Austin, Oakland, San Francisco, Detroit, New Orleans, Jacksonville, Denver, Portland, Seattle, Mesa. Tampa is almost there, as are other markets.

By Wolf Richter for WOLF STREET.

Here are 10 big cities where condo prices have dropped by 10% to 22% from their respective peaks. Most of those peaks were in mid-2022. They’re examples of home prices coming unglued in many markets, while they’re still rising in other markets. Every market dances to its own drummer, as we can see in the charts below.

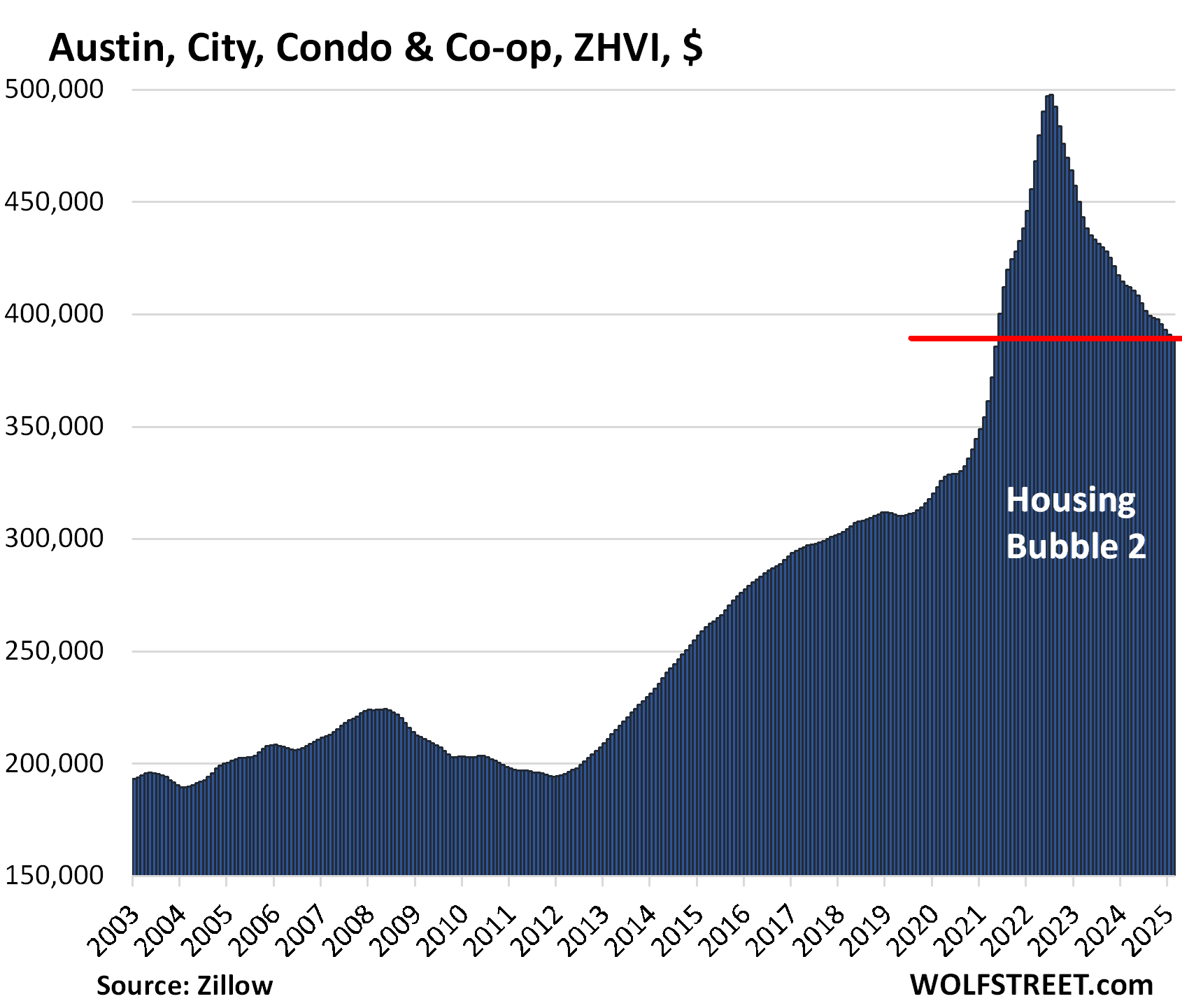

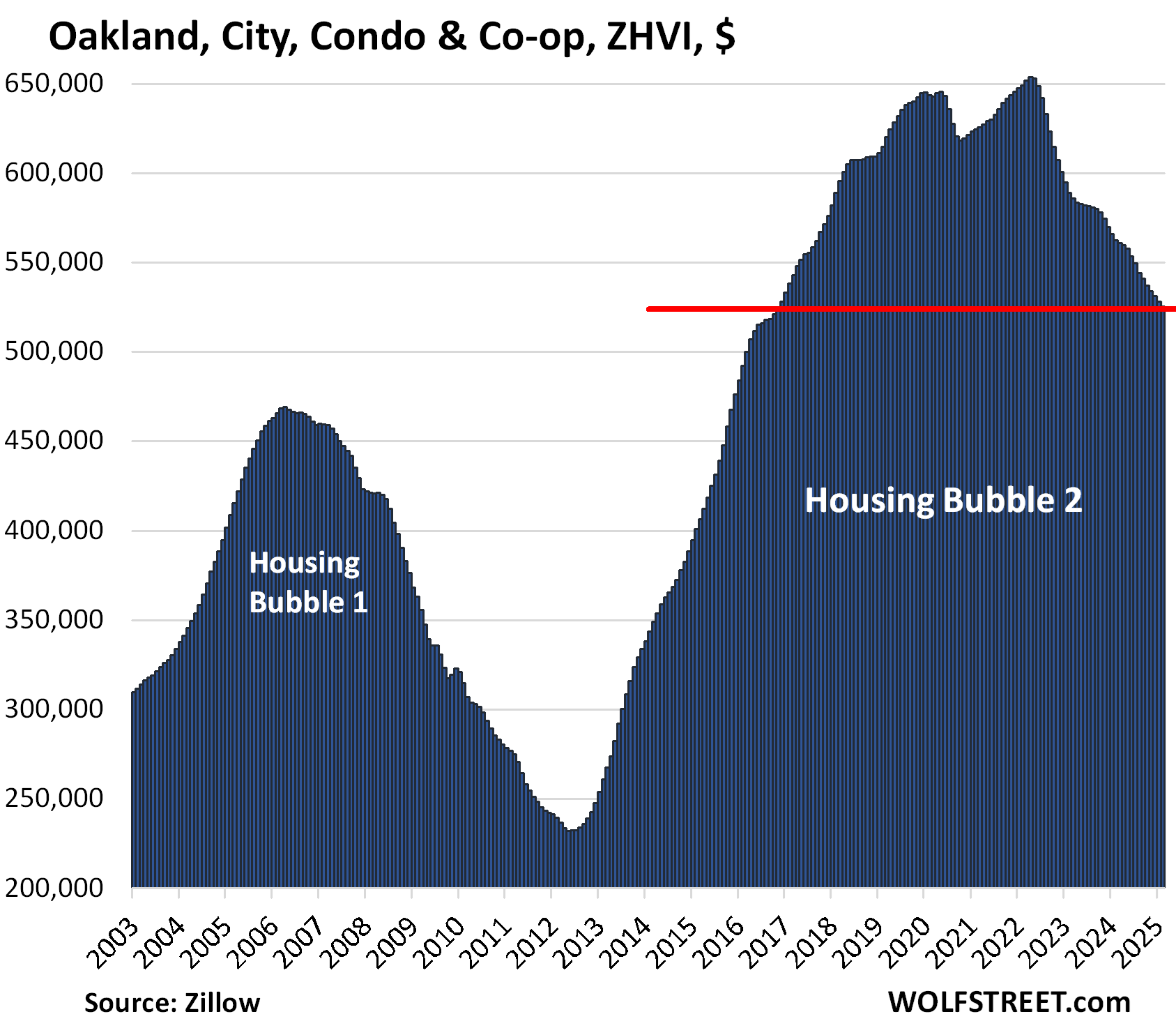

The city of Austin leads the pack with condo prices down by 22% from the peak in July 2022, followed by Oakland, with a decline of 20% from the peak in May 2022.

Not on this list yet is Tampa, which is a top runner-up, lacking just one small additional month-to-month down-tick to get to -10%, which would then qualify it for this list.

We’re looking at seasonally adjusted three-month average prices of “mid-tier” condos. Limiting the choice to “mid-tier” minimizes the impact of shifts in the mix. The data are from the Zillow Home Value Index (ZHVI), which is based on millions of data points in Zillow’s “Database of All Homes,” including from public records (tax data), MLS, brokerages, local Realtor Associations, real-estate agents, and households across the US. It includes pricing data for off-market deals and for-sale-by-owner deals.

If these charts look absurd, it’s because the housing market became absurd in the early 2000s, when the Fed kept interest rates too low for too long, creating the enormous Housing Bubble 1 that then turned into the enormous Housing Bust 1, which turned into the Financial Crisis, upon which the Fed used zero-interest-rate policy (ZIRP) and QE to restart this process all over again.

But nothing compared to what the Fed did during the pandemic, which led to below-3% mortgages further fueled by its trillions of dollars in QE and by the federal government’s trillions of dollars in annual deficit spending. And all this turned the housing market into an absurdity that is now coming unglued.

| Austin, City, Condo Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -22% | -0.6% | -5.7% | 122% |

| Oakland, City, Condo Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -20% | -0.6% | -6.7% | 183% |

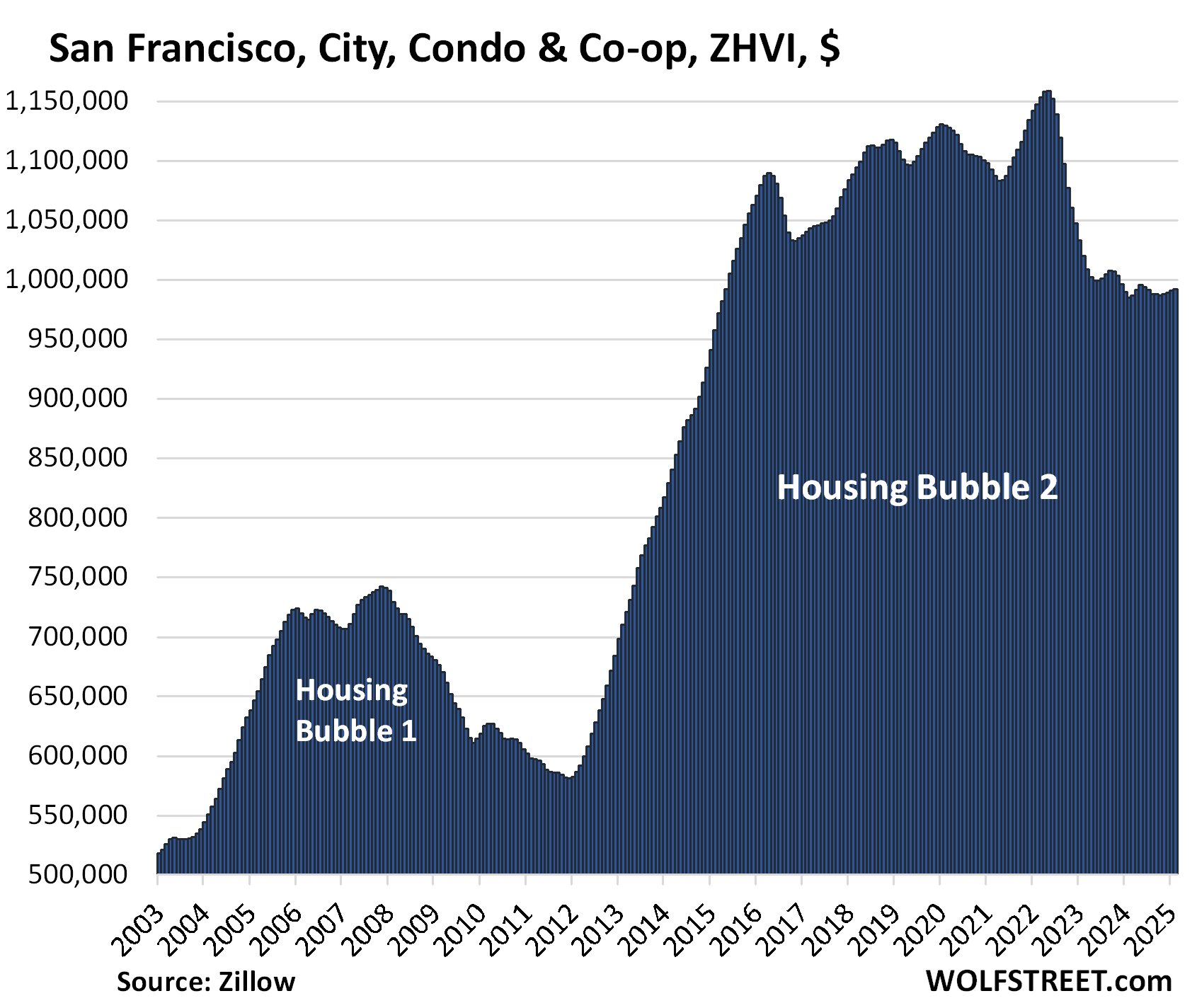

| San Francisco, City, Condo Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -14% | 0.2% | 0.1% | 144% |

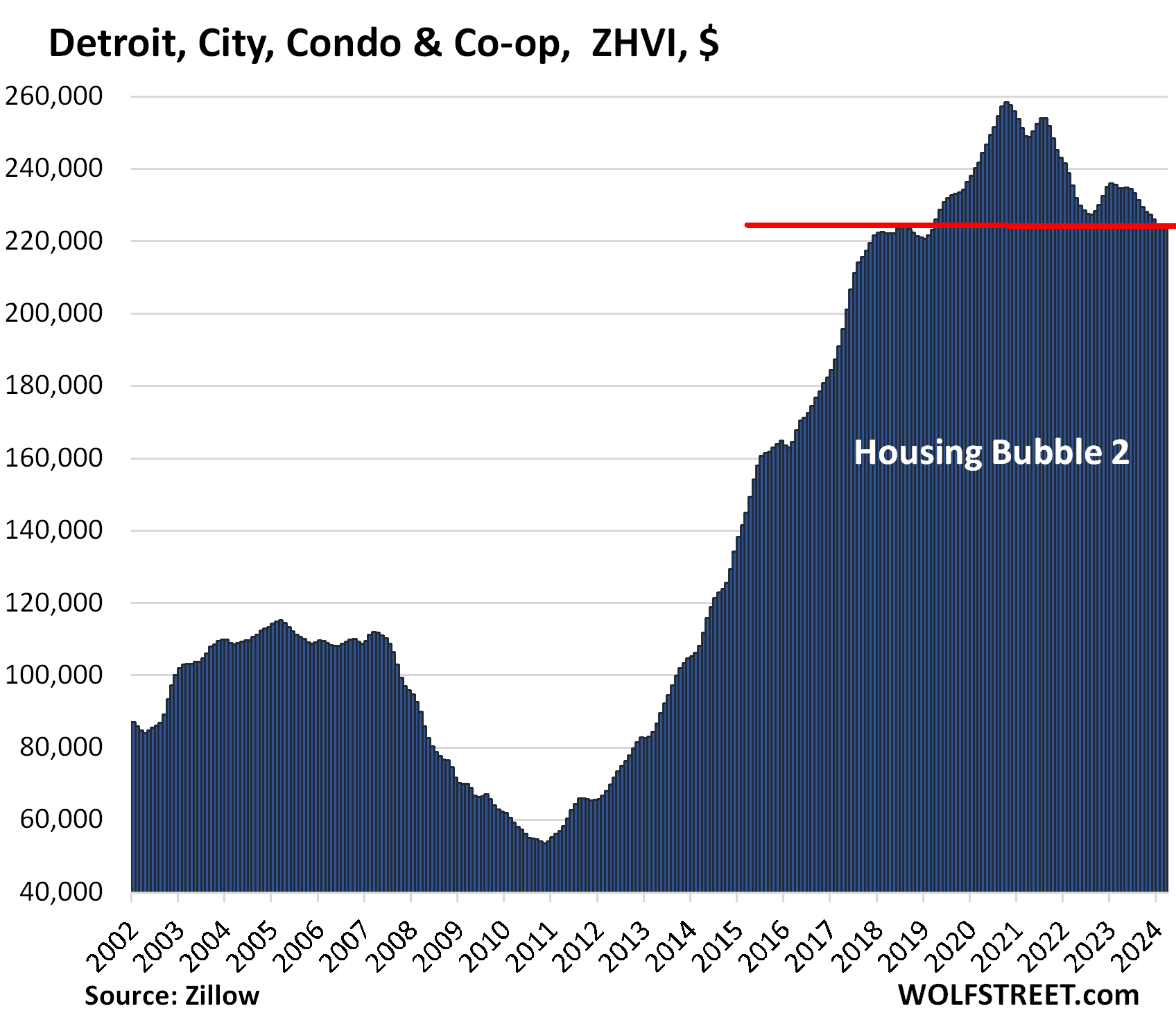

| Detroit, City, Condo Prices | |||

| From Sep 2021 peak | MoM | YoY | Since 2000 |

| -13% | -0.4% | -5.0% | 270% |

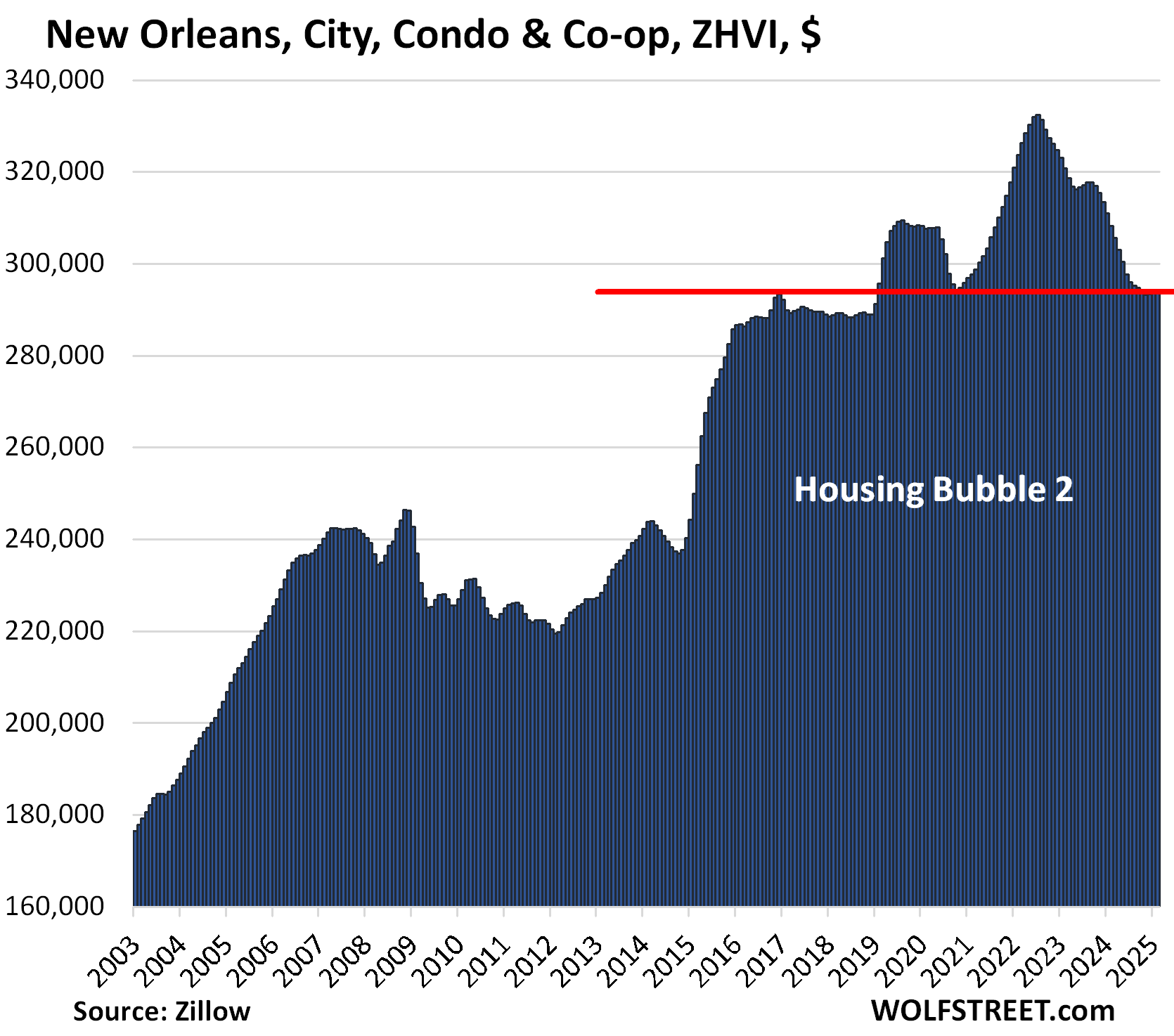

| New Orleans, City, Condo Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -11% | 0.1% | -5.5% | 102% |

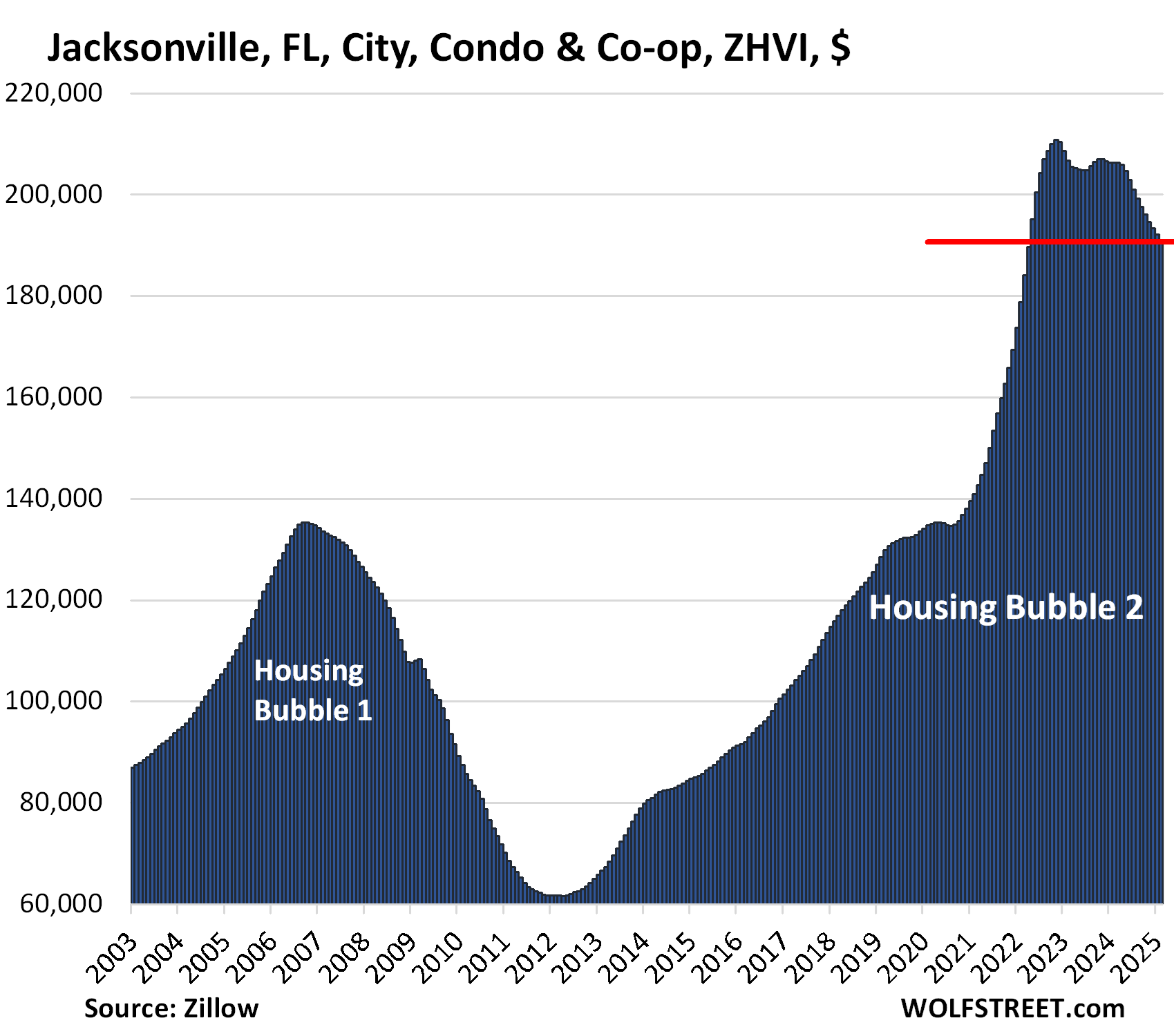

| Jacksonville, FL, City, Condo Prices | |||

| From Nov 2022 peak | MoM | YoY | Since 2000 |

| -10% | -0.6% | -6.9% | 176% |

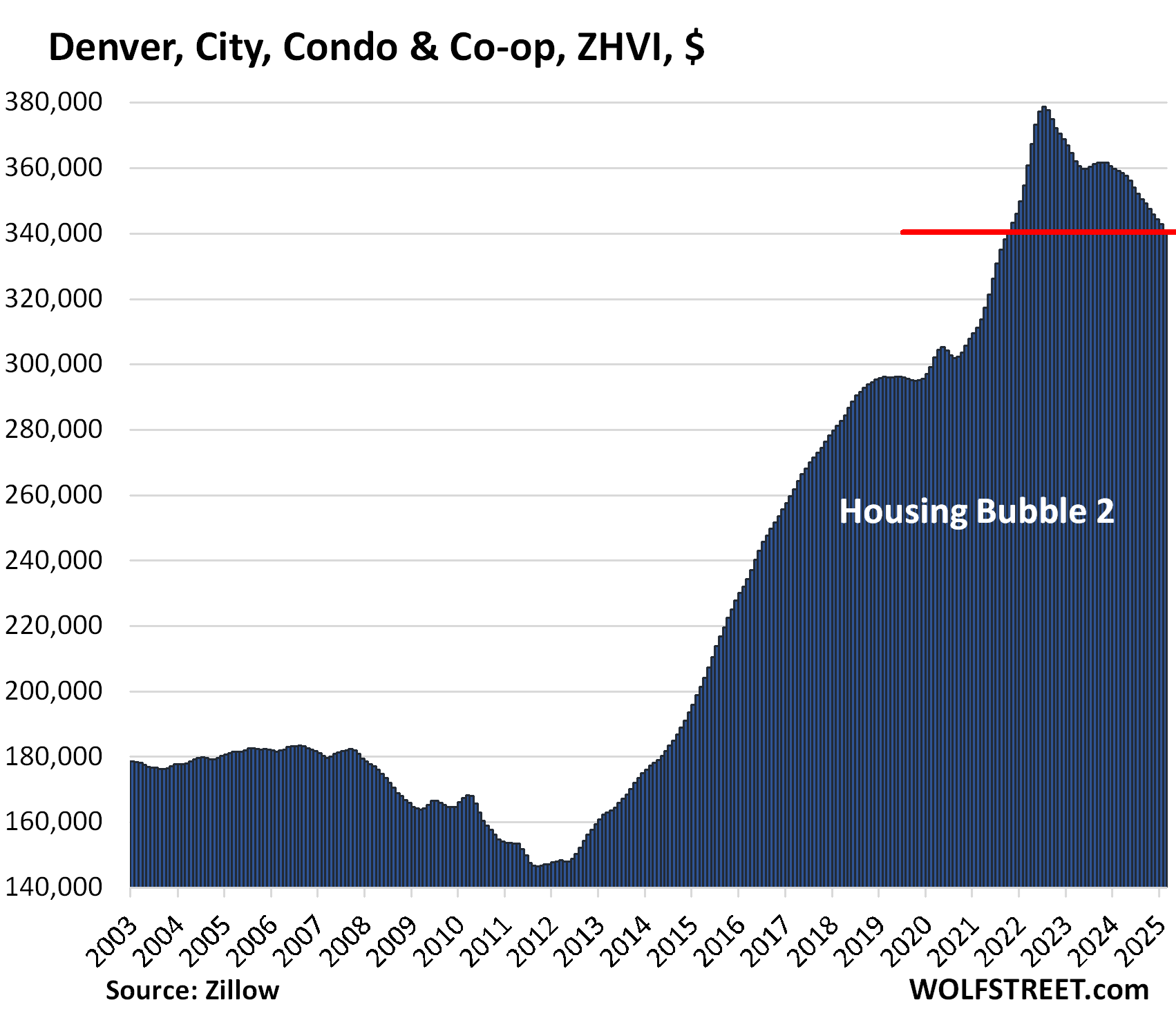

| Denver, City, Condo Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -10.0% | -0.4% | -4.7% | 152% |

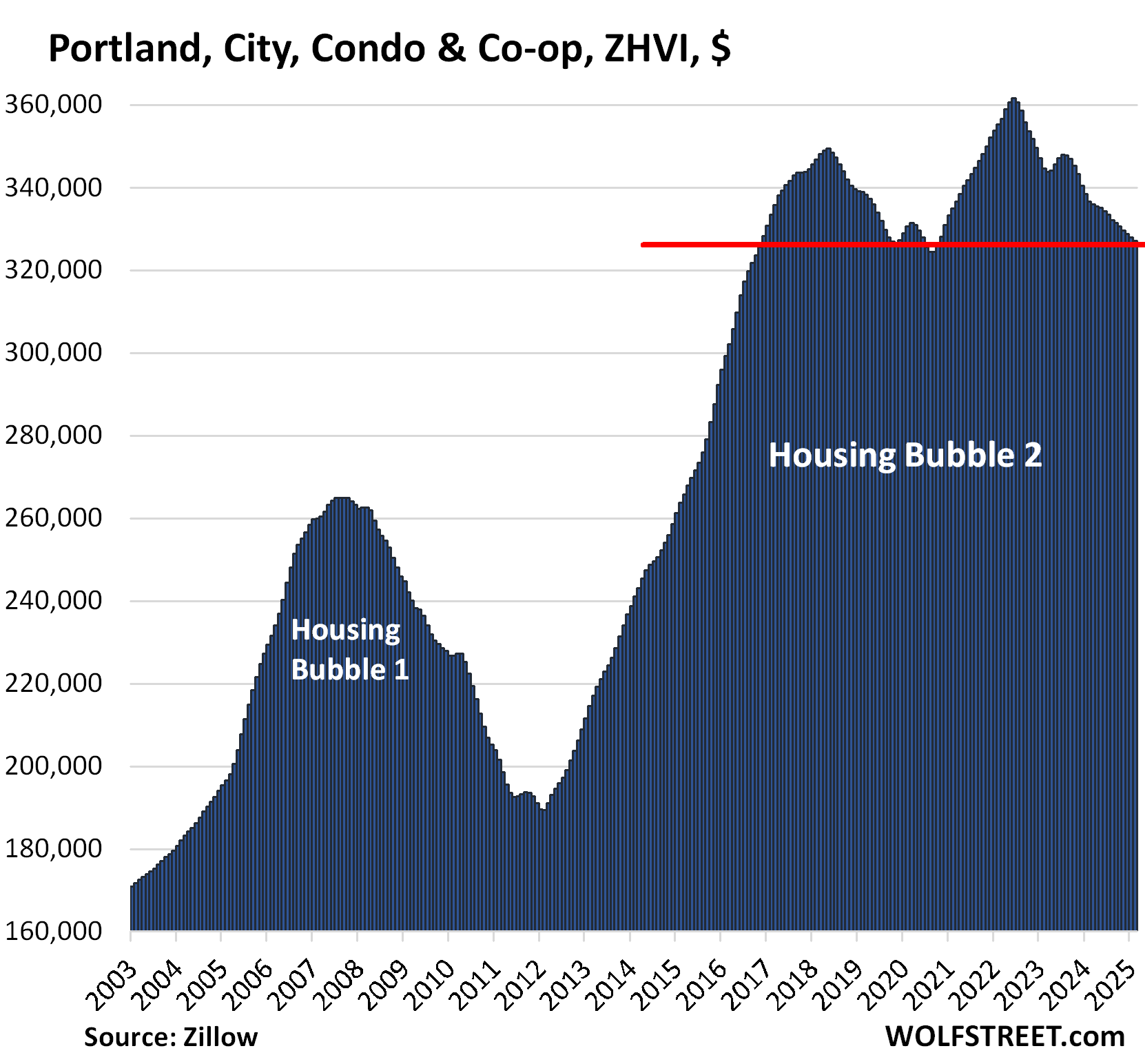

| Portland, City, Condo Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -10% | -0.3% | -3.1% | 118% |

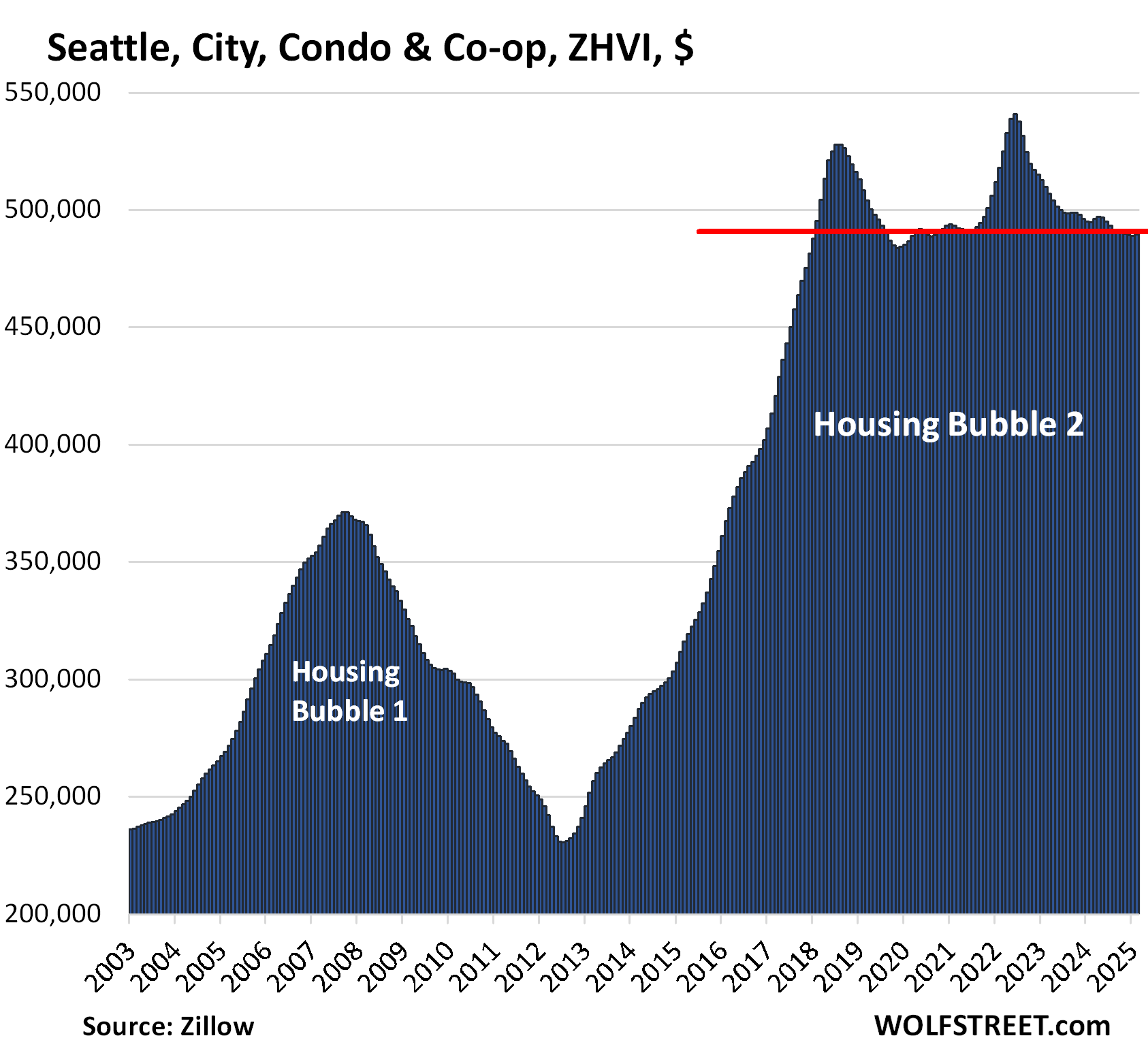

| Seattle, City Condo Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -10% | 0.0% | -1.2% | 148% |

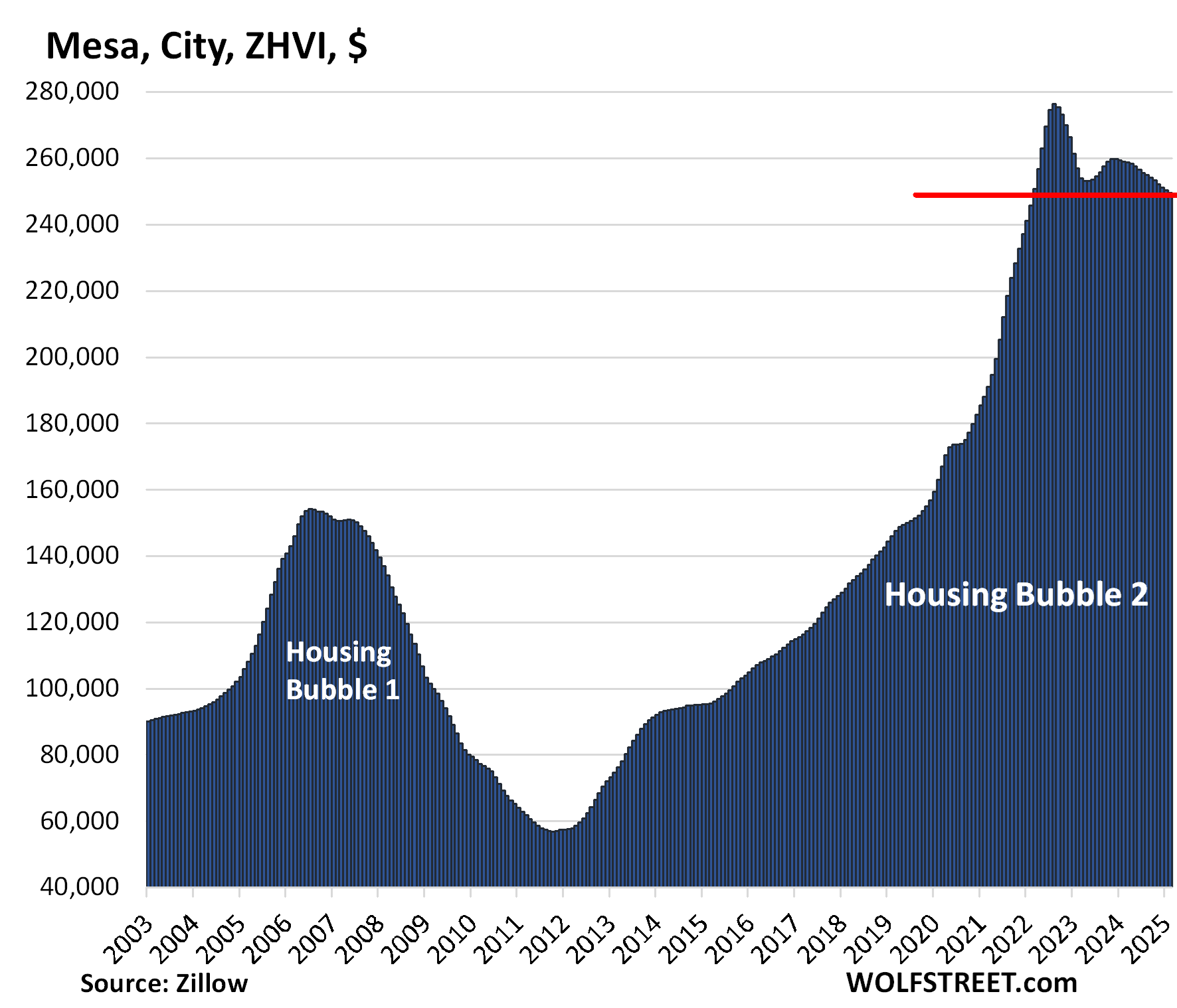

| Mesa, City, Condo Prices | |||

| From July 2022 peak | MoM | YoY | Since 2000 |

| -10% | -0.3% | -3.5% | 218% |

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Here’s Tampa anyway:

Too bad people didn’t explore buying a condo in Tokyo over the last few years or even better yet land.

Just released price changes for land and condos in Japan by the government has a lot of price increases in it spread almost all over the country.

With the yen now in the high 140’s/lower 150’s and looking to increase in value the extra currency bump would have added even more increase in value for US$ buyers.

Here is the link to an article about the change in land prices from the Asahi newspaper. It is in English.

https://www.asahi.com/ajw/articles/15674940

Good friend asked me last week if he should buy a waterfront condo on the Gulf ( of whatever ) here in the saintly part of the TPA bay area, claiming he was seeing some in the $70K range these days and was wanting to downsize now that all his kids are doing well outside the family home.

I replied, ”Sure, as long as you know what the current and likely coming MANDATES are” which he did not.

As usual the sellers and “”REALTORS” are not exactly lying, but also NOT telling the truth about the HUGE amount of repairs and rehabilitations that “SHALL” be required for any condo built before very recently,,, especially in locations where the building departments and various and sundry ”inspecting engineers” were not doing their jobs properly, and even if they did, ”after inspection” redactions were common and prevalent to my personal knowledge.

Woe and worst on the way for almost every condo and other structure not only ON the coast, but even near in FL far damn shore, and I suspect other states similar…

Hedge accordingly.

In the last hosing bubble – around 2003, I had coworkers buying homes and condos in Las Vegas thinking they were going to be the next real estate tycoon. I’ve been to parts of Vegas that are quite ugly. There are nice areas, but Vegas is so hot and dry and it gets very cold in the winter. I wouldn’t want to live there. Anyway, it was a magnet for those looking for less expensive real estate compared to places like California.

When the bubble burst, I think almost all of my coworkers lost their Vegas properties. Their tycoon status ended abruptly.

I remember inventory increasing 5x around 2005 in LV, same happened in San Diego but from a lower level. LV hit around 50k in 18 months or so. And bubble heads weren’t having it, same as now. They’d rather live the illusion that theyre going to be tycoons.

Agree with the LV boom/bust details, but…

” it gets very cold in the winter.”

January average daily low in LV is like 40-42 degrees.

There are plenty of places in the US where 40-42 is in excess of January average daily *highs*.

Vegas ain’t Miami but it beats the hell out of Boston, NYC, Chicago, etc. weather wise.

And the LV weather is inferior to *coastal* CA weather…but the housing costs are still about 45-50% of CA’s.

(There was a time, not too long ago, when LV home prices were 25-30% of CA’s or less).

Where is LA?? Any ideas as to why it might be different? The fires? Growing migrant population? Prices still seem pretty ridiculous but considering the minimum wage is 25 bucks I guess the prices are about what they always have been……unaffordable. Maybe it was listed and I missed it.

Condo prices in LA declined only 1.7% from the peak in Aug 2022, they’re -0.2% MoM and -0.8% YoY. So really not much movement, not nearly enough to qualify for this list.

I think the fires are going to have an impact. I expect it will take a minimum of 10 years to get Altadena to anywhere near what it had been, with more multi-units taking the place of the old single family residences. I think this because many of those lots were much larger than todays norm, having been laid out in the early 1900’s. Lot’s that burned are currently selling (or at least listing) over the prices pre fire when they had houses on them.

Palisades will be different, because those folks have more money. But still, there’s a limit to how many builders can work, how much material is available, etc. Those moving into the area to take advantage of the rebuilding are only going to make the available housing tighter. There wasn’t enough vacant housing to cover the loss of 15,000+ buildings before the fires.

There is another factor that is already limiting rebuilding in Palisades per the WSJ.

Multiple insurance companies are declining to insure rebuilt homes in the fire footprint. Unless this changes, rebuilding will be very slow and many people will choose to sell and move on.

Surely Felix, the fires are one important factor in the current RE situation!

As to affordability, last time I worked in SoCal, ’17-’19, everyone who wanted one and needed one had at least one ”side hustle.” Those were folx making wages under $100k/year and not able to share housing with enough family.

Several had several, many owning a small apt bldg, many of which were built cheap in the sixties, sized to fit onto a typical single family lot, and continued cheap into the ’90s. Most did most or all of their own maintenance, or bartered it, and were making decent returns.

At the time, the co. I worked for was bidding to demo and make much larger apts on the same lot.

Last time I lived there, late ’60s, I couldn’t keep up with demand for my labor, even with 164/168 hours scheduled (including sleeping and eating LOL.)

Owning a so-called “Huffman six-pack” of apartments in San Diego (having bought with good Prop 13 margins, hence low taxes) has been a cash machine for the fortunate ones. I am also recalling the 2005 era when tons of them were doing condo conversions. Some pretty rickety little buildings would become condo associations, real estate sales signs on the streets everywhere, it was an atmosphere of frenzy. A guy was telling me he paid $450k for a unit with some wild mortgage terms and asked if I thought that was smart, I was very quiet.

Condos are always the last to go up in a housing bubble and the first to go down in a real estate crash.

I hope I’m not posting this again from another post I can’t remember but anyway, you’re totally right, all that money that was printed and all those low interest rates have just decimated the poor middle class, if you weren’t lucky enough to own a home you’re just getting wiped out.

“Americans have suffered under crippling inflation, and the Federal Reserve is to blame,” said Rep. Massie. “During COVID, the Federal Reserve created trillions of dollars out of thin air and loaned it to the Treasury Department to enable unprecedented deficit spending. By monetizing the debt, the Federal Reserve devalued the dollar and enabled free money policies that caused high inflation.”

“Monetizing debt is a closely coordinated effort between the Federal Reserve, Treasury Department, Congress, Big Banks, and Wall Street,” Rep. Massie continued. “Through this process, retirees see their savings evaporate due to the actions of a central bank pursuing inflationary policies that benefit the wealthy and connected. If we really want to reduce inflation, the most effective policy is to end the Federal Reserve.”

“The Federal Reserve has not only failed to achieve its mandate, it has become an economic manipulator, directly contributing to the financial instability many Americans face today,” said Sen. Lee. “We need to protect our economic future, end the monetization of federal debt that fuels unchecked federal spending, and put American money on solid ground. We need to End the Fed.”

AGREE TOTALLY J:

Just looking at the ”official” degradation of the USD, since the FRB was started in 1913 really should be enough to convince any person with any ability to think that the FED should be either completely ended,,, OR, at least put back into it’s place as a private entity owned and operated by and for the banksters as it SO CLEARLY IS and always HAS BEEN.

And to be clear, ALWAYS protecting the banksters and the oligarchy at the expense of the workers and savers.

Please folx, DO NOT PRETEND otherwise…

Yes, the Fed is a failure, for most of its existence, it had one job, stability of the US dollar, total failure.

No, Congress gave the Fed two jobs which force it into a delicate balancing act: (1) maximum employment, (2) stable prices.

In order to accomplish the first, it must be able to stimulate the economy in downturns by forcing real interest rates negative. So it’s definition of “stable prices” then becomes a target inflation rate of 2%.

OKC planning to build the tallest building in the world or maybe USA at least as a plan . Since the building will occur after 2000 and 2020 the 100 index will be on different inventory . Just like Ivy League schools be added to their list difficult to ever have any new cities even have growth in USA maybe bringing back manufacturers to USA over time will provide some new areas.

Are orange county and SD similar to LA? Market is still tight despite news of an exodus to FL and TX.

I think those folks got priced out but the real estate market is still viscous.

Condos are selling like hotcakes here in the Swamp. All these double dippers who were working two jobs at the same time, one useless WFH government job where they did nothing but sign in and sign out, and one private sector job where they actually worked are now being force to report back to the office 5 days a week or be fired. They have chosen to report to work in the office. They need housing close to work, because the traffic jams here are horrendous. The only housing they can afford are condos. Townhouses are out of sight and unaffordable. We’re doing one condo today, its cheap for only $295K for an efficiency. Only problem is the high condo fees in the area in SW DC.

I wish I had been in on that!

Not that I believe you.

Enjoy Downtown.

I just saw a reddit thread about the Fannie Mae shakeup and someone was talking about their friend who works for fannie and has a second full time. Had an ex-coworker pulling half a mil working 3 at once, but one was part time and knew about 1 other.

My employer demanded we disclose all other side jobs, down to hobbies.

Ahh, so that is why the RTO mandate. Shake out the r/overwork people.

Yes, he’s living with Reagan’s Caddy-driving Welfare Queen.

I’ve been thinking about your comments about multiple jobs. The really funny thing is whenever that is actually the case, then the IRS probably knows just from tax filings. It’s too bad all of the government databases don’t talk to each other :D

northernlights

The second job is usually under the table, cash business, so there is no record with the IRS.

If some government workers have multiple WFH jobs it seems unlikely to have a substantial fraction off the books. I don’t think a person working for the FDA is running a roofing business on the side, but maybe I’m underestimating their entrepreneurial spirit!

If this is the real deal at any level which matters, I have to think the IRS has the info.

I was talking to a builder rep in NC last year and asked how the buyers afforded the higher priced homes. He said 90% of his buyers had 2 full-time jobs, and 1 buyer had 3 jobs. I wonder how many of those were government jobs

The WSJ (I believe) had a story a few days ago about federal workers getting laid off in Oklahoma City, which is a big center for federal workers, and the impact on the local economy. One of the examples that they picked, with impeccable tone-deafness, was an accountant at one of the federal agencies who’d gotten laid off. The article was talking about how disruptive this is for the local economy, because, you know, this guy was working from home, and during covid he’d bought some land and was starting a ranch, and so his second job was this ranch he was starting up. But starting up a ranch is an all-out full-time job. So you can see how hard he must have been working-from-home for the federal government. I don’t think the reporter wanted to express that. The reporter was focusing on the guy’s fears that he might not be able to make the land payments, and how disruptive that fear is. But turned into a hilarious indictment of government workers working from home.

I wish I could learn how to complain about the CORRECT economic hypocrisies and unfairnesses in this country…..(like the insane distribution of wealth here…..it seems to be incorrect for complaint purposes…….what makes it worse is I have the intelligence and had many opportunities to be one of the richest guys here……but no excuses, nobody to blame.

But as a proven (77+ years) lazy economic loser (meaning a pathetically low lifestyle relative to most others here), I don’t appear to be able to tell the right stories or generate the right complaints about the right problems.

Anyway, you folks have spouted quite enough proper complaining for me….time to move on to next article.

There is a system equifax has that has detailed pay stub information on everyone. Friends found Equifax had records of every past paycheck, even from small employers.

You can sign up for free to view your history, good chance your employer can buy the data as well.

Swamp, not to be rhetorical but reposting the same analogy, time and time again doesn’t gather any moss.

Freedomnowandhow

If you don’t like my posts exposing the waste and fraud which has been going on here for a very long time, then don’t read them.

Except you haven’t actually exposed any waste and fraud. You just keep repeating nutty conspiracies that were planted in your head by your political masters.

JimL

It would take volumes to list all the waste fraud and abuse that I saw while I was in the Federal Government. I could write a book about it and make some big bucks selling it on Amazon if I wanted to. Instead, I will just send a personal letter to Musk and Trump and tell them how proud I am for what they are doing with DOGE, and to keep up doing God’s work.

On the Monday 3/17 1:40:00 in Stocks & Jocks p cast The Chief was complaining about WFH because he was crying about the office buildings and restaurants in Chicago, not about anyone working more or less effectively.

I am an appraiser who works in the District of Columbia.

There are massive layoffs in Maryland & Virginia. If you

want to keep you government job and benefits, and you were

laid off you have to work five (5) days a week. I am seeing

a huge pick up in condo sales (only housing affordable in DC;

Why? Gov. people who live in DC & Md need a place close to

their gov. job. Most people are selling their homes in Maryland and VA to

move into the District of Columbia. DC is overall unaffordable.

Condos are the only game in town. Even I cannot believe what I am seeing in the condo market. However, this may not last, and time will tell what is really going on in DC. Wife of the swamp creature.

I am still waiting – and very curious – to see how this plays out in my lovely MD town. I’m still seeing incredible price increases here as well, but it looks like lots of rich people from the area are coming here to retire, and lots of young people moving here (especially from TX) to feel safe from “persecutions”.

But I’m also thinking, once you’re here, you really don’t want to leave. It is so great to live somewhere where people still seem nice, not always trying to force an angry political spin on everything. Hope it lasts. Wouldn’t want it to ever be DC.

I lived in the DC area for thirty years. I never visited any MD town I “don’t want to leave.”

My daughter has lived in TX for twenty years. The idea that she would move to MD to feel safe from persecutions is ridiculous. You must be referring to illegal aliens. But no worries your MD and other sanctuary cities won’t be magnets for such people much longer.

Yeah sure, Baltimore was nice 45 years ago and you could actually sit down and eat a decent meal in the downtown area and at seafood restaurants in the city

Now there are areas that are worse than 3rd world hell holes in and around Baltimore.

All compliments of the idiotic democrats that ruined the city and the state.

A lot of people don’t understand just how influenced by the DC economy MD and VA are.

MD has more millionaires per capita than any other state (and it ain’t because of the the mother-******* crab cake industry).

It is because of the courtier-class eco-system that inconceivable amounts of DC spending (since the Depression) has cultivated and insulated.

Bethesda-world and similar close-in suburbs live in a subsidized simulated-reality that very few other places in the US benefit from.

But that said, ironically (but predictably) Baltimore (away from touristy Inner Harbor) is the fairly accurate setting for “The Wire”.

So, in one state, you have many millionaires born of the (ahem) Welfare State, suburban simulated reality economies wholly contingent upon that dying Welfare State, and the ruins that said Welfare State long-claimed to address.

Wolf,

What does the Zillow condo data say about Washington, DC? Is it too early to tell? I am being lazy, of course, so if you don’t want to bother, that is OK. But there is an interesting story unfolding there given DOGE layoffs, what ever the data says….

Down 6% from the peak in June 2022, down 2% YoY. Didn’t make my list because the cutoff is -10%. There are little upticks since August.

This graph substantiates what we’ve been seeing on the ground here in Washington D.C. While condos are plunging across the land they are going up in D.C. That’s because all the WFH government workers that survived the Musk “Big Balls” purge and still have a job, have to move back in the crime ridden D.C. as they report to their office 5 days a week, in order to avoid 3 and 4 hour commutes from their rural getaways. As they say “all real estate is local”

Wolf:

Thank you. The Washington, DC condo demand driven by end of work from home for federal employees and the demand destruction and seller fear of Doge layoffs largely in equipoise, at least in mid-tier condo segment. It will be interesting how long that lasts.

re: “when the Fed kept interest rates too low for too long, creating the enormous Housing Bubble 1”

Despite 14 raises in the FFR (June 30, 2004 until January 31, 2006), – every single rate hike was “behind the inflationary curve”, behind RoC’s in long-term money flows). I.e., Greenspan NEVER tightened monetary policy.

re: “Most of those peaks were in mid-2022”

Textbook peak in money flows. See:

https://fraser.stlouisfed.org/files/docs/releases/g6comm/g6_19961023.pdf

“Quantity leads and velocity follows”.

Cit. Dying of Money -By Jens O. Parsson

If you study the discontinued G.6 Debit and Demand Deposit Turnover release, you’ll find that velocity increases for about 3 months after a surge in the money stock.

Some condos in my town have a “ $750 annual deferred water/sewer assessment for 33 years.”, presumably because the City knows the assessment wouldn’t pass their own rules. Two random people I know told me their (cheaper) developments have similar BS fees.

The question is, is this just a big scheme to lower the permitting component of the cost of housing so that it is not part of the bank’s loan ratios used to approve mortgage applications, thus basically pushing people to borrow more than they should?

Sorry, I posted this in another article, and then realized this was probably the right place to put it.

It is a favor to the developers. They don’t have to pay the fee upfront. They can tag the buyer’s with the fee. And it gets “financed” over time in the sewer assessment.

It would be nice if we had national policies that made it riskier to speculate on real estate.

Well, if this developer-president’s swing for the fences strikes out, maybe a vast pendulum swing to the equal and opposite follies will bring that. The one thing I fear most is a Prez with majorities in both houses of Congress. We get spectacularly unbalanced boondoggles then.

I agreebut at the same time PoTus is a billionaire himself surrounded by billionaires.

Looking at his policies and the way he is shaking things up.. looks like rich people are not happy.

Just look at what’s happening in stock market and tarries un certainities

Biden would have been better for stock market i guess.

Similar things happening in Canada. I follow a mortgage expert called Ron Butler on Twitter (X) who has a good handle on the issues. From 2019 (probably earlier) the market made a shift from residential condo construction to investor condo construction and then people would buy pre-con units and then flip them at a profit. Now rates are higher and the game of musical chairs is ending and those caught with these units have to pay mortgages of $4,000 with rents of $2,400. That or they lose $75K or more (sometimes much more) on the sale of the unit. In most of Canada, you cannot walk away from your property or deposit and hand the keys to the bank – they will go after you for the difference of the sale price. With the price of condos, especially the “dog crate” (500 sq ft) ones cratering, there is now a surplus of condos available in the middle of a housing crisis. 24,000 available to buy in Toronto now. Prices down I believe 17%? Go figure!

All of those 24,000 units would sell tomorrow if they were priced right but of course, they are not.

Cue the Carpenters’ “We’ve Only Just Begun”…

It would have been best if the government had never involved itself in housing; however, that was not to be. “Too smart by half” Clinton started this whole mess by introducing the capital gains exemption for house sales. Remember that?

Clinton’s plan was to make housing an “industry” that would help fill the gap of industrialization loss, some of which was inevitable.

Bushee 2, the most clueless president of our time, oversaw “bubble #1” when he/they let the market go crazy without a modicum of oversight.

And of course, once that bubble imploded, all sorts of other government intervention in housing happened.

The net result of all of this is what we see today. It won’t/can’t end well.

Uh, yeah, except before then you didn’t pay any cap gains if you rolled the proceeds into another house.

Don’t pin this on Bubba.

If someone put more money into the house than the difference between what the price sold than price bought did they make any money? Most gains were riding the inflation wave, at best. I’m will Billy Jeff on that one. Blame Greenspan…etc on interest rates and CONgress on favorable tax treatment of corporate real estate investors.

MW: Dow tumbles 400 points as S&P 500 heads for fifth straight weekly loss while NASDAQ is down 100

parkmerced, the largest apartment complex in SF just defaulted on $1.8B in loans with a $1.4B appraisal. My guess is banks are too savvy to hold this CRE debt, someone is holding the bag. Pension funds? The real price discovery will occur when this property changes hands.

Banks issued those loans in 2019 and 2020 and securitized $1.5 billion of them and sold these CMBS to investors. And there is some additional mezzanine financing. As we have seen so many times, the banks are off the hook. The loans matured in Dec 2024 and weren’t paid off because they couldn’t be refinanced. So this is a repayment default.

The CMBS loans were taken out as a cash-out refinance. In terms of the owners, I don’t remember all the details. But there was a default in 2011 and a PE firm ended up with the property. There were plans to take down these older buildings and redevelop this huge property. That never happened. Maybe the 2019-2020 CMBS loans were just a way for the PE firm to double their money or whatever and walk out if need be.

The 2019-2020 loans came with the very low interest rates at the time. To refinance them by Dec 2024, interest payments would have more than doubled, but the landlord cannot raise rents enough to even make the interest payments of any new loans, which is why the loans couldn’t be refinanced.

In a lot of these cases, a foreclosure sale for cents on the dollar is the best option, where the buyer comes in at a very low cost and then can invest heavily to do something with the property. Tearing down the buildings and starting over again could then happen. This would be a market-based solution. But the affordable-housing advocacy groups are going to vigorously oppose it, so it would be a long hard and costly battle to get the plans approved and to evict the tenants (many of them seniors who have been tenants for many years or decades). There is lots of stuff like this in SF.

For many individual investors, buying a few houses or condos and renting them out was a winning deal… until recently. In large part, many people fell for the mantra that “you can’t lose with real estate.” They were wrong! The expected “appreciation” piece is gone, and for some metro areas, the decline is also painful. Easy money story for home and condo investors is over! Reality is painful!

“Buy now or forever be priced out” LOL

I briefly rented out my first condo after moving into a house and never again. I had the best renters you could hope for and it was still just not a good use of my time. The main advantage was that the HOA did a major charge for a new elevator and it became deductible from the rent rather than having to eat it personally. When the renters left I just sold it and took my winnings (Look at Denver from 2012 to 2021).

Everybody votes for policies to increase the price of homes and acts shocks when homes get expensive. “I’m not against new development, just not near me!”

Years ago a lawyer friend of mine told this joke:

Q – whats the difference between a condo and a STI?

A – You can get rid of an STI

Wolf, you’ve probably seen this already, but there was an article in the Wall Street Journal earlier this week, saying a “secret mortgage blacklist is leaving homeowners stuck with unsellable condos,” since being on the list makes it nearly impossible for a buyer to get a mortgage in that building.

According to the article, the list is maintained by Fannie Mae, and expanded in a big way after the Surfside collapse in 2021. These are buildings that Fannie Mae doesn’t think have adequate insurance, or that need critical repairs. Most of these are in Florida, followed by California, but there are at least 100 buildings listed in a number of other states.

Yes, but the number of buildings on that list is too small to have an overall market impact. In the top two states on that list, the number of buildings on the list:

Florida: 1,400 buildings

California: 680 buildings.

Those two states are huge with huge condo markets with hundreds of thousands of condo buildings each. So it’s not a market issue, but it’s really building-specific.

BTW, back when I bought my condo in Tulsa, in about 1989, banks were collapsing left and right, and I bought the condo from a local bank that had ended up with it. The entire floor of the tower had been redeveloped by a developer that combined the 12 units into 6 big units. I was told he had borrowed $250,000 from that bank against the two units (that had become one) that I bought. I paid the bank $100,000 for the 1,800 sf condo on the 23rd floor, and I got a mortgage from that bank for $110,000, with the $10,000 being to finish up the work on the condo, which I did. I charged the down-payment of $5,000 to my credit card, LOL, but paid that off within months. The bank itself collapsed a few months later… and my neighbor bought his unit (same as mine) from the FDIC for $80,000 in cash (this would amount to about 30% of original loan value).

In those years, you couldn’t get financing at all for condos; and they sold for cash. The bank that sold me the condo had to agree to finance it or else it wouldn’t have been able to sell it at all because I wouldn’t have been able to buy otherwise and it had been trying to sell the unit for a while. The reason you couldn’t get loans on condos was because banks had lost huge amounts of money when the condo bubble in the oil patch blew up, and thousands of banks in Texas and Oklahoma collapsed, including MBank in Dallas where I had an account. I don’t know when you could start borrowing properly on a condo again, but it took a while.

I notice today a ZeroHedge (yes, I look at it occasionally) take on Wolf’s drunken sailors:

“But now that the formerly austere Germany is preparing to spend like a drunked Sturmtruppen, it no longer has any moral ground over the PIIGS.”

It has the usual large number of typos found in nearly all ZeroHedge stuff.

For myself HOA’s make condos un-investable.

But don’t forget, folks, that a 10% to 22% price drop is like an overweight Cinderella in her 40’s who let herself ‘go’ and now weighs 450 pounds. After Cinderella loses 10% to 20% of her fluffiness, she doesn’t revert to the 16 year old Cinderella she once was. Still much progress to be made! Keep it up, Cinderella.

re: “But nothing compared to what the Fed did during the pandemic”

The FED injected money at a rate exceeding all prior expansions. An all-time high was recorded in November 2020. Because of the remuneration rate on interbank demand deposits, this channeled money into stocks and housing. The payment of interest on interbank demand deposits is a monetary policy blunder as high real rates of interest have an economic multiplier effect.

California has the 49th lowest rate of home ownership! Only state lower is NY. In the town that I lived in, it was 30%. No joke! 70% renters.

Oh, and what was the recent news – that in the U.S. the average age of homebuyers is 56 (for 2024). Fifty six.

What a screwed up market! What a bizarre world we now live in.

70% renters is a BS number for California overall. 44% of the households in California are renters, compared to 35% for the rest of the country. In the city of San Francisco, 65% are renters, and that is the highest in California, and maybe one of the highest in the US. In big densely populated urban cores, such as San Francisco, multifamily totally dominates, and lots of renters live in multifamily buildings/towers, including renting condos. A lot of this stuff is higher end. If you want lower-cost, you move into the distant suburbs or towns, with a 1-2-hour commute.

Jaylen

I wouldn’t be surprised if a lot of the renters have subleted to other sub-renters and are pocketing the profits from packing more people in these units than was in the rental contract. This happened to me when some college punks moved into the house next to me. They packed 5 people into a house with only 2 listed on the rental contract. The house was trashed, and rats infected the place.

You deleted my link which showed a 55.8% home ownership rate in California. The town I lived in was like a small San Francisco (a smaller coastal town) and had a 30% home ownership rate. Sky high prices. Just to clarify.

You said “70%,” which is BS.

It’s 45% of households, for the state overall. Go check the actual data.

Condo HOA fees in the Seattle region have gone totally insane. The standard now seems to be around $600/month though they go higher. Some include some minor utilities in older buildings.

It’s still amazing to think you’ll pay $7k+ a year in fees. Most homes Ive owned in my lifetime, excluding remodels, have never cost me that in maintenance. And yes I had to clean my own gutters & powerwash once a year.

Waikoloa Hawaii six month lease on 1.2 million condo $30k versus full year HOA and taxes $29k. 5th grade math

Easton MD house 500k/2k property & school taxes = 250 year rebuy

Las Vegas, a city that captures changes in the world’s disposable income in real time, not there (yet). Mostly it’s west coast. Oakland, San Francisco, Portland, Seattle. Denver and Austin seem to be weed towns that have lost their buzz.