Nonbank mortgage lenders and loan brokers react quickly to demand, which has collapsed.

By Wolf Richter for WOLF STREET.

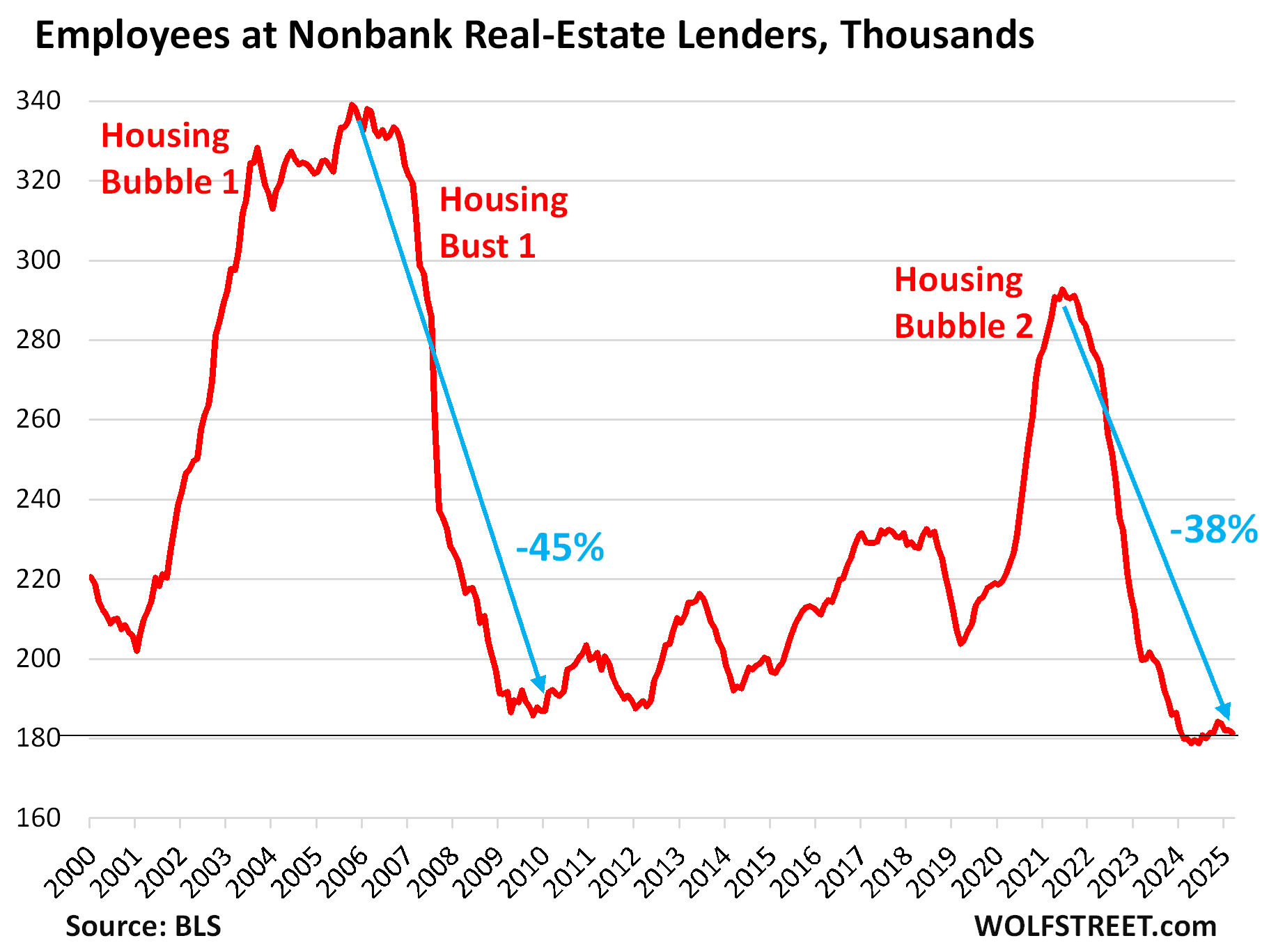

Mortgage lenders give a special perspective on the housing market because they sit at the epicenter of it. Employment at nonbank mortgage lenders – which include the largest mortgage lenders in the US, see list below – has re-declined four months in a row through March, after a mini-rise, having now plunged by 38%, or by 111,400 workers from the cycle peak in 2021, according to data from the Bureau of Labor Statistics.

Housing bubbles create employment bubbles at mortgage lenders. And housing busts undo those mortgage-lending employment bubbles as companies react rapidly to plunging demand in the housing market. The housing bust this time around is the plunge in sales volume to the lowest levels since the mid-1990s. Prices have also started to decline in many markets after the crazy spike.

The employment bubble of Housing Bubble 1 was even bigger than the employment bubble in Housing Bubble 2. Since then, a lot of work in mortgage lending has been automated, digitized, and moved online, requiring less human work today, and a relatively smaller workforce than 20 years ago:

Nonbank mortgage lenders dominate mortgage lending. The top three mortgage lenders by the number of mortgage originations – purchase mortgages and refinance mortgages – were nonbanks in 2024, according to data from Bankrate. Of the top 10, six were nonbanks.

The two largest mortgage lenders combined – United Wholesale Mortgage and Rocket Mortgage – originated more mortgages in 2024 (727,000) than the next eight largest mortgage lenders (banks, nonbanks, and a credit union) combined (647,000).

There are thousands of banks, credit unions, and thrifts that engage in mortgage lending. But the industry is concentrated at the top. The top 10 mortgage lenders provided 26% of total dollar-volume mortgage originations in 2024.

Note the right column, which shows the average size of mortgages by mortgage lender originated in 2024 – how they vary!

| 2024 | Mortgage lender | # of Mortgages | Billion $ originated | Average mortgage $ |

| 1 | United Wholesale Mortgage | 366,078 | 139.7 | 381,613 |

| 2 | Rocket Mortgage | 361,071 | 97.6 | 270,307 |

| 3 | CrossCountry Mortgage | 101,894 | 39.4 | 386,676 |

| 4 | Bank of America | 83,143 | 29.5 | 354,810 |

| 5 | Navy Federal Credit Union | 80,019 | 17.7 | 221,197 |

| 6 | LoanDepot | 79,418 | 23.8 | 299,680 |

| 7 | Chase | 78,529 | 38.2 | 486,444 |

| 8 | Guild Mortgage | 75,356 | 23.2 | 307,872 |

| 9 | Fairway Independent Mortgage | 74,404 | 23.7 | 318,531 |

| 10 | U.S. Bank | 74,138 | 29.2 | 393,860 |

| Total | 1,374,050.0 | 462.0 |

The jobs at the mortgage lending divisions of banks and credit unions are not included here – just jobs at nonbanks. But mortgage-related employment at banks ran a similar course as we saw with the announcements of mass layoffs in 2021-2023.

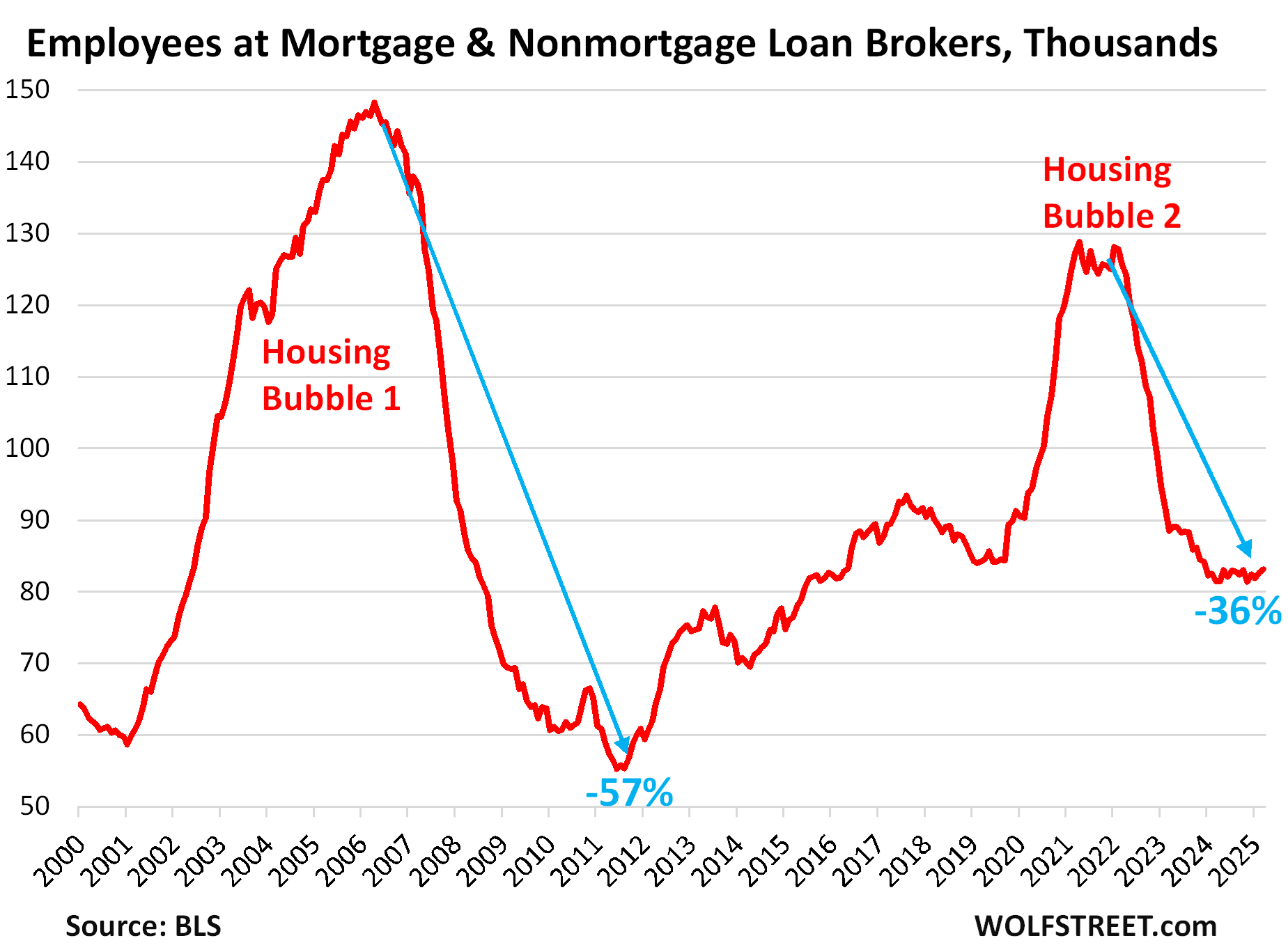

Loan brokers have seen a similar housing-bubble-to-housing-bust trajectory of job bubbles and job destruction. The metric here from the BLS includes all loan brokers, dominated by mortgage brokers.

But here, employment has ticked up a tiny bit in February and March. The mortgage-broker industry lost 57% of its jobs between 2006 and 2012 during the Housing Bust.

Currently they’re down 35% from mid-2021 levels, or by 42,500 jobs. But at the current level of 83,100 jobs, they didn’t get anywhere near setting four-decade lows, as employment at nonbank mortgage lenders has done.

At nonbank mortgage lenders and at loan brokers combined, employment plunged by 37%, or by 155,300 jobs, since mid-2021, or 37% of their total staff.

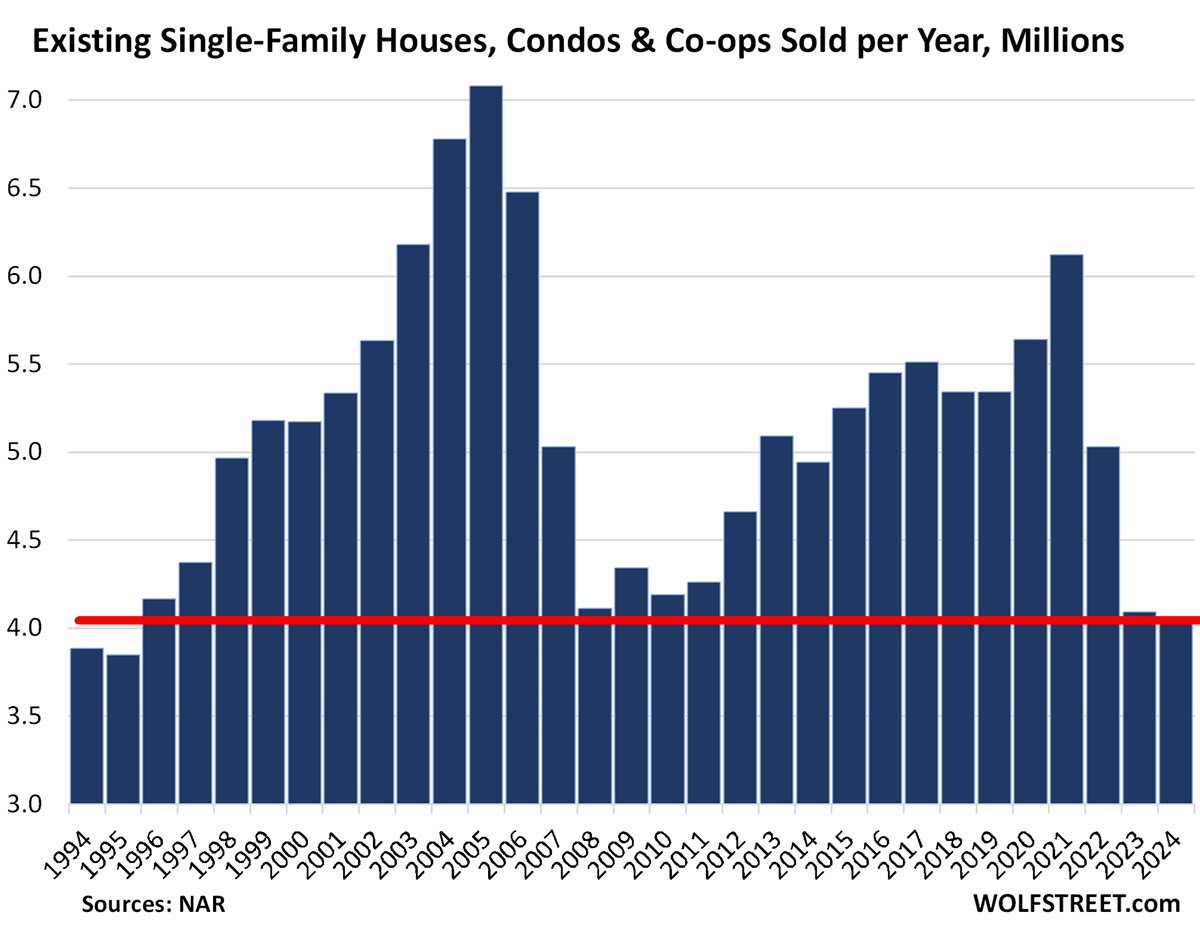

Employment in mortgage lending plunged because home sales plunged, and so mortgage originations plunged, and there wasn’t enough work to do.

Sales of existing homes in 2024 plunged by 24% compared to 2019, and by 34% compared to 2021, to 4.06 million homes, the lowest since 1995, below even the worst years during the Housing Bust, and demand destruction has continued so far this year, according to data from the National Association of Realtors.

This time around, demand destruction was caused by the spike in home prices that in many markets reached 50% or 60% or more in just two years. Those prices don’t make economic sense.

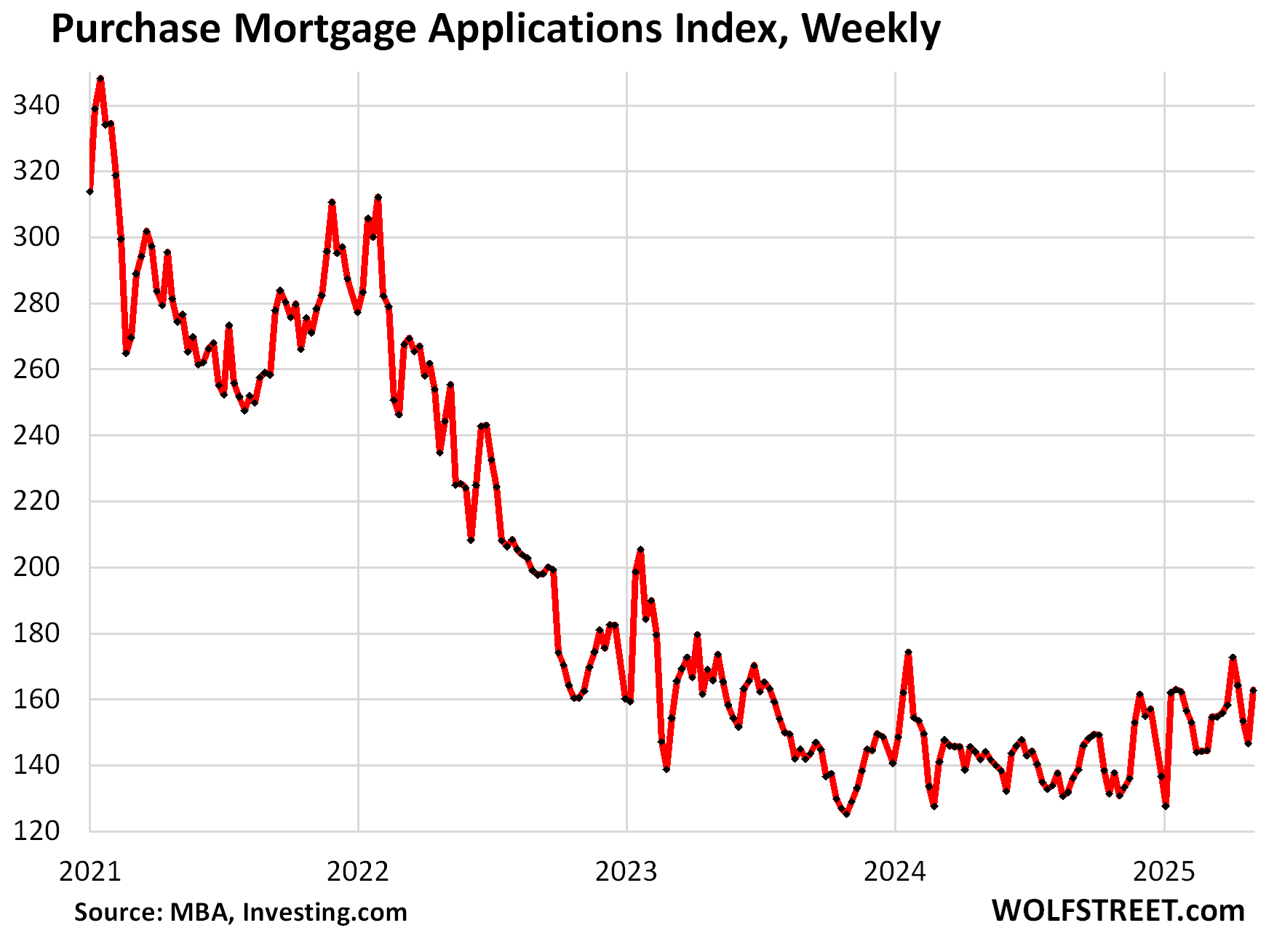

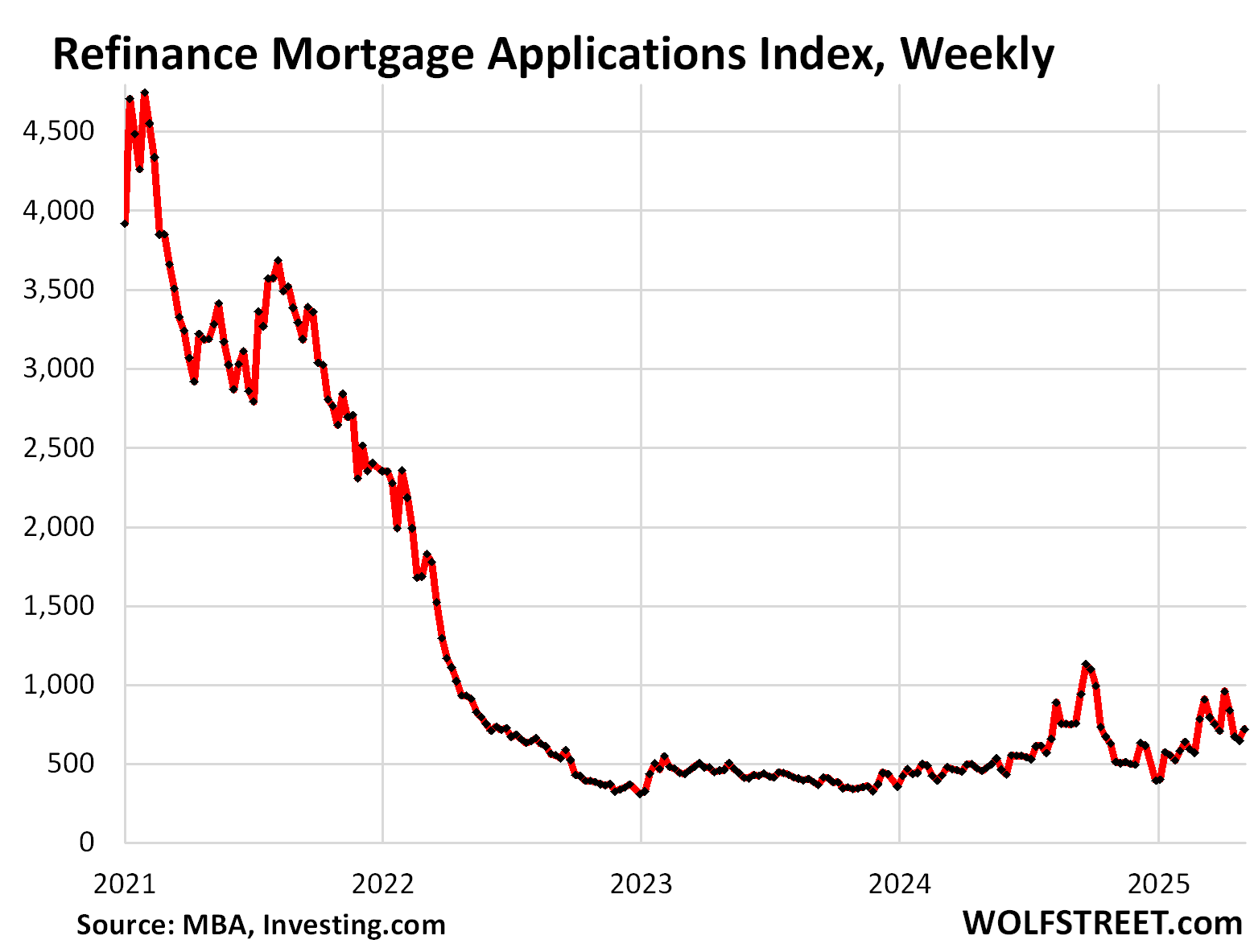

Mortgage applications plunged even more than home sales. And for the mortgage lending industry, that’s the metric that ultimately matters the most. The charts below of mortgage applications track the job destruction in the mortgage industry above fairly closely.

Applications for mortgages to purchase a home, though they ticked up from the lows, were still down by 40% compared to the same week in 2019, and by 44% from the same week in 2021, according to data from the Mortgage Bankers Association.

Applications for mortgages to refinance a home plunged by 42% compared to the same week in 2019 and by 78% compared to 2021, which had been during the historic refinance bubble triggered by the Fed’s interest-rate repression, when mortgage rates fell below 3%.

For mortgage lenders and brokers, this was a huge business that vanished overnight very quickly.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I suppose we can’t blame AI for these job losses? They need real humans to approve the deals?

You cannot blame AI for those job losses. But automation, digitization, and the internet, as I pointed out, have created efficiencies over the past 20 years that caused the employment bubble #2 to be quite a bit smaller than #1 at the peak. A lot of mortgage approvals have been automated for two decades or longer.

People will always need mortgages, so I wouldn’t weep TOO MUCH for those involved in that financial industry. The rage in the real estate market, the churning froth, has begun to finally settle down, a natural consequence of the business cycle. Strangely, the rise in real estate has been a worldwide phenomenon, from Australia to Canada to the U.S. Ah, well. We live in an interlinked world.

I watch a couple of real estate markets, and I see local market are not in concert. I see Oregon looking weak, and Phoenix is much stronger. The national directions is meh, and this article shows down.

Real estate stagnation and decline are always underreported, but this employment level says buckle up. But hey, look, the stonk market was full party today. So no need for the spear and magic helmet.

Three months into 4 years of chaos.

What? This bubble was because of the last 4 years of money go brrrrr.

It won’t have the same drop out as 08

Six years actually, they started printing again in 2019……….

Probably nothing like it but I still remember when I used to work at a company right next to New Century Mortgage, it was kind of unreal to see people in mass all leaving in tears from getting fired overnight…if there’s avalanche, this current definitely feels more slow moving than 08 or perhaps as they say this time is different….

08 was a subprime loans crisis that turned into a real estate crisis.

This is a pull back because houses are way too expensive and unaffordable. I like 06-08 we aren’t handing out loans to unqualified applicants anymore.

Volume collapsed this time. Not prices. They have come down in many markets but slowly.

If the collapse in volume persists, this should lead to a collapse in prices.

When prices fall, buyers disappear from the market because they are waiting for bigger discounts, and this leads to an avalanche of falling prices as sellers rush to get out through the exits faster.

Isn’t volume, especially in new construction directly related to price?

In SW Michigan the cost of new construction is at least two-to-three times per square foot more than the price of an existing home. And the quality of framing lumber, interior sheetrock and exterior material used today is nowhere near the quality found in the sixty-year-old mid-century homes.

Yes, the price increases of the past few years that exceeded even the broader elevated rate of inflation. But the super-heated over pressured air in that balloon for the most part has dissipated.

I can’t speak for anywhere else, but In our local market anyone hoping for materially lower prices is likely to be in for a long wait.

See the listing gor Coloma, Michigan for context.

Old Beyond Caring

“In SW Michigan the cost of new construction is at least two-to-three times per square foot more than the price of an existing home.”

I don’t even live in the US, but I read the wolf’s articles regularly. From them I know that new construction sales are well ahead of existing homes which have collapsed sales. This is because builders are offering discounts and selling while owners are stuck with 2021-2022 prices and are unwilling to accept the fact that they will not be able to sell at those prices.

“I can’t speak for anywhere else, but In our local market anyone hoping for materially lower prices is likely to be in for a long wait.”

The market is moving slowly, very slowly, and I have time to wait.

Patient people spend the money of the impatient

It will take awhile the reason some markets are moving down faster is also the 2nd home/Airbnb/vacation rental effect as those need to be sold and in strange places like Galveston or Tampa over saturated with higher costs all of Airbnb growth is international right now, the US is frozen in this category as well.

I agree. Every boom/bust is unique; this one fueled by COVID and then sky-high interest rates. COVID served to dislocate and encourage 2nd home buyers to work remotely pushing demand into more remote areas of the country. The high interest rates have “frozen” us into this situation with these high costs. Not sure what drives those prices back down – a recession? If interest rates were to come down significantly, it would encourage folks who have low rates to put their houses on the market. Why jump into 7% rates when you have 3.25%?

Be happy that present home mortgage rates are not as high as the long term average rate. 30 Year Mortgage Rate in the United States averaged 7.71 percent from 1971 until 2025, reaching an all time high of 18.63 percent in October of 1981 and a record low of 2.65 percent in January of 2021. The 1981 rate was an outlier just as was the 2021 rate. Responsible savers deserve an average interest rate just as responsible home buyers deserve an average rate.

Rates were not sky high the highest rate in the last 5 years has been our average the last 45 …

It will work itself out when individuals are forced to sell for any variety of reasons, from divorce to relocation for work to simply “aging out” into an assisted living or the great beyond. These individuals who are forced to sell will do so at the price the market sets, and this will ever so slowly lead the market back down. A recession with low interest rates would lead to a more rapid decrease as well.

“Volume collapsed this time. Not prices.”

Not yet.

Actually, who knows?

Although, in general, as volume evaporates, it becomes harder and harder to sustain current price levels – that seems like fairly basic supply and demand – less demand at the current price levels…prices have to fall to move the inventory.

That said, I will admit the adjustment downward has been very, very slow.

Given the fairly transparent insanity of 2020-2021 (especially in light of housing implosion 1.0) I would have thought that the *second* that the Fed ended the long night of ZIRP, a zillion speculators (see 2020-21) would have rushed the door.

(I wonder if holding period for capital gains treatment might have played a role in the exit lag).

It took 5 years after the financial crisis for prices to bottom out. This bust will also take that long.

Happy Jack,

While the absolute bottom may have taken 5 years, within 1-2 years from the top there were Wiley Coyote like plunges.

We have seen nothing like that this go round.

You are clearly correct that volume has collapsed, but not prices…the question is why, exactly? Why are prices so sticky? And if prices have not declined, is it realistic to say what houses are worth? If there is no one ready to purchase my home at its “real value,” isn’t the real value less? And why, with supply and demand (sorta) functioning, why is it that volume has declined so much faster than values? I know others are asking similar questions, but I just wondered what your take was on the split between volume and value. Thanks.

Very hard to say (my capital gains treatment holding period requirement theory was a WAG…if anything, I think it may only be 2 years…in which case, the ballsy speculator could have white knuckled it through 2023-24…in which case the panic dumping should have already begun).

In the end, I think it really matters *who exactly* went on a buying binge in 2020-2022, in the wake of a million-killing pandemic and Home Implosion 1.0 easily within living memory.

Rich speculators can white knuckle it longer because they have the resources and the risk-loving mindset. But you would think they (of anyone) know best the exact game they are playing (essentially interest rate speculation – hugely impacting the affordability of homes, especially after an insane run up in prices).

Because the need to buy has been weak as well either poor savings or not interested in a higher mortgage people are staying put the last 2 years a lot more then the last 30 year average.

Here in SE Tennessee I see PulteGroup and DR Horton clearing farmland and forest alike to slam up absolutely crap homes. Built close together these layouts are ugly acres of roofs. Sections arrive and are connected. No local subs all their guys. Called “10 year homes” here. A personal friend is a garage door supplier and installer. He and his son very conscientious and meticulous. Very few callbacks. A new owner in a mass-produced house called him and ask for repairs on their are garage door. Friend said it was such a poor install he’d have to remove it, supply proper framing and rails and reinstall. Owner said he tried to get builder to help, no response. These large builders blow in and go. Even their materials are brought in bulk. And not low-price either. Talk about depreciation literally built-in. We are a destination for internal refugees, not to mention border-crossers of course. The schools need more classrooms and utilities can barely keep up with infrastructure. Traffic counts exploding. Very frustrating for longtime locals.

We have a Dr. Horton travesty neighborhood going up in my town as well. Ugliest crap I have ever seen. People say exactly this on the local subreddit all the time, and a few people defend them desperately, poor souls having apparently settled for a life in this dystopian neighborhood.

I call them “doctor” on purpose. Everything else about them is ridiculously pretentious and pathetic. Our Dr. Horton neighborhood has alley names like “shiraz” and “pino”; make me barf. (Ought to be “Old E” and “Mickeys”).

Hey, why do these new developments have sets of six or ten townhouses, but then a bunch of wasted space until the next grouping? If it’s gonna be dense and ugly, why not go full bore?

Toured a Pulte development in Vero Beach, Florida, where the buildings were sandwich together so they could literally spit on your neighbor’s house. They were so close. They called the view privacy, but I think penitentiary would be more appropriate.

Small wonder they can compete on price with existing homes.

That sounds a lot like The Villages in Florida. Nothing but cookie cutter with zero charm and character. Wife and I are renting for a year trying to decide if we really want to be here. Love the active lifestyle but hate the “penitentiary” feel.

Unlike the KnoxvilleTN area, the listing inventory is growing exponentially in The Villages. We smile at the $5K price drops when other sellers are dropping $25K and $50K multiple times.

You’ll know the neighborhood has hit rock bottom when you see a street named “Mad Dog 2020”

“Sections arrive and are connected. No local subs all their guys. Called “10 year homes” here.”

Bill, I get it.

*But* unless the supply of homes increases, the insane price levels (60%+ median income for monthly mtg pmts?) will last and last and last.

I think most people would choose living in a fairly crap house rather than living in a field – or selling oneself into mortgage debt slavery for decades.

Bill Voelz,

Life can be hard in a developing country like the US with few regulations or wealth. Someday perhaps we will have enough wealth to provide housing, health care, affordable education and food security. Our military barely gets by on a shoe string budget and corporations barely squeaking out a profit.

Billionaires Worldwide Race to the Bottom just means higher prices and lower quality for us debt Slave peons.

Wolf,

This was a good post on the mortgage *origination* side.

But the indispensable actor of the last 25 years of mortgage insanity is the mortgage secondary market (those mortgage brokers and banks *know* they are very frequently originating crap loans – and get them off their own books as fast as humanly possible).

So how about a post doing a deep dive on the mortgage loan secondary market – the ultimate bag holders and why they are willing to/incentivized to hold the bag…over and over).

The ultimate bag holders for most mortgages are the taxpayers of course, because the government (via Fannie Mae, Freddie Mac, Ginnie Mae, VA, FHA, etc.) buys and guarantees most residential mortgages. There are lots of articles and comments about this here on this site.

Huh, so kinda like student loans? Everything they touch turns to crap in desperation to remain in power. And they hold the populace hostage with muh “investments”, clowns to the left of me, jokers to the right, stuck in the middle with you.

Interesting question – do those Government Guarantors pursue mortgage default deficiency judgments…and if not, why the F not?

Absent the threat of being pursued for Guarantor losses/mortgage shortfall on the house(s) (deficiency judgment) then the system is really just absolutely inviting abuse (coupled with all the other Guarantor subsidies ladled throughout the system).

Right now, nearly anyone who bought in 2021 or before even with zero down can sell the home, pay off the mortgage, pay off the arrearage, and still walk away with some cash. Which is why defaults are a NON-ISSUE now. There are essentially no deficiency judgments with these high home prices. Deficiency judgments are only an issue after home prices drop a whole bunch for a long time so that lots of people are under water. In the future, if there are lot of forced sales like these, then prices might drop enough to where deficiency judgements will become a thing in the 38 states and DC where they’re allowed (not allowed in CA and 11 other states).

Given that non-bank mortgage lenders don’t have access to bank deposits and low-cost debt, who has been buying all of this non-bank mortgage paper?

The government, of course, all the entities: Fannie Mae, Freddie Mac, Ginnie Mae, VA, etc. They’re buying most of the mortgages regardless of who originates them.

Those government agencies only buy conforming mortgages for low-end housing and almost all mortgages in California, for example, are in the jumbo mortgage category and excluded from being purchased by those agencies.

Conforming loan limits, San Francisco metro: $1.21 million; San Diego metro $1.08 million; LA metro $1.21 million

The scandal of the relentless-upward-ratchet of conforming loan limits.

As with many other G policies, it is like the G has nothing better to do than french-kiss catastrophes-in-the-making

We have 13 cities in Florida where starter homes cost one million dollars. We have many older people living in huge homes, but unwilling to downsize. Why is this? One word sums it up, Inflation!! And the prospect for inflation. Governments are dispicable money spenders, they are all bad and nothing stops them.

@Andrew Pepper: Yes, we should dispense with all governments. Then we will have a perfect country. /s

“We have many older people living in huge homes”.

It really is magnificently idiotic that the McMansions trend simultaneously occurred with the shrinking of American family size.

It is reported that there are about 32 *million* unoccupied bedrooms in the US – versus 4 million in 1970.

And…think about how few (how very few) of those bedrooms got mobilized during the recent period of massive housing inflation.

It is hard not to think of superannuated British aristocracy rotting away in their unmaintainable manor houses or Citizen Kane wandering in senility around his empire of acres and acres of antiques.

There have been 12 boom/busts in real-estate since WWII (along with 13 recessions). But this one is different. This one wasn’t accompanied by disintermediation – a term that only applies to the nonbanks since 1933.

This seems to be a forward looking indicator.

Sales volume is now made up of a large percentage of cash transactions, people who had to sell or who have money to park (before the ever present “imminent crash”).

A probably lagging indicator is the number of realtors. The recent rise to a record 1.6 million, is now in decline. Nothing crazy, but another year of a frozen market will probably bring the number down substantially.

As an above comment notes: Older people are hanging on to their oversized (but paid off/ down) homes. Affordability in terms of absolute price, financing and insurance costs are still a factor for those who have accumulated wealth.

Don’t forget that even with health insurance and medicaid etc. Healthcare is a huge expense for an aging population (which is now including anyone over 40 who has been raised on the SAD: standard American diet).

I am selling one of my rentals. The market just does not make sense. CAP rate is too low. Appreciation is leveling off. But, looking at these charts though, it would make me thing we are at short term bottom on sales volume and not sell.

Insurance went up from $1750 to $3100 / year. Property tax went up from $2200 two years ago to $2800.

Zillow says it is worth $360k. Realtor thinks this is too high. Realtor said I should list the home for $340k and get a bidding war to get it up to $350k. That comes to $125 sq ft. I can only rent it for $2400/month so it is better to take the cash as CAP rate is now below 5%. It is better to put the money into treasuries IMHO.

Insurance company said two reasons for the increase was replacement cost is now $520k (up from $420k about 3 years ago) and I had the claim for the roof replacement after a hail storm. But, what is crazy is this house is insured at $180k (54%) more than what I can sell it.

“But, what is crazy is this house is insured at $180k (54%) more than what I can sell it.”,hmmmmm……,if no near neighbors seems a dropped cigarette in home is your ticket!

Kidding……,I think!

I would say a bigger/better hail storm would be also the ticket!

One of my customers is on your list. Went from 10,300 employees down to 4,400.

I find it interesting that people still think there will continue to be a supply problem. Baby boomers are dying at 6,000 a day, headed up to 10,000 a day. They are around 75% homeowners, and 80-85% of inherited homes go straight into the market for sale. Fannie or Freddie did an article not too long ago saying there will be a glut on a million homes a year for 8-9 years. I’m just renting until then.

Great data Wolf; quick question, do the loans include HELOCs?

Yes, in terms of the list of the top 10, it includes all types or mortgages including second lien home loans such HELOCs that nonbank lenders originated.