Epic demand destruction has ensued after prices spiked by 50% in three years. And now supply is piling up.

By Wolf Richter for WOLF STREET.

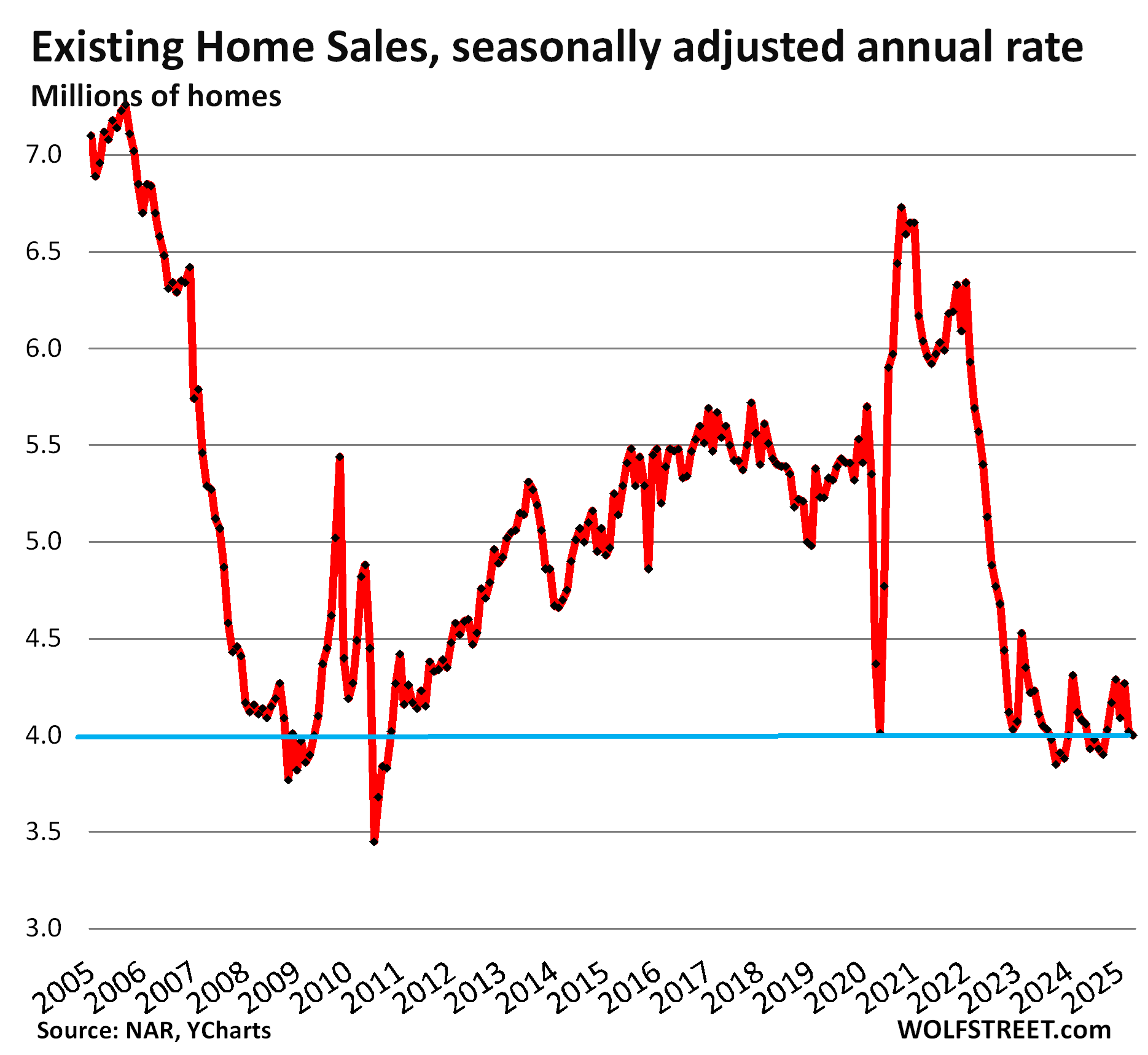

Sales of existing single-family homes, townhouses, condos, and co-ops that closed in April fell by 0.5% from the prior month and by 2.0% year-over-year to a seasonally adjusted annual rate of 4.0 million homes, the worst April since 2009, according to data from the National Association of Realtors today.

Sales began collapsing in early 2022, after the national median price had spiked by 50% in just three years, which was more than the market could bear. At the same time, mortgage rates were on their way to the 7% range. And demand destruction ensued. At first, in 2022, low inventories were blamed for the collapse in sales, but now supply has soared to the highest level in years, and sales have plunged further.

The seasonally adjusted annual rate of sales in April of 4.0 million compared to Aprils in prior years (historical data from YCharts):

- 2024: -2.0%

- 2023: -5.2%

- 2022: -28.2%

- 2019: -23.5%

- 2018: -26.3%

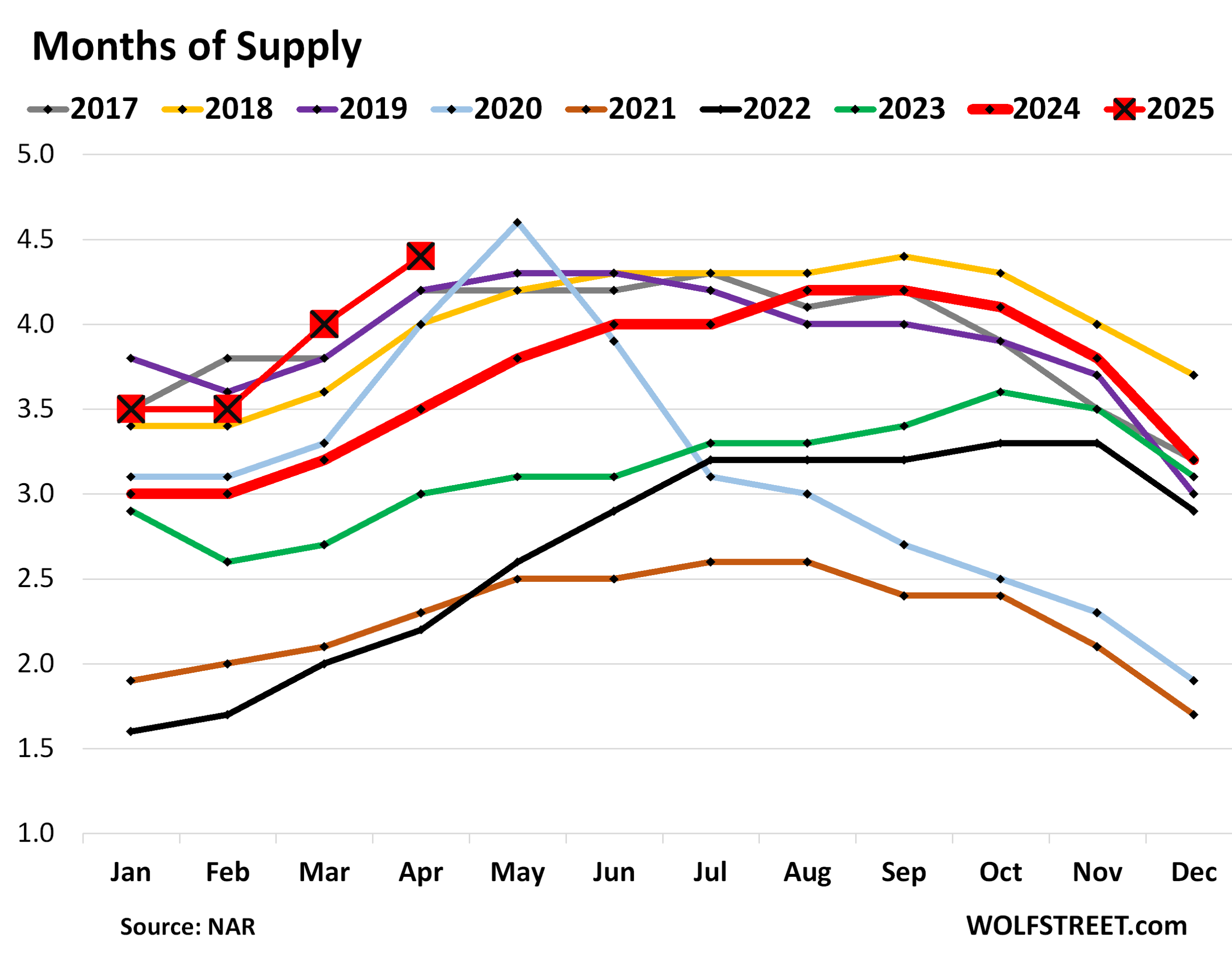

Highest supply for April since 2016.

Inventory of homes listed for sale jumped by 9.0% in April from March, and by 20.8% year-over-year, to 1.45 million listings. This jump in inventory occurred because buyers were on strike and weren’t buying enough of the homes for sale, and inventory is piling up.

Even in the formerly hottest markets, there are now big surges in inventory, such as in the major markets in Florida and the top four markets in California.

Supply of unsold homes on the market jumped to 4.4 months at the April rate of sales, the highest supply for any April since 2016. The months of 2025 are shown as the red squares:

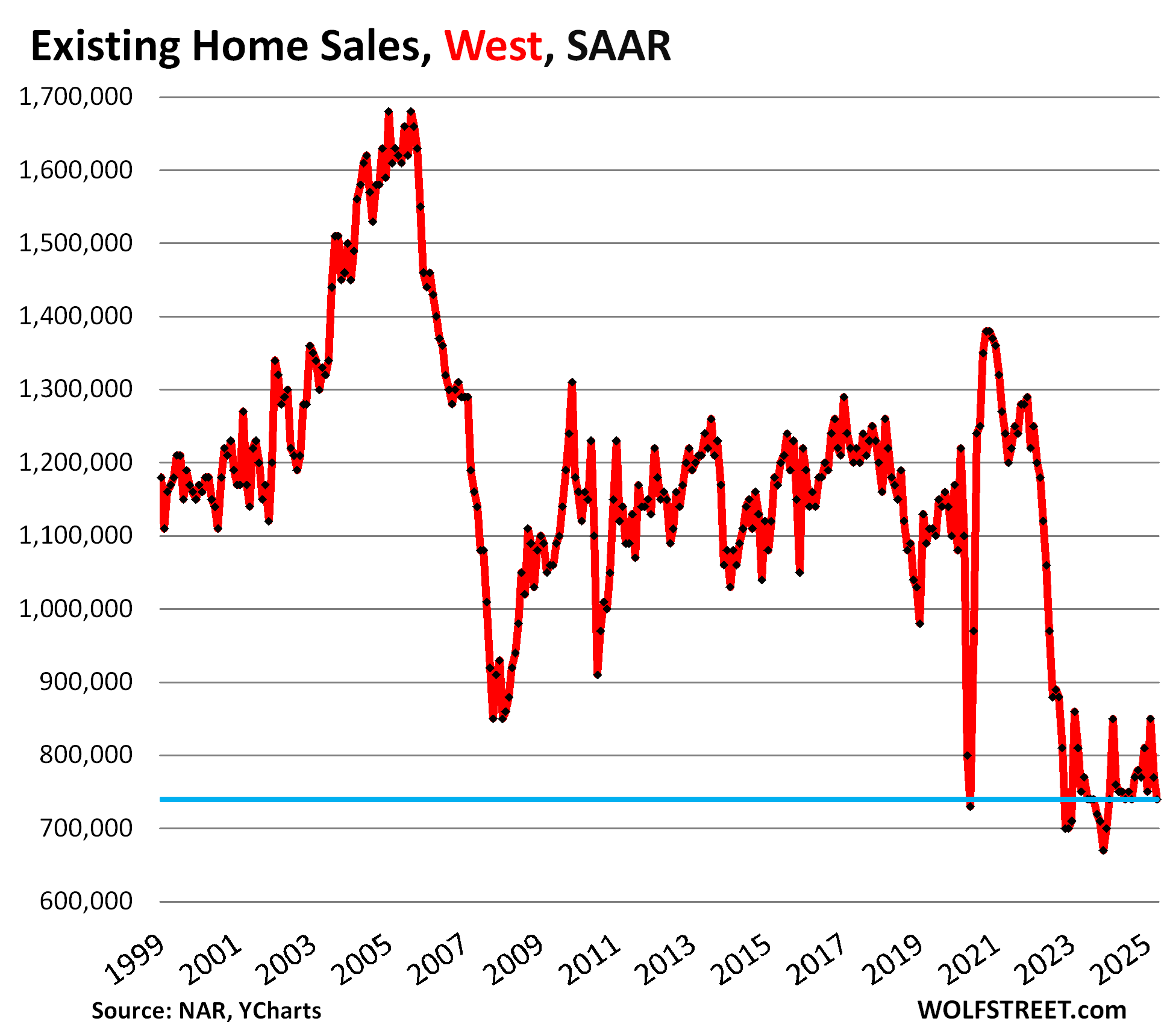

Demand destruction by region.

The hotly awaited spring selling season has fizzled across all four Census Regions. A map of the regions is in the comments below the article.

In the West, the seasonally adjusted annual rate of sales (SAAR) fell to 740,000 homes in April, the worst April in the data going back to the 1990s, and down by 1.3% from the already dismal sales in Aprils in 2024 and 2023:

| Sales in the West, compared to April in: | |

| 2024 | -1.3% |

| 2023 | -1.3% |

| 2022 | -33.9% |

| 2019 | -33.3% |

| 2018 | -37.3% |

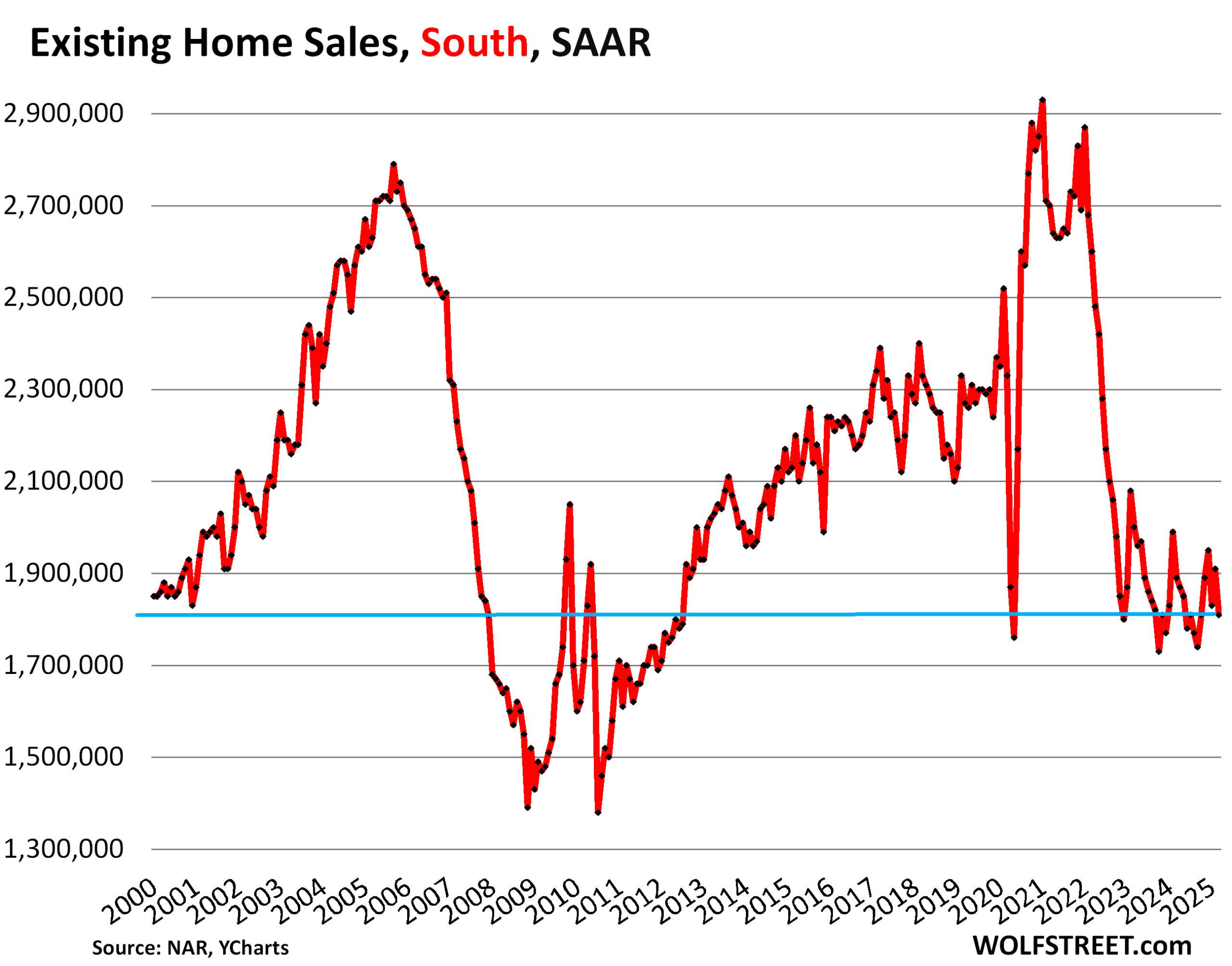

In the South, the sales remained at 1.81 million homes SAAR in April, worst April since 2012.

| Sales in the South, compared to April in: | |

| 2024 | -3.2% |

| 2023 | -7.7% |

| 2022 | -27.0% |

| 2019 | -19.9% |

| 2018 | -21.6% |

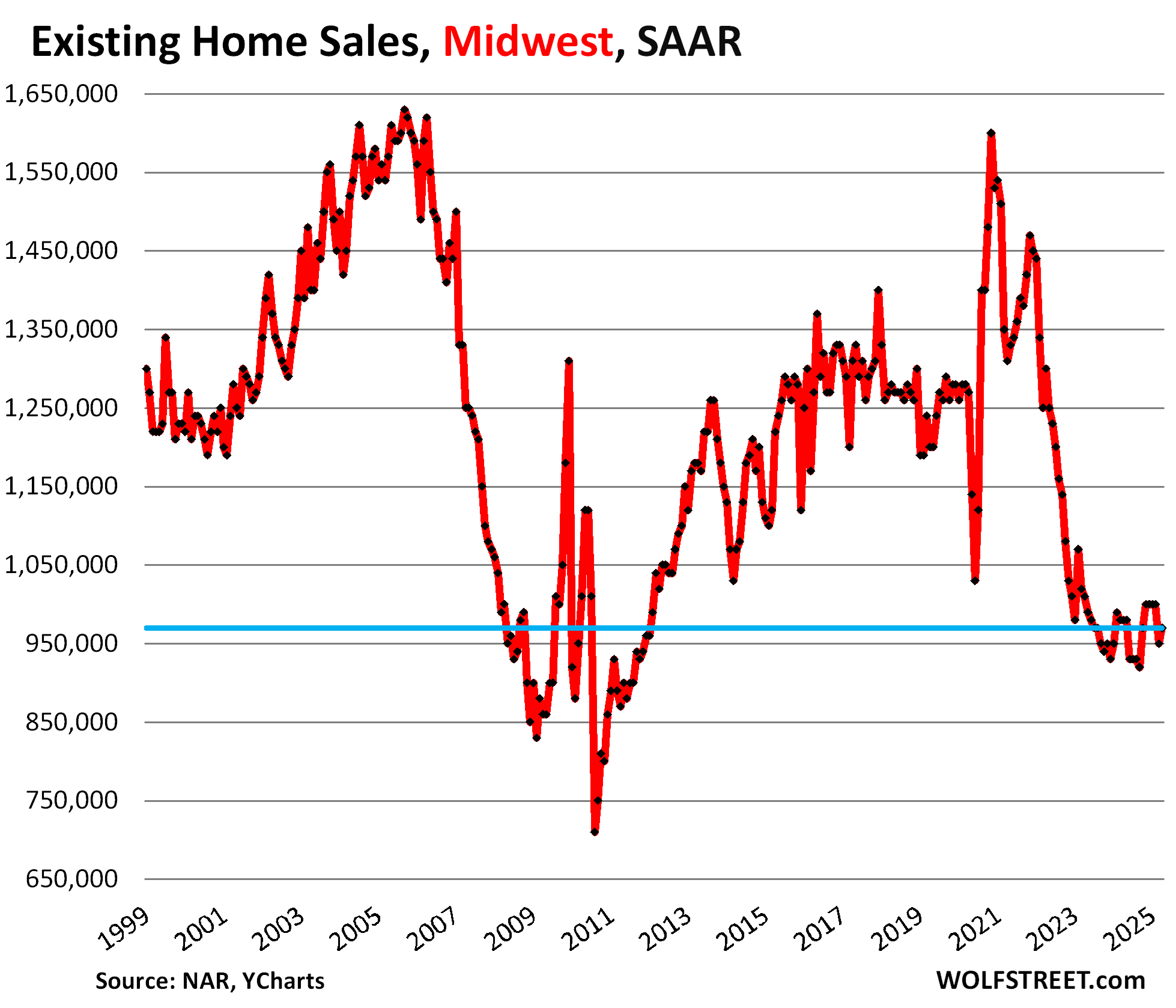

In the Midwest, sales rose to 970,000 homes SAAR, the worst April since 2011.

| Sales in the Midwest, compared to April in: | |

| 2024 | -1.0% |

| 2023 | -4.0% |

| 2022 | -25.4% |

| 2019 | -19.2% |

| 2018 | -24.2% |

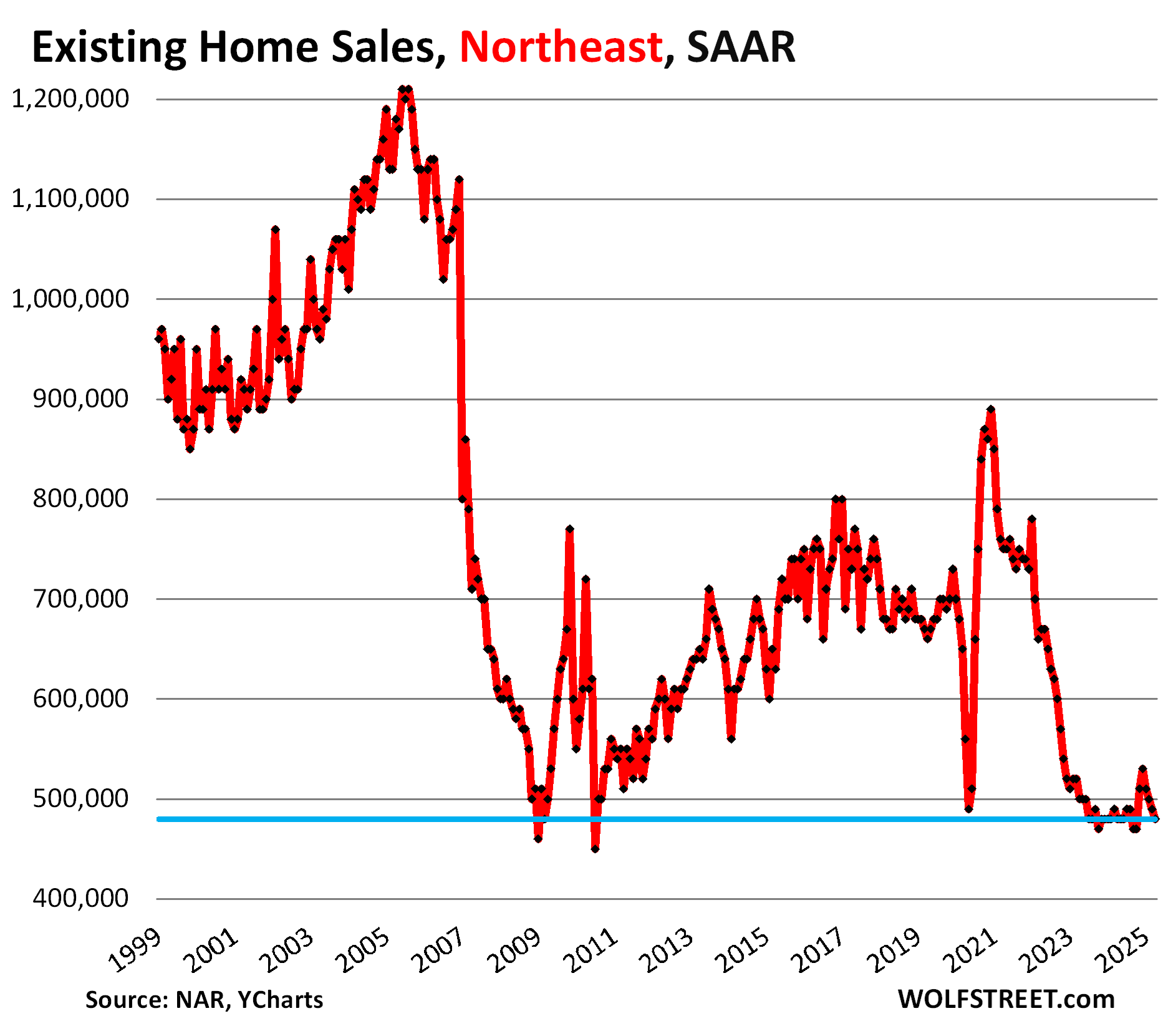

In the Northeast, sales dipped to 480,000 homes SAAR in April, same as in April 2024, both the worst Aprils since the 1990s.

| Sales in the Northeast, compared to April in: | |

| 2024 | 0.0% |

| 2023 | -4.0% |

| 2022 | -28.4% |

| 2019 | -27.3% |

| 2018 | -28.4% |

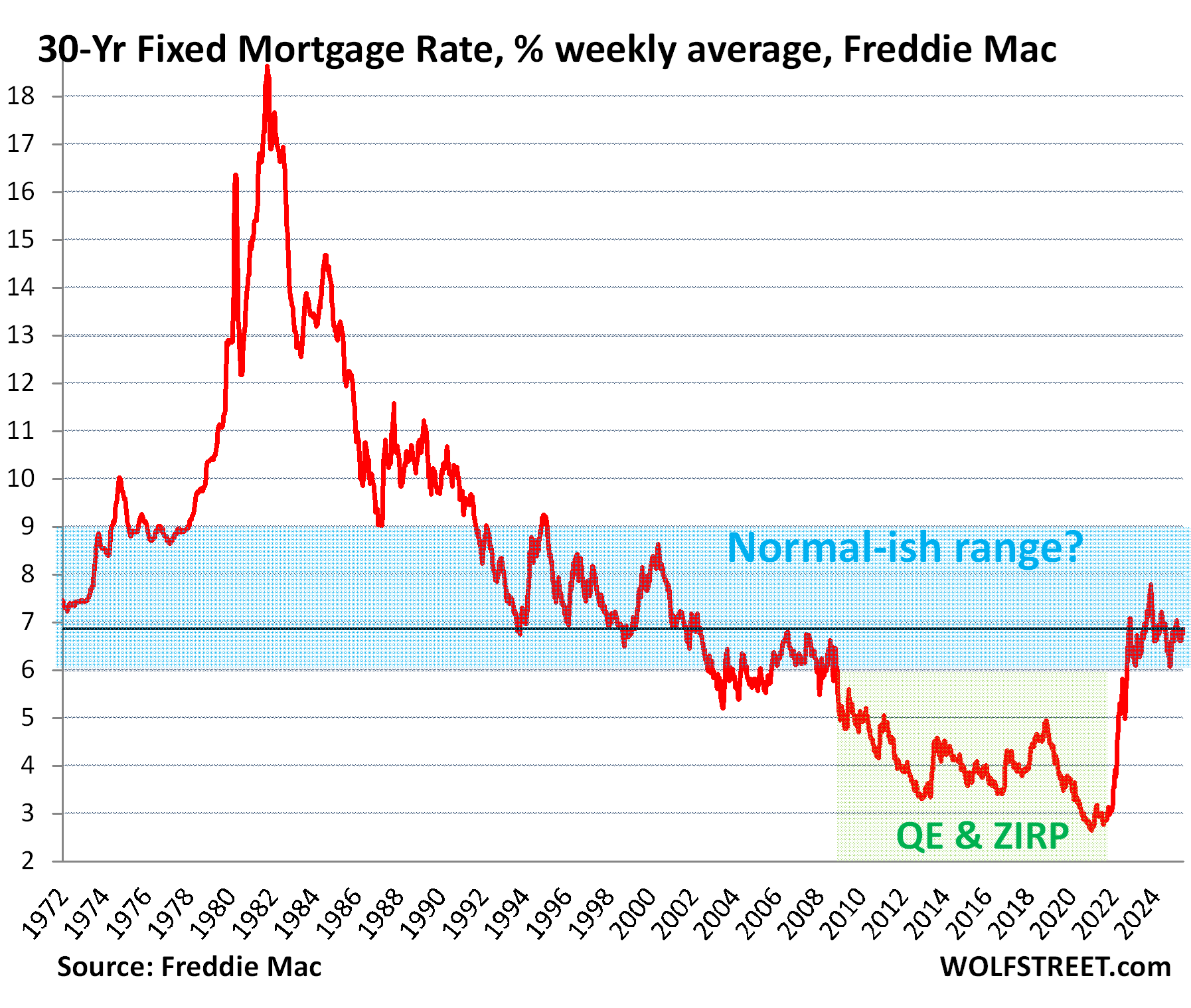

Mortgage rates are in the historically normal-ish range.

The average 30-year fixed mortgage rate ticked up to 6.86% in the latest reporting week, according to Freddie Mac today. This measure of mortgage rates has been between 6% and 8% since the fall of 2022, and most of the time just above or below 7%.

Historically – with exception of the outlier period of interest-rate repression by the Fed through QE that started with the Financial Crisis – these rates are roughly normal-ish.

The housing industry obviously loved the Fed’s interest-rate repression because it caused home prices to explode, and so the industry blames the historically normal-ish mortgage rates for the plunge in sales without blaming the ridiculously inflated prices that the ultra-low mortgage rates produced and that are now far higher than the market can bear.

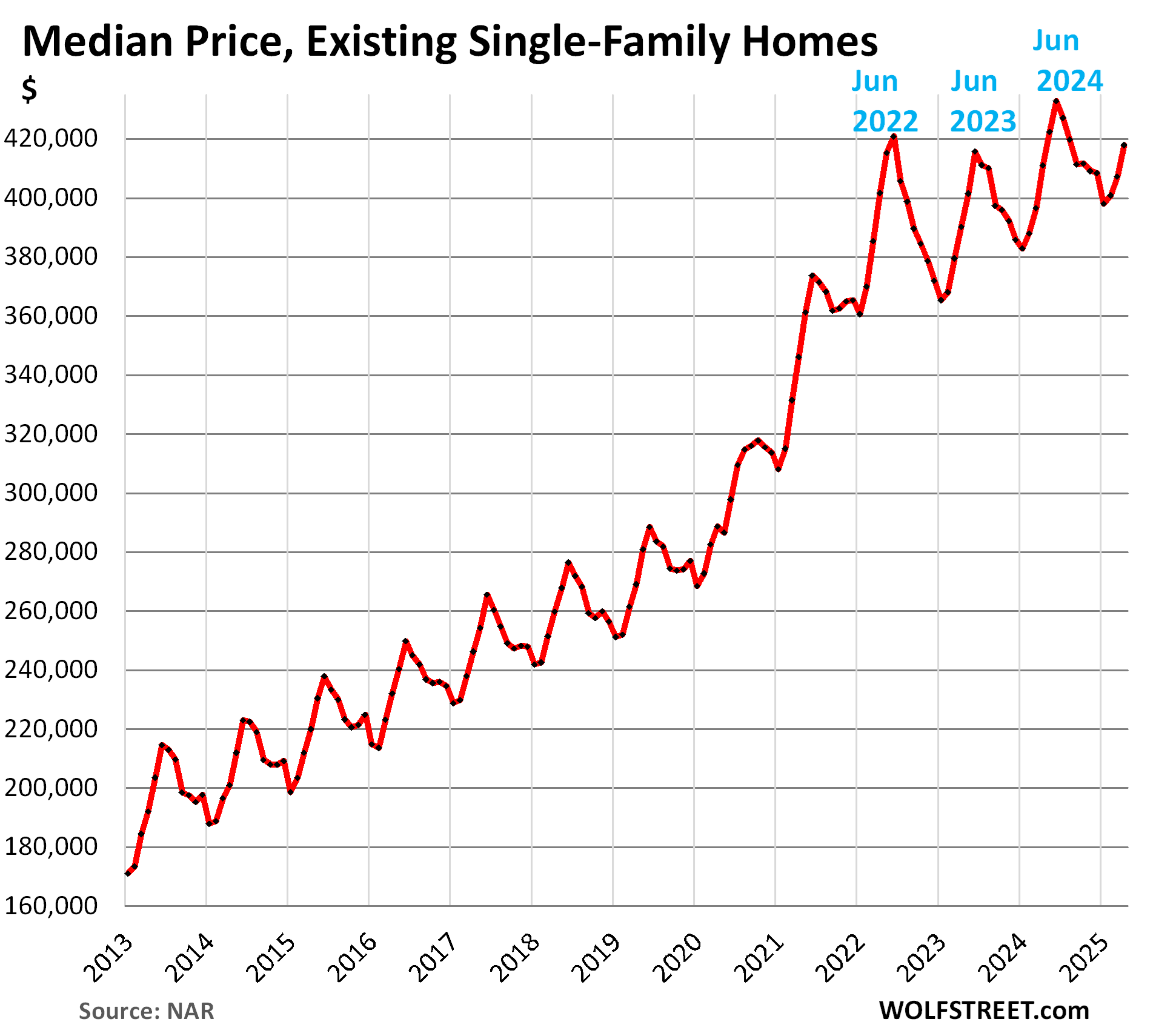

Median price for single-family homes and condos.

The median price can be heavily skewed by changes in the mix of homes that sold. In the spring, nationally, more higher-end homes come on the market and sell, which changes the mix of what sold and shifts the median price higher. It does the reverse in the fall and winter and shifts the median price lower. Hence the seasonal ups and downs in median prices.

Single-family homes: The national median price rose to $418,000 in April, whittling the year-over-year increase down further to just 1.7%, the fourth month in a row of narrowing year-over-year increases (from +5.9% in December).

This measure of the national median price had exploded by 50% in the three years between June 2019 and June 2022, on top of the large price gains in the prior 10 years, driven by the Fed’s interest-rate repression. Now prices are simply way too high and don’t make economic sense. Textbook demand destruction has ensued.

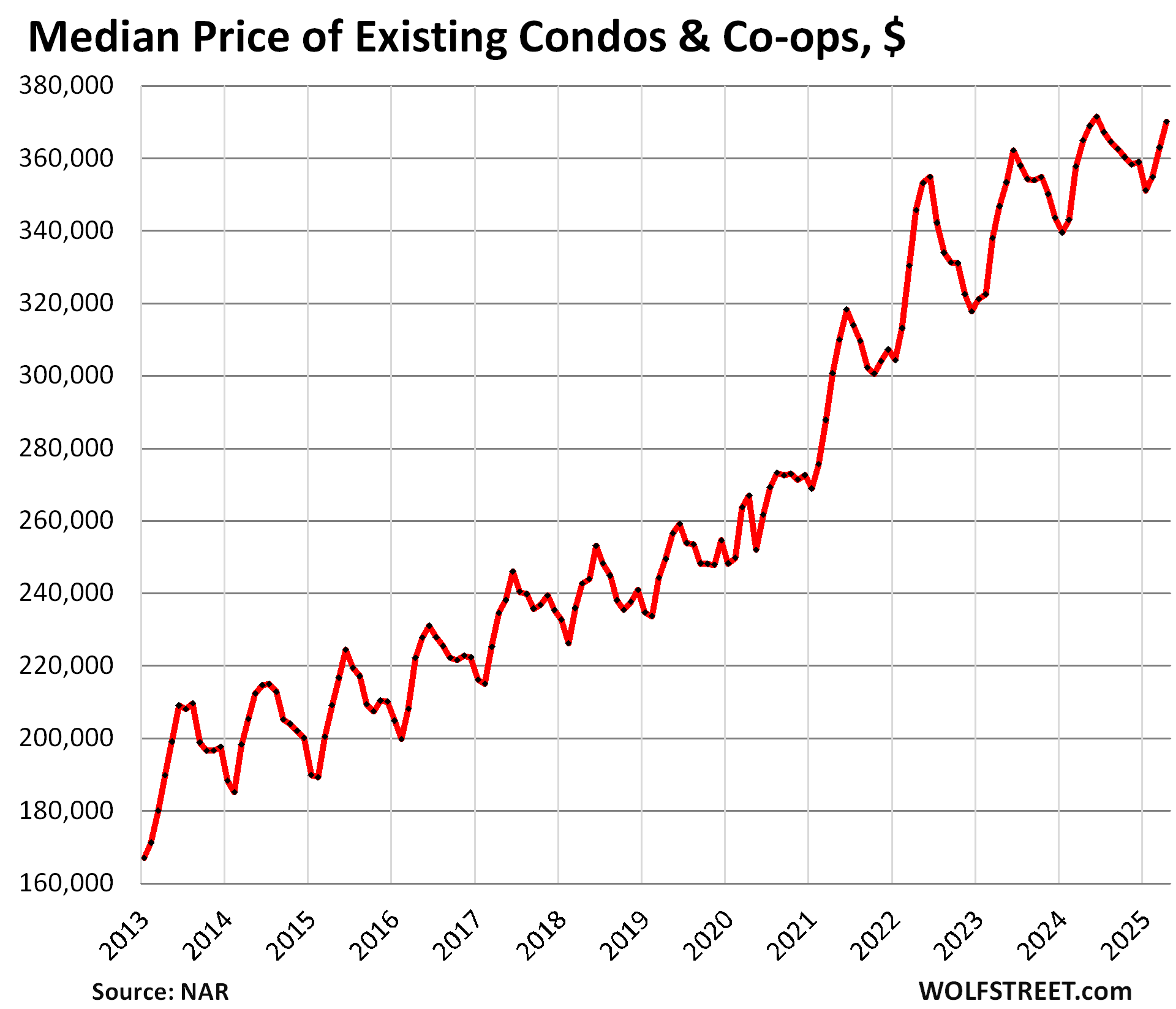

Condos and co-ops. The national median price rose to $370,000 in April, which whittled down the year-over-year gain to 1.4%, the fourth month in a row of narrowing year-over-year gains (from +4.5% in December).

But every market has its own dynamics. Some have significant price drops, others are still booking gains. I track home prices in the largest and most expensive 33 markets, quite a few of which are seeing home prices substantially below their peaks in mid-2022: The Most Splendid Housing Bubbles in America, April 2025: The Price Drops & Gains in 33 of the Largest Housing Markets

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The promised map of the four Census regions of the US:

Would be nice if we can carve out West to Coast West vs mountain West, the contrast might be pretty big I assume..

Interesting what will happen here. Because people all of a sudden become not in such a huge hurry to buy if prices are falling. They say, why not wait a little longer? Let them fall more?

Also if rents fall or stop rising another reason not to buy. Why buy when rentals are plentiful and rents are falling? Don’t have to worry about repairs, HOA dues, hurricane insurance, tornadoes, floods, property taxes, wildfires, etc…

Any rents pays for all of that in their rental/lease fee for property.

My friend bought a rental property last year for 1.2 million USD, and his monthly outlay was ~12K inclusive of everything.

He is collecting a rent of $5.4K/month in this 4BR/2BA home.

He thinks he is a smart investor and people renting from him are stupid, just wasting money on rent.

Only time would tell

So he rents at $5.4k per month and shells out $12k per month…

Sure, sounds brilliant…

Not every investment works out. Every investor knows that. It’s called “risk.” Investors get paid to take risks. The problem in RE is that there is this mantra, “you cannot lose money in real estate.” So people get into highly leveraged risky investments in RE and are delusional about the risks. CRE has been shredding investors and lenders to little bitty pieces for over two years. Mom and pop single-family rental isn’t exactly CRE but it’s very close to it. So you have rental income and you have costs, and you have tax benefits, and sometimes subsidies, but rent is set by the market, you cannot charge what you want or need, and so there’s this problem. And then the value of the property could tank, and has already massively tanked in CRE, and so what do you do? It’s a tough question. And every investor sooner or later has to deal with it.

“Any rents pays for all of that in their rental/lease fee for property.”

😂🤣👌

One of my favorite things I read recently was a quote from a woman who has an Airbnb in the northeast. She was griping about how she was bleeding cash every month, asking what to do, because she was having to subsidize the mortgage on the property while she also had her primary house to pay for.

Another real uppity woman chimed in and said something like “mortgage on an Airbnb? Hah! Ours are all paid for in cash. I don’t know anybody who has a mortgage on an Airbnb. Then the two got into a nasty exchange.

“why not wait a little longer? Let them fall more?”

I get what you are saying – but it basically translates into the rationale for every anti-deflation Jihadist since 2000 (“Oh sweet Jesus, sales have flattened/sunk in Product X – reset interest rates to zero before the universe ends!!!”).

Every ruinous bubble/implosion since 2000 has been the direct result of that thinking, its psychotic progeny ZIRP, and the resulting asset inflation delusions.

Rents won’t fall until everything associated with the property falls, specifically, the insurance, the taxes, the cost of upkeep, etc. Just covering the mortgage alone is a losing battle for the landlord.

What’s going to be interesting is the loss of tax revenue as property depreciates. How many wanna be buyers are also going to suck up the loss of services? Cities are notorious for not lowering taxes as assessed values adjust downwards. And all of those who’ve been giving out contracts based on the huge increase in property taxes are going to have to either cut entitlements (which is political suicide) or raise taxes elsewhere. There isn’t a whole lot of untaxed revenue left unclaimed.

If anyone has a house in the US to sell and actually wants to sell it, then just lower the price to something attractive such as 90% off what you ‘thought’ it was worth and then if it is worth more it will get bid up during the selling process. Simple as that.

Not so easy when you bought the house in 2021-2024 time frame and your equity is paper thin, plus your RE tax and insurance has gone up 30%. You have to mentally recognize the loss.

Currently, there’s a ton of listings by people in this position. In many cases they are trying to sell at the price they paid plus the expected sales commission. They don’t want to lose anything, because they don’t have a lot of money to lose.

Unfortunately, Mr. Market doesn’t care about that.

“Not so easy when you bought the house in 2021-2024 time frame and your equity is paper thin”

So lets ruin the economy (again), so that no speculative homeowner – ever, anywhere – has to take a loss despite their delusional valuations.

We’ve had 20 years of that in multiple asset markets and all we end up with in the end are the destruction of dollar earning power (ZIRP) and hopeless debts transferred to the G.

At least this time, the stack of the foolish was somewhat smaller.

It seems like the entire economy IS asset bubbles. At least that’s the way our leaders think.

Tsonder,

America’s last manufacturing industry is baloney.

I think that’s a pretty small subset of the sellers. There’s a much larger cohort that bought years and years ago, but watched in 2022 as their house was “worth” X and so now anything below X is a “loss” even though they bought at a price way way way below X. It’s that whole mental block. “well 3 years ago it was worth X if I sell it below that I”m losing money”.

I’ve seen it happen locally. One guy actually pulled his house off the market (and i quote) because he was getting lowballed and “I know what my house is worth”. Ummmmmmmmm that’s not how this works.

Nationwide, it’s a small subset of sellers. In places like Florida, where I live, Austin, Nashville, Colorado to a lesser extent, and others, it’s a huge percentage, as “investors” got involved. Remember, in some of these markets, prices doubled. A lot of people who bought during the peak bubble mania are now getting cold feet and want to sell to minimize their losses. The problem is there are too many of them for everyone to get out whole. They’re either going to have to hold on to the house or sell at a loss.

It’s only worth what somebody else will pay for it. Stupid market efficiencies…

Nah, this kind of stubborness only goes one way, human nature at the core. People have no problem and wont be stubborn to raise prices to 100% overnight if they can get away with it and try to explain it away somehow it’s logical. Yet, dropping 5-10% let alone 30% + more is heresy and just not possible unless they are forced to..

Will we see another chase the price all the way down event? Time will tell..

“Date the Rate” folks are in for a long term relationship with the rate…

Or maybe these people are gaslighting themselves it’s not an abusive relationship to begin with…

Probably prepared to marry for the life time of the loan.

US Treasuries and mortgage interest rates will just keep marching upwards nicely in the weeks, months, and years ahead.

Yep, it’s going to take time to grind away the damage of the ridiculous pandemic mortgage rates… and really the unnecessary Fed MBS buying since 2009.

Looks like a few more years of sawtoothing in the Median SFH price should do it. Houses will slowly change hands one at a time at the right price for that buyer and that seller at that moment, nothing more or less.

I continue to think renting and waiting for prices to “plunge 50%” is not going to work out well for most people. Do what you have to do though.

In the past, home ownership was the easy guaranteed path to financial stability. Not any more. Prices need to come down a good 25% to 50% to alleviate the extreme price risk that exists today. People can lose their equity in a big hurry. A 20% price drop on a $1.5M house is $300K.

It all depends on what you bought it for. You are missing a crucial element of that equation.

Home borrowers don’t understand that they are first off the gangplank when home valuation fantasies go bad – it is basically stock margin speculation with a thin veneer of greater respectability.

Banks have been running this game since time immemorial and everything is geared to make sure the rest of the world walks the gangplank before they do – that way the sharks may be full by the time it is the banks’ turn.

And yet people beg lenders for money…

I’d describe net worth as a bucket of water (the level is your net worth); with water pouring in (your income); and holes in the bottom (your monthly payment obligations).

It used to be that the mortgage was a large hole, but not too big, and it grew smaller over time, letting net worth (water level) grow over time. Today, the mortgage hole in the bucket is very large, and even if it gets smaller over time, it stays very large, leading to difficulties building net worth. Granted, rent, the only other choice, only gets bigger over time. So… it’s rock vs. hard place.

But you have a *lot* more affordable choices in apts – live in studio, 1 bedroom, or 2 bedroom with your 2 person family.

And don’t tell yourself that the 4-6 bedroom McMansion (50% empty) “is your only choice”.

It is a choice to *speculate* driven by perpetually horrible government policies (absurd zoning strangling supply, ZIRP providing crack-LSD to demand).

Prices are still making higher lows, and higher highs (except for 2023).

I agree with the idea that at some point, sellers will accept lower prices in order to move the merchandise. I just don’t know when that “some point” will arrive.

What would the median price chart look like starting in 2000 or so, to catch the runup to the 2008 bust? the FRED site’s existing home sales only had one year’s worth of data.

“FRED site’s existing home sales only had one year’s worth of data.”

I noticed that before.

Interesting, that.

Fortunately there are alternative sources of data – just Google “US existing home sales by year”

You have all the data right here. Why are you googling around to get the same data that is here on this site, and then when you cannot find it on FRED or by googling around, you complain about it here in the comments, and make up conspiracy theories. You people are funny. Here are some examples:

1. Median prices going back to 1989 for existing homes and new houses. I posted this chart many times, including here:

https://wolfstreet.com/2025/02/26/inventory-of-new-houses-for-sale-highest-since-2007-builders-push-mortgage-rate-buydowns-price-cuts-and-incentives/

2. Annual sales (actual sales, not rates or adjusted) of existing homes going back to 1994 (second chart, which I posted several times in different articles) ===> RTGDFAs:

https://wolfstreet.com/2025/01/24/sales-of-existing-homes-finally-begin-to-thaw-just-a-little-amid-highest-supply-for-december-since-2018/

3. Annual sales of new houses (actual sales, not rate, not adjusted) going back to 1984 by region:

https://wolfstreet.com/2025/01/28/glut-of-new-houses-for-sale-in-the-south-at-all-time-highs-bigger-even-than-during-the-housing-bust-the-west-is-getting-close/

and for the entire US (chart in lower part of article):

https://wolfstreet.com/2025/01/27/inventory-of-new-completed-single-family-houses-for-sale-spikes-to-highest-since-2007-builders-prop-up-sales-with-lower-prices-bigger-incentives-smaller-houses/

2. Seasonally adjusted annual rates of sales per month of existing homes, for the US (here going back to 2005) and by region (going back to the 1990s) ===> RTGDFA

3. Actual sales per month (not seasonally adjusted, not annual rate) going back to 2020 (the one where FRED only shows the past 12 months, LOL). I posted this many times, for example here, first chart at the top:

https://wolfstreet.com/2025/03/20/buyers-strike-not-letting-up-sales-of-existing-homes-have-worst-february-for-since-2009-as-inventory-surges/

3 to 4 million existing home sales per year was fairly much the norm from 1980 to 1995.

It was only with the rise of interest-rate speculating “buyers” and the insanity-rocket fuel of ZIRP that 4 to 5 to 7 million became the norm later.

With that wholly artificial surge in demand, prices went insane until they collapsed under their own unsustainability (interest rates were *never* going to be allowed higher than close to zero?)

The number of households was a LOT smaller back then. So fewer homebuyers and sellers.

“number of households was a LOT smaller back then”.

Sure, and it is amazing what human trafficking on a governmental scale will do to “demand”.

Under real economy stress (see 2000 to date) households rationally restrict their growth (in numbers, expenditures, etc.).

But that is Satan’s work (deflation) in Keynes-world (where perpetual deficit spending, granted to politicians, is an absolute necessity…for the children, ahem).

So every single policy measure (except reform) is slewed to “stimulate” “demand” no matter how artificial, transient, or unsustainable.

Let’s see how NYC, Boston, Chicago are loving those “incremental households” that resulted from the bus relocations of illegals that punctured the liberal cities’ empty moral gasbags.

WR has been documenting the prices in his site over many articles.

One of the hottest housing market Austin is already down 22% from peak.

SFO down 14% from its peak.

This is happening despite strong economy and job market.

Love love love to see this….funny how on /REbubblejerk on Reddits, this data is not going over so well with the folks in that sub. It’s quite funny how much cognitive dissonance people will go through to convince themselves RE is the no loss investment..

What we need now is for this momentum to continue and accelerate…I give it 50/50 this will be the case for desirable part of SoCal..

Fed needs to stay out of the markets and let it do its thing.

Eventually people are going to realize rate cuts aren’t coming and that home prices need to be lower in order to sell. The further we move away from 2021 era rates the better off the world will be.

MW: Home sales poised to slump even more as mortgage rates hit three-month high

The politicians are afraid of disturbing the fantasies of older voters, those who have owned homes for decades and have been chortling over the value increases in their properties… They should instead give priority to younger couples wishing to start families on their own priorities. This is more in the national interest.

In other news, Lawrence Yun says housing will be up 35-45% by 2027 so if you have any cash in any account should should simply withdraw it and give it to the nearest real estate agent.

We can always count on good ol Lawrence to earn his paycheck from REIT…if good old Lawrence wants a job, I am sure this adminstration could use another spin doctor to booster whatever narrative they want to sell

Its just a matter of time, waiting for the job losses to start. That is what will cause the dam to break.

Yes, job losses will trigger a mass sell off of properties at fire sale prices. We’re overdue for another recession. It won’t be pretty.

You’re in Canada. You’re speaking for Canada — “we’re overdue…” — Maybe that’s the scenario you’re looking at THERE.

West Coast Canadian here.

Similar story here. Especially in condos.

Other is issue is mtge renewals. Very short terms here. A lot was variable rates.

Rumours and readings say CDN banks are offering for renewals, 70 to 90 year terms.

Anecdotally, offers being made, lower than asking, but sellers declining.

Locally, premium waterfront prices are still going up and with fast turn over. Because new build costs have increased.

Property taxes, carbon taxes, maintenance, & insurance are all escalating too.

All by goverment policy, by design and/or incompetence.

Frank,

*Better dwilling”

April 2, 2025

“Greater Vancouver real estate sales continued to slow even further last month. The board’s data shows just 2,091 sales in March, down 13.4% from last year. Outside of March 2020, when the pandemic kicked off physical buying restrictions, this March was the worst in over two decades.

At the same time, sellers weren’t as deterred as buyers. The GVR saw 6,455 new listings on the MLS in March, up 29% from last year. Lofty inventory should have helped balance the market and ease price pressures, but the opposite happened.

Sales are much lower, and new inventory is higher than historically seen. Sales are 36.8% below the 10-year average for March. At the same time, new listings are 15.8% higher—meaning this is the most well-supplied market in years.

The sales to new listings ratio (SNLR) was just 32% last month, indicating an oversupply for the price point. Typically, prices fall when this occurs, but they’re heading in the wrong direction with even less demand. Bizarre.

Prices have eased from recent highs, mortgage rates are among the lowest we’ve seen in years, and there are more active listings on the MLS® than we’ve seen in almost a decade,” said Andrew Lis, GVR’s director of economics and data.

Adding, “Sellers appear ready to engage — but so far, buyers have not shown up in the numbers we typically see at this time of year.”

Buyers have largely been absent despite a well-supplied market with mortgage rates slashed in half over the past two years. Only a handful of buyers have been willing to jump in, and were willing to send prices higher—even if the properties have some of the lowest competition in years. “

This is the thing ^^^^^ or forced retirement, sickness, change of Job location, divorce, up sizing, down sizing or even ownership costs getting out of hand. The only constant in life is change and thus …Life moves.

SALT deduction will change the direction

It didn’t change the direction when the deduction limit was imposed. So why should it change anything now?

But one thing it might do: increase consumer spending a little since some people save some taxes and might spend this money. Not sure if it would make any visible difference though.

Only about 14% of filers itemize and not all of them are in high tax states… You’re gonna need a bigger deduction.

I don’t know anyone who has even mentioned SALT one way or another when buying or selling a house.

It’s one of those things that is a nice to have, but it’s not a game changer for most people.

Also, the states with the most ridiculous bubbles, Texas, Florida, and Tennessee, have no income tax

Parabolic chart moves risk crushing crashes; from your fist chart, rocket ship up post Covid free money over shooting revision to mean, looking at fall 2010 levels as the last support level or target to be tested, The Canadian buyer chart and overall foreign buyers of $UST that you posted on May 17 screams risk to my eyes. If Canada or ROW needs to raise capital or just wants to de risk from US debt and Dollar. Houston, we got a problem! It’s no fun having problems when we are in outer space from being intoxicated that the credit bubble will keep going on forever. Parabolic chart moves say danger ahead! the Candian holding of US treasure that you posted on May 17, looks to be completing a blow off top! I am Guessing a $TNX 5.5% yield stop loss and the bottom in price will fall in bonds and housing!! The Supply of new UST DEBT will overwhelm buyers!!! Congress just ignores the math, but the high yield is a looker she will demand our attention.

When the dust settles what would the national average become. Will we ever see $280k average like 2019 or have we permanently changed to $380K national average?

That was my call. When this is over all the covid equity will be gone. unless the dollar crashes like 15% than i will be sad! I bought my dream house in fall of 2010 from a hedge fund that bought it from a bank post REO while i was in negations to buy it from the bank, they sold few hundred homes to hedge fund in one transaction It was 50% off 2008 ask, i sold another house shortly after for 30% loss, i was happy with our new home. Yeah, it can happen again.

10% depreciation nationally over the next 5 years would be a lot.

In the 60 months following the feb-07 top the national index dropped 26% before turning north, and that was a housing driven recession. Homes were the toxic assets. Lots of other bubbles will need to pop before we get much more than 10% nationally

It might make sense to rent an apartment for a while, rather than invest in a home, until the current pricing disturbance is over. Y’think?

If Trump can separate the lips of GSEs (FNMA, FMCC, etc.) from the teat of government backing, and he is actively trying to do so, then the concept of unmanipulated supply and demand will return to the housing market, and affordability will skyrocket.

Why is Trump considering privatizing Fanny/Freddy if it would be another negative for housing?

It depends how they’re going to do it. If they also privatize the guarantee for buyers of future MBS, it would likely increase the yield of those future MBS, and thereby mortgage rates. But not by much, since the market will interpret the privatization like it was before the financial crisis, that there is an implicit guarantee hiding behind the privatization. The devil will be in the details in this deal.

I posted an excellent article here about a potential privatization, written by two authors who understand these issues much more so than I do. One of them, Alex Pollock, is an occasional commenter here. This is a very important read:

https://wolfstreet.com/2025/04/01/not-another-free-lunch-dont-let-fannie-and-freddie-turn-back-into-gses/

And the great housing freeze grinds on.

My guess is, eventually, inflation over a long period of flat pricing, a recession squeeze forces sales, and/or the Fed slashing interest rates should unstick things.

‘Cause right now, at these prices and interest rates, not enough buyers can make the math work.

House Republican Shreds Trump’s ‘Big Beautiful Bill’ as ‘Titanic’-Level ‘Debt Bomb’

Rep. Thomas Massie (R-KY) broke ranks to deliver a stark warning that President Donald Trump’s “Big, Beautiful Bill” was a time “bomb” in a scathing Titanic-inspired takedown that argued the policies will send the U.S. full speed toward a fiscal “iceberg.”

During a combative stretch of floor debate into the early hours of Thursday, House Democrats lambasted the legislation as a cynical giveaway to the ultra-wealthy that guts federal health and nutrition programs, Massie joined them in protest to offer what he called a “dose of reality.”

Both interest rates and the growth of massive government and corporate debt are indeed headed much higher in the months and years ahead.