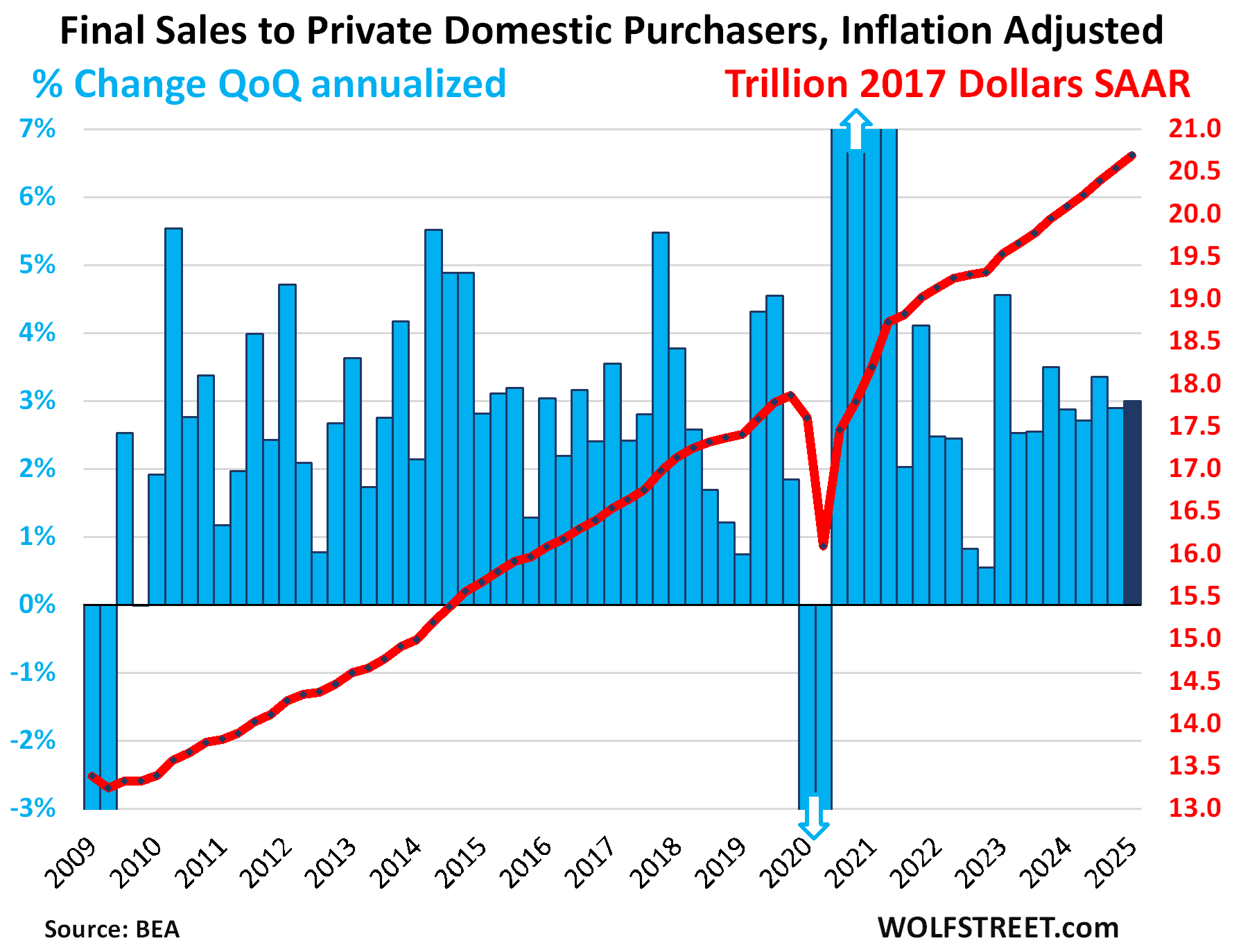

“Final sales to private domestic purchasers” jumped by 3.0%, on strength in the private economy of businesses and consumers.

By Wolf Richter for WOLF STREET.

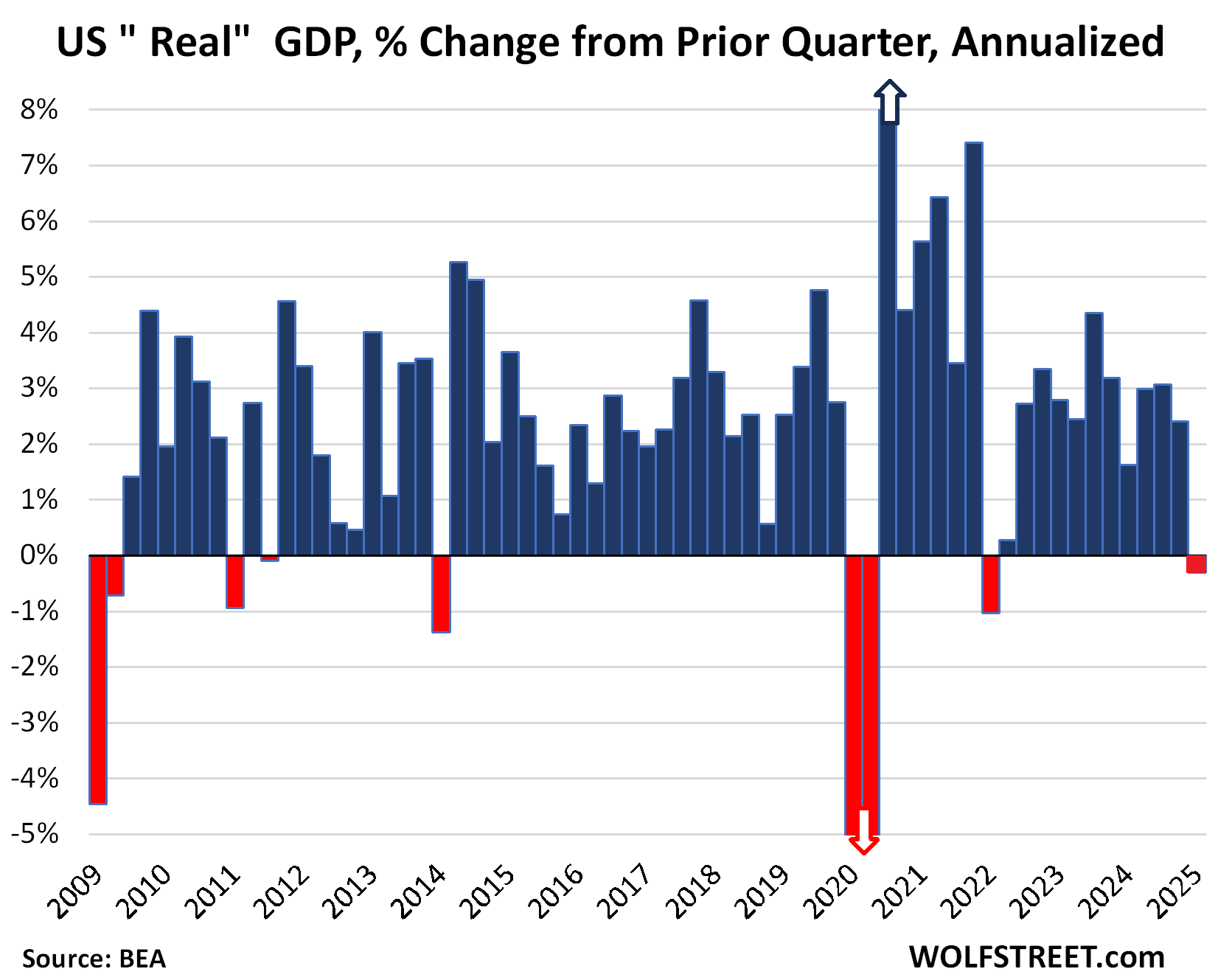

A massive spike in imports, by far the worst ever, on tariff-frontrunning subtracted 5.0 percentage points from GDP growth (adjusted for inflation), turning it negative. A decline in government spending subtracted another 0.25 percentage points, and turned GDP growth to -0.3%, despite decent growth in consumer spending (+1.8%) and a huge surge in gross private domestic investment (+21.9%), including a 22.5% increase in investment in equipment, as companies have begun ramping up investing in production in the US to avoid the tariffs.

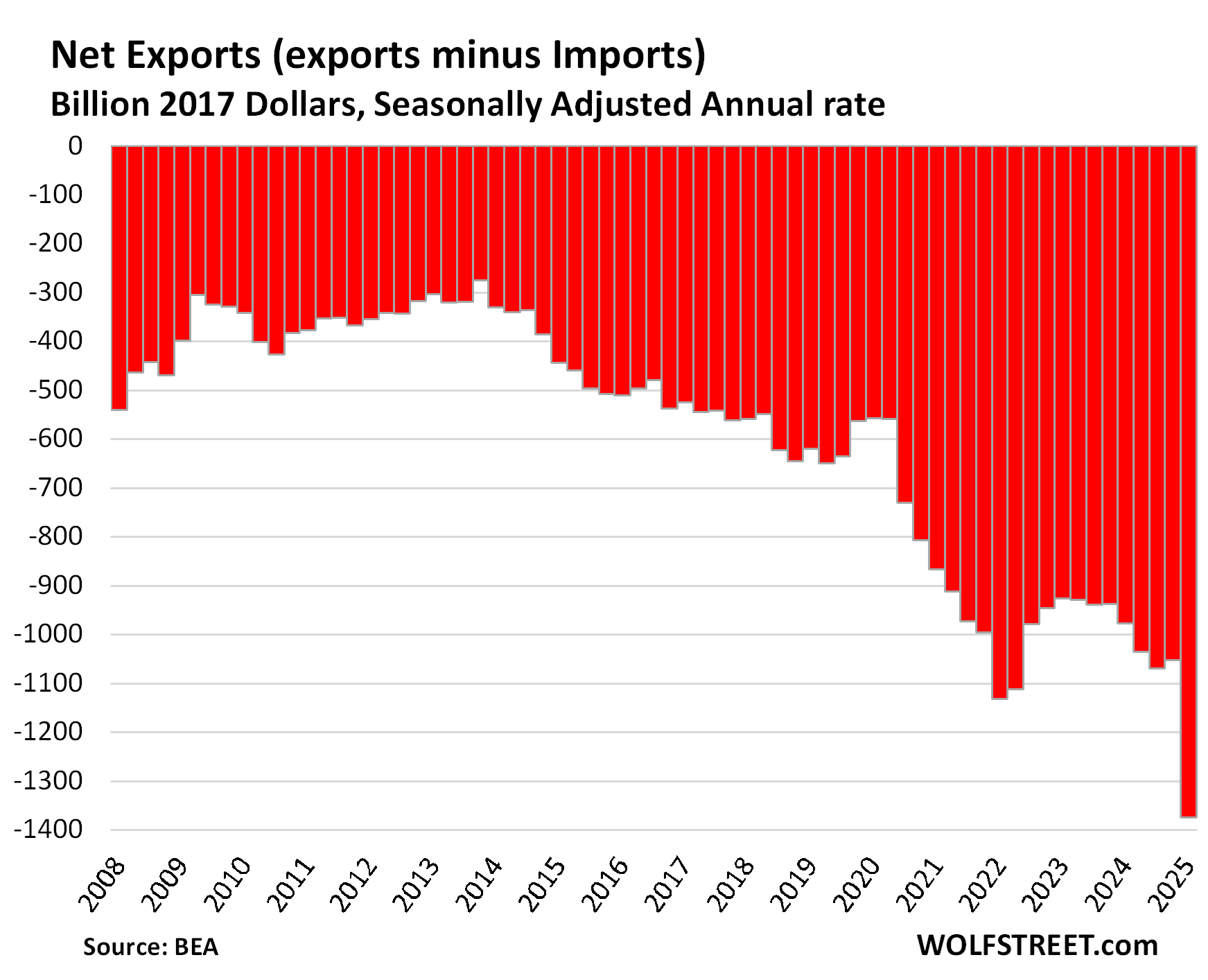

We’ll start with “net exports” because they’re the stars of this show today. Net exports are exports minus imports. Exports are a positive in GDP, imports are a negative in GDP. Net exports, driven by an explosion of imports on tariff frontrunning, worsened to a seasonally adjusted annual rate of negative $1.37 trillion in Q1.

- Exports: +1.8% (goods exports +3.2%, services exports -0.7%). Exports added 0.19 percentage points to GDP growth.

- Imports: +41.3% (goods imports +50.9%, services imports +8.6%). This reduced GDP growth by 5.0 percentage points.

GDP dipped by an annualized rate of 0.3%, adjusted for inflation (“real GDP”), after growth rates of 2.4% in Q4, 3.1% in Q3, and 3.0% in Q2.

Exploding imports are not a sign of weakening demand. The Q1 2022 drop in GDP was also caused by a surge in imports after the shortages as supply chains recovered and backed-up goods began arriving in the US.

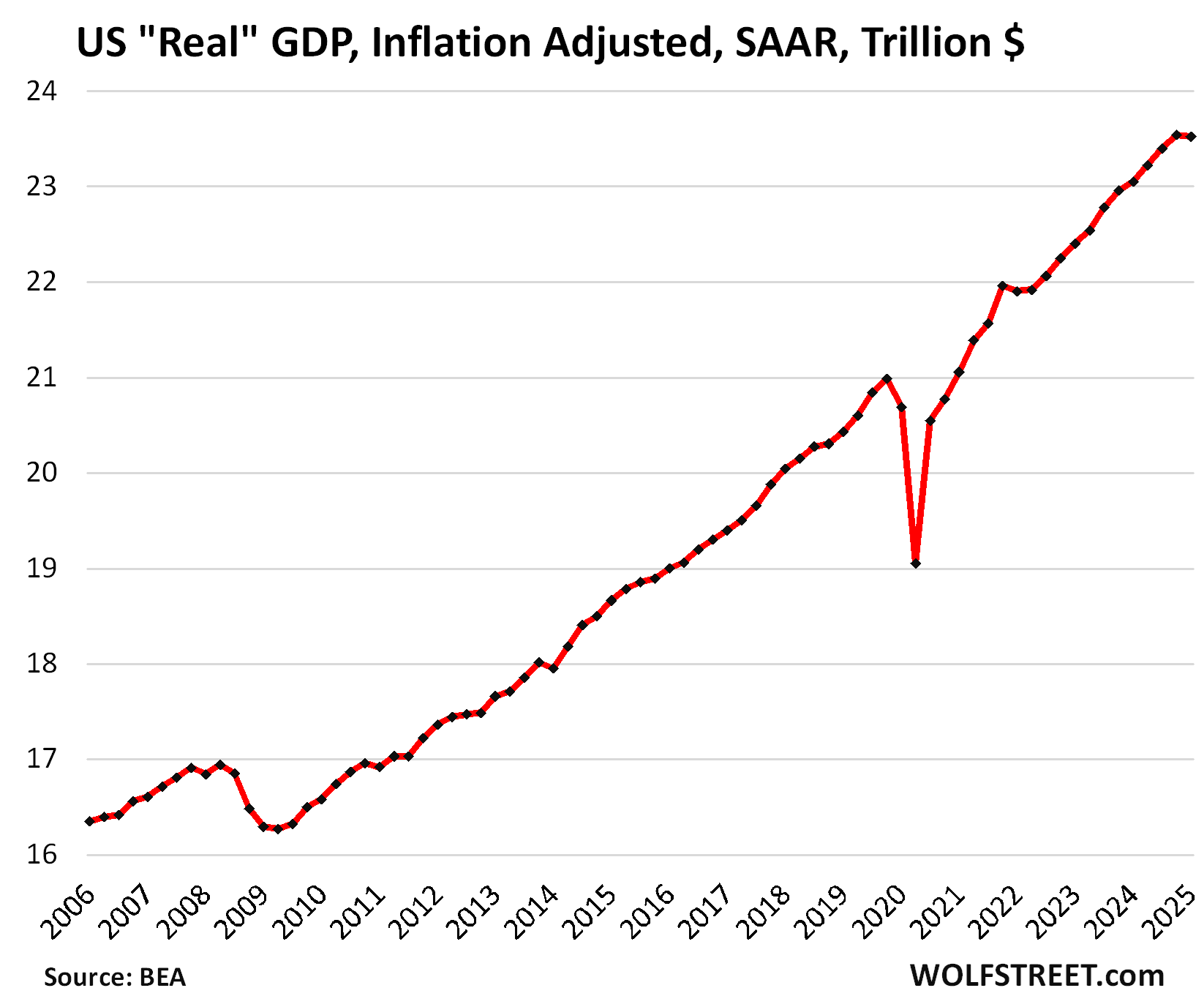

In terms of dollars, “real” GDP dipped to an annual rate of $23.5 trillion in Q1, according to the Bureau of Economic Analysis today.

“Final sales to private domestic purchasers”: The private US economy.

This metric is part of the GDP report, released today by the BEA, and tracks US private domestic demand from consumers and businesses, including fixed investments by businesses. It is GDP less exports, less imports, less government consumption expenditures, less government gross investment, less change in private inventories. It covers about 87% of GDP and presents the core of the private US economy.

Powell also mentions it from time to time as a purer indicator of private domestic demand from consumers and businesses – which is what monetary policy is trying to influence (not trade and government spending).

Adjusted for inflation, final sales to private domestic purchasers jumped by an annual rate of 3.0% in Q1, to $20.7 trillion, up from 2.9% Q4, attesting to the strength of private domestic demand and investments by consumers and businesses.

The blue columns show the growth rates (left axis), the red line shows the dollars (right axis), all in seasonally adjusted annual rates (SAAR):

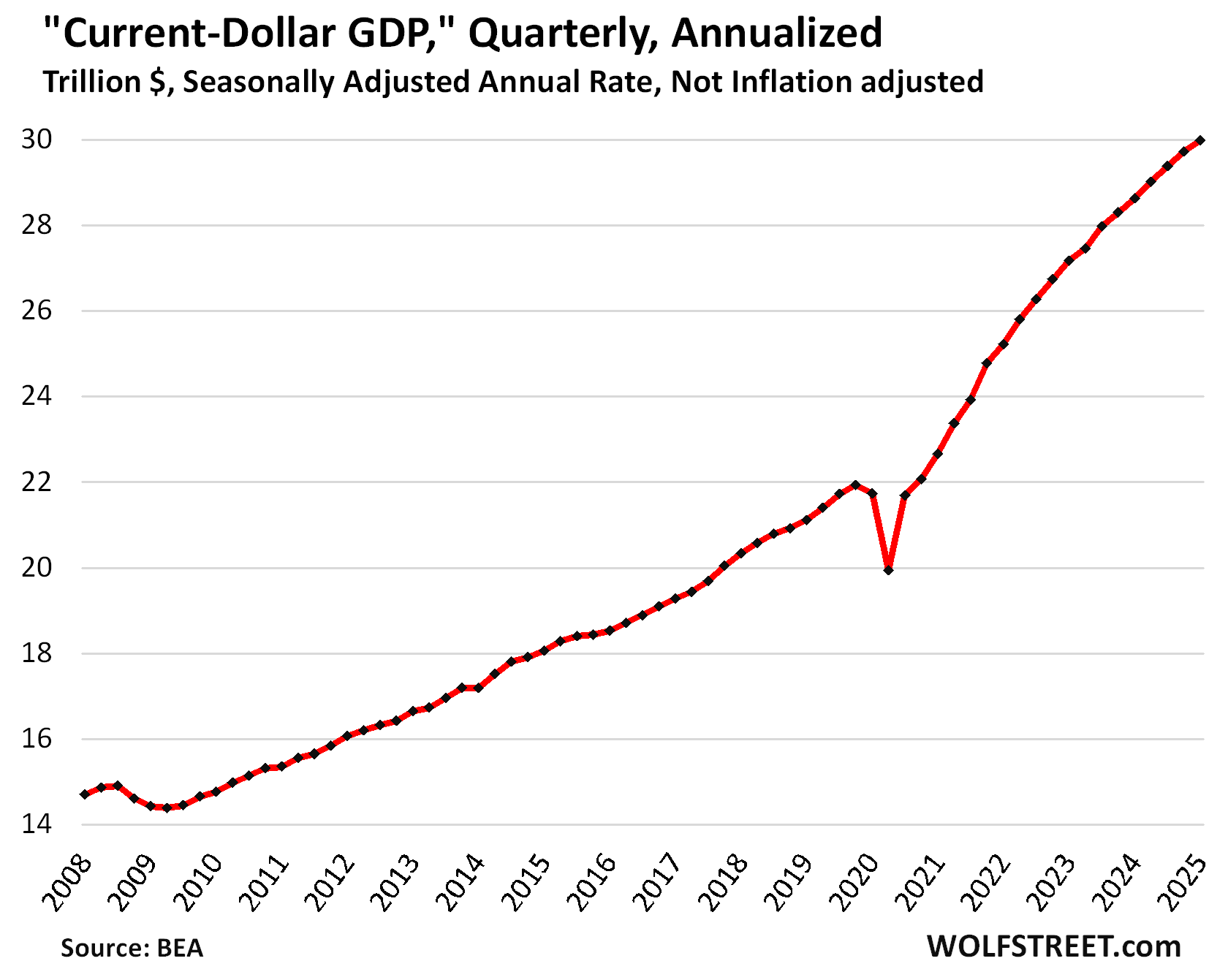

Not adjusted for inflation, “current-dollar” GDP grew by an annual rate of 3.5% to $30.0 trillion, measured in current dollars, not inflation-adjusted dollars. This sometimes called “nominal GDP” represents the actual size of the US economy in today’s dollars and forms the basis for the Debt-to-GDP ratio (further down) and similar GDP-based ratios.

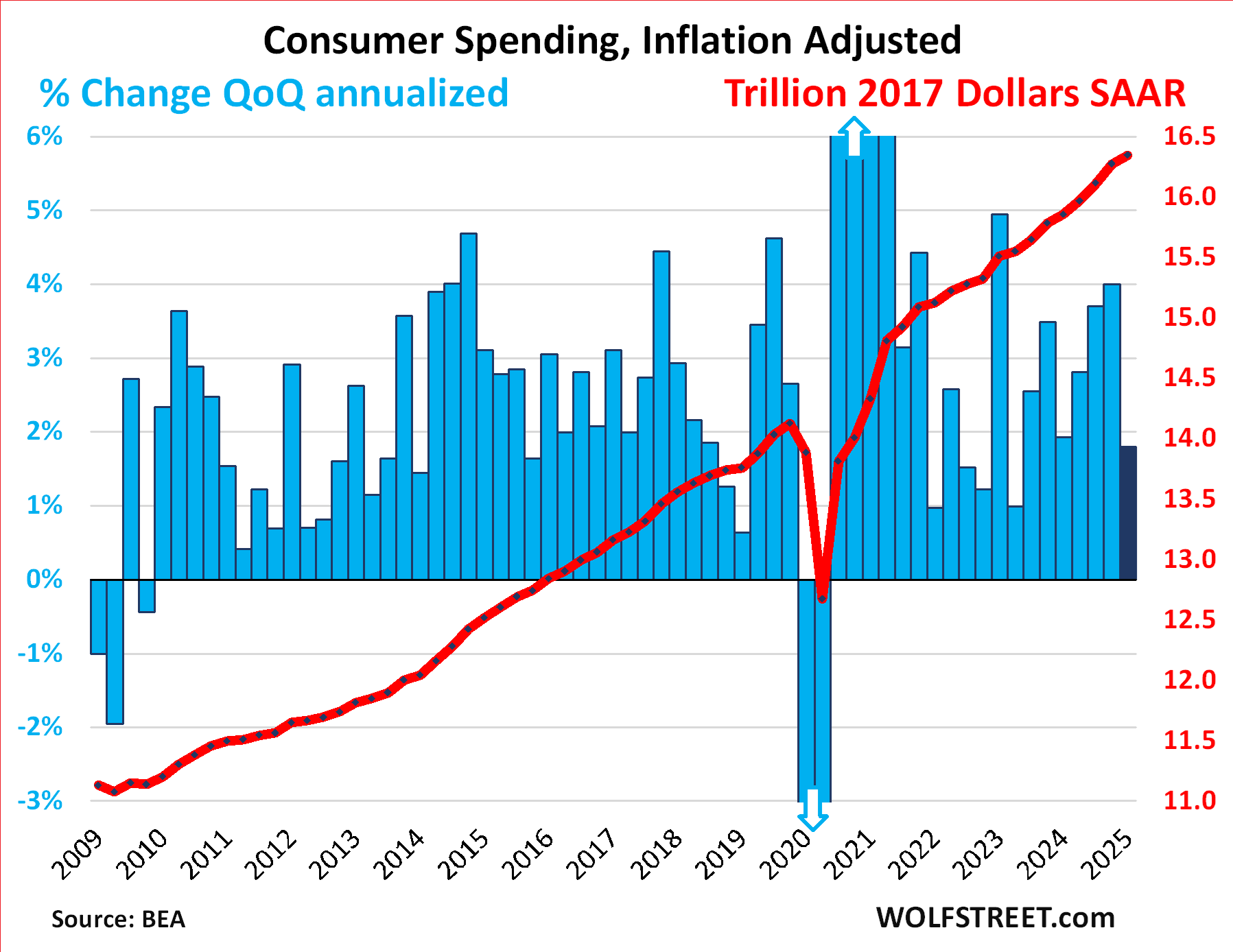

Consumer spending rose by an annual rate of 1.8% in Q1, adjusted for inflation, to $16.4 trillion, after three quarters of higher growth rates.

- Services: +2.4%.

- Durable goods: -3.4%%

- Nondurable goods: +2.7%.

Consumer spending along with business activities got “disrupted” by the wildfires in Los Angeles County (nearly 10 million population) in Q1, and the disruptions is included in the GDP data, but the BEA says, “it is not possible to estimate the overall impact of the California wildfires on first-quarter GDP.” So it’s in there, but it can’t be split out:

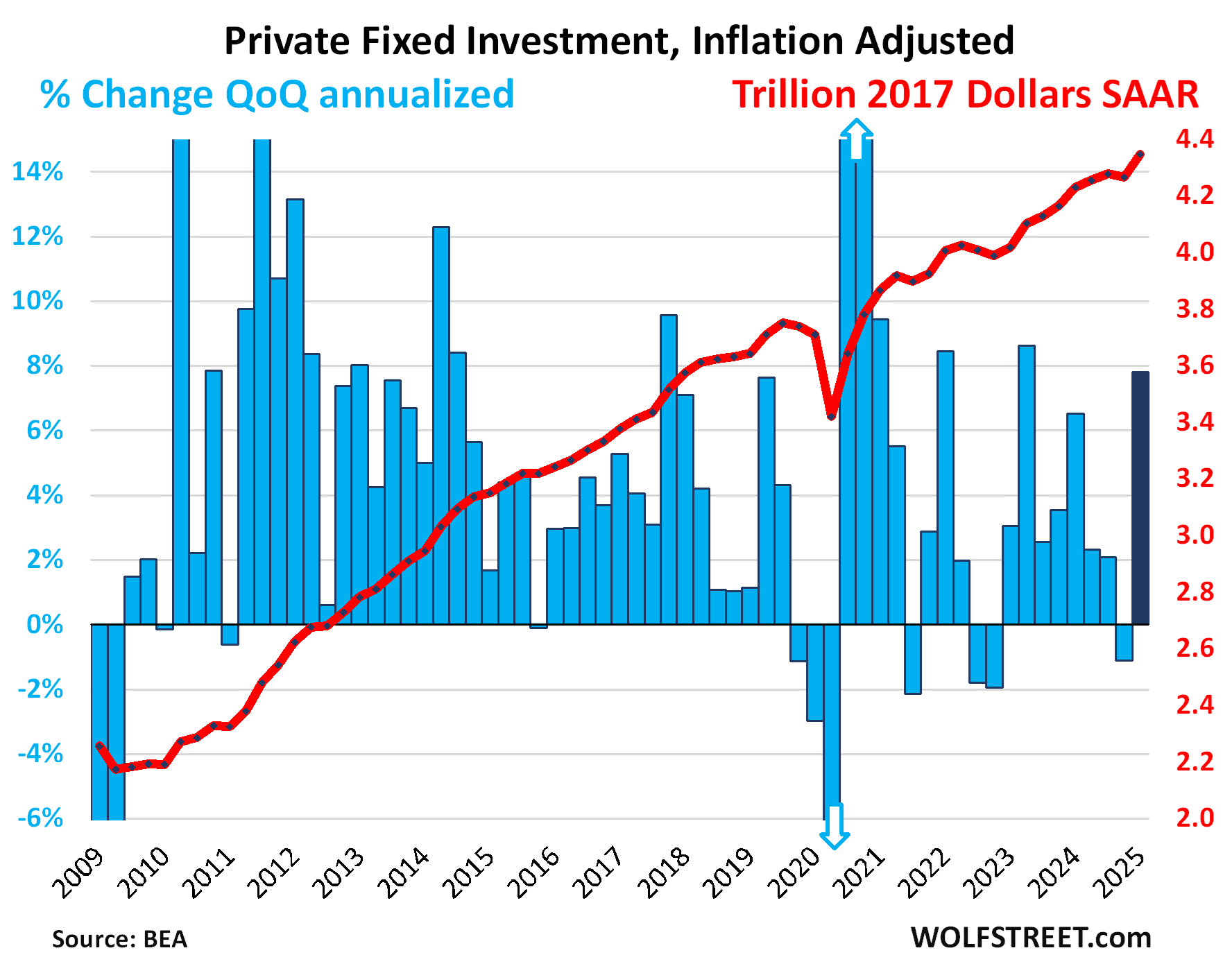

Private fixed investment jumped by 7.8% annualized and adjusted for inflation, the highest growth rate since Q2 2023, and the second highest since Q1 2022. Of which:

- Nonresidential fixed investments: +9.8%:

- Structures: +0.4%

- Equipment: +22.5%, the highest growth rate since Q3 2020, and the second highest since Q3 2011, as companies invested to ramp up production in the US, which is what tariffs encourage them to do.

- Intellectual property products (software, movies, etc.): +4.1%.

- Residential fixed investment: +1.3%.

Private inventory investment rose to $3.0 trillion in Q1, driven by the surge in imports that went into wholesale inventory. According to the BEA, the top contributor to this increase in wholesale inventories was imported pharmaceutical products, as drug companies were frontrunning the tariffs. This change in private inventories contributed 2.25 percentage points to GDP growth.

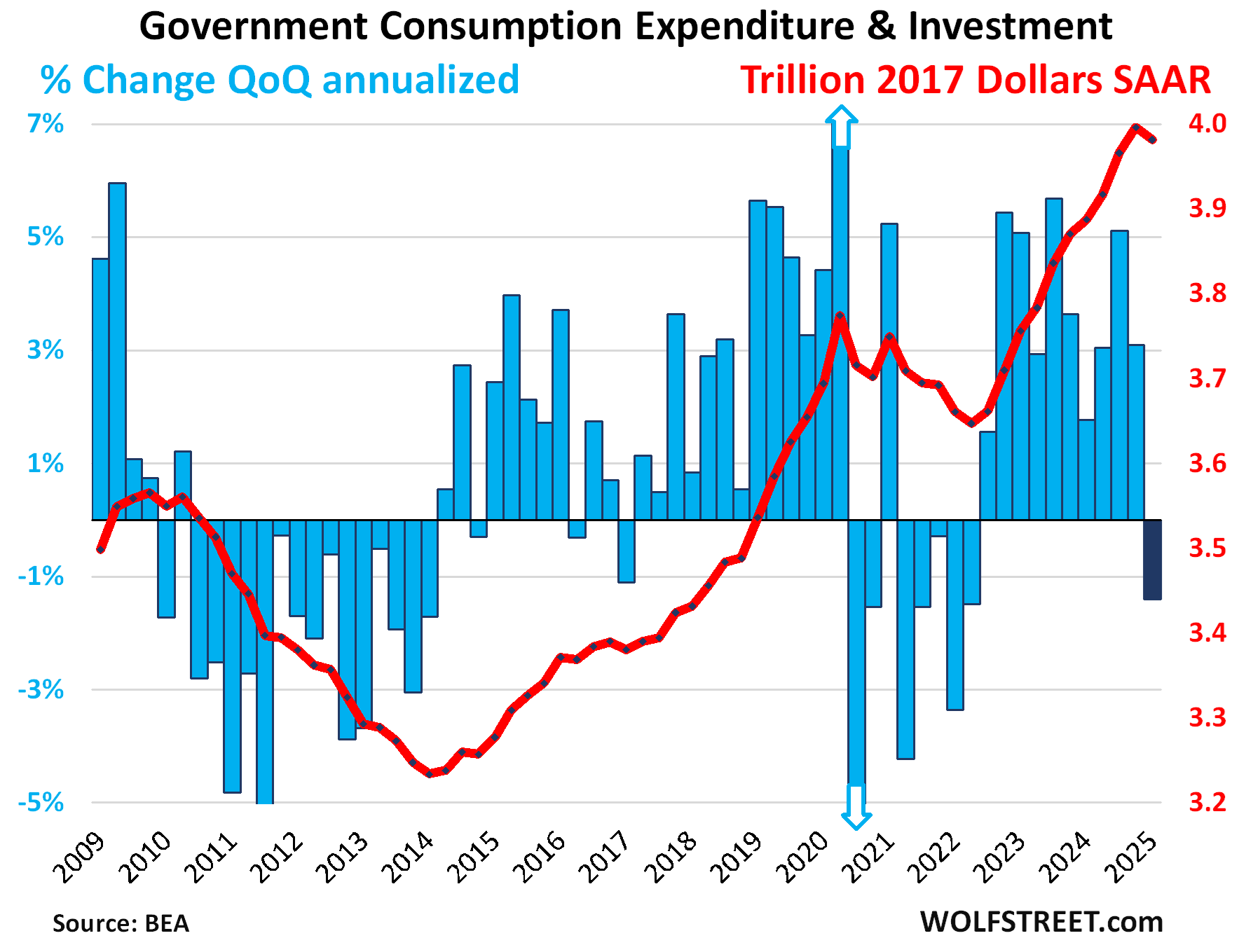

Government consumption expenditures and gross investment dipped by 1.4% annualized and adjusted for inflation, the first decline since Q2 2022.

The drop reduced overall GDP growth by 0.25 percentage points.

Combined, federal, state, and local government consumption and investment accounts for 17% of GDP.

Within total government spending, state and local governments account for 61% and the federal government for 39%.

This does not include interest payments, and it does not include transfer payments directly to consumers (the biggest part of which are Social Security payments), which are counted in GDP if and when consumers and businesses spend these funds or invest them in fixed investments.

- State and local governments: +0.8%.

- Federal government: -5.1%.

- National Defense -0.8%.

- Nondefense -1.0%.

The Debt-to-GDP ratio improved slightly to 120.8%, on 3.5% growth in current-dollar GDP (see above) and the Treasury debt that has been stuck at the debt ceiling of $36.2 trillion since the beginning of the year. As soon as the debt ceiling is lifted, the debt will spike, and the Debt-to-GDP ratio will worsen.

The Debt-to-GDP ratio is based on current-dollar GDP and on current-dollar Treasury debt, neither adjusted for inflation (the effects of inflation being both in the numerator and denominator cancel out).

The spike in 2020 occurred as GDP collapsed during the lockdown while the Treasury debt jumped on the government’s free-money-giveaway spree.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

LA Wildfires and “disruption.” Makes sense that it can’t split out, but was it positive or negative for the numbers? After the fires, the malls (and hotels) throughout Southern California were packed with people…a lot of spending to replace lost things. So did this potentially artificially drive up consumer spending numbers? How much could it move the needle?

How much could it move the needle? Not much, really. The minuscule number of people affected by the fires compared to the size of the general population mitigates against it having much of an effect. If the malls WERE packed, it was probably people seeking comfort in being with people.

It’s not only the people hit by the fires, it’s the population overall of the area who were shocked by the fires and affected in other ways by the fires, including the smoke and pollution, and the psychological impact of having part of your area burn down, and they made decisions in ways that they might have made differently otherwise. This could be not going out to dinner, not going shopping, etc.

Incidents like fires, earthquakes, hurricanes, large floods etc etc, they really have an impact.

I would say that for 5 years after a human and their family are still recovering mentally and financially from the event.

People not affected just have zero clue what it is like, until they go thru it.

There are lots of these “zones” in life that slow you down, while others will gain ground, the afflicted will lose it.

It helps to know, that this kinda annoyance might come your way. Power thru peeps

Gold imports, measured in dollars, are up roughly 30X from a year ago. Without that surge,

1st quarter gdp would be positive.

Imports of gold that investors buy are excluded from GDP calculation. I discussed this in detail here:

https://wolfstreet.com/2025/04/28/how-gold-imports-blew-up-the-atlanta-fed-gdpnow-the-old-model-is-dead-long-live-the-new-gdpnow-model-starting-apr-30/

No, they are not at all, and moreover those are excluded from GDP.

Doesn’t sound as bad as some of the more dramatic sites suggest. The US economy certainly seems strong. My son lost his job yesterday in Canada as he works in an industry which supplies special medical lasers for cancer research, which have no competition except for a company in Britain. The tariffs or a fear of recession, caused a big reduction in orders and layoffs of about 10% of the company. He’ll get a job elsewhere but I think the fears being amplified in the media are causing a reduction in spending and reduction in full-time employment. Without this fear and uncertainty, the US economy would probably be even stronger

Tariffs are just now being applied and the lack of goods coming on shores is very real. There are layoffs that are happening in the trucking industry.

I personally see price hikes on products my company purchases. Shien essentially being unaffordable in the US is huge. Shien sells more than Nike in the states.

The recession fears are still here and still very strong. We just aren’t seeing them right now. The COVID inflation wasn’t until later. It happened during but largely the year or two after.

There are many companies worried about inflation. Yes people are making more money because they are keeping up with inflation but so purchases increase accordingly. But none of the current data is predictive of a future results.

Yes, many people are afraid to spend on new products in the future. That sentiment is real and will show up in the data once the products show increases. Reduction in orders is because of the uncertainty. Trump changed tariffs from 10% to 37% on some countries but now there’s exceptions except maybe not? Nobody knows how it’s going to be implemented in the real world yet. There’s a lot of unintended consequences that are about to pop up as well. Wolf does a great job. The graphs show that for the last few months until today, the economy seems relatively healthy.

Except for the housing market that is slowly tanking yet spending keeps going up. People can’t afford houses and are spending spare cash. Especially with high prices and high rates. That’s good for now, but it’s not good for individuals who are deeply unhappy about not owning property. Total home owners have dipped. Employment is fine, for now, but we aren’t in a bull market kind of healthy.

JK N. Howling,

Shien and Temu are Chinese gangster organizations, selling way under their cost in the US, and were able to get through the de-minimis loophole to dodge any tariffs. Their purpose is to KILL US RETAILERS. No American should ever have bought anything from them.

China has done that with other US industries and has killed them. That process needs to be shut down.

Americans can buy from American retailers and will be just fine. F**k Shein and Temu! And American retailers will benefit at the expense of these Chinese gangster organizations.

Wolf, you sound like you could be really good friends with Peter Navarro & Kevin O’Leary. I saw O’Leary give an interview about the Trump tariffs & what the administration hopes they’ll do to bring China to heel. These guys, you included, really get how badly we’ve been screwed by China in all sorts of ways.

I guess I could get more exercised about Chinese behaviour if it wasn’t primarily the short sighted decisions of American businessmen and US policymakers which led to the massive offshoring which enabled it.

Play stupid games, win stupid prizes …

I think it is unfair to blame the Chinese for this.

The culpability lies with American companies, American politicians and frankly and ultimately with the American public particularly middle class and below demographics, who have been all too happy and eager buying cheap crap from China and elsewhere at a terrible long-term cost to their job/income prospects.

These are the same people who consume a terribly unhealthy diet and then find themselves obese and choking down a series of pharmaceuticals to prolong themselves…

Very sad, but also very much on them.

Yes, there’s that.

Canadaguy,

Also there have been massive cuts to federally funded research in the US, and some federal agencies are still under an effective spending freeze for new equipment, repairs & maintenance, and supplies.

‘Exports are a positive in GDP, imports are a negative in GDP. ‘

If the importer is a retailer, doesn’t it add to GDP when he resells the item?

If the importer is a retailer (Temu, for example), then the import wipes out the retail sale. I presented this simplified example the other day (excluding the effects of shipping and delivery):

If you buy a $20 product from Temu, imported and sent directly to you: GDP growth = +20 retail -$20 import = $0 added to GDP.

If you buy the $20 product from a US producer: GDP = +20 retail -$0 import = +$20 added to GDP (and more later if you consider the benefits of jobs and investments)

That’s the choice. That’s why large amounts of imports instead of domestic production are so devastating to the economy.

Wouldn’t the import be lower? Assuming the cost to import to the importer is $5 and retails for $20, wouldn’t that result in GDP growth of 20-5=$15?

If the importer is a foreign company that sells and ships direct from China to the US customer, that retail price = import price because that’s the price at which it crosses the border. That’s the example I gave with Temu. All of that consumer money just goes overseas.

If the importer is a US company, that buys in bulk in China, ships the container to the US, distributes the contents of the container to its retail locations (including ecommerce fulfillment centers), and then marks up each individual item and sells the individual item to a customer, the import amount is the amount at which the bulk items crossed the border, which will be quite a bit lower than the retail price.

If the retailer doesn’t buy from overseas, but from a US producer, and all of the components and materials are produced in the US, the entire amount of the purchase prices goes into GDP, and that money stays in the US an circulates in the US.

That’s really the choice: if you buy from Temu, no part of the sale ends up GDP and it didn’t help the economy at all; if you buy from a US retailer that imports the item, part of the purchase ends up in GDP; If you buy a US-produced product, all of it goes into GDP.

And there are additional secondary and tertiary benefits of producing in the US that either already went into GDP (for example, investment in production facilities) or will go into GDP later. Which is why production in the US is hugely beneficial… it’s not just the sale without imports, it’s the whole activity of making it, including building the facilities and production equipment and the payrolls involved that then get spent and taxed.

You are here mixing different calculation-techniques.

You either calculate GDP from the production side or from the sale-side. Both give the same endresults.

Standard valuation is from the production-side and net-positive exports are always added to GDP. Imports therefore a negative for GDP. Nevermind who owns the import firm.

Thorleif

It doesn’t matter who owns the manufacturer. But it matters where manufacturing takes place — where the product comes from.

I never discussed ownership, just location of the manufacturer. Most big companies are publicly traded and ownership is spread around the world.

BTW, the two common ways to calculate the economy are GDP (spending and investment) and GNI (income by businesses and people), and both should come up with similar results over time.

Wolf

Ok fine. I just wanted to make clear you can calculate GDP from different sides. Main thing is that GDP is the production-value created domesticly.

Gross National Income (GNI) is an expanded metric where you include income from abroad and income going out. GNI is what you can consume. The US national debt is 35 Trillion USD for which you pay interest (income for the receiver). A lot are owned by foreigners. You could say imports are always good as long as you create the income to afford it. But going into large debt to be dependant on net imports is not good for the economy in the long run. “Trump but NOT Biden seem to understand this! “

Imports destroy domestic demand for labour (this is at the core of Klein and Pettis’ “Trade Wars Are Class Wars”). If US policymakers had better understood this relationship decades ago, they wouldn’t have turned a blind eye to the short sighted decisions of American businessmen to offshore so much production (provided of course that the former aren’t entirely in the pocket of the latter 🙄) OR they would have exercised a robust industrial policy to sustain manufacturing in emerging sectors while simultaneously providing employment opportunities to those whose labor had been rendered obsolete by the imports.

Of course they did neither, so having sown the wind, they now reap the whirlwind …

Wolf, I am confused by something, I thought I remember you saying the government spending was not calculated into GDP, but it would appear that government spending on actual things does?

My love, Would you please please RTGDFA?!

It’s the same as I’ve ALWAYS said.

That last debt-to-GDP chart really tells the tale of post-2000 macro economy dysfunction.

Reagan rode to victory in 1980 decrying Fed deficit (ultimately debt) financing that was 25%(!!!) of today’s.

Timeline of US astronomical debt spikes…

1) The Fed insisting on phoney-baloney post-2000 ZIRP (and fused-at-the-spine Home Bubble 1.0 overvaluations) leads to Housing Implosion 1.0…

2) Which the Fed insists upon “saving” via epic QE money prints post 2009,

3) Leading to Home Overvaluation Bubble 2.0 (implosion pending, oh-so-pending…),

4) Then $10 billion per year CDC (as in “Disease Control”) manages to make rather massive hash of Covid,

5) “Justifying” second leg of massive debt spike (“Never let a hash go to waste…”)

And we still have the massive entitlements crisis (frequently cited in 19 freaking 80…) to deal with.

I thought Reagan got elected for his breakthrough movie “Bedtime for Bonzo”

Reagan was elected first and foremost to address the “clear and present danger” of a nuclear first strike by the Soviets. He apparently succeeded.

When Reagan took office the total debt of the US was one trillion dollars. Then came the Reagan tax cuts, aka Reaganomics, which would of course pay for themselves ( see Laughter, (Laffer) Curve. 4 years later the debt accumulated over 2 centuries had doubled. This began the political era of ‘deficits don’t matter’

Reagan said : “the deficit is big enough to take care of itself.”

Enjoy it. Just make shure you have 2-3 times as many assets as cash. Governments never stop spending, but asset application is not all profit.

Ironic, then, that Reagan and his successor Bush oversaw more than one-third of the increase in debt since 1980!

The point wasn’t any particular defense of Reagan (kinda amazing some readers saw it this way), but rather the massive, relentless, frankly terrifying (and nation destroying) surge in federal debt-to-(likely inflated)-GDP.

If there was a political point, it was that a large segment of the population did already see the dangers of national debt in 19-friggin-80 (enough for Reagan to exploit if nothing else) and yet the annual deficit horror show proceeded apace for the next 45 years.

Essentially every single year. Year after year. For 45 years.

*That* is why a large fraction of the US population thinks of DC as a life threatening science fiction blob.

It would be very interesting to compare 1979 (still post 70’s era inflation!!) Federal spending levels for the largest 2 or 3 dozen programs versus today.

The aggregate total is inarguably a horror show – but pointing out the primary drivers of the horror (which in all likelihood are “entitlements” – SS and Medi-care/Aid – and the military) would be very useful for people who still care whether America lives or dies (obviously not those in charge of the last 45 years).

In 1979, Federal spending as a percentage of GDP was 20%. Today it is 23%. Larger, but not as extreme as you think. Same for total government spending.

Entitlements have increased substantially, almost doubling from 8% to 14%. But this is largely balanced out by the fact that all other spending has decreased by a lot, from 9% to 6%.

Even more extreme when you subtract out defense spending: In 1979 defense spending was 5% of GDP, and now it’s 3%. So non-defense non-entitlement spending was 4% of GDP in 1979 and 3% of GDP today.

Which is why DOGE has been a joke from day 1. The only way to cut today’s spending to 1979 levels is to either a) completely eliminate all non-defense non-entitlement spending (completely zero it out, no VA, no medical research, no food stamps, no FBI, no Homeland Security, no federal grants to local schools, no Pell Grants, no TSA), or b) deliver a 10-15% across the board cut to everything, including defense AND Social Security AND Medicare.

When you give this choice to people, it’s interesting to see what they choose.

It seems that the markets have read Wolf’s article because they are shaking off earlier losses.

I don’t see how this GDP report isn’t a good thing, but the headlines of course lead with the worst news of it.

No country should be relying on Government spending aka taxes to boost jobs and GDP as Biden was doing. It is devasting long term and then there is a hangover when it runs out. Sure, some gov’t spending is necessary but it should not be a driving force.

Congress played a large part in using fiscal spending to cushion GDP. Both Republicans and Democrats.

More consumer spending, more investment, less government. What’s not to love?

If the tariffs stay as they are, we’ll be in recession because of government layoffs, government contractor layoffs and cancelled contracts, higher prices and car sales will be down. Tariffs on aluminum and steel will raise prices of everything with those metal parts.

You should look into what the word deep means.

Even two quarters like this wouldn’t be a deep recession

Another great article to ground us solidly onto the earth.

The economy has become big media business meaning that talking/reporting on it has become part of the entertainment industry. The needs of entertainment and understanding are in conflict.

Entertainment needs drama and fast pacing.

Unfortunately the actual economy operates over many quarters and many months.

no, the media has become a dishonest arm of wall street and the democratic party.

“Equipment: +22.5%, the highest growth rate since Q3 2020, and the second highest since Q3 2011, as companies invested to ramp up production in the US, which is what tariffs encourage them to do.”

Investing in US production to avoid tariffs of products, or purchasing equipment earlier to avoid paying tariffs in THAT equipment? I.e. front-running, which you point out for the import piece. My bet is on the latter, as decisions to change manufacturing locations and supply chains were not made early enough to change Q1 numbers.

Increased imports due to front-running, while a negative on GDP, are matched with increased spending (positive on GDP) and come out in the wash. Either consumers front-ran, which increases spending, or businesses did – increasing investment, or inventory (both are positive to GDP).

The only issue here is that the initial reads on GDP tend to be bad at counting inventory (slower reporting). Expect the later revisions to adjust inventory counts, possibly improving GDP numbers a little.

Imports are going drop in future quarters (the other side of frontrunning), boosting GDP. Inventory adjustment in future quarters is going to reduce GPD by some.

The issues of imports and inventories are UNRELATED TO DEMAND IN THE US ECONOMY.

That’s why I gave you in the article above this, quoted verbatim from my article above because people don’t seem to have read the article:

The health of the private US economy: Growth of “final sales to private domestic purchasers” accelerated to +3.0%.

This metric is part of the GDP report, released today by the BEA, and tracks US private domestic demand from consumers and businesses, including fixed investments by businesses. It is GDP less exports, less imports, less government consumption expenditures, less government gross investment, less change in private inventories. It covers about 87% of GDP and presents the core of the private US economy.

Powell also mentions it from time to time as a purer indicator of private domestic demand from consumers and businesses – which is what monetary policy is trying to influence (not trade and government spending).

Adjusted for inflation, final sales to private domestic purchasers jumped by an annual rate of 3.0% in Q1, to $20.7 trillion, up from 2.9% Q4, attesting to the strength of private domestic demand and investments by consumers and businesses.

And similarly, the front-running purchases, inventory-building and investing will plunge, lowering GDP

A ton of confusion here and elsewhere about GDP seems to miss what the P stands for. It’s meant to measure what we produce. But because it’s much harder to count every thing we produce, we use accounting identities to get that answer from other numbers that are easier to collect (exports, imports, change in inventories, consumption, and government spending).

Saying GDP was reduced because imports were high is mistaking an accounting identity for a cause. Technically, imports do not affect GDP at all, as Wolf has explained. What affects GDP is how much stuff is made here (both goods and services, so not just manufacturing). The only question with regards to tariffs are if they will increase production because people can’t just buy stuff from overseas, or if they will reduce production because people will be poorer or because they can’t access the parts they need to make stuff or because the stuff we do make can’t be sold overseas anymore.

So what actually happened this quarter is that people and companies bought more stuff, some of which they used (consumption), and some of which companies stored as inventory (change in inventories). They also built more stuff (fixed investment). But all of that increase was stuff they bought from other countries (imports), meaning that we didn’t make it, which means it didn’t go into GDP.

This can be interpreted in two ways: 1. people need/want to buy more stuff (i.e. high demand for goods and services), which is good for an economy or 2. people are abnormally buying more stuff because they know they won’t be able to buy/afford that stuff in the near future and this will disappear in future quarters (i.e. “demand pull forward”), which doesn’t actually indicate a strong economy, but indicates that future demand will actually be less.

Is this like a “core GDP” a la “core PCE” type figure going forward now? Hopefully the fed can focus on this one and delay rate cuts out further.

FYI, BES web site: https://www.bea.gov/index.php/news/2025/gross-domestic-product-1st-quarter-2025-advance-estimate

Very informative, like our host.

Really great analysis! Wolf you are the one place on the web that reports the data with any of your conclusions or opinions squarely based on that data. You make it clear even to non-financial experts like me.

And the difference can be like night and day between the data and what is reported in the rest of the media.

The one financial site that’s a must have.

You added to your response after I added mine… Note that I did read your article.

“The issues of imports and inventories are UNRELATED TO DEMAND IN THE US ECONOMY.”

Of course, but all 3 are part of GDP, which is what this article is ostensibly about.

GDP is a measure of domestic production, which is calculated by [domestic consumption] + [domestic storage] + [export] – [import].

Domestic production (GDP) should not plunge from front-running – it goes in both the plus and minus columns – however the (mis)-counting of those columns isn’t always equal.

The final sales to domestic purchasers will also contain front-running, so the fact that it did not jump up 5% is a bit of a red flag for demand.

An analogy:

Let’s say we want to know how many cows are born on our farm. But we don’t really pay enough attention to when they’re born to find out directly. But we do record how many we have, how many we buy and how many we sell. So we set up a formula. The number of cows that were born this year are the total number of cows this year, minus the ones we had last year, minus the ones we bought from other farms plus the ones we sold to other farms.

So if we buy twice as many cows from our neighbors, did any more cows get born on our farm?

This is bad Mmmmkay. Anyone? anyone? Buelluer Buelluer?

Anyone?

This GDP number in aggregate is fairly useless with so many consumers frontrunning and the consequent increase in imports. Maybe it is time for the government to post a “Core GDP”, which Wolf has clearly discussed above, and which the Fed apparently prefers. I’m not holding my breath about this happening any time soon, if ever.

I was amused by the term “Net Exports”. I would prefer the terms “Exports minus Imports” or the more conventional “Balance of Trade”. These terms are longer, but generally understandable.

serious question. how can microsoft, google, meta, and amazon have 20-30% increases in profits, year after year, decade after decade, when the economy is growing 2-3%?

i’m finding it hard to wrap my head around how this happens.

If you were a publisher relying on internet advertising, like me, you’d know exactly why Google’s profits soared every year while publishers went out of business one after the other because their ad revenues declined year after year. Google has a monopoly on the internet ad infrastructure and on many parts around it, which it created by buying out other companies, and by producing its own services and products, and it dominates everything with its browser, and now uses no-click search results where AI steals the publisher’s content without linking them.

Google has been sued over its monopolistic behavior by the government, joined by big publishers, including News Corp (WSJ), and lost both lawsuits. It will appeal. But this might ultimately lead to the breakup of Alphabet.

Microsoft has done similar things. Big Tech is all about creating monopolies. This is an insidious force in the economy that blocks growth, and the government slept through it for 20 years, and thereby encouraged it, until Biden started cracking down, and Trump continues to crack down.

thanks, this is a helpful explanation. but given that the stock market is held up by the mag7 wouldn’t a breakup of the monopolies cause a major stock decline? we’ve seen now how the media presents any decline in the bloated stock market as a catastrophe, so are they going to attack anyone, trump or otherwise, who is working to break up these anti-competitive companies?

The collapse of anti monopoly enforcement in the US is more like a 40+ year project (beginning with the execrable Bork and his droogs) but yes, the specific tech element of that abject failure as exemplified by Alphabet, Meta and Amazon are as Wolf describes it a 21st century project.

could we all keep this on the d.l. for just a few more weeks.

Tryin to scoop up as many equities at a panicked discount as possible.

what equities are at a panicked discount at this point, pray tell?

“including a 22.5% increase in investment in equipment, as companies have begun ramping up investing in production in the US to avoid the tariffs.”

Is there any data to support this statement? For example, are companies already starting to announce that they forecast higher capital needs to build factories and to buy equipment in response to the tariffs, over the next N years (N>>1)? And wouldn’t shareholders react negatively, and prefer to buy cheap stuff, import it, and re-sell it (or integrate it) here, versus having to sink money into building out capacity (when it already exists, just not on American soil)?

How does the math work out on this? Suppose a Chinese-made widget costs $1, and there are 100,000 units sold a year. Due to tariffs, the price goes to $2, and nobody wants one from China anymore. So then I decide to buy a widget machine for $100K, install it in my garage, and start making widgets. The profit is 50 cents per unit, and so I make $50K per year, and in 2 years I start turning a profit. But how do I have any confidence that the tariffs will stay in place? How do I do the math to determine if my little business makes sense, if I have no idea if the tariff plan will stick? I could be stuck with a $100K boat anchor in my garage.

The announcements of huge investments of construction of new production facilities in the US, or in expansion of existing production facilities in the US, by US and foreign companies, from Apple (server factory in Houston) on down, have been all over the place all year. This process started two years ago, but it has picked up momentum. There has been an “eyepopping” factory construction boom since 2022 that continues:

https://wolfstreet.com/2025/02/24/apple-announces-server-manufacturing-plant-in-houston-adding-weight-to-eyepopping-us-factory-construction-boom/

Wolf,

I’m curious if you have any input on how much the AI bubble has fueled the factory construction boom. I’m sure you’re aware this bubble began popping this year. I wonder how much this will effect construction spending.

My company has been supplying equipment to one of those AI-focused manufacturing facilities. They went from writing us a blank check throughout all of 2024 to pausing all new spending as soon as Microsoft announced their pullback.

The AI bubble has fueled a data-center construction boom, not the factory construction boom. The factory construction boom is related to auto makers (EVs), battery makers, electrical equipment makers, makers of semiconductors of all kinds (but none of Nvidia’s chips… its contractors will eventually start making some of them in the US at some of the new chip plants, but that was just announced so it will be a while before it shows up in the data).

I have trouble tracking the data-center construction boom because construction spending on data centers is lumped together with office buildings, and construction of office buildings has collapsed, while data-center construction has soared, and the overall category kind of looks normal.

Wolf, you said:

“A massive spike in imports, by far the worst ever, on tariff-frontrunning subtracted 5.0 percentage points from GDP growth (adjusted for inflation), turning it negative. “

An increase of 41% in imports was reported for the quarter and presumably is not anticipated to continue. So does this mean that if the one time increase were ignored then the actual gdp (which was negative 0.3) would be roughly 1.7%?

I am assuming this was a one off event and subtracted about 2% ie 40 percent of 5% and also that net exports are typically a 3% drag on GDP.

You could look at it that way. But then you also have to include a portion of the inventory adjustment, which goes the opposite way.

It’s just easier to look at “Final sales to private domestic purchasers” which excludes all trade, the inventory adjustment, and government spending. It’s the 4th chart down. It grew by 3.0%

1. United States of America

Final Consumption Expenditure in 2022: $21 trillion

2. The People’s Republic of China

Final Consumption Expenditure in 2022: $9.5 trillion

Regardless of what China, Canada, and the others countries around the world say about Trump Tariff’s, its is clear that they need us buying their products. The media portrays doom and gloom all day/everyday since Jan 20th 2025 inauguration. Trump is winning the shock and awe campaign. Democrats forgot what it means to be American, as did many of the behemoths who run Wall Street. I guess if you built your business and asset model based off of cheap labor inside a communist totalitarian government there is a need to worry. Just look at what good old NAFTA did to Detroit and the Midwest heartland. Just think their are those in Congress who thinks we should lay down and roll over to be a part of some globalist, socialist, communist regime, after building the Greatest Country in World for Capitalism.

Including Canada as you have done here demonstrates typical American ignorance of the composition of trade between our two countries. Canada’s “trade surplus” against the US is made up almost entirely of heavy oil (think Alberta tar sands here) which you would otherwise have to import from Venezuela — the US is a net fossil fuel exporter to the rest of the world but that’s because of natgas (and possibly some light, sweet crude) and fossil fuels are NOT entirely fungible, as petroleum engineers can confirm.

In just about EVERY category of goods (other than potash, aluminum and softwood lumber) Canadians have a trade DEFICIT with the US.

As with all aggregates, composition matters!

Nonsense. The US is a huge exporter to Canada of ENERGY products too. It’s a bilateral trade. The US exports petroleum, petroleum products, natural gas, and electricity to Canada. In part of 2023, the US exported more electricity to Canada than it imported. It’s a Canadian propaganda coup to take the total trade deficit the US has with Canada and subtract out energy imports from Canada to the US and then lie that the rest is manufactured goods that the US exports to Canada. It’s a propaganda lie spread in Canada for political purposes. You need to take the total trade deficit, subtract out Canadian energy exports to the US, and US energy exports to Canada, then subtract out the lumber and food commodities that cross the border in the BOTH directions, and then the rest is manufactured goods, which will show you a very different picture.

And don’t talk to me about services exports by the US to Canada. Much of that is Canadian tourists spending on food, airfares, lodging in the US. That’s a very low level of economic activity, unlike manufacturing.

I will see if I can find such an analysis. I certainly can’t claim to be immune to politically motivated propaganda here in Canada — we just had an election, so we’re soaking in it!

https://www.eia.gov/todayinenergy/detail.php?id=63684. Hi Wolf. This data doesn’t support your understanding that the U.S. is a net exporter of energy to Canada. Some border States rely heavily on Canadian energy because of the infrastructure in place. Thanks

Freedomnowandhow

I never said “net exporter to Canada.” Don’t make up bullshit and try to stuff into my mouth. That’s one of the seven mortal sins here.

I said “huge exporter.”

The text of the article you linked confirms what I said in my comment about electricity exports from the US to Canada. Too bad you read neither my comment nor the article you linked, another one of the seven deadly sins here.

This is what the article you linked said:

“Monthly average exports from the United States to Canada in 2023 increased 70% on a year-over-year basis to 1,809 gigawatthours (GWh), while monthly average imports from Canada to the United States decreased by 36% to 3,315 GWh. …. The decline in imports from Canada was large enough that by September 2023 the United States switched to become a net electricity exporter to Canada, which continued for five of the next nine months, “

Wolf,

I appreciate your analysis. It’s a nice reprieve from all the doomer bait. I’m personally pivoting from equities because tariffs will for sure hit company profit margins, but profit margins are not the economy.

I work manufacturing in Michigan, which some have called ground zero. We’re forging ahead with caution and trying to stay optimistic. Yes, inputs have gotten more expensive, but most Americans – especially us here in the midwest who’ve rejected becoming a services economy – can afford it.

“because tariffs will for sure hit company profit margins, but profit margins are not the economy.”

Yes, companies will be fine, but profit margins won’t be quite as fat. See GM today. It announced today that tariffs would cost it $4-5 billion, and it lowered its earnings forecast for that reason. But it’s still profitable. That’s how tariffs work. Maybe GM can pass on some of it someday, but right now, no way, it has been throwing lots of incentives on the market to sell what it makes. Any price increases would kill its sales.

GM imports the Buick Envision from China, from its joint-venture with SAIC. It’s GM’s own idiotic decision to import a China-made vehicle. After GM got bailed out by taxpayers, it offshored much of its component industry to China, and it offshored a lot of technology and design work to China, while it shed dozens of facilities in the US. So now there is finally a price to pay.

It _all_ looks like front running to me. Question is will they get choked out or not? People still believe he’ll cave.

If I were a betting man I’d say abject capitulation and mission accomplished banners (with a heapin’ helpin’ of finger pointing if things go really wrong). You know the sort of cold hard integrity we’ve learned to expect.

“Government consumption expenditures and gross investment dipped by 1.4% annualized“

Elon told me it would be 1.4% MoM… where have the Trillions gone?

The sky fell. We used (Re)generative Ai to put it back together again, better than it was! Time to restore the 30-50+ PEs!

It kind of looks like there might have been a large amount of imported capital equipment. Is there a way to use the BEA, etc. data to determine how much of the import surge was CapEx? (As a retired economist/quant nerd, I love Wolf!)

Wolf, the non-residential fixed investment number is the incredible one: +9.8%.

Anecdotal: Visited a prospective client in the custom metal fabricating business this week. Roughly $40mm/year operation that is looking to expand from 2 to 3 shifts, pending the ability to hire staff.

Order books are full, looking to expand current production facilities.

I suspect AI will help domestic manufacturers more quickly locate new sources of production. This isn’t going to happen overnight, but I suspect in 3-5 years we could see a massive net improvement in our domestic manufacturing base if this trend continues.

Good to hear. I think you’re right in terms of your 3-5 year ballpark

Using the Expenditure approach to calculating GDP the formula is: GDP=C+I+G+(X−M)

C=consumption, I=investment, G=Gov spending, X=exports, M=imports.

Front-running the tariffs would increase M by some amount (thus decreasing GDP) But is would also increase I by the same amount as it adds to someones inventory. Front-running the tariffs should net out to 0 in the GDP formula.

So the thing I don’t understand is how imports would be able to decrease GDP. How am I looking at this wrong?

You’re not thinking this through at all.

If the importer is a retailer (Temu, for example), then the import wipes out the retail sale and the amount of consumer spending. To simplify let’s exclude the effects of shipping and delivery:

If you buy a $20 product from Temu, imported and sent directly to you: GDP growth = +20 consumer spending -$20 imports = $0 added to GDP.

If you buy the $20 product from a US producer: GDP = +20 consumer spending -$0 imports = +$20 added to GDP (and more later if you consider the benefits of jobs and investments to make that produce in the US)

That’s the choice. That’s why large amounts of imports instead of domestic production are so devastating to the economy and to GDP.

Then there is the money-flow aspect, which doesn’t show up in GDP but shows up in other data. A Temu customer just sends their S20 to China with no benefit to the US economy, but that $20 has left the US economy and is now benefitting the Chinese economy. That’s the other aspect of imports exceeding exports: the twin deficits – the trade deficit and the government deficit. They’re linked via money flows. The US could not have funded that kind of 40-year trade deficit (cash going out to the rest of the world) without indebting the US to the rest of the world, including with the US debt. That’s a burden that now lies on the US, and that no one knows what to do with.