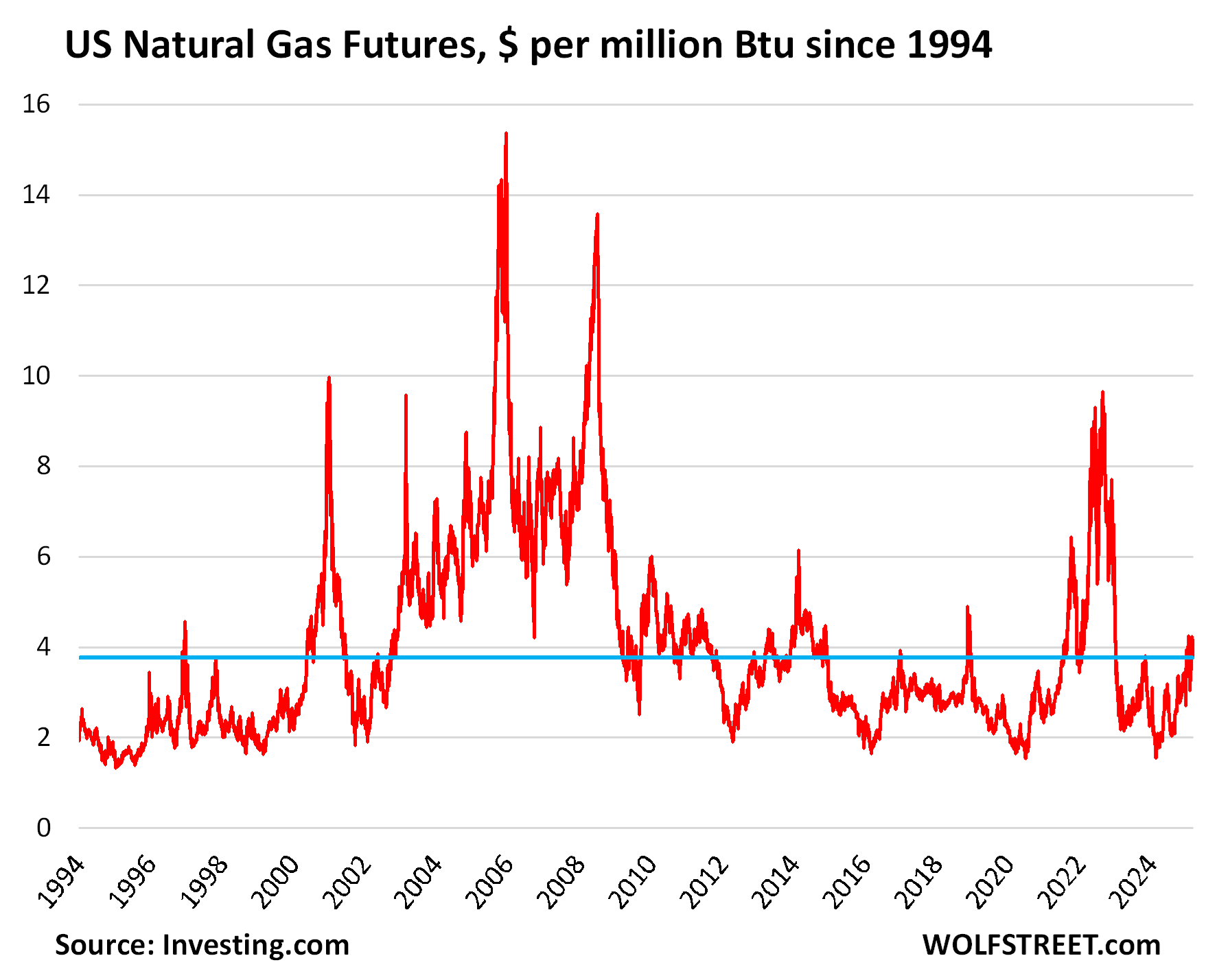

Prices rose from the collapsed levels in the prior year and are back where they’d been in 1996, down by 70% from the peak in 2005.

By Wolf Richter for WOLF STREET.

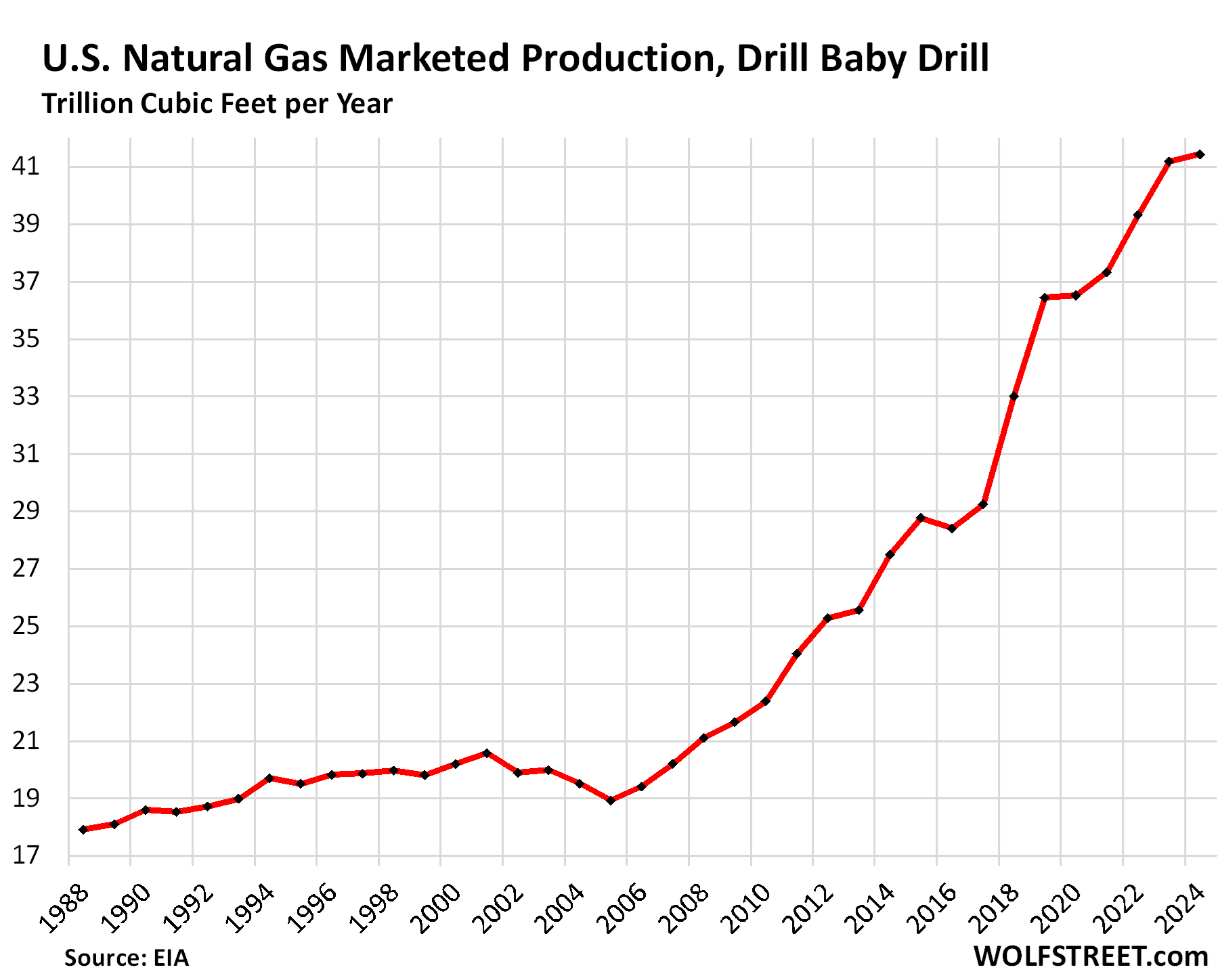

When it comes to US natural gas production, exports, and imports, a key element is that the price of natural gas in the US has collapsed since about 2008, a few years after US production from fracking took off majestically and reversed the years-long trend of declining production.

Currently, natural gas futures trade for about $3.76 per million Btu, after a 12-month surge, roughly the same as in some periods in 1996 and 1997. The year-ago price of around $1.90 was right back where it had been in 1995, despite 30 years of inflation in other products and services. The price collapsed as overproduction set in by 2009, with no liquefied natural gas (LNG) export terminals in the lower 48 states as an outlet.

A substantial part of natural gas is produced as a byproduct of fracked oil wells. Some years ago, in shale fields that lacked gas-takeaway capacity, the associated gases coming from the oil wells, including methane, were flared, a huge waste of a valuable natural resource, and also a big source of air pollution.

In North Dakota’s portion of the Bakken Formation, between 30% and 35% of the associated gases were flared in 2012 through 2014. Flaring is now down to 5%. Across the US, flaring is down to about 0.5% of total gas produced, from close to 2% in 2018, according to EIA estimates.

This concept of associated natural gas – natural gas as byproduct of oil production from fracked wells – led to overproduction of natural gas amid limited demand and was one of the factors why the price collapsed.

US natural gas production: Drill Baby Drill since the early 2000s.

Marketed production of natural gas rose by 0.6% in 2024, to a record 41.4 trillion cubic feet, according to EIA data on Friday.

Since 2006, production has surged by 113%. Since 2017, production has surged by 41%. The fracking boom in the US – including the surge in crude oil production – has rejiggered the energy landscape globally.

Some Drill-Baby-Drill milestones:

- In 2011, the US became the largest natural gas producer in the world.

- In 2016, natural gas surpassed coal as the dominant fuel for power generation in the US.

- In 2016, the first LNG export terminal in the lower 48 states came on line, and large-scale LNG exports began.

- In 2017, the US became a net exporter of natural gas, exporting more than importing.

- In 2023, the US became the largest exporter of LNG.

- In 2024, power generation from natural gas rose by 3.3% to a record of 1,864,874 GWh, with a share of 42.7% of total power generated. Coal’s share dropped to a record low of 14.9%, from 51% in 2001 (I discussed US power generation by source in 2024 here).

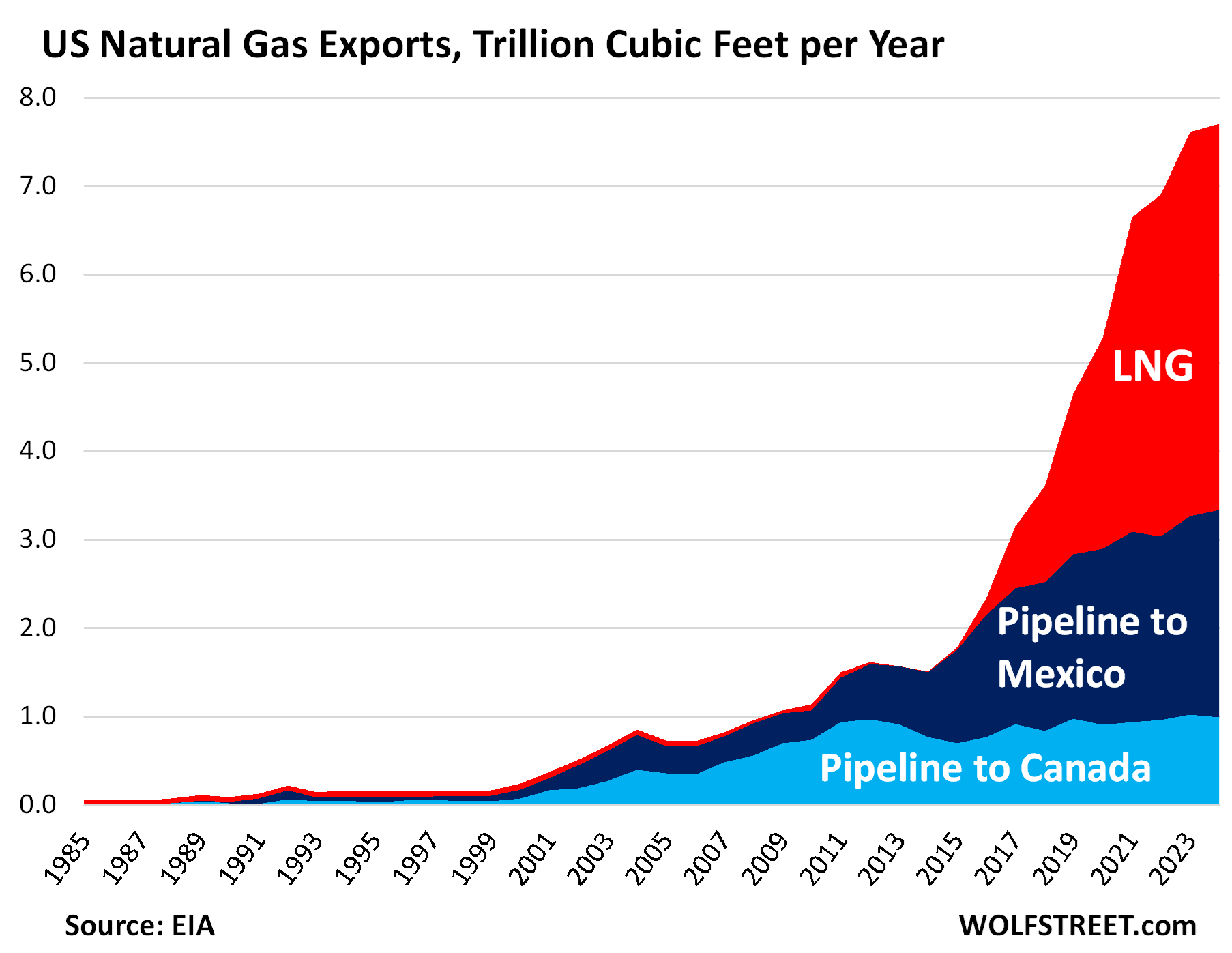

US natural gas exports.

The US exports natural gas via pipelines to Mexico and Canada. Since 2016, the US has been exporting natural gas as LNG to the rest of the world. As more export terminals were built, LNG exports soared, creating more demand for US production.

Total exports of natural gas via pipeline and as LNG rose by 1.3% in 2024 to a new record of 7.71 trillion cubic feet, or about 18% of US marketed production.

LNG exports rose by 0.6% to a record 4.37 trillion cubic feet.

Pipeline exports to Mexico and Canada rose by 2.3% to 3.34 trillion cubic feet:

- To Mexico: +4.6% to a record 2.35 trillion cubic feet

- To Canada: -2.8% to 1.0 trillion cubic feet.

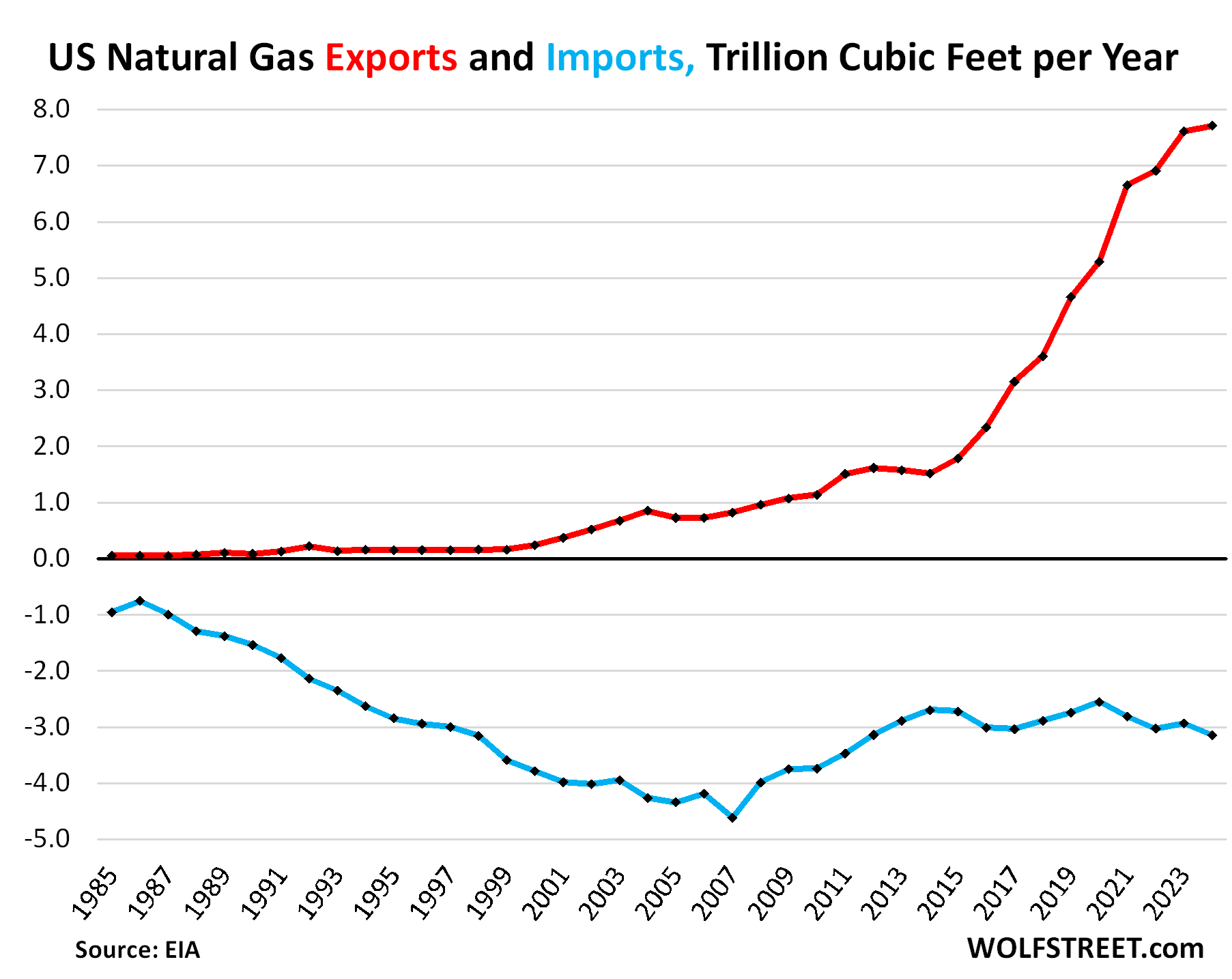

Imports increased by 7.4% to 3.14 trillion cubic feet, of which 3.13 trillion cubic feet via pipeline from Canada, and 0.016 trillion cubic feet via LNG in the Boston area, which is still inadequately connected via pipeline to the producing areas in the US.

This chart shows imports (blue) as a negative figure and total exports as a positive figure (red). The import peak was in 2007.

Canada imports from the US and the US imports from Canada because the geographical layout of where pipelines, producing areas, and population centers are. On a net basis (exports minus imports), the US imported from Canada 2.13 trillion cubic feet in 2024.

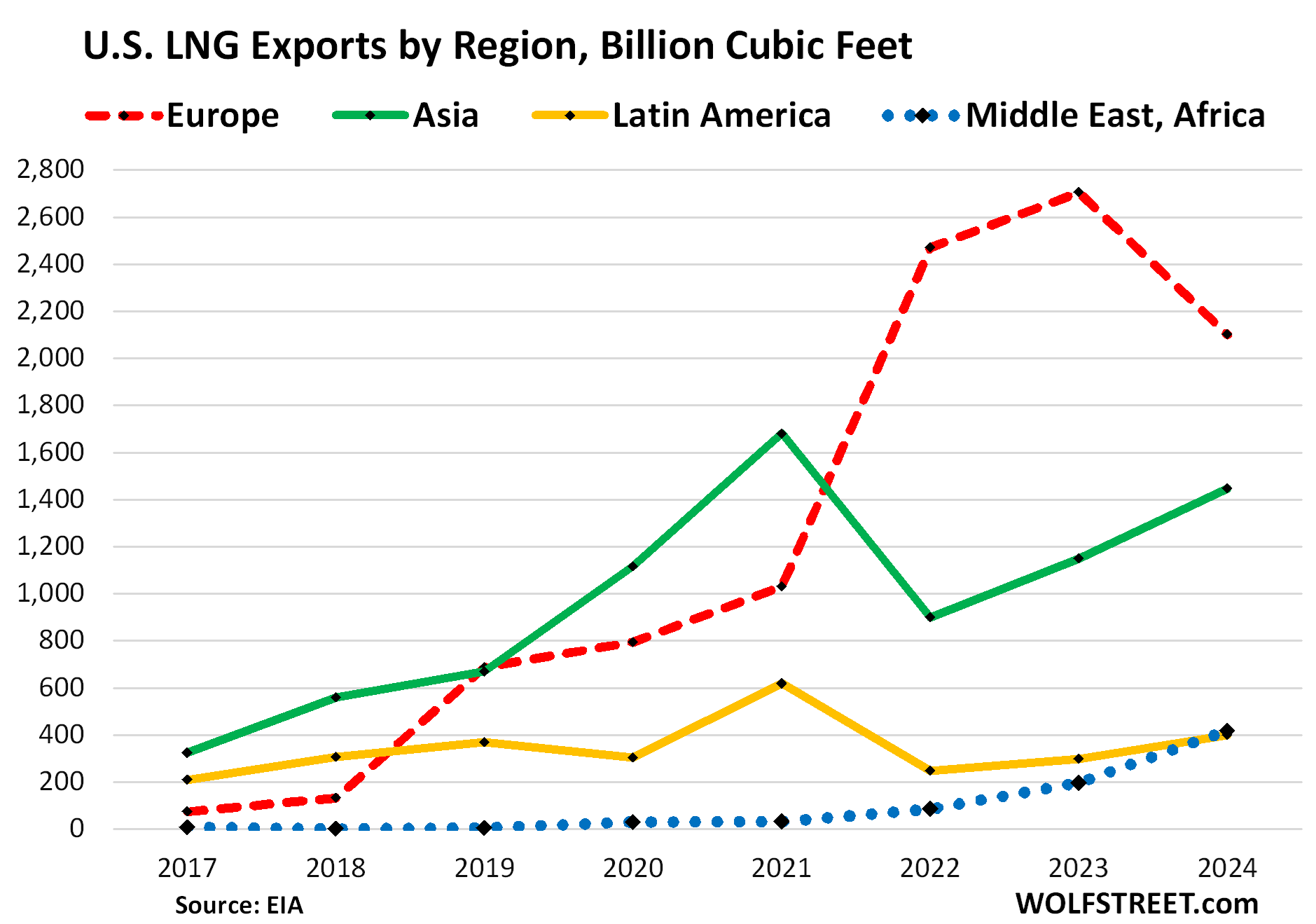

LNG exports by region.

LNG exports to Europe – the largest buyer of US LNG for the third year in a row – dropped by 22% from the record in 2023. They still accounted for nearly half of US LNG exports (dotted red line in the chart below). Germany started setting up LNG import terminals in 2022, and by 2024, 15% of US LNG going to Europe was unloaded in Germany, up from 0% in 2021. The other big importing countries were those with LNG import terminals that feed into the European system of pipelines, on top of which were the Netherlands, France, the UK, Spain, and Italy.

LNG exports to Asia rose by 33%, but were below the record in 2021. All major LNG importers increased their imports. The biggest importers were Japan, South Korea, China, India, and Taiwan (green).

Exports to Latin America and the Middle East & Africa rose but remained relatively low.

And in case you missed it last week: Demand for Electricity Takes Off, Driven by Data Centers (AI, Cloud, Crypto) and EVs. US Power Generation by Source in 2024: Natural Gas, Coal, Nuclear, Wind, Hydro, Solar, Geothermal, Biomass, Petroleum.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I find drill baby drill to be preferable to the Quixote approach of chasing windmills and building huge solar farms with questionable results and with ensuing grossly negative impacts to the landscape.

Of course, there is no perfect energy solution, except the pie in the sky fusion perhaps; how close are we to that? Let’s see, just as an analogy what the leaders and media tell us, Time magazine was stating in late 80s that super conduction was then possible. How close are we to that now?

Physical sciences, including those that lead to superconductors and flying cars, advance linearly and so more slowly that people’s imagination. Data sciences, including those that lead to analysis and AI, advance exponentially and so much faster and in more directions than people’s imagination.

High-temperature superconductors will likely come but the data sciences still need to advance to the point of being able to predict them rather than stumbling along with human-brain prediction. If they are physically possible, which seems likely, then I’d guess we’ll start seeing them within 15 years.

The flying cars concept is hilarious. Can you imagine the carnage?

On another note regarding cars, apparently Toyota is going to be bringing a hybrid to market in a few years where the internal combustion engine – a totally new design – is not used for propulsion, but as an onboard generator which charges the battery bank and runs all the accessories, with electric drive motors to power the wheels. This is the future, IMO – HYBRID. Not all EV, not all ICE.

This is what the big 3 should have been designing for HD diesel trucks long ago. You get the massive torque and hp of the electric motors, but with the range and quick fuel up of ICE. There is a lot more efficiency to be squeezed out of internal combustion engines, too.

I can assure you the Big 3 have been, and are, working on what you mention. However, whether it will go to market and/or be accepted is another story. The Corvette does what you say, uses electric for performance/acceleration. However, in a big HD truck it’s more about energy and not so much power/torque, since the diesels already provide much of that. HD is always last to go modern (electric steering, electric gearshift, etc) and for good reason, function is more important than technology, so until fully adapted/proven with minimal sacrifices and downtown, it’s not worth it, as the customers don’t fall for the marketing the same way. If it doesn’t work, they are out, because these vehicles are moneymakers for them. Look at diesel emissions devices and their perception amongst these folks, they’ll pay thousands just to rid themselves of the headache. That’s been my experience designing stuff for this crowd, anything you do…you better get it right, which is hard to do starting off with something new.

This thing you’re describing is just another version of a plug-in hybrid. Plug-in hybrids are dead. Very few people are buying them. Regular hybrids are doing well, but they’re cannibalizing ICE vehicles without hybrid drive. EV sales are soaring despite Tesla’s decline.

This thing you’re describing has proven to be inefficient because it’s inefficient to use an ICE to power a generator to charge a battery to then send electricity to electric motors to drive the wheels because there is some energy loss in the generator and in the battery when charging, and in the battery when discharging, and in the electric motors. The question for this setup is: Where is the energy loss greater: In an ICE-to-transmission/transaxle setup or in an ICE-to-generator-to-battery-to-motor setup. Automakers have looked at this for many years, and abandoned it because it’s inherently inefficient; the current ICE-hybrid setup where the ICE and the electric motors BOTH power the wheels has turned out to be the more efficient.

But Toyota’s problem is that it fell behind by 10 years on EVs, that it is now scrambling to catch up, that it promised to have dozens of EV models out over the next few years. Meanwhile it has just one model out and is just dabbling in it. Here are Toyota’s sales in the US:

Wolf: Yes and no. There is energy loss in every conversion but you can get better overall efficiency with a smaller engine running at peak efficiency all the time (with a battery to manage variations) vs a bigger engine that must vary it’s output depending on the momentary load.

Brian

That’s what a regular hybrid does by design, without all the energy loss of an ICE charging up a battery to drive electric motors.

The power of the ICE in a regular hybrid goes through the transaxle/CVT to the wheels, while the electric motor supplies power for the variations. The battery is charged through the braking system (regen braking). So just lifting the foot off the gas kicks in the regen braking and charges up the battery. Which is why they’re so efficient, compared to an ICE-only model.

Our Ford Fusion has a 2.3L low-torque Atkinson cycle engine that runs very efficiently at a steady state. But without the electric motor, it’s a dog because it doesn’t have enough torque. I know because I test-drove a Fusion hybrid whose hybrid drive had failed (I’m not sure why it was still sitting on the lot, but after the test drive with the salesman, they removed the car from the for-sale inventory).

Which is also a reason why regular hybrids are so relaxing to drive because the ICE runs at about the same quiet RPM without revving up when you gently accelerate. The electric motor supplies the additional torque. If more power is needed, such as on long up-hills, the ICE gradually increases the RPMs. The CVT makes this process ultra-smooth.

GOOD START BB:

How some ever, and apparently, it will take close to 4 ever, as it becomes apparent that only the development of the physics and the engineering following those physics will enable humans, IF THERE are any left by then, to overcome the temporary use of ”fuel” ,,no matter what form the fuel takes, to become at least somewhat to the level of human adaptation needed for permanent human life of this planet.

CAN WE do it,,, of course We can;;; WILL we do it???

Possibly, but I would not want to ”bet the farm” on the possibilities at this point in time based on SO much BS at every level and the clearly extensive BS due to prioritizing ”funding” over fundamental ”science”.

Just one more reason why I support Wolfstreet.com more than any of the others I support…

Well I am happy with that info, I hold many LNG producers, shippers, pipelines and other related stocks. Lots of dividends in that field..Europe and also data centers are in big need of LNG. I believe it’s going to be greatly needed now and in the near future as well!

Why am I paying so much more since Covid for the natural gas that heats my home in Henderson, NV if prices are so low?

Get mad at your utility.

Utility prices are based on utility investment * rate of return plus expense allowance plus a rider to cover all natural gas costs. Gas commodity prices have traditionally been about 1/3 to 1/2 of the bill price. Utilities know customers don’t understand this and only know about the final total bill. They also know customers won’t complain about increases that are small enough (0-5%). So, when prices are mostly flat, the gas utilities keep investing a lot of money in replacing old lead pipes and whatnot so that they keep increasing bill totals. If the utility commission won’t let them do annual increases for their investment, it all gets pushed into a “rate case” where bills might go up 15% or more. So it could be you had increases paused or delayed during COVID, then a new rate case, plus the gas company is probably going hog wild making new investments to get a higher stock price.

3rd rate increase in gas prices since Sept 2023.

And the source of NG keeps shifting . West Texas NG (Shale oil byproduct) pipelines to the west are full and with inflation, reduction of coal production in NM and Utah for electrical generation and even possibly less Electricity from hydro causes higher demands for NG fired generation.

Gas production increases have been focused on the NE, west texas, and East Texas/NE LA.

Basically, a surprisingly large amount of the utility bill goes to repaying the utility’s ratepayer-guaranteed upfront infrastructure expenditures (transportation lines over hundreds/thousands of miles, switch over from coal generating plants to natural gas/wind/solar…some inherently less economic, etc.).

And state/local governments frequently piggy-back off of utility billing for energy related/marginally related taxes.

A non-US example (if I recall correctly) was in Greece.

When the Greek national finances were imploding post 2010, the Greek government looked to utility bill surcharges as the most reliable/least evade-able means of generating substantial amounts of semi-stable revenue quickly.

When LNG exports rise there is less for domestic consumption. keep that dynamic in mind when NA crude stocks are being exported to the EU/NATO. you will be paying $10 for gasoline. but NG has been a gift, courtesy of Yellen who kept EFFR too low too long in 2015. low NG prices were on Greenspans wish list. war in Europe changes everything. the dip in oil prices that would occur in a recession is probably going to mark a generation low in oil prices.

“When LNG exports rise there is less for domestic consumption.”

Look at Wolf’s second chart – it goes up and to the right for the last 20 years.

There is plenty of domestic gas, don’t worry.

There’s plenty of crude oil here and in Canada. Plus, we imported about 1/3 of our needs here due to contractural agreements as it is a worldwide commodity.

Your state might also impose clean energy surcharges on your utilities that are being passed onto you.

In Massachusetts, a lot of folks got huge gas bills this winter due to the utilities needing to buy clean air credits from Mass DEP, but those of us just over the NH border had much lower prices – despite our gas coming from the same pipelines and sources.

I am not familiar with NV environmental regs, just speculating.

This is exactly right. And Nevada also exports a lot of electricity produced there (by gas fired plants) to other states and those states impose penalties on NV generated power that is not “renewable”. At least that is one of the many stories the Utilities in Wyoming use to justify their rate increases.

What it comes down to is the Utility Commissions are generally captive s of the power companies. Who knows what sort of phone calls they get sunday evenings from “interested” stake holders. In the long list of influencers pushing on Utility Commissions, the consumer is near the bottom.

Because they printed trillions of dollars to devalue the currency.

Because NG has gone from 1.50 to 4.40 in the last year.

Merchandise trade deficit for December 2024 set a record at $122,000,000,000 (billion). That record lasted for One Month. The trade deficit for January 2025 was $153 billion!!! This deficit takes away from GDP, 1st quarter estimate GDP dropped to negative 1.5%!!

Hope we can ship lots of this natural gas—we need all the trade dollars we can generate.

Yes, they’re trying to front-run any tariffs. They did that last time too, and after the warehouses were stuffed to the rafters, they stopped bringing in stuff, and imports plunged, and GDP growth bounced back. So it balances out over time. But it does move GDP growth from one quarter to the next.

Great news as USA needs to be an efficient exporter of wealth and natural resources that in turn build wealth and prosperity from within. The market has always been about moving products from areas of surplus to area of deficit and demand. Trump gets that, while the other side wants globalization and constant wars and anarchy. Cleaner energy, just think Biden and Democrats wanted to take my gas stove away, so I could freeze in winter when the power go completely out.

When my daughter was rehabbing her house, she had the gas connection removed completely. Her house is all electric. Let them burn the gas at the power plant.

Electric is ok in places where it doesn’t really get cold, but it’s a very inefficient way to heat one’s home.

When I wake up and it’s -20 F outside, my 90% efficient nat gas furnace has my home at 62 F. Last two nat gas bills have been $187 & $189. House is just over 1,000 sq ft and 105 years old. Furnace is 22 years old, and replaced an older 60% efficient furnace.

Six bucks a day to heat my home, to cook with, and to have hot water? No, that ain’t a bad deal, I reckon.

Why? If you can heat your home with a 90% efficient furnace, why not get 90% of the energy directly to your home instead of letting the powerplant convert that fuel to electricity at some lesser efficiency, and then ship it to you under high voltage where even more is lost, just so you can convert it back to heat in the end? Seems like it doesn’t make any sense. What is wrong with burning the fuel as efficiently as possible to generate heat?

Wolf’s comment above about why PHEV is a bad design (energy loss and inefficiencies) is also why electric heat is a bad design.

You’re taking some hydrocarbons, combusting them for heat, then capturing that heat to do work (at some efficiency <100%), converting that work to electricity (<100% efficiency), and then converting that electricity back into heat (also <100% efficiency).

Why not just capture the heat from combustion and skip all the rest?

A heat pump moves heat from one place to another using electricity. A typical air source heat pump with a coefficient of performance of 3, moves 3 units of heat energy per unit of electricity and thus is very economical and efficient compared to electric resistance heat. A more efficient water or ground source heat pump with a coefficient of performance of 5-7 is cheaper to operate and more efficient than natural gas heat, and they also function as air conditioning in the summer so you only have to maintain one unit for heating/cooling.

Return Jedi, yes, lots of progressive-run cities in California want to do away with gas in new homes and apartments. But they don’t seem to think about what happens in an all electric housing unit when the electricity goes off in the middle of winter. It can be very dangerous for elderly and disabled users. Also electricity outages seem to happen more frequently nowadays. In California, the utilities will turn off electricity if they see their power lines are in danger of coming down and causing a fire during a wind event. This often happens in foothill and mountain areas, the places where cold can be a factor. My gas wall furnace is also cheaper to run than a comparable electric heater. I am glad to have both.

During a power outage, the pumps or fans that move heat from the furnace/boiler to the rest of the structure don’t function – no heat. The only heat source in my house that works reliably in a power outage is my old fashioned fireplace!

Drill-Baby-Drill for 20 Years: Its`n a good idea

LOL, it’s fuel consumption that isn’t a good idea. You people keep getting that confused. Cut your fuel consumption – not fuel production.

Production needs to meet demand, and if consumption is falling, such as of gasoline, then that’s a good thing. But if production is falling while demand keeps rising, then you’re paying out of your nose for basic stuff, and this money goes to some foreign country. Been there done that. See what US dependence on OPEC oil did to the US gas prices and prices overall when OPEC decided to f**K with the US in the 1970s. Then in the early 2000s, the US was paying out of its nose to import expensive LNG because US demand for natural gas, which was rising, exceeded US production, which was flat to dropping.

In addition for you anti-production folks, the US has largely shifted fossil-fuel power generation from coal to natural gas. Coal’s share of power generation collapsed from 51% in 2001 to 15% in 2024, while the share of natural gas soared from 17% to 43%. Natural gas is the cleanest-burning fossil fuel out there. Over the same period, the share of renewables soared from 8% to 24%.

More details here:

https://wolfstreet.com/2025/02/27/demand-for-electricity-takes-off-us-power-generation-by-source-in-2024-natural-gas-coal-nuclear-wind-hydro-solar-geothermal-biomass-petroleum/

Thank God for this country’s Natural Gas. It’s the reason we aren’t in the terrible position of the European economy.

I truly believe that the benefits we have reaped from fracking and our natural gas reserves really goes unnoticed to most people. It’s huge , and has been a game changer in so many ways

I appreciate your comment that natural gas is the ”cleanest burning fossil fuel” out there Wolf, but the facts show that IF the coal burning facilities around the world were to put into place the ”scrubbers” that would capture EVERY bit of the clearly needed products included in every coal, they would produce not only a net benefit for clean air that we all certainly want, but many worthy products.

Why this has not been not only mandated, but also subsidized is just another result of political corruption.

VVN,

Are you defining “clean” as pollution-free, or lowest GG emission?

Gattopardo,

Methane is a C1 alkane straight-chain hydrocarbon, which only has one carbon atom per molecule. All other hydrocarbons have multiple carbons per molecule.

Properly combusted methane produces only water and CO2 as a byproduct:

CH4 + 2 O2 = CO2 + 2 H2O

Contrast that with propane (C3) combustion:

C3H8 + 5 O2 = 3 CO2 + 4 H2O

Propane has a higher energy density than methane, but it’s not 3x higher – yet it produces 3x more CO2 per molecule combusted.

And propane is still a fairly clean fuel – gasoline (petrol) is a much more complex molecule with a lot more carbons in it.

I just re-read VVnVet’s comment and realized I misunderstood.

“Clean” coal will never have the same ultra-low emissions that natural gas does. It’s just not chemically possible.

Per atom oxidized, carbon delivers 2.75 times as much energy as hydrogen.

Coal has a bunch of other concerns before you scrub the SO2, which is the bad actor, and other pollutants.

Mining, processing, rail transportation , storage, handling, etc create a lot of particulate emissions and take up vast quantities of real estate. And you use a lot of energy getting the coal product to the power plant.

Plus, coal production can get costly when you have to deal with handling lots of produced water (from coal bed methane operations – Wyoming) and restoration of mining properties.

Nat gas is so much easier to deal with.

They literally used to just burn the natural gas coming out just to use it up. That’s how much there was. It’s clarified in the article. Why fight for coal when it’s not needed? Why come up with fancy contraptions to make coal clean-er when natural gas and renewables are making it less necessary than ever? The fact of the matter is coal is primarily carbon, so all the scrubbers in the world aren’t gonna keep it from turning into C02 when it’s burned. You can’t say the same for natural gas (CH4). Other than preserving coal miner jobs, what’s the benefit of coal? The world changes, seems like we should just let the utility companies decide which way to produce power cheaply. If that’s acres of solar panels, so be it. If it’s burning plentiful reserves of natural gas, so be it. I don’t see the benefit of fighting to bring back coal unless we are just importing crazy amounts of fuel because we don’t have enough to go around here. But seems we are making it work, because of plentiful amounts of NG.

I suppose one could argue coal is logistically easier to handle – solid vs gas.

But it’s a really stupid argument b/c we obviously have the technology for gas distribution, including right to the home.

Gas is the future, and coal will soon assume its rightful place in the dustbin of history.

Very well said, Wolf. Supply always follows demand, and drunken sailors can’t wait. It’s not the geo-politics, or the drinking media that supplies the demand. The destruction of the environment precludes the demand for goods, natural gas in this case. Methane in the air doesn’t help anyone and anything.

MW: Ray Dalio warns US could face a surprise debt-crisis ‘heart attack’ within three years

MSN: Vehicle Prices in the US Poised for $12,000 Surge…

I saw this stupid headline too. The headline provides incontrovertible proof that the media are run by braindead AI, for sure.

Automakers are already having trouble selling new vehicles at sticker prices and have to pile on massive discounts to move the vehicles. Lots of dealers are massively overstocked. What do these moron AI reporters think Ford’s sales will do if it raises the price of its Mexican-built F-150 by $12,000??? Sales will go to ZERO, that’s what sales will do, and Ford will go bankrupt. Automakers cannot pass on a dime of any tariffs right now. Instead, they have to eat them. I would pair them with a hop-forward nicely bitter double-IPA Bon appétit.

Auto makers will obviously pass along 100% of the Trump tariffs and they are faced with no other choice. That all starts tomorrow and if sales go down somewhat, so what?

Each automaker’s choice is to eat the tariffs or watch their sales go to zero.

They can’t sell what they’re making as it is, inventories are building. They won’t get to Jack up prices with the tariffs. Watch and learn. This train was in motion before the tariffs.

And today’s headlines: Honda to produce next Civic in Indiana, not Mexico, due to US tariffs, sources say.

No $12k price increases there.

Some US auto workers will be happy about that too.

Something from Boneyard in Bend? After all, they claim to have started in an old auto shop.

These production stats are not possible. Biden shut down the fossil fuel industry. I heard the whole GOP say so.

RE: getting mad at your utility, it’s really hard to pin them down on what actual costs are until you get your bill. The maze of different rates and tiers and surcharges and delivery charges, etc….maddening.

Are you unaware that P&G lost a massive lawsuit in NoCal?

Actually, the only thing Biden did of any significance is sell most of the Strategic Petroleum Reserve of crude oil. And a good bit of that got sold to foreigners through brokers and reportedly the Chinese got some. All that did was put a temporary lid on retail fuel prices, nothing else.

The U.S. crude oil production was very high throughout the Biden years.

Sikeston MO has one of the cleanest coal generation plants in the country. I know little about it but do know it scrubs the flue gas for all pollutants and produces sulfur for fertilizer. The engineers on here can explain as I’ve given up on keeping current on events. Retired in 2000 after working in oil 31 years.

One of the great ironies of recent history is that the Biden administration did more than perhaps any other administration is improving the USA’s fortunes for LNG exportation through its support of Ukraine during the Russo-Ukranian war, and thereby allowing USA natural gas producers (where we were running a surplus) to eat Russia’s lunch in the natural gas market.

If his administration really wanted to hurt Russia, they should have /subsidized/ domestic producers to sell oil below cost. Crash the price and deprive Russian industry of the profits from selling at $70-$90/bbl which they’ve been able to do despite sanctions.

Domestic oil companies have proven their willingness to flood the market with supply and crash the price, even at their own peril. With a little encouragement from Uncle Sam, it would have been no challenge to execute this plan.

The Dow is doing very nicely and is down 776 going into the close while NASDAQ is down 554 and the S&P 500 is down 126!

MW: Stock market tanks after Trump confirms tariffs to start at midnight

The stock market plummeted after President Donald Trump confirmed tariffs would go into effect at midnight.

Yes, here is what I said a month ago how that worked last time:

https://wolfstreet.com/2025/02/03/what-trumps-tariffs-did-last-time-2018-2019-had-no-impact-on-inflation-doubled-receipts-from-customs-duties-and-hit-stocks/

Amazing. And PG&E continues to shaft us despite the Rio Vista Gas Field being near the bay area and producing 324,000 cubic ft of gas in November alone.

PG&E should have been dismembered in bankruptcy court last time it was in it.

If you check your bill closely, about 2/3 of the cost is for “distribution” not “generation.” Since around 2000, PG&E doesn’t generate any power, it buys it from generators and charges you a princely sum for delivery. That’s why my bill has tripled in the last 5 years while KWH used has decreased 20%

Ashland Oregon, Justin posed $4,000 fees on all new construction for gas heating systems and gas appliances. Is this the future? Will it be challenged in courts? Let’s watch

It’s so dumb to me that we are penalizing people for burning gas to produce heat. That’s literally the best thing you can do with it. If you have a natural gas stove that is un-vented in the winter, the heat coming off it is literally 100% efficient, as 100% of the heat from the combustion is going into the home. Same with a water heater. Why burn that gas at power plant at 70% efficiency, lose some of the energy into the sky, just to make electricity so we can send it to an all electric house and consider that more ‘green’? Crazy to me.

A couple reasons.

1) There are health concerns from burning gas (stove).

2) Leaks.

3) Ka-boom.

4) By getting everyone to tilt toward using more electricity, via super efficient heat pumps, and using solar on rooftops, and growing renewables by the utilities (and less gas), you end up with less GHG emissions.

Whether you buy into those arguments is another thing.

In theory, but electricity can short circuit and go zap, just the same. I think the goal is if everything is all electric they feel it will drive more renewable demand. But that’s short sighted, and I don’t think people realize the demand of electricity that would be required to eliminate all fuel combustion in households. It would just push renewables to a lesser percentage. I definitely don’t buy into it, not right now. Maybe in 100 years I will. Lofty goals at best

Heat pumps can make sense if it doesn’t get below freezing there. They are fairly efficient in warmer temps, and you can get heat pump/AC combo units – if it doesn’t get that cold, it probably gets hot enough to warrant AC.

But I’ve seen heat pumps with a backup heating element which is just stupid. If it gets cold enough that your heat pump can’t keep up with demand, it’s inadequite for the space (or maybe a gas furnace makes sense).

W/r/t powering all this via solar… there is some benefit, sure, but it’s usually coldest (=highest heat demand) at night.

Blake – think of all the fires caused by spaceheaters.