Up-revisions pushed the 12-month core PCE price index for February to +3.0%, and the 6-month index to +3.4%, worst since July 2023. But March was benign?

By Wolf Richter for WOLF STREET.

The inflation measure released today for March – the PCE price index favored by the Fed as yardstick for its inflation target – has a salient feature that it had many times before: Sharp up-revisions of the prior month’s data, this time for February, triggered by hot up-revisions in core services inflation.

The February month-to-month data were revised sharply higher today, driven by core services which dominates the overall index.

- Overall PCE: to +0.44% (5.5% annualized), from originally +0.33% (+4.0% annualized)

- Core PCE: to 0.50% (+6.1% annualized), from originally +0.37% (+4.5% annualized)

- Core services: to +0.52% (+6.5% annualized), from originally +0.35% (+4.3% annualized).

The February year-over-year readings were also revised higher, which caused the core PCE price index for February to hit +3.0%, highest in a year:

- Overall PCE: to +2.7%, originally +2.5%.

- Core PCE: to +3.0%, originally +2.8%.

- Core services: to +3.8%, originally +3.6%.

In March, the price changes were from the up-revised February levels.

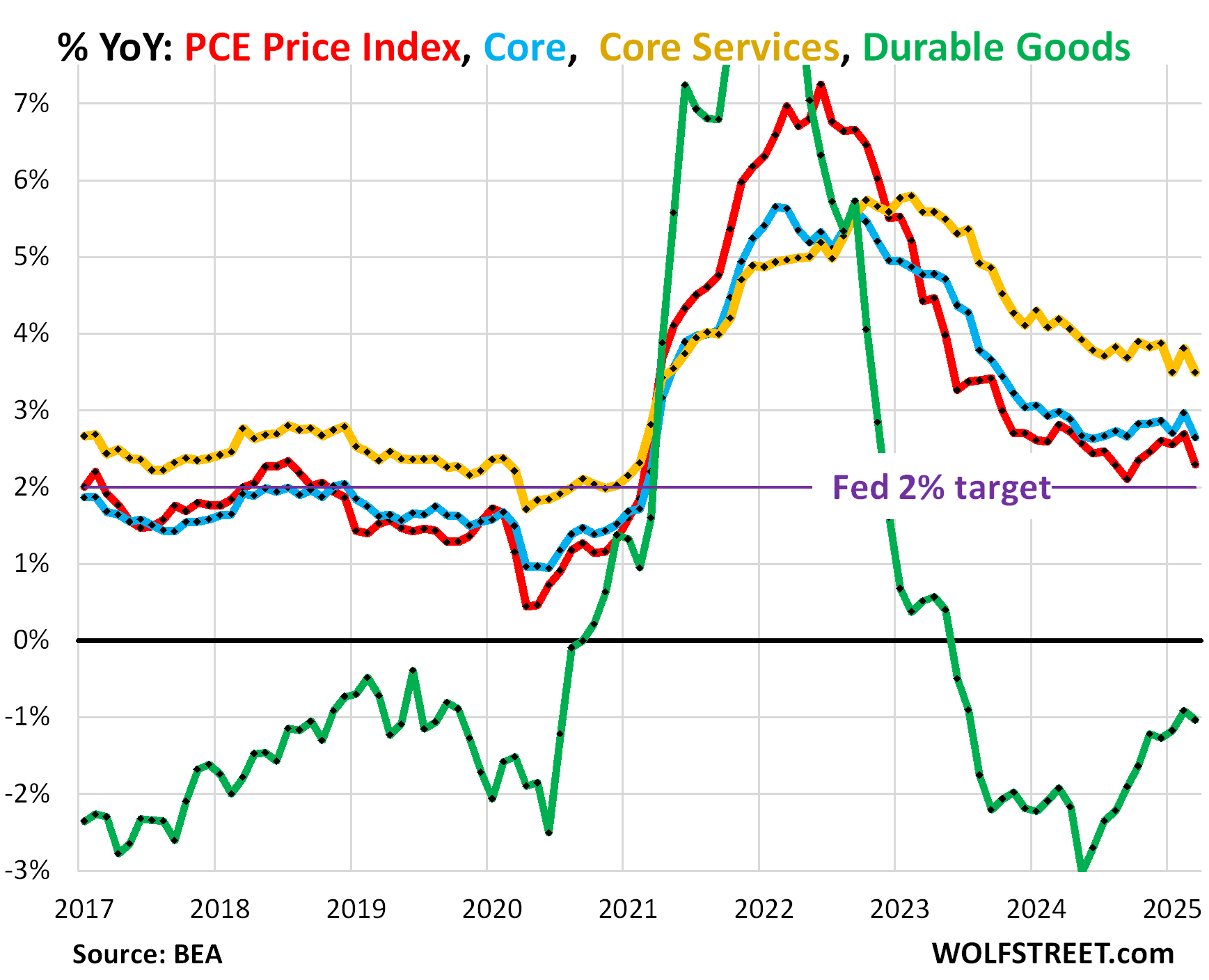

On a year-over-year basis in March:

- Overall PCE price index (red): +2.3%, driven down in part by plunging energy costs. The Fed’s target is 2.0%.

- Core PCE price index (blue): +2.6%

- Core Services PCE price index (gold): +3.5%.

- Durable goods price index (green): -1.0%.

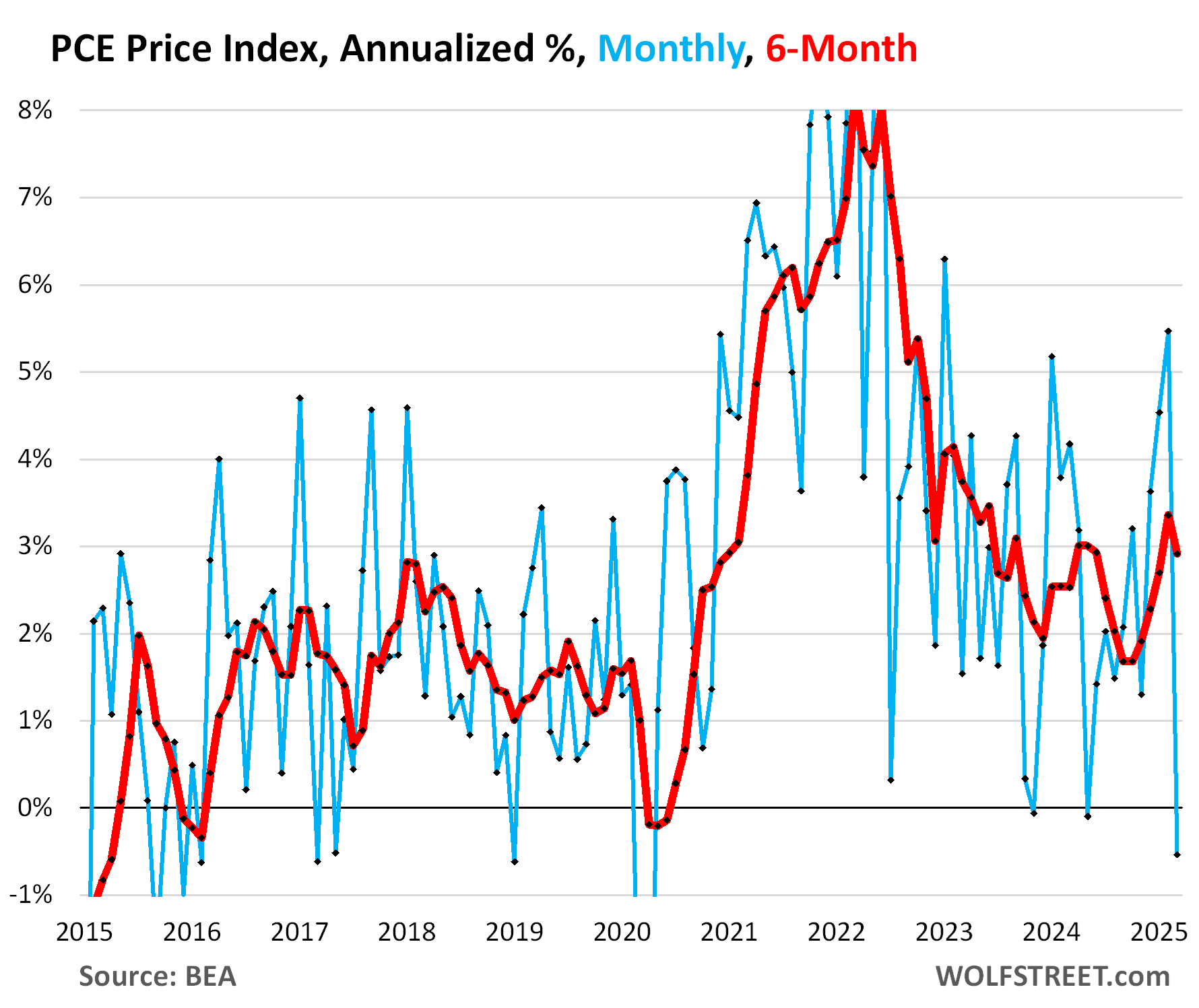

The overall PCE price index edged down by 0.04% (-0.5% annualized) in March, from the up-revised red-hot level in February (+5.5% annualized, the worst since January 2023). The March dip was driven by a 2.7% month-to-month plunge (-28% annualized) in the energy price index.

The 6-month PCE price index decelerated to +2.9%, from February’s up-revised 3.4%, which had been the worst increase since June 2023.

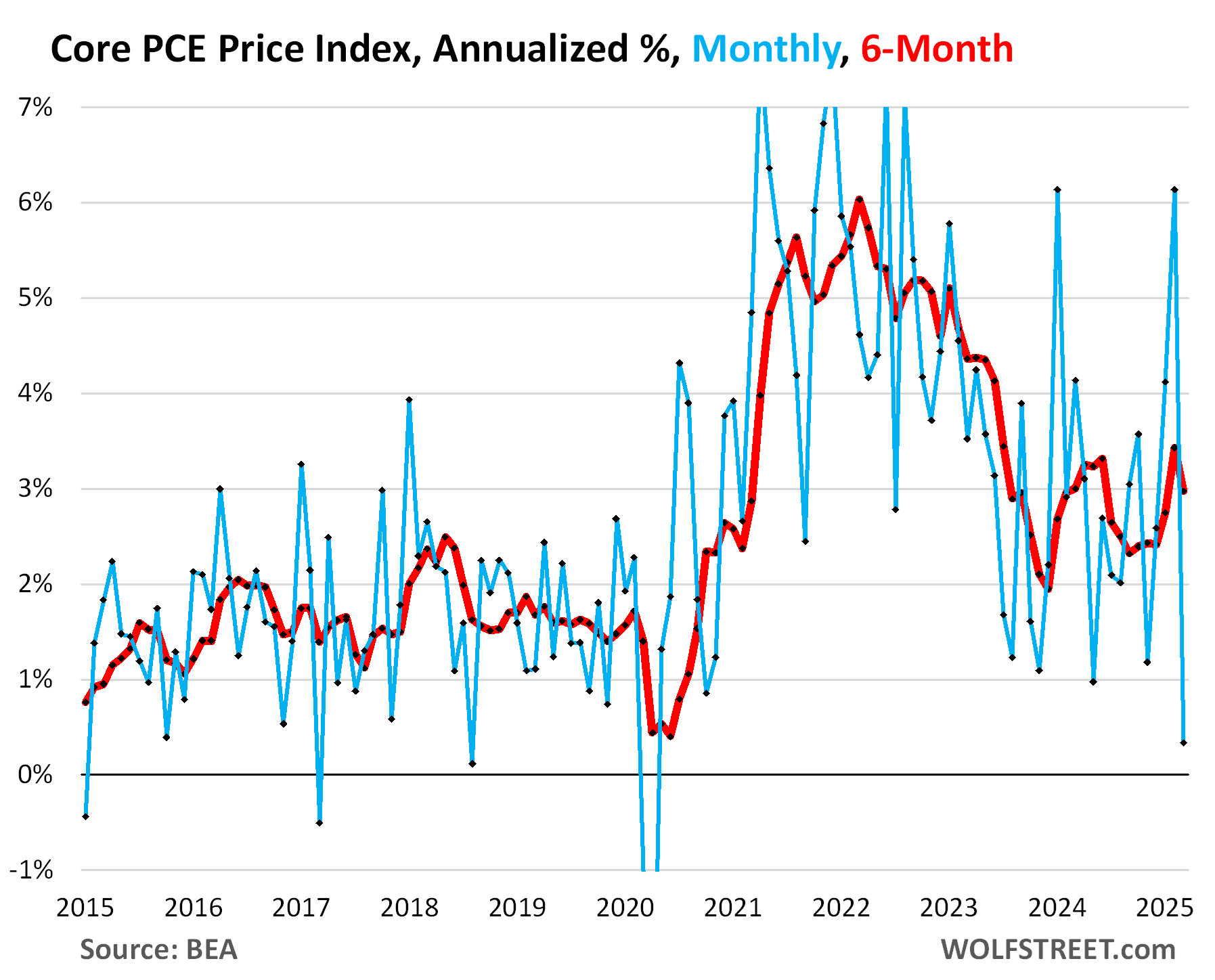

The core PCE price index, which excludes food and energy items, decelerated in March to +0.03% (+0.3% annualized), from the heavily up-revised level in February (+6.1% annualized).

The 6-month core PCE price index (red) decelerated to +3.0% annualized. But February was revised up to 3.4%, the biggest increase since July 2023, from originally 3.1%, which had been the biggest since June 2024. Inflation is in the revisions?

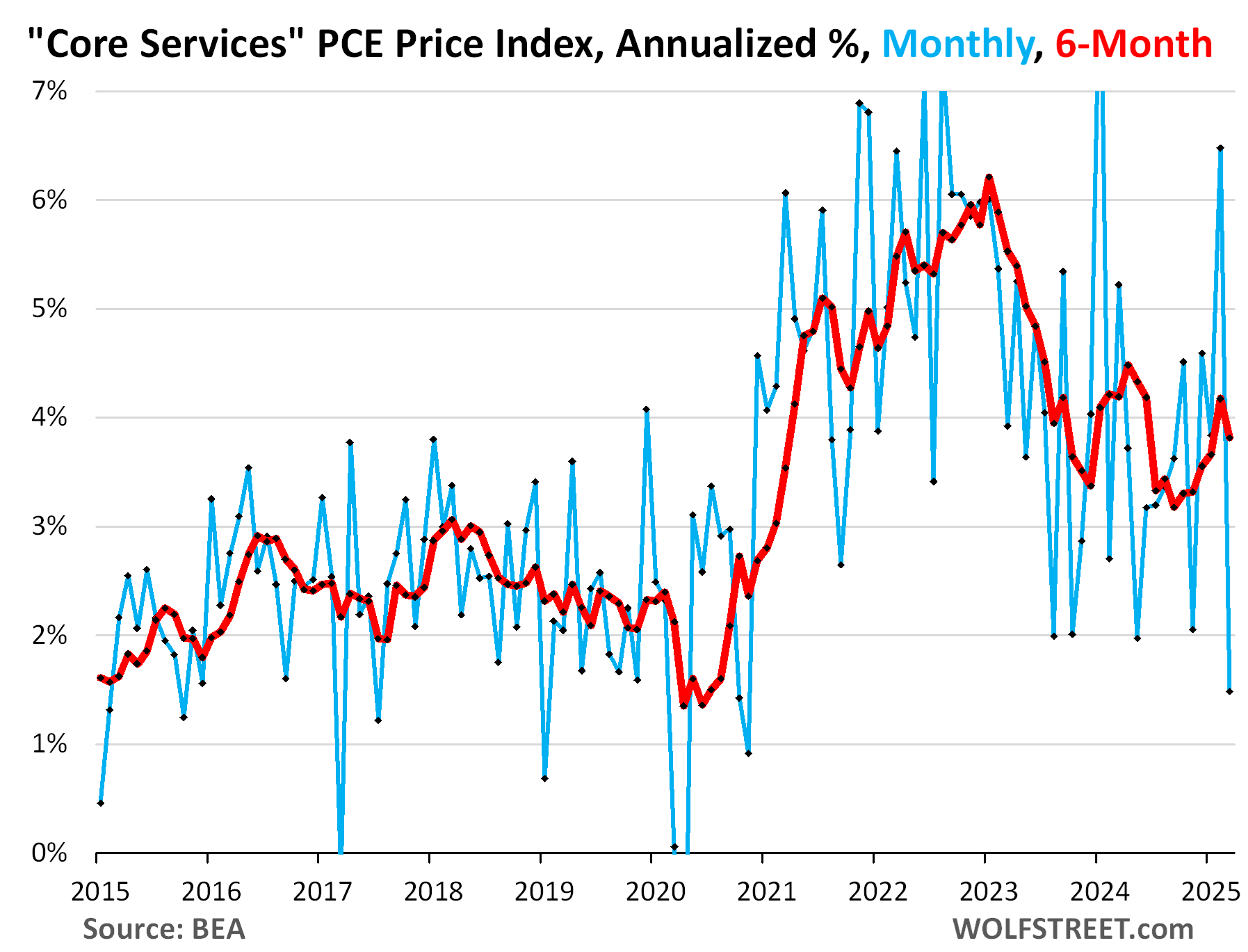

The core services PCE Price Index, which excludes energy services, decelerated in March to +0.12% (+1.5% annualized) from the red-hot up-revised February.

The 6-month core services PCE price index decelerated to +3.8% from the up-revised 4.2% in February.

Inflation is in the revisions? The originally reported 6-month core services PCE for February had accelerated to +3.7% annualized, and it was up-revised today to a +4.2%. And so today’s readings for March, at +3.8%, would be an acceleration from the originally reported February reading (+3.7%).

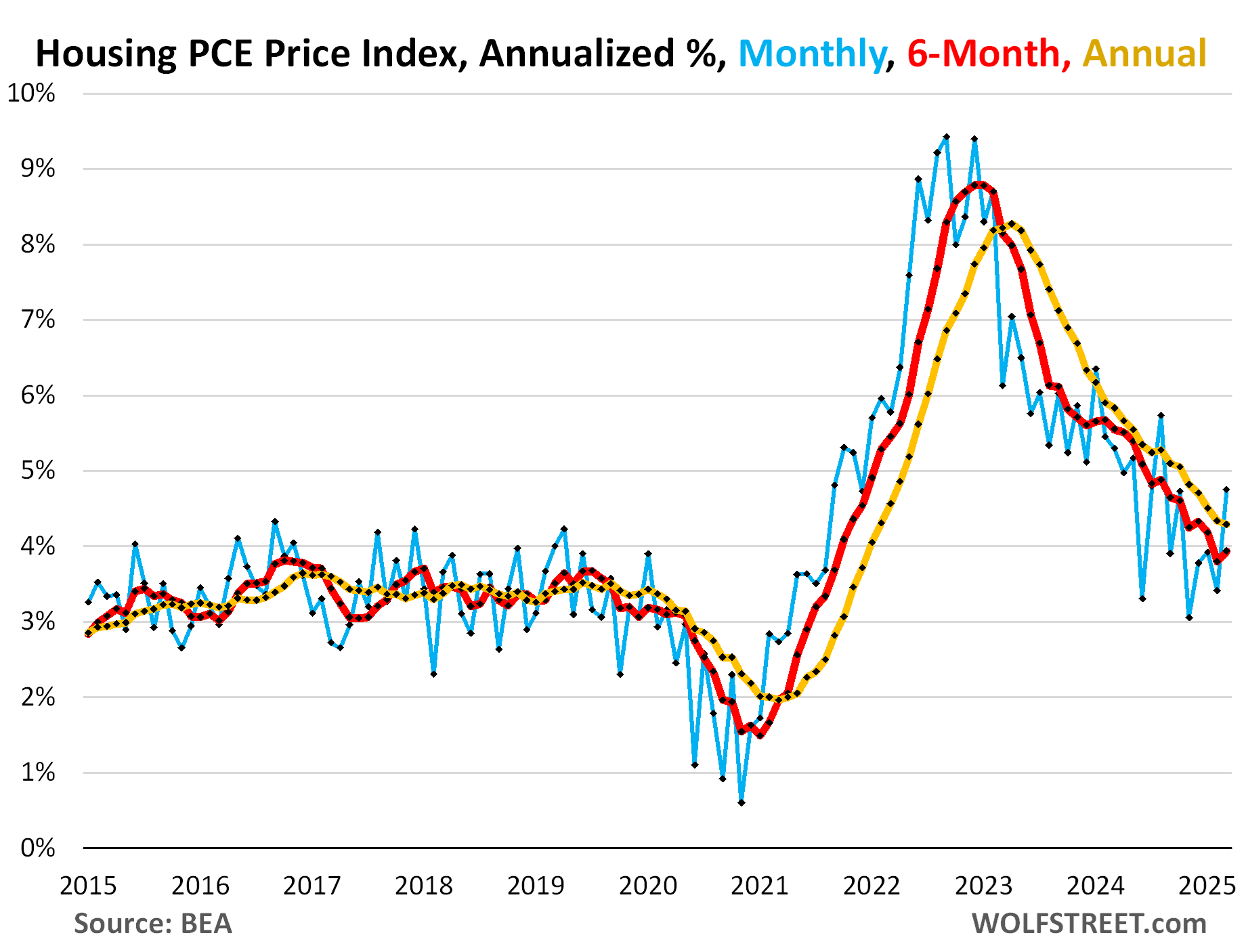

Housing inflation accelerated. The PCE price index for housing – one of the main components of core services – is based various rent factors. It surged by 0.39% (4.8% annualized), the biggest month-to-month increase since August 2024, having accelerated in a zig-zag manner since the low point in November last year (blue in the chart below).

The six-month index has now accelerated to 3.9% annualized (red in the chart below).

The year-over-year index has slowed its deceleration to nearly unchanged at +4.29%, from February’s 4.33% (yellow):

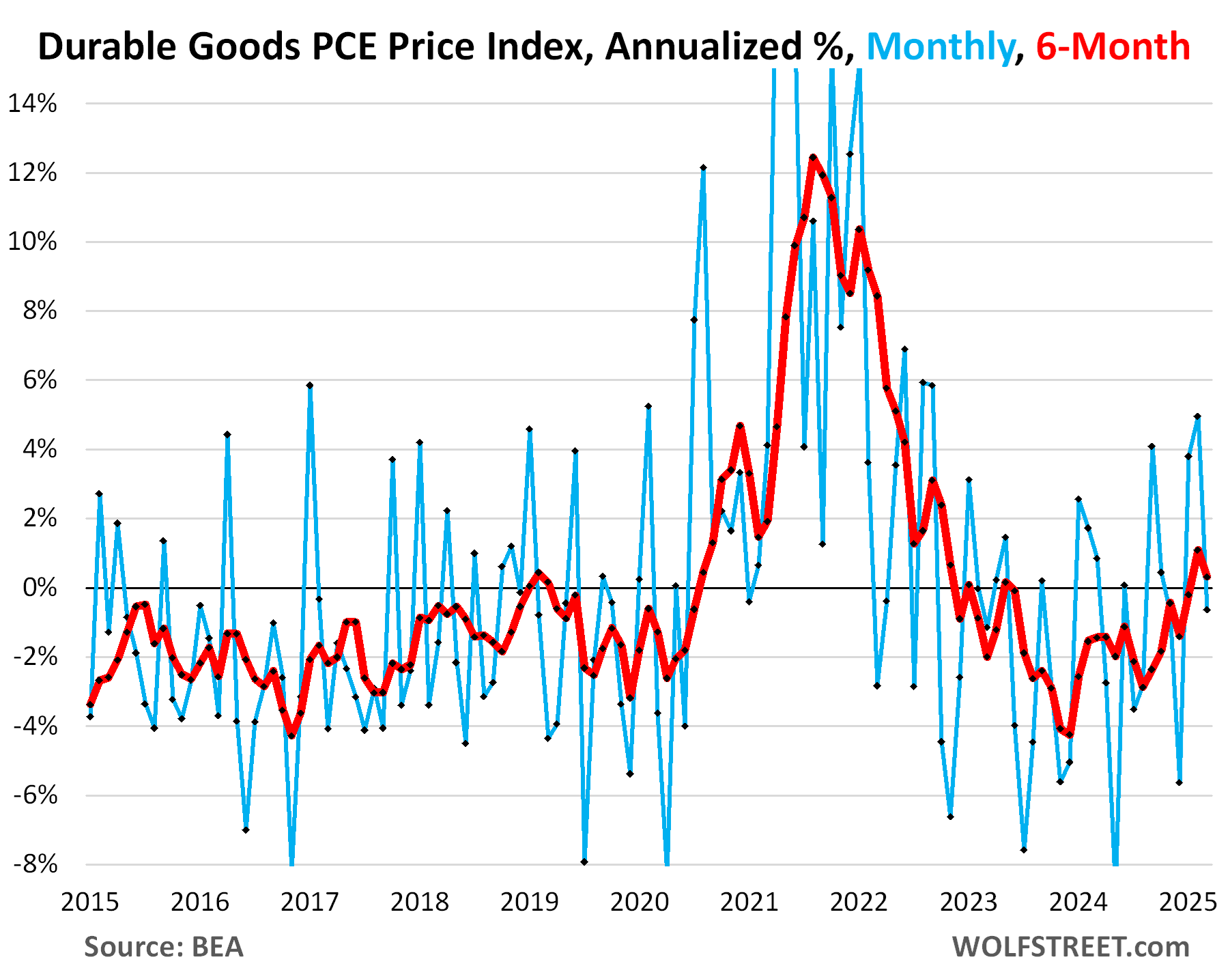

Durable goods prices declined in March from February by 0.05% (-1.0% annualized). They’ve been zigzagging up from the deeply negative hole since early 2024, and the negative reading in March, after two positive readings, might just have been another zag.

The six-month PCE Price index for durable goods shows the trend: It started heading higher in September last year, from deep deflation (negative), and became less negative as it went, was barely negative by January, turned positive in February, and remained positive in March at +0.31% annualized. Durable goods have been in deflation for many years before the pandemic due to manufacturing efficiencies, offshoring production to cheap countries, and other factors.

Durable goods include motor vehicles, appliances, consumer electronics, furniture, etc. Many of these products or their components and materials are produced overseas and are subjected to new tariffs. But that hasn’t left any traces on retail prices yet. And it didn’t leave a lot of traces last time tariffs were imposed in late 2018, as you can see in the chart. It’s the inflation coming out of the pandemic that had a huge impact on prices of durable goods.

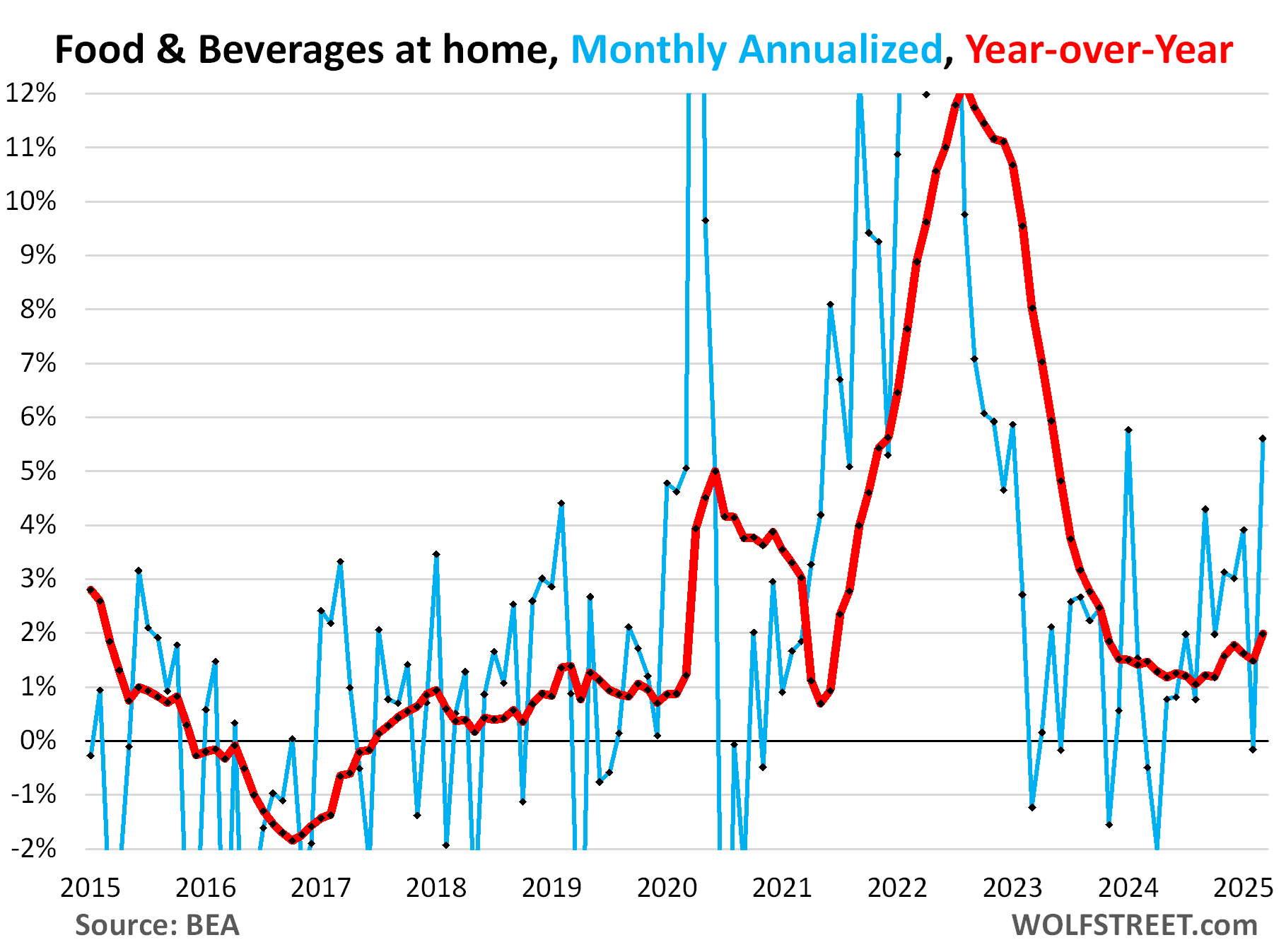

Food and beverage prices surged by 0.46% in March from February (+5.6% annualized), and have been zigzagging higher from the low point about a year ago. These are food and beverage products that consumers buy to consume off premise. They do not include food and beverages consumed on premise, such as at restaurants, bars, cafes, etc.

The year-over-year food price index (red line) has been accelerating since mid-2024 and in March rose by 2.0%.

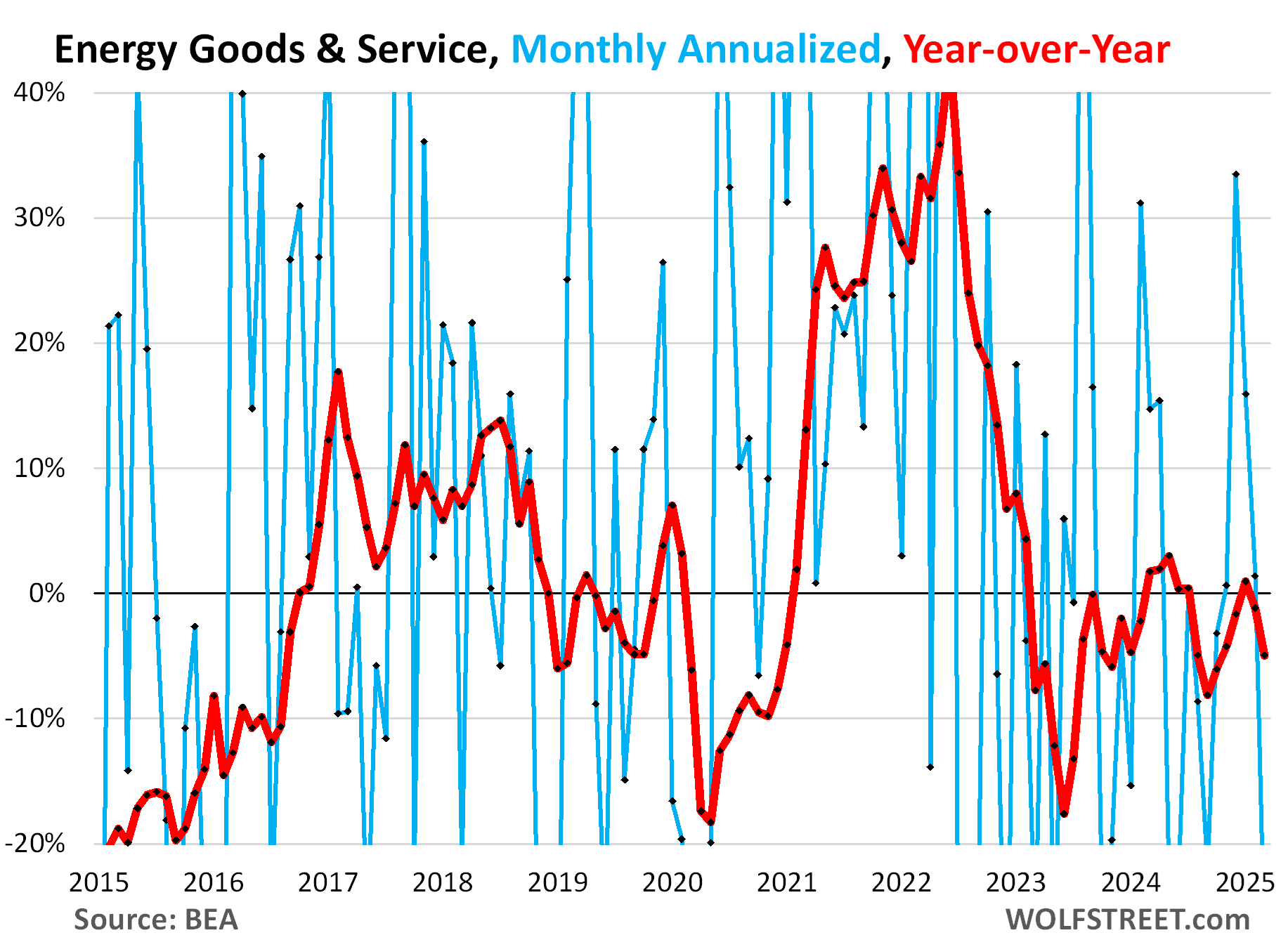

Energy prices plunged by 2.7% in March from February (-28% annualized), driven by the plunge in gasoline prices, which followed oil prices down. Year-over-year (red), the index fell 5.6%.

Energy is a hugely volatile category, along with food, both driven by commodity prices, which is why “core” inflation measures that remove energy and food were conceived to reveal underlying inflation trends.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Seems like all the recent numbers will keep fed in a cautious wait and see position. I would think regardless need to do as who knows when 90 day pause on reciprocal tariffs ends. Guessing the administration has learned its lesson and will put some in place but more tactical.

It’s nothing about learning a lesson – it was shock treatment for maximum impact. Gradualism has no impact; it probably wouldn’t rate a headline on page 3.

The tactical comes after the designated adversaries react appropriately and negotiate.

The FED is INFLATION…no FED, no inflation.

The integrity of the reported results are an agreed upon narrative that we all hope is honest, without bias. Corruption, as codified by the Supreme Court of America in their Citizens United decision that overturned a century of precedence.

Expect a big deflation in stock prices. Rally almost ran its course. Maybe a day or two left. Time to get on the bear wagon again. This time for keeps.

Lol

I realized today, after being bombarded by non stop adverts, that the stock market had bottomed and it was an opportunity to buy. Which wasn’t the small victory that, perhaps, made me look forward to tomorrow.

It was a suspicion that the motivating obsession of a champion sales person is not the price. It is the sale, the transaction.

I think that rocker was right:

Being normal has become a lot harder.

Yeah, no. They (the billionaires who own everything that matters) are going to pump that pig to oblivion. DOW 100k.

Too which I retort, the infamous quote, ” Bulls make money, Bears make money, and Pigs get slaughtered ”

I agree with your sentiment and have lived my life with hope based on a belief that my beloved country is just and kind.

Which didn’t protect us from the exportation of America’s manufacturing prowess to the destitute Chinese Communist Party in order to undercut the American wage and benefit structure for the purpose of becoming wealthy. An ignoble epitath, that is soon forgotten. Several days after a rich person dies the world returns too normal.

Right. Are corporate profit margins going up from here in this business environment? Or down…

They seem pretty healthy so far. It’s one of the reasons Wolf doesn’t expect tariffs to impact prices as much, but more so the fat profit margins.

I am a bear by nature, but learned my lesson not to overstay my welcome in a stock market determined to go up. I don’t call tops or bottoms. We have a bullish trend. It may end this Wednesday (FOMC) or may go on till late summer (more likely scenario). Fear is v-shaped, but greed is a rounded emotion. It doesn’t die quickly.

The result of tariffs might be different this time around considering their aggressiveness in this term. Durable goods seemed to be one component of the CPI that was keeping it down, but if it’s assailed regularly, inflation would rear it’s ugly head.

Do we know what proportion of durable goods is produced offshore vs domestically? And is the recent manufacturing boom able to buoy the durable goods market?

As for energy I’m curious as to how large the impact of renewables is now. Renewables recently passed the price parity of coal and most coal fired plants are simply unprofitable to run these days.

ThePetabyte-

“Renewables recently passed the price parity of coal and most coal fired plants are simply unprofitable to run these days.”

More details and a source would be useful.

I refrain from posting links here but google “renewables coal price”, it’s also been mentioned a handful of times here at WolfSt as well

John H, I’ll provide some sources as long as Wolf is OK with it.

https://decarbonization.visualcapitalist.com/the-cheapest-sources-of-electricity-in-the-us/

This is one source from 2023. A search for “levelized cost of electricity” will return plenty more results that show the same thing. Investing in renewables for electricity production is definitely the best bet for the US.

The advantage that renewables have is that they are new technologies and are thus still affected by learning curves that allow them to become more efficient and thus cheaper over time as more are installed, the siting improves, forecasting energy production improves, parts are made cheaper, installation becomes more efficient, wind turbines become larger(so less need to be built for the same amount of power, solar panels are made more efficient) and the fuel is free, so unlike natural gas or coal, there is no lower bound where producers will no longer dig for fuel because it’s not profitable.

Here is another source that does a good job explaining why renewables have gotten much cheaper very quickly while coal and nuclear have not. While natural gas has gotten cheaper, it hasn’t gotten cheaper at anywhere near the rate of cost declines seen with renewables.

https://ourworldindata.org/cheap-renewables-growth

Hopefully Wolf will be OK with the links

It’s good to see durable goods holding steady. The last thing we need is everything from Whirlpool washing machines to GE appliances to spike upward. I’m not sure what can be done to calm the core services inflation upward agitation. Services are such a large part of the economy that they almost deserve their own chapter in any inflation report. If the core services can come down 2 or 3% YoY, Trump will be seen as a genius.

This stuff can get really interesting: You mentioned Whirlpool — it manufactures lots of appliances in several factories in the US, under several brands, including in Tulsa, which it opened up when I lived there, and which is still making appliances. It will be much less impacted by any tariffs than overseas factories, and it has already said so. And those overseas factories will have to compete with Whirlpool.

Whirlpool also doesn’t make shit appliances unlike Samsung and LG

Meh. Ice maker’s been replaced 3 times in my made in America Whirlpool fridge.

you likely have too much pressure in the water line feeding your ice maker.

I’m in Canada and the reciprocal tariffs are making US products unaffordable compared to Korean or Chinese products. Whirlpool is the best brand in the world but it’s not worth the price now. And US made AC and Heating units, same thing (but I want).

This loss of exports has to be affecting these companies

See: Daikin, Mitsubishi. Although I’m not sure if they do full split units.

To each their own but many people overpay for basic appliances with extra features. I just expect a refrigerator these days to give me in best case 7 years until compressor goes out and then repairs outweigh cost of new more often than not. Almost given up on in door ice makers but do love the convenience. My most recent is Chinese made but for $1200 I am okay if I only get 4 or 5 years.

Inside of every whirlpool are Chinese components. Tariff will hurt whirlpool but not fatal because its price is so inflated. US only makes the casing with imported metal and final assembly.

The components are cheap, no matter where they’re made, compared to the retail price. On any components that are imported, tariffs are applied to the cheap price the importer pays. Whirlpool can and will likely shift more components to US manufacturers to keep its costs down, and so yes, that’s good too. I don’t know why that’s so hard to grasp?

“Call me pro tariff,” Whirlpool chair and CEO Marc Bitzer

“I’m not sure what can be done to calm the core services inflation upward agitation.”

A recession will probably do it

Time will tell

I realize the posture on this site is that tariffs will push multinational corporations to pay taxes and not abuse cheap labor abroad. While that’s true, I’m a bit concerned about the impact to much smaller outfits whose production depends on cheaper parts who are not tax evading multinationals.

It’s apparent to me that the administration is caving to the tariff worries of big business, e.g., Apple, automotive manufacturers, but I have yet to see much relief for smaller players, e.g., small businesses you see on places like Etsy, small manufacturers. They may be able to eventually replace their suppliers to be American but if big business competitors are getting exemptions and they are not: who is this really benefitting after all?

You should be lamenting the hundreds of thousands of manufacturers in the US that were killed by offshoring of supply chains.

Manufacturers in the US are benefitting hugely. Why doesn’t anyone ever mention that? Actually, the WSJ did mentioned it, it mentioned US textile makers the other day. Their business – those that survived — is now booming, and they’re making plans to expand production, invest, and hire.

“Why doesn’t anyone ever mention that?”

Politics

You got it. MSM totally bought out.

MSM for the most part reflects the views of the Democrat Party, which is comprised of leftists, liberals, globalists, socialists and communists. Trump has mentioned this time and time again. People have to search the internet for sites that have generally unbiased news reporting, like Wolf Street. It’s not easy getting real news anymore, like we usually got from Walter Cronkite and Huntley and Brinkley.

thurd2,

Agreeing that the standard wails and moans are easily heard, apparently your devices have FOX News blocked, eh? As mainstream and widely accessed as they come. And as blaring as anything out there, pushing a narrative. There is all kinds of media out there. Another aggressive misplaced wail of persecution? It’s vigorous free speech. You like it free for yours, not others’?

Hello,

View from Europe: the global globalization of markets began with President Reagan and British Prime Minister Thatcher

Less control, opening up to competition; etc…

Over 40 years ago now.

Phleep, the Murdoch family owns both Fox and WSJ and they clearly are against tariffs and in favor of globalization. This is reflected in their general editorial stance.

Phleep, I have no objection to free speech. MSM or anybody can say what they want, but I reserve the right to question it and ignore it. As CSH says, Fox is owned by the globalist Murdoch, and in fact is neither fair or balanced.

Sal, globalization really started with Nixon, Kissinger’s lapdog, with the opening of China. I always thought it was a bad idea. It accelerated under Clinton, with the disaster called NAFTA. I remember in grad school, most of the econ professors advocated globalism, but called it comparative advantage. I thought they were ignorant, having no idea about the security of our country and no interest in its impact on workers in American manufacturing.

ChS,

Just not sure why those that off shored all the manufacturing aren’t held to account. Not like they were forced to and government let it happen. And of course consumers benefited. Was all a win/win until it all caught up where industrial production in US is low. Go figure!

I am a small US manufacturer. I can guarantee we are not benefitting from tariff policy in any way. Quite the contrary actually.

It’s been made abundantly clear to our business and our trade associations that we are too small to curry any favor or obtain any relief. We’ll do what we can, but small manufacturers are starting to take a beating and we will be shedding jobs imminently.

Sounds like Covid lockdown redux(Big Box OK, Mom & Pop SUPERSPREADERS!) which IMO small business has never recovered from.

Lee Fang has a great blog out today regarding the “mass” deportations that aren’t really happening.

You have no competitors that source or manufacture out of China?

Because if you did, that’s to your benefit right now.

Yes. My sister-in-law is getting screwed hardcore, and her family is barely scraping by.

There is no one looking out for less than rich people here. In fact, they are apparently all basement dwellers. And the true basement dwellers keep asking for more.

How? I appreciate your comment, but how is she getting screwed? Your comment is like a post some rube does on facebook about trump defunding fed .gov and people are starving. Nobody is starving in America unless they’re dead.

Remember,before the election, when the MSM

was talking about the “ personal inflation rate”

and how it wasn’t so bad for most people ?

And? Funny how that didn’t win the election or Congress last year. Your point? That free speech should be curtailed?

Not at all. Just wondering why that talking point went away after the election.

And that is why we got out of the making stuff biz,the way things have advanced, production quickly outstrips the market. Everyone loves the concept,the reality not so much. Residtance to price increases shorthand for excess ptoduction…..the great bane of the fetid swamp.

Had a rancher friend in western Nebraska explaining the cattle industry’s reliance on high end exports. “We’re already eating as much as we can,look around. To keep the industry growing,we must export.” Weed industry anyone..??

Agreed, and include Crop products too. Indiana, from my reading sources is a net exporter to foreign trade. Soybeans, corn and beef being the largest export advantage. Medical supplies comes into play also.

Farming at least the level below 1 million dollars of production per farm has been U.S. Federal subsidized for decades.

In a nutshell we as a Country over produce to export. There’s a chain that may be broken.

2 thoughts.

It looks like we are following the upward trend in inflation that existed before the pandemic surge in inflation.

The tariffs in 2018 weren’t broad enough or large enough to really show up in PCE. They are large enough and broad enough to start showing up once current inventories deplete and new inventory starts arriving.

The first place where tariffs show up is in corporate profit margins that will be squeezed. Whether or not companies can pass on higher costs depends on market conditions. Lots of companies have had to CUT PRICES, as you can tell from the negative durable goods PCE price index. They had to cut prices in order to achieve their sales goals. The alternative would have been to not cut prices but sit on growing inventories until hell freezes over or go bankrupt, whichever comes first. So how are they going to raise prices now and achieve their sales goals?

So, squeezed profit margins is where higher costs show up first — and lower stock prices – which is why companies hate tariffs so much and lobby against them so much.

If companies could pass them on, they wouldn’t mind tariffs: their revenues would go up by the amount of the passed-on tariffs, and profit margins would be left intact, and their stocks would continue to rise. But that’s not the case.

During the pandemic, prices spiked because everyone got lots of free money to blow, and they did. But that’s not happening now. The free money is gone, and Americans HATE HATE HATE price increases. It is very tough to raise prices in this environment.

Companies have had record fat profit margins – they are going to eat some of those tariffs, no problem.

“Companies have had record fat profit margins – they are going to eat some of those tariffs, no problem.”

Dear Wolf. May I most humbly request that you release a report on total US Corporate Profits when the BEA makes the numbers available alongside the Second Estimate and Third Estimate of GDP. (The final estimate has a breakdown of profits by sector.)

Yours very humbly, graphic.

Very few people read them in the past. So I gave up. Here is the last one — one chart for each of the major industries:

https://wolfstreet.com/2024/09/26/corporate-pricing-power-and-therefore-inflation-not-vanquished-says-renewed-spike-in-corporate-profits-in-most-industries/

Here is the overall chart for non-financial industries:

and here is the financial industry:

so yes, their profit margins can handle tariffs just fine.

Wow. Shocking to see graphically the rise in profit margins. I suppose I too didn’t pay attention to that chart and report before.

Oh yeah, companies can afford to lose some of those fat margins in response to Tariffs.

And if it also means much less stock buybacks (like GM just announced) I’m definitely in favor of that .

BTW, IF companies can somehow pass all the tariffs on without profit margin reductions, doesn’t that imply there are Monopolies or Oligopolies that should be targeted by free market supporters in Government to allow competition ??

It seems when you refer to companies, what you are actually referring to are large publicly traded companies. Most smaller manufacturers like us do not have fat margins we can simply squeeze. Additionally, the component shortages we are starting to see negativity affect our total volume and delivery. Not a death spiral…yet, but I ain’t optimistic.

Yes, buying from China killed most of you smaller manufacturers and also large manufacturers in the US. By buying your components and materials from China, you also killed smaller US manufacturers. It’s an insidious game, and after 40 years of it, a big part of US manufacturing has been hollowed out, and lots of stuff is no longer made in the USA. So it’s time to rethink this before it’s completely too late. If it’s no longer made in the US because all orders go to China, then make those orders going to China so expensive via tariffs that it will give someone in the US an incentive to make them.

There’s nothing here to give the Fed an excuse to cut interest rates.

The ISM Manufacturing PMI for April out today may be interesting, especially the New Orders and Prices numbers.

Im reading that “corporate profit margins” is what gets hit by tariffs, but, weren’t corporate taxes reduced greatly by the administration several years ago? Are these opposite policies? Can somebody explain it? Thanks

1. See my charts above your comment about corporate profits, and click on the link to see the rest of the charts. Huge record profits.

2. Yes, tariffs have the effect of a tax on corporate profit margins, see GM’s announcement today, that tariffs would cost it $4-5 billion, and it lowered its earnings forecast for that reason. But it’s still profitable. That’s how tariffs work. Maybe GM can pass on some of it someday, but right now, no way, it has been throwing lots of incentives on the market to sell what it makes. Any price increases would kill its sales.

Wolf, what would inflation have been the last four years without corporate profiteering (if profits had stayed at the stable 2012-2020 level). Your data suggests a couple trillion of gouging out of $27T GDP….

No, they’re not opposite policies, though there is some overlap. Corporate income taxes apply equally to all profits of importers as well as domestic producers (ignoring for now the use of tax havens to shield profits by some multinationals). However, tariffs only apply to importers. As a result, tariffs encourage domestic production and the use of domestic suppliers who are not subject to the tariffs, but domestic producers and suppliers still benefit from lower corporate tax rates.

In short, a reduction in corporate income taxes applies to all corporations. Tariffs only tax the profit margins of the smaller subset of corporations that use imports.

An interesting aspect of this situation is that a significant fraction of the advertising on Facebook, X and Google is for goods that clearly sourced from Asia, especially China, that are in many cases drop-shipped and so have been coming tariff-free under the “de minimis” rule (no tariff for shipments under $800), which is ending. Going forward, all these goods will be tariffed. There is likely to be less advertising of this stuff, hitting revenues.

https://chatgpt.com/share/68137985-89d4-8002-bcc7-77bd79efca38

My site was inundated with ads from these Chinese outfits that sold and shipped direct to US consumers. At one point, Temu just about monopolized my site’s ads.

I turned off personalized ads and they have clearly put me in the category of an aging white dude who should do chair yoga. They aren’t wrong!

I like the occasional “Busty Russian Women for Mature Men” ads. My favorite eye-candy on this site.

Its a good thing my wife thinks WolfSt is an economic blog Wolf

Fed’s initial inflation mandate was made in the Federal Reserve Reform Act of 1977.

The January 2012 Statement on Longer-Run Goals and Monetary Policy Strategy, introduced the 2 percent inflation target

“The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run.”

If you exclude the Korean War, 1955-1964, the rate of inflation, based on the Consumer Price Index, increased at an annual rate of 1.4 percent. Unemployment averaged 5.4 percent.

The U.S. Golden Age in Capitalism was driven by the application of savings, where the economy was propelled in 2/3 by the velocity of circulation and 1/3 by new money. Obviously, the economic engine has never been optimized.

While it looks like inflation will accelerate, the long-term prospect looks good by the 4th qtr. of 2026 based on the 2-year distributed lag effect of monetary flows, the volume and velocity of money.