Adios, “spring selling season.”

By Wolf Richter for WOLF STREET.

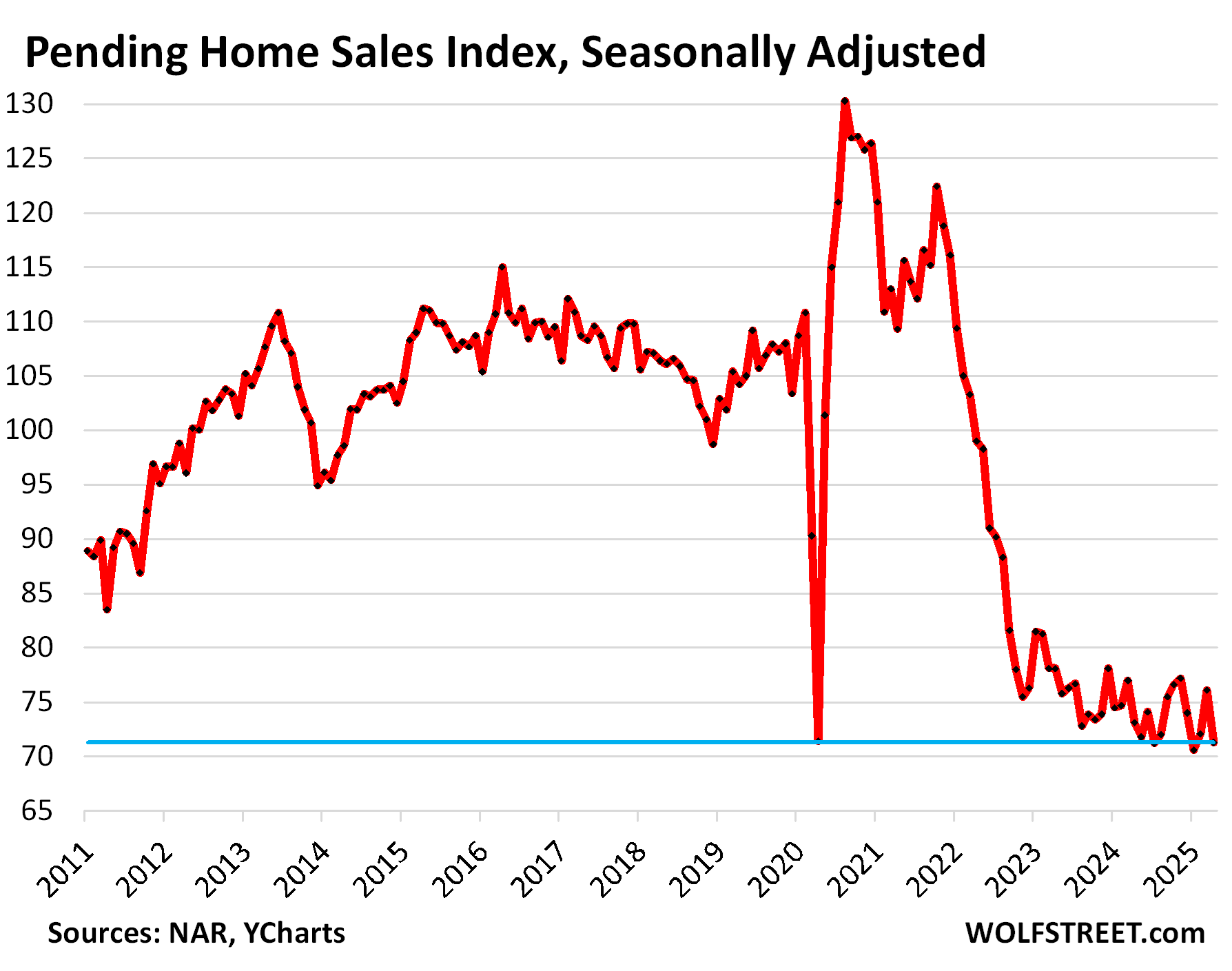

Pending home sales, a forward-looking indicator of “closed sales” of existing homes, plunged by 6.3% in April from March, seasonally adjusted, according to data from the National Association of Realtors today, driven by even bigger plunges in the South and the West, with the West carving out new lows in the data, just as inventories for sale are piling up.

Compared to the Aprils in prior years (historic data via YCharts):

- 2024: -2.5%

- 2023: -8.7%

- 2022: -28.0%%

- 2021: -34.8%

- 2020: -0.1% (lockdown April)

- 2019: -31.6%.

Pending sales reflect contract signings and track deals that haven’t closed yet and could still fall apart or get canceled, for all kinds of reasons, such as buyers being unable to afford or even get homeowner’s insurance, or financing falling through. While signed contracts that later fall apart are included in pending sales here, they’re not included in the data of closed sales reported later.

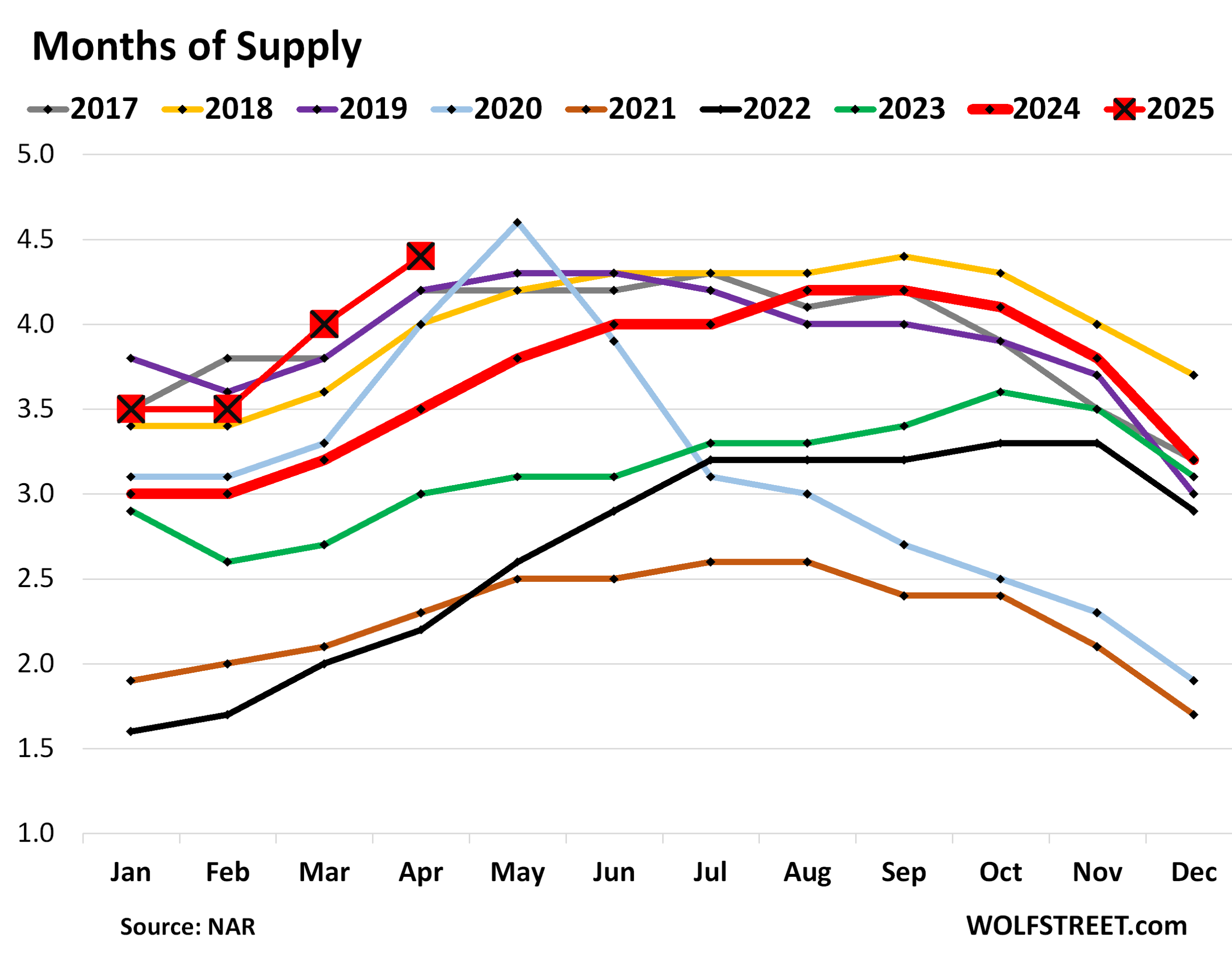

“Moreover, with housing inventory levels reaching five-year highs, home buyers in nearly every region of the country are in a better position to negotiate more favorable terms,” the report said.

Indeed. Home prices spiked by 50%-plus in just a couple of years during the pandemic, and these artificially inflated sky-high prices have triggered demand destruction on a massive scale, that’s what we’re seeing here – one of the most fundamental economic principles. When retailers or airlines are hit with demand destruction, now measured in real time online, they respond instantly by lowering prices, and demand comes back up. The housing market is still struggling to figure out that lower prices, after the artificially fueled spike, would revive demand.

Supply of homes for sale across the US has surged to 4.4 months in April, the highest for any April since 2016:

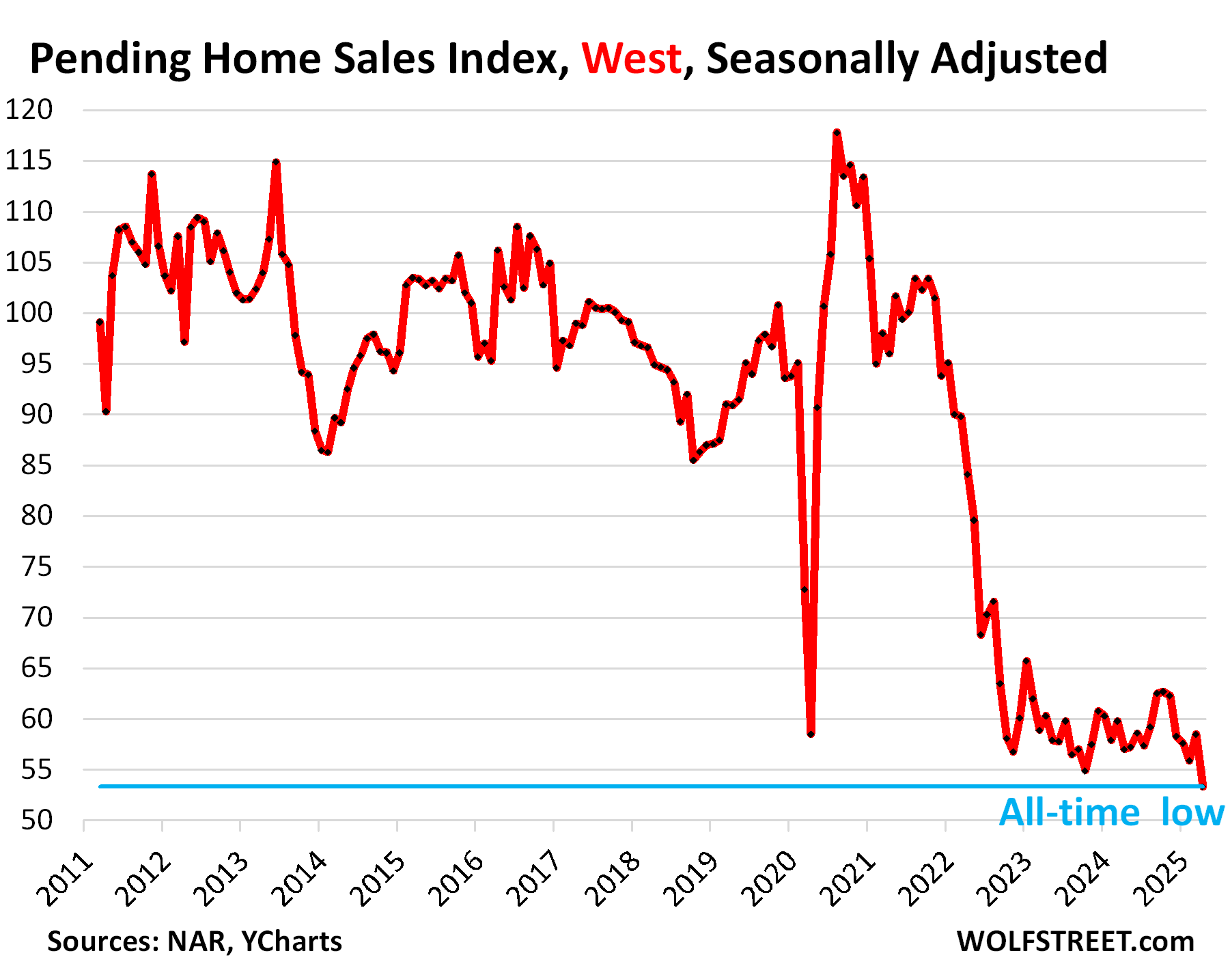

In the West: collapsed sales, ballooning inventories.

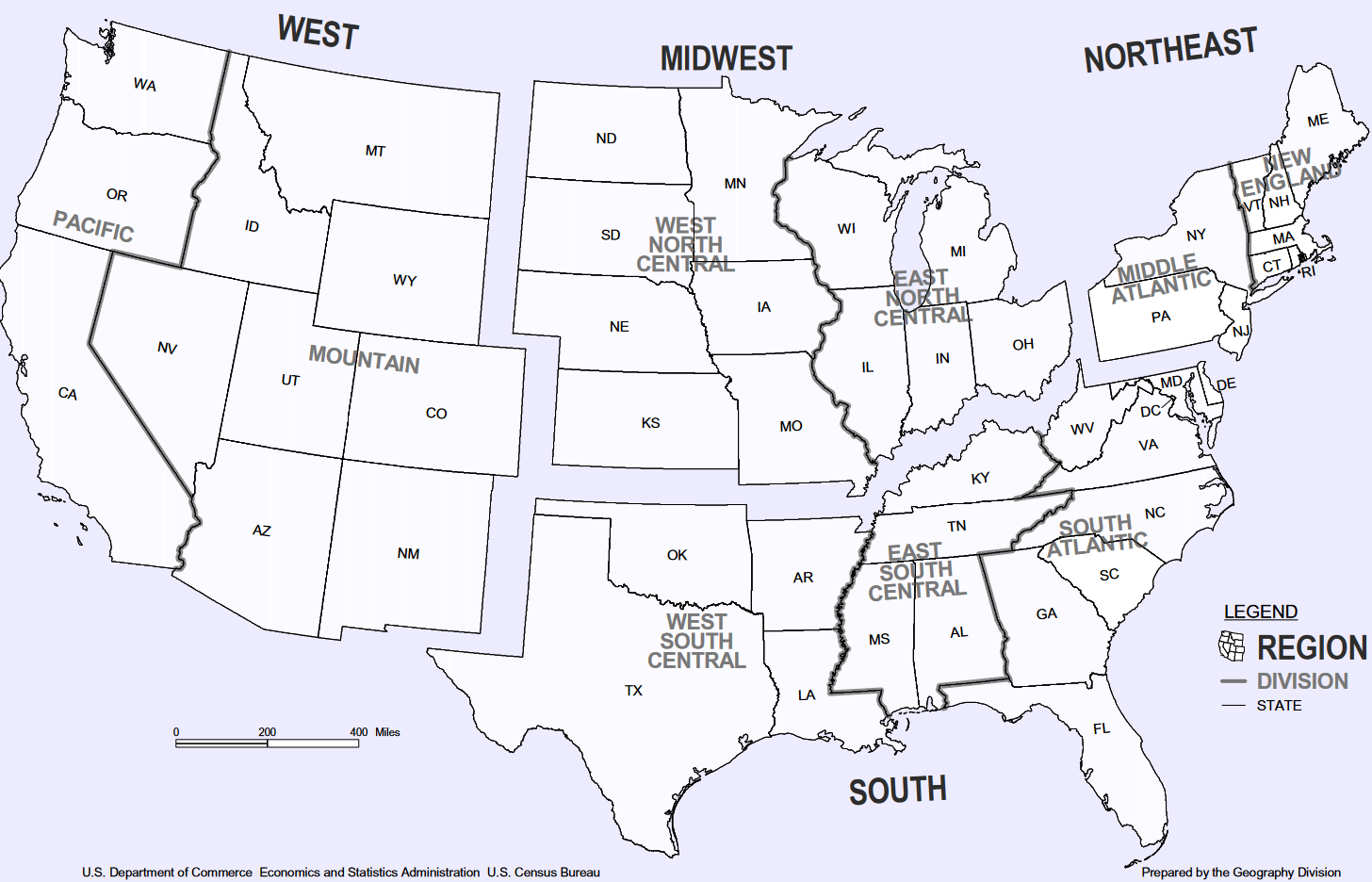

Pending sales of existing homes in the West (see map of the four Census Regions in the comments below) plunged by 8.9% in April from March, seasonally adjusted, to the lowest rate in the data going back to 2011.

Pending sales in April compared to Aprils in prior years:

- 2024: -6.5%

- 2023: -11.6%

- 2022: -36.6%

- 2021: -44.5%

- 2020: -8.9% (lockdown April)

- 2019: -41.4%.

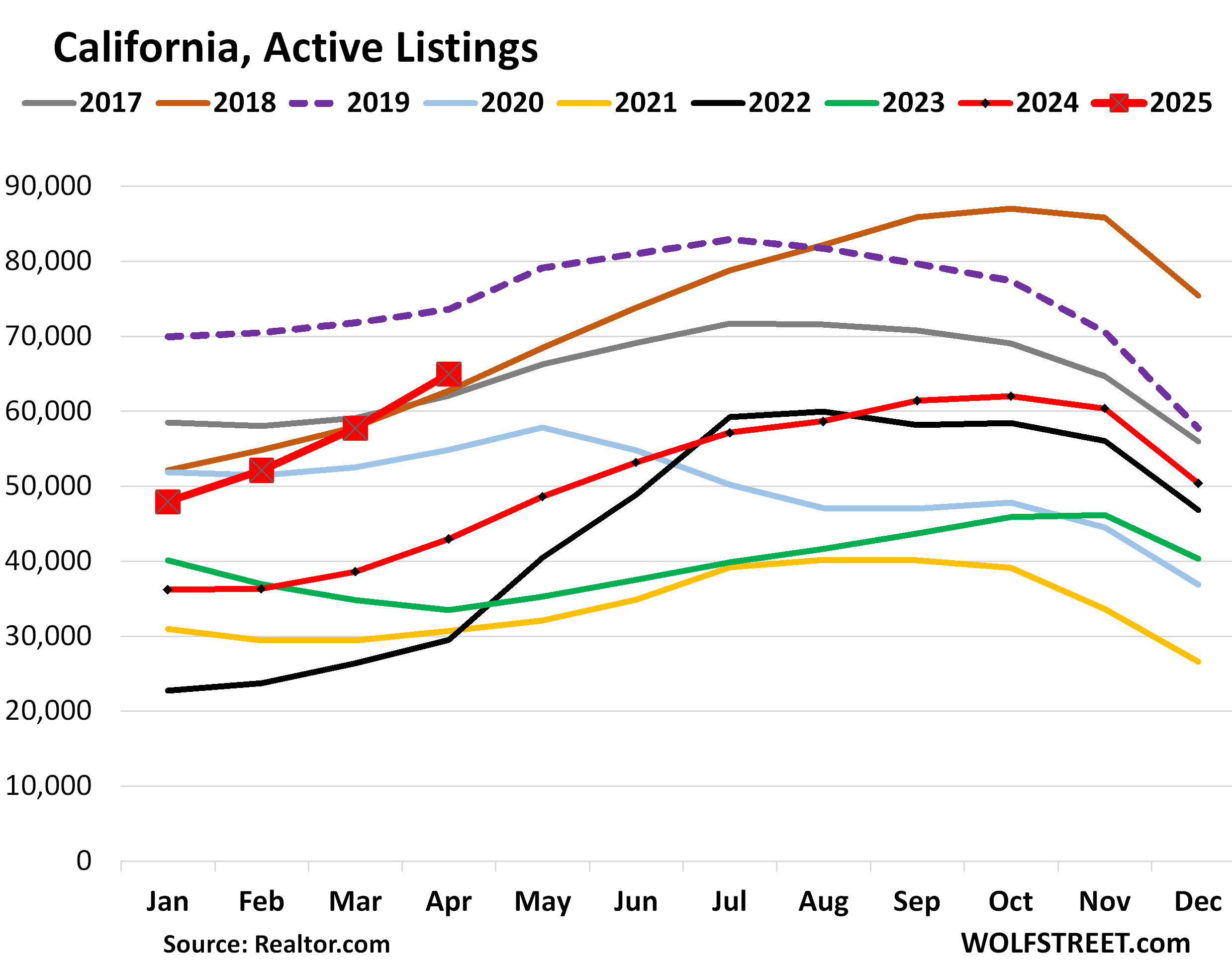

Inventory of existing homes in the West are dominated by the huge market of California. Active listings of existing homes in California spiked by 51% year-over-year in April, to 64,963 homes (red squares in the chart below), the highest for any April in the data from realtor.com going back to 2016, except for 2019 (dotted purple line):

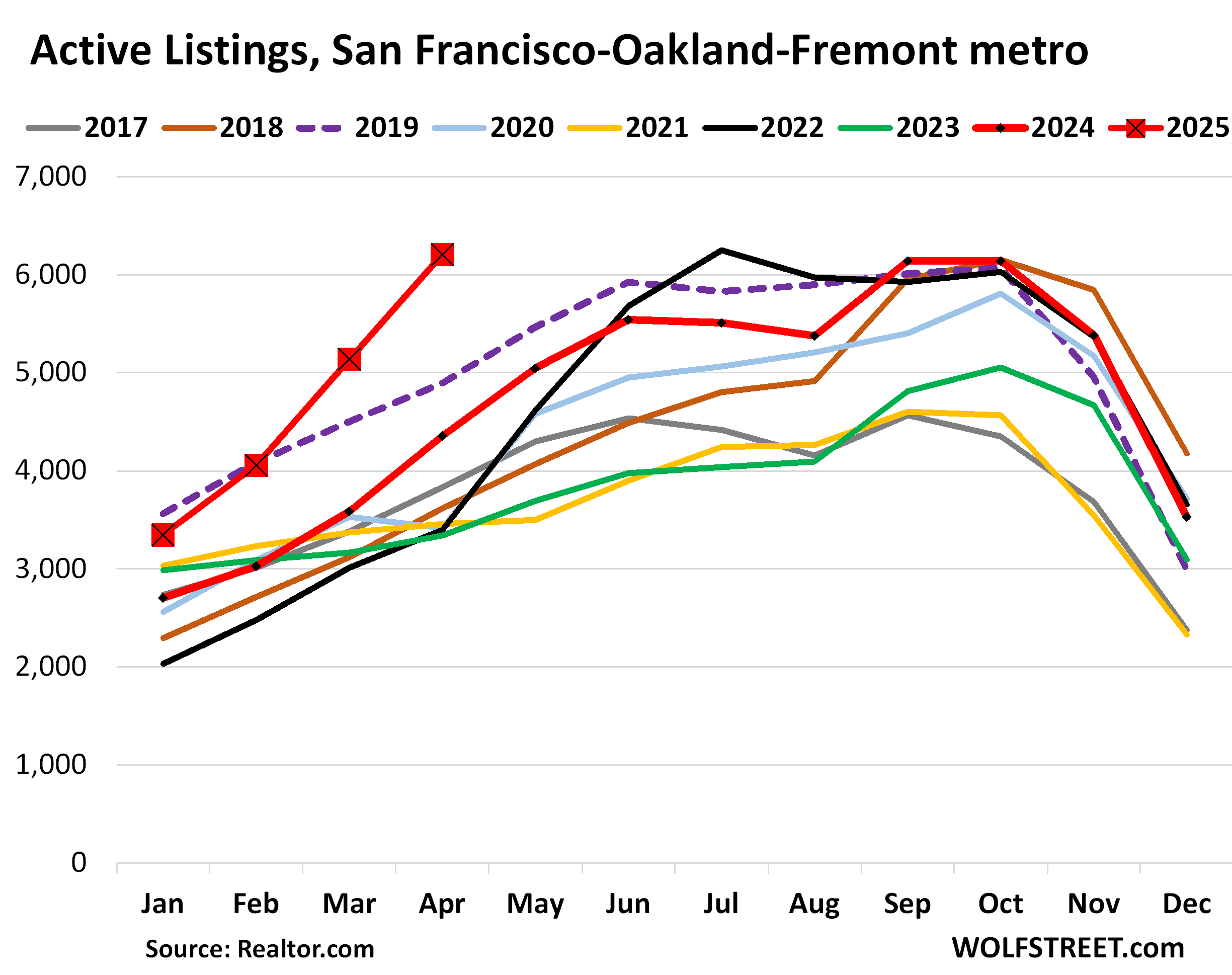

Ballooning inventory for sale is a good thing for the overpriced US housing markets. It’s what these markets need the most. So inventory is piling up in all major markets in California, such as by +70% year-over-year in San Diego County, +68% in the San Jose-Sunnyvale-Santa Clara metro, +50% in Los Angeles County, +43% in the Fresno metro (Central Valley), +75% in Orange County, or +43% in the San Francisco-Oakland-Fremont metro, where the inventory pile-up is a little more advanced than in some of the other California markets (we discussed major California markets here):

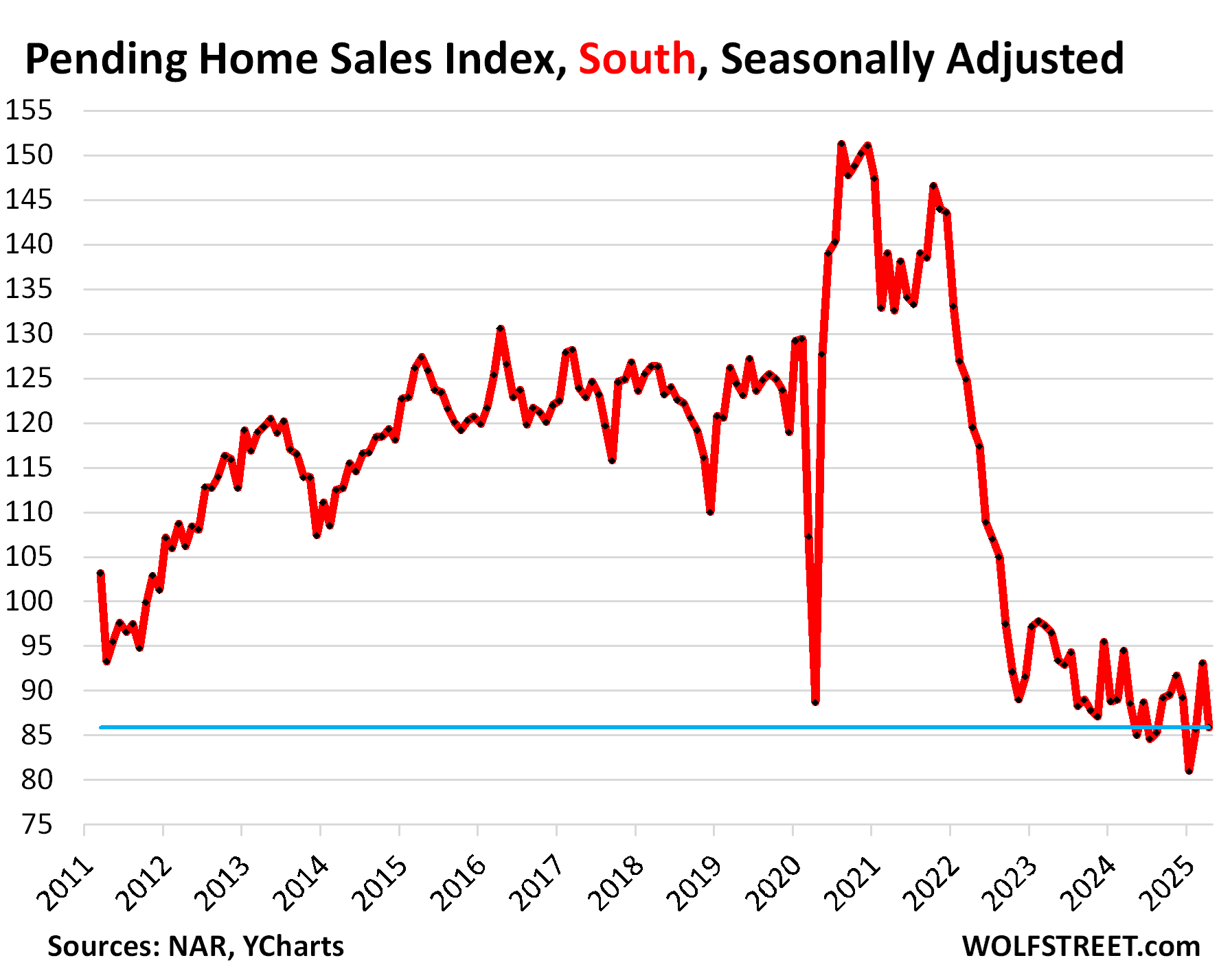

In the South: collapsed sales, ballooning inventories.

Pending sales plunged by 7.7% in April from March, seasonally adjusted, below lockdown April, and the worst April in the data.

Pending sales in April compared to Aprils in prior years (historic data via YCharts):

- 2024: -3.0%

- 2023: -11.0%

- 2022: -28.1%

- 2021: -35.2%

- 2020: -3.2% (lockdown April)

- 2019: -30.9%.

It’s precisely in the South where inventories pile up.

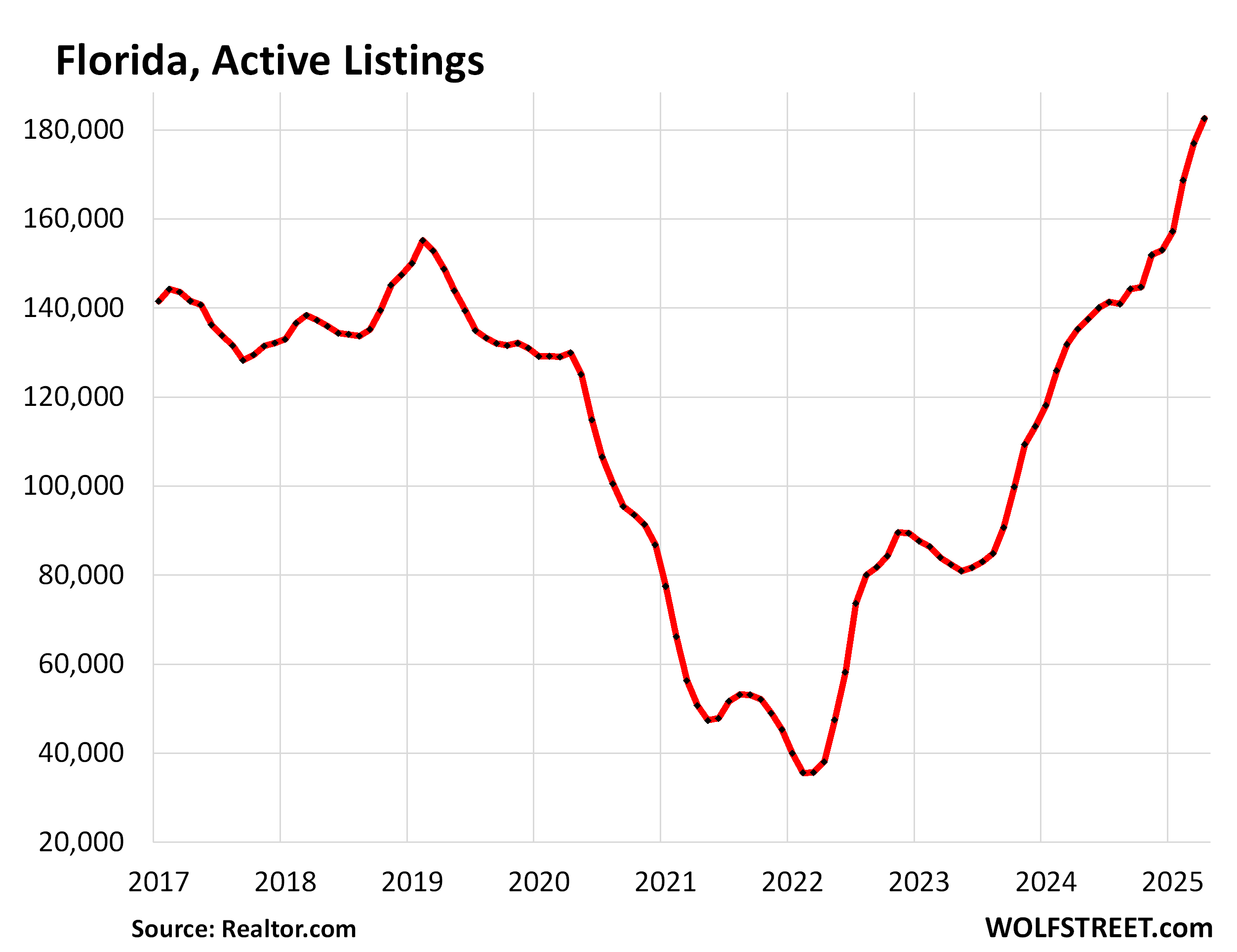

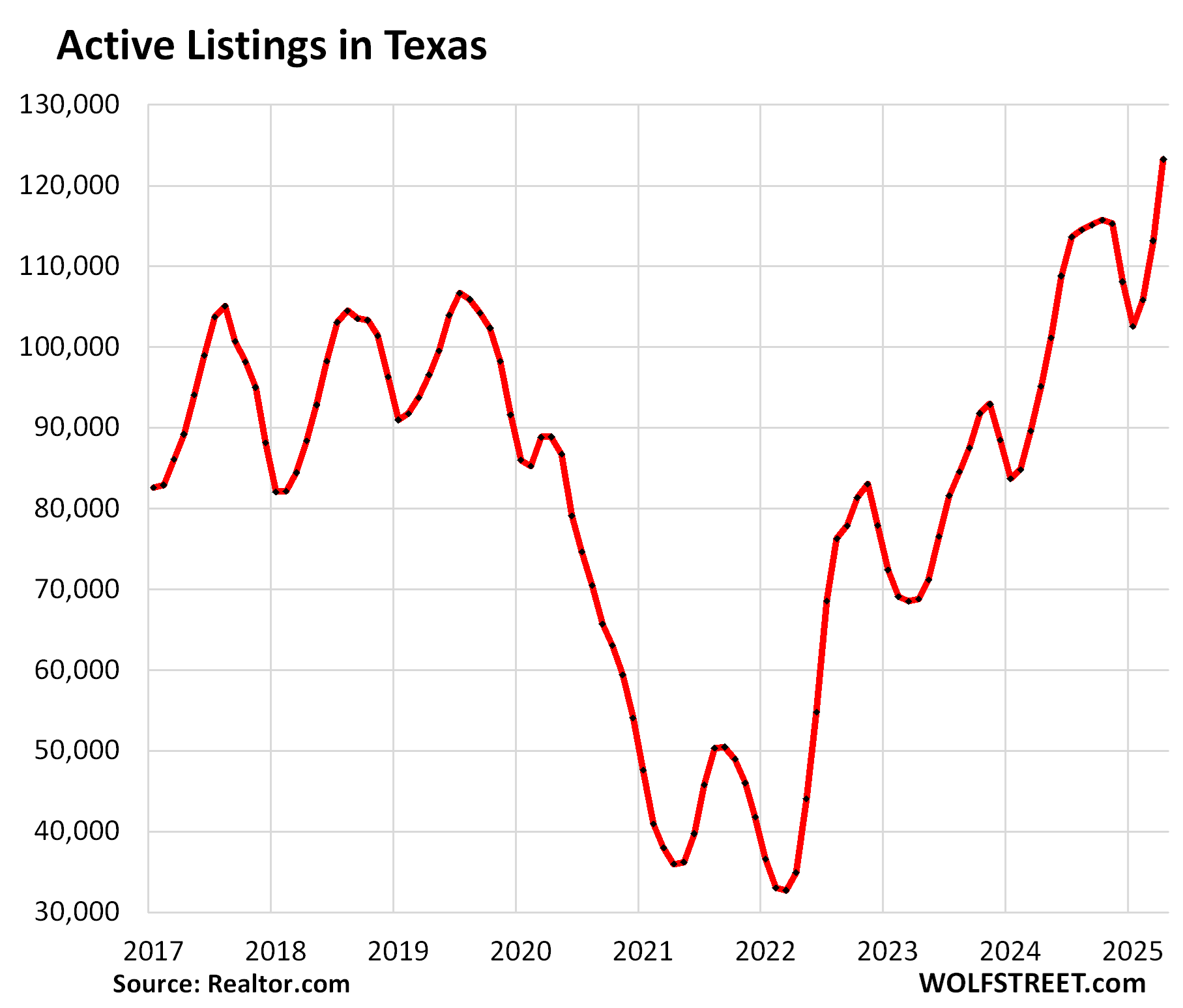

Florida and Texas dominate the vast South (map of regions in the comments below). And that’s where inventories of existing homes are ballooning, which is a good thing because the housing market needs these inventories.

In Florida, active listings of existing homes surged by 35% year-over-year in April, to 182,589 listings, the highest in the data by Realtor.com going back to 2016.

In Texas, active listings of existing homes jumped by 29% year-over-year in April, to 123,237 listings, the most inventory in the data by Realtor.com going back to 2016.

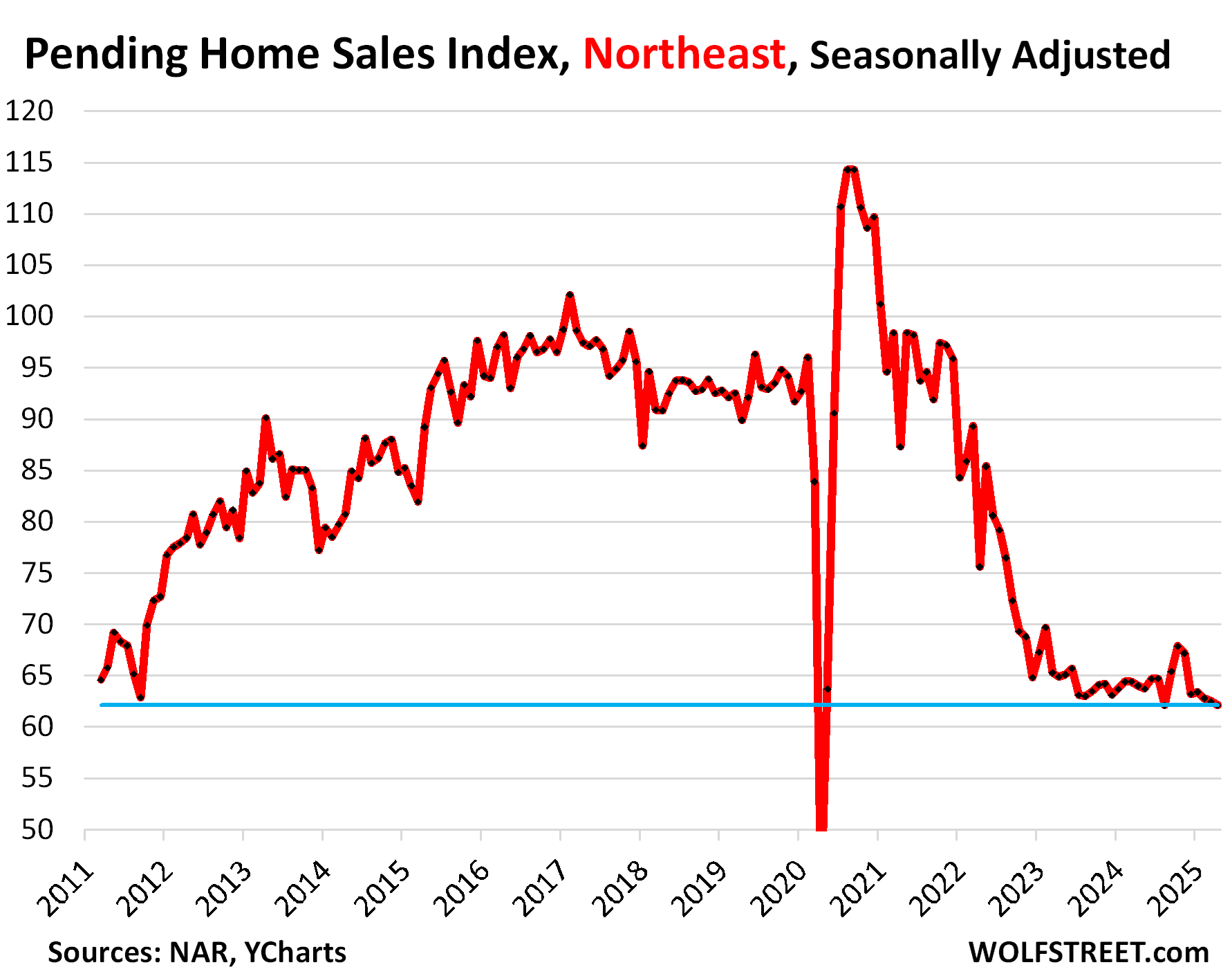

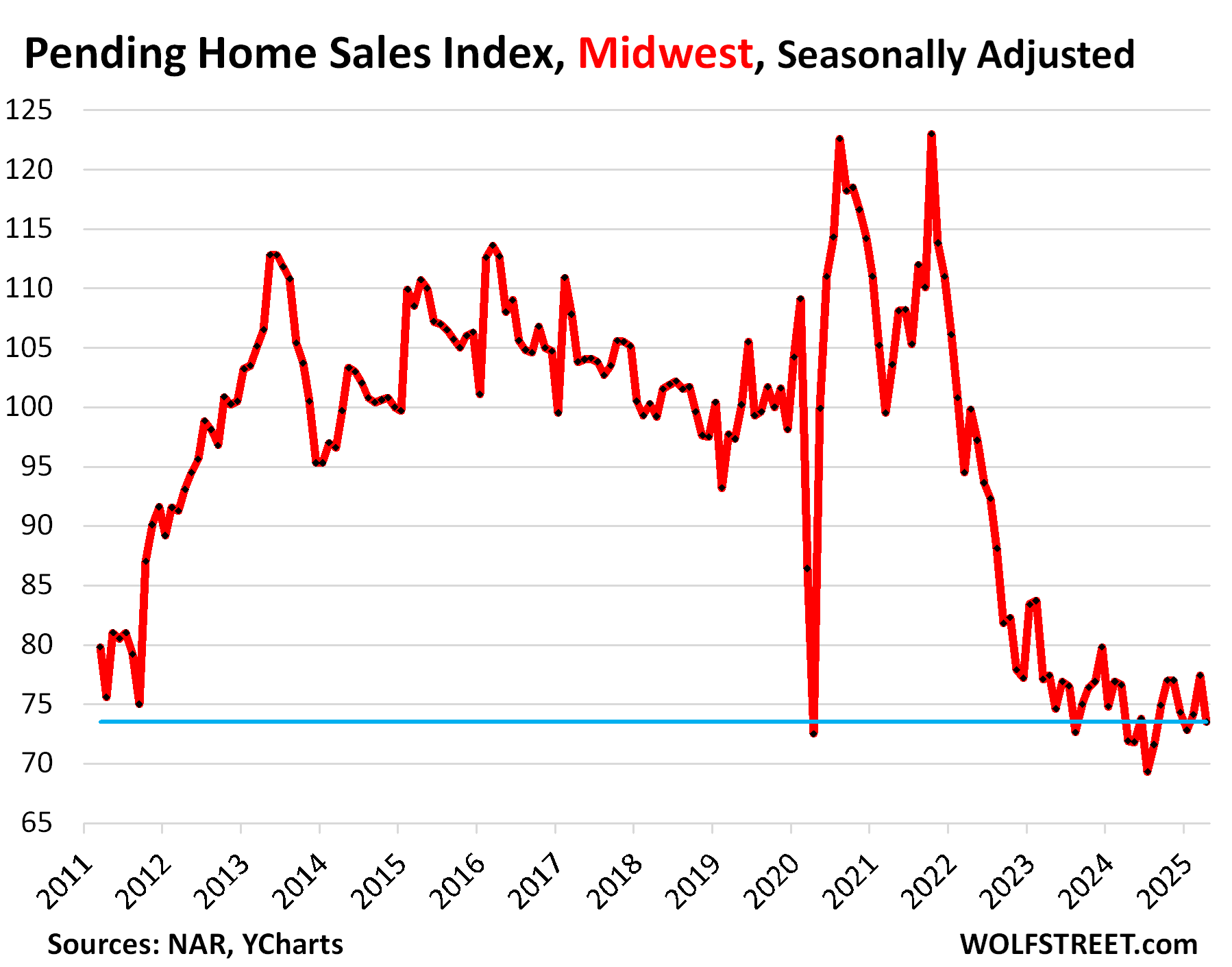

Pending sales in the Northeast and Midwest.

In the Northeast, pending sales of existing homes fell by 0.6% in April from March, seasonally adjusted, the worst April in the data, except lockdown April 2020, when sales essentially dried up.

Compared to the Aprils in prior years:

- 2024: -3.0%

- 2023: -4.3%

- 2022: -17.9%

- 2021: -28.9%

- 2020: +43.1% (lockdown April)

- 2019: -30.9%.

In the Midwest, pending sales plunged by 5.0% in April from March, seasonally adjusted, but were up by 2.2% from April 2024, and a hair above lockdown April 2020.

Compared to the Aprils in prior years:

- 2024: +2.2%

- 2023: -5.0%

- 2022: -26.4%

- 2021: -29.1%

- 2020: +1.4% (lockdown April)

- 2019: -24.5%.

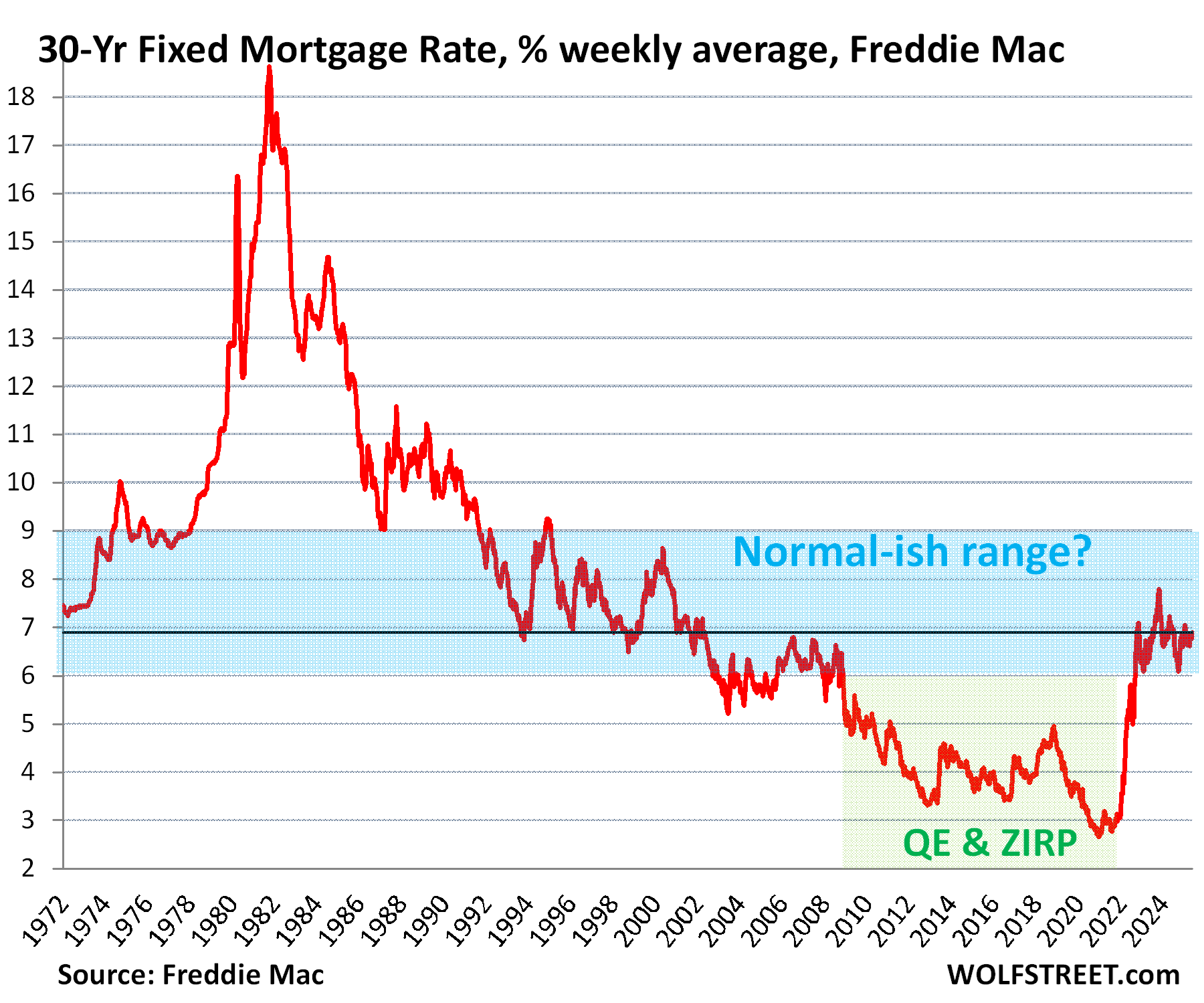

Mortgage rates are back in the normal-ish range.

The average 30-year fixed mortgage rate inched up to 6.89% in the latest reporting week, according to Freddie Mac today. It has been above 6% since September 2022.

Below-5% mortgage rates were brought about by the Fed’s QE, including the purchase of vast amounts of mortgage-backed securities, coupled with low inflation. But inflation returned aggressively in 2021 and has stuck around to form a new inflationary era, with higher interest rates to compensate lenders for higher inflation. And the huge national debt, and the ballooning national deficits that need to be financed with new debt sales, are putting upward pressure on long-term rates, including mortgage rates.

It’s not normal-ish mortgage rates that are the problem, but prices after the absolutely crazy price spikes that resulted from the Fed’s QE and interest-rate repression.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

As Mr Burns would put it when looking at the numbers for the West….”Excellent…” let this be the appetizer before the real main course begin..

Then again I do expect you’ll get the usual not in my neighborhood comments from Re agents repping SGV, OC or Santa Monica..afterall we’re still in Spring season…just remember from Got, Winter is coming, can’t wait to see what that will look like.

P_I,

Guessing Winter will be slightly cooler and wetter.

The four Census Regions of the US:

Hi Wolf: How far back do the data go? Can you see back to, say, 1990?

The pending home sales data, reported today, go back to 2011.

The existing home sales (=closed sales) go back to the 1980s. But that’s a different data set. The last one reported was for sales that closed in April (contracts signed in prior months), reported on May 22:

https://wolfstreet.com/2025/05/22/spring-selling-season-fizzles-worst-april-for-home-sales-since-2009-supply-surges-to-highest-since-2016-yoy-price-gains-fade/

Anecdotally, I’m seeing more and more price reductions on Zillow-listed single-family homes (SFHs) in the Tampa metro area. Supply seems to be increasing too based on number of for sale signs in nearby neighborhoods. Wolf’s reporting and analysis backs up these anecdotes.

I welcome more “for sale” signs, but many SFHs need price reductions in order to sell. For any also interested in buying in FL, I encourage you to wait.

Here in Florida the for sales signs go up every week on just the few blocks I travel on each week…

And good ol’ Lawrence Yun, as expected, again blaming slow sales on interest rates being “too high”, rather than mentioning prices at all.

Realtor commissions are based off sales price, so sales prices are never high enough for him. Nobody should listen to Lawrence Yun. He’s an industry propagandist. Any publication that legitimizes his comments is a rag.

Yes, him and everyone else in the industry complaining about interest rates instead of realizing that the prices are outrageous!

And they are calling on the FED to lower interest rates! Like the FED has any power to determine the interest rates on mortgages:))))

People have to realize that the sellers of MBS’ and the sellers of the 10Y treasuries are competing for the same pool of investors. Low risk treasury for 4.4% return or MBS for 6.95% return. Pick your choice of risk and return. If there’s low demand for the 10Y at low returns than certainly there’s a low demand for MBS’. Even if the FED drastically slashes the rates on the short term treasury it will not have a lot of effect on the long term ones 10Y 20Y 30Y

The fed does have the power to lower mortgage rates and bond yields by doing QE, “buying”, with trillions of new dollars, bonds and mbs which they did massively during the gfc and covid, and thats why bond yields went extremely low and mortgage rates got down to 3 percent, but that led to inflation, house price explosions followed by cratering sales. Thankfully theyve been doing the opposite for a few years now, letting at least some of the bonds and mbs they “bought” mature without re buying, and destroying some of the money they created from nothing.

This fed and its major policy errors of QE and deliberate target of at least 2% inflation was appointed by the Republicans and Democrats, so people should be aware of that when they vote. Its Congress persistent deficit spending that is contributing to these policy errors. The Libertarians which are on the ballot, have a policy of balanced budget.

I agree with you that the FED has the indirect power to influence mortgage rates by doing QE on MBS. However that has turned out to be a disaster the way they did it last time and it got us into the current mess

What I was trying to say in my comment above is that they can’t just say “starting tomorrow the 30Y mortgage is x%” and MBS buyers will do so.

IMHO the only way out of this mess is sellers lowering their asking prices significantly….and that is a process which takes years!

In SoCal realtors were also culprits of 2008 housing crash. Without them manipulating naive or dumb people into buying, no mortgage to talk about. Yet no one I mean no one ever said a word about them. Majority of SoCal realtors are dumb “wanna be” who prey on emotionally weak buyers (FOMO). NAR is a very powerful political organization. That Mr Yun probably is a product of DEI. I am Asian so I know when I see one. Common sense to them is like rare mineral yet good @ getting good score 🙄 whenever I read his article, I wanna shake his head like what bar tenders do to the drink order. 😂 Nop nothing material still.

“The housing market is still struggling to figure out that lower prices, after the artificially fueled spike, would revive demand”

Struggling is being kind, imply they are trying but can’t figure it out. In reality it’s more down to toxic combination of stubbornness and entitlement for most of these existing sellers to get their head out of their rear end and accept the fact that their crap shack in some crappy part of their hood is not bound to some artificial baseline of a million. See new home builders figure that one out much quicker so they “struggle” less so to speak .

The real struggle will be getting all the municipalities to finally accept lower property values! I am considering liquidating some properties that need work just to give the city a big FU. There is no way I will get anything close to what the property tax valuation is. These are older rentals and completely paid off. F’em.

Do all your neighbors a favor by resetting the valuation based on real arms length sales.

Next tax year they can all file complaints against valuation.

You only have 45 days from the time you receive the assessment notice to file a complaint. Around the country people typical receive their assessment letters right after they pay their taxes (April).

Yep my valuation increased this year while there are several homes for sale for 6 months or longer 2 did sell out of 6 listings

The lowest price listings sold

NE Texas market

Prices need to come down for sure mtg equity maybe the floor for those that don’t have to sell. Having sold into depressed markets having to sell with negative equity is painful. My home in oil bust of 1986 sold for 40 percent of my purchase in 1983

Same thing in midland Texas with a 20 percent loss

Denver in 2009 a 30 percent loss

I have experienced lots of home sale losses and very few gains having been in the oil field for 40 years and 20 moves

Looking back on it do you think renting would have been better? With that timing on moves?

My father was in the oil industry and I recall my parents’ friends commenting that “two moves equals one fire.”

Think of a poorly educated housing speculator as a sort of crack addict and a lot of irrational behavior becomes…if not, rational, then at least predictable.

I wonder, do home loan lenders/leverage fool providers/crack dealers ever have anything like loan “call” rights – forcing the borrower to sell/exit in order to protect *lender’s* 80%+ interest in the house whose implicit valuation is falling fast.

The lender’s “80% interest” is not like a share of stock. The lender’s interest is not impaired until both (a) price drop exceeds borrower’s equity (often >20% if loan is seasoned) and (b) borrower stops paying.

And the lender does have call rights (foreclosure option) once borrower stops paying.

Sure – that is the standard (and perhaps nigh universal contractual) way of looking at things but…

If you are a lender witnessing the SFH ZIRP/Valuation Volatility Madness of the last 25 years…I don’t know that you would *want* to *have to* wait around for borrower default as insanely overvalued collateral value plummets…

(Stock margin lenders don’t – come up with new margin call equity or be cashed out).

I *know* that mortgages are subject to all sorts of debtor friendly rules – but I think it is a fair question to ask how lenders can be sufficiently stupid (repeatedly) to put up with them.

Of course, the answer lies in the Government Agency default guarantees….

You so called experts…ugh …. What we are going through is a combination of greed of Home builders and apartment builders in Tampa who have overbuilt and are suffocating home buyers and home sellers.

The issue is simple: every homeowner’s association is literally killing the market for new housing as well as existing housing. HOA’s in Florida are out of control, charging as much as 30% of the average owners mortgage, while providing non equivalent services.

We Floridians want to desperately leave our homes, condos and villas to break free of HOA tyranny.

Its the Republicans and Democrats deranged deficit spending that is a big part of the problem and in the 2024 Florida US House election, voters voted 99% for the Republicans and Democrats. The voters aren’t holding their reps accountable.

I wonder, do these inventory numbers in Florida reflect the total size of the market? I am sure since 2017 Florida has added at least a million new homes, maybe 2 million or more, who knows.

So with an increased market size, should we not expect more inventory available and the number would have to be adjusted? Would percentages be more accurate? I mean, 180k is big, no matter what.

Or does that not even matter.

I only wonder about this because they have built on every square inch of land they could grab the last few decades, and that only accelerated with the Blue exodus. Its been insane.

Maybe, but look at the slopes of the lines – if inventories can collapse…they can explode.

ZIRP caused absolute psychosis about long term affordability (again) – everything else pales in significance to that reality.

If rate normalization (following home inflation insanity), prices out 60%-80% of demand…nothing else matters.

If you take a look at new home sales over that period the figure would provide the increase in homes in the Florida pool

Have to subtract off hurricane destruction and teardowns, though.

Presumably most the houses built in the 1920s Florida real estate bubble aren’t worth keeping up…

I live in California, 20 years in San Francisco, and now in Monterey. San Jose Days on Market is now under 30 days, thus I think it is time to include that figure in these observations. A rise on inventory in the peak selling season combined with a low Days on Market means something completely different than just Inventory alone. California: people come and people go, but real estate wise we are Sold Out. There’s that old saying:

People move to California to Become Somebody

People move to New York when they Are Somebody

People move to Florida etc.. to Become Somebody Else

“San Jose Days on Market is now under 30 days,”

Likely typo, should be “over 30 days,” namely 37 days in April, the highest April in the data going back to 2016, except for lockdown April 2020.

And note that days on the market means before the home gets pulled because it didn’t sell or before it actually sold.

Also highest active listings for any April in the data going back to 2016.

To explain the price spike, a competing theory to interest rates is a lack of supply compared to the large millennial generation entering peak homebuying years.

What % of price spike would you say is from interest rate (ZIRP, etc.) and what % would you say is due to lack of supply?

Another way to ask this question: how much would prices have risen in the past 5 years if mortgage rates had stayed at 5-7%?

Supply collapsed in 2021 and 2022 because homeowners that bought another house and moved into the new house SAW the 3% mortgage rates, and prices spiking out the wazoo, right in front them, and they decided to hang on to their old now vacant home to ride up the price spike all the way. So these were buyers (demand) that decided not to sell (lack of supply, which created this shadow inventory of vacant homes). And now they’re putting those vacant homes on the market (added supply, inventory coming out of the shadow) without having to buy one to move into because they already bought and moved in 2021/2022 (now lack of demand).

That’s where this supply is now coming from, from those vacant homes from homesellers that now don’t buy because they already bought a few years ago.

Obviously, not all homebuyers/sellers did this, but enough did it to move the needle. This was a very bizarre situation back then.

I discussed this back then and said those vacant homes (shadow inventory) would someday flood the market without the sellers also being buyers, and that what they’re now doing.

This is salubrious for the housing market, it will help the housing market get over the distortions from the pandemic, it’s part of the healing process that has started some time ago.

“So these were buyers (demand) that decided not to sell (lack of supply, which created this shadow inventory of vacant homes). And now they’re putting those vacant homes on the market (added supply, inventory coming out of the shadow) without having to buy one to move into because they already bought and moved in 2021/2022 (now lack of demand).”

Couldn’t agree more and this point fascinate me to no end. Perfectly encapsulate how majority of these sellers logic/cautious side went out to lunch/vacation and let their greed brain dominate their thinking. Even if the old second house is fully paid off (which probably not the majority if I have to guess) by not selling and let it sit in hopes of good time to maximize profit, the idea of running cost like property tax, insurance, maintance, HOA even on vacant are a freaking running cost that you have to pull out of your pocket. It’s less than ideal to let it sit because you’re actively losing small portion of that gain every month but somehow this equation is never a thing for these people and if you lose an income, then it will only fuel to the fire…

On the contrary, you can afford to let money just sit in Tbills, notes..etc, sure you might still end up losing some compare to inflation but it’s not actively costing you money out of pocket. Same even goes for if you want to hang onto loser stock like Beyond Meat after buying at the top. Your cost will be opportunity cost but once again you’re not paying cold hard cash periodically to maintain it.

But I guess this kind of greed thinking have its root in that this is just a lull and historical housing is that bullet proof goldmine and price will 10x in as long as they can hold out for better days, like the way people HODL their bitcoin back up to $106k now

COVID caused a lot of unnatural movement in the housing market. Lots of demand shifts. People who had roommates and were working from home decided they needed more space and to live alone. Concerned upper middle class parents rented one bedroom apts for their college aged kids instead of letting them live in a house with roommates. Mass immigration. Huge Airbnb demand with everyone working remote and wanting out of the city. YOLO travel in 2021/2022, people moving out of COVID restrictive states but keeping their old houses so they could go back – this was big in Chicago, they bought up houses in Southeastern WI because the schools were still open and they didn’t have to home school their kids. I’m sure this happened elsewhere instead. Bored people saw 3% interest rates and listened to a podcast and thought I took could get rich from Airbnb and bought one thinking they’d get rich super easily, etc.

Anyways the majority of these trends are reversing. People have roommates again. YOLO travel is over. Mass immigration is over. People have figured out where they want to live and keeping the extra house even empty is a lot of maintenance or they realize being a landlord or Airbnb host is a lot of work. People are getting called back to the office.

My understanding is we didn’t have a housing shortage in 2019. What’s kept prices somewhat stable is nothing is forcing people to sell. They can pull the listing and try again next year. I think people are slowly realizing that next year probably won’t be better either. That being said if there’s a recession or spike in unemployment I think people start having to sell.

What is forcing people to sell their vacant homes is the cost of carrying a vacant home. That worked when prices were soaring 20% to 30% a year, fine. But now that’s over, and all that’s left are the costs.

I bet a lot of people are also learning that being a landlord is not all it is made out to be on biggerpockets. The hassle of fixing and maintaining a rental property is fine when things are shooting up and making you a huge return on a leveraged asset. Not so much when you aren’t gaining anything YoY and are still spending 1000s in maintenance and prop management.

I’m in San Diego and have been seeing large cuts and still no action. The house next to me has been on the market for 2 months now.

Every once in awhile a fully remodeled and nice home will sell quickly but even then it is below asking price. And while the median price doesn’t reflect drops yet, the homes selling for a lot are nice homes and not 30 year old beat up houses that were going $300K over asking like three years ago.

My neighbor paid $1.6M ($350K over ask) for an original 1960s era house in Feb 2022. Other Neighbor just sold for $1.5M for a fully gutted and remodeled home. So things are changing

All they need do is lower prices and that inventory will clear. 🤣

The early 2020s will be remembered as a golden age for those sellers who managed to cash in on a gigantic tidal wave of inflated expectations.

Fantastic news ! Thank You for the report Wolf.

Yes price is important variable, cost of financing is also a variable. Chart out the relation between closings and financing, perhaps a correlation there as well.

But rates are now normal, prices have shot up abnormally.

As Rick Pitino said “Sub 5% rates not walking through that door” So something will have to give in the pricing.

Florida insurance rates and the next hurricane season will put the nail in the coffin to the real estate boom in Florida. Look for vacation home owners and even primary home owners to be running away from there like scaulded dogs.

Same for CA. The home insurance rates have gone crazy high here.

Every now and then I look at home prices in Florida on a popular website that I won’t name. I see many listings that seem as though they are priced NOT to sell. I have no proof, but I strongly suspect that there are a great many disingenuous people that list their homes online at ridiculously high prices, with no intention of selling– unless some sucker with big bucks happens to come along. It doesn’t cost anything to list, so they have nothing to lose.

Except that you’ll have people traipsing through your house with no intention of buying. Seems silly to me.

My guess in 10 and 30 years yields will be brought down to stimulate demand

LVRJ – Las Vegas home sales being canceled at high rate. Much lower prices may cure that.

Airlines need to sell tickets to stay in business. In this market most homeowners don’t need to sell. A significant portion own outright. Not like 08 when investors purchased on margin. Also the economy is still good, so few need to sell due to hardship (as happened in 08).

People that bought when prices were 20 percent of what they are now are hanging on often so their kids have a place to live and they a place to visit in CA. Getting rid of prop 13 would drop prices and expand inventory rapidly. That may happen as the voting power of the immigrants takes over the voting power of the old white people and immigrants take over their houses. Immigrants need cheap places to live….prices of vacant houses have to drop.

That’s a common misconception. People not “needing” to sell ony means no fire sales and a rapid drop. It doesn’t mean prices don’t drop. Even if people don’t need to sell because they’ve lost their jobs, no one wants to pay carrying costs, especially with increased property taxes and insurance in many places, indefinitely while a house sits empty.

Eventually, these people cut their losses and decide to sell. That’s why inventory is skyrocketing, especially here in South Florida.

Sure, they can list at an aspirational price and hope for the best, or they can reduce the price and actually sell it. Enough people do that, and now your comps are different.

If homeowners don’t need to sell then why is inventory sky rocketing? Seems like a hassle to list a house and then say “I don’t need to sell”.

Then I wonder why inventory is rising and prices have already fallen 22% plus from its peak in once hottest market like Austin.

We don’t need no water, let the mother fr burn. Burn mother fr, burn!🔥🔥🔥🔥🔥🔥🔥🔥🔥💥💥💥🔥🔥🔥🔥🔥

Looks like some of the “frying pan” charts have started jumping “into the fire”.

Still seeing a fair amount of Floridians moving to Denver Metro. It seems that the land of Disney, Hurricane Central, and Flying cockroaches has become overbearing for those who no longer wish to play risk manager and evacuation coordinator. Since moving to Colorado in 2014, I have not regretted 11 years of peace not having to deal with New Orleans hurricane season. You must have that bend but don’t break mentality and plenty of financial resources June-Nov every year is a crap shoot. Destination Demand Destruction $FOMO to $YOLO has fizzled out. Those sold in 2022 made a fortune, the rest of us are left holding the bag with increase property taxes and insurance. The Seagull effect is real, the option to fly in and shit on everything and leave never fails.

It’d be nice, if data is available, to expand these charts out to 2006, just to get a comparison with the great recession.

Pending home sales data only go back to 2011, as I said a few times in the article. This metric came out of the housing bust.

I’m on the front lines of home sales here in the South and I can clearly see that the sales for the month of May will close at levels of 20% to 30% lower than last year’s May….20% lower than April this year! I really don’t see the increased activity typical for the “Spring Market”. On top of this, the “Active under contract” metric means pretty much nothing nowadays since 1 in 5 contracts are falling through. Some motivated sellers are reducing the asking price but nowhere near meaningful amounts. The inventory levels keep rising and homes just roll over to the next month or are taken off the market to be re-listed at a later time. Talking to these sellers I get mixed feedback….some say they can still last for a while and are not very motivated to sell at whatever price the market is offering…some want to desperately sell because they are running very low on money.

So, in the West, home sales are BELOW the home sales numbers during the ‘health scare’ of 2020❓

Stand by for the Great Depression 2.0❗️❗️Home prices will crumble like a buttermilk biscuit.

I just saw an article on realtor.com the other day saying sellers are pricing there homes too high. This market has to be killing realtors and with the fallout from the lawsuit, buyers agents are forcing clients to sign contracts before showing a house. I have some friends that casually in the market to buy a new house, but are refusing to look a listed houses because they will not sign a contract.

Btw, for people curious to see what greed and disconnect from reality looks like for existing home sellers…look up this gem of an address, that price cut is pretty hilarious, guess they were really hoping some sucker would pay the original asking, comedy gold for sure.

200 E 7000 S, Hyrum, UT

Isn’t that a business property for executive retreats, as opposed to a home people would actually live in?

A prominent realtor in my area is expecting a minimum 30% drop in prices of real estate in the next year.

It has already fallen 10% this year.

Short position in full force: BERNSTEIN MAINTAINS ZILLOW STOCK RATING, TARGETS $65