But it may take a while before these federal lease terminations work their way into CRE delinquency rates.

By Wolf Richter for WOLF STREET.

Vacant office space in the US grew by an additional 8.06 million square feet (s.f.) in Q1, the 18th quarter of negative net absorption over the past 20 quarters, increasing the amount of vacant office space to a monstrous 1.1 billion s.f.

This pushed the vacancy rate to a record 22.6%, up from the 12%-13% range before the pandemic, according to JLL’s Q1 report.

The drivers behind the jump in vacancies were primarily lease terminations by the federal government and federal contractors putting leased office space on the sublease market.

Under DOGE, terminations of federal office leases since January 20 reached 7.56 million s.f. through April 15 across 653 leases around the US, representing about 4.3% of the total amount of office space leased by the government – not including contractor leases – according to JLL’s separate Federal Lease Termination Tracker.

The announced lease terminations had been higher, but the terminations of 181 leases, totaling 3.08 million s.f., have been rescinded amid enormous chaos.

According to a report by S&P Global Ratings earlier this year, about 78 million s.f. (or 52%) of the General Services Administration’s total 149 million s.f. of leased space could be terminated by the end of 2028 as these leases either expire by then (59.2 million s.f.) or have termination options (18.5 million s.f.). These leases are spread across all states around the US.

Overall office inventory declined by over 11 million s.f. in Q1, to 4.8 billion s.f., driven by two factors:

1. Conversions and redevelopments, such as converting an office tower into condos or apartments: 15 million s.f. of office buildings, where such projects began in Q1, were removed from inventory.

2. Minuscule deliveries of new office space: Only 3.5 million s.f. of new office space was delivered in Q1, by far the lowest in the data going back to 2016. Of that, over 1 million s.f. remained vacant. During the heyday, 15-20 million s.f. of new office space were delivered every quarter.

New office construction has fizzled obviously under these conditions, with groundbreakings in Q1 being under 1 million s.f.

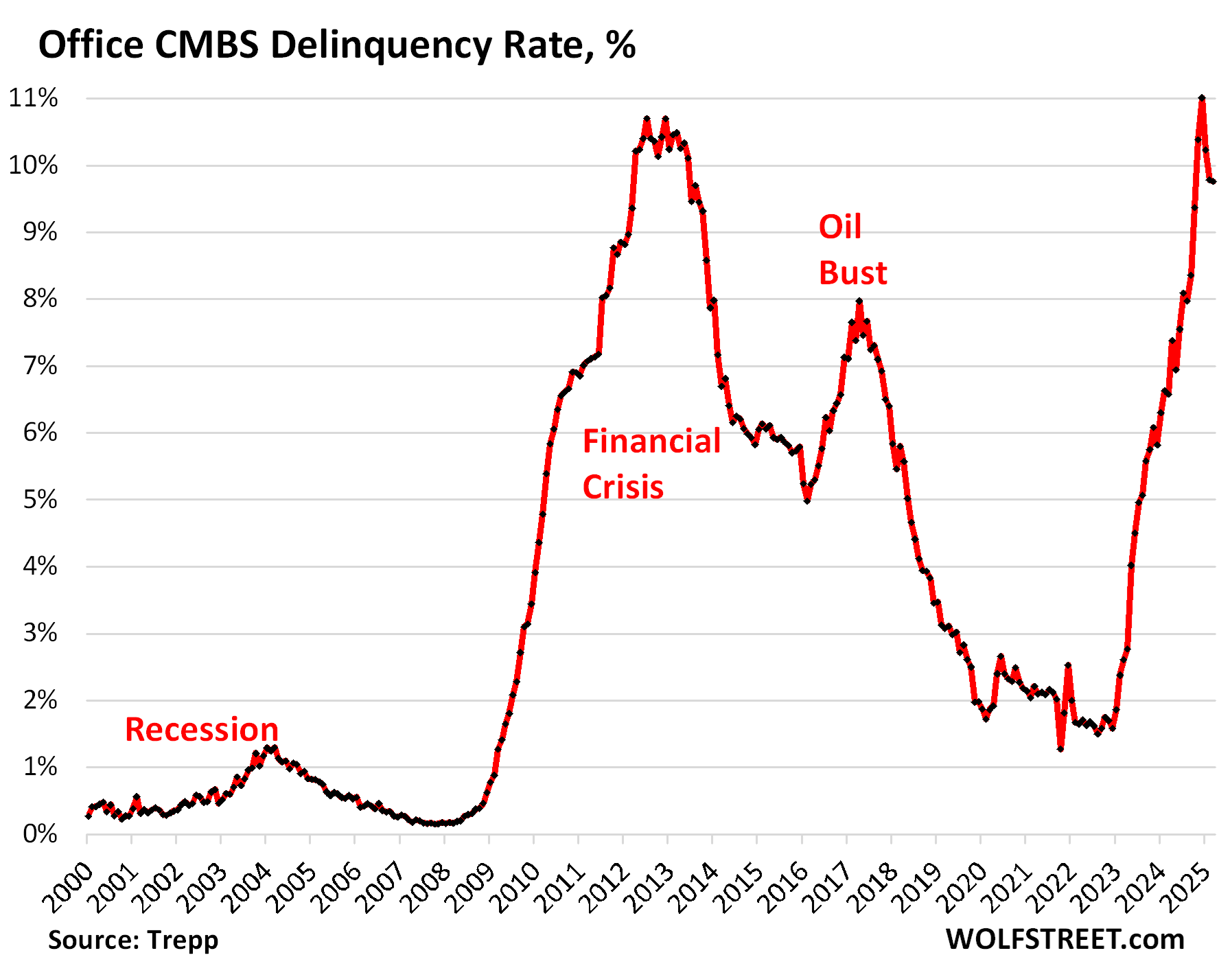

The delinquency rate of office mortgages that have been securitized into commercial mortgage-backed securities (CMBS), after spiking to 11.0% in December and surpassing even the debt-meltdown during the Financial Crisis, declined to 9.8% by the end of Q1, according to data by Trepp, which tracks and analyzes CMBS. CMBS have substantial exposure to government leases that have been or could be terminated.

But it could be a while before these lease terminations show up in the delinquency rates, given how sudden these lease termination announcements came about since January, and how long it will take amid the general chaos for the government to actually stop sending money for those terminated leases, and how long it will take before landlords react by not servicing their debts on those projects, and even then there’s a 30-day grace period before triggering delinquency rates.

So it is likely that most of these government lease terminations have not worked their way into CMBS delinquency rates by the end of March. This is something we’re going to keep out eyes on:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Man, federal government used to be the dream tenant for CRE.

Imagine how much money we, as a country, could save if we just let ‘em all go back to teleworking, and rent or sell the buildings out.

Don’t you mean how we, rich corporations, could boost our profits by shifting all workspace costs onto employees without compensation?

Isn’t the classic capitalist dilemma? How to make profit from products while paying the workforce less while making sure they buy the stuff made?

1. So many employees are let go. Their office space will be also gone.

2. Federal government leasing from the CRE is a kind of legal way for the CRE investors and legislature to make money.

3. COVID showed us Teleworking and WFH are efficient and cost-less

The best part of WFH is not having to waste time and money to travel to work.

The second best is being able to eat at home.

Of course, many employers don’t pay for the costs you incurred for WFH and some employers think that you are on call all the time.

Two hour nap comes in 2nd for me. Really missed that when moving back to US from overseas.

Ross,

I was one of those who voluntarily quit working in an office environment and spent the remainder of my career working from home in 1991. The firm I went to work for specialized in hiring and supporting the “independent broker” and my payout more than doubled. Over the years, my “costs of doing business” shrank so it was very much to my benefit.

if working from home was such a bad thing because you had to pay for your workspaces, why would people be fighting tooth and nail to keep remote jobs?

So the grossly inflated funds dumped into govt leases for empty or significantly underutilized spaces get cut…and insider grift takes a hit. The days of free money and the govt funded vig lining pockets of cCongressional critters, their bureaucrat sycophants, favorite donors, banker/private equity buddies, future employers, family and friends dries up. Hooray! No wonder ridiculous valuations and market insensitive lease rates have driven real estate speculation to the moon. Taxpayers and businesses get the shaft. Time for reality to make an appearance.

You’re funny. Government tenants negotiated hard on rents. The dream part is that they’re never deadbeats. Too many people have this vision of dopey pay-anything-without-a-care feds just handing out money. Nuh uh.

Yeah, owners love the USG. USG rarely downsize so once you sign them up (even if the deal is not great) – tenants for life. The owner’s bank likes them as well. They always pay (legally obligated). Generally more reasonable to work with relative to private companies. I worked gov leases overseas, even with our complex and demanding lease documents they had to sign, they loved us at tenants. We always paid, and on time.

Yeah, that’s what happens when the TGA empties out and liquidity dries up.

Can you folks imagine if housing vacancy rates were at 22.6% ⁉️ ⁉️. Prices would be in the toilet. Prices would be decimated.

However, in the business world, we have 22.6% office vacancy rates and most businesses that rent their stores are getting reamed with sky high rents. Upside down world.

Prices of office buildings plunged 35%-70%. Prices reacted very cast. The whole sector was repriced in a year, with HUGE haircuts.

So the govt needs lower rates. They will make it happen.

I work with my 2 dogs who are NOT named Busybody and Prima Donna.

There will be a secondary wave as a lot of state agencies and associated non-profits are losing funding and will have to let go of their space as well – its not just the feds. Some states like HI and AK probably have a ton of office space that has federal or state tenants. On the bright side, if you’re an entrepreneur that is looking for space, prices should be pretty cheap over the next few years.

Hawaii has a lot of military and is the destination for weekend warriors to do their two weeks. They won’t be hurting.

I’m grateful for this information, because I don’t read enough economic news to fish this stuff out.

However, it makes me nervous / uneasy because the socialism-for-the-rich power-mongers will, by hook or crook, see to it that the general population pays for any serious collapse of the CRE investment world.