Here’s who dumped and who bought over the years through Q1.

By Wolf Richter for WOLF STREET.

Who holds that ballooning US national debt? Who is still buying these Treasury securities that the US government issues in such huge quantity? These are increasingly iffy questions. The Treasury Department’s monthly Treasury International Capital data and the Federal Reserve’s quarterly data on US financial accounts, both released this week, provide some (surprising?) answers about foreign holders and US holders.

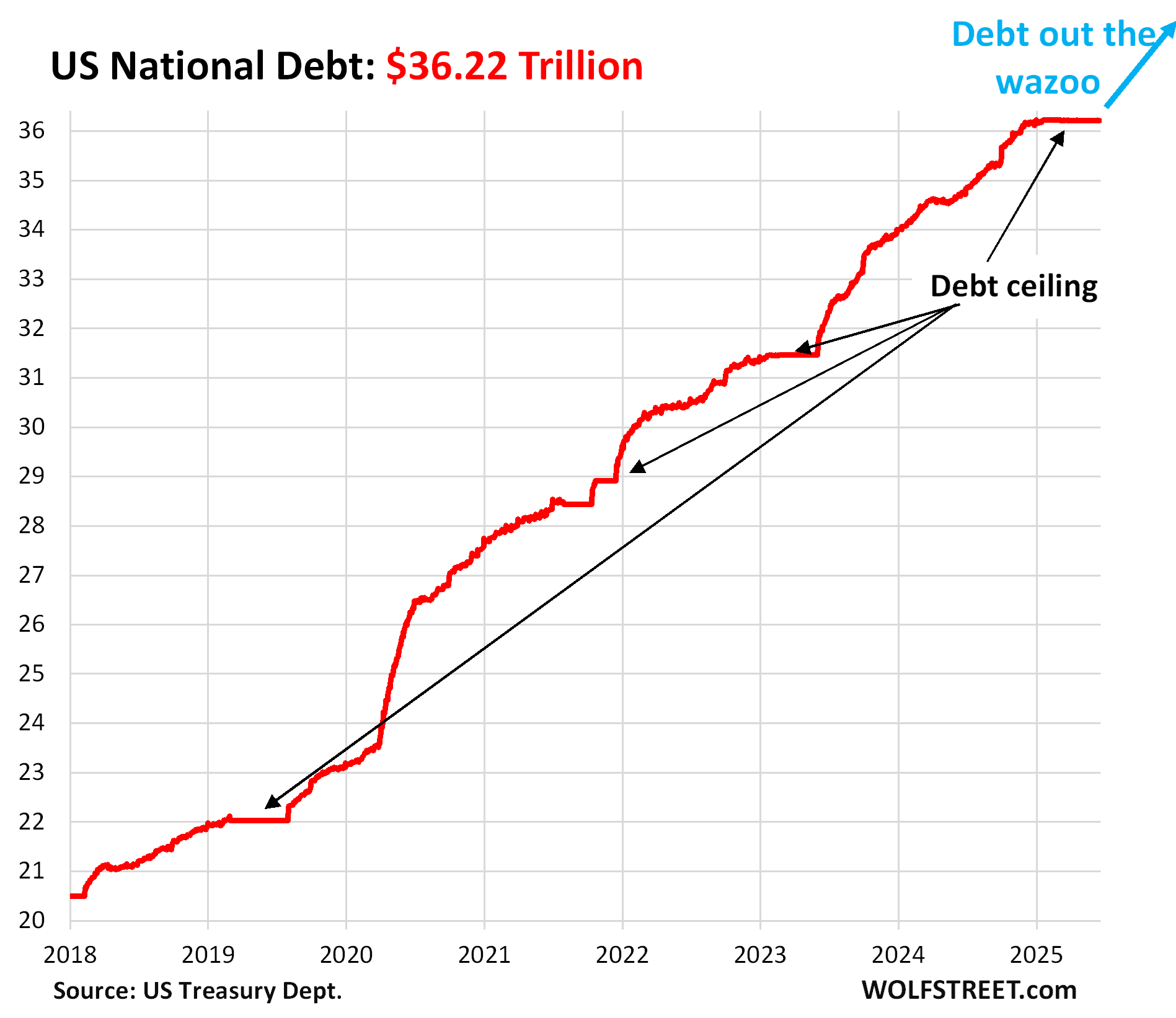

The US debt has been stuck at the “debt ceiling” of $36.2 trillion since January. After Congress makes a deal with itself to raise the debt ceiling, the debt will spike by hundreds of billions of dollars as the government shifts money around and issues huge amounts in T-bills to refill its depleted checking account. In the chart, the flat parts followed by spikes show that dynamic.

Who held this $36.2 trillion in Treasuries at the end of Q1?

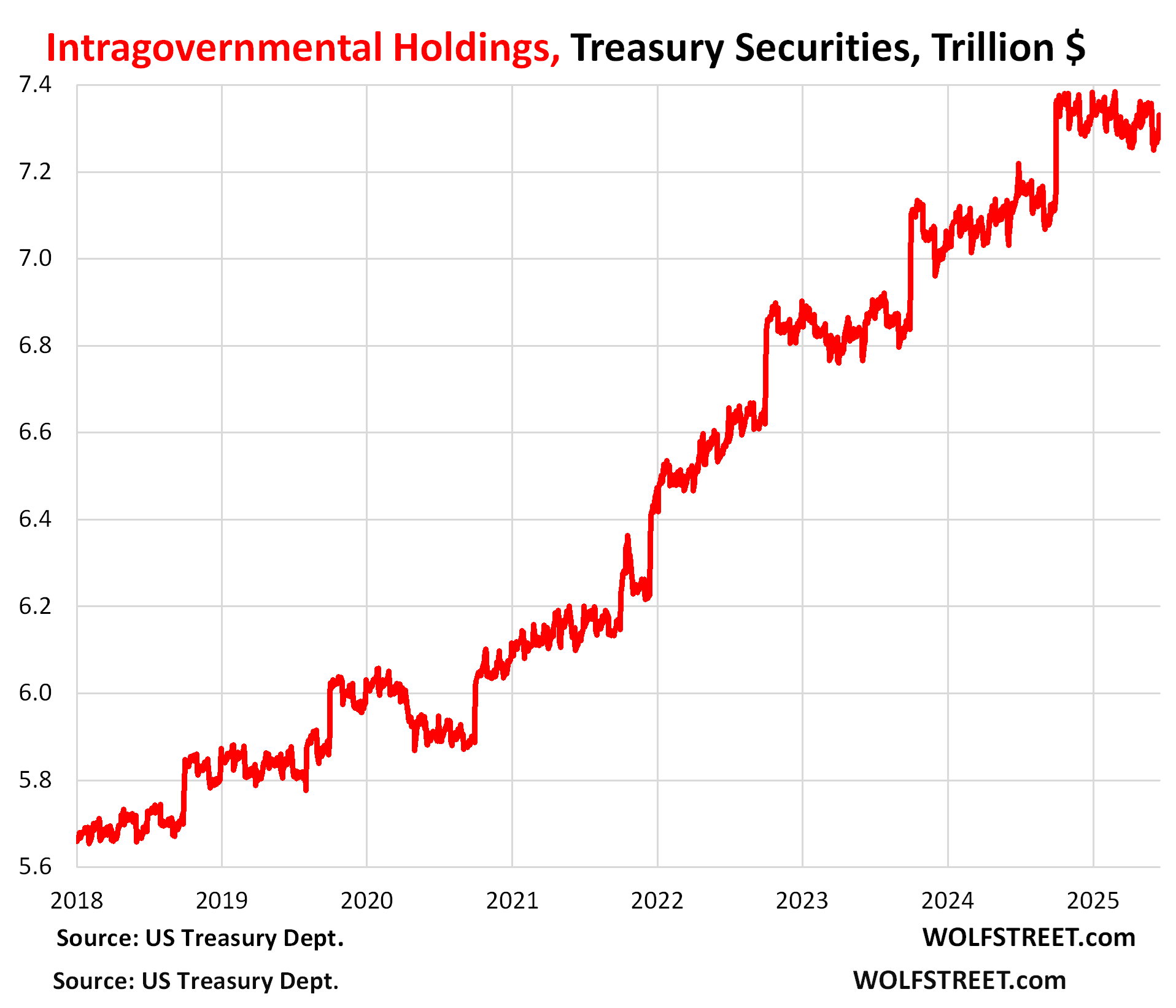

US Government entities: $7.3 trillion. These “intragovernmental holdings” are Treasury securities held by federal civilian pension funds, military pension funds, the Social Security Trust Fund (I discussed the Social Security Trust Fund holdings, income, and outgo here), the Disability Insurance Trust Fund, the Medicare Trust Funds, and other funds. These securities are not traded in the bond market and are not subject to the vagaries of that market.

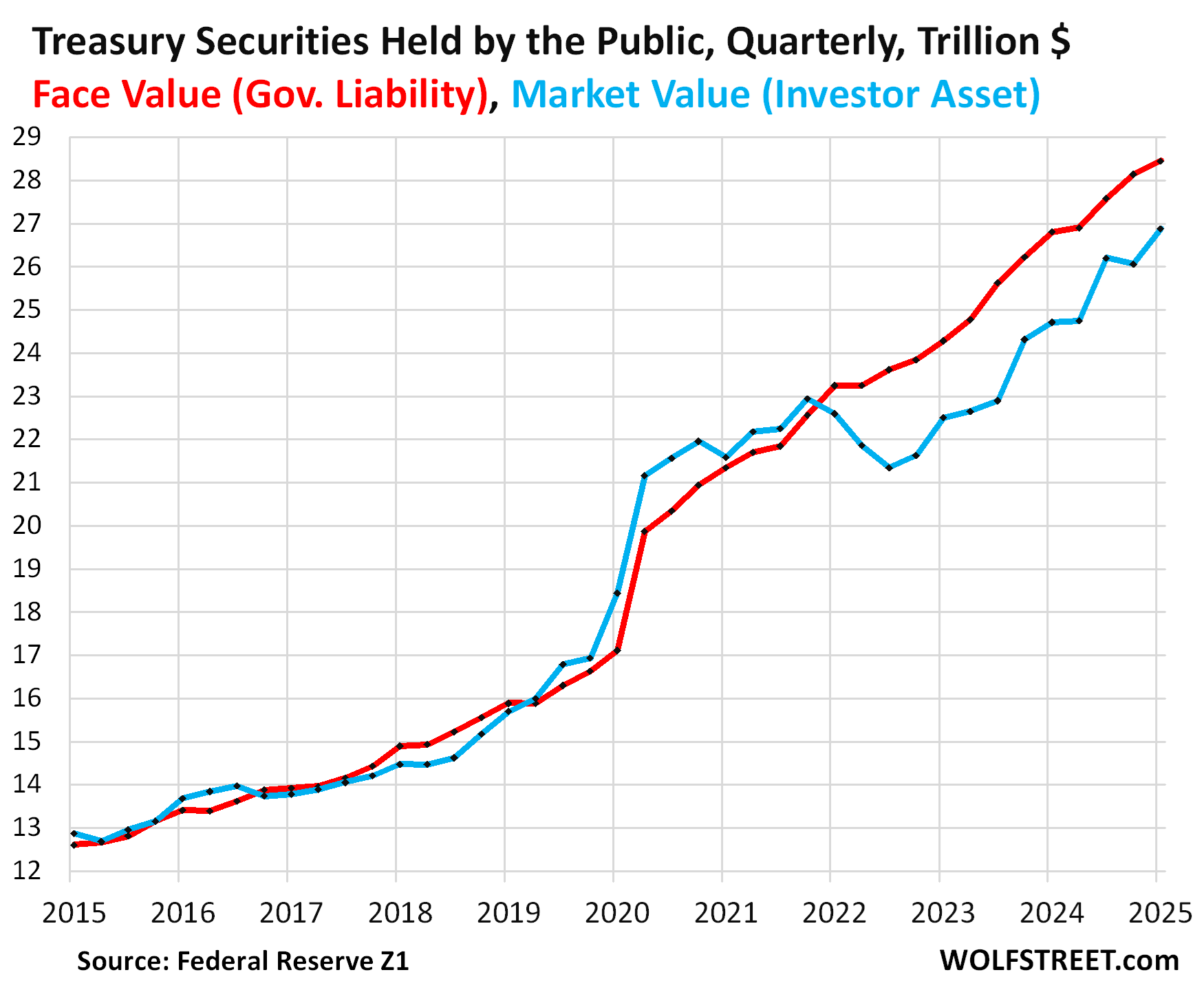

Debt held by the “Public”: Liability versus Asset.

When the government sells Treasury securities at auction to the public, the government owes the public the face value of these securities when they mature, and for the government, these Treasury securities are a liability measured at face value (see above charts).

But for investors, these securities are assets that are traded in the market at prices that change from second to second. Rising yields mean falling prices; and falling yields mean rising prices. Since early 2022, yields have risen substantially.

So from the government’s point of view as a liability, the Treasury debt held by the public was $28.45 trillion at face value at the end of Q1, according to the Z1 data from the Federal Reserve (red in the chart).

But seen from the holders’ point of view as an asset, the same debt held by the public had a market value of $26.88 trillion, also according to the Z1 data from the Federal Reserve (blue in the chart).

So at the end of Q1, the market value of the debt held by the public had dropped by $1.57 trillion compared to face value. But during QE, which repressed long-term interest rates, the market value of the debt was higher than face value (the blue line is above the red line):

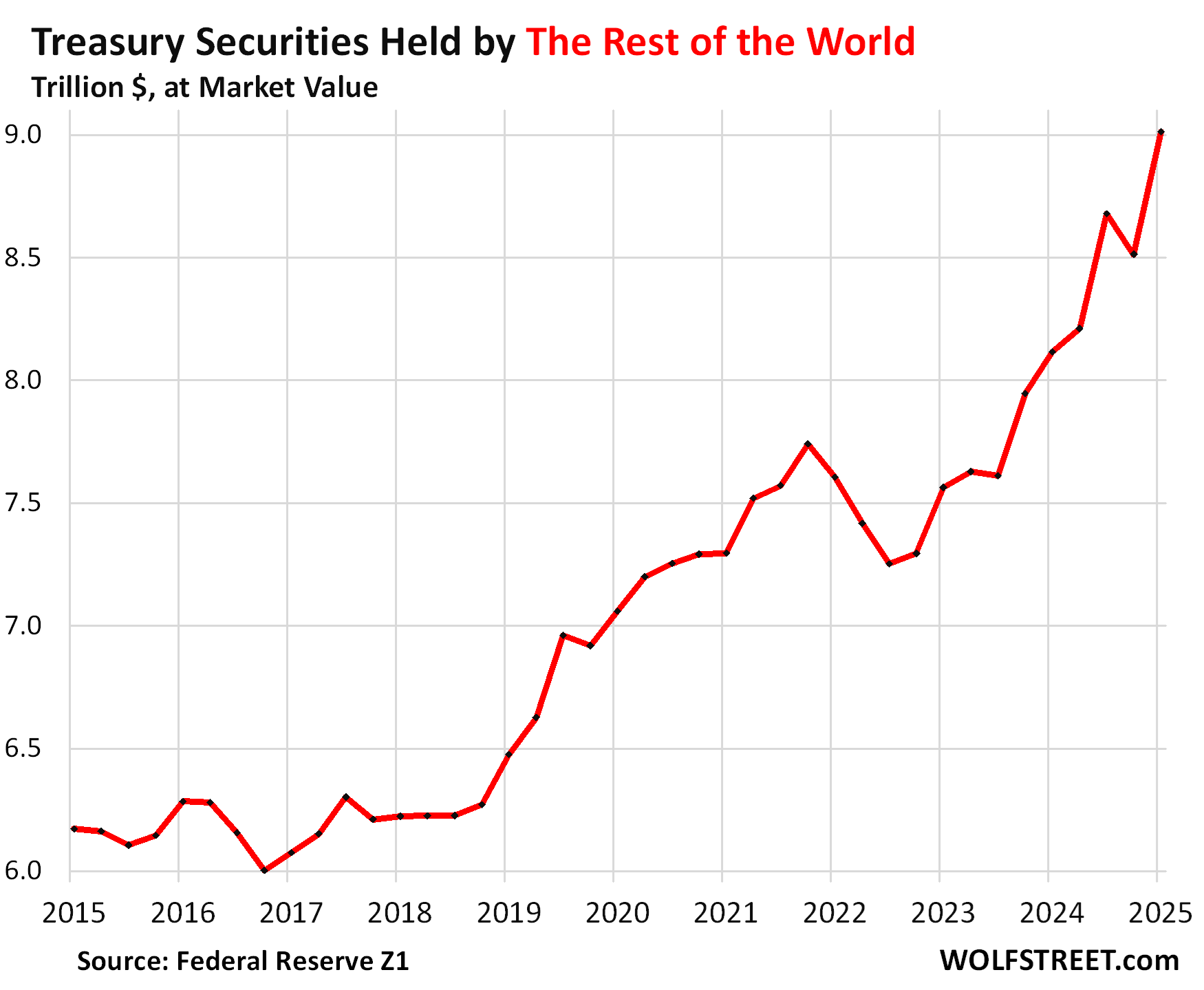

So who is this “public” that holds this $26.88 trillion at market value?

Foreign holdings at market value reached $9.01 trillion at the end of Q1, or 33.5% of the debt held by the public at market value, according to the Fed’s Z1 data, indicating strong demand from foreign holders.

In a moment, we’ll look at their holdings at face value – the amounts that the government actually owes foreign entities.

Foreign holdings at face value… Treasury Department’s monthly Treasury International Capital data through April, released this week, details foreign holdings from the government’s point of view, as a liability, the amount it owes at maturity, so at face value.

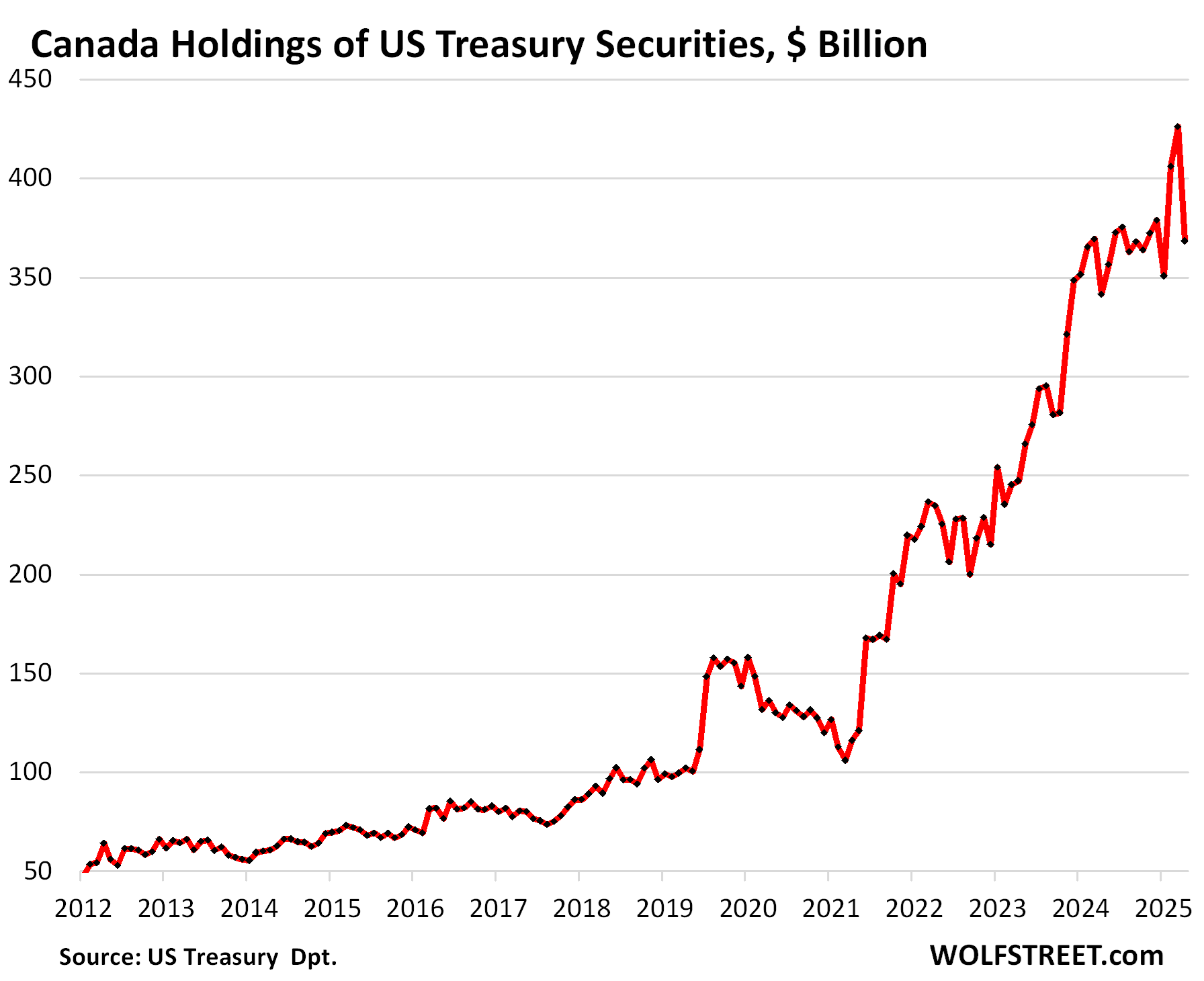

In April, foreign holdings at face value dipped by $36 billion from the record in March, due to the $58-billion plunge in Canada’s holdings.

Biggest foreign holders at the liability level:

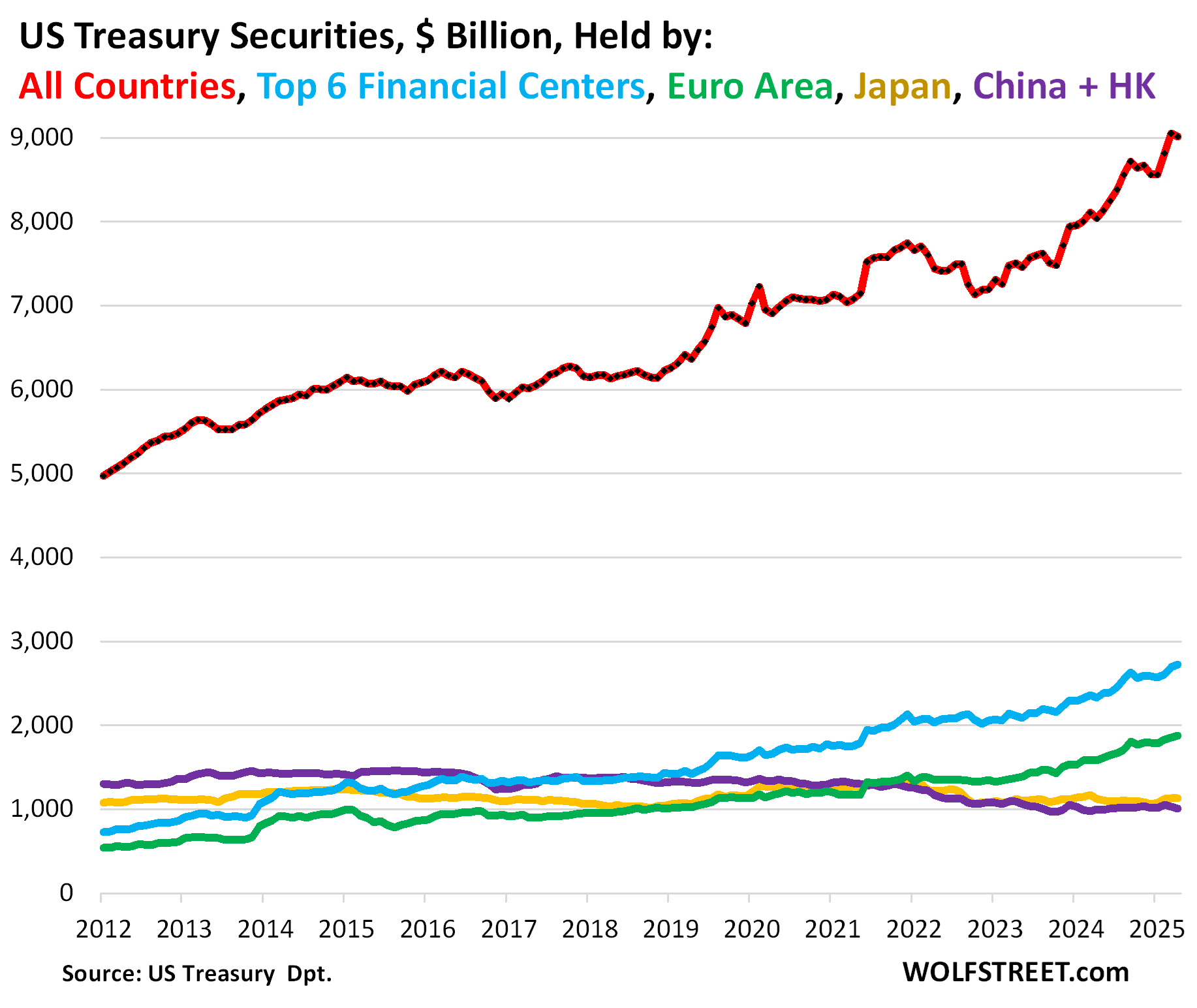

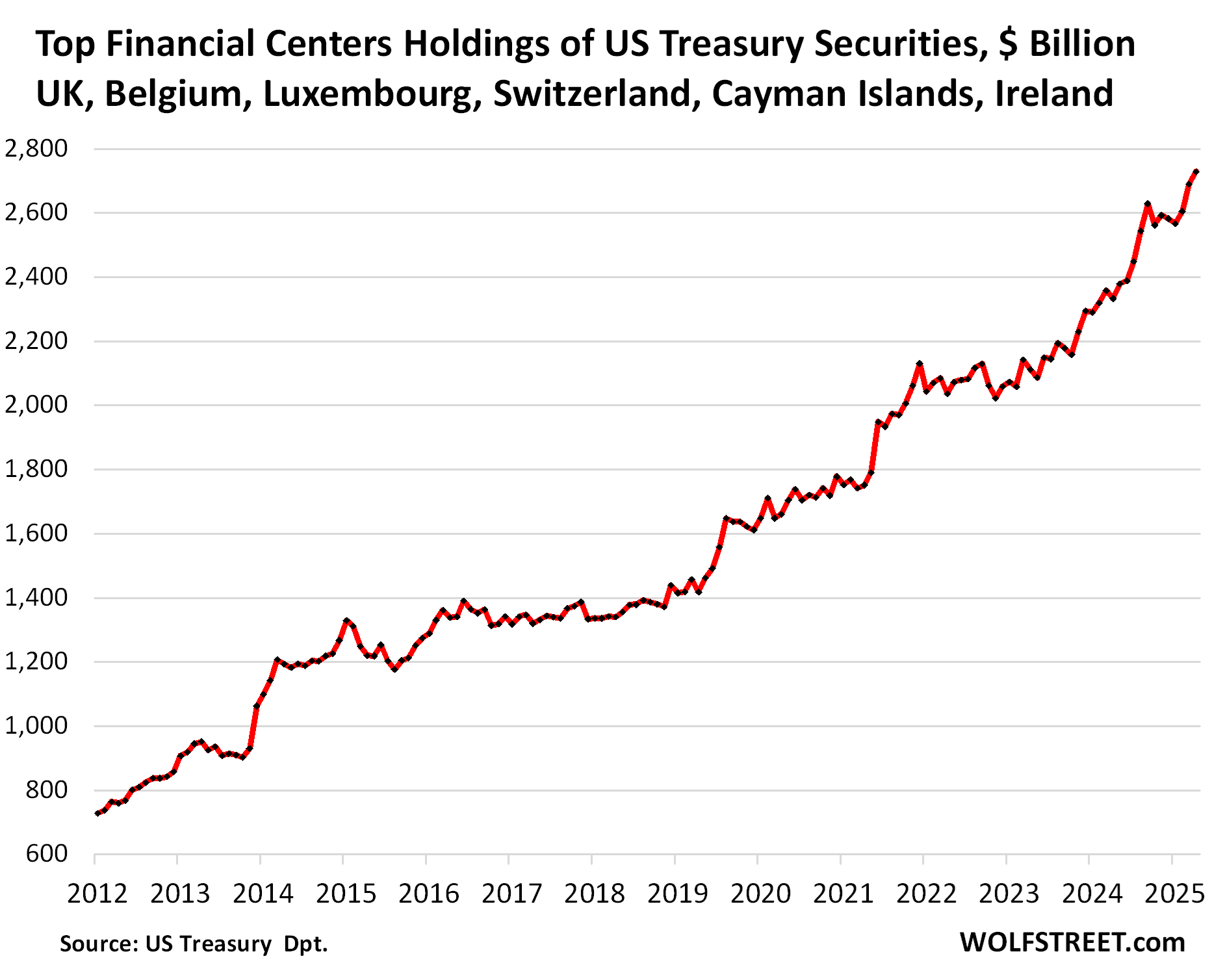

The importance of China and Japan continues to fade as Europe, financial centers, Canada, India, Taiwan, and others have been piling them on:

- The top six financial centers: $2.73 trillion (blue)

- Euro Area: $1.88 trillion, which includes three of the financial centers (green)

- Japan: $1.13 trillion (gold)

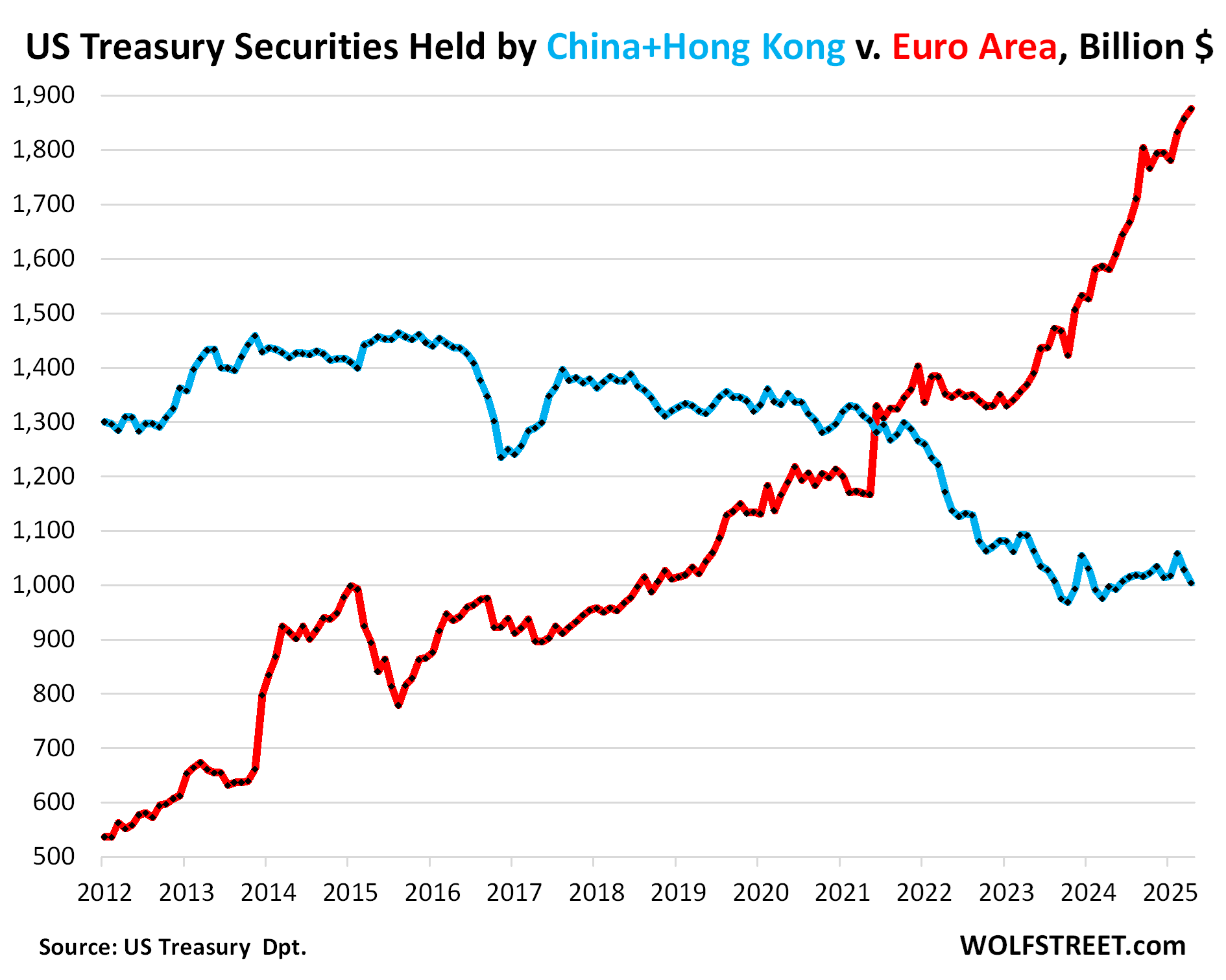

- China and Hong Kong combined: $1.0 trillion (purple).

Top 6 financial centers held a record $2.73 trillion, up by $396 billion year-over-year.

US corporations hold a portion of these Treasury securities to park their overseas profits there to avoid US income taxes.

China unloads, Euro Area loads up: The Euro Area – which includes the three financial centers Luxembourg, Belgium, and Ireland – has been purchasing Treasury securities on a large scale over the years. The Euro Area now holds nearly twice as much as China and Hong Kong combined.

Over the past 12 months through April, the Euro Area added $295 billion, bringing its total holdings to a record of $1.88 trillion at face value.

Over the past 12 months, China and Hong Kong added $7 billion, despite shedding some securities in March and April. Over the long term, they have been reducing their holdings of Treasury securities. At the end of April, their total holdings were $1.0 trillion, down by 31% from 2015.

Canada became a large buyer in the wake of the pandemic, more than tripling its holdings in a three-year span, to a record $426 billion at the end of Q1.

But in April, Canada shed $58 billion, and total holdings plunged to $368 billion, back to February 2024 levels. That was a historic plunge – not surprising though.

Other big foreign holders include Taiwan (holdings rose to a record $299 billion), India (holdings dipped to $233 billion), and Brazil (holdings dipped to $212 billion).

US Holders are 66.5% of this “public.”

So now we return to market-value holdings, according to the Federal Reserve’s Z1 data.

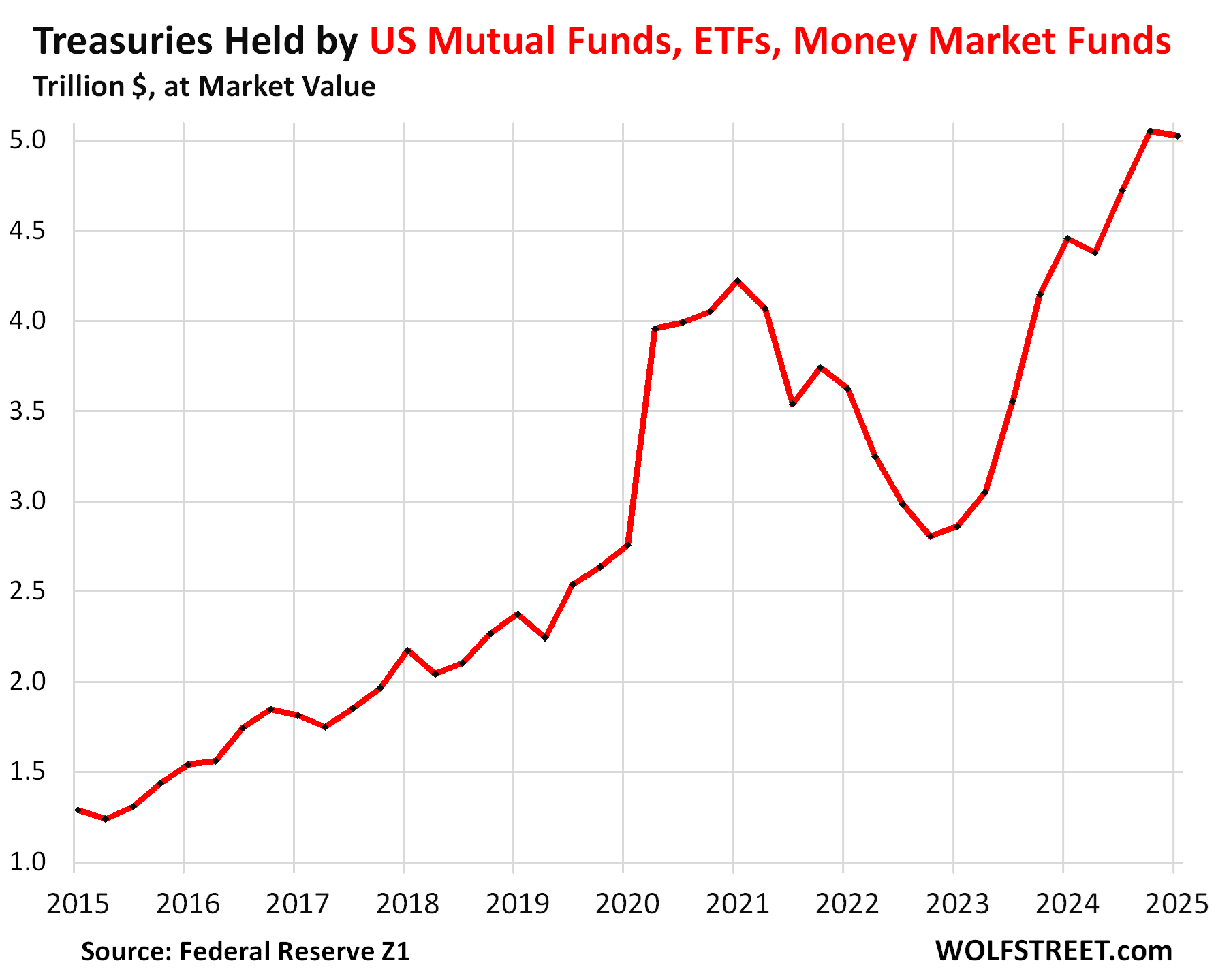

US mutual funds, ETFs, and money market funds held $5.02 trillion at the end of Q1 at market value, or 18.7% of the debt held by the public.

- Money market funds: $2.88 trillion – amid a surge of money market fund balances held by households

- Mutual funds: $1.54 trillion

- ETFs: $605 billion.

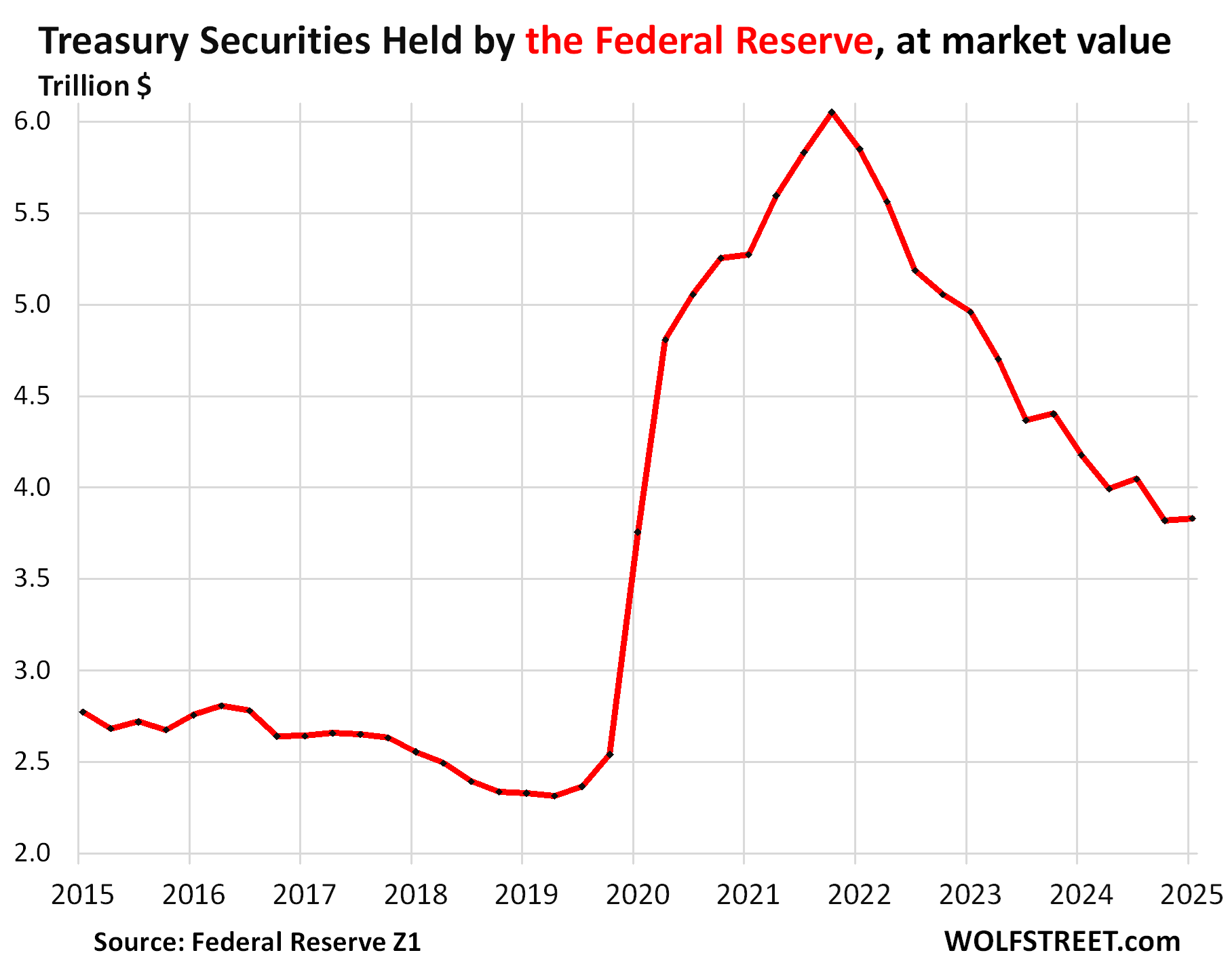

The Federal Reserve held $3.83 trillion of Treasury securities at market value, or 14.3% of the debt held by the public.

On its weekly balance sheet, the Fed accounts for its assets at face value, not at market value, but it discloses the unrealized losses – the difference between face value and market value – in its quarterly financial reports.

Under its QT program, the Fed has shed at face value $1.56 trillion of Treasuries since mid-2022.

But at market value, the Fed’s holdings of Treasuries declined by $2.22 trillion since mid-2022, on this mix of QT and lower market value of its remaining holdings.

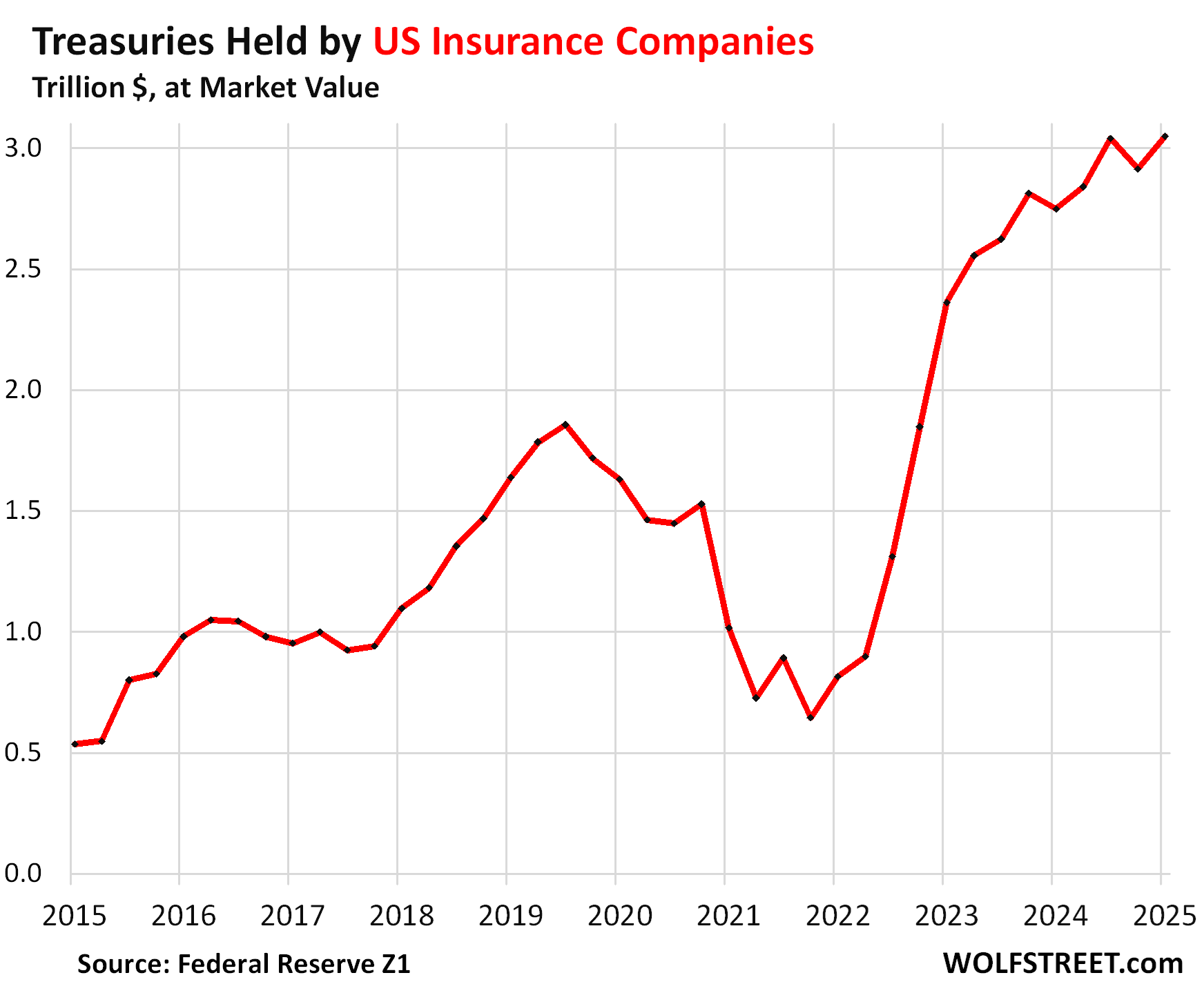

Insurance companies held $3.05 trillion of Treasury securities at market value, or 11.3% of the debt held by the public, of which property and casualty insurance companies held $2.86 trillion and life insurers held $191 billion.

Insurance companies have been huge buyers after yields started to rise, and Treasuries started to make a little more sense again. Since mid-2021, they multiplied their holdings by nearly five.

Also note how they got out of Treasuries during the Fed’s interest rate repression, starting in mid-2019 when the Fed started cutting rates again, and market prices were rising. Insurers got out, while banks were loading up.

As prices were rising and yields were falling, insurers shed two-thirds of their holdings. So when yields started rising again in 2022, and banks took huge losses and several collapsed in early 2023 because of it, insurers came out with low holdings of these securities, and they started buying again at these lower prices and higher yields.

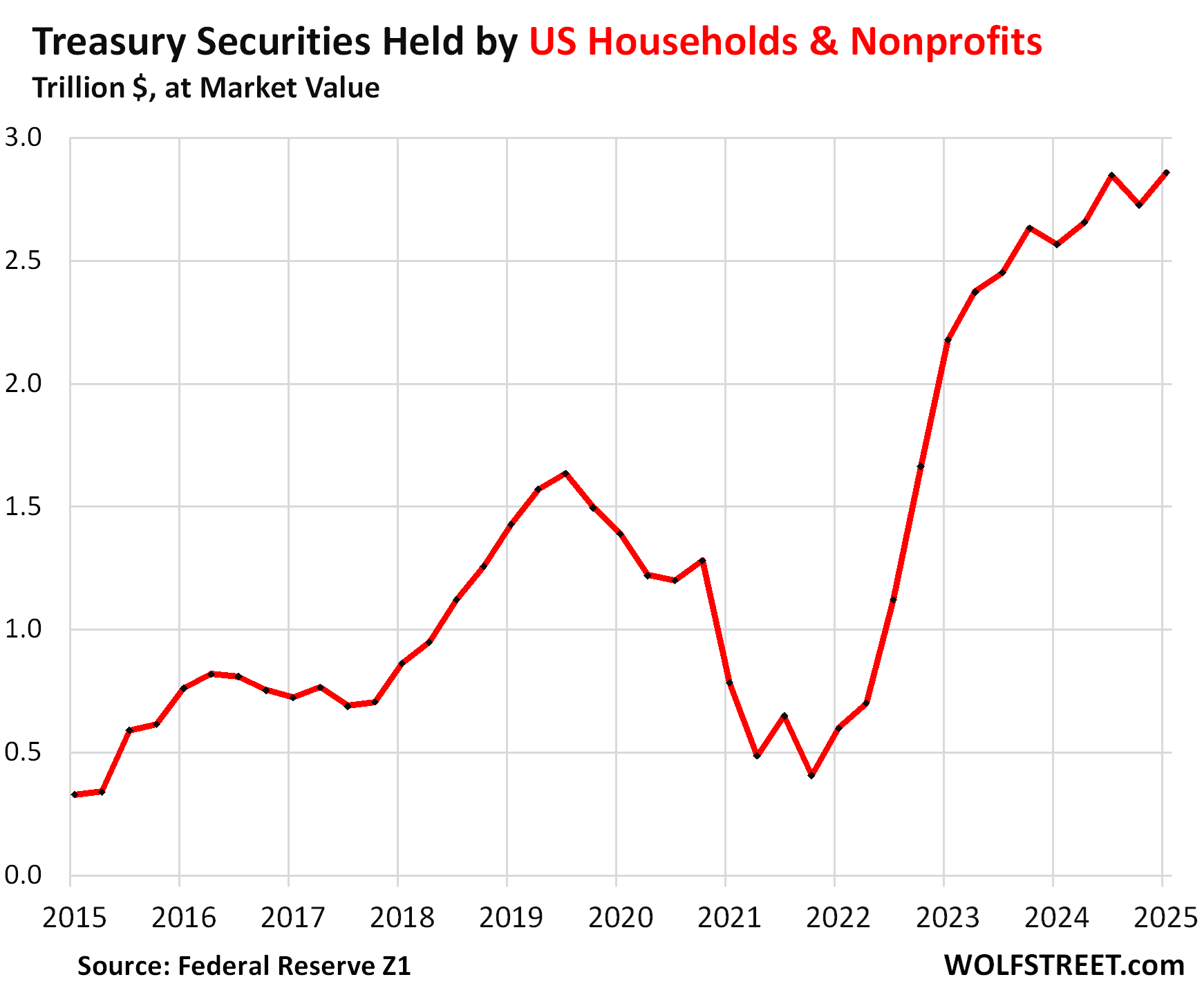

US Households and nonprofits held $2.68 trillion of Treasury securities at market value, or 10.6% of the debt held by the public. They too were the smart money, doing what insurance companies did.

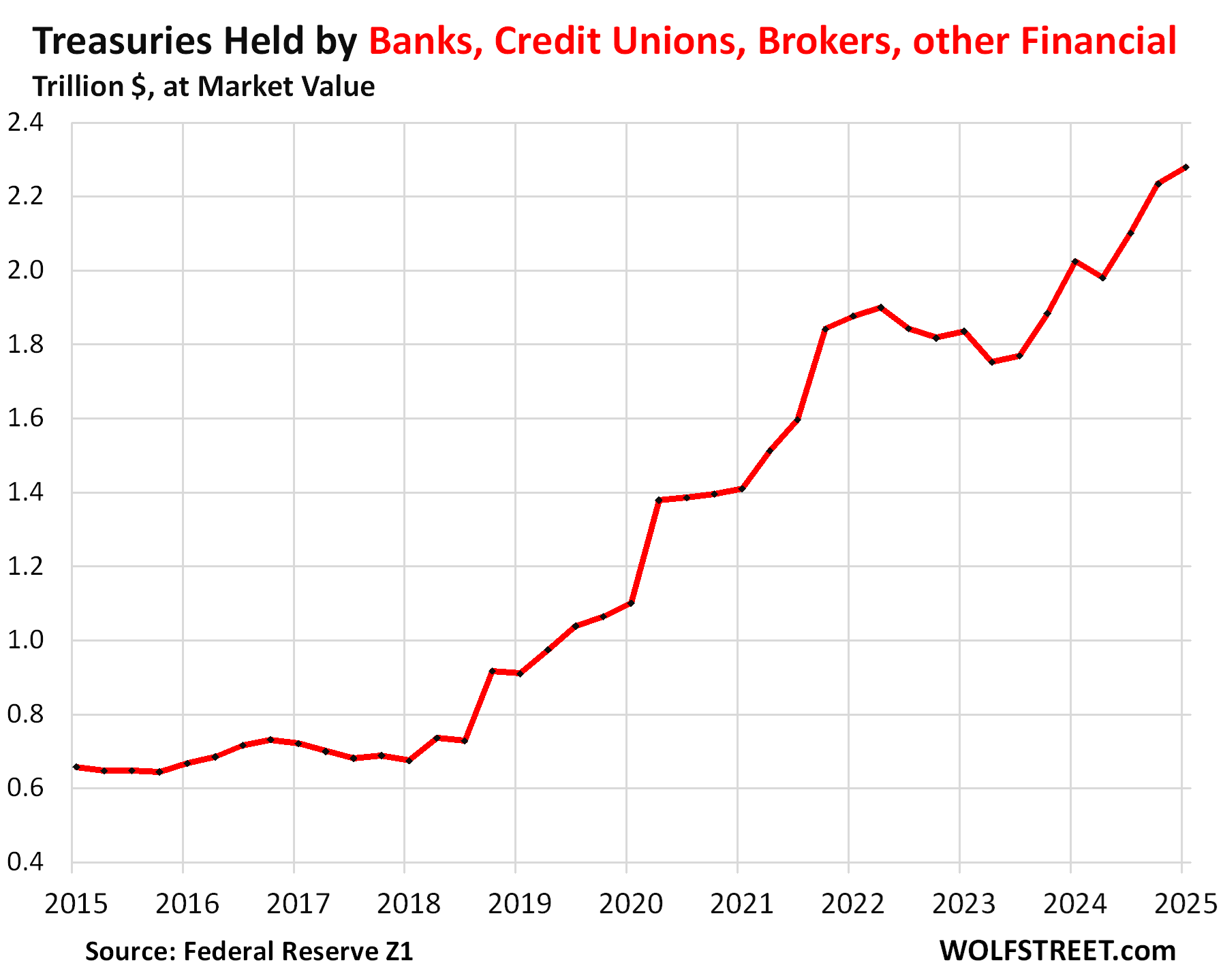

Banks, brokers, dealers, credit unions, and other financial firms held $2.28 trillion of Treasury securities at market value, or 8.5% of the debt held by the public.

Banks alone held $1.54 trillion and securities brokers and dealers held another $488 billion. They’ve had a relentless appetite for Treasuries, come hell or high water:

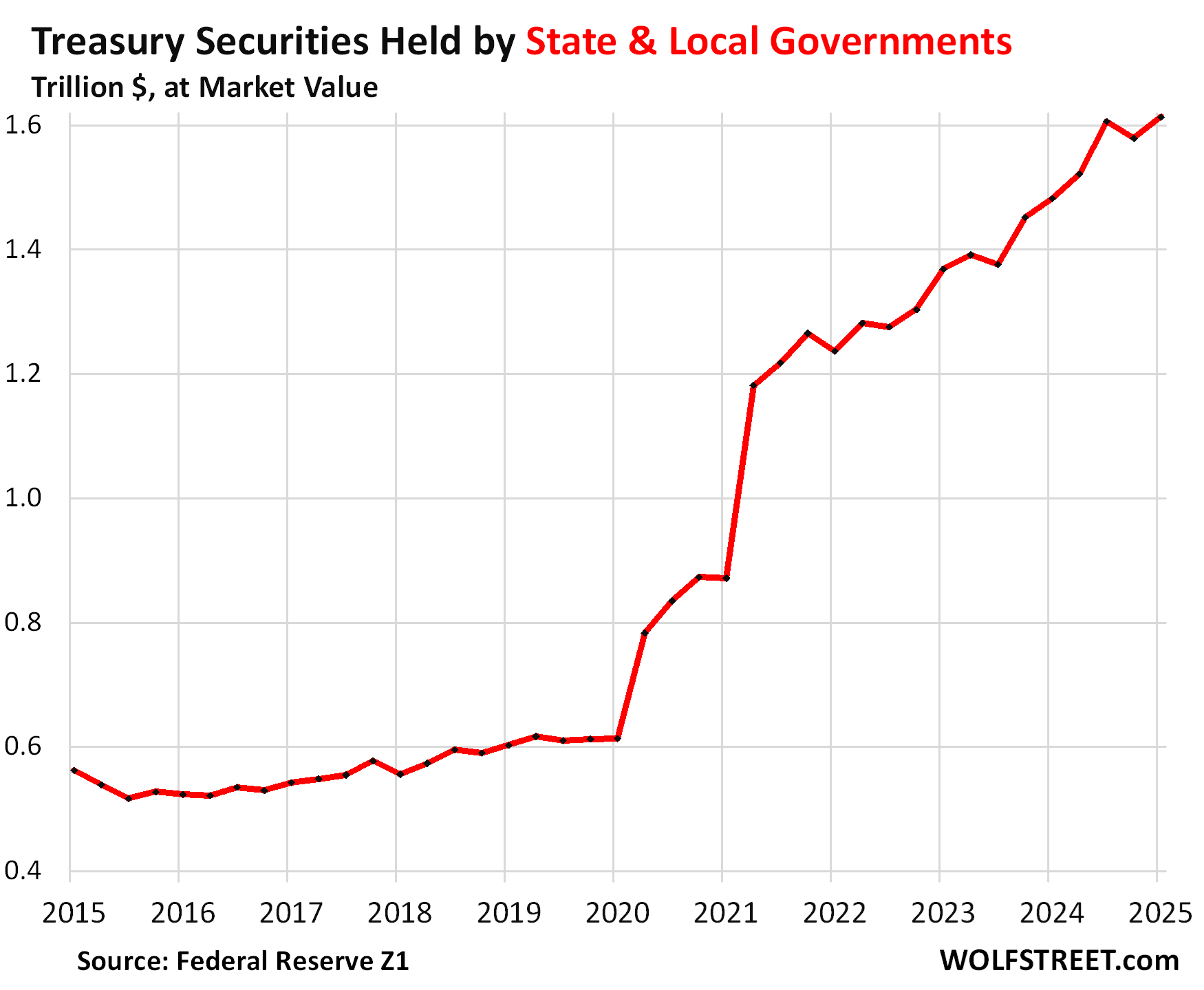

State and local governments held $1.61 trillion of Treasury securities at market value, or 6.0% of the debt held by the public.

During the free-money era, the manna from the federal government snowed upon state and local governments, and they had surpluses and increased their rainy-day funds, and so they plowed their extra cash into Treasury securities.

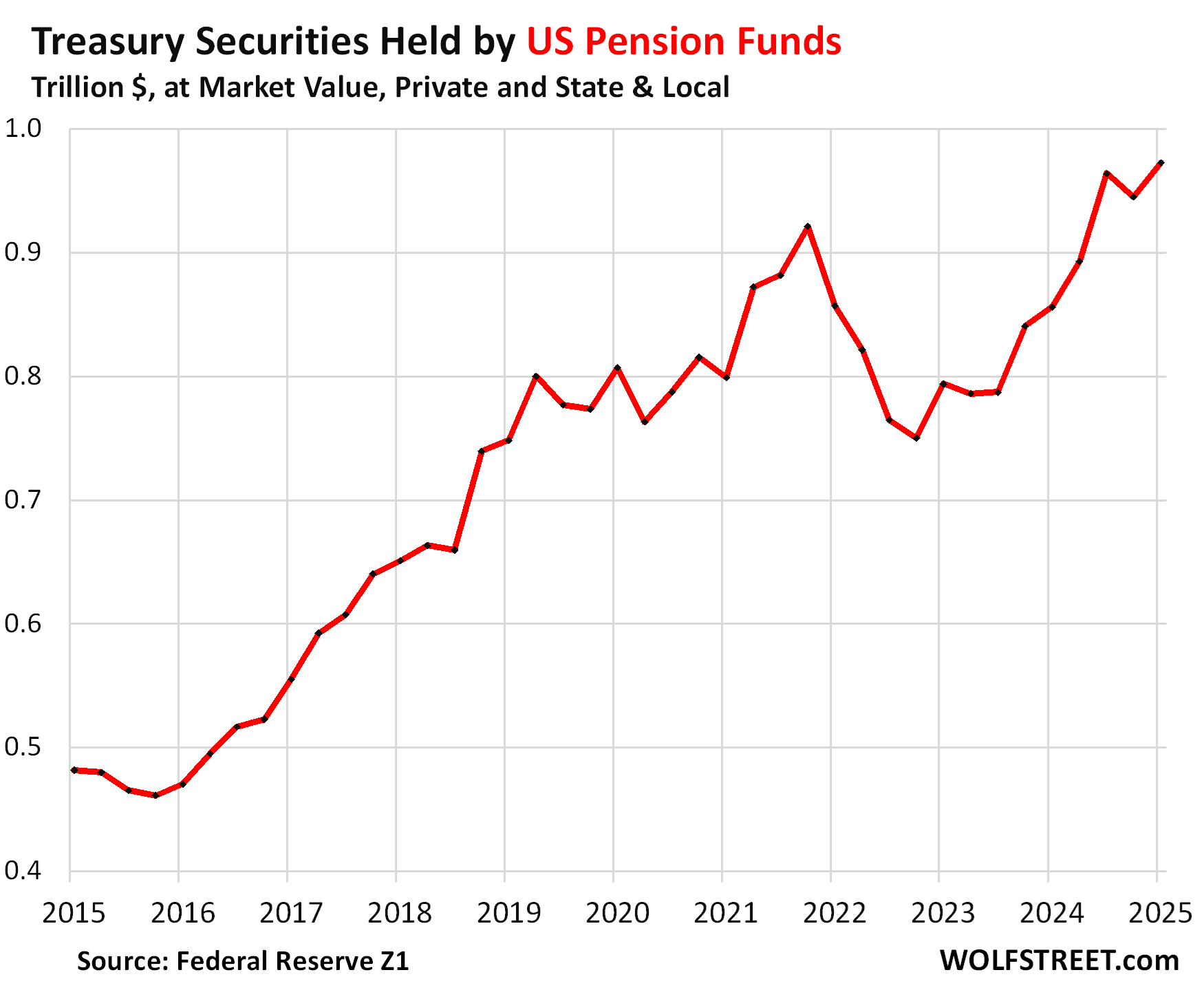

US pension funds held $972 billion of Treasury securities at market value, or 3.6% of the debt held by the public. This includes private pension funds and state and local government pension funds.

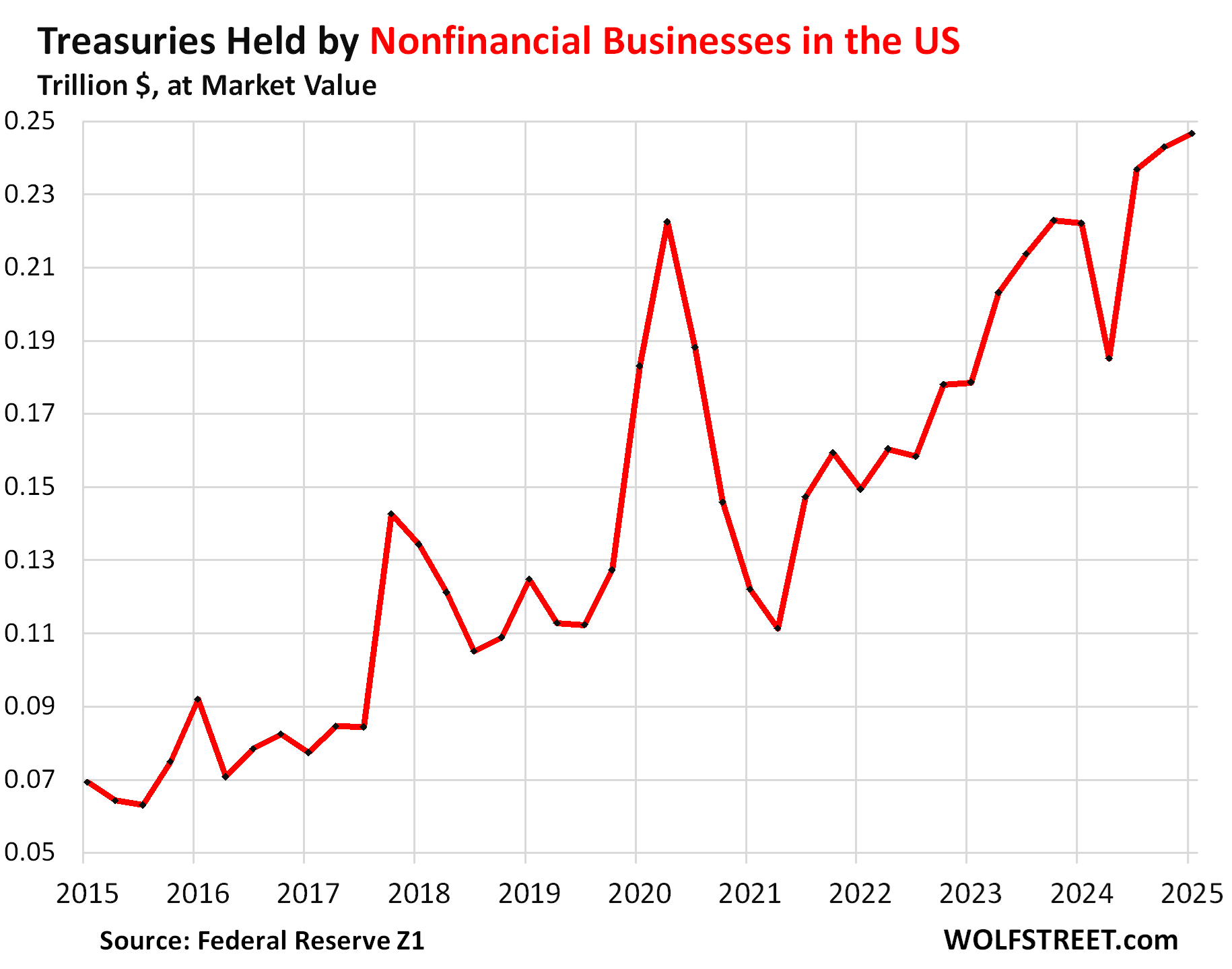

Nonfinancial businesses held $246 billion of Treasury securities at market value, or 0.9% of the debt held by the public. This includes corporate and noncorporate businesses.

But note, Corporate America has gotten very good at stashing its profits in overseas financial centers, such as Ireland, Luxembourg, the UK (City of London financial center), etc. See the chart of the top six financial centers above, which held a combined $2.73 trillion in Treasury securities, part of which is for US corporations.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thanks. As always very good, very useful information.

Yep, and really understanding who buys up the US Treasury’s freely printed scrip will be more and more important as time goes on.

Educated guess – entities who *also* have the power to freely print their own scrip (with which to buy the US Treasuries) – the Federal Reserve and “partners” the US is still able to put the screws to (shrinking pool).

(“Partners” – shrinking pool of foreign nations and growing pool of entities subject to Fed/Gvt regulation of their asset holdings – banks, insurers, pension funds…)

Well shown, insurance companies investment income and future capital gains will be outsized again once they cut rates…I’ve been hearing the next event is on the West coast…of course 1st known case of covid was Seattle…

Wolf, Technically debt is around $28 trillion. Even in that 66% of $28 trillion are held within the border. 34% outside the border. In the 34% outside the border, many US corporations are holding the debt for avoiding taxes. Hence nearly 75% of debt is held by Americans. Give or take. Interest is paid within and they pay taxes on interest. I don’t see it as a major issue. What do you think? Thanks

The issue isn’t where the debt is held. The issue is tax avoidance. It’s legal and designed into the system by our Congress — the best that money can buy. Now Trump started shutting some of it down by imposing tariffs on imports, which forces these companies that keep their profits overseas and don’t pay US income taxes on them, to at least pay some taxes on those imports. He specifically named Ireland as one of hotspots for this.

Imports from Ireland are mostly pharma products, which are currently exempted from tariffs. It will be interesting to see if Trump admin manages to change that.

Yes, the actual imports, but not the invoicing of China-made products via entities in Ireland, where the company takes the profit in Ireland, and “exports” from Ireland at a price that is not very profitable in the US — something Apple was found out of doing during the 2021 Senate investigation.

The company that I work for is an American company, but for the last 5 or so years they have been incorporated in Ireland. Before that it was incorporated in Switzerland.

Debt ceiling needs to be raised.

Current limit: $36.1 trillion (as of January 2, 2025).

Likely increase: $4–5 trillion (i.e., raising the ceiling to ~$40–41 trillion or even $41–42 trillion).

Why: Necessary to finance projected borrowing through FY2030 without default.

When needed: Before mid‑July to avoid hitting the X‑date this summer.

To me it is a combination of WTF, FUBAR & SSDD.

Cheers,

B

“The Euro Area – which includes the three financial centers Luxembourg, Belgium, and Ireland – has been purchasing Treasury securities on a large scale over the years. ”

So in the chart that shows both the Euro Area and the Financial Centers, do you exclude the treasuries held by the Financial Centers from the amount shown for the Euro area?

No, they’re shown in their full value, just like I sometimes show France separately (because it’s a big holder) plus the Euro area as a whole.

When less than 20% of our country’s debt and obligations is owned by outsiders, I’d say we have a crisis in the making. Essentially we are in debt to our eyeballs to ourselves.

Opposite. The last thing you want to be is dependent on foreigners because they can blow up your economy in no time when they stop buying that debt, see Greece in 2009-2012.

Re: “ These securities are not traded in the bond market and are not subject to the vagaries of that market”

I think there may be a typo — was vagaries supposed to be vulgarities?

That would certainly work too 🤣❤️

Wolf, in another article you had mentioned Congress didn’t start to take our debt seriously until the bond market forced it to in the late 80s/early 90s if I recall. There doesn’t seem to be any desire for the bond market to force Congress to take debt more seriously now. This seems surprising given all the substantial new debt coming on board soon. I’m surprised, are you?

I used to think of ‘financial centers’ as New York, London, and possibly Hong Kong, and Frankfurt (Hqs of the ECB). But by listing Luxembourg, Ireland, Switzerland, and the Cayman Islands, it seems that term is now synonymous with “tax haven.”