation

The Fed and Congress bear joint repsobsubikty for inflation. Powell could have hiked rates in the spring of 2021 to stop the inflation caused by the March 2021 spending bill…

As long as the demand holds up it feels like we won’t get great rates, although great is very subjective. I could see putting money into 10 year treasuries at 5% but not for 30 year given a combination of my age and that the US decline, while happening, is unlikely to show up measurably in 10 years, but obviously higher over the longer term. By decline I mean the hegemony of the US dollar and potential alternatives. Competitive alternatives would drive yields up so 30 years at 5% isn’t enough risk/return for me. I think at this point it is a given with a combination of deficits and spending and demographics we won’t have any fiscal sanity.

Wolf said: “And mortgage rates were above 10% for nearly the entire 12 years between November 1978 and November 1990.

The culprit were three massive waves of inflation that caused a revolt in the bond market,”

————————————

What was the root cause of these three massive waves of inflation?

There was no single “root” cause, though among the triggers were the Vietnam war funding and the 1973-4 Oil Shock, followed up by another Oil Shock. Inflation was already high before the oil shocks. Inflation had been accelerating since the mid-1960s. The first wave peaked in 1970 (6%), the second wave in 1974 (12%), and the third wave in 1980 (14%). There was a 4th wave of inflation, a straggler wave, that peaked in 1989/90 (over 6%). After 1991, inflation calmed down in a sustainable manner.

The federal funds rate was pretty high during that time, usually well above the CPI inflation rate. It peaked in 1969-70 at around 9%, in 1974 at around 13%, in brief periods in 1980 and 1981 above 18%, and in 1989 at 10%.

Books have been written about those waves, and why it took so long to get inflation back down, and why there was such a high price to be paid to accomplish that and only slowly (the Double Dip recession, and that second “dip” was really terrible).

Once Warren Buffet (the world’s best investment genius as of this writing) asked fed chair Vlocker, “what can you do?”

Vlocker responded

“There is not much we cannot do”

What is the correlation between the size of the FED’s balance sheet and M2?

M2 is a ridiculously bad measure of anything. Look up what accounts it includes and excludes.

Isn’t the spread between mortgage rates and 10 year rates a measure of uncertainty of future inflation? Treasuries have payment streams that are set. The buyer knows what they will get and any change in inflation won’t change what they are owed.

MBS’s backed by FNMA or Freddie also have risk free payments, but those payments are uncertain. There is an expectation of the timing of future repayments, but these can change based on the prepayment speeds of the borrowers underlying the MBS’s.

Lower inflation, results in lower interest rates which drive higher refinancing and lower MBS payments. Alternatively, higher interest rates, decrease refinancings and ‘lengthen’ the period of repayment.

These are adverse outcomes because declines in interest rates mean these prepayments occur at the time the holders of the securities want to keep the higher interest payments. Similarly, if payments are slower in a high interest rate environment, investors aren’t able to take advantage of those higher rates because of slower prepayment speeds.

We’re currently in a market where (1) a recession is coming, which will lower rates, or (2) tariffs that are fully implemented which drives inflation, resulting in higher rates. The tension between these two can keep the 10 year rate in a holding pattern, but negatively impact the price of MBS’s.

You forgot scenario (3) a recession is coming, which the Federal government will try to spend its way out of (again) with a glut of deficit spending which will send rates soaring – despite what the Fed does.

Wolf has mentioned this a number of times – the bond markets are less interested in the Fed moving the needle (with the EFFR) than they are in inflation and government debt – and how that translates into credit risk. The government’s credit rating has already been downgraded… just keeping borrowing and borrowing and see where that gets you.

When the Fed say ‘buys 30 billion’ of Treasury auctions, do they bid non competitive? Thanks.

Yes, the Fed gets whatever it bids to buy at the yield established at the competitive auction. What the Fed buys is on top of the regular offering. It doesn’t take away from other bidders. It doesn’t influence the auction at all. So if the regular offering is $40 billion of notes, and the Fed bids $5 billion, the government sells $45 billion in total at the yield established at the competitive auction.

Another way to look at it maybe: People are not expected to be in their house for an average of 10 years anymore so mortgage rates are decoupling to the 10-year rate.

I bought 7 years ago, if I sold my house and bought a new one at the price I sold for – my payment is 1.5-2x. If I wanted to move up to a bigger/nicer house I’m between 2-3x for difference to the upside.

Stuff happens. But if stuff doesn’t happen I’m not going anywhere – where if prices and interest rates didn’t both jump I’d probably be looking for the next place right now. Many people like my pushing away from the 10yr average time at each house.

with the passing of the bb bill, do you think that the bond vigilantes will come out like they did in 93-94?

‘spreads get our attention because it’s via spreads that the market expresses its worries and fears.’

We have a Christmas stocking of worries and fears. But at least they are ‘known unknowns’ Here is one not on the radar yet: California, on the coast, has past Japan to become world’s 4 largest economy, and is 14 % of total US economy. How much longer will it tolerate things like National Guard troops being deployed against the Governors objections?

“How much longer will it tolerate things like National Guard troops being deployed against the Governors objections?”

Forever. All we’ll do is sue. And when that leads to nowhere, end of story.

There is a much higher chance that Alberta will leave Canada (Premier Smith already agreed to hold an independence referendum in 2026 if there are enough signatures on the petition) than California agreeing whether to split into three different US states, or remain one state and think about steps to think about thinking about a referendum.

If there is a referendum in Alberta in 2026, I doubt that there will be enough votes to trigger the next step to independence. But Albertans are way ahead of Californians in that respect. Here it’s just a tiny minority that has been agitating for decades fruitlessly to be taken seriously about their nutty drive for California independence.

But if Albertans succeed in their independence procedure, what would they do? Would they then go through the procedures to become the 51st US state? Is that what they want? We’ll welcome them with open arms and big smiles, for sure. But is that what they want?

Rates need to stay here or move higher.

Many houses on the market with sellers determined to get the big payday they feel entitled to. Refuse to credit the idea that higher rates means their homes are worth less. They hang on because the FED has always come through in the end and they are sure rates will go down and buyers will return.

That fever needs to be broken. Higher for Longer…but I’m sure many brilliant manipulator minds are thinking hard about how to get those rates down without breaking the bond market.

Secretary Bessent last week says he now looks for Stable Coins to account for 3 trillion in Treasury borrowing.

The Genius act, specifically bans payment of yield by issuers so effectively he hopes for a big pool of Treasury buyers who will be indifferent to yield.

To your first and second paragraphs:

In the markets I watch (Northern Nevada – e.g Reno and vicinity) as well as Northern Montana (e.g. Kalispell/Whitefish) I am FINALLY beginning to see a small break in pricing – namely listing price at or near purchase price from 2021-2023. On a few properties. Which aren’t selling. But too many are at 2022 price (supported by a 3% mortgage rate) plus expenses plus a profit of 10-20%. I’m ALWAYS early, but I think that this summer may be the moment where prices finally start to turn down. Sellers may finally wake up to the fact that they’re not going to get $625k for the house they paid $499k for three years ago.

Having said that, there are SO many Realtors ™ who are happy to tell a potential client that, yes, you can indeed expect potential buyers to pay DOUBLE what you paid for your house way back in 2022! Or TRIPLE what you paid when dinosaurs roamed the earth in 2018!

I think Wolf listed the stages of pricing of houses in a market like this (much like the stages of grief). We should start calling it the “Richter stages of house selling grief”.

Boomer are dying off (and their houses with the “original finishes” from 1984) are up for sale. At a point, people just want the money out of the property. Add in divorce and relocation, prices will start to move.

Two unrelated points:

1) Look at the pictures of interiors of properties for sale and note how many are either obviously staged or empty. Empty houses have real carrying costs, even if they are unmortgaged. Especially for inherited houses – getting 80% of what you want is better than getting 0% of a wishing price.

2) In Wolf’s discussion of the late 1970’s / early 1980’s inflation / recession (these were brutal – I lived through them as a teenager/young adult) the one factor that partially mitigated the pain were COLA’s in union contracts which flowed through to wages generally. Yes prices went up, but wages went up as well. Maybe not as much as inflation, but still up. So as long as you could make the first year or two of the mortgage payment, the real value of the debt went meaningfully DOWN with respect to wages. It definitely lessened the sting. Today, COLA’s are long gone and wages definitely DON’T pace inflation.

As far as I can see, there’s no real formal unbiased research or white papers for stable coin — especially by Treasury. There is a lot of hype and con games and grifting.

I did see a beginners fyi attempt from Fed recently, which concludes:

“ Our research aimed to present several areas worth further interrogation, and our resulting analysis raises more questions than it answers”

That from: February 23, 2024

Primary and Secondary Markets for Stablecoins

Also, from TBAC:

TBAC cited a report by Standard Chartered (NASDAQ: SCBFF) in which the bank predicted that stablecoins could grow into a $2 trillion market by 2028. The committee expects half of this to be invested in U.S. government securities, translating into over $1 trillion in demand for the sector.

Re: “ Treasury buyers who will be indifferent to yield”???? Huh??

It’s a crazy world, but the enthusiasm here looks like biased hype — I can’t believe trillions in cash will be diverted into hybrid *hitcoins, cause a few grifters are selling that BS.

FBI stopped investigating Coinbase & Coinbase becomes part of the S&P 500,…

So crypto must all be legit…right?

In other exciting news, Don Jr’s stablecoin was used by Zach Witkoff so UAE could invest $2Bn in Zhao’s Binance (which is banned in the US).

(Lemme see if I got this right – felon’s kid teams up with slumlord’s kid to run $2Bn bitcoin scam with another felon’s money laundering crypto scheme….?)

Sure, no problem there.. I’m gonna double down, back up the truck and load up on Circle crypto…

Don’t think Treasury back bitcoins will increase demand for Treasuries.

It’s just demand substitution – retail that bought Treasuries switch to Treasury backed bitcoin for whatever reason (usually tax evasion), but overall demand will be close to unchanged….

Wolf, I can’t recall right away if you covered this elsewhere…

How big a “buyer” of Treasury securities is the Fed compared to the total purchases every month, quarter, year? If sizable! I’d assume that would influence interest rates a lot.

The Fed now replaces most of its maturing Treasury securities, except for $5 billion a month. It doesn’t add new securities; it’s a net seller as its Treasury holdings are declining by about $5 billion a month (the new reduced pace).

For the past five months through May 2025, the government sold $12.2 trillion in Treasuries ($2.4 trillion a month). All of them were just refinancing maturing securities due to the debt ceiling. The total debt remained at $32.2 trillion.

Of that $12.2 trillion in refinancings, $10.4 trillion were T-bills (they mature all the time, given their short terms), and $1.8 trillion were notes and bonds.

But after the debt ceiling is lifted, the government will sell a lot of new securities that will add to the debt, maybe $1 trillion in the space of a few months, in addition to the refinancings.

The Fed holds only $195 billion in T-bills. So they don’t matter.

In terms of Fed’s notes and bonds, about $240 billion will mature over the next six months through the end of this year, and the Fed will replace about $210 billion of them. So that’s about $35 billion a month in refinancings. The government will refinance about $360 billion a month in notes and bonds. So that’s the part where the Fed plays. The Fed will have no role at all in buying the new securities to be issued after the debt ceiling that add to the debt. That’s up to the market to absorb.

By contrast, none of the Fed’s MBS balances that come off the balance sheet are replaced. Any issuance of MBS has to be entirely absorbed by the market.

According to Grok (I’ve no idea how reliable it is), if the Fed stopped buying Treasury securities entirely, the runoff would increase to > 65B per month, > 750B per year…isn’t that pretty huge?

The answer is another AI hallucination. The runoff from maturing Treasury securities declines every year as the Fed’s portfolio shrinks. So it’s not “per year.” And it’s not “per month” either because the runoff varies widely.

The chart shows the maturity schedule of the Fed’s holdings of notes and bonds. In all of 2025, $528 billion in notes and bonds will mature. In the second half of 2025, about $213 billion will mature ($35 billion average per month). In all of 2026, $450 billion will mature, but for apples to apples: in the second half of 2026, $198 billion will mature ($33 billion average a month).

Never ask AI anything, and if you do, don’t drag it into here. It’s not my job to debunk AI hallucinations. If you get an answer from AI, take it like a man and cry into your pillow. I now delete AI-based comments.