The Atlanta Fed’s GDPNow could be all over the place, but nothing compares to how gold imports blew it up this time.

By Wolf Richter for WOLF STREET.

The U.S. Bureau of Economic Analysis (BEA) will release its first estimate of GDP for Q1 on April 30. The Atlanta Fed designed and maintains a model – an algo essentially – that takes in all kinds of economic data for each quarter and provides a running estimate of the BEA’s first estimate of “real” (inflation-adjusted) quarter-to-quarter annualized GDP growth.

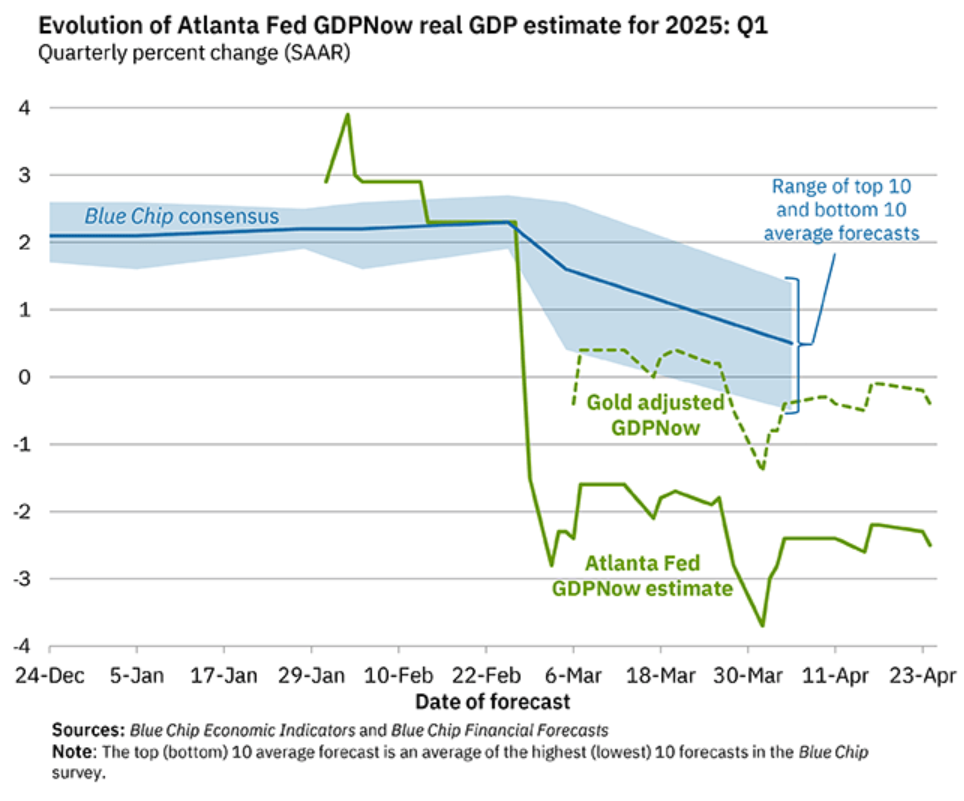

For Q1, GDPNow began providing estimates in late January, and they looked OK, with growth of over 2% annualized. But on February 28, when imports for January were released and taken into the GDPNow model, GDPNow plunged by 5 percentage points to nearly -3%, and went viral. The depression was here, if you believed the clickbait on the internet.

The problem was the spike in imports of gold that investors buy. Imports are a negative in the GDP calculations by the BEA. But gold that investors buy and sell, import or export, is treated like stocks or cryptos that investors buy and sell: It doesn’t enter into the GDP calculation. So imports of gold that investors buy have always been removed from the BEA’s GDP calculation and don’t reduce GDP growth.

But the designers of the Atlanta Fed’s GDPNow model ignored the issue of gold imports. The amounts were small, and it didn’t matter much, until the amounts of gold imports spiked in January, and since monthly amounts are “annualized” (multiplied by 12) to feed into annualized quarterly GDP growth, that one-month spike became a 12-month spike that blew up its GDPNow model, made worse by an additional large amount of gold imports in February, causing the model to forecast a collapse of the US economy.

On March 6, the Atlanta Fed began calculating an alternate GDPNow (the green dotted line) that treats gold imports and exports correctly, by removing them from the GDPNow model. That “Gold adjusted GDPNow” has ranged from slightly positive to slightly negative. The last estimate, released on April 24, was -0.4%. The final estimate will be released tomorrow, April 29, one day before the BEA will release its first estimate of Q1 GDP.

Ignoring gold imports in its GDPNow model went unnoticed until there was an unusual spike in gold imports. And that happens with models: They’re working fine, until they aren’t. The pandemic blew up all kinds of models, including seasonal adjustments and of course infamously on WOLF STREE the CPI for Health Insurance. And those models then have to be fixed in some way.

Last week, the Atlanta Fed published an explanation of what blew up its GDPNow model and how it fixed that in its “New GDPNow Model.” The current GDPNow model will die on April 29. The “New GDPNow Model” (described in detail in this 10-page PDF) will start on April 30.

The Atlanta Fed described the issues and complexities that felled its GDPNow model, and how it included them in its “New GDPNow Model”:

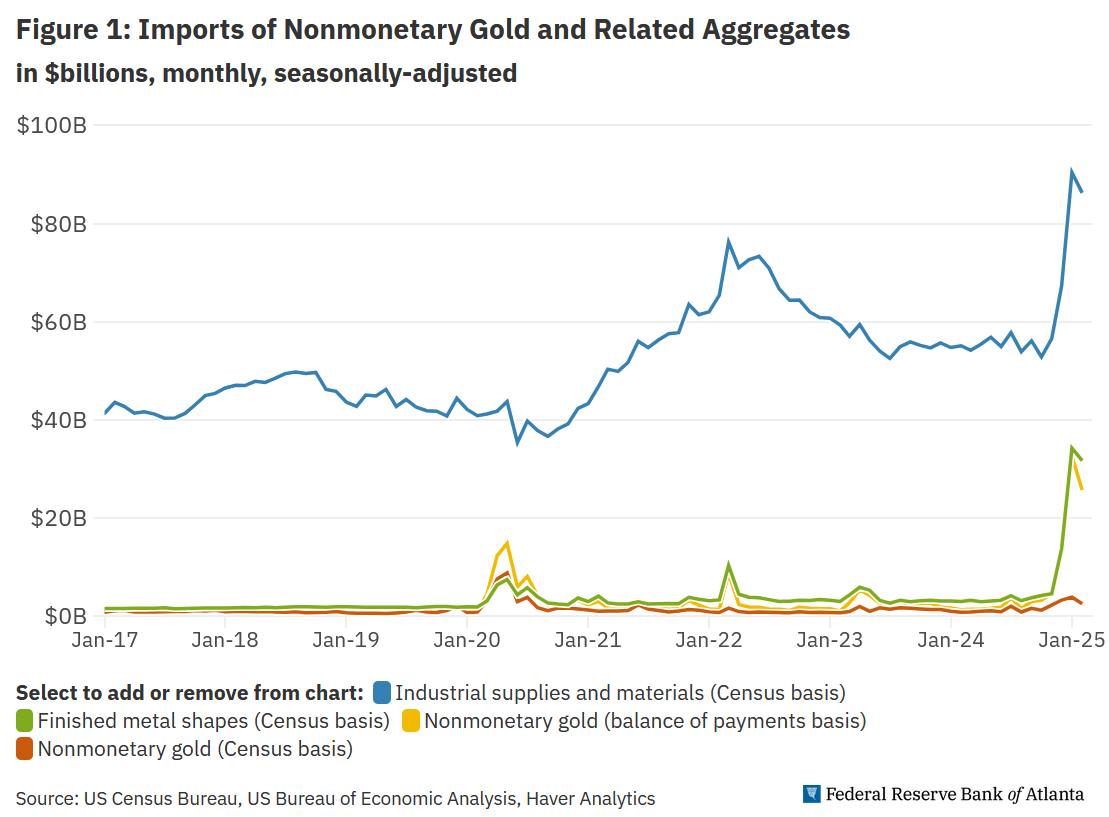

“The measure of nonmonetary gold imports, tracked by the orange line in figure 1 and whose monthly value has never exceeded $9 billion in its 35-year history and has never exceeded $4 billion since 2020, is reported … jointly by the BEA and the US Census Bureau…. Not included in that report, but released [two hours later by the BEA] is a second ‘balance of payments’ (BOP) measure of nonmonetary gold imports. That measure spiked to a monthly average of $29.1 billion for January and February of 2025 (the yellow line in figure 1).”

“Why the disparity in these measures of gold imports?”

“As the BEA notes in an FAQ, the BOP measure of gold includes a portion of ‘finished metal shapes’ imports (the green line in figure 1) that are reclassified by the BEA as gold. Recently, the most important of these commodities by far is identified as harmonized system code 7115900530: ‘Articles of precious metal, in rectangular shapes, 99.5 percent or more by weight of precious metal, not otherwise marked or decorated, of gold.’ In other words, gold bars. According to data from USA Trade Online, these imports surged from $2.08 billion in November of 2024 to $28.69 billion in January 2025 before falling back a bit to $22.96 billion in February 2025.”

“In the 8:30 a.m. (ET) international trade report, the finished metal shapes imports that include these gold bar imports are all classified on a Census basis within “industrial supplies and materials.” These also spiked recently, as can be seen in figure 1 (the blue line). Industrial supplies and materials imports are of interest because they, along with five other sub-aggregates of goods exports and imports, are included in the Census Bureau’s Advance Economic Indicators (AEI) report often released about a week before the full international trade report.”

So how to deal with this mess in its New GDPNow model?

“Unfortunately, the AEI report does not separate gold bars or finished metal shapes from the remainder of the industrial supplies and materials imports aggregate, and this affects our methodology. Is there a way we can utilize the international trade data in the AEI until the full report is released?

“A number of analysts have noted Swiss gold exports to the United States have surged. According to Swiss-Impex data and Federal Reserve Board exchange rates, Swiss gold exports to the United States spiked from under $400 million in each of the first two months of 2024 to $17.2 billion in January 2025 and $14.8 billion in February 2025.

“The reason for the spike is likely due to the move of smaller gold bars, stored in London, to Switzerland, where they are refined into the larger gold bars acceptable in the New York market. These Swiss data are often released about a week to ten days before the AEI, and Comex data on gold inventories are available even earlier.

“Nonetheless, because this data is not available from US government sources and the industrial supplies and materials trade data in the AEI is not further disaggregated, we discard that trade data when using the report to forecast net exports. We do, however, use the remaining trade data in that report as described here”….

Long live the “New GDPNow Model.” Until the next thing blows it up.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

When GDPNow breaks down, at least the economists don’t eat the tourists.

Nice Jurassic Park reference – took me a minute to recall.

Extra points for capturing that sense of unjustified, reckless arrogance by experts – be they dinosaur resurrectionists or our Government betters.

Here’s a couple –

“”I can handle things! I’m smart! Not like everybody says, like dumb. I’m smart and I want respect!”

or

“Respect my authoritah!!”

one matter of concern, money that goes into gold is leaving the economy.

The amount that the buyer pays is the same as the amount the seller receives, minus fees, spreads, etc., received by the middlemen. So the buyer takes money out of the economy, and the seller puts it back into the economy? But maybe the buyer’s cash was never in the economy, it was in a bank account, and the bank had put that cash on deposit at the Fed (as part of its “reserves” to earn interest on), and thereby removed it from the economy. So that buyer’s cash wasn’t “in the economy” in the first place. There are $3.4 trillion in reserves at the Fed right now. There are other possibilities here too. Nothing is simple.

Buying meets two criteria. Cash and Non-Cash. This is buyer side. Buyer takes money out by putting it in seller’s hands. Conversion/Transfer. Buyers buy with credit (borrowed dollars) and earned dollars. (cash) Earned dollars are always in the economy. Likely invested better than a checking account. The money always goes somewhere, to the maximum believed benefit of those who have it. This can drive one mad. Because the buyers become sellers, and the sellers well… gotta put their money somewhere, right?

economists hate gold b/c its not an investment, the capital is locked up like cash in a mattress. i can get a HELOC (boy can i get a HELOC) but there is no GELOC. there are some interest bearing physical gold funds. the world moves on leverage. Greenspan thought the home atm would boost the economy by unlocking equity. worked well in theory. and for another subject those bank ‘reserves’ are capital with restrictions. not all money is equal. what situation would arise where those reserves would become physical cash? you should write a book on the metaphysics of money:)

Gold has no counter party risk and it pays no interest. The buyer traded his dollars for the gold and the seller accepted them. Both of them can’t be right about inflation unless the seller trades his dollars for more gold to sell at a higher price. Another way to value gold is to look at the inputs to produce it. The two most significant inputs are energy and labor. If both are going up then the cost to mine/produce gold is going up provided someone is willing to pay more for it. Reminder: Basel III designated gold as a tier 1 asset(equivalent to Tier 1 capital).

Hi ambrose,

My wife was a manager for Deak Perrera through its transition to Deak International and an eventual Thomas Cook takeover of their FX/precious metals business.

Back in 1980 the Hunt Brothers tried to corner the silver trade and the precious metals market blew up; $50/oz silver and $900/oz gold. Those were the days.

Then came the inevitable bust. Keep in mind gold trades per se don’t directly affect the economy any more than equity or debt trades do.

There are an estimated 250,000 tons of gold above ground, half of which is in jewelry. That’s $25T or so at today’s spot. Contrast that value to BTC; 21 million at $90K or $1.9T.

What killed the Hunt’s trade was the above ground jewelry and coins. Higher prices creates more supply in the medium term than demand, in my experience. Making any guesses as to the effect of fluctuating gold prices on the economy is an uncertain endeavor in my view.

Regardless, best regards to all and RIP Nicholas Deak.

No what killed the Hunt brothers was down to two simple facts:

1. The COMEX changed the rules.

2. The Hunt Brothers bought silver futures and not physical silver.

Had they bought physical silver the rule changes would have no effect on them and they would have been okay.

When you have an exchange that can unilaterally change the rules and force cash settlement of a futures contract at a price that they alone can establish then you are in trouble.

With all commodities, especially gold and silver, of you don’t physically own it, it isn’t yours and it isn’t real.

In that market at that time watching what Hunt bros tried and riding it both ways and made a few coins; word on the street was that Russia was holding gigabucks of silver that Hunts did not know about when they tried to corner…

And BTW, my activity was in those large bars and coins, bars 100 oz IIRC??

They were great, and the local coin shop was selling less than a nickle over and under the close each day.

Lotsa fun far damn shore.

Doubt we’ll ever see such again with SO much more communication due to WWW.

In 1933 the FDR administration implemented order 6102 ,which forced

The surrender of gold coins, bullion etc to the Federal government . It was not confiscation since those surrendering their gold were paid .

I have read numerous ideas on how to store their physical gold coins, but no one has mentioned a viable strategy to

avoid government orders such as 6102.

Hunt Bros go from all that to slanging frozen pizzas reheated and sold at failing convenience stores.

Palladium, Ford, year 2000-2001, Japan, Pd runup on futures/physical based on rumors of possible Russian limit on export, then liquidation only on futures causing crash, same story as the silver except Ford had 2 million oz physical palladium after accumulation which they had to write down when Pd went from 1000+ to 400 early 2002. Their average cost would have been less of course as they were accumulating all during the bubble.

Don’t remember if they flogged it off or kept it – if they kept it, they could just cost it into car production at a reduced input cost because they showed it as an impairment in 2002. By 2011 it was back to 900-1000/oz. And in the interim they did need Pd for production.

“The measure of nonmonetary gold imports, tracked by the orange line in figure 1 and whose monthly value has never exceeded $9 billion in its 35-year history and has never exceeded $4 billion since 2020, … that measure spiked to a monthly average of $29.1 billion for January…”

Boy, that’s ripe for a little internet disaster porn. Heading over to Zero Hedge.

Yeah, leaving GDP calculations out of it, it is very interesting to learn about historic levels of gold importation.

Interesting, that’s definitely a massive revision to the upside. It still leaves GDP projections in the red though.

Bad news is much less bad, but still bad.

The new version of GDPNow (“gold adjusted”) is in the red, but only slightly (-0.4%). I think a slight negative reading in the BEA’s GDP is a possibility.

I just want to point this out here in terms of general imports:

When you buy a $20 item from Temu, shipped directly from China, that $20 boosts consumer spending and is added to GDP, but it also boosts imports by $20, and the entire $20 import is subtracted from GDP. So GDP impact = +20 -20 = 0. This is why Temu’s direct sales have not boosted GDP, and why the collapse of Temu’s sales will not reduce GDP.

If you buy the $20 product from a US manufacturer, and none of it is imported, than the $20 is added to GDP, and nothing is subtracted (no imports), producing a net increase of $20 for GDP.

This is the best example I have found that explained how imports reduce GDP. They don’t. They just cancel out the foreign production based consumption.

You misread this to fit your own narrative. Imports ARE a negative in the GDP formula, and thereby wipe out a positive, such as consumer spending. Imports are insidious when they get large.

Wolf,

Good to know.

Also, a nice, simple, straightforward explanation – which can be hard to come by when covering various government metrics and central bank operations.

Only marginally related, but this issue about imports’ impact on GDP does indirectly bring up the dangers of the US’ scary migration to a “retail flipper/dropshipper” based economy.

1) If a US buyer pays $20 to a US retailer for a $10 item that the retailer bought in China, the US GDP will increase by $10 – but that $10 GDP increase is wholly contingent upon that China produced item…without it, the US retailer has nothing to flip and $10 in GDP (or $100 billion) can vanish pretty damn quick.

2) Also note, the reported GDP increases *more*, the more egregious the US flippers’ mark-up – for an item the retailer did not remotely physically produce.

(Makes you wonder a *lot* about the *true* China price of the last 25 years compared to what US consumers actually paid)

So, the more the US consumer gets jacked by an import dependent US retailer, the higher the GDP becomes. I don’t know if this is broadly understood.

3) At least partially, this troubling aspect of GDP is the result of Keynesian antipathy for *savings* (I think Keynesians view savings as an idle, counterproductive impediment to growth most of the time).

But with US imports from China (at their $400-$500 billion astronomical levels) the seed corn of US savings is expended to primarily reward the productive real economy base of *China* with only an incidental (and ultimately easily disposed of) benefit to US retail middlemen.

To the extent that cheaper Chinese imports are, in turn, used to further build the *US* real productive economic base they are a plus (even with the US retailers’ mark-up skim).

But if Chinese imports are not such that they improve the US real economy, then they are a detriment in the long term – since, in the end, they represent the ongoing erosion of the US capital base (*savings*).

Again, I don’t think this view has been covered enough/clearly enough.

This is also a good illustration of why GDP does not equal “the economy”.

A fictional “balanced” economy that imported everything it consumed and exported an equal value of product would have a GDP near zero. And yet everyone would be busy making stuff.

Arguably, if you draw a line around an area in the US and calculate its GDP, it would look a lot like this. Some county in West Texas produces little more than cattle that are exported out of the county, and almost everything they consume comes from outside the county. All that work for zero!

No narrative….we are saying the same thing.

Y = C + G + EX – IX

C and G includes spending on ALL final goods (including goods that may have been foreign produced). So {C+G-IX} is final domestic spending produced domestically.

Better?

Aman,

READ THE SECOND PARAGRAPH OF MY COMMENT ABOVE THAT YOU REPLIED TO BEFORE YOU POST THIS BS. This is what it says verbatim:

“If you buy the $20 product from a US manufacturer, and none of it is imported, than the $20 is added to GDP, and nothing is subtracted (no imports), producing a net increase of $20 for GDP.”

YOU assume that the consumer doesn’t spend the $20 at all but saves it, instead of spending it at Temu. So that increases savings and the savings rate, and allows bigger future consumption, and you ignore that too. But import versus savings is not the discussion here.

The discussion here is buying an import versus a US-made product. The 2nd paragraph shows you what happens when the consumer spends the $20 on a US-made product (GDP +$20) versus a Temu product (GDP +$0). Got it???

Your narrative has clouded your brain.

“All analysis is a model” – Nobel Laureate in Economics Dr. Ken Arrow.

I think the economy is stronger than gDp shows:

Manufacturers’ New Orders: Nondefense Capital Goods Excluding Aircraft (NEWORDER) | FRED | St. Louis Fed

March retail sales were very strong too.

With 6-7% fiscal stimulus, loosey goosey financial conditions (thanks to Fed created reserves), if the economy is not booming then it means America is screwed.

The true health will only be revealed when policies normalize….if they ever do.

i don’t know how honestly it’s presented, but there’s an article cnbc now about how the wealthy increased spending while others cut back. it seems that my theory that the top will continue to spend as long as the stock bubble is maintained, which the media has made the average american think is necessary for their own survival.

Franz G,

“The others” have not cut back — see the huge boom in used vehicle sales and new vehicle sales all year. But the big spenders are what really matters to the economy because they spend so much, AND because they make economic decisions because they run or own companies, and they make employment decisions, investment decisions (new factory), etc. If they cut back in their spending and their companies’ spending and investment decisions, the economy tanks.

okay, but let’s say we all agree wealth inequality is a problem. if the top, whose spending and investment decisions are driving the economy, how do we deflate the asset bubble and mitigate wealth inequality without tanking the economy?

Franz G, “okay, but let’s say we all agree wealth inequality is a problem.”

It’s not a problem for the wealthy. It’s called capitalism. Wealth inequality is a problem for socialists and communists, until they become wealthy.

Thurd2: “It’s not a problem for the wealthy. It’s called capitalism. Wealth inequality is a problem for socialists and communists, until they become wealthy.”

It’s a problem when the monetary/fiscal policies are skewed unduly in favor of rich people. This is not capitalism but it crony capitalism.

thurd2, if the inequality happened organically, i would agree. in this case, it’s a result of poor government policy.

the question then becomes, are we obligated to maintain the stock bubble, and thus, inequality, to prevent the wealthy from stopping consumption and causing the economy to tank?

Franz G.

“…okay, but let’s say we all agree wealth inequality is a problem.”

Your statement implies that wealth inequality is THE primary problem. Isn’t that like saying that because the sun causes skin cancer, we should try to extinguish the sun? Wealth inequality is an unseemly but motivating side effect of capitalism. It motivates savings, innovation and production.

Wolf’s point about the “big spenders” providing (or NOT) much needed jobs and thurd2’s point about the corruption involved in redistribution schemes cast sunlight on the tempting prospect of “leveling the playing field.”

Equality-oriented systems have been less effective at production — and even more prone to abuse — than economic systems based on saving and property rights.

My opinion only.

John H., Yes. Capitalism in its purest form is based on merit. Alternatives like socialism or communism are supposedly based on some ideas of “equality”. By merit, I don’t mean just being smart and innovative within the market, but also being able to work to your advantage the economic system you find yourself in. For example, looking for flaws in the system, like short-term interest rates being decided by a small group of imbeciles, or the fixed rate on I-bonds being decided by a small group of imbeciles, or various kinds of arbitrage, or idiotic laws (especially IRS and DEI stuff), or loopholes . You will notice that most wealthy people (I am not talking about inherited wealth) are fairly intelligent and work hard and work smart. It can be a fun game if you know how to play it.

All social systems evolve (or devolve) into hierarchies, usually measured by wealth. The USSR, a supposedly communist system, had its elites who had the best dachas and the best vacations and the best houses.

In Monty Python and The Holy Grail there’s a scene:

SIR LANCELOT: Look, my liege!

[trumpets]

ARTHUR: Camelot!

SIR GALAHAD: Camelot!

LANCELOT: Camelot!

PATSY [the serf]: It’s only a model.

Ah, I thought I spotted an arbitrage opportunity when I saw that. I thought GDPNow was adopting a change in method not used by the BEA. So thanks for setting me straight.

There’s still a chance markets crash on Wednesday because even after the adjustment it looks a lot like a recession announcement.

And I wonder about the effects on PCE, reported the same day. March CPI was low so the combo effect of falling GDP and PCE could look very recessionary to those who don’t read wolf street.

There was an arbitrage opportunity. Gold prices had been about $20 lower per troy oz in London compared to New York.

J.P. Morgan alone moved $4 billion in gold reserves from London to NYC this February.

Traders moved about 400 metric tons of physical gold to the New York prior to the tariffs.

Chris B,

“… even after the adjustment it looks a lot like a recession announcement…”

Recessions in the US are called by the NBER, not the BEA. “Recessions” have always required a broad economic downturn, including in the labor market, and there has been no downturn of the labor market. A negative GDP reading alone — such as caused by a surge of imports and a big change in private inventories that have nothing to do with an economic downturn — never triggered a recession call before. We’ve already had a few of those.

So for a recession call you need to see a substantial series of big increases in weekly initial unemployment claims, a couple of nonfarm payroll declines, etc… a group of data in the labor market that show that the labor market is turning down. And so far, that hasn’t happened. It could happen, but it hasn’t yet despite the government job losses.

I should have said “recession warning signal” to be more clear. Sentiment is in the garbage can. Investors are primed to see one quarter of negative GDP growth and interpret that as the likely start of a recession to be announced by the NBER in a year. A clap of thunder can set off a stampede, even if it is a misread of a statistic.

You are right that surging imports did this before. It happened in 2022 IIRC. Investors took the opportunity to flee. In hindsight… what a buying opportunity!

Tariffs had nothing to do with it.

The gold was needed to settle demand for physical settlement.

Australia also exported a lot of gold to the US during that time period as well.

At COMDEX all gold offered for sale by contract must be deposited at COMDEX repositories BEFORE contracts for its sale are issued. Read the COMDEX rules.

SoCal:

Nice to hear from our resident gold hater.

Your post is totally wrong and it’s obvious that you have limited knowledge about the futures market and how they work.

Lol. COMDEX is the computer trade show. COMEX is the metals market.

COMEX, not COMDEX. COMEX has NEVER any any delivery issues whatsoever and any gold sold under contracts must be deposited at COMEX repositories prior to being sold by contracts. I would suggest that you learn about the CME and COMEX.

SoCal, gold producers sell futures based on future production and that becomes their revenue basis.

Users buy futures based on projected consumption and that becomes their cost basis.

Specs are in the middle.

And if settlement for physical delivery becomes a temporary problem, price, cash settlement, or liquidation only is the solution. Comex running out of anything is a legend; they just have to have a normal manageable inventory.

My new formula: GDP = Mindless Consumption (C) + Inbred Corruption + DisInvestment (I) + Market Lurches (M) + New Forms of Predation on Unprotected Consumers (F) + Continued Government OverSpending (on different cronies) (G) – Collapsing Exports (X) – Collapsing Imports (M) – Toilet Paper Currency Gyrations

The really important question is who bought the huge amounts of gold which were imported. The buyer clearly had very, very, very deep pockets. Was it the US Treasury or Fed?

Well we will never know.

There have been huge physical delivery out of the COMEX over the past several months.

As this was classified as non-monetary gold it should NOT have been the Fed or the US government.

Had it been monetary gold then the price of gold would have soared by thousands more as would have indicated huge trouble with their supposed gold holdings.

There have NEVER been any ‘physical delivery’ issues of any commodity including gold out of COMDEX.

Except computers, which are not a commodity, so I guess what you say is right, in a wrong way

The US Treasury and Federal Reserve do not buy gold.

Well you show your ignorance again.

The US government does in fact buy gold.

It also sells gold.

It also borrows gold as well.

The official price of US government gold is $42.42 per ounce and it rarely ever purchases gold for the US Treasury. The Federal Reserve has no interest whatsoever in gold for its own assets and merely leases vault space for storage of that stuff. The US Treasury does not sell gold except for minted coins which it has been doing in small amounts since 1986.

This is the first article about Gold I think I’ve read on Wolf Street – and it’s not exactly about gold. At least not about Gold as a monetary metal.

Lots of reasons floated for why Gold is leaving LBMA and coming to US. Some say there is an arbitrage play, but that seems to have been there for decades and is kind of the underpinning of the whole Gold derivative paper trade – or at least thats what some articles assert.

Some way it was a tariff scare.

Some say it is a reflection of a run on Comes Gold liquidity as Futures contracts are stood for physical delivery in increasing volumes.

I don’t have any idea what the truth is. The FED and “mainstream” economists assure me that Gold has no monetary role any longer. I don’t know the truth or falsehood of that either.

But can we still agree the price is some sort of signal ? Probably, but good luck on finding any agreement on what it’s signaling. Every answer has an element of “talking your book” to it.

So much noise, so little information.

“This is the first article about Gold I think I’ve read on Wolf Street…”

March 31 was the most recent article where gold played a major role and appeared in the title, and it also sort of answered one of your questions:

https://wolfstreet.com/2025/03/31/status-of-us-dollar-as-global-reserve-currency-central-banks-diversify-into-other-currencies-and-gold/

April Fed Reserve I think has reduced QT down to MBS and 5 billion roll off treasuries. I did not understand why the Fed slowed QT this was before tariff discussion maybe to soften the tariff scare .

If GDP is lower as a result of deficit spend then the front run tariff buys may be the reason for the negative GDP and can be explained away

I have some metals as part of a larger basket.

I first though to best of ability have set meself up to eat/have water/basic med ect. for a yearif I can keep it,these are good investments for a natural/man made disaster(hope India and Pakistan cool their jets!).

The United States Mint has been making and selling gold and silver bullion coins every year since 1986. I will assume they are buying gold and silver to make these. Is this part of reported GDP?

They are not a part of any currency system that I know of.

Gold coin sales are seen as financial transactions and are generally not included in GDP.

So gold imports pushed down GDP by at least 1%. Who knew?

And I just thought the new dot line meant it was a better measure.

Yikes! I got that one wrong.

I lost interest in GDPNow a long time ago. Mish Shedlock (whose site I also read every morning) keeps reporting on it as though it’s something of value but has never shown any use for it. Anyone who has watched its moves quickly sees that reading tea leaves gives a similar result.

Oops, sorry for that.

I was just trying to spend my Christmas money on something shiny.

Next time I’ll spread out the deliveries.

Like others, I think the more important question is who bought all this gold, and why now?

As the saying goes “Full FAITH and credit”…

Same as it ever was.

My first real investment in life was buying some USAA Gold Fund shares while in college in 1987 as gold made a run-up in price. I soon learned that gold is NOT a safe investment because a spike in prices brings out people selling excess jewelry as well as gold miners expanding production.

THIS time as it happens I am sitting on a stockpile of the stuff because about two years ago I bought a few hundred computers, servers, and switches to just experiment with how much gold is available in old electronics. By all rights (and the prices of gold back then) I should have barely broken even. At THESE prices you can bet that I am stripping these components for sale as quickly as I can… trying to put the (expensive) lesson I learned in the late-80s to good use.