The minutes mentioned it. New York Fed’s Perli added some background. The Fed will likely provide details at its March meeting.

By Wolf Richter for WOLF STREET.

No one has ever drained $2.2 trillion in liquidity through QT from the financial markets, as the Fed has done since July 2022, and there is no playbook to go by. Withdrawing liquidity too fast can cause some places to run dry while others are still awash in it. Normally higher yields cause liquidity to move where it’s needed, but if it drains too fast, there may not be enough time for yields to do their job distributing liquidity, and then something blows out, like the repo market did in 2019. An accident like that would cause QT to stop. And the Fed has consistently said it wants to avoid another accident, which is why it slowed QT in June 2024 so that QT can keep going further.

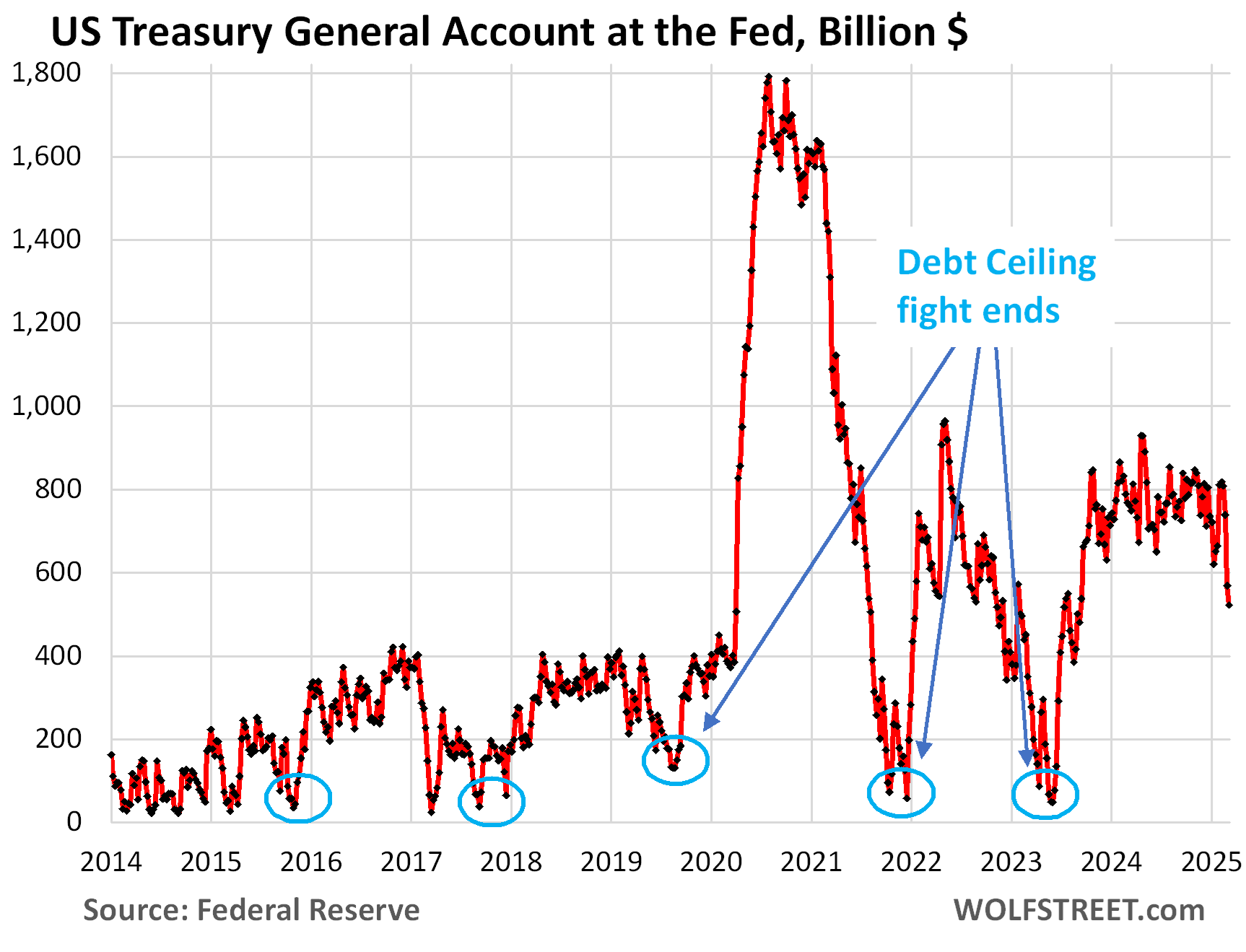

And now there’s a new potential issue for the Fed – for its balance sheet and liquidity in the financial system: the debt-ceiling fight and the $800-billion checking account of the federal government. When $800 billion in liquidity suddenly pours into financial markets and then vanishes from the financial markets even faster, it moves the needle.

The first official mention came in the minutes of the January 28-29 FOMC meeting: that the FOMC is considering “pausing or slowing balance sheet runoff until the resolution of this event.”

So, not stopping QT entirely, but pausing or slowing it temporarily until the issues of the debt ceiling are resolved.

Then on March 5, the New York Fed’s Roberto Perli, Manager of the System Open Market Account (SOMA), which handles the Fed’s securities transactions, gave a speech about the more distant future of the Fed’s balance sheet, which paralleled what Dallas Fed President Lorie Logan had said a month earlier [Future of the Fed’s Balance Sheet: How Assets Might Shift from Longer-Term Securities to Short-Term T-Bills, Repos, and Loans after QT Ends. MBS Entirely Off the List]. But Perli included a detailed discussion about the near-term issue related to the debt ceiling.

While the debt ceiling is in place, the government cannot raise more cash by issuing new Treasury securities and instead will run down its checking account at the Fed, the Treasury General Account (a liability on the Fed’s balance sheet).

Before the debt ceiling was reached, the TGA had a balance of over $800 billion, which is what the Treasury Department normally wants to keep in it. While the debt ceiling persists, that balance will be drawn down. It has already been drawn down to $530 billion. In past Debt-Ceiling fights, it was drawn down to near zero.

Drawing down the TGA effectively injects liquidity into the financial system, potentially close to $800 billion. But that’s not the problem.

The problem occurs when the Debt Ceiling gets lifted, and the government refills the TGA rapidly by issuing lots of T-bills, which sucks that liquidity back out of the financial system, and very quickly.

Last time, $500 billion got sucked out of the financial system in eight weeks in June and July 2023, and another $300 billion got sucked out over the next 12 weeks, to refill the TGA back to $800 billion by mid-October 2023. That was a lot of liquidity to vanish from the financial system in a short time.

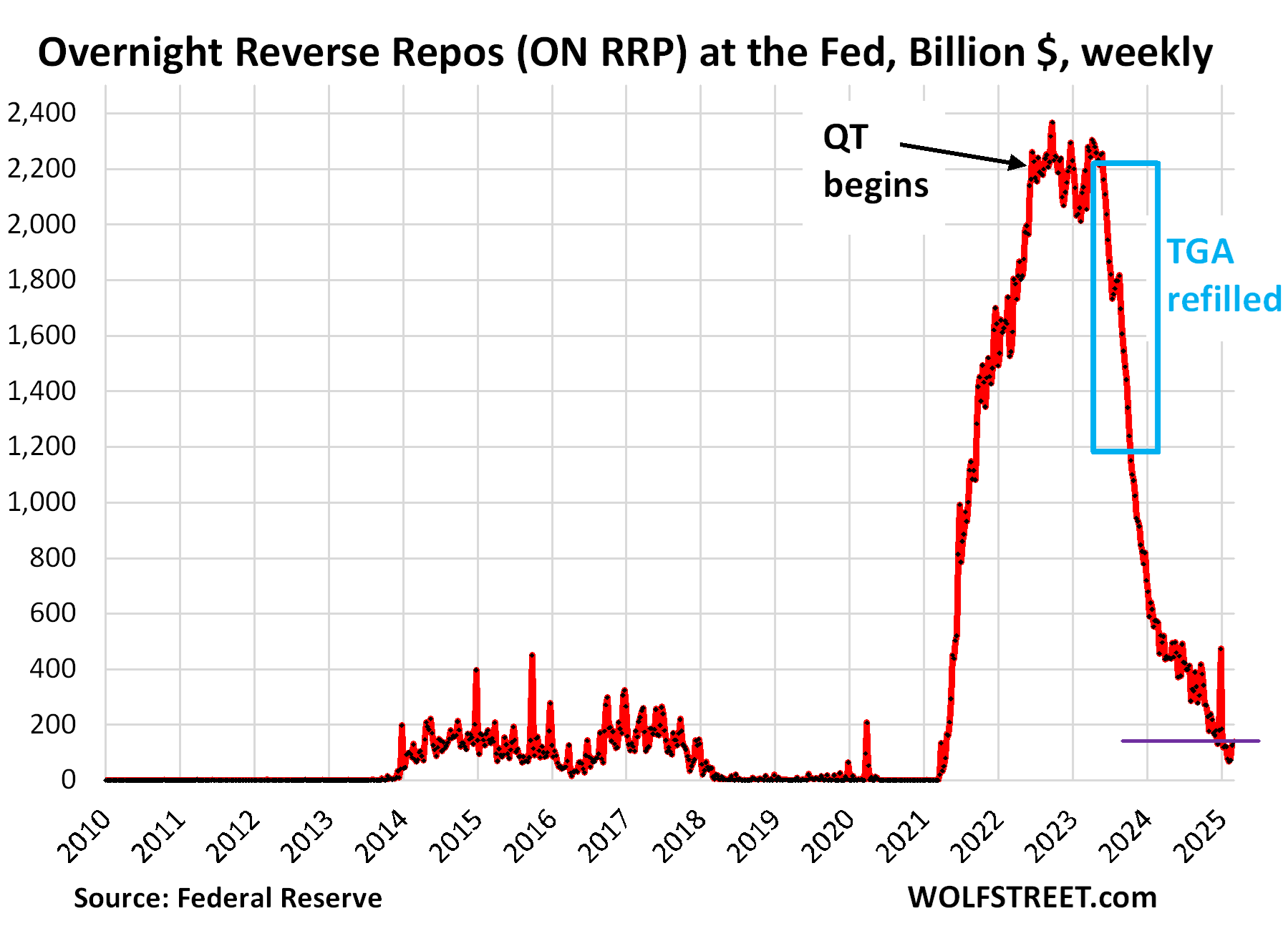

Last time, the overnight reverse repo (ON RRP) facility at the Fed, by which money markets deposit unneeded cash at the Fed to earn some interest, still had $2.1 trillion in balances, and that’s where the $500 billion came out of in June and July 2023, and the $300 billion in August to mid-October 2023.

It was smooth: Money market funds bought the massive amounts of T-bills the government issued during the TGA refilling process and paid for them with cash they got from exiting their ON RRP positions at the Fed. The cash went from the Fed’s ON RRPs via the money markets to the TGA. Both the ON RRPs and the TGA are liabilities on the Fed’s books. It didn’t impact the Fed’s assets. And it didn’t impact banking liquidity. It was unused cash from money market funds that funded those T-bill sales.

But this time around, QT largely drained ON RRPs and is starting to drain liquidity from the banking system.

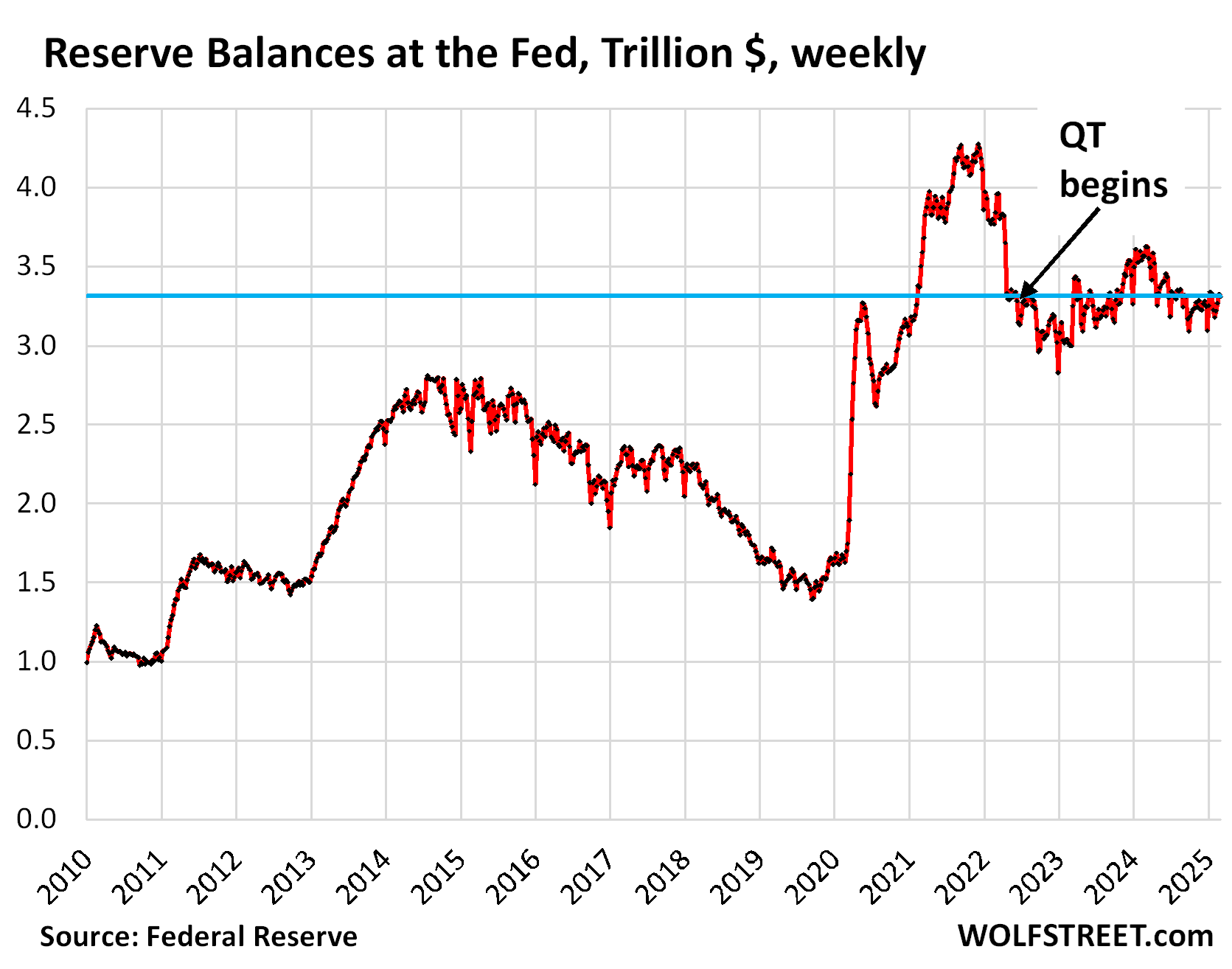

The banks keep large amounts of cash on deposit at the Fed in their “reserve accounts,” as the Fed calls them. With these reserve accounts, the Fed acts like a central clearing place for bank transactions. Banks pay each other on a daily basis through their reserve accounts at the Fed. Huge amounts of cash flow through these reserve accounts every day. In addition, banks keep substantial amounts of cash in their reserve accounts for financial stability purposes, because it is the most liquid cash.

These reserve balances are what the Fed is trying to reduce with its QT. And they haven’t come down yet at all because all of the QT came out of the ON RRPs, and now, during the Debt Ceiling, liquidity is moving from the TGA to reserves.

So now, that liquidity needed to buy the $800 billion in T-bills that the government will issue to replenish the TGA will largely come out of the banking system – including reserve balances.

But the TGA is also now draining due to the debt ceiling, and part of that liquidity is going into the reserves, thereby temporarily covering up the drain on reserves from QT.

And this liquidity from the TGA now pouring into reserves is obscuring the effects of QT on reserves – that’s what the Fed is fretting about.

After the debt ceiling is resolved, the government will refill the TGA quickly, and this sucks liquidity back out of reserves, very fast, much faster than QT, potentially hundreds of billions of dollars in weeks.

The Fed is worried about the speed with which this happens after the debt ceiling, and that its signaling system – such as surging yields and spreads related to repo markets – will warn of reserves being low enough (near “ample”) in real time, rather than in advance.

By which time it may be too late, and liquidity demand could cause some major gyrations in the money markets, similar to the repo-market blowout that occurred in the fall of 2019.

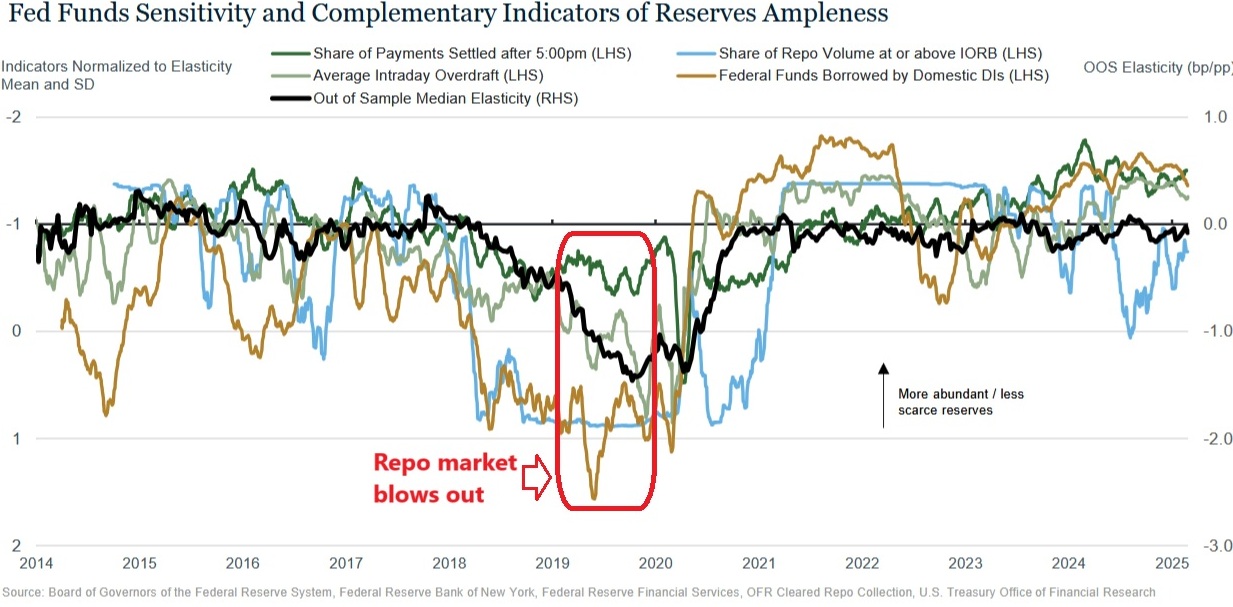

In his speech, Perli noted that reserves are still “abundant,” and not yet near “ample,” but noted that “there is evidence that pressures in the repo market have been gradually increasing.” And he added, “For now, these signals from the repo market suggest no cause for concern.”

And he said with regards to the rates and spreads they’re following:

“With the partial exception of the repo indicator, these measures are currently all toward the top of the chart, and about in line with their benign levels of a year ago.”

“On the other hand, you can see that during periods when reserves were becoming less ample, as was the case in 2018 and 2019, these indicators tended to show movement and were further toward the bottom of the chart.”

This is the chart he referenced. I added the red box to show the period when trouble in the repo market arose after QT drew down reserves (click on chart to enlarge).

“Pausing or slowing balance sheet runoff until the resolution of the debt ceiling situation.”

To forestall a blowout in the repo market or other segments of the money markets, the Fed said in the minutes that it is considering “pausing or slowing balance sheet runoff until the resolution of this event.”

Perli provided some details in his speech and repeated the language from the minutes:

“Sharp and sudden changes in the supply or demand for reserves [through the TGA getting drained and then refilled] could in principle prompt reserve conditions to shift rapidly, depriving our indicators of much of their early warning potential. One factor that could lead to large and relatively fast swings in reserves is dynamics related to the federal debt limit.”

“Put simply, the longer balance sheet runoff continues while the debt ceiling situation persists, the higher the risk that, upon the resolution of the debt ceiling, reserves could rapidly decline to levels that could result in considerable volatility in money markets. “

As noted in the minutes of the January 2025 FOMC meeting, various participants thought it may be appropriate to consider pausing or slowing balance sheet runoff until the resolution of the debt ceiling situation.”

The back-to-back announcements about “pausing or slowing balance sheet runoff until the resolution of the debt ceiling situation” indicate that the Fed will provide further details fairly soon, likely on March 19, after the FOMC meeting.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

$800 billion is 32 months of Treasury securities QT at current pace.

I think I get it. The Treasury maintains an $800 billion chequing account funded with T-bill issuances out of which it pays its obligations during any period after the debt ceiling has been reached until it is lifted. When ithe ceiling is lifted the chequing account is replenished with further T-bill issuances which occur concurrently with regular T-Bill issuances to fund the monthly deficits. The concern is that the regular fed tightening runoff would choke the system if it continued during the replenishment. With all that is happening in the Trump administration at the moment I can see why the Fed wants to avoid a failed treasury auction, and I guess all this does is smooth out the demand, although I wonder, could the Fed have finessed it by selling securities into the market to fill the void when the debt ceiling prevented treasury issuances to maintain the pace of the runoff?

At these asset price levels, any bump in the road has potential to create market panic. The financial system is fat and lazy. Shame on authorities who shunned exercise and fed donuts to the system for 30 years.

Dogecoin has a market cap 2x that of Subaru who produces cars. WTF is a DoggyCON, and what does it produce? Jerome Powell and his sick and twisted banker buddies caused this.

Depth Charge,

Musk (and to a lesser degree Trump) had a far larger role in pumping up the scam bubble of DOGE coin than Powell did.

I am pretty sure you can’t see this though.

Withdrawing liquidity too fast can cause some places to run dry while others are still awash in it.

I agree with the philosophy but disagree with the reason.

Great article, thanks.

Interesting, Mr. Wolf, you should have been a plumber.

Only place I’ve ever found analysis like this – simplifying the most abstract systems that create

the flow that is all around us, in damn near understandable terms.

Rational economic behaviors. Let’s hope we can maintain them.

Please let there be enlightened macro incentives for us to all carry on. Our good neighbors to the north and south, as well.

Actually the Federal Reserve ought to have a blog like this, stating its rationale in simple, chart-illustrated terms.

But since they have to speak in carefully-hedged, anodyne, obscure gobbledygook, Wolf Richter was obliged to step up to the plate.

If I were president, I’d dispatch the entire FOMC to Fort Knox to count and stack gold bars (if there are any) with their bare hands … and keep tallies with charcoal pencils by flickering firelight.

Agreed. Then the mass media could conjure up more upside down cake and whistles.

Ah, there is the rub. Rational economic behaviors are totally dependent on one’s current station in life.

Thank you Wolf for detailed explanation. Appreciate it.

I understand that TGA drain out can increase Reserves in short term but when Debt ceiling fight is over, filling up TGA could bring down Reserves at much higher speed than FED and Markets can handle using current mechanisms.

My question: Now FED has reopened the SRF to handle such sudden surges in Repo Markets/Reserve fluctuations. Will it not be helpful? Isn’t that purpose of SRF?

I understand FED’s pro-activeness. But I am also worried if FED gives an inch, Markets take a Mile. Pause/Slow down can become Permanent soon enough. Last year ‘slowing down so that we can go further’ approach will be defeated too. We still have Abundant Reserves.

Yes, the SRF will be very helpful. But there are still kinks in it, according to the Fed, and it’s trying to work them out, including the time when trades settle, and the auctions times.

“if FED gives an inch, Markets take a Mile.”

What throws liquidity into the markets is the draining of the TGA. And that’s already going on, and yet, stocks are tanking. But the Fed is worried about the money markets (repo markets, etc.) when the TGA is getting refilled. And that’s a different issue.

I wonder if Trump could dust off Executive Order 11110 ?? Used by John Kennedy back in 1963 to issue a limited run of National Currency Notes. Maybe send a few hundred billion over to the TGA if Congress is unable to act on the deficit.

Let us not consider the Fed as a sainted. Especially since they are the ones who screwed the pooch in the first place.

Yes, I think their public attempt at demonstrating rehabilitation is believable.

Their balance sheet is still obese and they are still paying the ones that caused the victims, America, too adjust.

The details of SRF may be useful as a reference. Right now the SRF has a $500B balance limit. I was not able to find what the current balance is.

https://www.newyorkfed.org/markets/repo-agreement-ops-faq

The current balance of the SRF today = $0. It’s reported daily by the NY Fed, and it’s reported weekly on the Fed’s balance sheet. And I discuss it monthly as part of my Fed QT articles.

https://www.newyorkfed.org/markets/desk-operations/repo

I never thought the debt ceiling was of value except to a few Congressional grand standers. I believe the current administration asked Congress to allow automatic increases for a couple of years. Wouldn’t that just create potentially a much bigger issue for the Fed down the road? Maybe Congress should just get rid of it.

Well, yes if we lived in Disneyland. Unfortunately, we live in the dog eat dog world that democracy attempts to mitigate. Like a heavyweight prize fight.

The Republican economic plan, the game plan, is fuck the deficit we are going to pass the tax breaks for the wealthy, come hell or high water. IMO

The rest is just theatrical misdirection.

What a surprise. They want to spend and grift at will for the next couple of years – but not permanently, just so they can then make it available as a political grandstanding issue again, just in case if (when) they screw the pooch so badly that the other guys manage to get back in. See the Tories in the UK.

The American electorate has the memory of a goldfish.

The average IQ is 100. Half the electorate has an IQ below 100. So, yes, we are ruled by such. Welcome to the Idiotcracy.

If Congress got rid of it they would be eliminating one of the few tools the actual budget cutters have at their disposal. While it may be all Kabuki Theater in the end (since the Debt Ceiling ALWAYS gets raised)… the budget cutters usually do get some concessions out of the negotiations.

Yep, the ceiling made some sense when the dollar was backed by a commodity, gold or silver,take your pick. After Nixon ‘s executive order It is only backed by the full trust in the U.S. Federal Government. Dang, how self-serving is that? Lol.

Could it have to do with the fact that more than half of CRE loans are coming due in 2025 and if liquidity gets tight, rates could rise in that environment wrecking havoc with local and regional banks?

Clip from NY Times:

“The debt on those office buildings will soon come due, whether or not the spaces are full. More than half of the $2.9 trillion in commercial mortgages will need to be renegotiated by the end of 2025. Local and regional banks are on the hook for most of those loans — nearly 70 percent, according to estimates from Bank of America and Goldman Sachs.”

Nonsense. This is a confused mess, and the numbers are BS.

1. total CRE mortgages outstanding = $4.8 trillion. CRE is dominated by multifamily, with over half of multifamily loans guaranteed by the government. CRE also includes industrial (in pristine condition), retail, lodging, life sciences, and office.

2. Only 20% ($957 billion) of ALL CRE mortgages mature in 2025.

3. Office CRE mortgages = $815 billion

4. Only 24%, or $195 billion of office mortgages mature in 2025.

5. The majority of CRE mortgages and most office mortgages are held by global investors (pension funds, bond funds, REITs CMBS, CDOs, family offices, etc. around the world), not banks.

Data from Mortgage Bankers Association (MBA).

So, Wolf, you present fact from a reliable source to refute Observer’s comment. I do believe that Observer made their comment in good faith, citing what appeared to be reliable data sources (NY Times, B of A, Goldman). Do you believe the misinformation is driven by incompetence or by willful intent to misinform? Made me think of a quote attributed to Napoleon…

“Never ascribe to malice that which can adequately be explained by incompetence.”

Reading comprehension is likely the problem. Observer likely didn’t read the article he cited, just read the quote on X or somewhere, and instead of reading the quote carefully, he ran with it because it was more fun to spread around.

So re-read the quote carefully. Seems you didn’t read the quote carefully either, LOL. The quote talks about two different things, separated by a period. The article likely discussed both things separately, but that context is missing from the quote

#1 item in the quote is about office debt: “The debt on those office buildings will soon come due, whether or not the spaces are full.”

#2 item in the quote is about CRE debt in general: “More than half of the $2.9 trillion in commercial mortgages will need to be renegotiated by the end of 2025.”

Lacking the rest of the article, we don’t know for sure what the “$2.9 trillion in commercial mortgages” refers to. My gut feeling is that it refers to total CRE mortgages but without multifamily CRE mortgages, which is a common distinction. The MBA for example talks about “commercial and multifamily mortgages.” In this sense, “commercial mortgages” = industrial, lodging, retail, office, and life sciences, but not multifamily.

This is why I called Observer’s comment “a confused mess.”

Congress needs to be held accountable for setting, and maintaining, a Federal budget. That is their job. Talking about a debt ceiling when you don’t have a budget is like using your credit card when the bank is overdrawn and you don’t have an income.

The whole process of becoming financially responsible starts with a budget. Talking about the amount of debt that can be incurred requires this.

Set a budget. Hold the agencies responsible to that budget. Draw down the debt. Act responsibly. Is this too much to ask?

Apparently, as the last President to have a balanced budget was Clinton

Imagine that. A balanced budget hammered out between Clinton & Gingrich. Hard to see that happening now. Back then there were only billions at stake. Today its trillionsssssssssssssss at stake.

They don’t even bother railing about millionaires.

By what means is Congress ever held accountable for anything? These topics are too complex for the average voter to understand. Since Congress is accountable only to the voters there is not likely to be any “come to Jesus” moment in the foreseeable future.

Remember that in fact, the members of Congress are accountable to no one. Thanks to gerrymandering, the members have chosen their voters so it doesn’t matter what they do. My representative is the absolute worst but he will safely win re-election with over 60% of the vote forever.

Escierto – remember also that the Founders only placed a LOWER population limit on Congressional districts, but no UPPER limit, which was then exacerbated by the House fixing its numbers at the current level waay back in 1929! It might be observed, given that the nation’s population has roughly-doubled since then, the halving of of the power of the average citizen’s actual DC-representational vote has greatly reduced the influence of local politics (even in its own understanding of it’s growing distance from them) and the necessary sausage-making of inter-Representative legislative compromise on same in favor of our current extreme divisiveness and bifurcated attitudes stemming from national-party platforms and well-funded vested interests…

may we all find a better day.

More succinctly put; “K-street OWNS CONgress”

Joe & Jane taxpayer have NO representation.

The actual number of Representatives is no more than one per 30000 using the Article One arcane counting method. In theory that is why we have a census every ten years, as opposed to trying to figure out who is in fact Hispanic, e.g. Filipinos are not, but they use pesos, so go figure.

I believe the number was 433 after the 1910 census, and it went up to 435 in 1912 because Arizona and New Mexico were added, and then didn’t change after that with the exception of going to 437 for a few years for Alaska and Hawaii. So when everybody complains about “Worst Government Ever.” I’ll peg it at 1913 for the Federal income tax, the Federal Reserve, popular election of Senators, and possible machinations to freeze the size of the House.

Well, the geriatric Congress is not likely to make an informed decision before they are advised by their younger cotillion what to do.

The democratic Congress has old age psychological symptoms.

The only reason that Trump, ranting and raving in the background during the debate wasn’t noticed was Biden age related spectacle.

Wolf, if banks get a temporary deposit surge as the TGA gets drained, wouldn’t the liquidity pressures on the banks from refilling the TGA and reversing the boost in reserves be muted if the banks are not dumb enough to use those surge deposits to invest in longer duration treasuries, etc?

No. The issue is the speed with which this happens. It’s not the banks that are at risk, it’s various segments of the $5-trillion-a-day repo market. Just like in 2019. The banks were fine when the repo market blew out.

Could the Treasury be convinced to refill the TGA more slowly and avoid this problem?

They need to get off from near-zero in absolutely no time to avoid a potential catastrophe. There are huge risks connected with a checking account that is nearly empty, given the huge amounts that flow through it, such as to pay off maturing Treasury securities and to pay for daily bills.

They may not need to go to $800 billion right away. And they didn’t last time. But the first $500 billion happened in 8 weeks. The remaining $300 billions was spread out over three months.

Wolf’s quote in comment above: “They need to get off from near-zero in absolutely no time to avoid a potential catastrophe.”

Am I correct in reading this as a form of governmental bankruptcy, where the federal government is unable to meet its obligations to make payments?

This time around government payments are where the “rubber meets the road” in systemic debt crisis, and an overdrawn Treasury checking account is the contact point.

“Paper (money) is a mortgage on wealth that does not exist, backed by a gun aimed at those who are expected to produce it. Paper is a check drawn by legal looters upon an account that is not theirs: upon the virtue of the victims. Watch for the day when it bounces, marked, “Account Overdrawn.” “

— Ayn Rand

Apologies for referencing a quote by Rand, who is usually a lightning rod for big-government/small-government vitriol, but her analogy seems nearly literal.

Wolf, thanks makes sense. One more follow up if i may: Do you see the potential risk in the money markets associated with a TGA refill skewed toward the “demand” side from money funds, hedge funds, and certain banks or from the “supply” side which is mostly from banks?

i always viewed the 2019 disruption as a “supply” driven one in which banks were hesitant to provide liquidity because they were prioritizing their own liquidity needs first.

More micromanging from the Fed.

Your back handed comment suggests that the Fed operations are a nuisance, impeding the ability of the financial god’s to transact in a manner befitting the importance of wealth as the most important component of society. Perhaps.

The historical record indicates that the relative importance of wealth in determining the course of human history, is definitive.

Really?!?

They plan steps to avoid possible catastrophic effects by a government that can’t get it’s shit together and you think this is a BAD thing?

The Fed are the adults in the room these days.

NO Brian:

As usual, the Federal Reserve Bank IS, absolutely and once again, THE gangster in the room screwing those of us in the USA who are ”workers” and ”savers of the results of that working” while ABSOLUTELY PROTECTING THE BANKSTERS.

That, and THAT ALONE, was WHY the FRB was started in 1913,,, and THAT ALONE IS WHY THE FRB continues to this point in time…

Clearly for those of us not invested in the VAST machinations of the FRB and the rest of the global so called ”Financial system” the FRB and the entire antique and anachronistic ”financial global system” continues taking SO much from workers and savers now around our entire world needs to go sooner rather than later.

You put it mildly.

THAT is absolutely false. They’re not perfect but they’ve stabilized the economy and made for a far better place to live for everyone.

Perhaps the rich have benefitted more as they’re involved and play the game better but EVERYONE has reaped huge benefits from their steadying hand.

Frankly they have been the only adults in the room for the past decade. They have made a few mistakes since 2015 when the last of the politicians to want to balance the budget (John Boehner) got run out town on a rail (by his own party). But it is hard for a Central Bank to fix a nation’s financial problems when the political leaders would rather just spend their way to re-election.

Wolf,

What am I missing? While the Fed lets its balance sheet roll off, Federal deficit spending atimulus is much greater. While the TGA balance is only $800 billion, why can’t Treasury continually refill with just a few key strokes. Oilla, no need to worry a out bond issuance or spending limits.

No, the Treasury cannot create money with a click of the mouse, not even with two clicks. Only the Fed could do that, and did do that during QE. Now under QT, the Fed is un-creating money with the click of mouse, so to speak.

Since the budget is going to be balanced next year there is no need for a debt ceiling increase, assuming progress is made this year.

The budget cannot be balanced next year. It’s impossible. The deficit is too huge. If they’re lucky, they will be able to cut the deficit by some this year. And by some more next year, etc. But it will take many years of reducing the deficit before the budget is balanced, if it ever gets that far.

Sorry, I should have added ‘sarc’ label. And of course there will have to a short term debt increase no matter what cuts are made right away because the interest expense continues even if you halted all other expenditure. My non- sarc take on this is that there is zero chance of the budget being balanced, especially with the ‘plan, talk?’ to cut back or eliminate? the IRS, a key source of government revenue.

Getting getting rid of small budget items like Veteran Affairs won’t be enough but there is always Social Security to axe. Should this last be labelled sarc? Not sure: the minister of everything has called it a Ponzi scheme. Is normal economic analysis even possible with this crew?

Watch the bouncing ball of the performative budget ceiling play while the most important objective is maximizing the tax breaks for the super rich.

Restore the Bill of Rights would be a good start.

I would love to see the minister of everything cut Social Security and truly unleash the wrath of the population. Not just the elderly and disabled who depend upon it but their family members who are well aware of the burdens they face. Finally, we would be a nation worthy of our patriot ancestors.

Escierto, if that were to happen, you can bet myself and a dozen close, very old, friends would take notice and do what we were trained to do while serving in the military. Heck, we are too old to worry about a jail sentence!

“ Drawing down the TGA effectively injects liquidity into the financial system”

Govt is paying its bill all the time.

I’m struggling to understand why this instance is special and injecting liquidity into financial system. How does this differ from paying from TGA other times?

Isn’t all withdrawals from TGA stimulative?

I can connect the dots as presented in this article. But I’m not able to understand the basic premise.

“Drawing down” creates the liquidity. It throws that $800 billion into financial markets from that account at the Fed.

A steady-stage TGA, with lots of funds coming in and an equal amount of funds going out does not impact liquidity.

“No one has ever drained $2.2 trillion in liquidity through QT from the financial markets” and left $6.85T on the Fed’s balance sheet.

Agreed. There’s no playbook, but maybe that’s part of the problem.

But then again no one ever has created so many trillions using QE. Why can’t they steadily drain what they created for emergency use, now that the emergency is over? So what if stocks lose 50% of their value?

The debt ceiling always gets resolved and it is hard to have any expectation that the deficit will even be reduced over time. You either have to significantly increase revenue, cut spending or obviously a combination of both. Tariffs aren’t going to fix the revenue problem, tax increases aren’t on the table, and while there are some spending cuts possible they aren’t enough and in many cases just pushes big problems down the road to become even bigger problems or to states which creates other problems. Admittedly politics like the debt ceiling is just reality TV with unfortunately real negative consequences for many. To fix big ticket items there needs to be fundamental changes and that will never happen.

If it doesn’t, there will be massive inflation and unrest coming. If debt payments increase much more, there will have to cuts regardless of political pain.

Or they could end the ‘temporary’ tax breaks for the rich all the way back to Reagan.

That should bring in a decent chunk of income. Contigent on the IRS existing or having the people to enforce them

Or as some would say, the debt ceiling drama in DC is Hollywood for ugly folks.

Comment from half in my cups, on this erudite forum. Curious thought, USA dollar is the World’s reserve currency, but no other big players want that title.

There are many reserve currencies, but the USD has the dominant share, which dropped to 57% in 2024, from 66% in 2015.

The euro is #2, with a stable share of 20%.

Other currencies are rising. Here are the details with charts obviously:

https://wolfstreet.com/2025/01/05/status-of-us-dollar-as-global-reserve-currency-usd-share-drops-to-30-year-low-central-banks-pile-on-other-currencies-gold/

I do not understand the practical implication of the rising risk of “considerable volatility in the money markets, as Wolf quotes Perli. Are t-bills and bond funds based on t-bills now risky investments?

By money markets they mean among other things the $5-trillion-a-day repo market. The repo market is a crucial link in distributing liquidity.

DXY down about 5% from Jan 2025 high. Adds pressure to stocks

In what way does it add pressure?

If US stocks are priced in USD, they should be up 5%?

In the “great repricings” of history, both volatility and correlation seems to increase as things take hold.

Markets are upset. Uncertainty in policy, a dose of reality regarding growth/ valuations, technically overbought on a longer term basis, and some “huge volume” up days have sort of told me the “smart money” has been bailing.

They always say it’s a good time to buy: How else can they find the Greater Fool?

The markets are having a bit of a Trump Tizzy this morning with the NASDAQ now down more than 700, the Dow down more than 450, and S&P 500 down more than 125.

Core CPI is over 3.5% annualized. Recession is in the wind. Trump got his wish for lower long term rates, but because of safe haven flight because of worries about a sagging economy just around the corner.

Stagflation is starting to rear its ugly head.

DM: Stock market tumbles as Trump stokes recession fears with bleak update on the economy

Wall Street kicked off the week in the red as investors wrestled with economic uncertainty and fresh turbulence from Washington.

so basically, stocks dropped because he announced that he wouldn’t rule out letting a recession happen.

for years, stocks and other assets have been only up, with btfdippers all around, because they were convinced the fed, congress, and white house won’t tolerate a recession, and will move heaven and earth to prevent it.

just think about how screwed up that is.

My target for SQQQ is 200.

The largest rallies on the stock market are during bear markets.

yes, but that assumes that the market drops in response to declining economic conditions.

if it never drops, because everyone is convinced that the fed has their back, then you don’t ever get that opportunity

MW: Don’t expect Trump or Powell to bail out investors this time as stock market nears ‘danger zone’

It is good to know that the Fed is war gaming this out. The problem in 2018-2019 seems (to me) to have been that they just rather blithely continued escalating QT and interest rate hikes until something broke. WHEN it broke they had to completely halt what they had been doing altogether.

If I had a vote it would be to halt QT for everything except MBS’s until the Debt Ceiling “crisis” goes away (for now). As I understand it, the amount of MBS’s the Fed holds have zero impact on the reserve balances or REPO markets. Plus the Fed has had such a hard time getting rid of their MBS’s that there is good reason to let that low-level runoff continue in the background. It would show a continued commitment to the notion of QT (even if the bigger parts of it have to be temporarily curtailed) AND it would show their commitment to getting rid of their MBS holdings altogether.

Nice signaling tool all around.

I agree. Especially since the Fed NEVER should have touched MBS. All the people/corporations that created that toxic shit should be made to choke on it.