What homebuilder Taylor Morrison said about the costs of mortgage-rate buydowns v. actual price cuts.

By Wolf Richter for WOLF STREET.

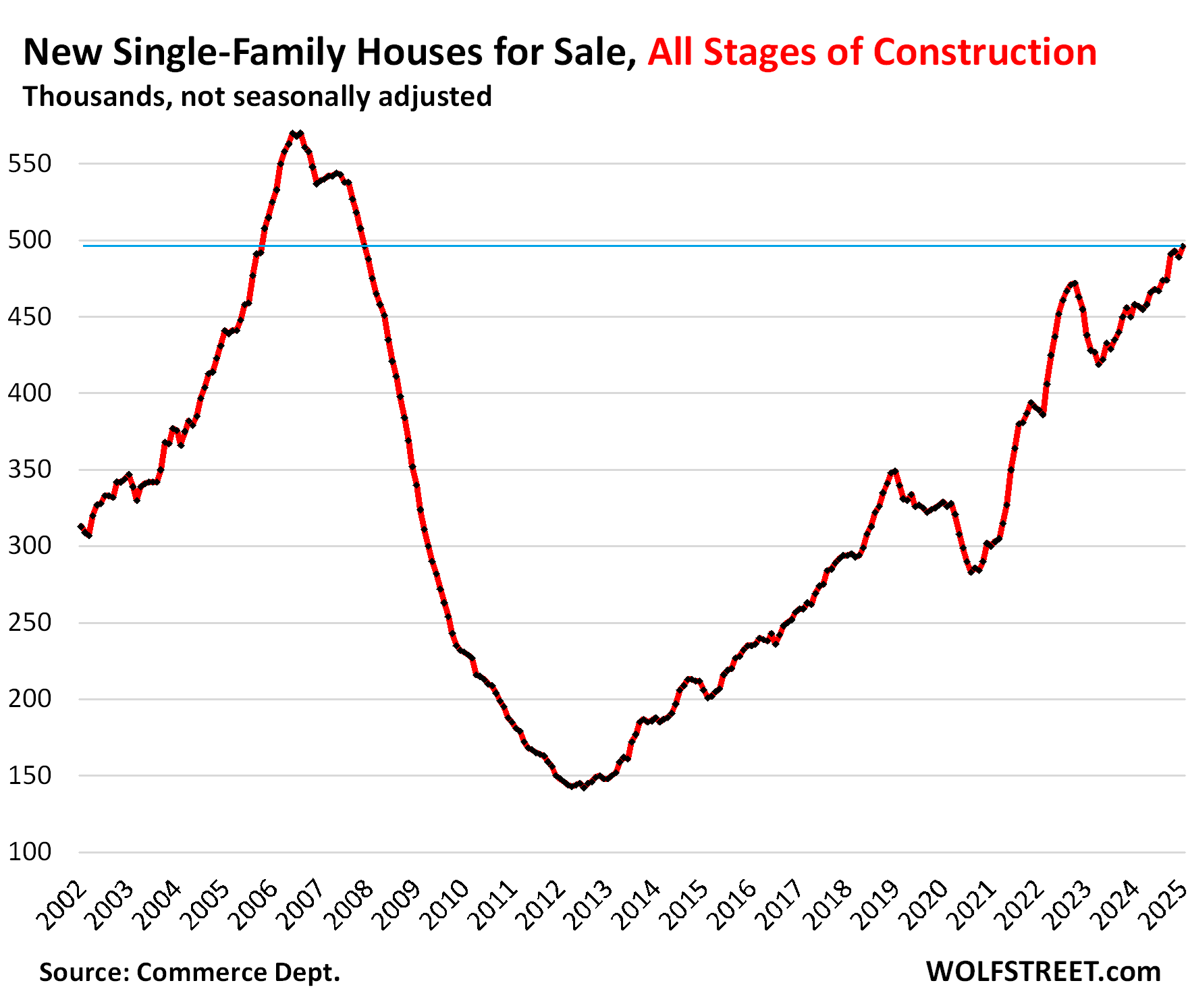

Unsold inventories of new single-family houses for sale at all stages of construction in January rose by 8.3% from the already hugely bloated levels a year ago, and by 42% from January 2019, to 496,000 houses, the highest since December 2007 during the Housing Bust. Supply rose to nearly 9 months.

The overall housing market needs this onslaught of new supply. It’s competition for homeowners selling their homes, or thinking about it, including their vacant homes they’d moved out of years ago but didn’t put on the market to ride up the price spike all the way.

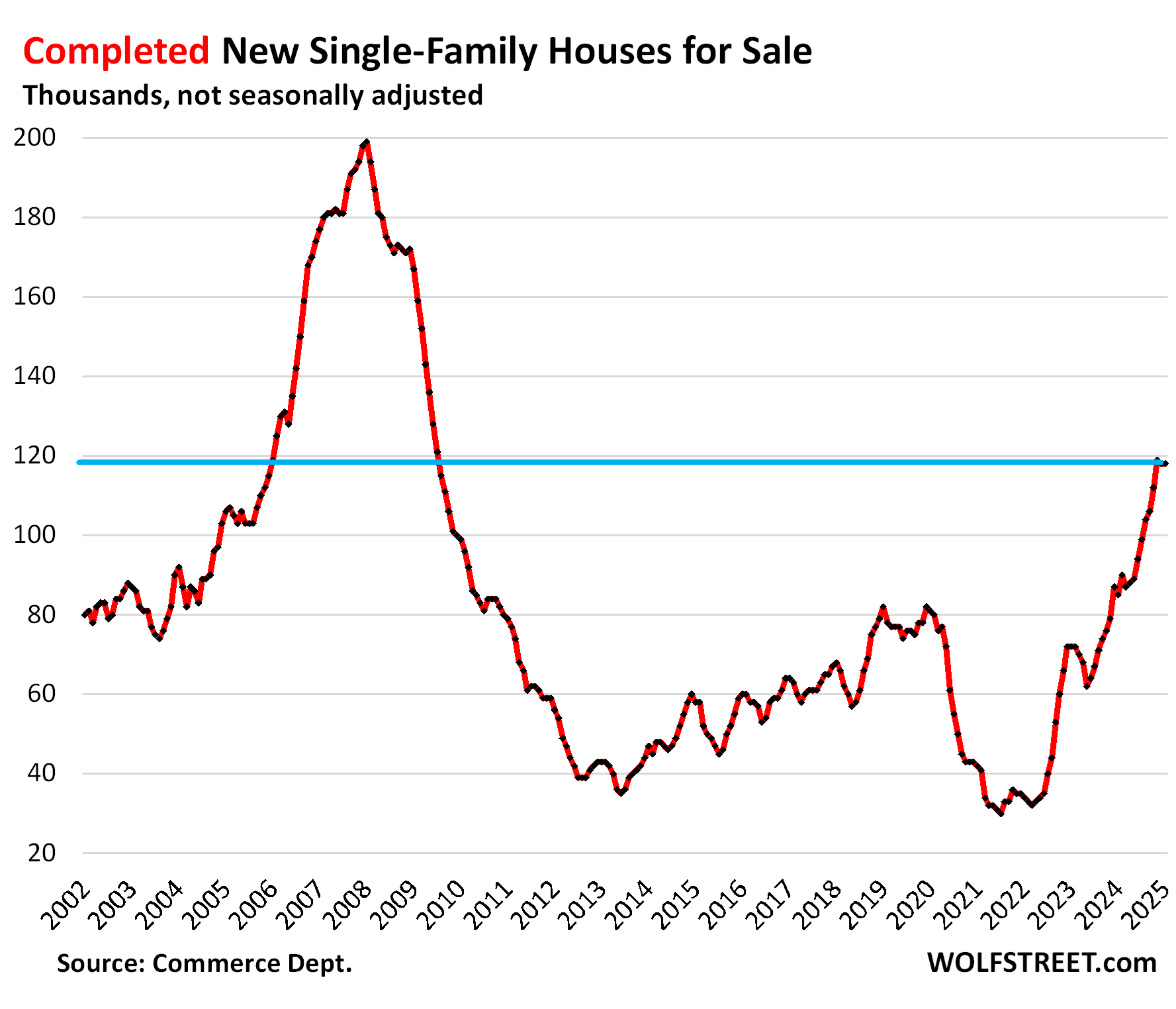

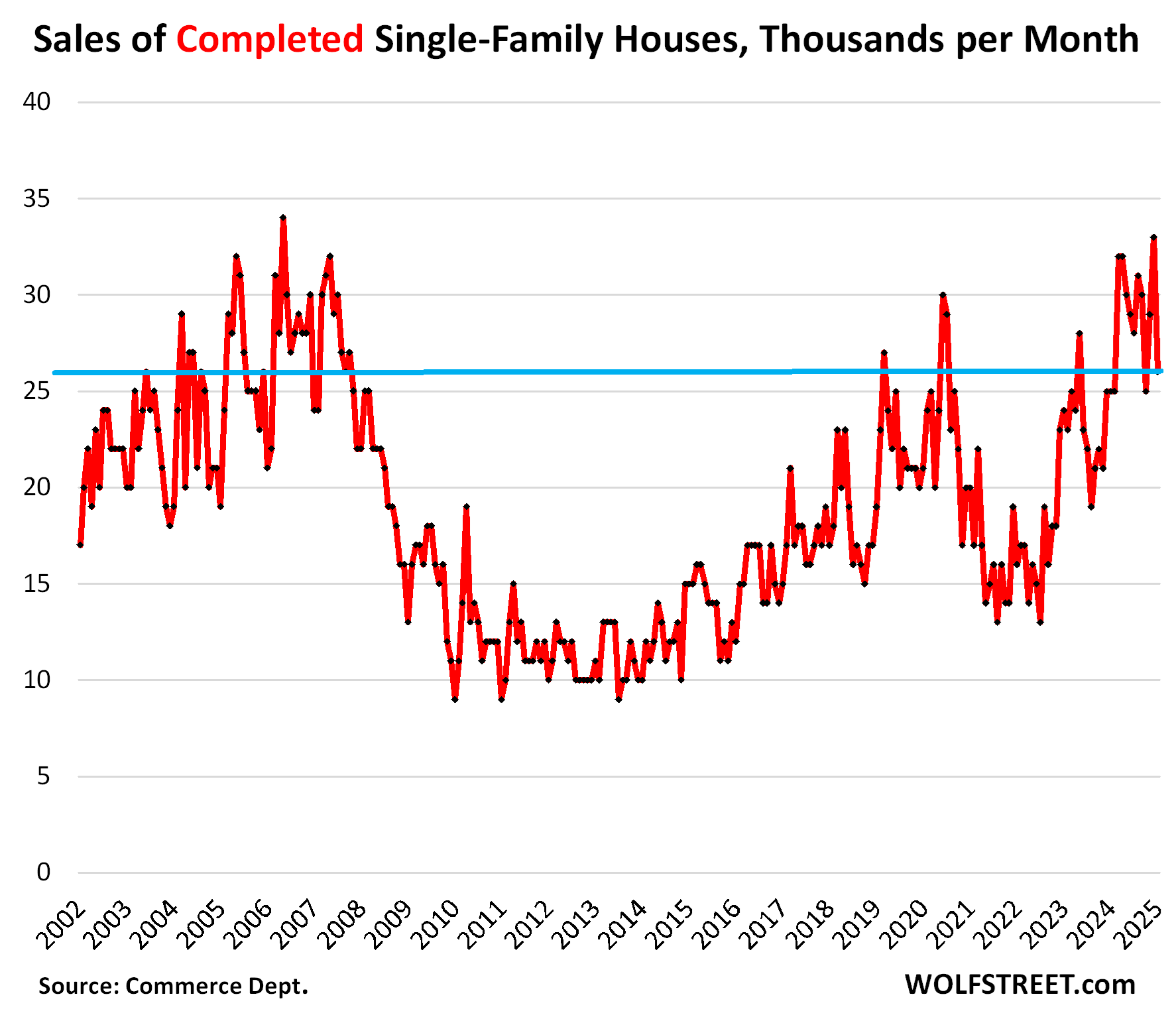

Completed new single-family houses for sale have formed a huge pile of around 118,000 houses for the third month in a row, the highest since August 2009 on the way down, and the same as January 2006 on the way up, as the Housing Bust was taking off.

These are “spec houses” that were built without buyers lined up. Homebuilders need to sell this inventory of spec houses quickly because they’ve sunk a lot of capital into it.

These inventory levels are up by 39% from a year ago, and 44% from January 2019, according to data from the Census Bureau today.

Homebuilders have been putting substantial efforts into selling down their inventory, including price cuts, mortgage rate buydowns, and other incentives, as we can see in their earnings calls and ads.

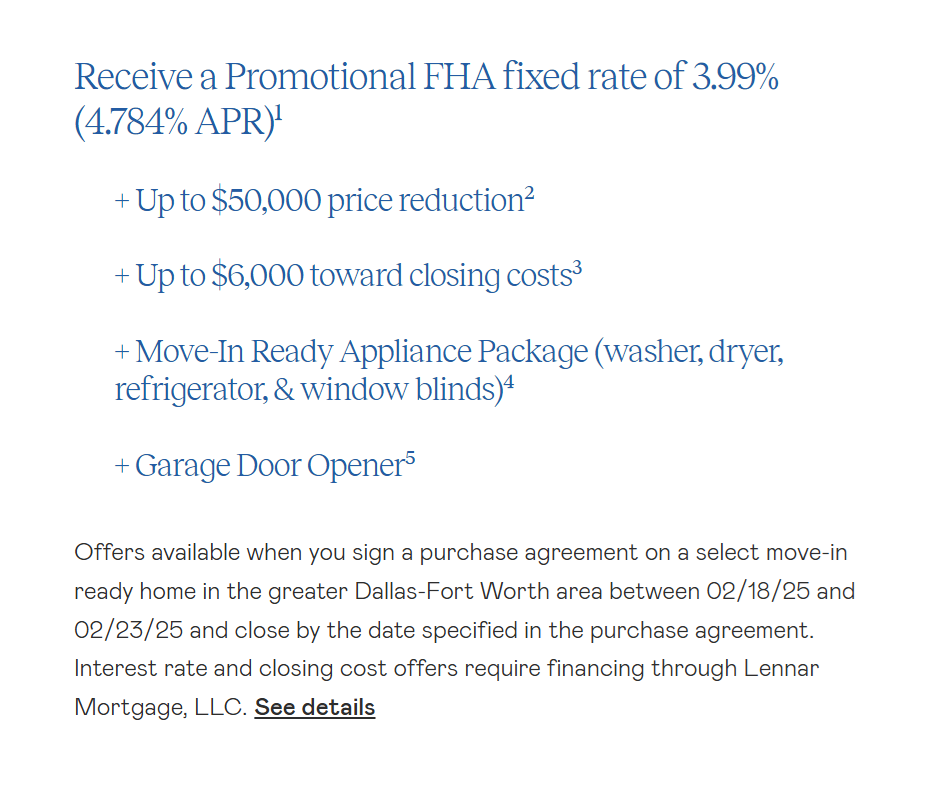

Here is a screenshot of an ad from Lennar that ran earlier in February for the Dallas-Fort Worth area. We’ll discuss the tiny print of the footnotes below:

According to the tiny print of the footnotes, the offer is available “on select move‑in ready homes.”

- Footnote #1: the 3.99% mortgage rate is “for a home price of $240,999,” with a minimum of 3.5% down, a minimum credit score of 680, and an owner-occupancy requirement.

- Footnote #2: “Up to $50,000 Price Reduction is valid towards the total purchase price (prices listed reflect reductions).”

- Footnote #3: up to $6,000 credit for closing costs “as determined on your Loan Estimate, excluding prepaids.”

- Footnote #4: incentives of up to $7,720 retail value in form of Lennar’s appliance package. “If you are obtaining a loan, the lender may reduce the purchase price of the home on a dollar for dollar basis for the value of these items(s).”

- Footnote #5, garage door opener, retail value not to exceed $770.

Overall sales dip year-over-year despite price cuts & incentives.

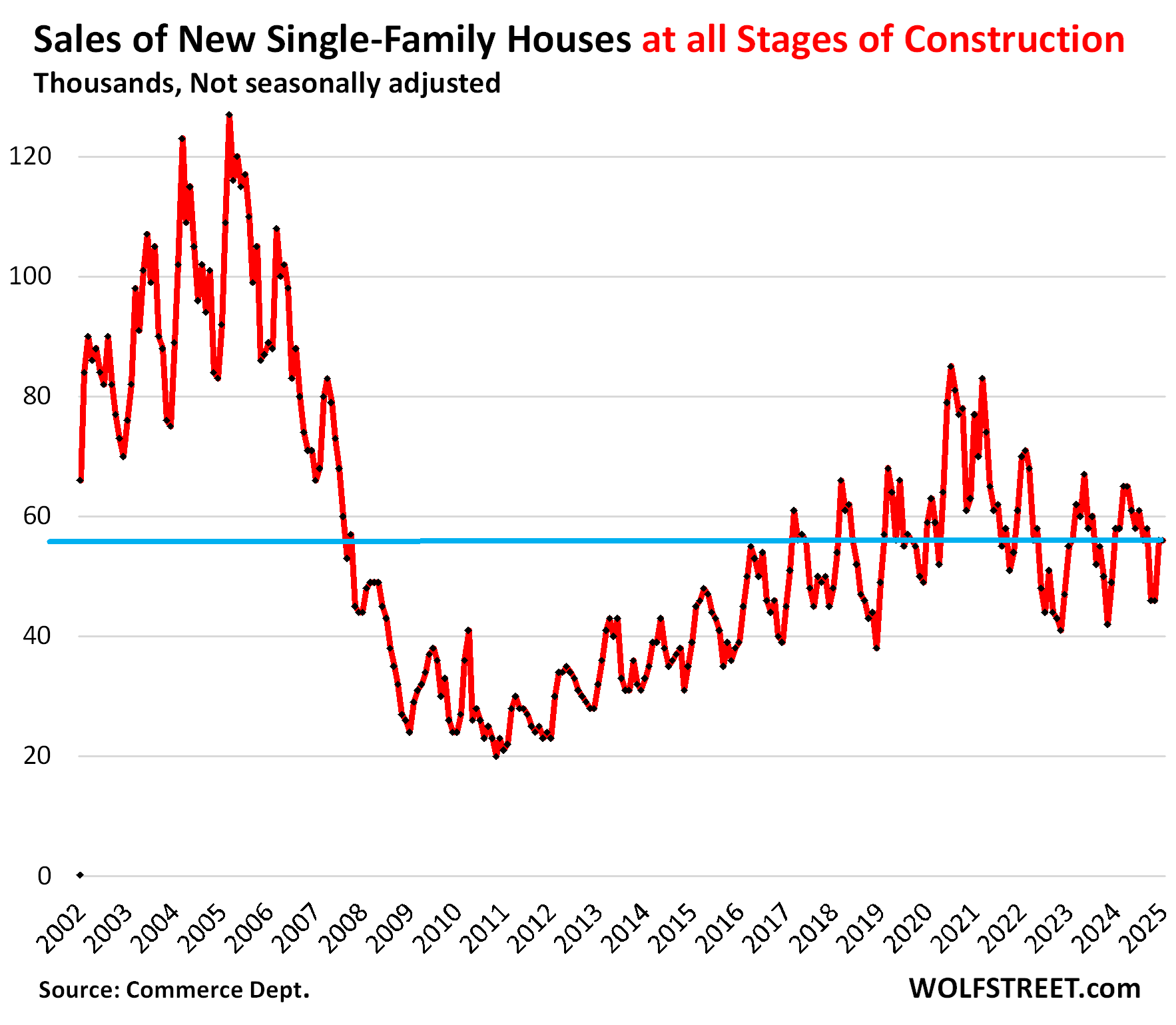

Sales of new houses at all stages of construction rose in January from December seasonally, but dropped by 3.4% from January a year ago, and by 11% from January 2019, to 56,000 houses, not seasonally adjusted, despite all the promos out there. Last year, they had held up at decent levels. This comes as sales of existing homes in January also fell, after having tanked last year to the lowest level since 1995.

Homebuilders have been selling houses at a slower clip than they’ve been building them, which is why inventory levels have surged.

These sales are based on contract sales, not on closed sales. Things can happen that prevent contracts from closing, such as not being able to get affordable insurance.

Sales of completed houses fell in January from December, to 26,000 houses, but were still up by 4.0% year-over-year and by 37% from December 2019.

The costs of mortgage-rate buydowns v. price reductions.

These types of discussions and disclosures have been creeping into homebuilders’ earnings calls. For example, we’ve learned from D.R. Horton [DHI] that they’re hedging mortgage-rate buydowns when those hedges blew up in late 2023, triggering big losses that had to be disclosed. Or from Lennar [LEN] that the costs of incentives per home delivered jumped to $48,100 in Q3, or 10% of revenue, up from $36,400 and 7.5% a year earlier.

Taylor Morrison Home Corporation [TMHC], during its Q4 earnings call two weeks ago, discussed some of the math involved in mortgage-rate buydowns v. price cuts. CEO Sheryl Palmer laid out an example (transcript via Seeking Alpha):

“Instead of having to discount the house or do a very expensive forward commitment, we’re assisting a consumer, guaranteeing that they’re going to have a 1% reduction to the market rate.

“Let me take a $500,000 house with a 20% down payment, a 400,000 loan, to do that it’s costing me approximately $16,000.

“To get that consumer to the same monthly payment [via price cut], it would cost me $60,000 to $65,000 price adjustment.

“So, when I can use these tools most efficiently to help that consumer and I’m using $16,000 as compared to what we’re seeing things in the market today that are 2.99%, 3.99%, those can cost 700 to 900 basis points. We’re doing some of these programs at a fraction, and we’re not taking it off the price, which is also protecting our margin.”

But costs of incentives are not reflected in the “Contract Price.”

The Census Bureau tracks contract prices, but the costs of the mortgage-rate buydowns and the costs of other incentives are not part of them.

These costs are included in the gross profit margins of the home builders, and are therefore reflected on homebuilders’ financial statements. They’re just not part of the contract prices that the Census Bureau tracks.

The incentives such as Lennar’s closing cost credit of $6,000 and $7,720 appliance package, and the costs of the mortgage-rate buydown to 3.99% are not part of the contract prices. The $16,000 cost at Taylor Morrison to buy down the rate of a $400,000 mortgage by 1% is not part of the contract price.

But the $50,000 price reduction offered by Lennar in its ad is part of the contract price when that home sells.

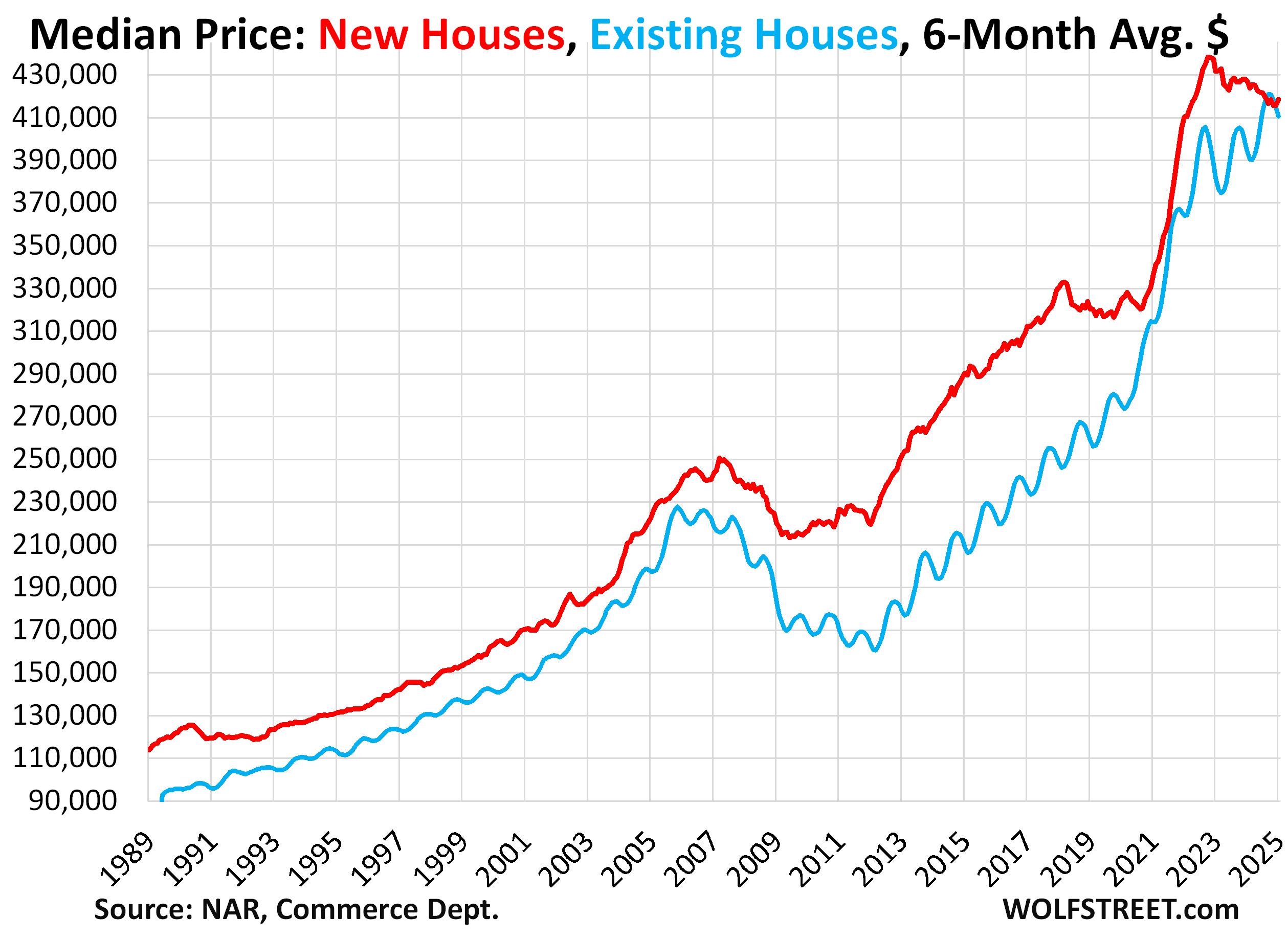

The median contract price of new single-family houses sold at all stages of construction – a super-volatile figure that jumps randomly up and down and is often revised sharply – jumped to $446,300 in January.

But the prior two months were revised substantially lower. November was revised down to $396,400, the lowest since July 2021.

With these two downward revisions and the jump in January (likely to be revised down over the next two months), the three-month average rose to $419,200, down by 5.2% from the peak in October 2022.

The six-month average, which irons out most of the month-to-month zigzags and revisions, ticked up to $418,500, same as in October 2024, and down by 4.5% from its peak in October 2022.

Again, these contract prices do not include the substantial costs to homebuilders of mortgage rate buydowns and other incentives, though they do include price cuts.

Prices of new houses versus existing houses.

From 1989 through 2023, the median contract price (six-month average) of new houses exceeded the median closed price of existing houses (six-month average) all of the time, with new being usually 5-30% more expensive than used. This scenario changed for the first time in 2024, which explains why homebuilders’ sales have been decent, while sales of existing homes have plunged, as some buyers shifted from buying overpriced used to buying new.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It’s full speed ahead for new starter homes by all the Big Players here north of Houston, Texas (Montgomery County). And the Big Guys are offering all the stuff in the article. Thousands of acres of flat forest land are going under the chain saw and bulldozer. The roads will need to be widened here in a couple of years. And taxes will go up due to the NEW SCHOOLS being built. And I live right in the middle of it all.

Nothing appears to be stopping or slowing this madness (progress?)!

Anthony A, The only thing stopping in your area is the traffic on I-45! It had been a couple of years since I drove through there. Crazy amount of development going on.

Times are hard when they’re giving away garage door openers.

Hear ye, here ye, thee house includeth garage portal opener!!! I’ll make sure to include that in the description of the next house I sell. Problem is I need to first I buy a house :(

Maybe I can get a new one!!!

Gotta wonder why a garage door opener needs to be limited in price to $770. They must be overcharging for the install, and acting like that money is going to you.

The best normal garage door openers you can get are the Chamberlain RJO101 and Liftmaster equivalent. Chamberlain has MSRP of $500 and takes a noob 3 hours to install, max. If you buy the Liftmaster equivalent from HD, they charge you $1k installed. They give the door guy $150 to install it (I asked him). So, $350 in profit for doing literally nothing.

In this case, your free garage door opener could not be a jack shaft opener, and a new garage with some old school opener is just downright sad, IMO. And those legacy openers cost about $150-300 retail…

All smoke and mirrors.

Chamberlain and Liftmaster are the same company.

I know. I tried to express that by saying “equivalent”.

Too lazy to look up what % of profits “$48,100 in Q3, or 10% of revenue” is but considering the build quality of places going for 350-400k in my neck of the woods I get the impression it isn’t much.

I just tore down a 2019 house that got nailed by a large tree and it wasn’t any more difficult than removing a mobile home – and was easier in some respects.

No tears for the crocodiles here…

When they decrease the build quality, they pocket the extra profit. You didn’t think the builder was trying to give you a deal, did you?!?

my bad… closest house in that neighborhood going for $620k now.

Yes mortgage rates are relatively high compared to those of ZIRP days but prices are an impediment to buyers also. It is not easy to come up with a down payment and closing costs if you are a first time buyer.

“It is not easy to come up with a down payment and closing costs if you are a first time buyer.”

It never is, and never has been.

What if one isn’t “fit” enough?

-Herbert Spencer

Wolf, why do homebuilders prefer mortgage buydowns over price reductions? Do they think that when conditions improve they can remove the mortgage buydowns and keep the price? Do they think reductions in price will be reinforcing and drive future prices down again?

If I understood the article it is because a reduction in rate drives the monthly payment down for a lower cost than a reduction in price does. Someone with more time than me can play with the mortgage calculator can confirm.

NR,

It’s explained in the article, by a homebuilder. So go ahead and read the article… that section is in italics even.

Midwest Ralph,

It doesn’t quite work that way. The typical 30-year mortgage gets paid off in something like 8 years (moving, refi, death, divorce, kids, etc.). So there is an expected average life of the mortgage. You can figure the expense of the buydown over the expected average life of the mortgage. That’s why the cost is so much lower. A mortgage calculator is useless here.

There are hedges involved, and builders only mention them in passing until they blow up, such as DR Horton’s hedge which blew up in late 2023, at which point they have to discuss them. So we’ll see a little of that every now and then.

What the builder said is cryptic.

She said it costs $16,000 to buy down the mortgage rate by 1% on a $400,000 mortgage, while it costs $60,000 to $65,000 in price reduction to get to the same payment.

You went ahead and spoon fed them anyway, Wolf.

sounds like subprime-adjacent, just without the sketchy underwriting…

Avoiding price discovery sounds like a horrible idea. When the market finally turns there is no refinancing possible and value will be way below what the monthly repayments are based on the artificially propped value.

Let’s hope no one falls for this bc it’s a recipe for disaster.

Thank you. Missed it. I should have been more careful.

NR – They are taking a page out of the car dealer handbook, “What do you want your monthly payment to be?”

Are these buydowns effective for the life of the mortgage, or only for the first few years, with the rate then rising to the current market rate around 7%?

Around here, the ones I see are for two or three years.

So teaser rates? where have I seen that before

When this thing breaks, and IT WILL, it will be just like a dam that finally gives in. It will trickle and trickle and people will think “Huh!”. Some will wonder if the trickle will be a permanence, or if we are in a new normal of price stagnation.

But when the big one comes and it finally happens, it will be just like the Hoover Dam breaking down from all the pent up pressure.

The Big Short will pale in comparison to this humdinger of a catastrophe.

Narrators Voice: the Hoover Damn never broke down.

But Damn Hoover’s economic beliefs sure did. He was a trickle-downer.

I am pretty sure Will Rodgers coined that phrase in a comment about him.

Look it up and learn….that’s what I think this site is for…..at least it’s why I read it……my ONLY social media, FWIW.

An excellent turn of a phrase and a worthwhile point to reflect on replete with a Will Rodgers reference. Brilliant!

Years ago there was a song – ‘Hot Rod Lincoln’.

It talks about driving so fast in your hot rod that telephone poles (now) look like a picket fence.

I call it distorted reality. My wife has this distorted reality phenomenon when it comes to housing. A house that not many years ago cost $250K, and with the Magic Bubbles Machine went up to $800 or $900k, now has fallen to say, $500K. The wife says it’s “cheap”! I remind her that a half a million isn’t cheap. Distored reality – when telephone poles become picket fences. I’m guilty of it too. After prolonged immersion in an alternate ‘universe’, your reality does become distorted. I’m hoping to get back to the terrestrial realm soon.

Commander Cody and the Lost Planet Airmen were revising and updating a much earlier song called “Hot Rod Ford”. Just goes to show you the continuous mindset of everyone who believes they’ve got to upgrade their purchases beyond what older generations had achieved. “Moar!” is never enough when they’re dishing out gruel in the workhouses. Son, you’re gonna drive me to drinkin’z if you don’t quit buying those hot rod Linkin’z.

The $ isn’t worth a $hit compared to what it had been. I don’t see anyone in power trying to “re-value” the dollar anytime soon, either.

That is why housing prices go up so much, they are priced in devaluing dollars. Houses themselves are not worth more, it is just the dollars you pay for them have lost purchasing power because of inflation. Deflate the dollar if you want house prices to drop.

I wish more people understood this

And the opposite happens when prices go down and the dollar re-gains value:

“…well, the fellers ribbed me for bein’ behind……”

Like your neighbors act if your tailgate doesn’t fold 6 ways…….

Veber.

With large increases in unemployment coming via the Federal workforce I think you’ll see more housing up for sale, which will impact prices. And inflation as the Fed pivots back to worrying about unemployment. Which isn’t going to help the consumer if interest rates go back up.

I wonder just how much regret Powell is feeling with the last rate cuts and inflation still years away from getting below 2%.

Imagine how much regret he is feeling at his new weekly meetings at the WH.

Just imagine! Laying off a few federal workers will end the USA as we know it ! OMG

Perhaps not the layoffs. BUT the trillions in additional debt heaped on to give tax cuts to billionaires might end poorly.

“You see, we’re saving $25 million but adding over $4 trillion – see how that math works?!? That’s called balancing the budget, children.”

@NotHere,

If spending was simply cut back to 2019 levels, there would be no ongoing deficit problem. Tell me why the increased “emergency” COVID spending should be our new baseline forever? Both parties are at fault for this, but one party is at least attempting to do something about it. And the 2017 tax cuts benefit people in all income strata, billionaires a little less than high income wage earners.

I know 3 old guys in my neighborhood who took the buy-out package from NASA. All were going to retire this year anyway. So the buy-out just means they get paid to stay home. All own their homes and have no interest or need to sell. Two young guys took the package. They are way sharper than I ever was. One already got another job with Blue Origin and the other is interviewing with Lockheed. They will get double pay for the next 8 months. Again, no need to sell their homes.

NASA buyouts? Interesting. I wonder if there will be buyouts for SpaceX – after all, it’s just taxpayer dollars as well.

A love poem to the home builders:

All your unsold houses,

They’ve been sitting so long, they’re now filled with ‘mouses’.

It would be very nice,

If you’d lower the price.

A house isn’t supposed to cost a fortune.

It’s starting to feel more like extortion.

All my money has been spent.

I’ll soon be in a tent.

The houses aren’t sellin’.

Are you going to blame Yellen?

Or, you could blame Powell,

But I’m throwing’ in the towel.

I think I need to buy a vowel.

Or, we can blame Jo and the Ho,

Because nowadays I can only afford to buy in Mexico.

What was once the American dream,

Now seems like some ugly scheme.

It seems we have to work 24/7/365,

Just to stay alive.

With all the tricks and games,

It’s makin’ me want to be like Jesse James.

1) From bondage to spiritual faith

2) From spiritual faith to great courage

3) From courage to liberty

4) From liberty to abundance

5) From abundance to complacency

6) From complacency to apathy

7) From apathy to dependence

8) From dependence back into bondage.

Hard times create strong men, strong men create good times, good times create weak men, and weak men create hard times.