Austin, Oakland, St. Petersburg (FL), San Francisco, Chula Vista, Detroit, New Orleans, Denver, Jacksonville, Naples, Tampa, Mesa, Portland, Seattle.

By Wolf Richter for WOLF STREET.

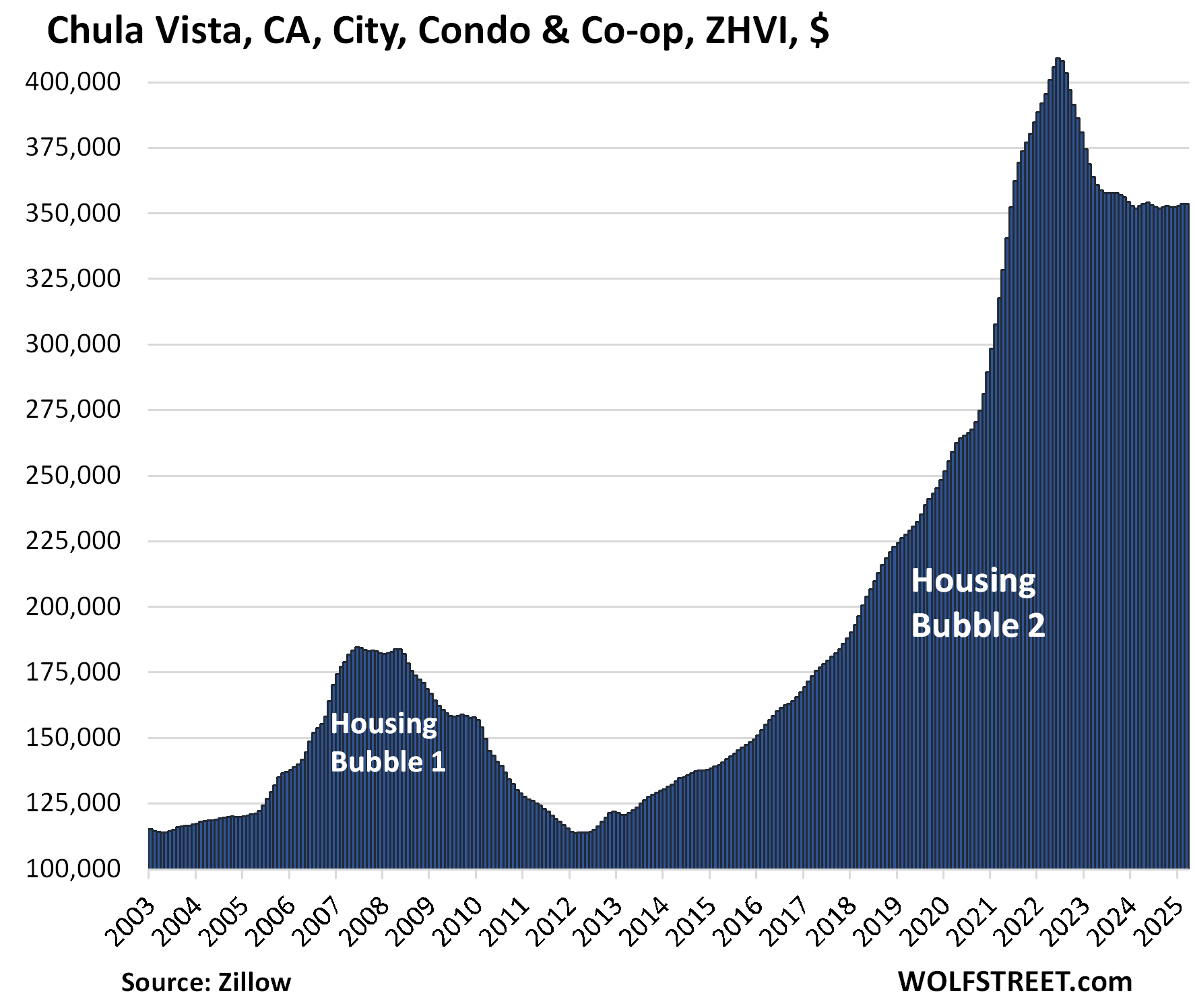

Condos are often the first and biggest movers in local housing markets. Prices exploded in many of them over the three years between mid-2019 and the peak in mid-2022, by 60% such as in Austin, TX; by 70% such as in Tampa, FL, and Chula Vista, San Diego County, CA; or by 80% such as in Mesa, AZ, and Lakeland, FL.

But this absurdity is now coming unglued, and prices have begun spiraling down. In Austin, which is on the forefront of this movement, prices have already given up nearly two-thirds of the 60% three-year gain. People who bought at the top in mid-2022 are 22% underwater. People who bought in mid-2019 are still sitting on a 20% gain that is shrinking.

Price drops from peak (charts below):

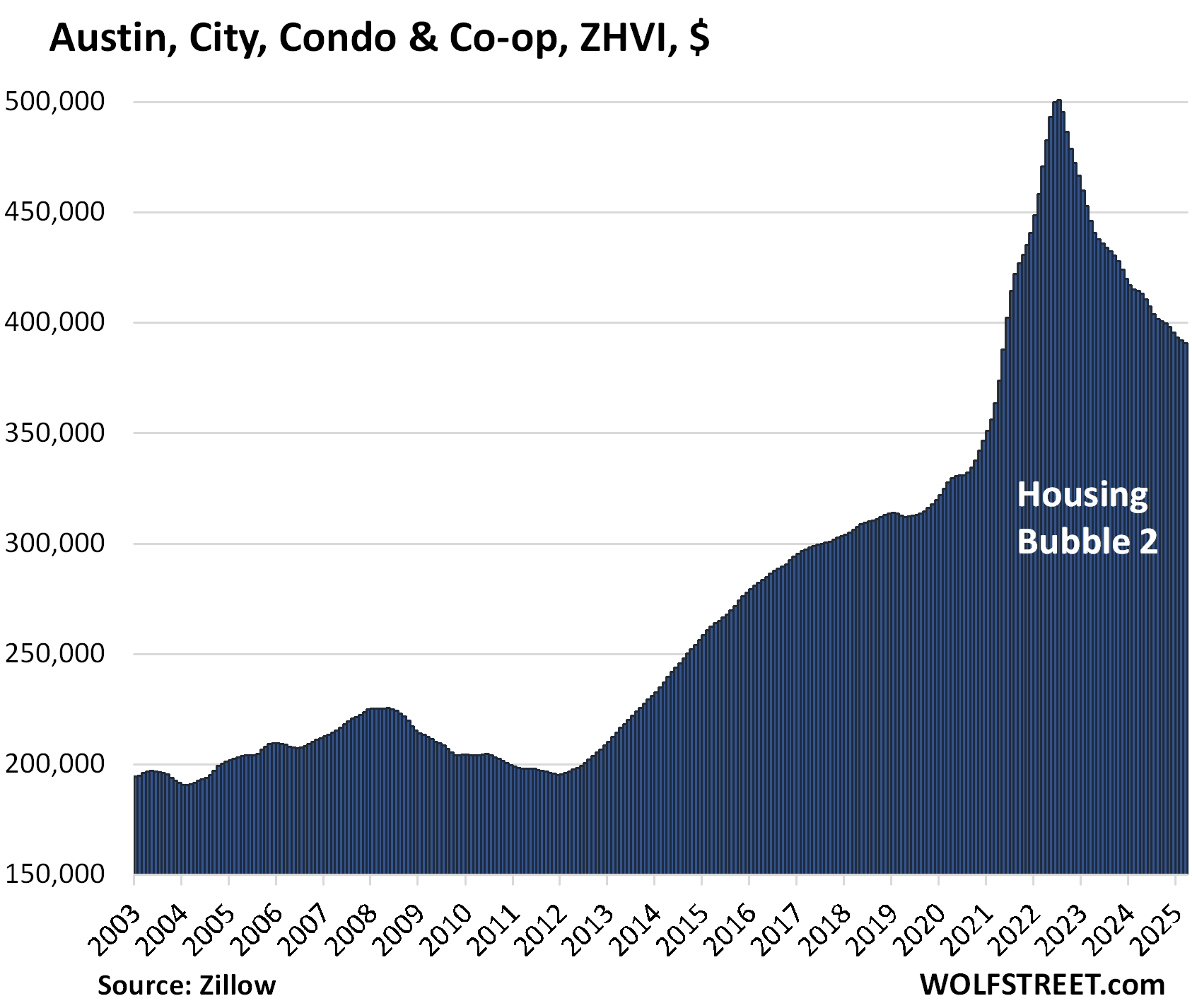

- Austin, TX: -22%

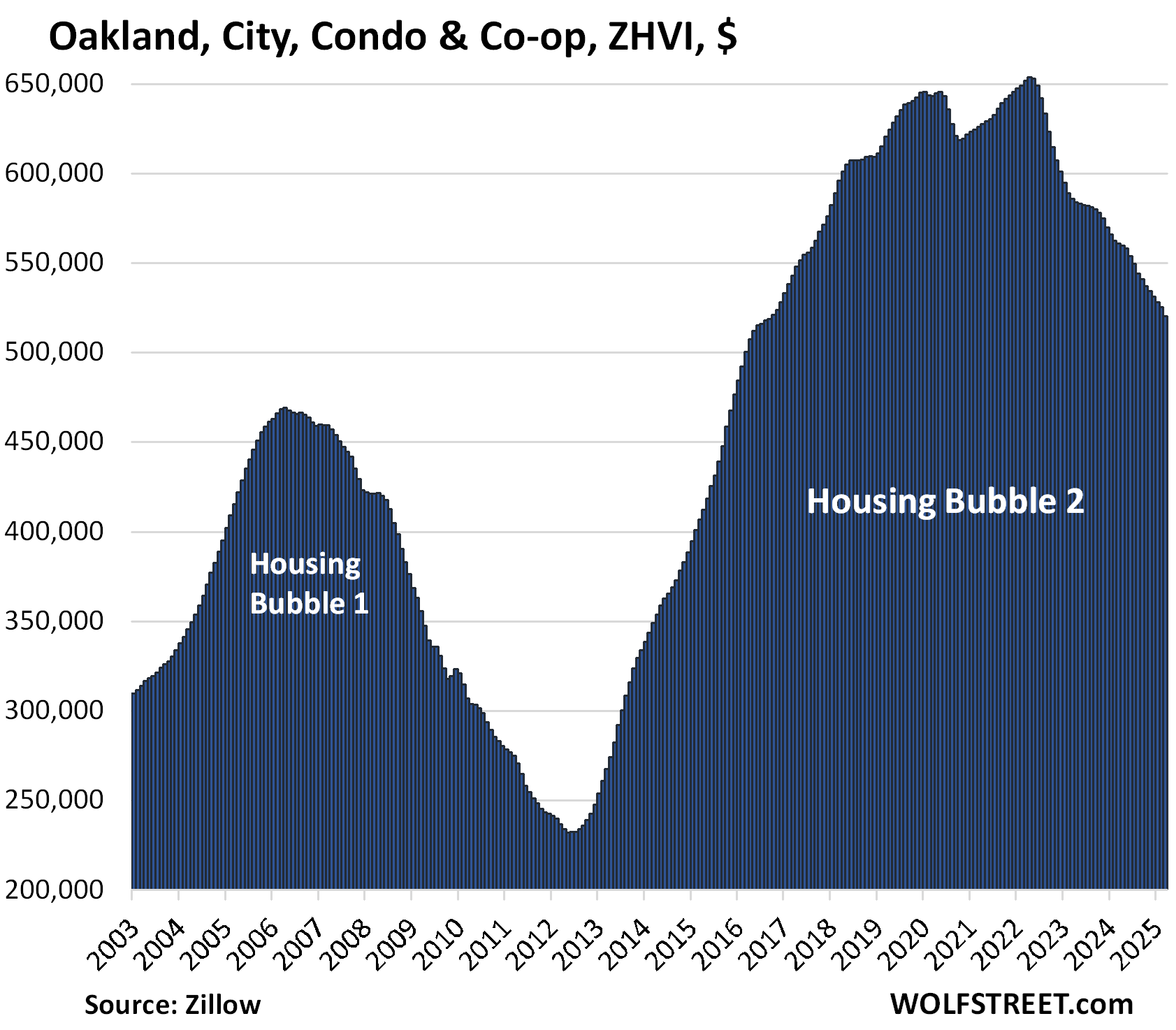

- Oakland, CA: -20%

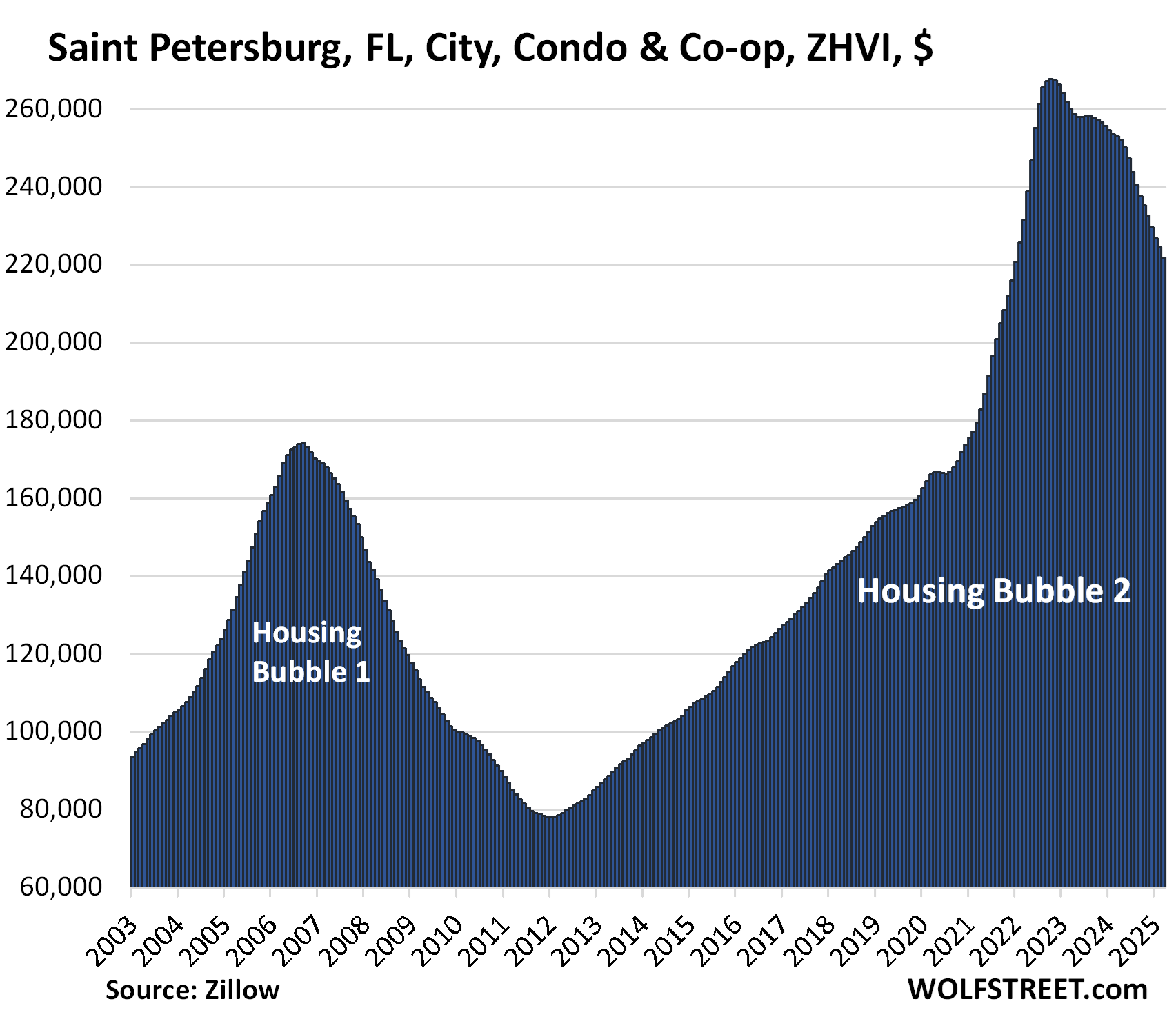

- Saint Petersburg, FL: -17%

- Chula Vista, CA: -14%

- San Francisco, CA: -14%

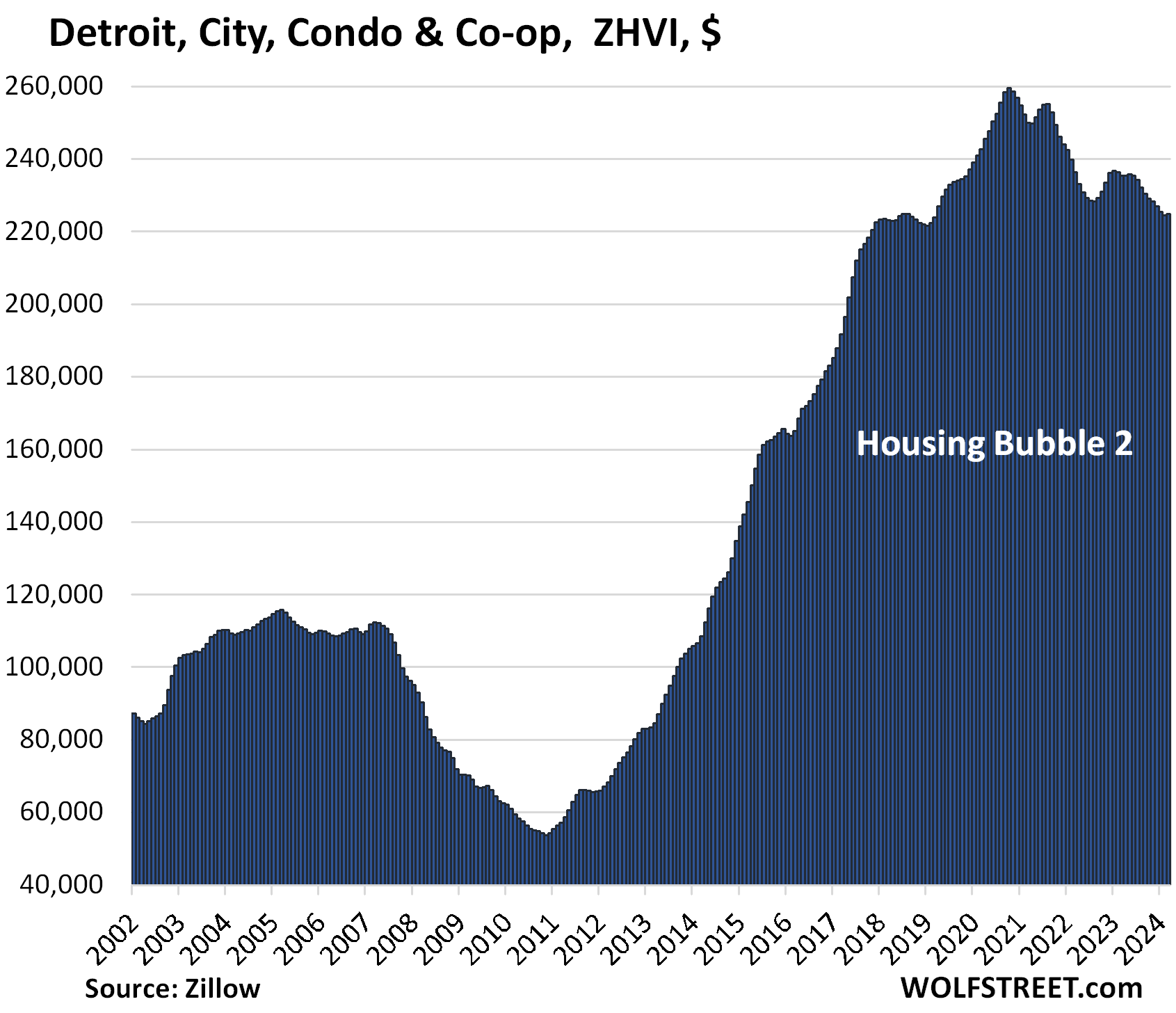

- Detroit, MI: -13%

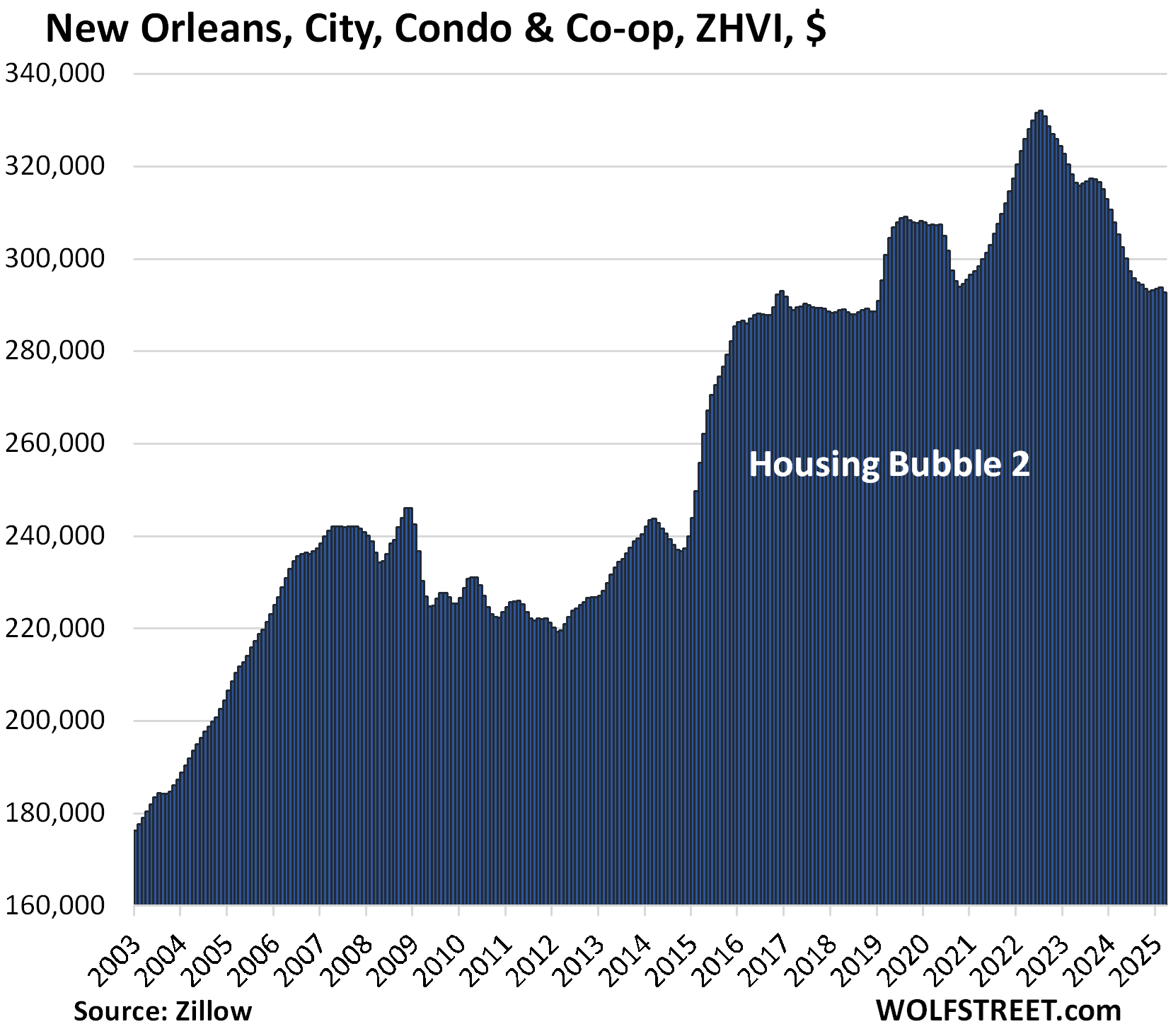

- New Orleans, LA: -12%

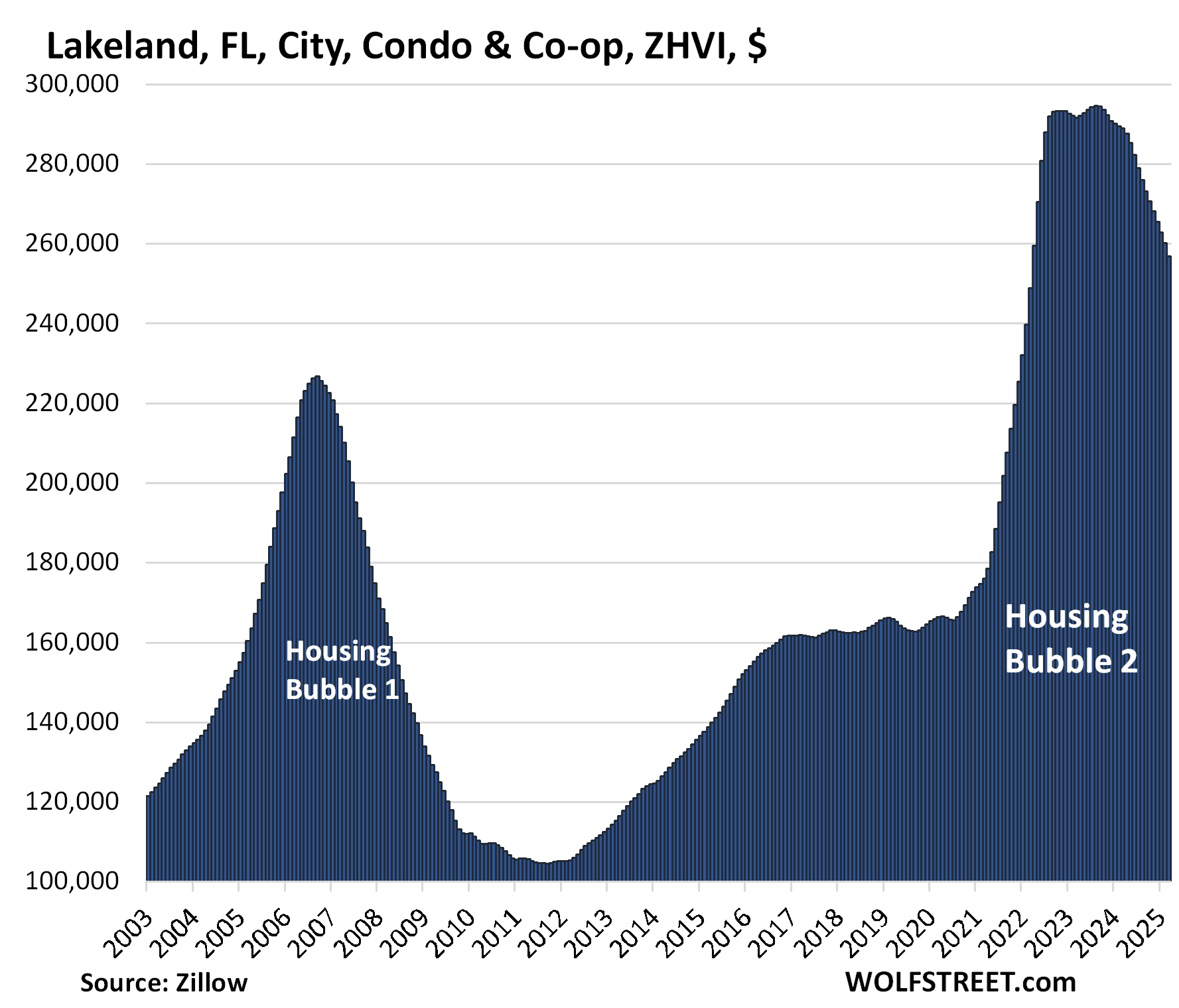

- Lakeland, FL: -13%

- Denver, CO: -11%

- Jacksonville, FL: -11%

- Naples, FL: -11%

- Tampa, FL: -10%

- Mesa, AZ: -10%

- Portland, OR: -10%

- Seattle, WA: -10%

In Florida, price drops are accelerating. Of the 15 cities here where condo prices through March have fallen by 10%-plus from their peaks, 5 are in Florida, but not yet including Miami and some other cities in the state with declines of still less than 10%. In the little tables for each city below, note the sharp month-to-month drops in those cities in Florida – a sign that the declines are heating up.

Condo dynamics are different.

Condos attract a large share of investors, including mom-and-pop investors, that want to generate income from long-term rentals, student rentals, or vacation rentals. And they want to cash in later on the expected huge capital gains. Condos also attract second-home buyers, especially along the coasts and in the mountains. In the southern part of the US, they also attract snowbirds, often retirees, from parts of the US and Canada with long and harsh winters.

But long-term rentals have come under pressure from the massive supply of brand-new apartment developments that sprang up over the past few years. The vacation-rental boom over the past few years created a huge supply of vacation rentals, and demand for them may have peaked. And snowbirds from Canada anecdotally are said to be getting second thoughts about their condos in Florida, Texas, and Arizona.

Then there are the issues of soaring HOA fees in some areas, driven by soaring insurance costs.

Older condo buildings can whack owners over the head with huge special assessments to fund long-neglected repair and maintenance projects. For investors, that’s a tough nut to crack: Instead of getting regular cashflow from the unit, they’ve got to plow more money into it. Owners that don’t want to or can’t pay for those assessments would have to sell their units.

Interest rates have risen and stayed high, making purchases much more expensive after the 60%, 70%, or 80% three-year price spikes in the erstwhile hottest markets.

In addition, news of a growing “mortgage blacklist” at Fannie Mae began circulating. It has grown to over 5,000 condo properties that failed to meet Fannie Mae’s lending criteria. Over 1,400 of these properties are in Florida and over 700 are in California, the two states most impacted by it. Obviously, the numbers of properties on the blacklist are only a minuscule portion of the total number of condo properties. But condos in one of the blacklisted properties are difficult to finance, and therefore are difficult to sell other than to cash buyers, often at a big discount. In the broader sense, there may be more of a psychological impact from that blacklist, including the fear that an older not-blacklisted property might end up on the blacklist in the future.

In some densely populated cities, such as San Francisco, condos make up a bigger part of the housing market than single-family residences.

The absurd price spikes come unglued.

So here are the 15 bigger cities where condo prices have dropped by 10% or more from their respective peaks. Most of those peaks were in mid-2022, but some peaks were in prior years.

Condo prices here are seasonally adjusted three-month average prices of “mid-tier” condos. The data are from the Zillow Home Value Index (ZHVI), which is based on millions of data points in Zillow’s “Database of All Homes,” including from public records (tax data), MLS, brokerages, local Realtor Associations, real-estate agents, and households across the US. It includes pricing data for off-market deals and for-sale-by-owner deals.

Blame for this absurdity in 2020 through mid-2022 goes to the Fed’s schemes of money-printing and interest rate repression at the time, which triggered a general mania for asset purchases. But those schemes stopped in 2022, and then were reversed to some extent, including by un-printing $2.24 trillion so far and by much higher short-term policy rates, the combination of which caused mortgage rates to surpass 6% since September 2022, and lingering on either side of 7% much of the time, including now even after the Fed has cut short-term policy rates by 1 full percentage point (here is my explanation why mortgage rates have remained high).

The left figure in the little tables below shows the drop from the peak. The right figure shows the still huge gains since 2000.

Cities in Texas, and Denver, didn’t really have much of a Housing Bubble 1, and therefore didn’t have much of a Housing Bust 1. But they made up for it during Housing Bubble 2.

| Austin, City, Condo Prices | |||

| From Jul 2022 peak | MoM | YoY | Since 2000 |

| -22% | -0.3% | -5.7% | 121% |

Lowest since April 2021.

| Oakland, City, Condo Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -20% | -1.0% | -7.2% | 179% |

Lowest since September 2016.

| Saint Petersburg, Fl, City, Condo Prices | |||

| From Oct 2022 peak | MoM | YoY | Since 2000 |

| -17% | -1.1% | -12% | 226% |

Lowest since January 2022.

| Chula Vista, CA, City, Condo Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -14% | 0% | 0% | 222% |

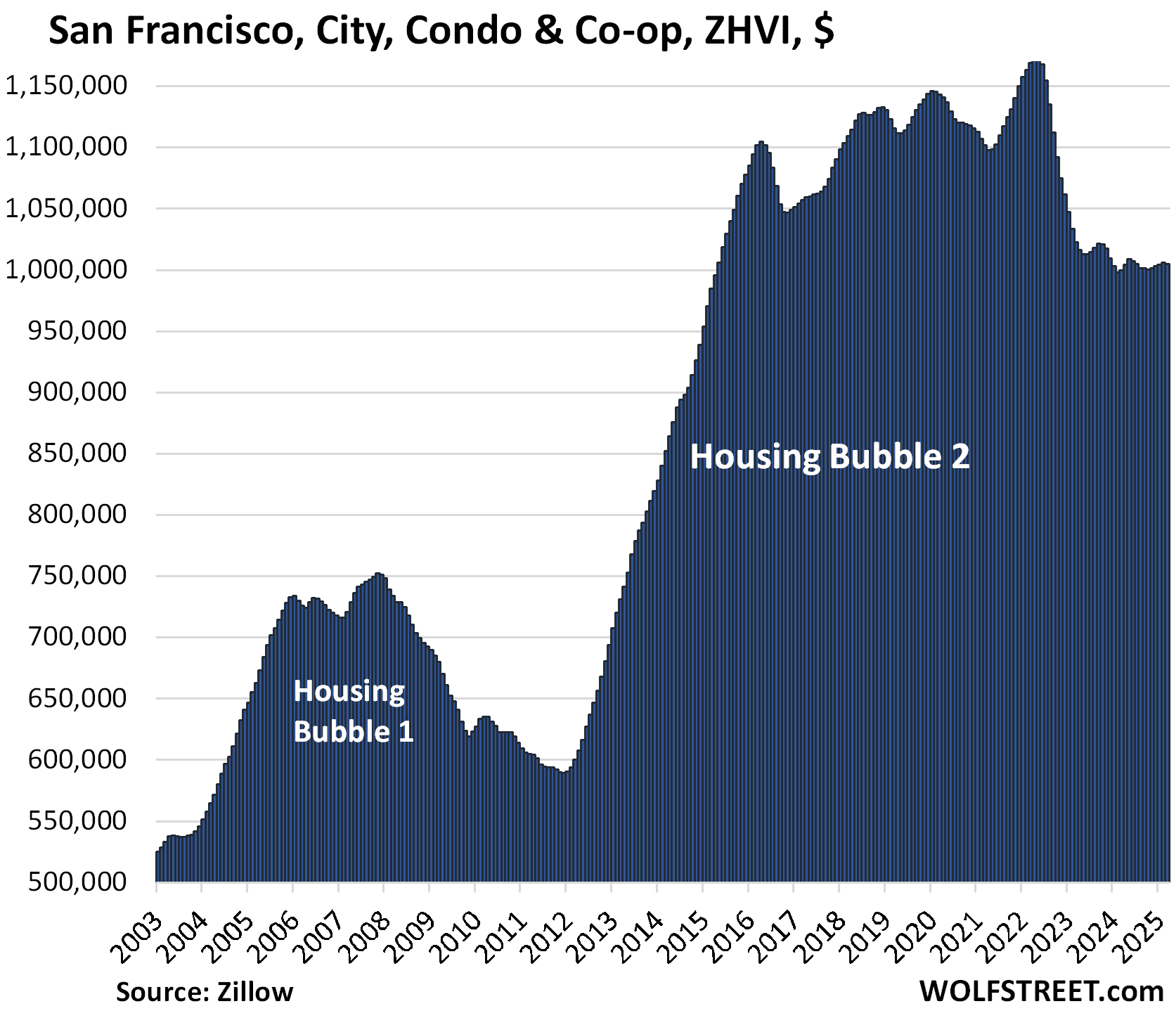

| San Francisco, City, Condo Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -14% | -0.1% | 0.5% | 145% |

Back to May 2015.

| Detroit, City, Condo Prices | |||

| From Sep 2021 peak | MoM | YoY | Since 2000 |

| -13% | 0.2% | -4.3% | 271% |

| New Orleans, City, Condo Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -12% | -0.4% | -4.1% | 102% |

| Lakeland, FL, City, Condo Prices | |||

| From July 2022 peak | MoM | YoY | Since 2000 |

| -13% | -1.3% | -11% | 161% |

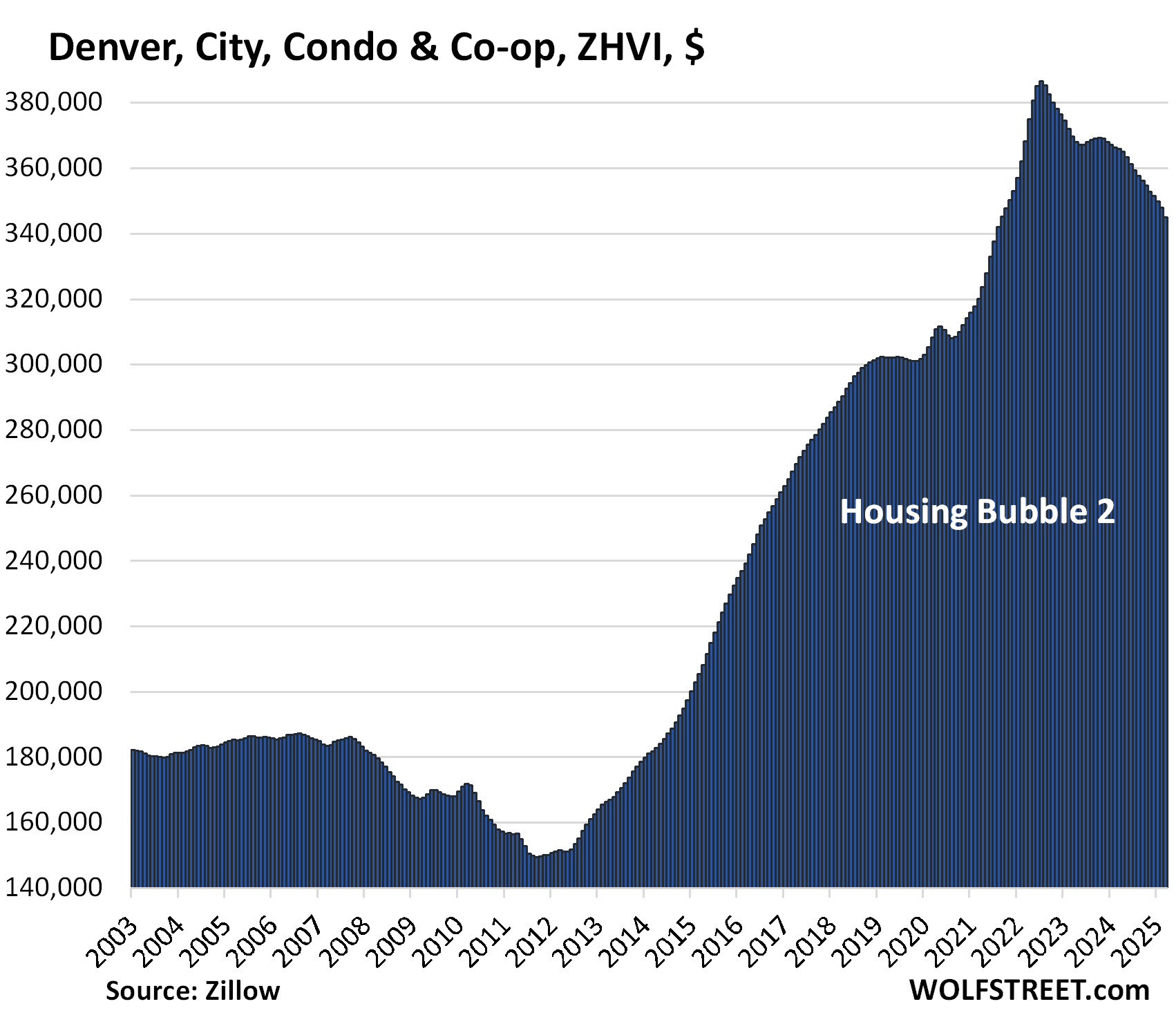

| Denver, City, Condo Prices | |||

| From Jul 2022 peak | MoM | YoY | Since 2000 |

| -11% | -0.9% | -5.7% | 148% |

Lowest since September 2021.

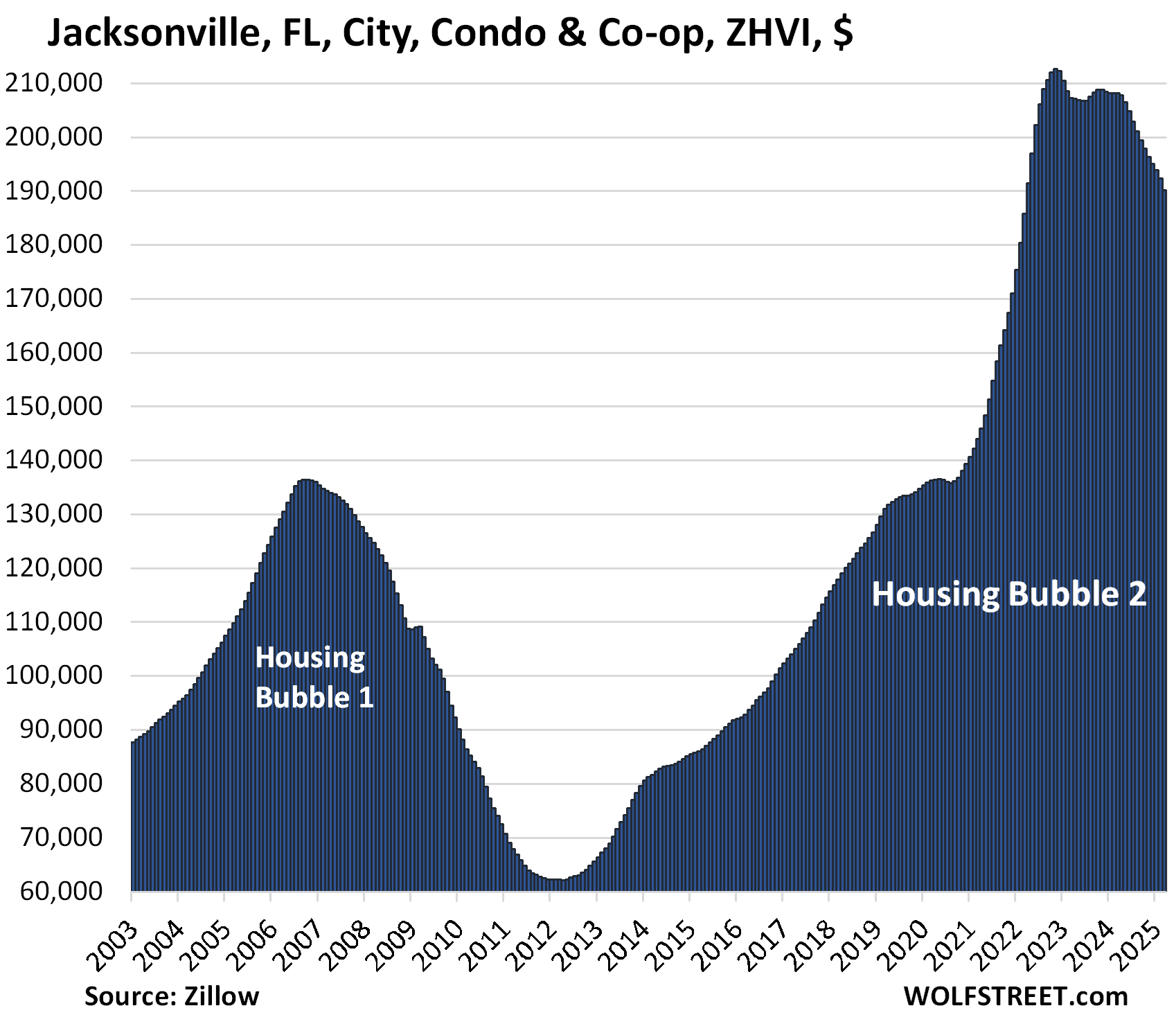

| Jacksonville, FL, City, Condo Prices | |||

| From Nov 2022 peak | MoM | YoY | Since 2000 |

| -11% | -1.1% | -8.6% | 171% |

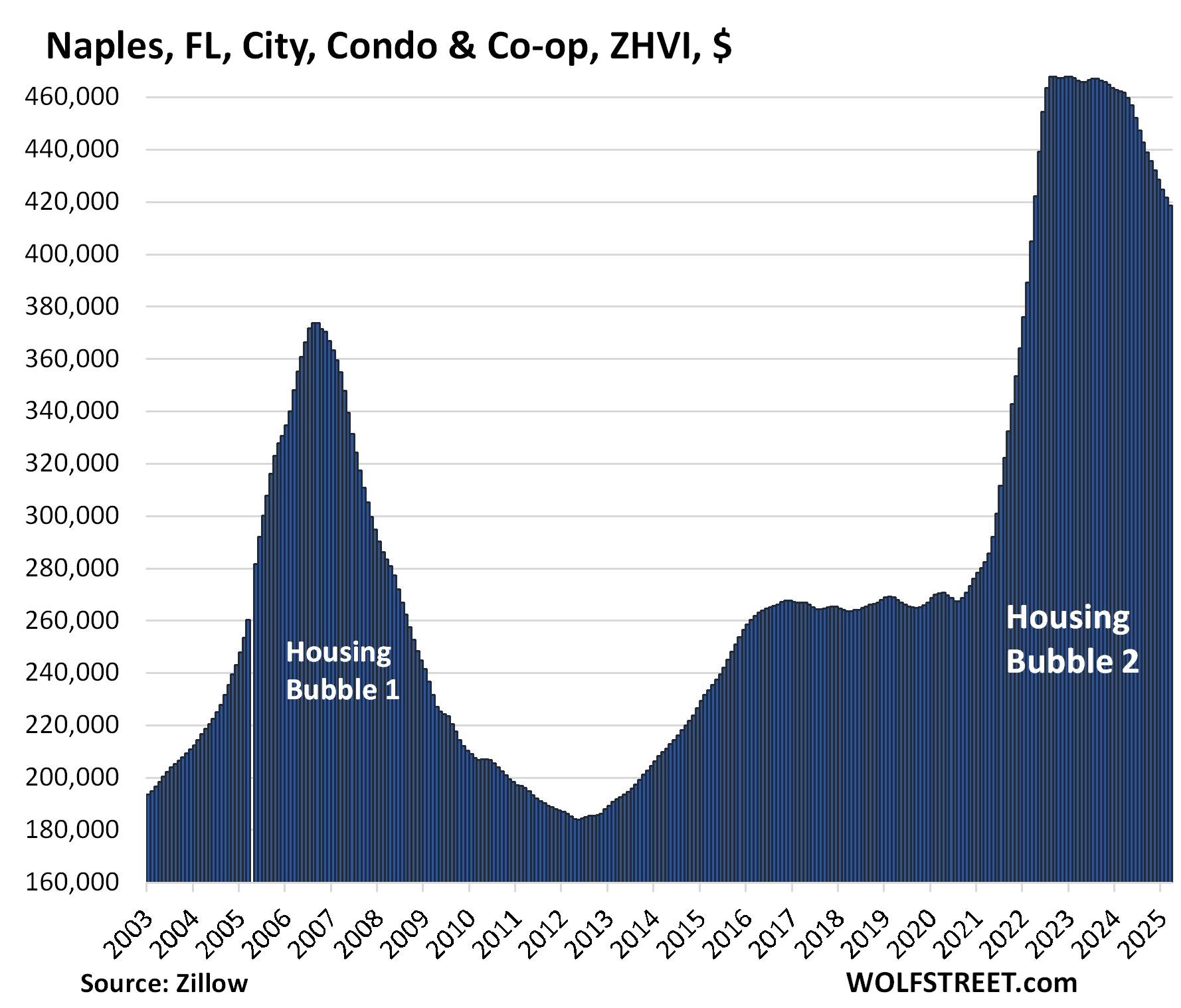

| Naples, FL, City, Condo Prices | |||

| From Aug 2022 peak | MoM | YoY | Since 2000 |

| -11% | -0.7% | -9% | 175% |

This would kind of funny, if it weren’t so serious:

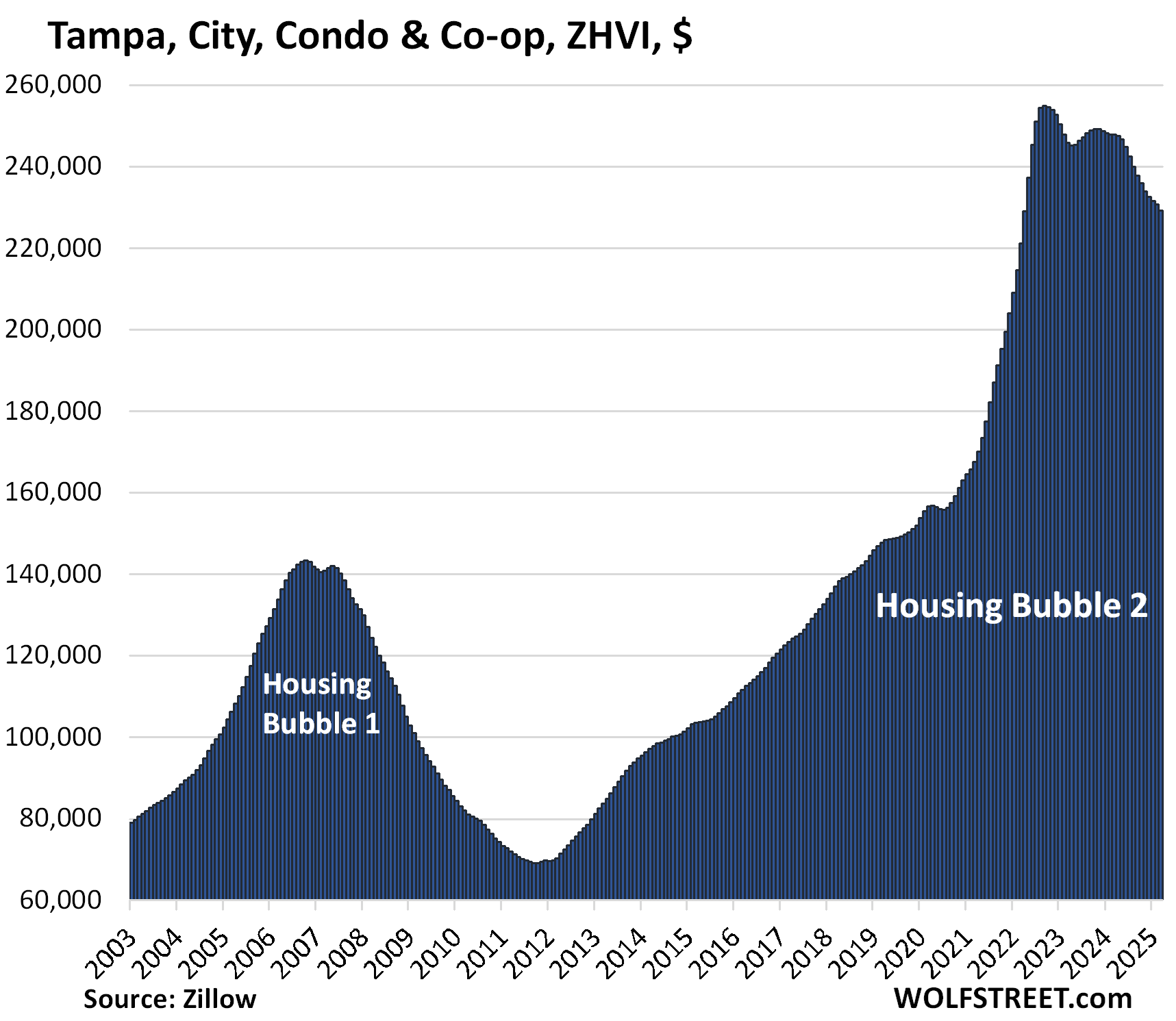

| Tampa, City, Condo Prices | |||

| From Sep 2022 peak | MoM | YoY | Since 2000 |

| -10% | -0.7% | -7.5% | 293% |

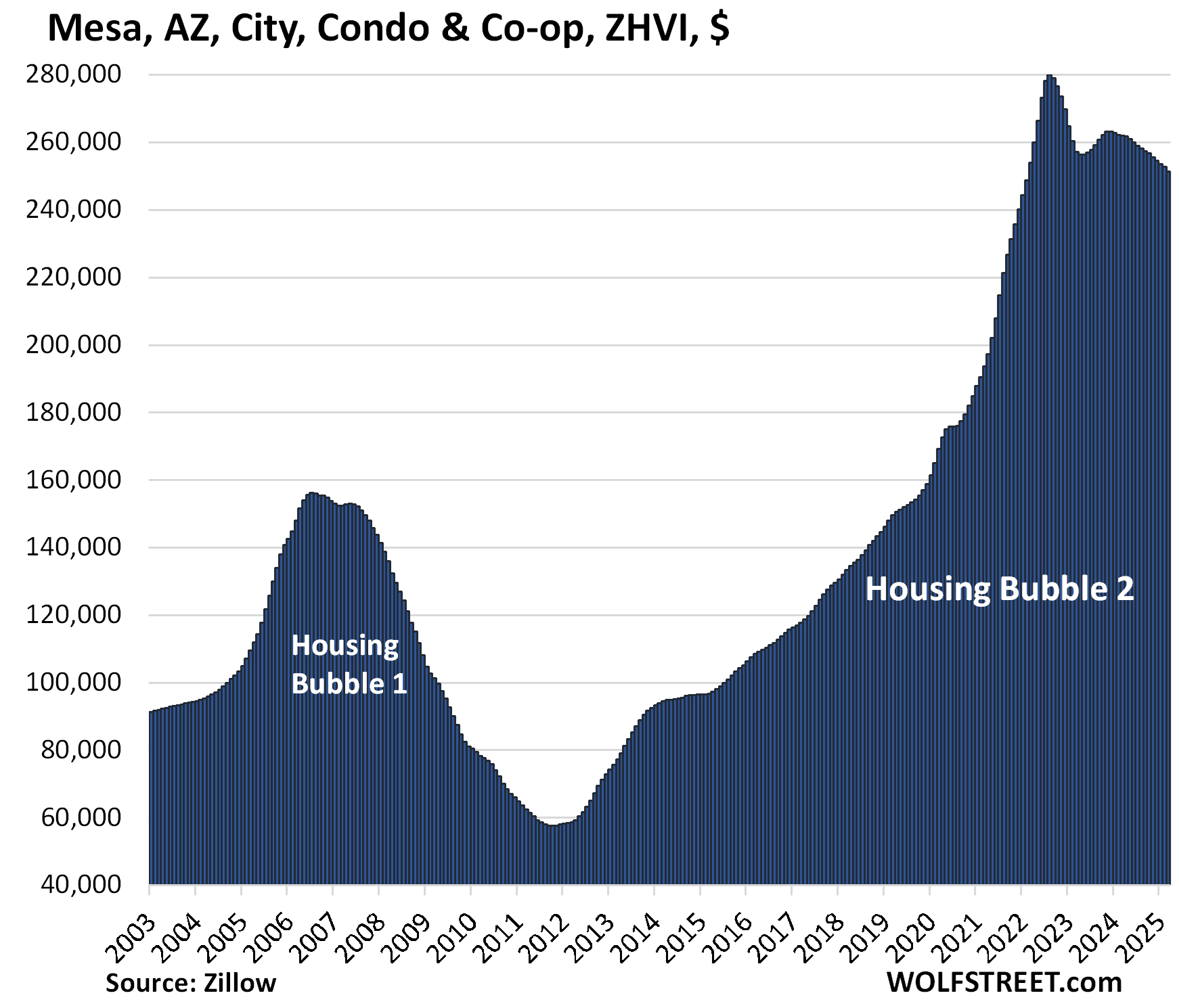

| Mesa, AZ, City, Condo Prices | |||

| From Aug 2022 peak | MoM | YoY | Since 2000 |

| -10% | -0.5% | -4.1% | 215% |

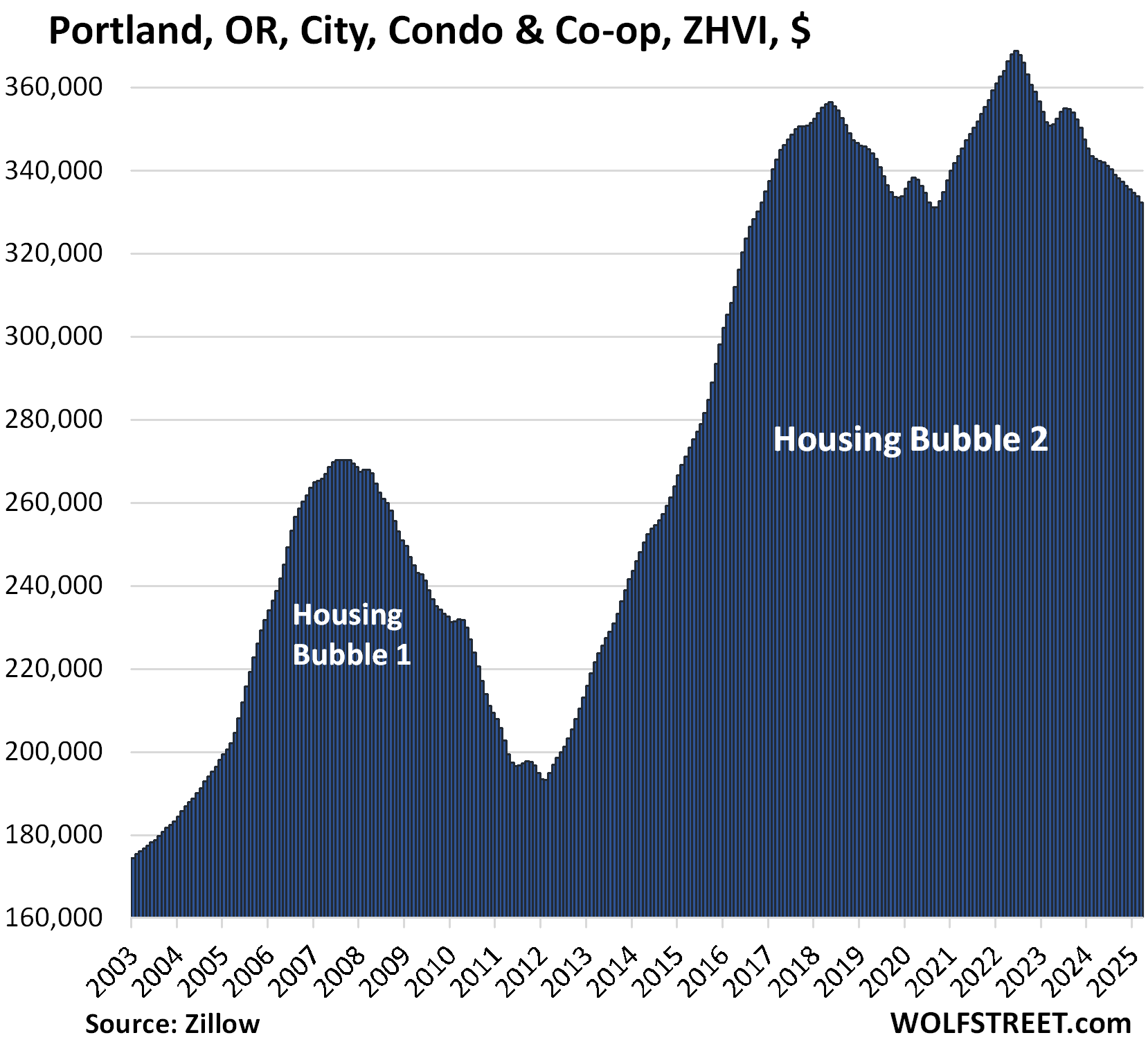

| Portland, City, Condo Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -10% | -0.4% | -3.0% | 117% |

Back to November 2016.

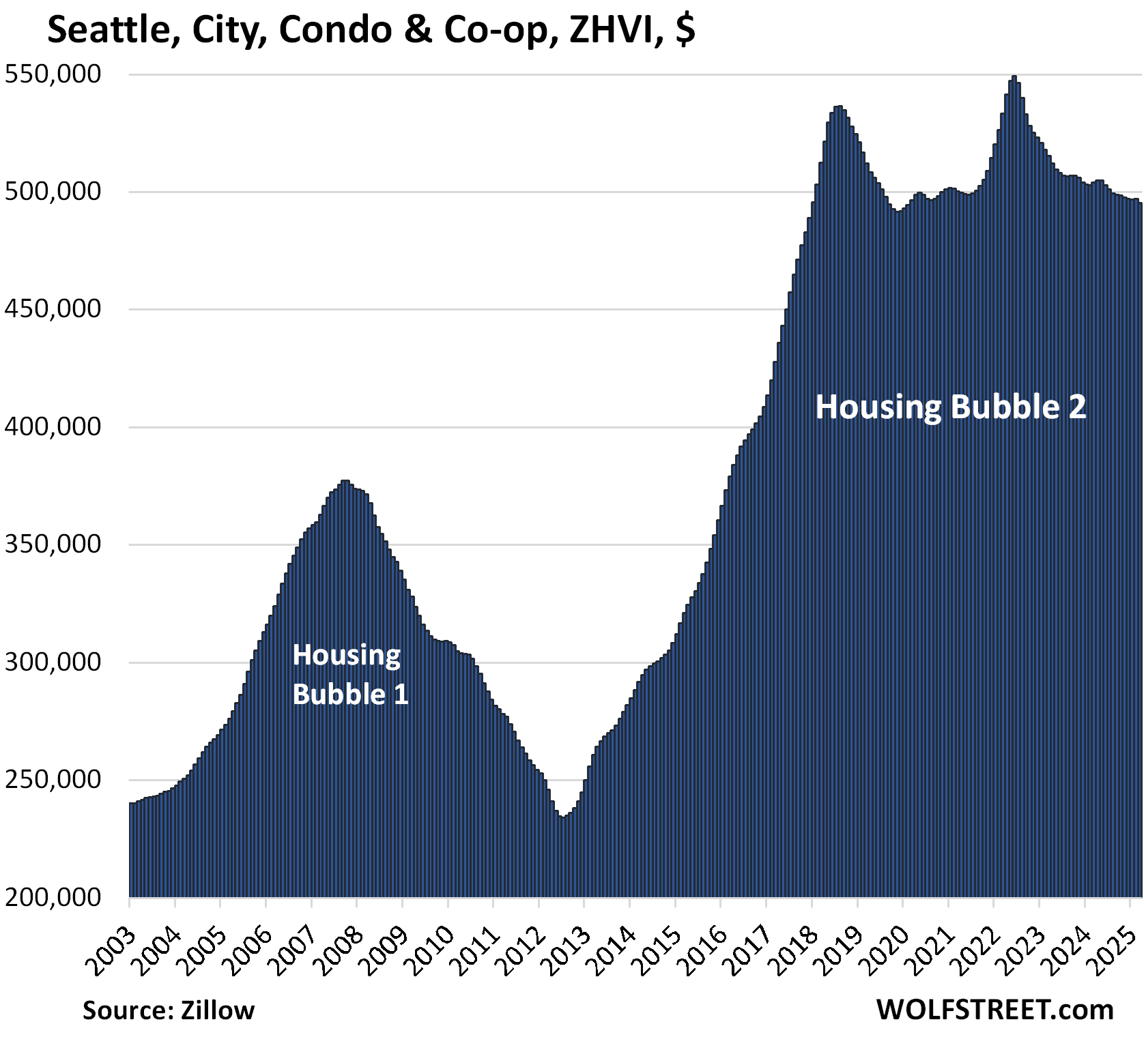

| Seattle, City Condo Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -10% | -0.4% | -1.7% | 147% |

Back to early 2018.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Tesla revenue down 20 percent. Stock goes up 10 percent today (counting regular and after market hours). When does that absurdity come unglued?

Because Musk said he’ll return to his day job and run Tesla, and will step back from DOGE. And Tesla shareholders are believers in Musk.

Musk running DOGE was a bad deal for Tesla.

So how the heck is your comment related to condos?? Just because you’re pissed off??? You’re trying to hijack the comments!!

“And Tesla shareholders are believes in Musk” – You gotta give it to the power of a cult……the chosen messiah is back so better buy the dip now before stock back to the moon.

Americans do have short term memory, so this is probably not as far fetch and the cultist might be onto something if their messiah is back to working FT at Tesla..

Anyway, back on topic, crossing my fingers, hopefully one day will see Orange county and more cities in SoCal make this list..

Found the lunatic. +3 points

This comment is related to condos because I’m typing it from my condo. 😊

“Because Musk said he’ll return to his day job and run Tesla.” Let me add an ‘I’ – and RUIN Tesla.

Also, Wall Street has to pump up Tesla bcuz that’s what they specialize in –

Shi* sandwiches. It’s what they do best.

i think musk underestimated how entrenched the status quo of government spending is and how strong the forces for it, and thus against him, would be.

i underestimated just how entrenched the “prop up stocks at all costs” movement is, among the left and the right.

I did too. It is kinda crazy to be honest. Stocks topped out at an all time high and people are screaming at a 15% pullback. Sure the tariffs caused a lot of it but ffs. If you are about to retire then why are you in equities?

Even if you are, that’s fine. Why would one liquidate their entire portfolio at the start of retirement? Taking a loss on a sale that is a small percentage of your stock portfolio shouldn’t be a big deal for prudent investors.

the coordinated effort from the media “stocks are crashing” and “401k americans’ have taken a huge hit and set people back years” is really incredible.

it’s also part of the gaslighting to make the average person think that their personal situations are enmeshed with the stock market, so that when there is a crash, extraordinary measures are justified to bail it out, when it in reality it’s just bailing out the top 1%.

Believe it or not, most Americans don’t retire rich. Millions of Americans didn’t quite make enough to be able to save a lot. And retiring with $300k in the bank with a 4% return in bonds gives them $12k to live on. And that just doesn’t cut it. For the last 30 years or so a lot of elected officials said that Social Security is communism and needs to go away and real, self-reliant Americans need to be able to save and invest their own money. Well, a lot did their best. And now they’re getting punched in the face.

“It is kinda crazy to be honest. Stocks topped out at an all time high and people are screaming at a 15% pullback.”

That’s what more-or-less 20 years of free G ZIRP heroin will get you – the deluded/demented junkie-investor.

Not only did the Fed not take the punchbowl away for years and years (and years), it went out of its way to spike it with LSD.

Kent, what are you talking about? Seriously. The stock market goes up and down on whims all the time. It had a huge drawback from 2022-2023 and the media was silent.

Then you go into an inane rant about SS. SS will probably not be around for people my age and younger unless it is significantly reformed.

kent, with all due respect, wth are you talking about? it’s true that most people don’t retire rich, but it’s also true that the vast, vast majority of stock is owned by the very rich.

let’s say you’re talking about someone with a modest, $750,000 portfolio. if the person started investing in 1988, it’s likely they only put a tiny fraction of that in as actual contributions. how is that $750,000 dropping to $650,000, after years of undeserved asset bubbling, “getting punched in the face?” the absurd hyperbole from the media and average people is how the american people are being gaslit.

eric, social security will be around a long time. what the dollars paid out in benefits will be able to buy, however, is another story.

DM: Trump has ‘no intention of firing’ Fed chair Jerome Powell

Despite tearing into the Fed chair for days, President Trump told reporters he has ‘no intention’ of firing Jerome Powell. He still made another appeal for Powell to cut interest rates.

Setting the table for a scapegoat always make sense. Doesn’t have to be logical, just served up. Your average person might believe that not lowering interest rates is causing inflation. Not here of course.

more like he doesn’t have the legal ability to fire him, and he knows it.

this way, he gets to act magnanimous, but it doesn’t actually cost him anything.

Legality is very fluid concept now a days.

And you believe what Trump says?

And you believe anything the MSM says about anything?

It is possible to simultaneously believe that Trump is a moron douce-bag and that the MSM has spent decades more or less deceiving the mass of people (mainly through lies of omission, half truths, and biased presentations).

For instance, for all the hysterical screaming about Federal employee and contractor layoffs – how much discussion was there about end-result employment levels relative to, say, the neolithic…2019?

The exact same analysis can be run for *any* G spending program…compare it to the spending level of just a few years/decades earlier – when the world did not cease to exist, either.

Then think, in a lifetime of watching television news, have you *ever* seen such an obvious comparison made?

Ever?

From a WSJ story yesterday about FL condo market: “After months on the market, the unit received only one offer, at $30,000 below their asking price. He and his wife pulled $210,000 out of their retirement funds to pay for the new townhome, and held on to the condo as a rental.”

Hard to believe someone would sac $200k of their retirement to avoid a $30k undersell on the price they made up in their head.

Psychology and prices are a tough combo sometimes.

I wonder if by “out of their retirement funds” they mean taxable retirement accounts. Maybe not, maybe it’s other savings or a Roth IRA. If that’s not the case though, that’s a horribly tax inefficient move. Presumably they have other taxable income they live on. Assuming they are in only the 22% bracket, the taxes on $210,000 will be $46,200. Will they need to take more funds out of the taxable retirement accounts to pay those taxes, only to incur more taxes. It’s a spiral at that point which is why it’s best to never take large lump sums from a taxable retirement accounts without considering the tax implications. Retirements can be destroyed this way.

I think this is a pretty good example of hot hand fallacy and FOMO combined…when you believe housing can and only go up, and in some case double digit every year…all caution/risk averse thinking is throw into the wind…maybe in this case into the hurricane since it’s Florida

The belief that housing can only go up is a product of deflation/recession avoidance. Recessions were allowed 40 years ago. Now they are avoided at all costs.

You can believe in the tooth fairy too, and support that with some kind of fancy theory.

Recent history is full of local markets – not the national median home purchased at the national median price that no one owns – where prices collapsed by 50% or more and didn’t recover for decades to their prior highs. I like to cite Tulsa because I used to live there during that time and bought a condo there. There was a huge housing bubble into the early 1980s, and then it popped hard and long. It took close to four decades for prices to get back to where they’d been in the early 1980s. The majority of homeowners who’d bought before the early 1980s died before that happened.

There are many local markets like that. But that’s where people actually bought homes at the local prices, and sold at local prices, not at the national median price. What homebuyers can actually experience in their local market turns your statement into complete BS.

I was just reading an article (today) on the glut of condos on the Toronto market.

Toronto is legendary for its rapidfire production of condos to live in especially in the downtown core. A buyer’s market would hurt a lot of investors who plowed their money into this “sure thing.”

The sad thing about capitalism is that underprepared people with money to burn make investments they can’t back up with logic. Only the smart money profits in the end. That’s why fools love communism and socialism; it compensates for their foolish mistakes and natures.

The counterargument is that it’s very hard if not impossible to consistently outperform market averages. That’s the business model of Vanguard and passive investing, rather than thinking stock pickers can outperform.

From that perspective, market outcomes are unpredictable, some people win and some lose, and government can soften or “regulate” the losses in ways that make society better off.

Social security is the maybe the best example of a socialist program that solves an unpredictable market outcome: how long will your body be able to produce labor that commands a wage? That’s hard to know in advance, which makes it hard to use logic to invest in ways that provide for you after you cannot produce salable labor any longer.

Yes, the Toronto condo market is getting messy too:

https://wolfstreet.com/2025/04/15/the-most-splendid-housing-bubbles-in-canada-march-2024-sales-plunge-supply-surges-overall-prices-drop-to-multi-year-lows-driven-by-toronto/

DS,

That is the my most bizarre argument I have ever seen. But I guess China is a country of fools and have no chance of success. The concept that the government can exist to ensure the economy serves the needs of society is a most insane idea. Much better to maximize profit regardless of costs.

Clearly you’ve not spent time in China if you think the economy there serves the needs of society.

China’s real estate sector has been melting down since 2021. Clearly government intervention did not ensure the economy in this case. And by the way they were also trying to maximize profit regardless of costs.

There is never a utopia and there are always issues such as the real estate sector. Deng Ziaopeng recognized the need to embrace the dominant economic model in the world to compete. That is why China considers itself a socialist country with Chinese characteristics which is not at all inconsistent with dialectical materialism. Profit is natural in any economic system as it allows to “feed” the next production cycle allow R&D and so on. The question is who the profit generally benefits and what influence those companies have over government policy. When societies ensure the economic system provides affordable healthcare, shelter, education and other core needs then it is fulfilling its purpose. Also important to consider modern industrialized China is in most of our lifetimes. What they have achieved since the revolution and especially since the late 70s is truly amazing.

I wonder why the happiest people in the world live in socialist countries?

Norway, Finland, Costa Rica… also live longer with no chance of bankruptcy from a corporate sponsored shitty American diet induced disease treated by a for profit capitalist medical system.

Yay unrestrained crony capitalism :-)

I know it’s harder to become filthy rich and YOLO your life away in those places.

Finland and Norway have not met the definition of “socialist” in decades. They have free market systems that put the U.S. to shame.

While not socialist the government owns 1/3 of the wealth and 90% of people are in a union in Finland.

Thanks WR for this report.

Good to see Chula Vista, one of the city in San Diego County. So far, San Diego/So Cal, had been standing tall but this breaks that myth.

We have long way to go on this.

How do you plug holes in the Hoover Dam?

Silly putty? Super glue? Clay? Sticks and Stones?

Does it really matter? The dam is going to break. First it’s condos. That’s the smoke. Soon will come the fire. A five alarm fire. It may be on the scale of LA, but on a nationwide scale. ‘Firemen’ will be useless hood ornaments for this fire. Get ready folks, the upcoming housing fire willmleave many homeless.

Lol no it won’t.

There is a NY Times article today on the Florida condo market .

Ties in nicely with this post.

I can clearly see the accelerated declines . No shortage of housing anymore and now deportations high mtg rates and competition from new apartment rentals . Condos used to be the item that one could pic up bargains for actual living in them . I don’t like seeing deflation but the 2.5 trillion roll off has an effect for sure

I do like seeing deflation, and it got really tiresome to have the government propping up housing and asset prices for the benefit of some. We had over a decade of that garbage and I’m not sad to see it end.

I wonder what the market is doing for condos in Rockies. Hoa assessments have sky rocketed due to wild fire risk and values. People own 2nd or 3rd homes and their is a huge air BNB market.

I don’t see any of this asset value crunch as a bad thing if that means more housing for people who actually live in the area

There’s a sizable population of “welfare rich” in this country who feel entitled to ever-rising asset and housing prices that they’ve done nothing personally to earn. This has been backstopped by the Fed & massive deficit spending, making it a huge burden on the rest of us. I don’t feel the least bit sad to see the air start to go out of this bubble.

My feelings as well, but “muh” 401k

The FED can buy a variety of assets. “Section 14 of the Act, titled “Open-Market Operations,” enumerates several categories of assets the Fed “shall have power” to buy—they actually extend beyond U.S. treasuries and agencies to include assets like gold, state and local government bonds, and foreign exchange—and equities is not among them.”

Buying MBS securities obviously stoked housing prices. It was a deliberate policy mistake. Letting them run off should help reverse the process.

My sister finally sold her furnished 2b2b condo in Volusia County Fl after a year of price reductions. She took it down from $495k to $375k when it sold. HOA is $850/mo. Fortunately she didn’t buy at the peak, just missed it like I did in late 2019.

I can see how at that price it’s a solid investment and I’m conservative. Property taxes are less than 1% plus HOA is a little over $1000/mo, in a huge complex that has never suffered hurricane damage. Yes eventually it will be underwater but so will I.

Like Wolf says, there’s always a buyer for the right price.

$850/month for HOA on a condo??? That’s $10,200 per year DOWN THE TOILET. Wow.

That’s cheap.

Take a look at the fees for condos in Hawaii.

Are you homeless? If not, then you are paying property taxes and property maintenance and the funds go “down the toilet” too. HOA is mostly these expenses.

HOA’s pay property taxes? I thought only CO-OPs paid property taxes?

By solid investment I don’t mean I would invest. I’m a lifelong Californian and I thought my sister was nuts for moving to Florida, lovely as it is. I pay twice in property tax but my house isn’t going to be blown away and the worst weather I have is summer heat and 4 months of AC bills. It’s worth it to hang on by financial fingernails to stay in California, especially now.

“HOA is $850/mo.”

When house humpers tell you why renting is throwing money away…feel free to refer to this as money being thrown away just the same and worse of all instead of one landlord you have to deal with, you can get the joy of dealing with some characters on HOA that might mandate you to follow some absurd rules within the community. There’s also higher HOA than that in other areas and keep in mind HOA only goes up and never go down, even when and if the house go down in value

Another landlord is the property tax clowns. Another landlord, if you have not paid off your mortgage, is the bank you got your loan from. Another landlord is the insurance company crooks. And as you say, another landlord is the HOA. Another landlord is Mother Nature, who can destroy a flimsy house in a second with a tornado, flood, storm surge, tsunami, or hurricane (or how about a sinkhole), or those poor suckers in Florida whose condos have become structurally unsound because of corrosive salt from the ocean. She doesn’t require any direct payment, but you have to pay to protect your house or condo from her. I think I’d just as soon rent.

I have a friend in Hawaii that owns a condo and is paying $1,600/month in HOA fees. Low property tax though!

What a bargain!

whether or not $850/month is a decent deal can’t be answered without more info. does that cover all exterior insurance? maintenance of a pool and hot tub? any tennis or pickleball courts? all outside landscaping and common areas?

people who decry these fees don’t, in my experience, do a good job adding up what those costs are at any single family house.

Relevant question. HOA covered two tennis courts, large gym, pool, exterior maintenance and insurance, and garbage. The complex is walking distance to the beach, although not directly on it. My sister paid cash and I’m not sure if she had additional homeowners insurance.

thanks, that makes sense. what is really comes down to is that those fees are pretty reasonable if you want and would use those amenities, as it would cost you far more to have a pool, gym, and so forth in a single family house or to pay membership fees at a country club.

if you don’t use any of them, then yeah, the hoa fees are a waste.

Being old and set in my ways real estate taxes come to mind. Here in my little village they have gone up every year for the last five. Southern Illinois isn’t the most expensive area but every increase adds to the fall.

Ground and house are paid but each year the county gets a ransom. I remember some retirees along the Gulf Coast being unable to afford their taxes. We also own a plot of country in that area. Hope I can hold on in both areas.

Property taxes are a scam

The State of Florida has a constitutional amendment that keeps the increase in property taxes to 3% or lower (based on CPI) for homesteaded houses. The county I live in: Brevard, has a county charter amendment that says gross revenues cannot increase faster than 3% or below (based on CPI). If new revenues, mostly from new construction, exceed 3%, the County Commission must reduce the millage rate correspondingly. I bought my 3/2 house in 2001 for $138,900 and the property taxes were $1216/annum. For 2024 they were $1465. Primarily due to reduced millage rates. Government runs very lean here.

Low taxes are dependent on the Fed providing money every year when a hurricane hits. That may change this year.

how do you figure? most of the damage from the recent hurricane hits has been to private buildings and houses, which is why insurance premiums have skyrocketed.

the amounts paid to the state and local governments, which is the portion that you could more accurately say is replacing property tax revenues, were miniscule in comparison.

Along the lines pointed out by Harold, let’s not forget that laws can be changed. Government might often be incredibly inefficient, but when it wants money, it’ll get it (or print it).

This is very welcome news and I hope the trend continues.

Amen. Inflated asset value are crushing the middle class. Homeownership is out of reach for so many people.

Home ownership being out of reach for a huge subset of society will have lot of unintended consequences. The latest election is one of them.

You can’t break the social contract of work hard and prosper and expect the next generation to be happy about it. I know lots of young people that don’t care if the whole thing comes crashing down because they feel left behind.

I hope the market crash continues too along with interest rates going up as well.

Might as well throw in some huge increases in property taxes, insurance, and utilities too.

Make everyone lose money and be miserable at the same time.

I really don’t understand why some people wish financial ruin on others….. especially for owners of real estate.

golden dragon, you may not like it, but if you don’t understand it, you’re buying your head in the sand.

the vast majority of the increase in america’s “wealth” over the past 40 years has gone to the top 1%. those people then use that money and their influence in government, education and the media to try to convince people that the status quo should be maintained so that that top can take even more of the pie.

everyone else might not be able to articulate the specifics, but they know a rat when they smell one. the last election was a cry for change (whether or not the current president is the right agent for change is another question entirely). why that large group of ordinary people who have been left behind by the unmitigated greed of the top would want those top to be ruined shouldn’t be hard to understand.

And the trade wars are reaching the RE markets. The tariff threat has paralyzed C. Powell’s rate cuts, as no one knows the scope, depth or details.

So, the very thing that P. Trump wants most is now blocked by his own policy. He’s done a great job lowering inflation, especially oil and rate cuts were looking palatable. Sadly, tariffs introduce new dynamics, such as increased prices and lower demand, that can affect employment and household spending.

As lower rates favor the real estate market, there are now bigger hurdles to jump depending on the tariff policies.

The trade wars are not reaching the RE markets. The RE markets imare its own inflated bubble from loose monetary policy

We are about to reconsider and reevaluate the price elasticity of demand.

“How much demand for a product changes when the price of that product changes.

Whether a product is elastic (ratio greater than one) or inelastic (ratio less than one).

How sensitive the quantity demanded is to changes in price.

How people react to a change in the price of an item.”

And all this is before the impact of reduced number of migrants due to Trump policies (illegal and legal) flow through and affect residential demand.

So the bottom may drop out of the market.

Canada and Australia have had the opposite ‘problem’ with absurd housing prices due to unchecked immigration and construction no keeping up with demand.

I see the emergence of the vaunted Mortgage Pig double pointy ears in Seattle. The world of investing versus a roof is emerging from this lunacy. And it won’t be pretty. Peak Airbnb is here. Condos should eventually settle down to 80-90x potential rent after HOA. But that’s gonna leave a Crater.

Houses face the same cliff, as does almost any US assets. Decades of asset inflation through exorbitant privilege are facing actual operating return analysis. I feel old, reaching back to how it used to be with scarce capital.

And make no mistake, capital flight is now on the table for the first time in generations. It has been over 30 years since subprime paid 10% interest rates. Even 8 percent mortgages with our crappy wages makes profit go poof.

Welcome to the everything bubble. And the chaos of endless resources cheap, delivered just in time, ending is understandably lost on this country.

on a similar note, there’s an article on realtor.com that was just published. google “second-home buyers flocked to maine” and you’ll see it.

it basically showcases two planks of housing in modern america. first, it discusses how second home ownership has become a thing for luxury buyers and investors. this is a result of poor monetary policy and the asset bubble which has led to enormous wealth stratification. that is, many people can’t buy one, but the beneficiaries of assets can buy multiple.

the second is that people are listing to “cash out” while the market is still strong. this showcases the paradox. for years, we heard that “inventory was low” and that was the reason for high prices. but obviously most people can’t take advantage of those high prices, as a huge number list to “cash out,” then inventory is no longer low, and prices will come down.

it’ll be fascinating to see how this plays out.

In Florida, special assessments are the problem. They can’t be passed on to any new owners and must be paid off upon selling. Things are going to get a lot worse for Florida real estate.

I think/hope this is just a starting trend in the real estate market.

Yes,I know folks will be hurt but how many have been hurt by putting off families ect. due to high housing costs/not being able to keep family home inheritances due to high value and thus high property taxes/insurance ect.

To quote a line from a great movie:

“Come little brother,it’s beginning”.

Another chart column that shows “Appreciation Since 2020 or 2019” (whichever year this bubbled appreciation started) would be interesting.

Mesa Arizona! The biggest city that nobody has ever heard of. Actually bigger than Atlanta, Miami, and Kansas City. Pretty much a couple hundred square miles of Phoenix metro sprawl. The far east side can be nice. Anyway, not surprising that condos have softened. That city (like much of the Phoenix metro) is filled with dilapidated strip malls that can be torn down and replaced with condos or apartments. Plenty of supply for the anticipated 2+ million more residents to come by the 2050s.

With what water? 2+ million? I hope that was sarcasm.

The bedrock of capitalism is the combination of the competitive mechanism and relatively free trade.

The bedrock of socialism is government ownership of production and distribution.

Preserving capitalism, which is far more productive and efficient than socialism, actually requires an element of government regulation [anti-trust, honest weights and measures, fair labor standards, etc.] and a welfare state for non-competitive items like public schools, public libraries, public hospitals, public health programs and by common western standards retirement systems support. What you don’t want is monopoly or oligopoly which suffers from the same inefficiency as socialism – one producer, one distributor.

The better reasoning in a capitalist free market for a limited welfare state is that it keeps a working floor on the macro-economy. No group of citizens become a massive drag of non-consumption and non-production as occurs in nations with no widespread education systems, or as would occur if the aged simply fell off the consumer bandwagon and their children stayed home to care for them.

The difference between theory and practice? Well, the economy is a moving target and politicians are peculiarly inept at playing favorites [think “Biden and Rivian” or “Trump and Big Oil”, or regulatory capture in general].

Keeping the Federal Reserve Bank independent has been and should remain a priority.

[steps down from soapbox].

No, Bernanke censored the FED’s technical staff. The FED’s polices should be open to both internal and external criticism. The FED’s Ph.Ds. used to be men of letters.

7:14 AM 4/23/2025

Dow 40,266.24 +1,079.26 2.75%

S&P 500 5,455.16 +167.40 3.17%

Nasdaq 16,957.56 +657.14 4.03%

VIX 28.00 -2.57 -8.41%

Gold 3,275.40 -144.00 -4.21%

Oil 63.39 -0.92 -1.43%

I’m convinced that nothing can kill this market. Maybe this time really is different.

Short sales could kill real-estate.

it’s not really surprising when you look at the full court press from wall street and the media over a piddling correction.

Pair this up with Wolf’s article on yields the other day and it seems obvious return to the 2022 peak is not coming anytime soon. QE era has ended (hopefully) and money actually costs something now. There is a better chance of landing back in the 2019 price area for some metro’s perhaps and at least in Toronto where I’m from.