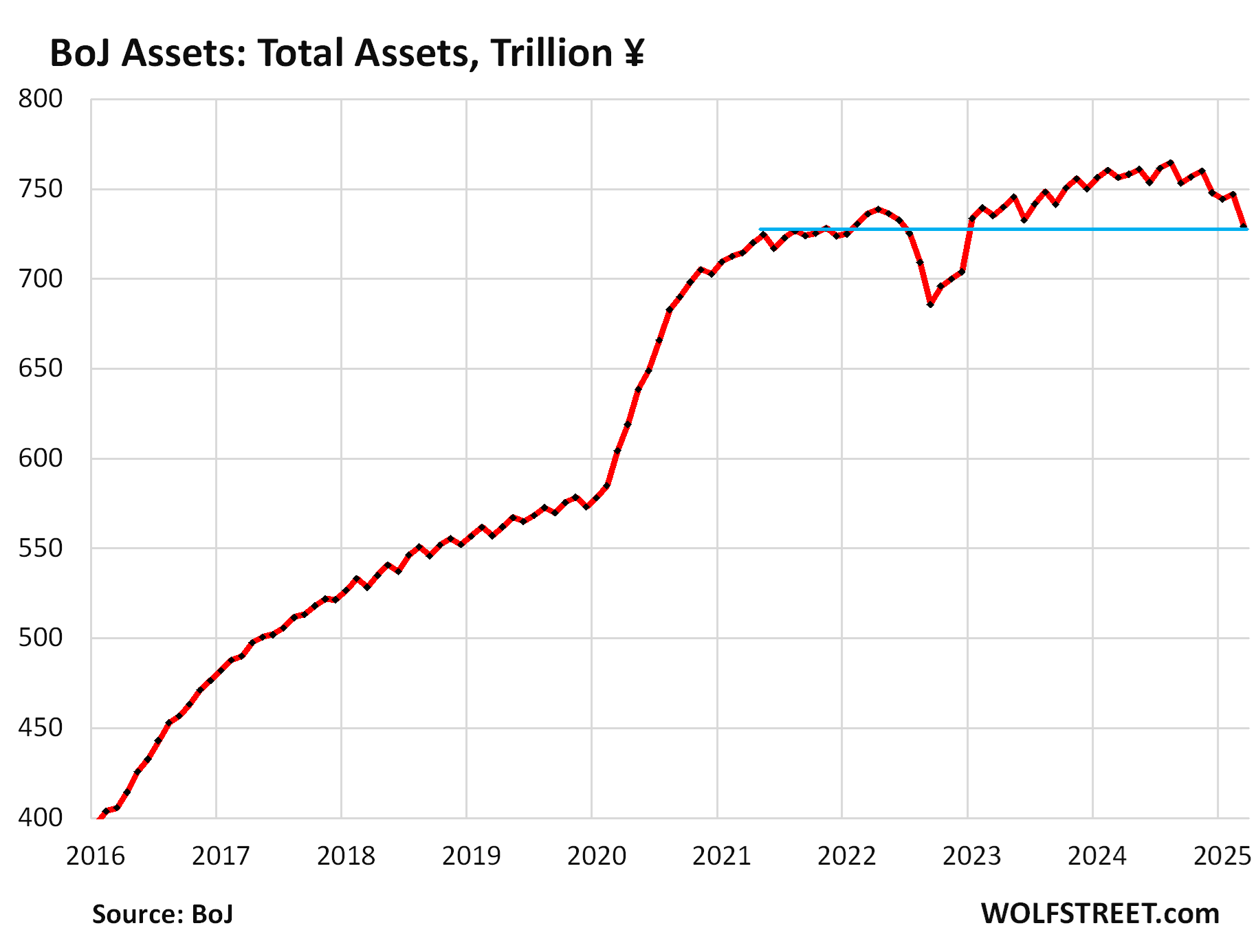

BOJ Quantitative Tightening: -¥18 trillion (-$120 billion) in March, -¥27 trillion YoY, to ¥729 trillion total assets, lowest since December 2022.

By Wolf Richter for WOLF STREET.

Quantitative tightening at the Bank of Japan has picked up speed in 2025. Total assets fell by ¥18 trillion ($120 billion) in March from February, by ¥18.8 trillion from three months ago, by ¥27.2 trillion year-over-year, and by ¥35.6 trillion ($247 billion) from the peak in August 2024, to ¥729 trillion ($4.93 trillion), the lowest since December 2022, and back to about where they’d first been in May 2021, according to the Bank of Japan today.

On July 31, 2024, the BOJ had announced details of the reduction of its Japanese government securities holdings and laid out a path for accelerating QT in 2025. Its huge government bond holdings had peaked in February 2024 and have zigzagged lower since then, with the acceleration becoming visible now.

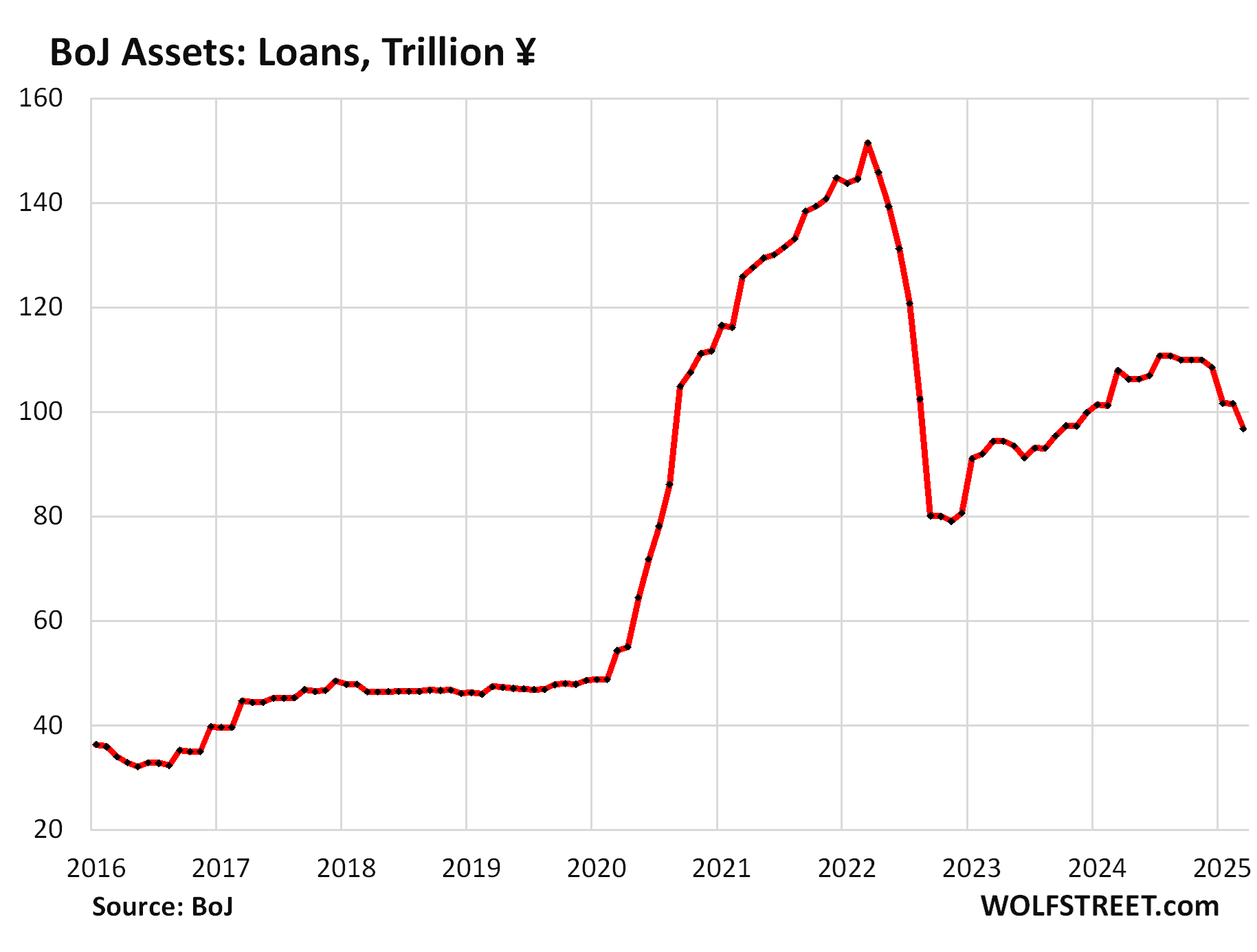

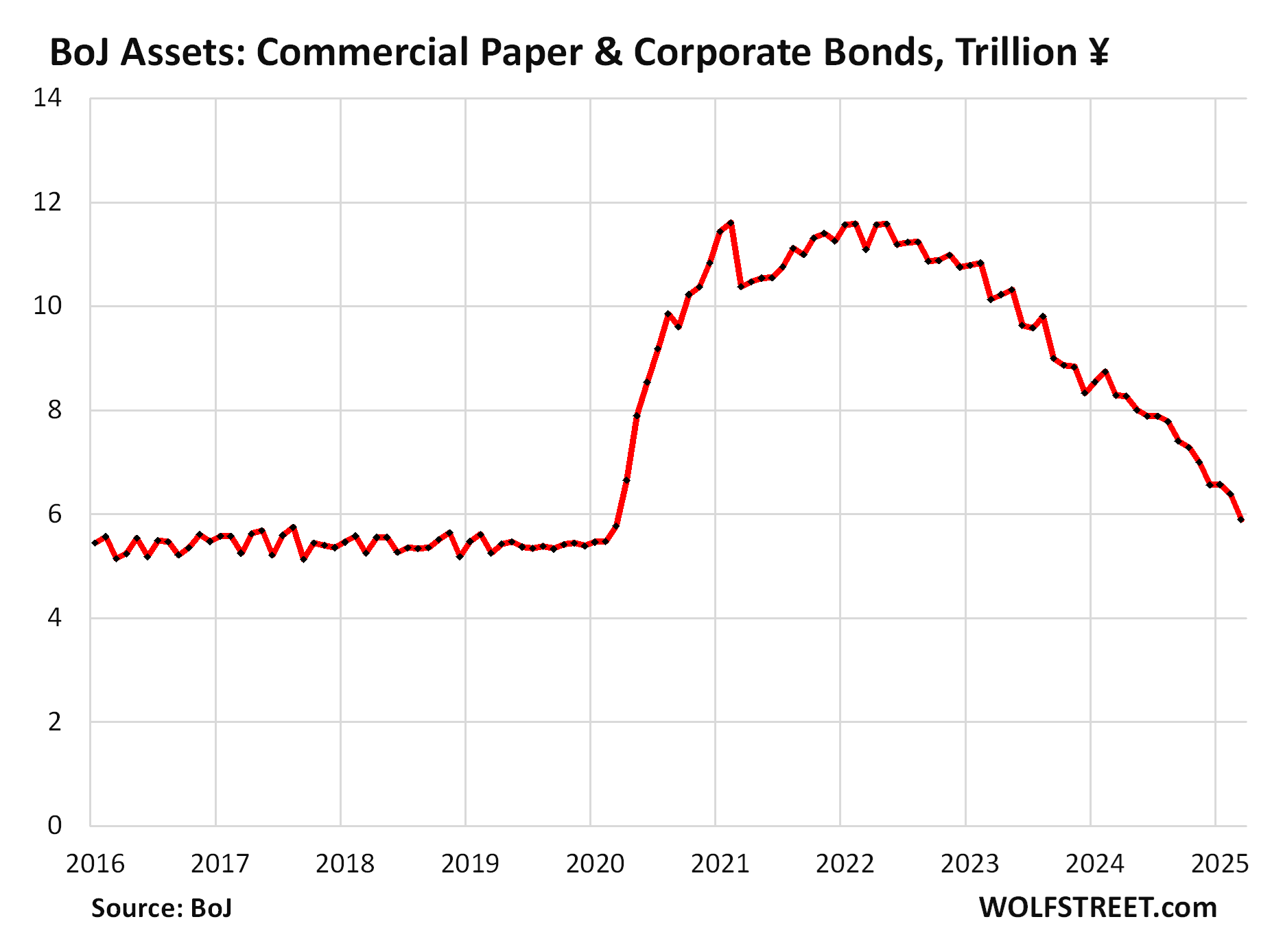

Its loan portfolio, a big factor in its pandemic QE, had peaked in March 2022 and has since then declined by 35%. It started shedding its relatively small holdings of corporate bonds and commercial paper in mid-2022, and about half of them are now gone. It continues to hold its relatively small holdings of equity ETFs and Japanese REITs but is discussing how to reduce them without disrupting markets.

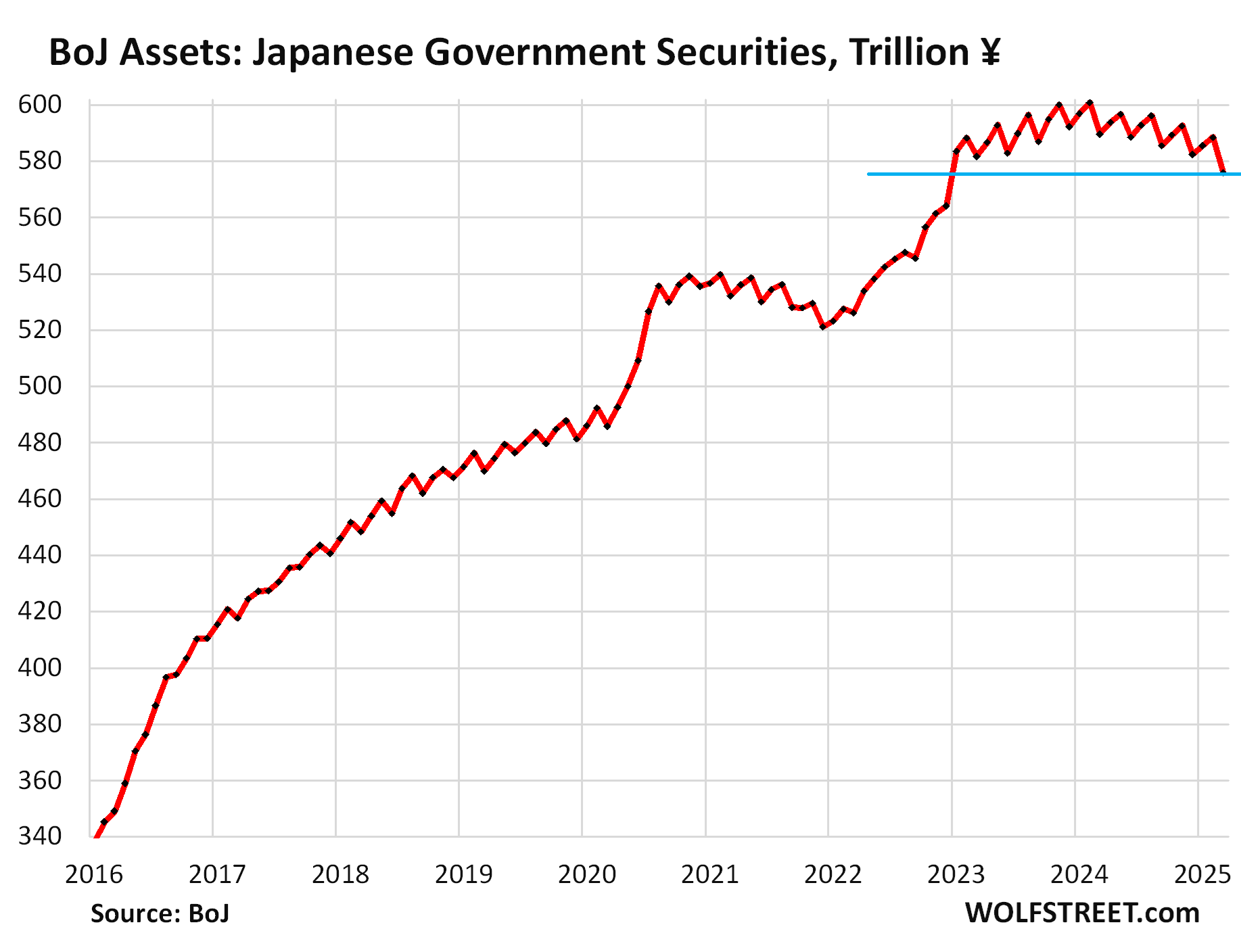

Japanese government securities: -¥12.6 trillion in March from February, -¥6.4 trillion from three months ago, -¥24.8 trillion from the peak in February 2024, to ¥575.9 trillion ($3.89 trillion), the lowest since December 2022.

The BOJ’s government securities holdings, which accounted for 79% of the BOJ’s total assets in March, move in three-month cycles due to the timing of when big long-term bonds (40-year bonds) mature and when they’re replaced with newly issued bonds of the same type.

In terms of the three-month cycle, the peak of government securities holdings was the period of October-December 2023. Compared to December 2023, its holdings of Japanese government securities fell by ¥16.3 trillion.

Loans: -¥4.8 trillion in March from February, -¥11.1 trillion year-over-year, -¥54.7 trillion (-36%) from the peak in March 2022, to ¥96.8 trillion ($654 billion), lowest since November 2023.

These loans accounted for 13% of the BOJ’s total assets. The BOJ provided loans to banks and other entities under several programs, including the massive pandemic-era loans that cause the total amount of loans outstanding to more than triple from ¥49 trillion in February 2020 to ¥152 trillion at the peak in March 2022:

Commercial paper and corporate bonds: -¥0.5 trillion in March, -¥2.4 trillion year-over-year, -¥5.7 trillion (-49%) from the peak in May 2022, to ¥5.9 trillion ($40 billion), lowest since March 2020.

The BOJ stopped buying commercial paper and corporate bonds in early 2022. And its holdings have been running off the balance sheet as they mature. In March, they accounted for 0.8% of its total assets.

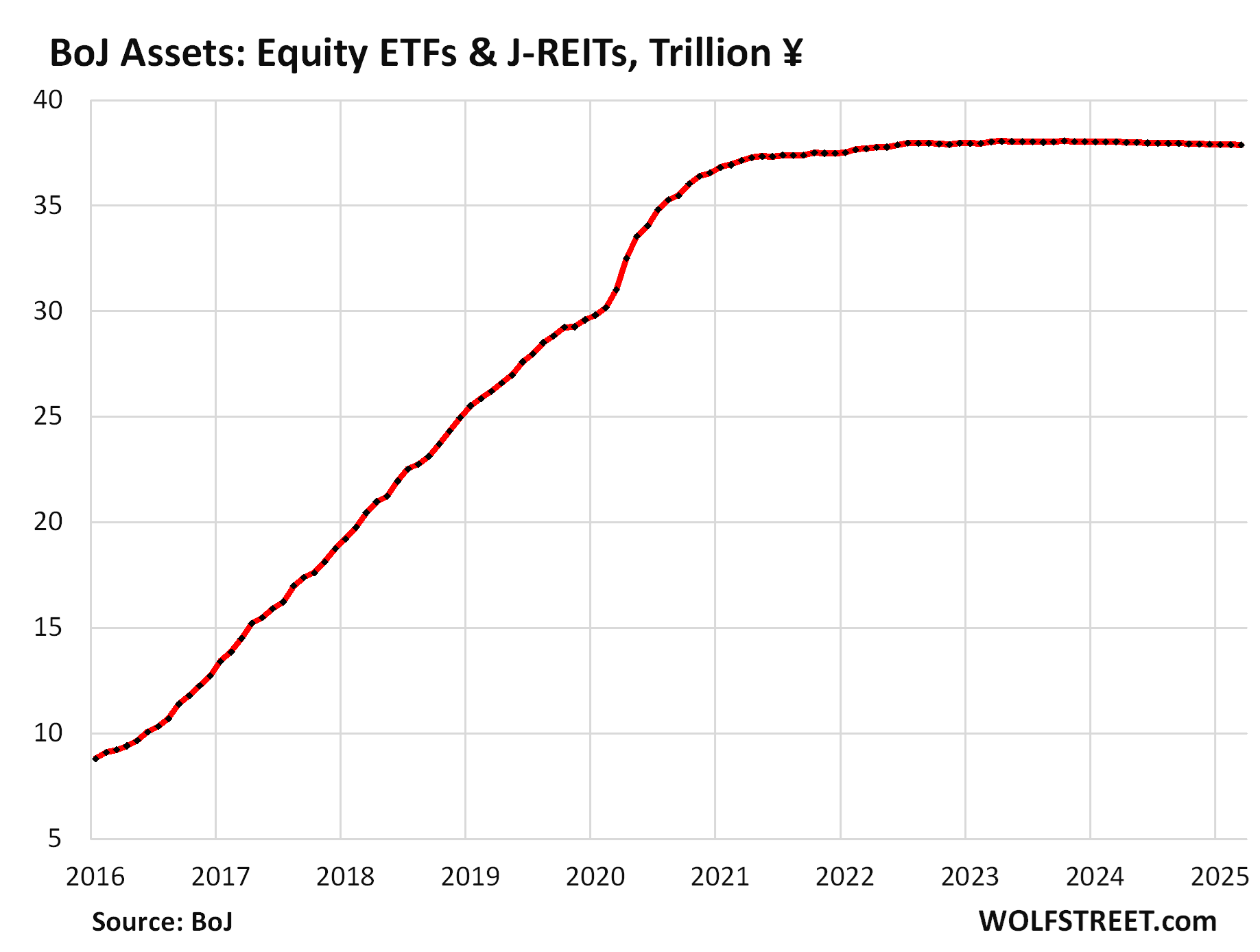

Equity ETFs and Japanese REITs: The BOJ, which started buying ETFs in 2012, carries them at acquisition cost, not at market value. The BOJ stopped buying equity ETFs and J-REITs in 2021, when they’d reached about ¥38 trillion ($240 billion) at acquisition cost, and have remained essentially unchanged since then in terms of the number of shares it holds.

It would have to sell them outright to get rid of them because they don’t mature and come off the balance sheet automatically, like bonds do.

Speaking before the Japanese parliament two weeks ago, BOJ Governor Kazuo Ueda said that they would “still need some time to consider what to do with” these ETF holdings. How to sell them is tricky. The fear is that selling them outright into the market could cause markets to tank.

Since he said that, the Nikkei 225 has tanked by 17%. But the BOJ doesn’t adjust them to market price, neither on the way up nor on the way down, but carries them at acquisition cost, which is a lot lower than current market value since it bought them years ago on the way up and stopped buying them in 2021. If market values fall substantially below its acquisition cost, the BOJ would write them down.

During QE, the US financial media hyped those ETF purchases as if they were a huge deal, though they were just a small part of the BOJ’s total assets (5% in March).

Joining the Fed’s and ECB’s QT party:

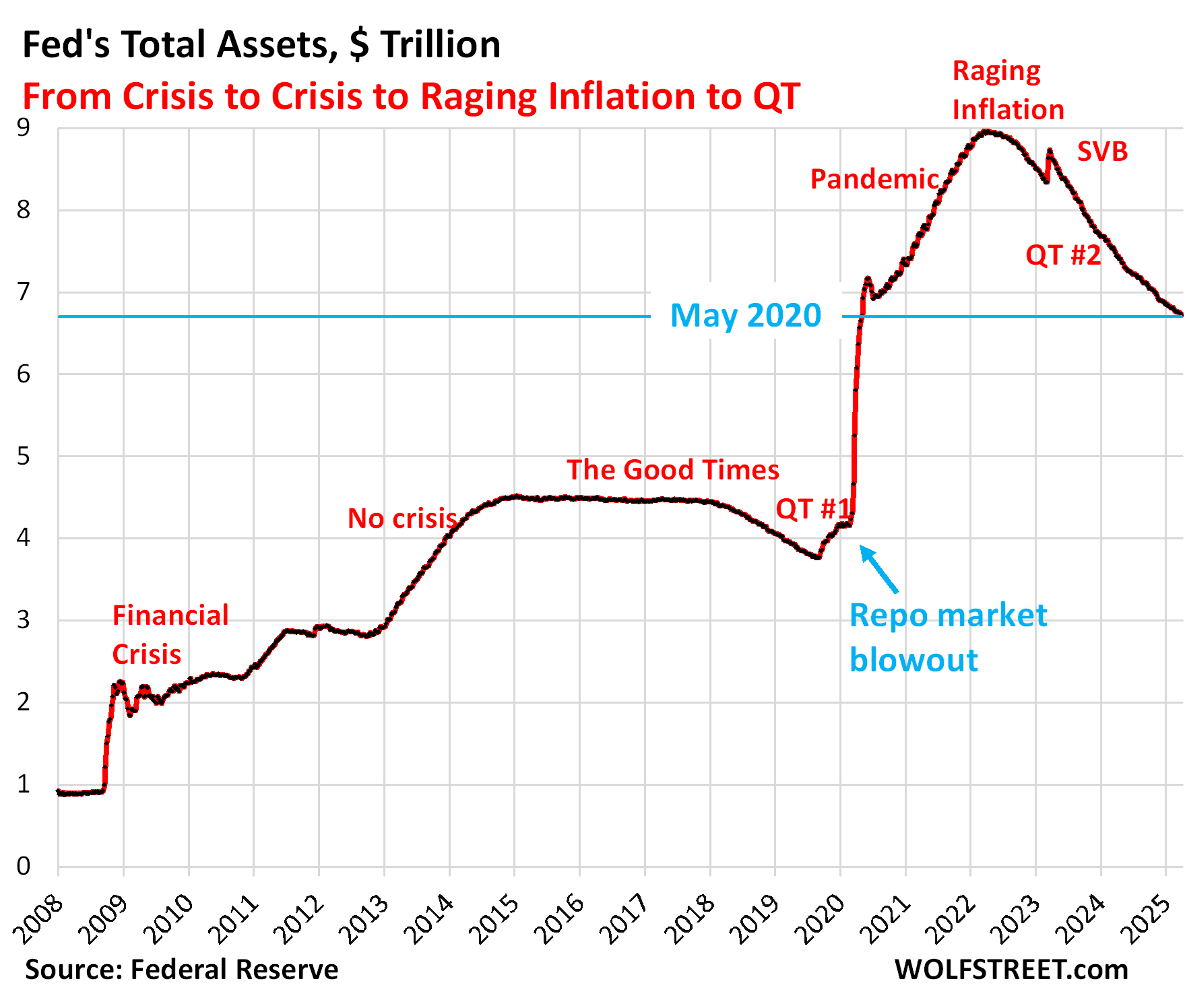

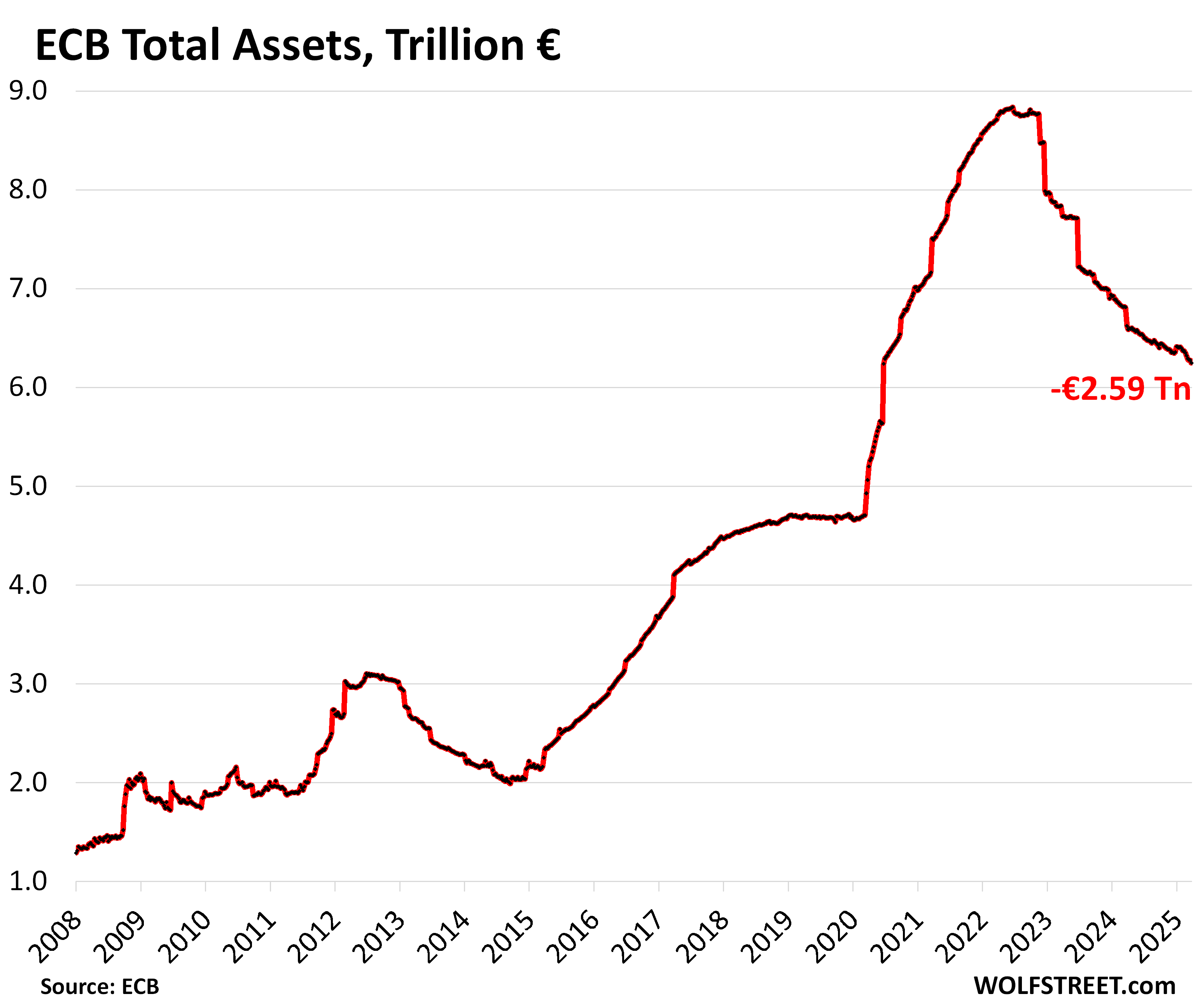

The Fed has shed $2.24 trillion of its assets, and the ECB has shed ¥2.59 trillion of its assets, about $5 trillion combined, each of them dwarfing the BOJ’s belated QT. But until 2024, the BOJ had been the missing link amid the big central banks that had switched to QT. Now it’s visibly part of the QT party, but far behind:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Just say it out LOUD, Wolf, in capital letters….the entire Monopoly money system is a disaster. A DISASTER, and should be abandoned. QT, QE, ZIRP, inverted yield curves. Yen carry trade. What a circus. Say it out LOUD, Wolf. You don’t need to tiptoe through the tulips.

Yen carry trade collapse could cause big problems for risk assets. Wolf, you follow Japan, do you see risks here?

Gutsy QE experiment by the BOJ, useful data for the rest of us to study forever. We’ll have to always just guess what would have happened had they not QE’d their b*lls off.

domo arigato

OT. I was wondering if you were still had tesla on short sales or did you ever have them that way. My brain doesn’t work as well as it did.

Thanks for all the other info you offer on this site.

I have never shorted Tesla. Way too risky.

It should trade like an automaker, which it is, with a P/E ratio between 10 and 20. It’s P/E ratio is still over 100. So you see where I think the share price price should be, but that doesn’t mean it’s going to go there in my time frame.

Thanks

Slight fix, above charts 5 & 6 in first sentence: ECB has shed 2.59 trillion in Euros, not Yen.

The BOJ could sell a lot of those shares directly to the companies. To get rid of them it could offer a small discount as well.

Lots of companies in Japan are cash rich and have funds available to reduce their shares outstanding.

The BOJ holds shares of equity ETFs. It doesn’t hold the underlying shares. So I cannot sell the underlying shares.

Trump has been complaining about the weak JPY. Bessent will start discussion with Japan with “currency rates expected to be on the agenda” according to Nikkei. What can Japan do? Speed up interest rate hikes? Speed up QE? Is it likely?

Trump complains about a lot of things, too many things to even keep track of. I dunno if it would be worth it to them to push the Yen up, just to get a smaller tariff level. You’re trading one problem for another, and that other problem applies to all your exports.

Good points. Thanks.