The new mantra among frackers: “Discipline” to not trigger another oil-price collapse through overproduction. Drill Baby Drill, but not too fast.

By Wolf Richter for WOLF STREET.

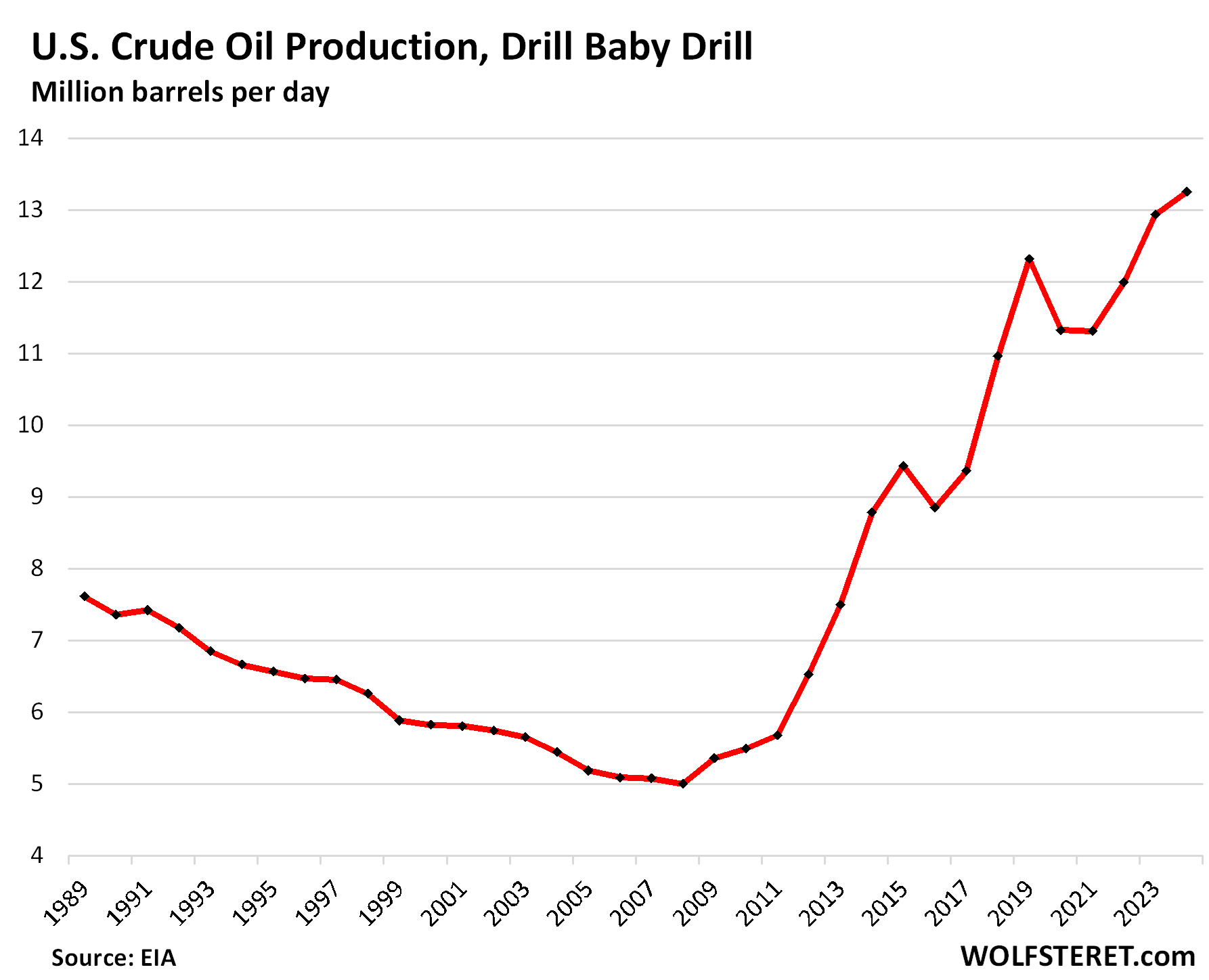

Crude oil production in the US rose by 2.5% in 2024, and by 165% since 2008, to a record 13.3 million barrels per day (MMb/d), according to EIA data.

By 2007, fracking started to ramp up on a large scale. In 2018, the US became the largest crude oil producer in the world. By 2020, the US became a net exporter of crude oil and petroleum products on an annual basis, exporting more than importing.

US oil production rejiggered the global energy dynamics, including the advantages of relatively cheap and reliable energy in the US for transportation and commercial uses, and as feedstock for the huge US petrochemical industry. The two kinks in the chart in 2016 and then again in 2020 and 2021 were the results of Oil Bust 1 and Oil Bust 2 when overproduction caused the price of US crude oil to collapse, and hundreds of oil-and-gas drillers filed for bankruptcy.

Trying to not trigger another oil-price collapse through overproduction.

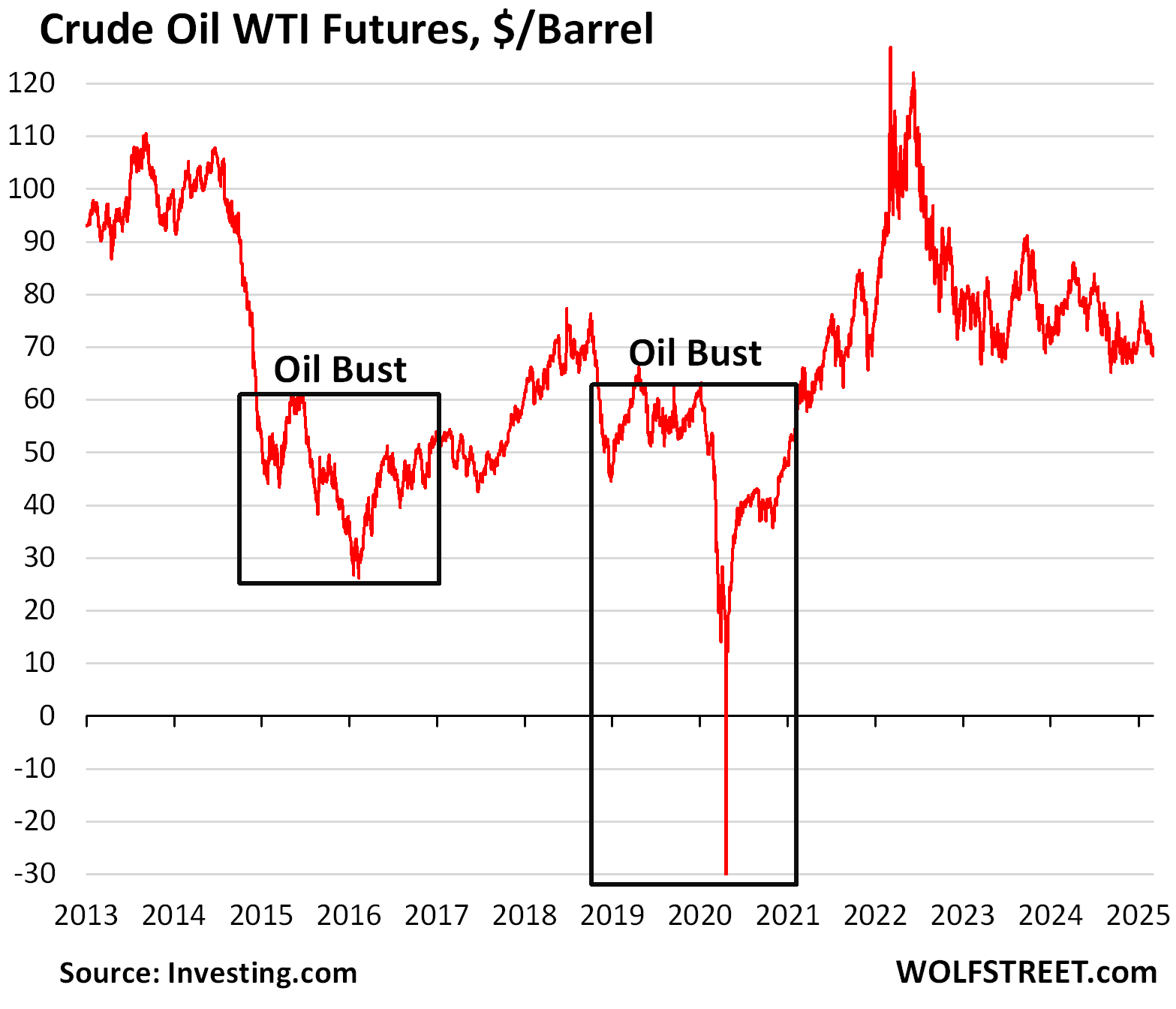

Currently, the mantra in the oil and gas industry is “discipline”: keep production growth at a pace that doesn’t collapse the price of oil again. They have learned the hard way twice in recent years, and they don’t want to relearn the hard way again, that overproduction causes the price to collapse.

They did it twice already: Leading to the 2014-2017 oil bust, when WTI plunged below $50 a barrel and stayed there, at one point hitting $26, and hundreds of oil-and-gas drillers filed for bankruptcy; and then again, leading to the 2019-2021 oil bust, when dozens of the survivors filed for bankruptcy, including three biggies, Diamond Offshore, McDermott, and Chesapeake.

Fracking is very profitable at current prices of around $70 per barrel of WTI. But the last two times WTI was selling for half that, oil-and-gas investors were massacred. There are many frackers, and each would benefit from maximizing production, but if they all do it, they’ll collapse the price, driving each other out of business. Hence “discipline” in production to not trigger another oil price collapse and Oil Bust 3.

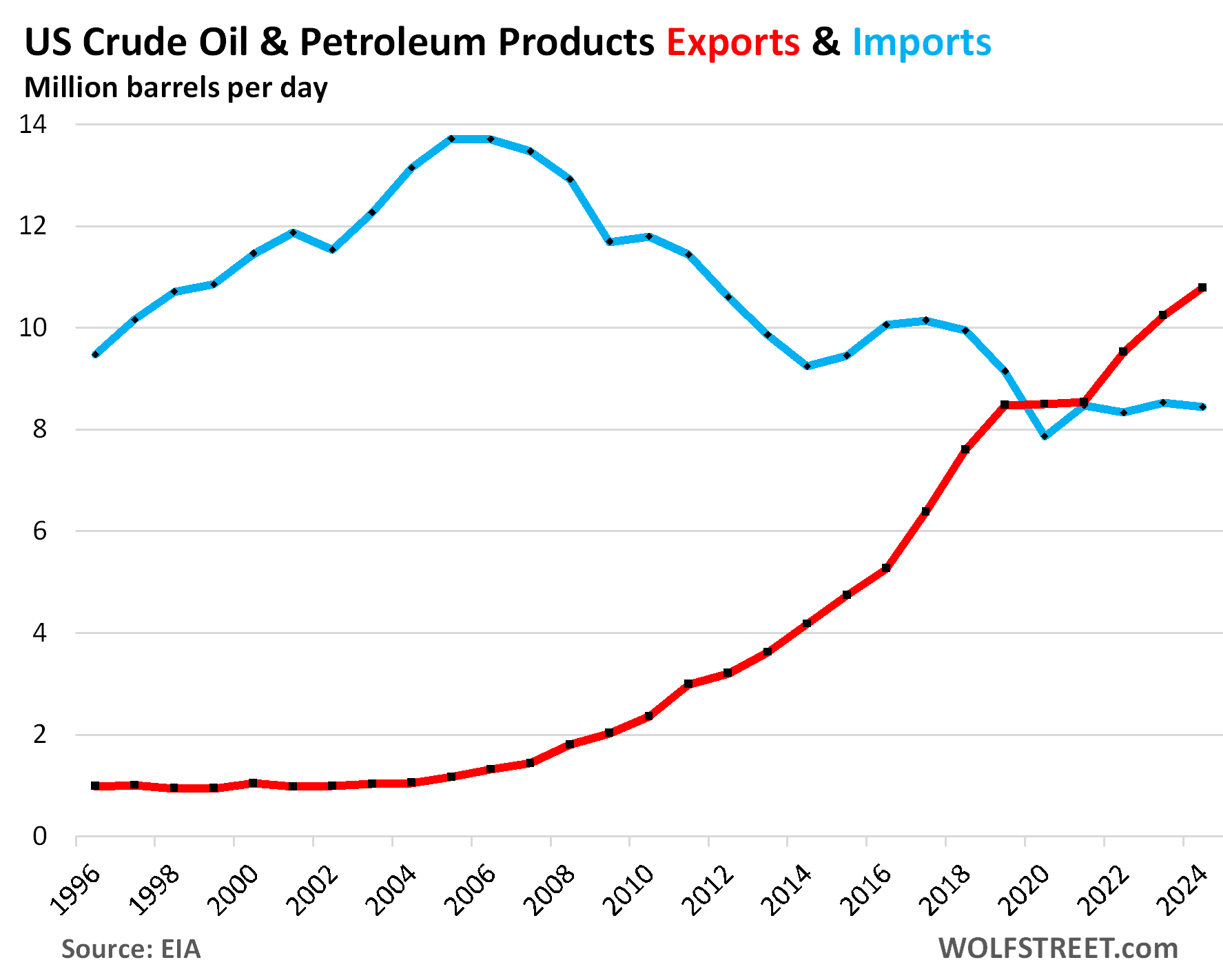

Surging exports, falling imports.

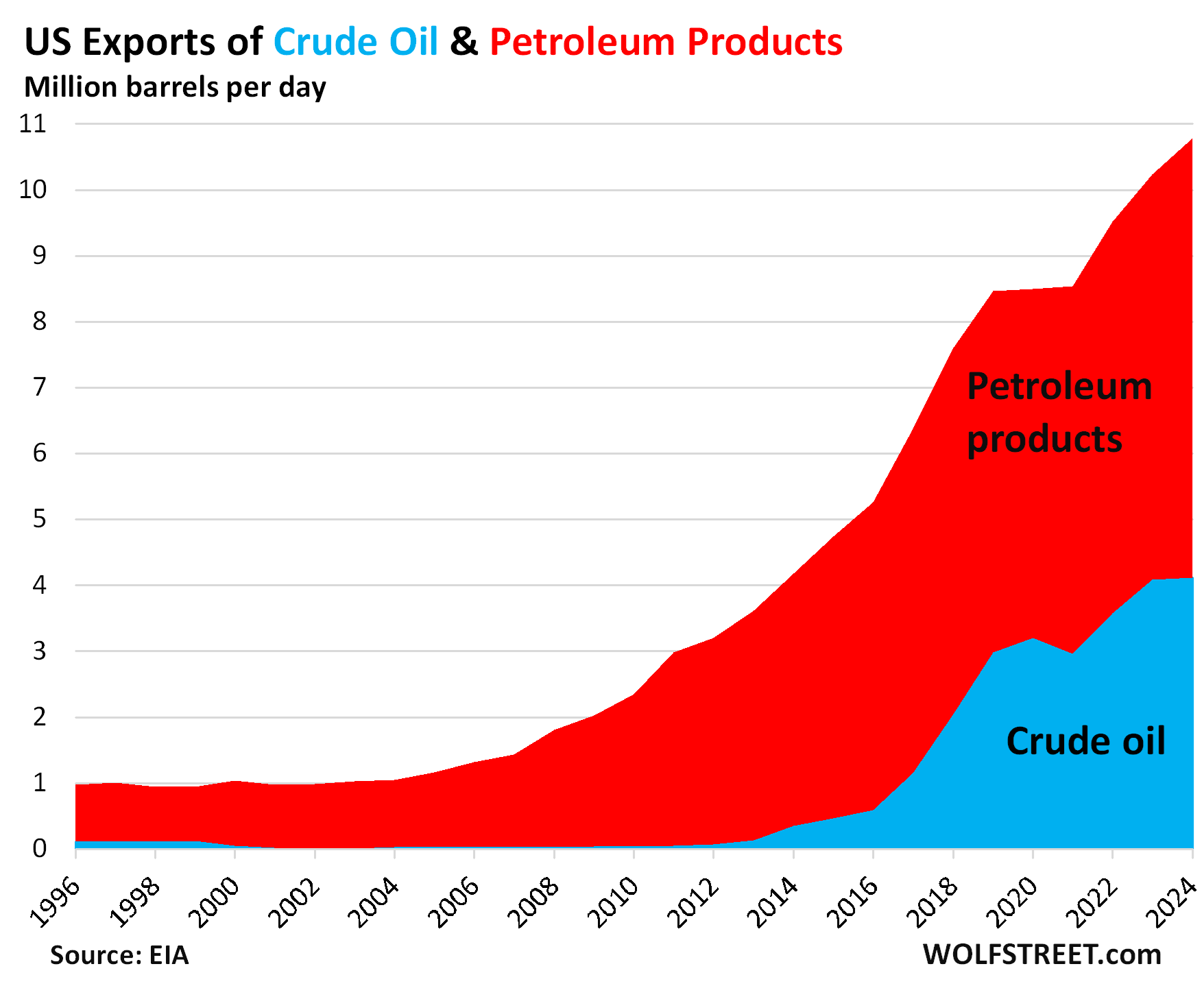

Exports of crude oil and petroleum products rose by 5.4% in 2024, to a record 10.8 MMb/d (red line in the chart below).

Imports declined to 8.4 MMb/d, far below the levels in the prior decades, which had peaked at nearly 14 MMb/d in 2005 (blue line).

In 2020, when the red line rose above the blue line for the first time, the US became a net exporter of crude oil and petroleum products, exporting more than importing:

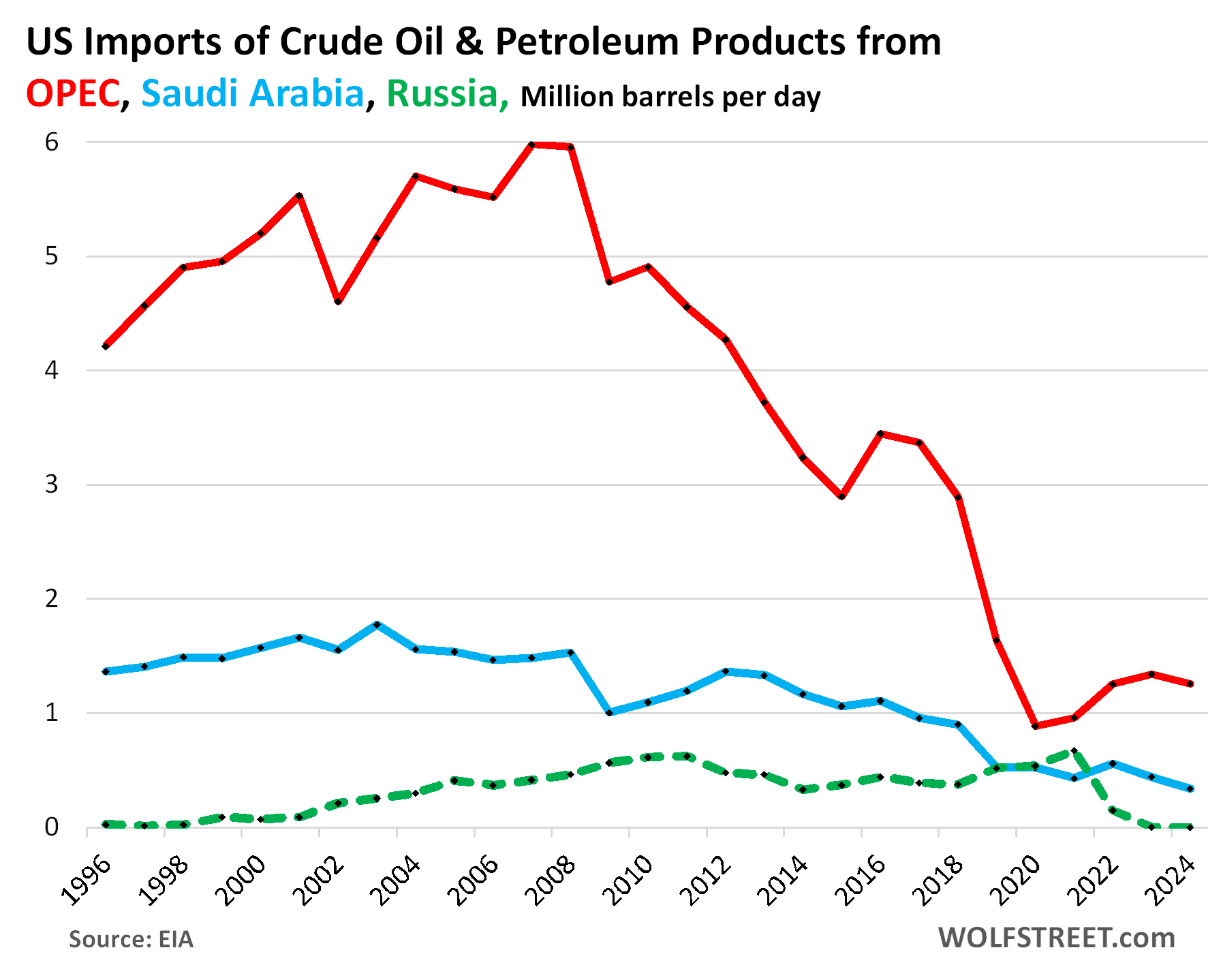

Imports from Saudi Arabia dropped to just 0.34 MMb/d in 2024, the lowest since 1986, and down from the 1.5 MMb/d range before fracking took off on a large scale (blue in the chart below).

Imports from OPEC dipped to 1.3 MMb/d, down from 5-6 MMb/d in the years before fracking took off (red).

Imports from Russia dropped to zero in mid-2022 and stayed there in 2023 and 2024. At the peak in 2021, the US imported 0.67 MMb/d from Russia (dotted green).

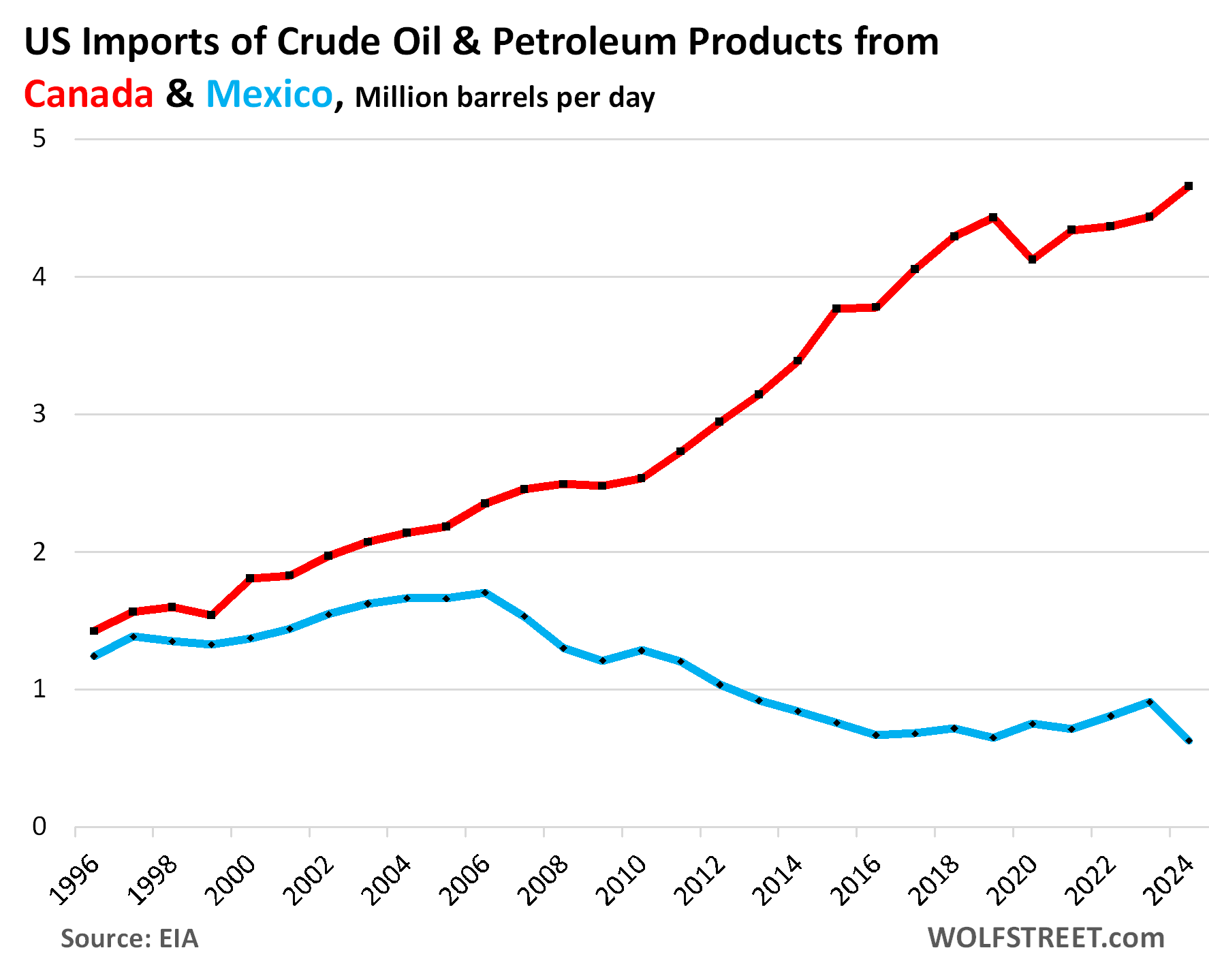

Imports from Canada rose to a record of 4.66 MMb/d, accounting for 55% of total US imports of crude oil and petroleum products.

Imports from Mexico fell to 0.62 MMb/d, the lowest since 1981.

Combined, Canada and Mexico accounted for 63% of total imports of crude oil and petroleum products:

Exports of petroleum products.

Crude oil accounted for 38% of exports, and petroleum products accounted for 62% of exports.

Exports of crude oil rose by 1% in 2024, to 4.1 MMb/d.

Exports of petroleum products jumped by 8.3% to 6.7 MMb/d. Included are 2.3 MMb/d of finished motor gasoline, distillate (such as diesel), and jet fuel.

Refineries in “oil island” California, for example, are not connected to US producing regions via pipelines. California produces some of its own crude oil, and imports crude oil from Alaska and foreign countries. But it’s also a large exporter of gasoline, distillate, and jet fuel, mostly to Latin America. The West Coast (PADD 5) exported 0.42 MMb/d to other countries in 2024.

Importing crude oil, refining it, and exporting the value-added product is a huge profitable business for refiners in the US, particularly on the Gulf Coast, which explains in part why the US imports crude oil: refiners sell the refined products to foreign customers.

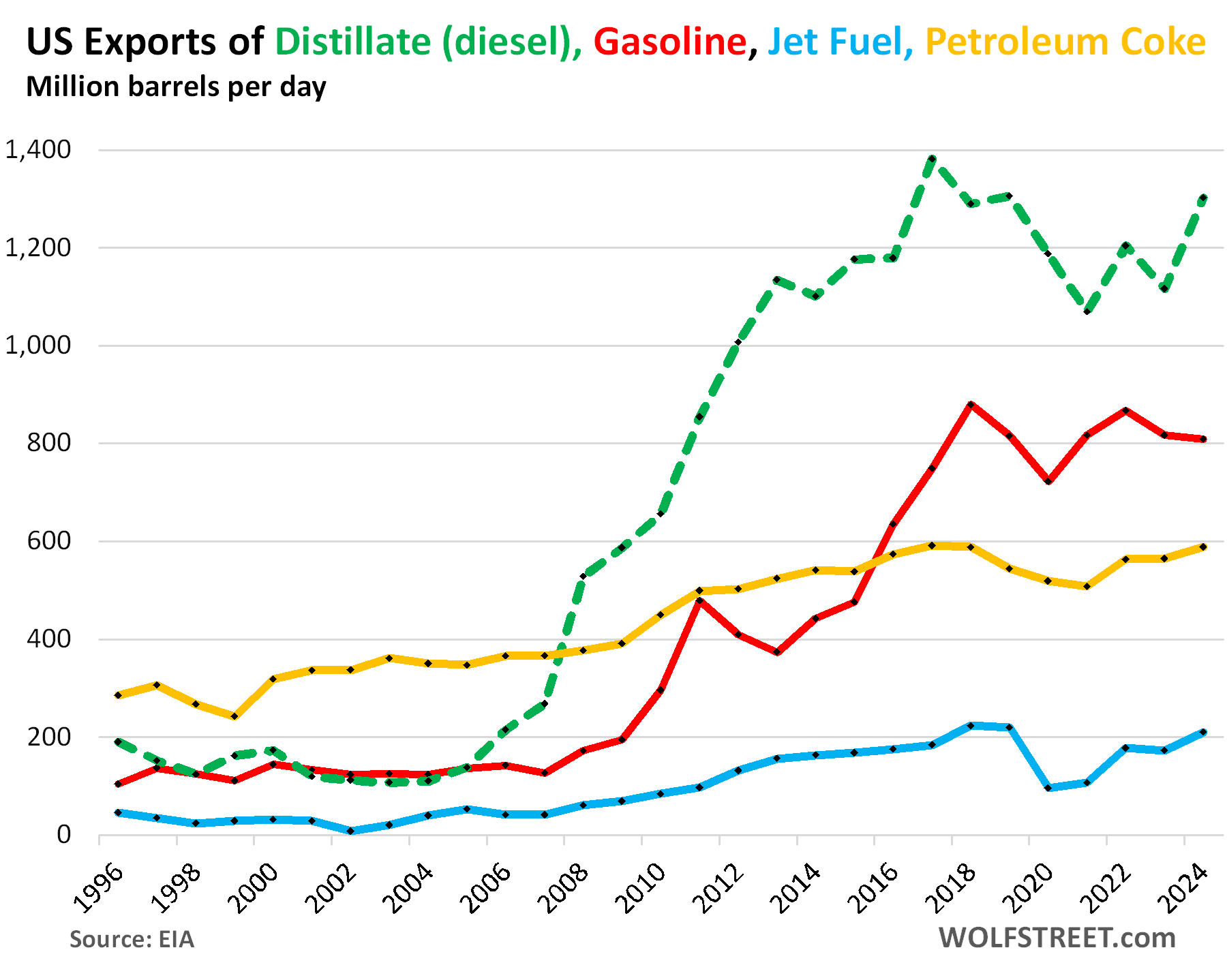

Among the many petroleum products that the US exports are finished petroleum products, of which the US exported 2.9 MMb/d in 2024:

- Distillate: 1.30 MMb/d

- Gasoline: 0.81 MMb/d

- Jet fuel: 0.21 MMb/d

- Petroleum coke: 0.59 MMb/d

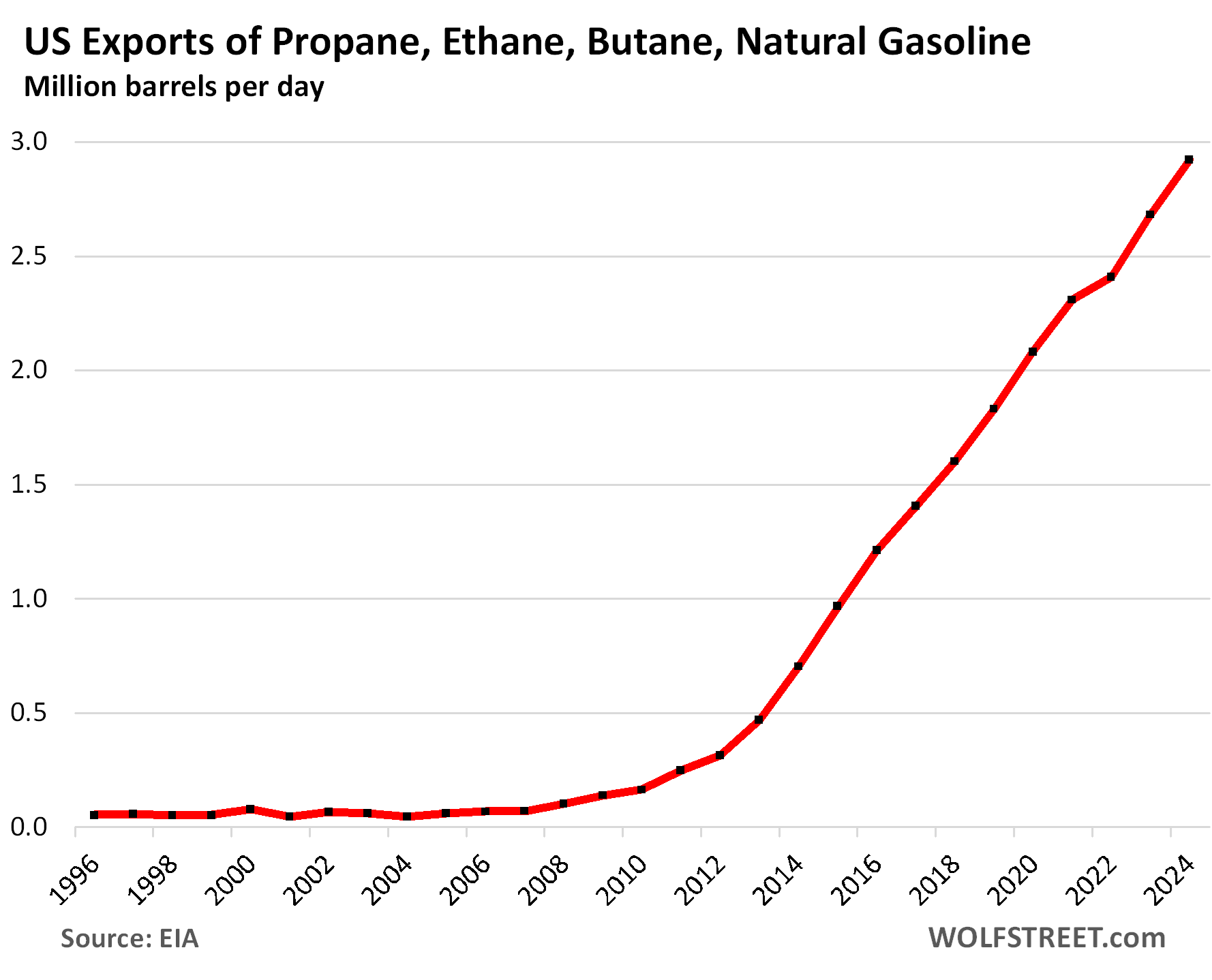

Exports of hydrocarbon gas liquids – mainly propane, ethane, butane, and natural gasoline – soared by 9.0% to 2.9 MMb/d in 2024, up from near zero in 2008, an astounding export boom:

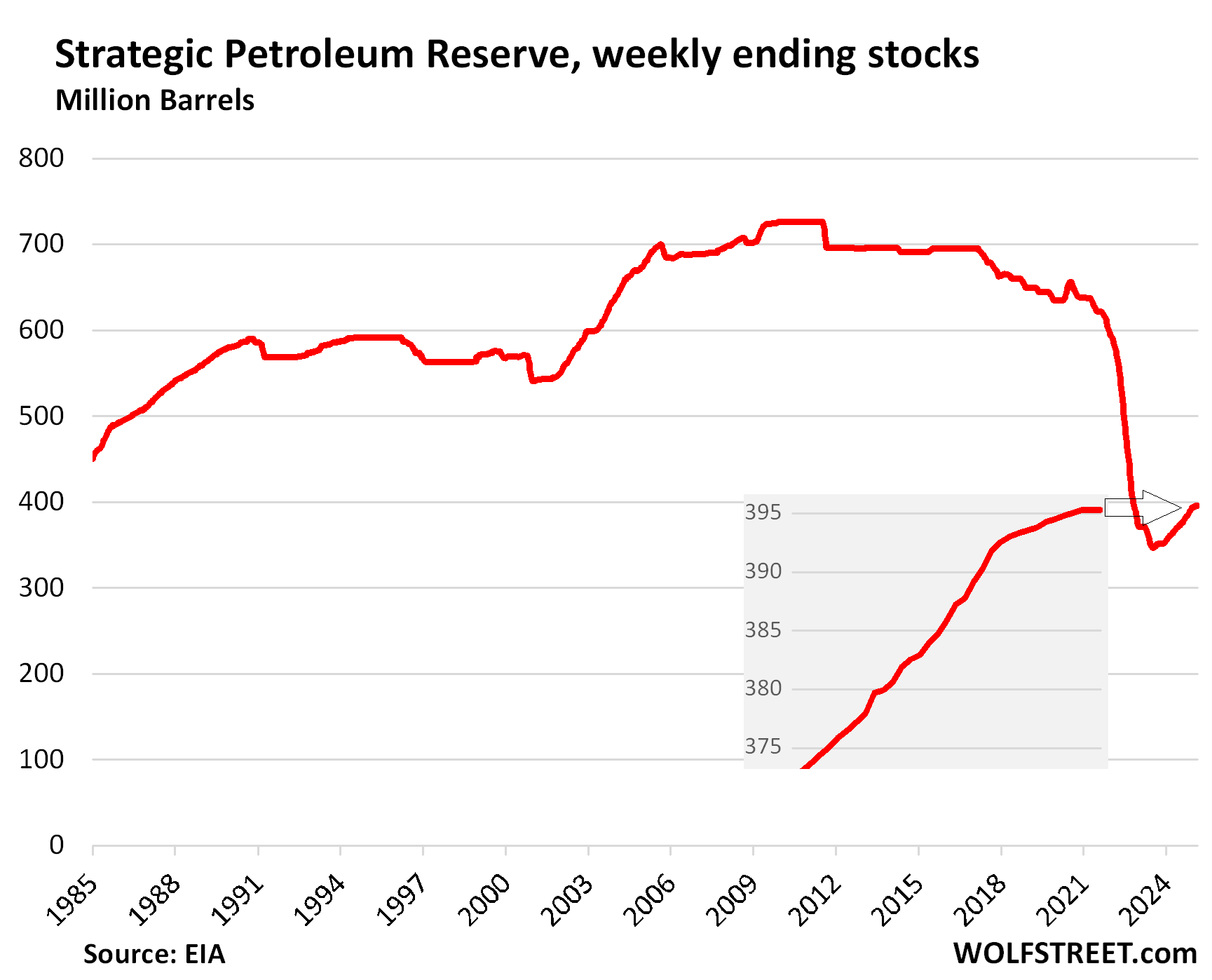

Refilling the Strategic Petroleum Reserve has halted.

The first Trump administration started releasing crude oil from the Strategic Petroleum Reserve at the beginning of 2017. Then the Biden administration released a large portion from mid-2022 through June 2023 to push down the price of crude oil that had spiked to over $100 a barrel.

Refilling the SPR started in August 2023.

But over the last two reporting weeks in February, the SPR level remained the same as in the week of February 7. Refilling has halted, possibly due to efforts by the Trump administration to allow the price of crude oil to drift lower, to push down overall inflation.

And in case you missed it:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So obviously we will 100% cease production of All That! *Waves hand* ✋🏻

And buy ALL Russian Gas. Cuz …

That’s on tap for Tuesday in a tense meeting with all the pertinent fracking executives. Tuesday because if it was Friday then SNL makes fun of everyone.

😂

*dryly* Gazprom appreciates your deflation of their rep.

But seriously, this fracking business cannot go on forever. Although new sources of oil are being accessed, they’re really OLD sources because they come attached to depleted regular deposits of oil. It’s just with new technology we can get at the remainders.

Because the oil is finite, and because the state of our energy needs is infinitely expanding and growing, we can expect to transition away from oil SOON. These are the glory years of fossil fuels; what with China building coal-fired plants to take up the slack from what the West is retiring, and more and more cars and motorcycles coming on the roads of the world, it’s looking like an Oil Century — but, like I said, it’ll be the LAST ONE.

The question of supplies is a hot potato that gets bounced around oil executives’ offices as they look at the charts of known reserves zigzagging downward, ever downward… An ornamental filigree to this whole mess is that climate change remains on the drawing boards and supposedly the nations of the world are dedicated to fighting it… The changes wrought to the atmosphere over the past hundred years necessitated doing something long ago, yet we dithered and dithered…

It’s all looking rather grim.

Nah, not true. The shale reserves in North America are actually staggeringly huge. The shale oil “revolution” was basically using an established technology (fracking) in a new medium (shale deposits). Horizontal/directional drilling is key, as well as an oil price above $50/barrel, as Wolf noted. Back when I used to run economics for BP in the early 2000s, we used a base case oil price of $16 per barrel with a stretch upside price of $20 (which we moved to $25). Amazing how things have changed.

I wonder at what point asphalt goes from being almost a waste byproduct of refining to a needed commodity? It’s not like concrete roads are cheap to make. You talked about the high value products that are easily made from the light Bakken oil and it’s definitely better to be making/ selling jet fuel, but no one wants to go back to gravel roads

Marginally related…

Fairly sure that damaged asphalt can be reheated/recycled so that a substantial percentage of in-place asphalt/roads do not need more expensive “virgin asphalt” from refinery.

Vague recollection from working 35 yrs ago for national oil company, so I might be wrong.

I had to patch road in front my drive way since city doesn’t

1 bag was $25 and does 12″ circle 2″

quote for new driveway – $5-6 SF

concrete very competitive

We use recycled asphalt on our driveways here at the ranch. They are call “millings”. They come from county/state roads that are being redone. They use a machine that chops the old road asphalt and loads to a dump truck. It makes a very good base and dust free driveway. Cost is comparable to gravel.

Tex and Cas: I was watching a show on Wonderum a few years back where it was stated that asphalt is the material with the highest percentage of recycling worldwide. I do not remember the exact percentage but it was an astonishing percentage well over 90%. Higher than glass, aluminum, iron, anything. It was hard to believe until thinking about all the highways for example redone, and the ashlphalt stipped off and always reused one way or another

Thanks, Tex, that is useful information and confirms my suspicions.

What “suspicions?”

That materials of old asphalt road surfaces are being recycled, OHG, as part of a huge government conspiracy?

History lessons:

The ONLY thing we learn from history is that we don’t learn a single thing from history.

amen!!!

On LinkedIn it was humorous to see some oil executive asking Trump to refill the SPR at 90/bbl to make “drill baby drill” reality because he warned US production would go down on current prices.

Like, yeah buddy, welcome to the real world.

The real world? …the real world where we have strategic crypto reserves coming? Refilling at $90 sounds more reasonable to me and a more reasonable action this administration might consider.

Yes. The very real world he voted for is the one where the government’s priority is blowing money on crypto.

There appears to be a typo, it looks like curd imports from Russia peaked in 2021, not 2001

And of course I have a typo my comment. I meant crude, not curd, imports. Although the latter would be really funny.

But I liked “curd” better. Russian curd is delicious. Not sure the US imports any though.

“Refineries in “oil island” California, for example, are not connected to US producing regions via pipelines. California produces some of its own crude oil, and imports crude oil from Alaska and foreign countries.”

California arguably has just as much oil in the ground as Texas – they just choose not to take advantage of it.

CA will be interesting to watch. If memory serves, the CA gov’t recently passed an initiative to shut down its oil refineries in the near term.

That’s a lie.

But gasoline demand in CA has been dropping for years, now faster than before — yes, EVs, over 20% of new vehicle sales in CA, and they don’t pull up at the pump — which is why refineries export gasoline and some 100-year old refineries will eventually be shut down because they’re not needed anymore because demand is dropping, and those old things are costly to operate. Yes, EVs.

Yeah, EVs are very popular in California (the state loves new tech), even though electricity rates are relatively high if you’re not running your own solar. Another reason to hopefully let the refineries go the way of whale oil production.

Gasoline consumption peaked in 2005. For some reason, Californians don’t like Big Oil or the House of Saud, poor them.

Short, don’t know where you got that information but,

Texas: Has the most oil reserves in the United States, with 17,031 (now estimated at 20.5 mm) million barrels of crude oil proved reserves.

California: Has 1,716 million barrels of crude oil proved reserves

I keep telling people willing to listen that the world is fast running out of “affordable” oil. “Affordable” meaning oil priced in the realm of supporting the massive infrastructure and glutonous lifestyle the west has created.

There are a number of serious minded people out there that are claiming that the Permian Basin has peaked in oil production; something worth looking into.

Regarding the proved reserve number Anthony A. has provided above…..20,500 million barrels, consider this rough analysis:

20.5 x 10e3 x 10e6 = 20.5 x 10e9 or 20.5 billion barrels. Sounds like alot. Except when you divide by 20 million barrels per DAY the US uses. That comes back with 1000 days of supply.

Now I realize there are other sources of oil, but if/when you start parsing through those reserve numbers as well, you find we DON’T have multiple decades of oil reserves left in the world that can be produced at current/”affordable” price levels.

Food for thought.

There is also the future challenge with how “dirty” fracking actually is and its effect on water supplies (over vast stretches of land.) Britain and France both have huge shale fields but in the end, decided it was far too polluting, especially as they can buy cheap oil from the USA and its shale fields.

Production break-even prices are pretty unique to each oil field. Some of the most productive ones in TX have break-evens as low as $40-$45/barrel (compared to today’s $70 WTI prices).

I understand what you are saying longer term – but there is a bit of comfort in seeing that the US daily oil consumption has stabilized at 19-20 Mbd for a pretty long time – and I’m fairly sure that some major economies (like Japan) are actually using notably less oil than they were in 2000(!).

Mike R,

1. people have claimed for 10 years that the Permian has peaked. And it hasn’t yet. So they will keep bullshitting about it.

2. the 20 million barrels you say the US “uses” includes 11 million barrels that are EXPORTED (see article above, LOL). Actual consumption in the US is dominated by the petrochemical industry and gasoline. Gasoline consumption flatlined in 2016-2019 at 9.3 million barrels per day, and then dropped. In 2024, gasoline consumption was 3.5% below 2016-2019 level.

Gasoline article coming, including miles driven and miles driven per capita.

Mike R,

Peak Cheap Oil is a giant bet against human technological progress. A sucker’s bet if there ever was one.

In 50 years, humanity will be collectively extracting, refining, and combusting more hydrocarbons than we are today.

P.s. natural gas is oil.

Proved reserves are only a small fraction of the available oil. Unproved reserves are yet-to-be-developed reserves. Proved reserves are only on the books for oil company depreciation purposes.

The actual amount of available oil is much, much greater than the proved reserves number. Once the infrastructure (drilling pads, pipelines, etc) is in place, the unproved reserves become proved.

So if you want to use a number for “amount of oil we have left to tap” you would probably want to look at the total of proved + unproved reserves. There are fine distinctions for the feasibility of unproved reserve extraction but bottom line is that there’s a lot of oil left.

Well…the thing about “reserves” is that they are continuously declining unless allowed exploration offsets the decline (and, not infrequently, locally speaking, more than offsets it).

My guess is that CA exploration expenditures are a tiny fraction of their historical levels (say pre-1970 or 1960).

Oil exploration companies know that CA is extremely hostile to oil production/transport/use – so it is likely near the last in line when drawing up exploration budgets.

But that isn’t saying the same thing as there isn’t *more* oil in CA…in fact, given CA’s old production *history* there might be a *significant* amount of oil still under CA lands.

But until CA becomes less hostile to oil, it simply won’t be explored for there.

There is a gigantic oil field in CA, the Monterey Shale, and it became part of a scam after a 2011 report was promoted that said that it could potentially yield 15 billion barrels of oil, which set off a wild surge in stock prices of the companies involved. I covered some of that here I believe. The oil is there, and it’s a huge amount, but with the technologies available at the time, it could not be economically recovered, and that was actually known, which is why this was a scam.

But drillers keep trying to find a way because that’s the big kahuna of oil in CA, and they keep working on their tech, trying to push it forward, but no cigar so far, and so the oil sits there waiting for tech to catch up, which tech has a tendency to do eventually when prices are high enough, which they’re not now. The tech progress in fracking has been huge over the past 10 years in every aspect.

Anthony A,

I’d argue CA’s ‘proved’ reserves are low because the exploration isn’t being done. Hard to find oil when no one’s looking.

CA used to be the #3 oil producer in the country 15+ years ago.

Short, I’m sure there is more there than the proven not produced numbers reported, but not 10 times as much, or even a smaller multiple. There are deposits offshore but they have been exploited for a long time and CA won’t allow any new platforms. I worked on the sale of Shell’s three platforms (Aera Energy?) off Huntington Beach about 15 years ago and only one platform was producing.

But, I did a lot of work in the oilfield in California for ARCO and recall from one of my projects (steam injection) that the Kern County oilfield (Bakersfield) was producing about 100,000 BPD around year 2000 (Chevron now). And also producing about 3 million gallons per day of produced water!

That field is huge, about 100 years old, and may be the biggest oilfield currently in production in the state. However, it’s old, in steam injection, and it’s coming to a close (someday). Plus, it’s very expensive to run huge boilers to inject steam and then deal with the resultant water that comes up with the oil.

The ancient fields around Long Beach are all played out, even after directional drilling has been tried 20+ years ago. From my memory, some are still producing, but stripper quantities of crude oil.

The “go to” states are Texas (once again) with the advent of horizontal drilling, and the Dakotas. Canada has quite a bit of oil and the Bakkan Shale field is roughly 2/3 in Canada.

Anthony, I would argue the biggest advantage of Texas vs CA is the favorable regulatory environment – this moreso than the geology, although of course they aren’t mutually exclusive. Capital tends to go where it will be treated well.

But to Texas’ credit, the Permian is still strong, and unlike the peak cheap oil nonsense, is certainly not rolling over. Right now oil supply is limited by natgas offtake capacity – they could pull more out of the ground if the gas wasn’t in the way.

Taking on the fracking environmental cost for the purposes of energy independence is one thing. To take on long term environmental debt for export profits is a form of corporate subsidization. Similar to how the cost of cleaning up old mines actually renders the lifetime profit of those mines negative at a cost to the taxpayers. Oh well, someone figured out the grift. Good for them.

Well, for a while now, there have been fees/taxes levied on oil producers to cover the capping/partial remediation of new sunk wells.

Granted there are tens (hundreds?) of thousands of wells that came long before this regime, but at least things aren’t getting as bad as fast.

Lots of those “orphan” wells are being closed, at least in Texas where I worked in the oilfield, under state funded programs. And yes, there are thousands of them in the U.S.!

We are now the United States of Grift. Is this what Thomas Jefferson and Ben Franklin had in mind?

Mostly – but only for white, land-owning men.

witness today’s action in u.s. stock market. all bs algo nonsense. nothing of value. stocks melt up all afternoon and then rug is pulled 30 minutes before closing, and stocks plummet.

this is not a healthy capital market.

If fracking is profitable at $70, the govt/SPR should be a buyer at $65 – to keep things moving without providing a windfall but to prevent large losses in driller capacity and the resulting shortage and price spike. They could also be sellers at say $90 to make a little profit for the taxpayer and keep gasoline from going too high. The SPR should be 80%+ full at all times. That’s ship, jet and battle tank fuel in the worst case.

This is a great idea, unfortunately, it’s something that would ultimately benefit taxpayers at the expense of the oil industry, so you can be certain it will never be implemented.

How much of those oil price drops were actually due to bullshit paper games in the futures market? Seem to me, with the continued deregulation and lack of oversight in markets, we may want to start paying attention.

Reduced hydrocarbons are VERY useful for industrial societies.

wolf, any shot at getting an article on nafta tariffs? this seems like a pretty big story everyone is ignoring, especially considering your interest in automotive.

I already said everything about tariffs that I’m going to say about a month ago:

https://wolfstreet.com/2025/02/03/what-trumps-tariffs-did-last-time-2018-2019-had-no-impact-on-inflation-doubled-receipts-from-customs-duties-and-hit-stocks/

https://wolfstreet.com/2025/01/13/some-basics-about-u-s-tariffs-and-what-trumps-new-economic-team-said-about-tariffs/

It’s useless writing about specific tariffs because they’re announced one day and rescinded the next day, and then deals are made and cave-outs are agreed etc.. I’ve been through this chaos last time.

Mw: Big Oil isn’t big on ‘drill, baby, drill’ — turning Trump to Canada and Greenland

It’s a sad state of affairs that the SPR became a play thing for the politicians. I don’t want to around on the day that oil is really needed but the SPR is dry.

The SPR should be drained and abolished. It is not needed now that USA is a major petrostate.

I wonder what policies or activities led up to the increase in export of petroleum products that started around 2010? Was it just the build up to fracking leading up to 2010? Or were there specific policies that helped exports after 2010?

Yes, fracking caused production to soar, this is a huge business and huge global trade, and lots of money is being made.

Unrelated to your question about petroleum products, in 2015 Congress repealed the ban on crude-oil export to non-allies, which allowed for more crude to be exported.

TBF the 2020 “Bust” was covid drop in demand when government forced people not to travel. I would have no problem with constant $70 per barrel and Trump can refill the oil reserves for a lower bulk price. They should be able to keep it consistent with ai and history knowledge.

That “2020 Bust” actually started at the end of 2018 when WTI skidded below $55, and then in January 2019, when it skidded below $50, and it stayed between 50-60 until covid. Production costs may have come down since then, but $50 a barrel for many oil and gas drillers, especially in fields with lots of gas and less oil, was not a survivable price over the long term.

WTF is “Natural Gasoline” ?

Try googling it? Comes right up. Even has its own Wikipedia article. Or a link to the EIA’s Glossary, which says (and before you ask, “NGL” = natural gas liquids):

Natural gasoline: A commodity product commonly traded in NGL markets that comprises liquid hydrocarbons (mostly pentanes and hexanes) and generally remains liquid at ambient temperatures and atmospheric pressure. Natural gasoline is equivalent to pentanes plus.

Natural Gasoline and Isopentane: A mixture of hydrocarbons, mostly pentanes and heavier, extracted from natural gas, that meets vapor pressure, end-point, and other specifications for natural gasoline set by the Gas Processors Association. Includes isopentane which is a saturated branch-chain hydrocarbon, (C5H12), obtained by fractionation of natural gasoline or isomerization of normal pentane.

Oil is cheap. For the past decade, there’s been a little volatility, but wage growth has been strong the entire time. In real terms, oil is about as cheap as it gets. If your gasoline at the pump is less than 08 era, you’re not paying much, considering wages have more than doubled over that period.