The aggressive Bash-Down by the White House of long-term Treasury yields and the dollar since January worked. Until it didn’t.

By Wolf Richter for WOLF STREET.

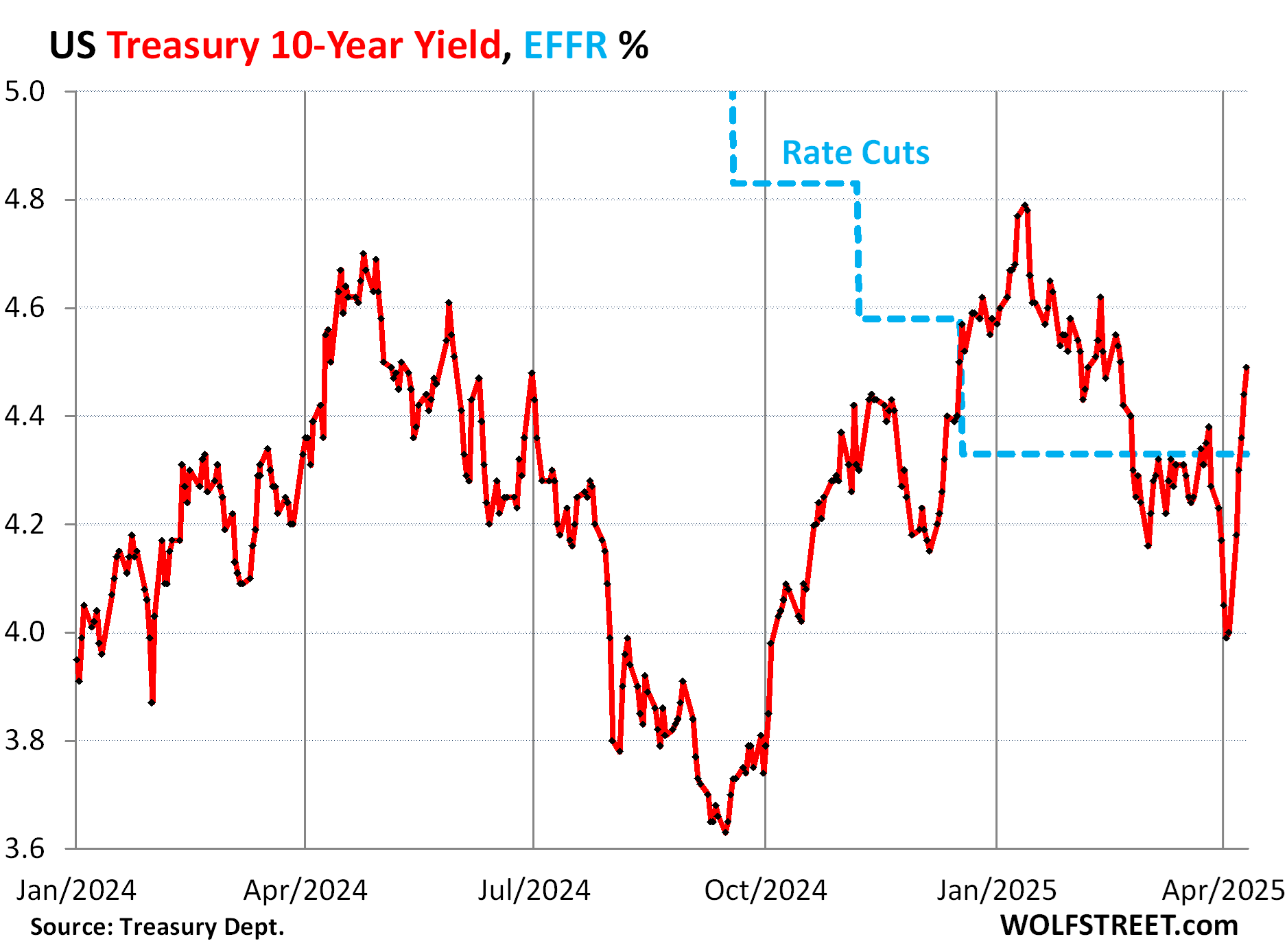

The 10-year Treasury yield rose to 4.49% on Friday, back where it had been on February 20. It has snapped back by 50 basis points from the recent low on April 3 of 3.99%, after a hard plunge.

By comparison: Starting in mid-September, the 10-year Treasury yield surged by 116 basis points to 4.79% on January 10, 2025, and there was no talk of an impending catastrophe. But now that the 10-year yield has risen by only 50 basis points, to only 4.49%, and is once again barely above the effective federal funds rate (blue in the chart below), the media – pushed by the crybabies on Wall Street – is generating piles of scary headlines about an impending catastrophe?

Starting in January, Treasury Secretary Scott Bessent began actively bashing down long-term Treasury Yields and the dollar. Lower long-term yields would translate into lower funding costs for the US economy. And a weaker dollar would boost the economy by favoring exports (a positive in GDP) over imports (a negative in GDP). This was the explicit two-pronged effort by the White House to give the economy a boost. And the bash-down worked. Until it didn’t.

The bash-down caused the 10-year Treasury yield to careen down 80 basis points, from its recent high on January 10 of 4.79% to 3.99% on April 3. That was a lot very fast.

But there was an issue with this bash-down of the yield: Inflation is sticking around, and may be accelerating further, and the Fed is worrying about higher inflation rates going forward based on the tariffs, and is worrying that this inflation might become “persistent.” Future inflation rates might be in the 3% range or higher. The long-term Treasury market fears out-of-whack inflation more than anything.

But amid the bash-down, the 10-year Treasury yield went from 4.79% in January, which was already somewhat unappetizing in this inflationary environment, to 3.99% on April 3, which was outright gross in this inflationary environment. And investors lost interest at these low yields. Yields had to shoot up to where the buyers were, and so the 10-year yield snapped back after having been push down too far, and on Friday closed at 4.49%.

That higher yield brought out demand, including foreign demand.

At the 10-year Treasury auction on Wednesday, there was very strong demand from indirect bidders, which include foreign buyers, including foreign central banks. The auction was described as “stellar.” The $39 billion in notes were sold at a yield of 4.435%.

Then on Thursday, there was the “stellar” 30-year Treasury auction, where $22 billion in 30-year bonds were sold at a yield of 4.813%, amid very strong demand from indirect bidders which include foreign investors.

So the White-House bash-down of the 10-year Treasury yield worked until it didn’t, as the market ran out of investors that want to commit funds for 10-years at 4%. But at the current yields, investors scrambled to buy at the auctions.

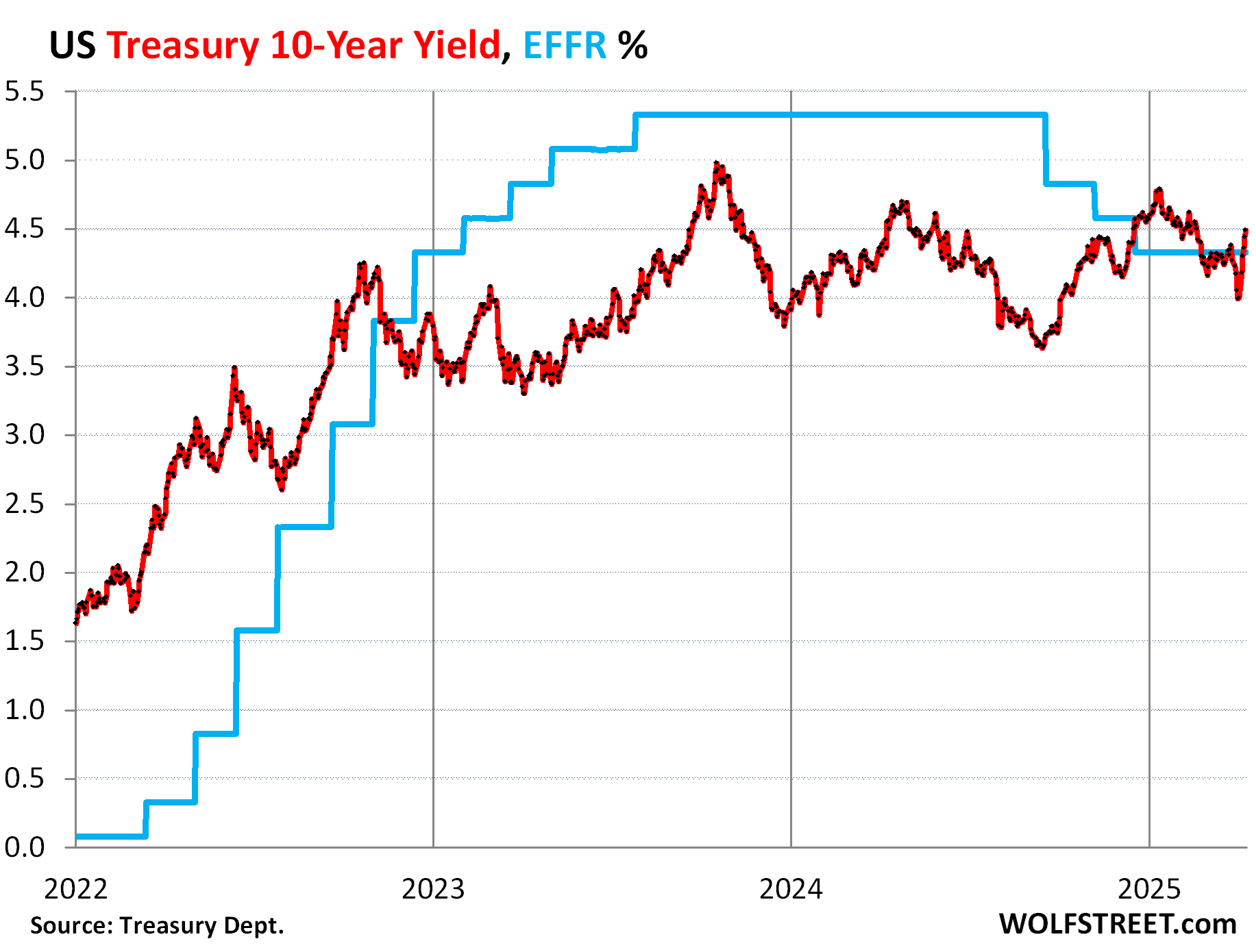

The longer view going back to 2022 shows just how funny the fretting in the media and by the Wall Street crybabies is:

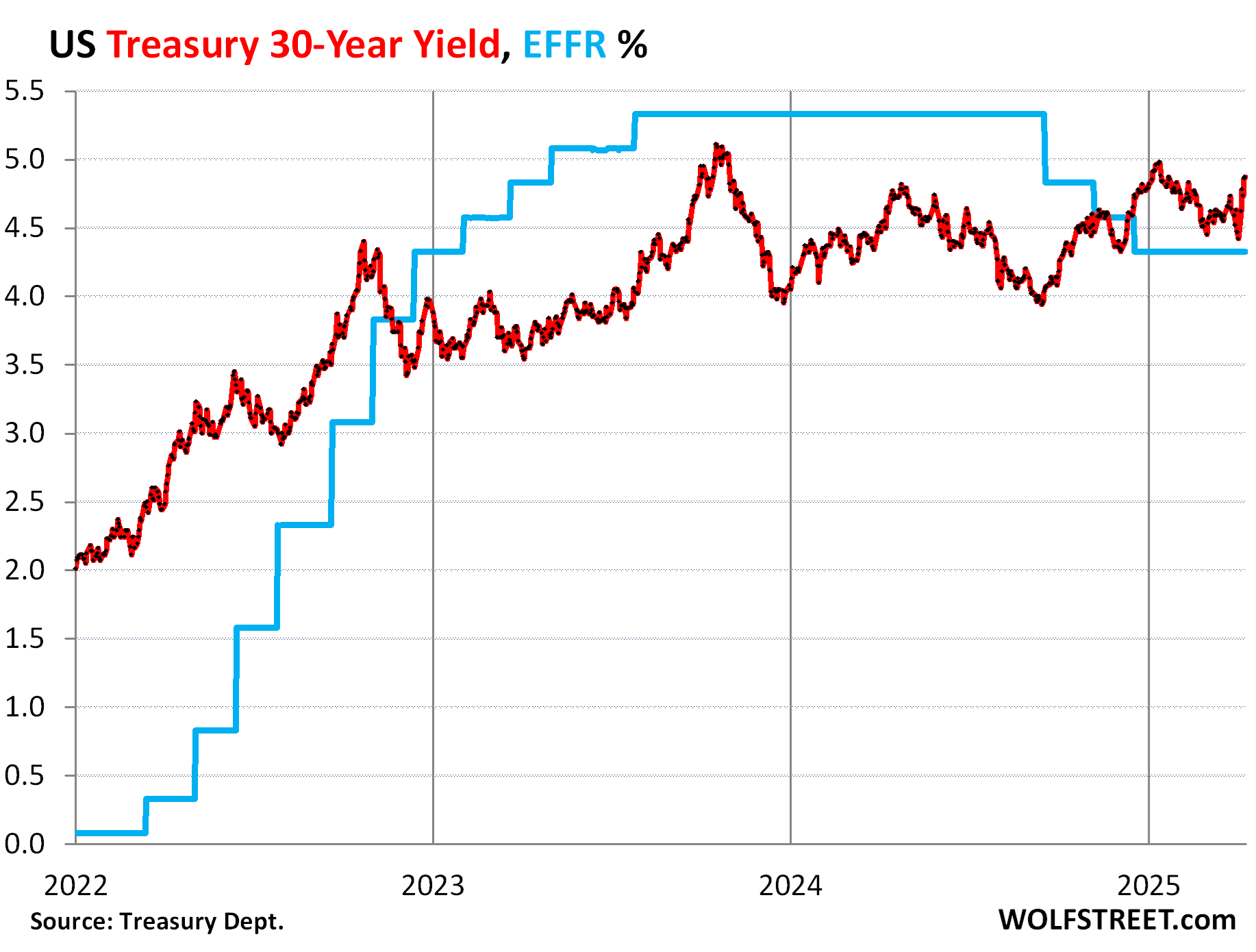

The 30-year Treasury yield closed at 4.87% on Friday, back where it had been on January 31, and below the near 5%-rate on January 10, and well below the 5%-plus range where it had been in October 2023.

It has traded in a fairly narrow range since mid-2023, and the recent snap-back from the drop, when seen over this time frame, wasn’t much to write home about.

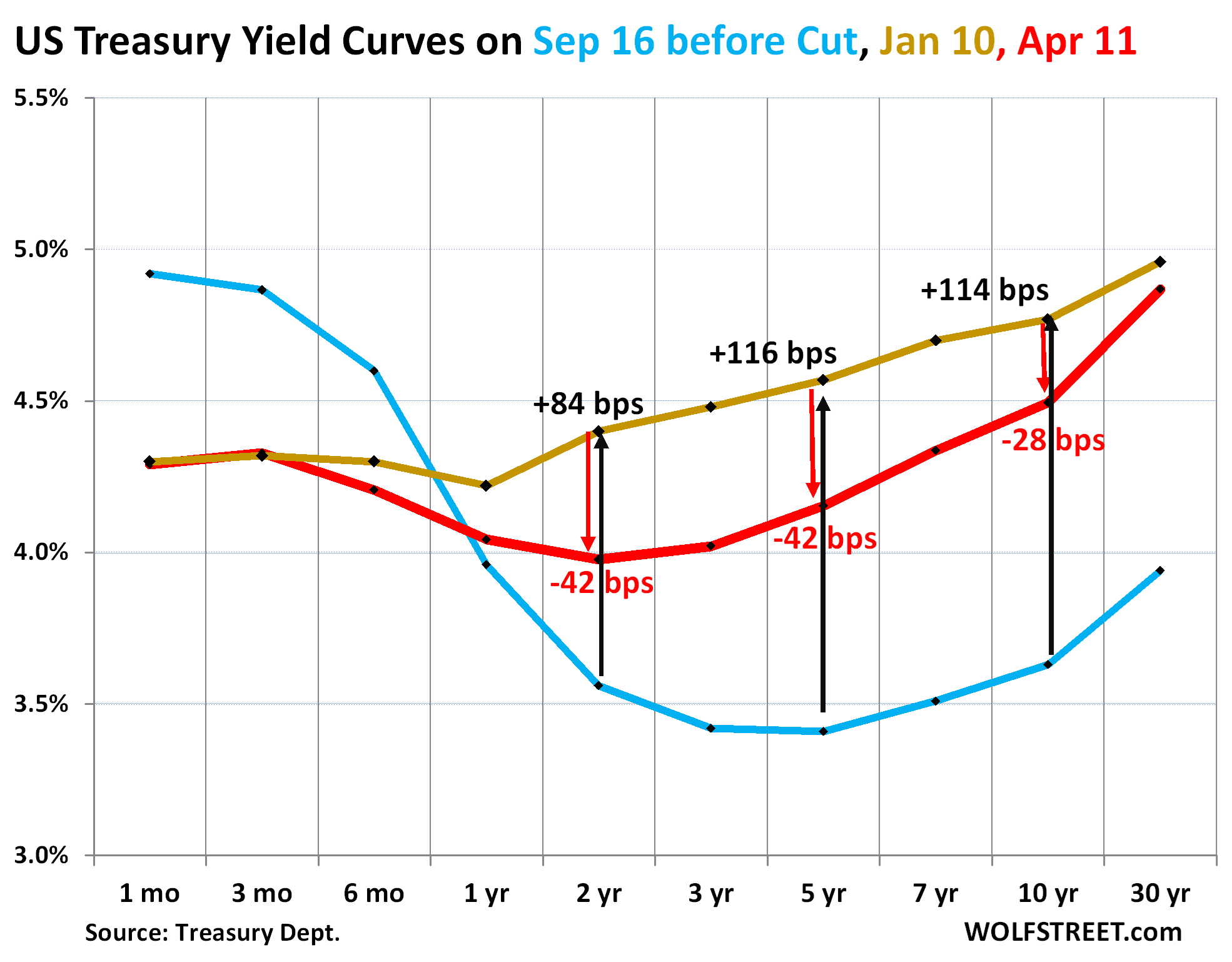

Yield curve re-un-inverted, still with a sag in the middle.

The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Gold: January 10, 2025, just before the Fed officially pivoted to wait-and-see.

- Red: April 11, 2025.

- Blue: September 16, 2024, just before the Fed’s rate cuts started.

Rate cuts are on ice, and so short-term yields haven’t moved much and remain glued to the EFFR.

Longer-term yields have snapped back from the recent lows, but are still lower than on January 10.

As a result, yields of 7 years and longer are now once again higher than short-term yields, and that part of the yield curve has re-un-inverted. But there is still this sag in the middle, though it is shallower than it was two weeks ago.

In a Treasury market that doesn’t get aggressively bashed down by the White House, longer-term yields in this inflationary environment should be higher than they’re now. A 10-year yield of about 5% and a 30-year yield north of that would look about right, in my view.

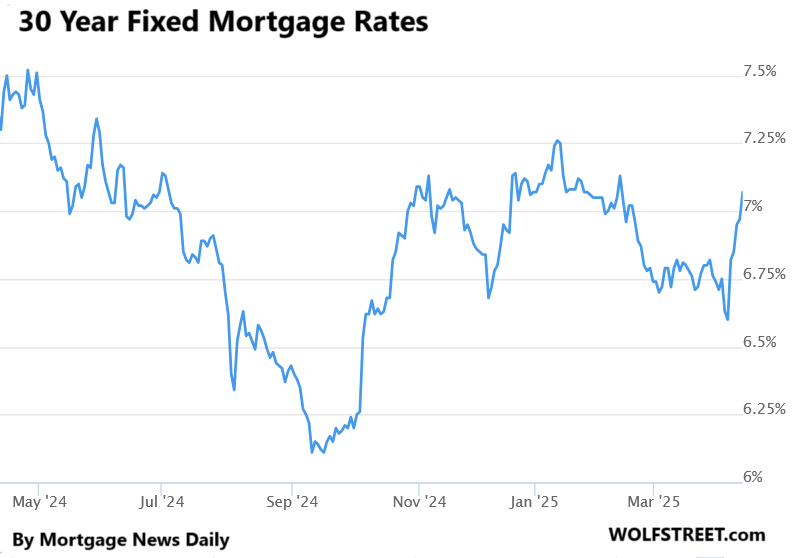

Mortgage rates are back over 7%.

The 30-year fixed mortgage rate roughly tracks the 10-year Treasury yield, but is higher, and that spread between the two varies.

Following the White-House interest-rate bash-down, mortgage rates fell with the 10-year yield, and now they too snapped back.

The average 30-year fixed mortgage rate on Friday rose to 7.07%, according to the daily measure by Mortgage News Daily. In the era before QE started, 7% mortgage rates were at the low end. In today’s inflationary environment, 7%-plus mortgage rates are somewhere close to reasonable.

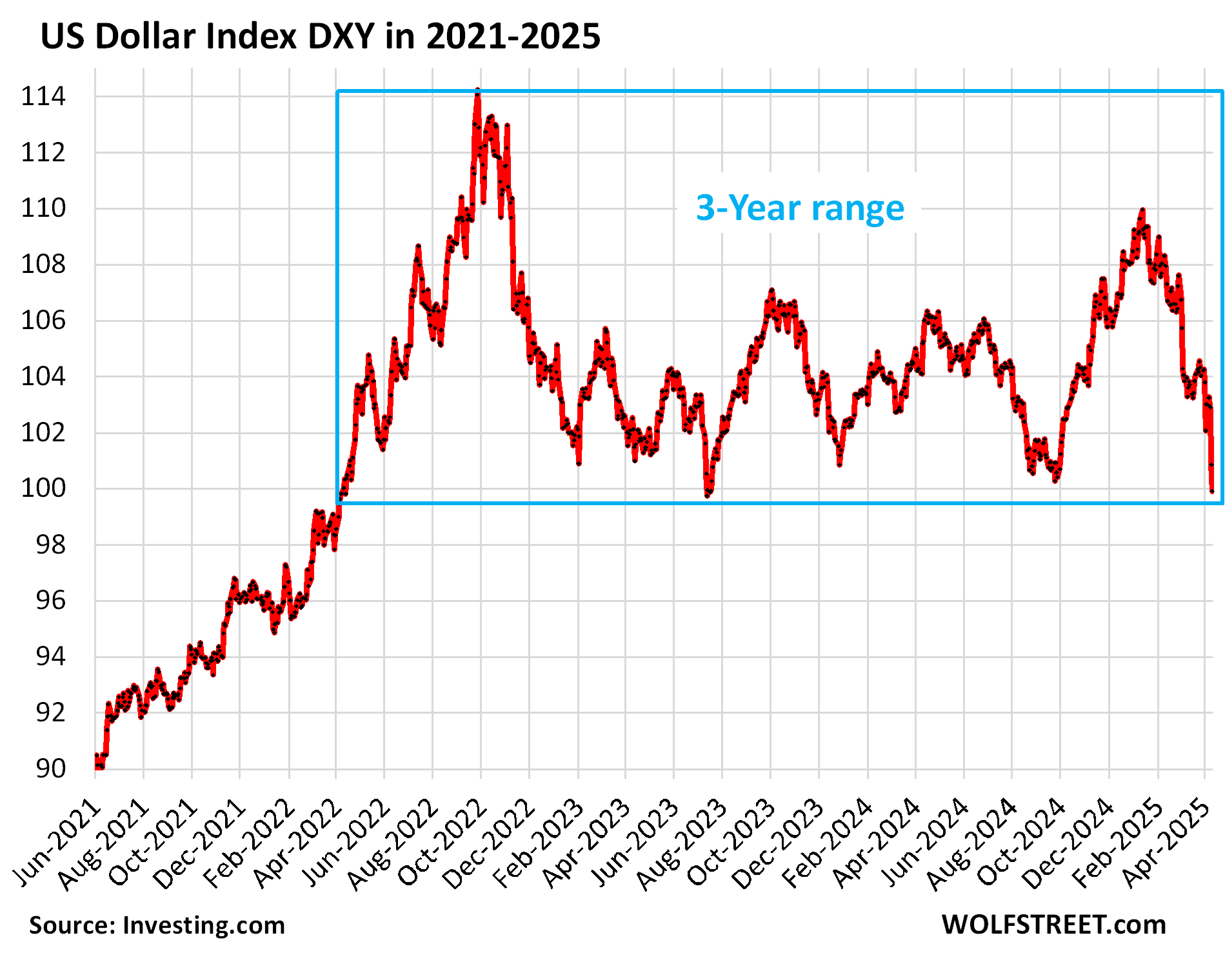

The dollar bash-down.

The White-House bash-down of the dollar was also very effective, but unlike the 10-year Treasury yield, the dollar hasn’t snapped back yet. Though it will sooner or later.

The dollar remains in its 3-year trading range and is higher than it was before that trading range. I had a little bit of fun on Friday with the catastrophist handwringing in the media over the dollar: OMG the Dollar Is Collapsing, or Whatever.

The dollar index [DXY], representing a basket of six currencies dominated by the euro and yen, dropped from 110 in January to 99.78 on Friday. But that drop was a lot smaller than the drop in 2022, and a lot smaller than prior drops, after which the dollar always bounced back. There were many years when the DXY was below 80. And at the current level, the dollar is still relatively high compared to where it had been in the prior 50 years. My article also includes a chart going back to the 1970s.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Any suggestion that a “basis trade” in treasuries and treasury futures might cause some sort of wider contain in the hedge funds, the treasury market, or the banks?

I frankly don’t see how it could, but this is being widely reported; then again, I only sort of understand how this is supposed to work.

The Basis Trade is always causing the next financial crisis or whatever. Back in Aug-Nov 2023, when the 10-year yield hit eventually 5%, there was a HUGE amount of talk about the Basis Trade, and even the Fed released a report about it. And nothing happened. Now we’re just at 4.5%, and the Basis Trade is going to blow up the world? It’s just like the dollar-collapse stuff.

You’re the best Wolf, thanks for your great perspective, and for making the topic of bond yields so funny and enjoyable 😄

I think that the concept of a risk premium as a component of the rational hypothesis of the interest rate structure:

i = Fed rate + inflation + the risk premium.

has suddenly become relevant. As the financial hot air supporting the asset bubbles cools, overvalued investments become risky.

The bond vigalantes are much smarter than Bessent et al

I respectfully disagree. The urban legend that there was an organized group of fixed income managers that disciplined the Fed is, on it’s face, demonstrably absurd.

Bond managers react to the Fed’s intention.

The bond vigilantes weren’t fighting the Fed. The Fed had already cut interest rates back then, by a lot. But the bond vigilantes (bond fund managers) refused to buy Treasury securities at lower yields, and so yields were far above the Fed’s policy rates, and even further above inflation, and borrowing by the government was very expensive. The reason these bond fund managers were reluctant to buy Treasuries was that they had spent 10 years getting beaten over the head by rising interest rates, soaring inflation, and plunging bond prices. They got bloodied from the early 1970s through the early 1980s, and when inflation and the Fed’s policy rates were falling, they said, we don’t believe in this scenario, we want to be paid lots of interest to take those risks. For the government, this was a scary scenario because demand for its bonds was so low that they had to offer this higher interest rates. This lasted for about a decade.

Sounds an awful lot like a “buyer’s strike.”

Yes, that’s what it was.

Thank you, dang — that ridiculous “bond vigilantes” trope needs to just go away and die.

LOL to all the people that listened to their RE agents on date the rate and married the price or you can just refinance to much lower rates because for sure it will come down very soon, so don’t mind that you are stretching on paying for mortgage now, lower rates are on the way to give you some breathing room..

Some of us have 2.69% 30 year fixed rates 😂😜

Difference this time than 2022 is this chaos was self induced.

As long as you don’t have to sell to someone facing a 7.2 pct new loan.

Just an aside, you can invest half the price you paid for your home in 30 year treasuries and the dividend will cover the mortgage payment. You essentially own the home.

The yield on 10 year US Treasuries should already be well above 10% given the huge amount of uncertainty and risk.

I wish….

However, I think it may take baby steps.

Every time this administration does something more stupid, it gets us closer.

In the meantime, I’m Tbiilling and chilling

Given the rate of stupidity, I think we’ll be at 10% by Fall.

“(Electronics are) exempt from the reciprocal tariffs, but they’re included in the semiconductor tariffs, which are coming in probably a month or two,” Lutnick told ABC News’ “This Week” anchor Jonathan Karl on Sunday.

Which makes you wonder if he knows if electronics are made of semis? Or is the idea that semis ( which begins with the simplest, the diode, but these days tends to mean chips) not yet in products will be tariffed but stuff using them won’t be?

New parlour game: figuring out what the WH press releases mean.

For at least Once, I agree with your opinion SCBD!

Other times far damn shore, and appreciate your posting Some of the updates you do.

Thank you,

The 10 year treasury is the least risky financial asset in the world.

The question I struggle with on whether to commit my hard earned dollars as an investment of 10 year treasuries is the risk that rates will increase from the current puny rate of 4.5 pct.

All the while, the dark cloud of recession, looms on the horizon. With the Fed prescribing QE again as the anti-dote too potential regression to the mean.

“The 10 year treasury is the least risky financial asset in the world.”

In terms of credit risk, yes. But not in terms of interest rate risk. If interest rates rise from here, 10-year Treasury prices will drop if you sell them before maturity.

“yield on 10 year US Treasuries should already be well above 10% given the huge amount of uncertainty and risk.”

The US macro economy/intl competitive advantage has been (slowly?) rotting away for 50 years.

So, long, long ago, US interest rates should have ascended and continued to ascend so long as the underpinnings of the US economy continued to deteriorate.

But the Fed/DC has aggressively intervened time and time again to obscure that fundamental economic reality (without remotely addressing the causative factors).

So needed changes/reforms in both the private sector and (especially) the public sector have been aborted – over and over and over.

That has suited/profited vested interests.

And pretty much ruined the country,

It is like the Fed’s actual job has been to actively obscure market signals – for decades.

And you said the price of gold should be $20….

Even the big investment outfits are now calling for $4500 gold.

The price of gold over the long term is going to keep going up in terms of most currencies – in other words the value of those currencies in terms of gold is falling.

This is exactly what gold should go to reflect increased money supply and out of control deficits by many countries

Telegraph: America risks ‘moron premium’ after Trump’s tariffs chaos

The president’s erratic leadership has sent a chill through the US bond market – and rattled investors

After Liz Truss’s ill-fated mini-Budget blew up the bond market three years ago, the former prime minister was forced into an embarrassing climbdown.

As well as sacking her chancellor Kwasi Kwarteng, she also quickly unwound her package of unfunded tax cuts to keep the markets at bay.

However, despite the radical reversal, borrowing costs did not return to their old levels and Britain was left paying what was unkindly dubbed a “moron premium”.

The US is now at risk of suffering a similar fate.

The US has accumulated trillions and trillions in trade and fiscal deficits over decades.

Trump is far, far from the genius this country needs.

But he didn’t cultivate the macro cancer for 5 decades – generation after generation of “American leadership elites” did that.

Blaming Trump for a “moron premium” is like blaming (your admittedly weak) Dr. for getting lung cancer after smoking for 50 years.

Economic conservatives have been screaming about this for decades – but until pretty recently, the MSM (media oligopoly really only ended in mid 90’s at best) pretty much dictated the hallucinated “reality” that Americans lived under.

By what means did Treasury Secretary Scott Bessent actively bash down long-term Treasury Yields and the dollar?

Google it! It was all over the news, and I wrote about it too.

For example, try: Bessent lower interest rates

The admin was busy bashing down my 401k, wait does that make me a crybaby?

Only if you cry about it.

Government and Fed policies inflated your 401k to levels it should have never reached (along with the price of your home), and now your 401k deflates as some of those polices end. What’s the big deal? You had it so good with these policies for so long. If you cry about it when they end, you’re a crybaby.

The other option is to act to deal with changing market conditions?

How’s you 401k now compared to 4 months ago? Mine did nothing for nearly 2 years 2022-2023 minus dividends/contributions/CDs/bonds. Cash stashed under my mattress for 2 years would have been financially better.

I learned. Last week was the best week for my 401k perhaps ever. Hoping for more bargains soon before this thing rips up.

You’re down what, 10% from the peak, which is what prices were less than a year ago?

Everyone in your positions should be stoked for a selloff. That means your monthly contribution is buying in at a LOWER price. ALL you should care about is the value when you’re taking distributions. Until then, the lower the better!

Chrisco

Wait till it turns into a 201K or 101K.Then you will really have something to cry about

Deregulation and improved fiscal policies. Not relying on the FED.

That’s literally what we need, and while it may have contributed to the short-lived recent drop, it is a long term play. Full support.

Seriously, the FED can’t be trusted during administrations it supports, so obviously it can’t be trusted during administrations it is hostile to.

Trump’s capitulation to big US tech. companies, allowing tech. imports from China to be tariff-free, will do nothing to hold down inflation or improve the trade balance or earn revenue to offset tax cuts.

We seem to be back at square one, where the Fed cannot cut rates because of inflation and the bond market will demand a higher return for a higher risk from soaring deficits.

“Back at”? We never left. The FED didn’t drop rates last fall to spur a low inflation economy….the FED never even got close to achieving their 2% max rate. Their rate cuts were for an entirely different purpose. We all know it. Go ahead, say it.

Howdy graphic. The exemption was already figured in at the beginning. US can not do without semi conductors militarily or much else. Hopefully we will really start making our own stuff and China can ______off.

Hi D-F-B. There is a quote from Apple’s Tim Cook in 2017: “In the U.S., you could have a meeting of tooling engineers in a room that’s not very large. In China, you could fill multiple football fields.”

Thar’s your problem.

That’s EXACTLY why we need big-fat tariffs that change the math for Apple to locate production to the US.

Cook has been on the forefront of the destruction of high-tech manufacturing in the US through his relentless search for cheap, to increase profit margins a little and to use this cash (and borrowed money) to pump up the share price with share buybacks. After 25 years of destroying US manufacturing and everything that goes with it – including infrastructure, knowhow, engineers, etc. – this gangster then complains that you can’t manufacture in the US? Give me a break.

There is a more nefarious side to Apple’s strategy to manufacture in China: In 2013, Apple got caught up in a Senate investigation in how it keeps its profits in Ireland on products that are made in China and sold in the US. It manufactures in China, routs its IP through Ireland, takes its IP profits there (to pay the low corporate tax rate in Ireland) and sells the iPhone at cost in the US, without generating a profit, thereby dodging US income taxes. Apple is one of the reasons why the US has the huge $87 billion trade deficit with tiny Ireland. And it looked like Apple would be in deep trouble when the Senate investigation results came out. But no, Cook schmoozed and lobbied his way out of it because we have the best Congress Money Can Buy. Apple should have at least a 50% tariff on anything it imports from anywhere. That will stop much of the bullshit it constantly pulls.

Thank you Wolf — that needed to be said. And Apple is far from the only offender.

AGREE TOTALLY with the Wolfster on this subject, in particular to Apple, and in general to all the paid political puppets/SOBs claiming patriotism while sending good USA jobs outside of USA for bribes and excess profits…

Both ”sides of the aisle” are guilty as hell far damn shore,,, and should be regarded that way by every current and former USA worker who has lost their job due to the greed of the politicians and oligarchs who have done this to us…

Including the FRB, doing nothing other than word salad for the workers actually making and doing ,, while protecting the banksters/oligarchs as the FRB was started to do and has done..

…interesting how ‘team (Party) loyalty’ has become more important than a well-played game on a level field (too-many casual spectators, perhaps?)…

may we all find a better day.

Relief for fabulously wealthy companies selling into the American market with zero manufacturing in the US and minimizes it’s taxes by hiding it’s income offshore.

Just the kind of red, white, and blue company we should give a pass too. A corporate deadbeat given carte blanche.

Exactly — it needs to be stopped.

Thank you for the article, and for the website. I’m so glad you’re showing contempt for the panic-mongers in the media, online and practically everywhere else. (I particularly loved “OMG, The Dollar Is Collapsing, or Whatever”. Pure Wolf! LOL)

Your completely rational, earlier article on what tariffs generally do, and don’t do, to prices (“Stocks Plunge As The Markets Understood What Tariffs Are: A Tax On Corporate Profit Margins”), was apparently spammed so hard, that you needed to close down the comments (first time ever?). Meanwhile, YouTube and all the socials are being targeted, systematically, by strange new accounts preaching in unison the same doom and gloom, often using the exact same terminology. The media, as mentioned in this and previous articles (and very similar to what they did during the COVID scare, etc.) acts a certain way for one team, and a completely different, almost hysterical way when another takes power.

Its obvious we’re being seriously manipulated by panic-stoking troll armies, both foreign and domestic, and by panic-stoking, blatantly biased corporate media. But not here. And for that, I sincerely thank you for keeping this space panic-and-BS-mongering-free.

But Trump admin doing an immediate softening on tariffs, after talking real tough, means nothing, everyone is is just overreacting. OK.

Did exactly the same thing in 2018. Lots of blustery announcements, then walk-backs, exemptions for specific products, carve-outs for specific companies, reductions, negotiations… it took till the end of 2018 to finalize the new tariffs, and they were a lot more limited and lower than what had been announced. But those did stick, and Biden largely kept them in place.

There is a HUGE amount of resistance against tariffs from the Wall Street goons and Corporate America because tariffs hurt their profit margins and personal wealth. And that resistance includes spreading manipulative lies and bullshit via the media to scare the bejesus out of everyone. If the White House moves slowly and timidly, trying not to upset anyone, it will never get a single tariff passed.

^^^^ This.

How many times has the finance world been on an imminent path to destruction over the last decades? And how many times did the world end? While this COULD be a disaster, odds are it is grossly oversold to us.

That said, equities are taking this maturely, and looking through a lot of this nonsense, not taking it fully seriously. Otherwise stocks would be down 30% or more by now.

Respectfully,

“If the White House moves slowly and timidly, trying not to upset anyone, it will never get a single tariff passed.”

“Passed” suggesting any else (like Congress, per the Constitution) would have any say? Trump is unilaterally doing this by his absolute personal (executive order) fiat under a declaration of national emergency under IEEPA. He does not not to “pass” it by anyone, unless the courts invalidate what he is doing. A lawsuit is pending on that on earlier Canada-Mexico tariffs.

TOTALLY AGREE juicy!!!

Just exactly why I contribute every year to the Wolf Wide Wonder.

And although I continue to read, at least briefly, many other websites that include at least some economic reporting, it is more in the vein of, “Keep your friends close and your enemies closer,” than respecting what those sites say.

This from an always independent and Always voter, although sometimes register to vote in primaries of one of the so called ”parties” of our republic, which are anything but parties, as they are SO sad, and SO ”overcontrolling.”

Yeah, you can get in trouble “swimming upstream” but when the turmoil hit Wolf said prices held at the same level they were at the beginning of 2024. So don’t expect large gains every year.

That assuaged a lot of fears.

Very well said.

Yes, ty Wolf.

I agree that long bond yields were insanely low and long overdue to correct up. And that the media, as always, overreacts. But you have to admit that the pace of the increase last week was spectacular and not normal. The alignment with the tariff chaos and equity volatility is much more eyebrow raising than the gradual variability over the past few years. Only time will tell if foreign demand for US long bonds has taken a blow. Great analysis Wolf.

I would be surprised if the USG has much trouble selling USG bonds. The old reliable will pay off in dollars come hell or high water for the duration of the bond’s life.

High quality paper in a world of uncertainty. As opposed to the status of CCP issued bonds.

Especially now, their biggest customer has slapped a tariff on their honey pot. They’re busy calculating who can they sell they’re production too.

The beauty of America is our capacity to spend money we don’t have. The optimism of spirit bequeathed too us by previous generations.

Truths all around. And you’re right, there won’t be a problem selling our debt, as Wolf says, yield solves all demand problems. It’ll all get sold, but with (potential) decreased demand comes increased yields, increased cost to service the debt, increased borrowing costs for companies, and increased chances for something big to break sooner than it would otherwise…

Volatility and asymmetry are sources of legitimate concern. Yields will fall again quite soon and the dollar will rise again quite soon, presenting new challenges.

It’s the speed of the moves which implies a loss of control. The ship has listed violently to the right and so it must list violently to the left. These are moments when it becomes clear that nobody is in full control and people get understandably spooked.

What really matters is for the Fed to take a “whatever” approach to all manufactured crises. A perfect score for Powell so far.

In no world has Powell done better than any 6th grader with rudimentary math skills.

My dog would make a better FED chair.

Would Trump make a better chair?

He seems to want to direct the Fed.

‘Stop playing politics Jerome. lower rates’

In other words: ‘My inept tariff regime has scared stock markets AND the bond market, so the Fed must bail me out.’

The Fed already lowered rates, and bonds TANKED. If the Fed lowers rates further, bonds will likely tank further. Someone needs to explain that to Trump. Bessent tried, it seems, but it didn’t stick. He also explained to the world what Trump really meant: lower LONG-TERM rates. And so Bessent bashed down long-term rates, until they snapped back, which is what this article is all about.

The perfect score was in relation to this tariff tumult only and only up to now.

I’m really not sure how to assess Powell’s pandemic response but that’s not for here or now. A lower score though if that helps.

Exactly why a globally diversified portfolio is important.

The relic that has been missing from the financial markets since QE suppression of the cost of capital is volatility, the public expression of fear, when discovering the fatal risk of a concentrated bet gone wrong..

All of the panic and pandemonium — a 1/2% decline in the 10 year treasury, followed by a round-trip uptick in said rates — seems almost understandable for a market that fears recession but expects inflation.

Two results of endless fiscal and monetary jiggering are:

1. Long-term currency devaluation (aka “inflation) due to debt and money production

2. Dramatic increase in price volatility (including bond prices)

This is what “rates grinding higher” looks like…

One thing is certain, the administration didn’t do a significant walk back on on tariffs so soon after “liberation day” because they wanted to. They were forced to by something that scared them, which means that they don’t have control over the situation. Now the cat is out of the bag that the tariff initiative is on shaky ground.

Maybe SO,,, Maybe NO bill:

Puts one who has studied history in mind of attempts to ”corner the /A market” ALA JP Morgan and Hunt Brothers.

With the current situation now ”stabilizing” some what after the crashes and surges of last week or so, it’s fairly easy to see ”market manipulations” in almost every ”edict” over the last few weeks.

Will anyone go to jail as they should? Very unlikely, eh?

Having experienced some of these kinds of things, sometimes on the good side of them due to what is now called insider trading, we have been OUT of the SMs since the 1980s for this exact reason…

GOOD LUCK and God Bless all of you who continue in the casino called the SMs these days…

BillMc,

Your conclusion is nonsense.

This scenario played out exactly the same way in 2018. Lots of blustery announcements, then walk-backs, exemptions for specific products, carve-outs for specific companies, reductions, negotiations… it took till the end of 2018 to finalize the new tariffs, and they were a lot more limited and lower than what had been announced. But those did stick, and Biden largely kept them in place.

There is a HUGE amount of resistance against tariffs from the Wall Street goons and Corporate America because tariffs hurt their profit margins and personal wealth. And that resistance includes spreading manipulative lies and bullshit via the media to scare the bejesus out of everyone. If the White House moves slowly and timidly, trying not to upset anyone, it will never get a single tariff passed.

Yepp. A lot of reasoning back and forth by «experts» in the media. In the comment section elsewhere I have read the same. The stock market was set up for an inside job. Did we just see «short and distort» and «pump and dump» by presidental decree?

Perhaps.

Wolf’s analysis seems believable and probably right. Unless a black swan lands.

Monday morning can be expected to be highlighted with feigned bluster which could turn into real bluster if the market rises or concern if the market falls.

If they can keep a 10% for a few years then ratchet it up another 10% in a couple years, the tariffs policy will be extremely effective at mitigating the boneheaded globalist trade policies of the past 40 years. It can’t be done overnight.

Color me skeptical, Bobber. You’ve likely seen all the discussion about what manufacturing can and cannot return to the US for practical reasons. I wouldn’t say “extremely effective” more like “marginally effective in some sectors”. The alternative would be “extremely effective at raising prices on a boatload of goods…..”

When I was young, I worked with several mid-western manufacturing companies in small towns.

I hope they are still there, although I doubt it after 50 years.

Apparently you didn’t hear than 70 countries reached out to renegotiate their unfair trading practices.

Have you seen a list? Plus 70 (if true) of out 180 means almost 2 out of three have not responded. Is China in that list of yours? They did respond…

Buy the DXY dip! 😀

I wonder what the real deficit is. I am not talking about social security and that sillyness.

I am talking about almost total lack of attention to all levels of our infastructure.

They are looking at a local site for a data center, but there is not a highway or utility in the area that is not obsolete and in lack of repair.

The US populace is nowhere ready/willing to make the hard sacrifices needed to “unpaint” us out of this corner. And Trump made it worse by telling everyone that it would be so easy, so “beautiful” with these tariffs. Remember, he was boasting tariffs would bring in so much revenue that we could eliminate income taxes in the US?

Now tariffs did/do need some adjusting; but his approach/personality made things worse. It will take quite alot to dig out of this.

The only leg of the stool that is somewhat working is government reduction. That is so important because we have to achieve much higher productivity in the country to compete and not only does this bureacracy add to the deficit, but it adds layers of unproductive roadblocks for private industry. But again, this is going to be a long haul effort; the country is not ready to give up all its little sacred “protections”. And they are everywhere.

Here’s one to chew on: Sometime back OSHA required protective caps on exposed (vertical) rebar on constrution sites. Now there are SOME instances where this is a good idea to protect workers from impaling if they fall. These used to be very cheap rounded plastic caps and then that morphed into very heavy flat caps that literally cost $10+ a piece. That’s just the tip of the iceberg. Then city codes starting requiring this nonsense for the T-posts that are driven in the ground to support “mud fences” (another overkill in MOST situations). T-posts at chest height mind you.

Look around, open your eyes and you will find thousands of these kinds of overkill requirements and of course the governemnt bureacracy to back them up. This has to be addressed.

I don’t know about you, but I think it’s worth it to spend a few thousand dollars for a bunch of these reusable caps to prevent someone from getting impaled saving their life.

“A few thousand” here and there and soon you’re talking real money. My point is that this safety feature is overdone and is one example of making us less competitive. It’s crony capitalism to the core. You don’t think the manufacturers and sellers of these caps have had a hand in promoting their expanded use?

Here’s the reason behind the safety caps on exposed rebar:

https://archive.seattletimes.com/archive/19910519/1283969/the-amazing-story-of-justin-stiner—-boy-shuns-heights-after-surviving-fall-from-roof-that-sent-spike-through-his-heart

Seriously? A child falls of a building (one in a many million occurence) and we’re supposed to protect from that? Don’t you see how ridiculous this belief in ultimate risk reduction saps our competitiveness? In fact, most of these costs are related to “risk reduction” but in reality, the risk is very low.

Remember the tip over bracket you get and are supposed to install when you receive a new stove? Because some child (or adult) used the stove door to reach something whilst the stove top was cooking. I mean, how far do we go as a society to protect against stupidity. Better to let evolution take it’s course and cull the heard.

Mike, the reason they morphed us because they became more reusable. Their higher cost involved a better product that the contractor wanted to re-use and less prone to failure. Sorry Wolf, off subject AGAIN.

I’m sure you believe your fantastical tails even if I don’t.

‘

Where I live we cut a plastic coke bottle in half and put the bottom over the rear tip to protect it. Seems to work ok

If higher interest rates have an effect on a real estate man’s business it seems policies may change fast. Money talks, bullsht walks.

The people who didn’t care about the stock market pain, seemed to care a lot about the bond market.

Howdy Youngins. Mortgage Interest Rates at 7 %???? How will non boomers make it??? HEE HEE. Relax and NEVER move and you will be safe, ” imprisoned ” with your cheap mortgage for decades to come. You were ZIRPed by Govern ment and have no idea what Real Normal Should Be……

DFB

So, by your “logic” a homeowner who owns their home free and clear is also “imprisoned”.

Your “logic” is defective.

Howdy OSB. If you do not need a mortgage you are not a prisoner. You will benefit from the higher value of your house while exchanging it for a different one. ZIRPing still caused a Real Estate Bubble and imprisoned millions needing a new mortgage…… Hope that helps

Remember that sitcom Too Close For Comfort? Cartoonist Ted Knight and wife the owner in one of the units, the two daughters in the other, and the comedic Munro in the third unit? Seemed to work out.

Wolf how useful is the DXY without the Peso and having the Yen as the only Asian currency given the huge amount of trade with Mexico and the rest of Asia?

I think you answered your own question.

You’re completely missing the larger context of what happy last week by only staring and bond charts. What was worrisome last week was that treasuries started steeply following the market down, instead of hedging it. THAT is what made the White House backpedal. It’s not about absolute rates, as you spent 90% of this article focused on. It’s about rate of change, and direction of change, not absolute value.

Long-term treasuries followed the stock market down in 2022. That has happened frequently recently. Earlier this year, long-term Treasuries followed the market up through its ATH, and then they followed the stock market down. During the Everything Bubble through 2021, Treasuries followed the stock market up. The exception was 2018, when long-term Treasuries followed the stock market down, LOL.

We discussed here for years that long-term Treasuries no longer provide a hedge against the stock market because since QE started back in 2009, they have often risen and fallen in tandem.

NO ONE complained when they rose in tandem? But now when they again fell in tandem, it’s the end of the world?

Why is it suddenly shocking that they follow the stock market down again? Why does this ignorant BS about this being a sign of a catastrophic problem keep getting spread? What is this motivation for spreading this ignorant BS???? Cui bono? (I have two candidates for the cui bono).

Often in financial markets, it’s not the levels that cause problems but the speed at which those levels change. This latest move at the long end of the yield curve was incredibly fast. My guess is that China sold at that end, bought euros. An fu to Agent Orange’s Art of the Deal, reminding the bozos that China has a strong hand to play.

Meanwhile, we now have some level of financial chaos, consumer confidence levels that will likely lead to a recession, and protectionist tariffs to allow us to rebuild our manufacturing center, but that will go away in 90 days as 90 beautiful free trade deals are negotiate, decimating the domestic manufacturing resurgence that will supposedly happen in those 90 days. What a plan.

1. The drop in yields was nearly as fast as the jump. That’s typical of snap backs. No one complained about the massive and fast drop in yields. You didn’t either. So why complain about it when they snap back?

2. China has been unloading Treasuries for many years. While other countries have been loading up. That’s not new. I discuss this when the data is released, and I include charts so you can see.

3. Huge foreign buying at the two auctions last week (RTGDFA). Lots of bullshit in the media about foreigners selling. There is no data on this. It’s just imagination. We will get the actual data on April foreign holdings in a few months, and you will read it about it right here.

4. The 10-year yield is still very low, a lot lower than it was a few months ago, showing that there is HUGE demand for Treasuries.

So I guess you’re saying that no matter what Trump/the US does foreigners will keep buying Treasuries with gusto?…no other game in town? (LOL!!)

That’s not at all what I’m saying. Don’t put words into my mouth!!!

What I said in my comment is “what I’m saying,” not your bullshit fabrication.

“China has been unloading Treasuries for many years.”

True, but the *rate* at which they dumped Treasuries might have accelerated.

I don’t know…and it isn’t really the core of the horror show.

Basically the same people who advocated for (apparently unmonitored) globalization – and failed to course correct for 30 years (despite empirical reality) are the same worthies who claim that the Fed and its magical printing press can always save the US from soaring interest rates.

(I understand the dynamics of the premise – but I question the real world reality of that MMT-like premise…ironically a situation like globalization *theory* going off the *empirical* rails for the US…)

But when interest rates rapidly puke upward (as in last week) you have to cast a jaded eye at the magical printing press.

Where was it? If it is indeed magical…why did Trump have to 80%+ reverse course? Why couldn’t the magical printing press save the day?

Because the US is *already* in an ugly inflationary environment – printing to buy Treasuries to drop rates just makes this worse.

The core of the horror show is the macro box canyon that the US has created for itself (perpetual trade deficits as consumption refused to match deteriorating intl competitiveness and perpetual fiscal deficits to hide the former).

Given the action in Chinese financial markets including the basic non- reaction in their stock market to the tariffs and the yuan falling and recovering Id guess that the Chinese have been dumping lots of US bonds to convert to yuan.

IIRC they did the same thing during Trump 1 tariffs.

I’ll guess we’ll know in a couple of months when the data comes out for April.

Falken says WOPR is learning.

The demand for money should not be confused with the demand for loan-funds. The demand for loan-funds is not a demand for money, per se, but a demand which reflects the advantages of spending borrowed money.

Insofar as there is a relationship it may be said that an increase in the demand for loan-funds tends to be associated with a decrease in the demand for money.

The equilibrium position will of course never be reached if new and disturbing factors are being continually injected into the situation.

Spencer-

“The equilibrium position will of course never be reached if new and disturbing factors are being continually injected into the situation.”

Is “equilibrium” ever “reached?”

Aren’t “new and disturbing factors” always “injected” (some anthropomorphic and others exogenous), forever and ever without end?

Your differentiation between money as a port in a storm, and money as a tool toward consumption is insightful, though, if I’m understanding your point…

Interest rates in any given market at any given time are the result of the interaction of all the forces operating through the supply of, & the demand for – loan-funds.

Spencer-

Yes, loan-funds for consumption or capital investment.

Your comment about “interest rates in any given market at any given time” brings to mind a concept in Murray Rothbard’s writing that he called “the constellation of interest rates” (though I think he borrowed the term from Knute Wicksell or some such dead economist).

“In today’s inflationary environment, 7%-plus mortgage rates are somewhere close to reasonable.” This makes sense, but if I show that to my real estate agent wife and her friends, they will have a melt down. Conversation after a few open houses yesterday:

Agent: We’ve already dropped the price by $10K, but we haven’t had anyone put in an offer. Its the cheapest house for sale in the neighborhood. Rates have come down, they’ll keep going down so they can just refinance in about a year.

Me: If you drop the price by $40K, I bet you’ll get a few offers.

Agent: What?! That makes no sense, that house is worth way more than that. At that price it would be below the County’s appraisal.

Me: Buyers set prices, not sellers or agents. The buyers are telling you they’re not buying at this price.

Agent: It’s the rates, these damn rates are too high.

That’s when I excused myself to refill my drink.

Great post. You literally encapsulated what has been going on here for the last 2 5 years.

Apparently, none of your folks were trying to sell real estate when rates were over 10% (or higher). I know that was a long time ago, but I clearly remember my 18.5% mortgage in California.

7% is not bad. I’ll bet those potential buyers have a car note higher than that.

The difference is that current home prices do not reflect reality. Yes, homes 40 years ago had rates in the teens, but the ecomonic formulas were very different. Home prices reflected the rates at the time accordingly.

Rates came down to ridiculous levels, so prices climbed to ridiculous levels. Rates have more than doubled across the board, but sellers have been reluctant to drop prices. Agents on the other hand, have also been reluctant to give their clients a dose of reality.

For example, I was selling my motorcycle which has been HIGHLY customized for one single purpose. There isn’t a market for this type of bike where I currently live. So I priced the bike very low, understanding I would get very little interest. Not a single person from my state was interested in buying this thing. Someone from 3 states away drove here to buy it. He couldn’t believe I was selling it for that cheap.

Like Wolf had stated before, price fixes everything. For the right price, anything will sell. These homes are still asking the high prices of 2021/2022 when rates were much lower. Something has to give. After watching other markets, clearly sellers will have to give in.

If that agent thinks 7% is high, then she should love to loan the buyer that money at that rate, right? I bet not.

It’s even worse than that. This agent’s advice to interested buyers is “Rates are coming down, so you will be able to refinance in about a year.” Another carrot being dangled is the seller offering money towards a rate buy down. This is currently the most common “incentive” at the moment.

I’ve convinced my wife not to provide financial advice to her buyers, so I’ll count that as a win. Instead, she focuses on the house, the fact that most people have to live somewhere, and people’s desire to own a home. As long as they show up with a real pre-approval letter, the math behind the scenes is the someone else’s business. Slim pickings, between zero and 3 interested buyers show up at the open houses at the moment. We are in full blown spring selling season!

“Agent: It’s the rates, these damn rates are too high.”

That’s what 20 years of ZIRP cocaine yields – addiction and delusion.

All these retail level, leveraged “players” who never really understood the dynamics of valuation (how “worth” is determined)

Feels like the plan is coming together perfectly to get trust back and lower yields. More money than you can imagine is going to flow in via tariffs, DOGE and Congress will significantly cut spending, and the deficit will gradually start to shrink and inflation will return to normal. The projections that national debt will rise to 43 trillion by 2029 must be complete fabrication. China will of course never develop advanced semiconductor machines and manufacturing capabilities and ever catch up, or at least not for 5-10 years. Cue Springsteen and start dancing. Golden years ahead for sure.

Already bought my options for cocktails on a Martian golf course!

In this race to advanced manufacturing, who is most likely to reach its pinnacle and unleash Skynet?

Its neck and neck on AI, but I have no idea who’s winning the iRobot race.

I have even fewer ideas on where to invest to capitalize on our future dystopia. I’d ask Grok, Chatty-G, and Gemini what their thoughts are, but they all get skittish about predicting markets.

Seems they are smarter than us.

ABC: Commerce Secretary Lutnick says tariff exemptions for electronics are only temporary

Commerce Secretary Howard Lutnick said Sunday that the administration’s decision Friday night to exempt a range of electronic devices from tariffs implemented earlier this month was only a temporary reprieve, with the secretary announcing that those items would be subject to “semiconductor tariffs” that will likely come in “a month or two.”

“All those products are going to come under semiconductors, and they’re going to have a special focus type of tariff to make sure that those products get reshored. We need to have semiconductors, we need to have chips, and we need to have flat panels — we need to have these things made in America. We can’t be reliant on Southeast Asia for all of the things that operate for us,” Lutnick told “This Week” co-anchor Jonathan Karl.

He continued, “So what [President Donald Trump’s] doing is he’s saying they’re exempt from the reciprocal tariffs, but they’re included in the semiconductor tariffs, which are coming in probably a month or two. So these are coming soon.”

Apple is going to have a blowout quarter. In my small circle, I know four people that ran out and bought new IPhones to beat the tariffs.

I think some of them were looking for an excuse to upgrade. The tariffs provided it.

I haven’t double checked this stat that I saw, but its insanity does seem in keeping with the delusions of the age…

It has been reported that Apple basically imports 50 million of its phones to sell in the US *every year*.

With only 135 million or so US households, if that stat is remotely accurate, the level of perpetual upgrading is lunatic.

(Personally, I kinda doubt the stat – Apple is popular but it doesn’t take anywhere near 100% of the US cell phone market, so 50 million iPhone sales in the US alone – given just 135 million households – seems…off).

But a household with four people might have four iPhones. So you should look at the overall population: 340 million,

You’ve identified one of the signficant root causes of American unproductivity…….smart phones.

Yes, people are addicted to these things and demonstrate that by queing up to buy the next version with new bells and whistles.

A few school districts are finally reaching some wisdom on this issue and banning smart phones in classes and between classes. They have to go in the locker and stay there until end of day. Bravo move. Why did it take so long to realize this and take action. This is America’s liberal/technology rapture culture. And it’s killing us.

The reasons the markets are nervous as can’t really trust anything regarding tariffs. Flip flops and reversals are more the norm than not.

You all need to understand how Trump deals. He makes an initial seemingly outlandish offer/proposition/policy, sees how it plays, and then gradually lowers the terms if necessary. It’s not crazy. It’s how one makes the best deals. Most Americans are not used to this, so they think it is crazy.

I think a solid strategy that works once then everyone rolls their eyes but also has to be pragmatic. It like a friend who is giving up smoking for to he 10th time. You are thinking “yah right” but you still want to be supportive. Not like most nations can call bluff on the US. The one that really can, did

Mortgage rate of 7% is IF you have perfect credit.

Use any of the mortgages sites, put in a FICO of say 725, and rates run in the 7.5% Plus range…

It seems long term bond rates are based mainly on two factors: an economic slowdown (at which rates go down), and an increase in inflation (at which rates go up). The reverse also holds. If the odds are about even, inflation will probably win out and rates will rise. Long term bond dealers seem to hate inflation more than recession. If it looks like a serious recession with not much change in inflation, rates will go down.

The Fed will have a serious problem if we have stagflation. It might lower rates to improve employment, but that might increase inflation. It might raise rates to decrease inflation, but that might slow the economy. It might do nothing, having been burned way too often with wrong policy decisions.

Right now, I like my three month T-bills which yield almost as much as ten year Treasuries (4.336% vs. 4.497%). The twenty year at 4.941% is the only other Treasury that is interesting, but needs to be higher for me to jump on it. With three month T-bills I do have to think about what the Fed thinks. I give the Fed some credit for pretty much staying out of the tariff fight, although Powell said he thinks tariffs will increase inflation.

Wolf, what’s the latest update on “Who’s buying our debt”? Thanks!

https://wolfstreet.com/2025/03/18/who-holds-the-ballooning-us-government-debt-even-as-the-fed-and-foreign-holders-unloaded-treasury-securities-in-q4/

Meanwhile, the data for foreign holders has been released for January. We’ll have to wait a couple of months for the April data.

Without China trade, wouldn’t there be less demand for US dollar, therefore, less demand for US treasury bonds? As a result, the US bond yield will be higher relative to the same stage of the last economic cycle. China was exporting deflation to US. Now that is not happening, shouldn’t the inflation be permanently higher?

China has been unloading US Treasury securities for many years. But other countries have loaded up.

The rollout of tariffs has been a disaster. Nonsensical equations, ridiculous percentages, violating current trade agreements, adding/pausing/retracting on a dime, rationales changing minute by minute etc…

it’s been miles worse than anything in the 1st term.

I think a lot of people are questioning the stability of the US economy with this level of incompetence at the helm. Signal-gate and the “gulf of America” stuff doesn’t exactly help sell the idea that we’re in good hands.

Dan

Agreed. A disaster is putting it mildly. The whole economic team of this administration needs to be fired for this bungled rollout of the Tariffs. It has become a gigantic distraction from what were otherwise positive developments in the DOGE efforts to reduce waste fraud, and corruption in the Federal Government.

Why did muni bonds get hit so hard if there’s no truth to the basis trade blowing up? Seems like there’s stress over something.

LOL. Muni bonds had a big run over the past 12 months, for muni bonds, which are not supposed to move much. The S&P Muni Bond Index (for prices) rose by 4.4% from April 13 2024 through April 4 2025. It has now given up that 4.4% gain. The low point was Wednesday, it bounced on Thursday, and eased a little on Friday. If you look on a 10-year chart, you’ll see that this was not much of a decline, compared to the much bigger declines in in the prior years.

I’ve got a muni bond mutual fund, DMBAX. I bought most of the shares in 2011 and it hasn’t done squat since. One of the worst investments I’ve ever made. The fund managers suck.

Higher interest rates are not evidence of “tight money”; rather they are the consequence, over time, of an excessively easy (irresponsible) money policy – money expansion so great that monetary flows (MVt) substantially exceed the rate of expansion in real-output.

While interest rates are not determined by the supply of & the demand for money, changes in the volume of money & monetary flows (MVt), can alter rates of inflation &, therefore, the supply of, & the demand for – loan-funds.

The significant effects of these monetary developments are long-term & involve an alteration in inflation expectations. Inflation expectations operate principally through the supply side for loan-funds. Specifically, an expectation of higher rates of inflation will cause the supply schedules of loan-funds to decrease. That is to say, lenders will be willing to lend the same amount only at higher rates.

Under the assumption of increasing rates of inflation, the supply of loan funds would decrease in both a quantitative and schedule sense. I.e., lenders reduce the volume of loan funds offered in the markets & refuse to loan any particular volume of funds except at higher rates.

At the same time supply is decreasing, the demand for loan -funds can be expected to rise as a consequence of the expected massive increases in federal deficits. With supply decreasing & demand increasing (in the schedule sense), there was only one way for interest rates to go – up.

So much hope re Doge- let’s just put that hot mess into perspective- there will be no major savings. The 150$ billion will be a few billion by the time they are done, especially after all the necessary repairs and contract penalties are paid. It’s moronic theater. If you can prove otherwise, I would be amazed. I worked in regulation for decades in gummint, and I have seen this same moron playbook up close and personal- right up to the “savings” from “privatization” and the only winners were the cost plus contractors who gave big campaign contributions. If you believe otherwise, then stop reading- nothing I say further will make any impression on you.

International trust has just been broken, and while a lot of buyers will hit the bid for a trade, the long term trust is pffft.

Our exorbitant privilege has existed on the very stability of the post Plaza Accords system. If they can’t sell product here with tariffs on a profitable basis, then the ships stop shipping here with all that crap, and foreigners will no longer need to buy our new debt. And then we start functioning as a national debt market with huge amounts of refinancing necessary. And then we shall have to RAISE taxes on workers (SS and Medicare fix), income taxes (all the loopholes and employ more IRS workers, not less), and even keep the tariffs to plug the huuuuge revenue hole. In short, welcome to the next crisis, which was going to be gradual, and now instead will be front and center the next decade.

And people wonder about buying houses? LoL.

It’s a broken system and has taken many years of bad or non policies to arrive at the beginning of the crisis period. We are just lucky to have front row seats. A new reality will eventually settle in but not without more resistance and can kicking.

This rollout of these Tariffs, and their execution is as bad as George H W Bush’s famous quote

“Read my lips, no new taxes”

It will cause major damage to this administration and lead to a loss of Congress in 2026. It was a self inflicted wound.

I’ve already noticed a panic in some stores around here as people are stocking up on essentials ahead of the tariffs and future supply chain disruptions.

I do NOT believe the Fed will be lowering interest rates this year. I will believe it when I see it. I just checked updated CD rates in New York. Citibank raised its rate to 4.25% for 9 months. Marcus by Goldman Sachs is even a touch higher, 4.3% for 9 months, and 4.5% for 14 months. Capital One which usually offers higher CD rates than the big banks is still paying 4% for a 12 month CD. So why have Citibank and Goldman Sachs, two institutions that typically don’t give consumers ice in the winter, both jumped higher than Capital One? I see this as as “Tell” that rates are headed higher.

Look at what has been happening with stocks, which appeared ready to take a big dump last week. Even after the wild Wednesday due supposedly to the Tariff Delay (and perhaps the biggest short squeeze in history) the selling resumed Thursday. At the low on Thursday, when the SPY was $510, an April 17 $400 put option (expiring in just 7 days on Thursday since the market is closed for Good Friday) was $2.70(!!!) This volatility reflects nervousness not seen in many years. Clearly, many traders are expecting something to go very wrong.

I have not budged from my prediction that the S&P will see 4500 again, which I have had since way before the election. I feel it could go much lower, but 4500 is still my “Lock Target.”

I would be delighted to see the S&P hit 4500 and would put a fair chunk of my “dry powder” to work if it ever did.

eg-

You might consider a S&P target below 2500.

Good time to be a cash buyer.

Just got $260k off list ($1.45m) on an investment property in Florida. I’ll leverage it when rates go down. If they don’t well I’ll just collect the rents.

What’s the insurance cost?

$8k

Here we go again. It is the spring time of 1978…

…with slightly more debt…

Hedge accordingly.

No one should lend the US government money for any amount of time at less than 12%. Even then. Mortgage rates should be about 15% which would absolutely crush any hope these deluded sellers have of unloading their over priced dumps. The entire US economy needs a Mike Tyson punch in the face.

“If President Donald Trump’s large tariffs remain in place for some time, the economy is likely to slow to a crawl, Federal Reserve governor Chris Waller said Monday. As a result, interest-rate cuts would be warranted, even if the taxes on imports cause a spike in inflation.” “The risk of recession would outweigh the risk of escalating inflation,” the Fed governor said at 13:00 today. Now we know that one member of the FOMC would rather have inflation than recession. He may get both (stagflation).

Dow opens and goes up 500 at around 11:00, then gradually drops to zero change around 13:00. After Waller’s remarks at 13:00 Dow gradually climbs back to 500 up at around 15:00. I wonder if Powell would say the same thing. It seems to me Powell is much more of an inflation hawk than Waller. BTW, ten year Treasury yield is now almost the same as the three month yield.

Waller is the odd man out. He is fishing for Chairmanship. He may be dissenting in the FOMC statements.

Powell and ALL the other Fed governors have sounded hawkish due to the tariffs. Powell most recently before Congress. They’re worried about inflation from the tariffs becoming “persistent.” They have said in unison, using nearly the same terms, that they would wait and see how all this turns out. One of them even put rate hikes on the table if inflation threatens to become persistent.

“Yes, I am saying that I expect that elevated inflation would be temporary, and ‘temporary’ is another word for transitory,’”-Waller.

Well, we have all heard about “transitory” inflation from the Fed. Waller could be wanting to replace Powell (May 2026) as Wolf suggests, but he could be digging himself a deeper hole in the process.