21 metros below 2022 highs: Austin, San Francisco, Phoenix, San Antonio, Denver, Sacramento, Dallas-Ft. Worth, Houston, Seattle, Tampa, Atlanta, Portland, Salt Lake, Raleigh, Charlotte, Nashville, Las Vegas, Minneapolis, Orlando…

Other metros powered past 2022: Miami, San Diego & Los Angeles now losing ground. Baltimore, Kansas City, Columbus, Washington D.C., Philadelphia, Boston, Chicago, New York…

By Wolf Richter for WOLF STREET.

Prices of single-family houses, condos, and co-ops fell in January 2025 from December in 32 of the 33 large Metropolitan Statistical Area on our list here. The one exception was the San Jose MSA, where prices were roughly unchanged for the fifth month in a row.

In some markets, there is essentially no seasonality to home prices, just wobbles, squiggles, peaks, and troughs that occur at various periods of the year, and price changes in those markets are not seasonal.

In other markets, there is distinct seasonality in home prices, with annual peaks occurring at roughly the same month of the year, and price changes may be in part seasonal. The charts below, which are based on raw, not-seasonally-adjusted prices of mid-tier homes in each market, visually demonstrate that absence or presence of seasonality in prior years.

Down from the 2022 peaks: Prices in 21 metros of our 33 metros are down from their 2022 peaks. Some by a smidge, others by a lot. The list of decliners from their 2022 peaks is led by the metros of Austin (-23.3%), San Francisco (-11.0%), Phoenix (-9.8%), and San Antonio (-9.1%).

No New highs in January 2025: No metro of the 33 metros here made a new high in January.

All data is from the “raw” mid-tier Zillow Home Value Index (ZHVI), released today. The ZHVI is based on millions of data points in Zillow’s “Database of All Homes,” including from public records (tax data), MLS, brokerages, local Realtor Associations, real-estate agents, and households across the US. It includes pricing data for off-market deals and for-sale-by-owner deals. Zillow’s Database of All Homes also has sales-pairs data.

To qualify for this list, the MSA must be one of the largest by population, and must have had a ZHVI of at least $300,000 at the peak. The metros of New Orleans, Oklahoma City, Tulsa, Cincinnati, Pittsburgh, etc. don’t qualify for this list because their ZHVI has never reached $300,000, despite the surge of home prices in recent years, but from low levels.

The first 21 metros are all below their highs in mid-2022.

The speculative mania in these markets through mid-2022 was driven by the Fed’s interest rate repression, including trillions of dollars of QE at the time, resulting in below-3% mortgages, which turned housing markets into absurdities.

But the Fed has let go of interest rate repression, and has been doing QT since mid-2022 and by now has shed $2.15 trillion in assets from its balance sheet. And mortgage rates have been around 7%, give or take some, since September 2022, which was sort of normal before the QE era started in 2008.

Note that Texas didn’t experience Housing Bubble 1, having finally gotten through with a huge housing bust some years earlier, and it therefore didn’t experience the big price drops in 2006 to 2012 either, just some moderate declines. But it made up for having missed out on Housing Bubble 1 this time around.

| Austin MSA, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -23.3% | -0.8% | -3.4% | 154% |

The Austin MSA includes the five counties of Travis (Austin-Round Rock), Williamson, Hays, Caldwell, and Bastrop. The index has dropped to the lowest level since April 2021.

Over the six months from February 2021 to July 2021, prices had spiked by nearly 30%, which were then followed by additional price spikes through June 2022. Not many people bought homes at the peak of the speculative mania, and it is now getting unwound, but more slowly.

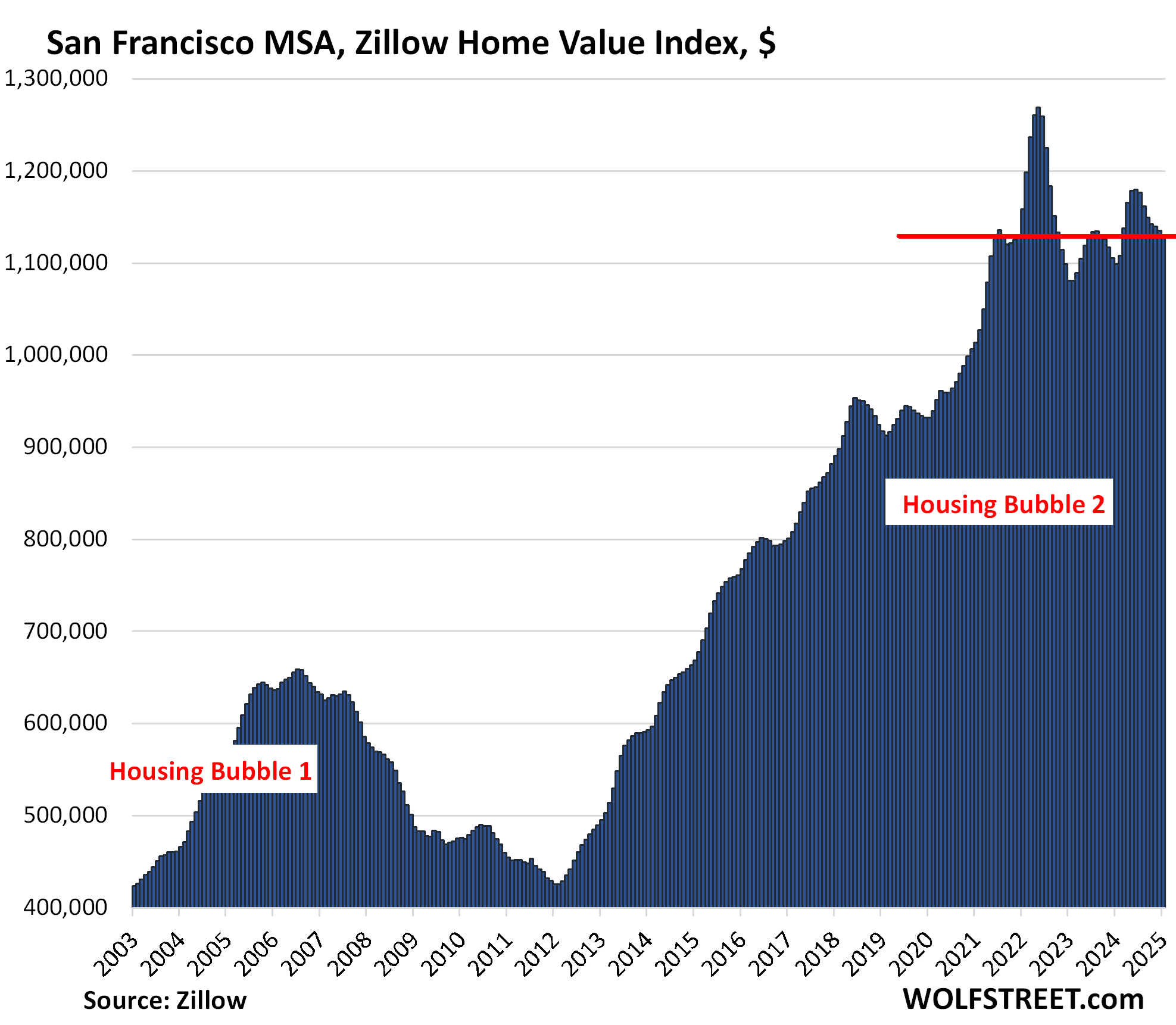

| San Francisco MSA, Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -11.0% | -0.5% | 2.7% | 288% |

Prices in the San Francisco metro are back where they’d first been in June 2021. The MSA includes San Francisco, Oakland, much of the East Bay, much of the North Bay, and goes south on the Peninsula into Silicon Valley through San Mateo County.

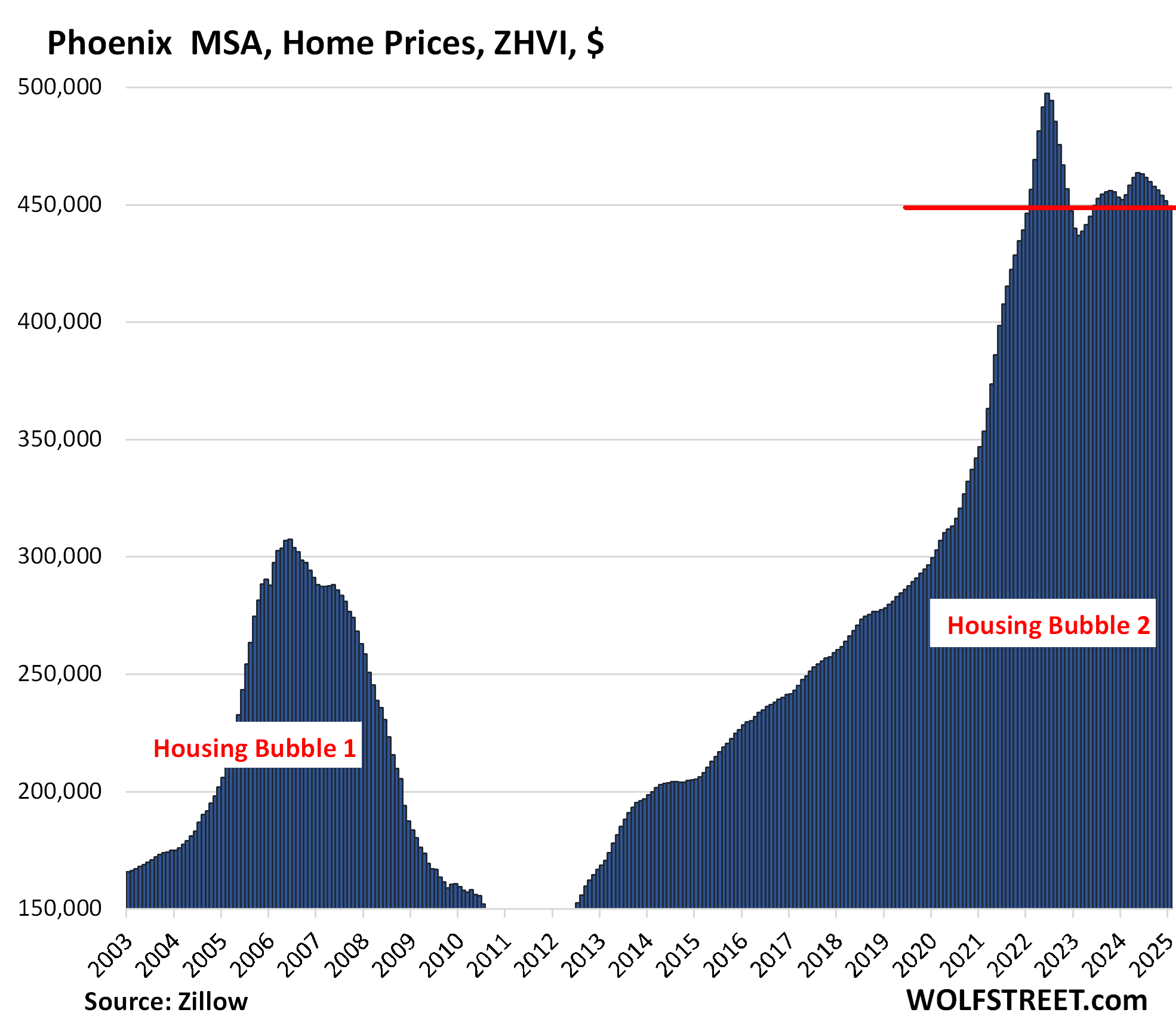

| Phoenix MSA, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -9.8% | -0.6% | -0.8% | 217% |

Prices are back where they’d first been in February 2022:

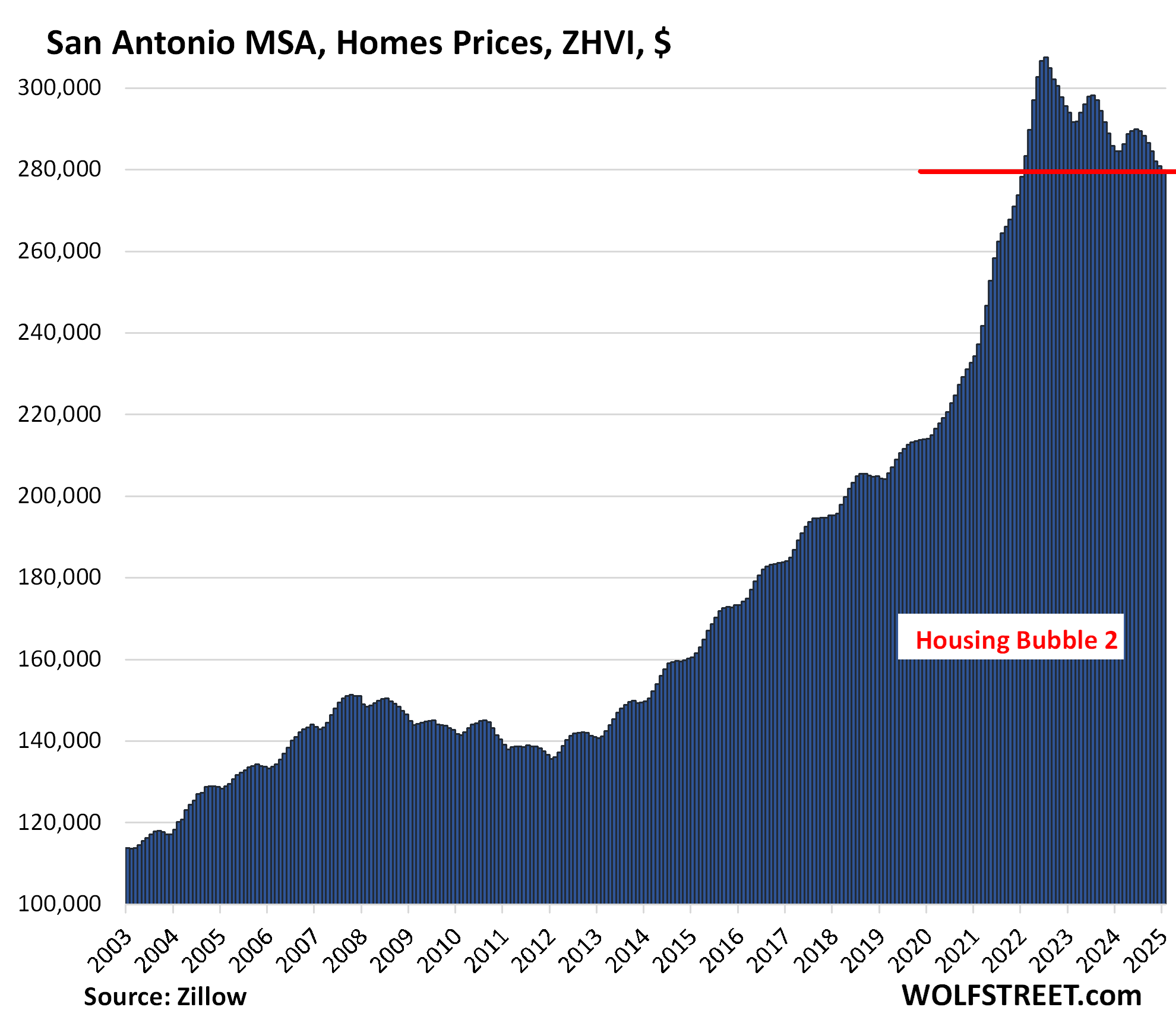

| San Antonio MSA, Home Prices | |||

| From Jul 2022 peak | MoM | YoY | Since 2000 |

| -9.1% | -0.5% | -1.8% | 146.3% |

Prices have dropped to the lowest level since January 2022.

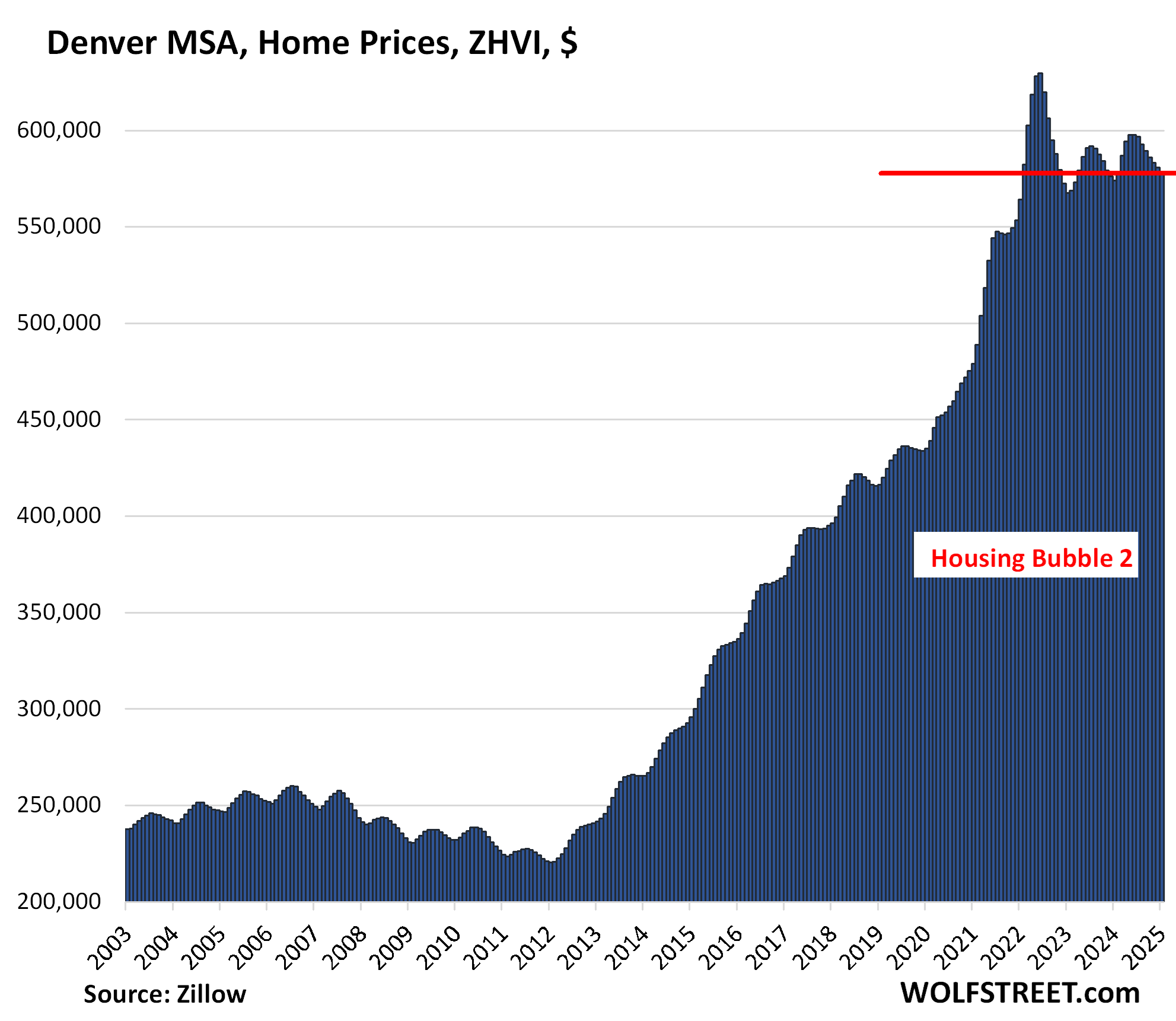

| Denver MSA, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -8.2% | -0.5% | 0.7% | 210% |

Prices are back where they’d first been in February 2022.

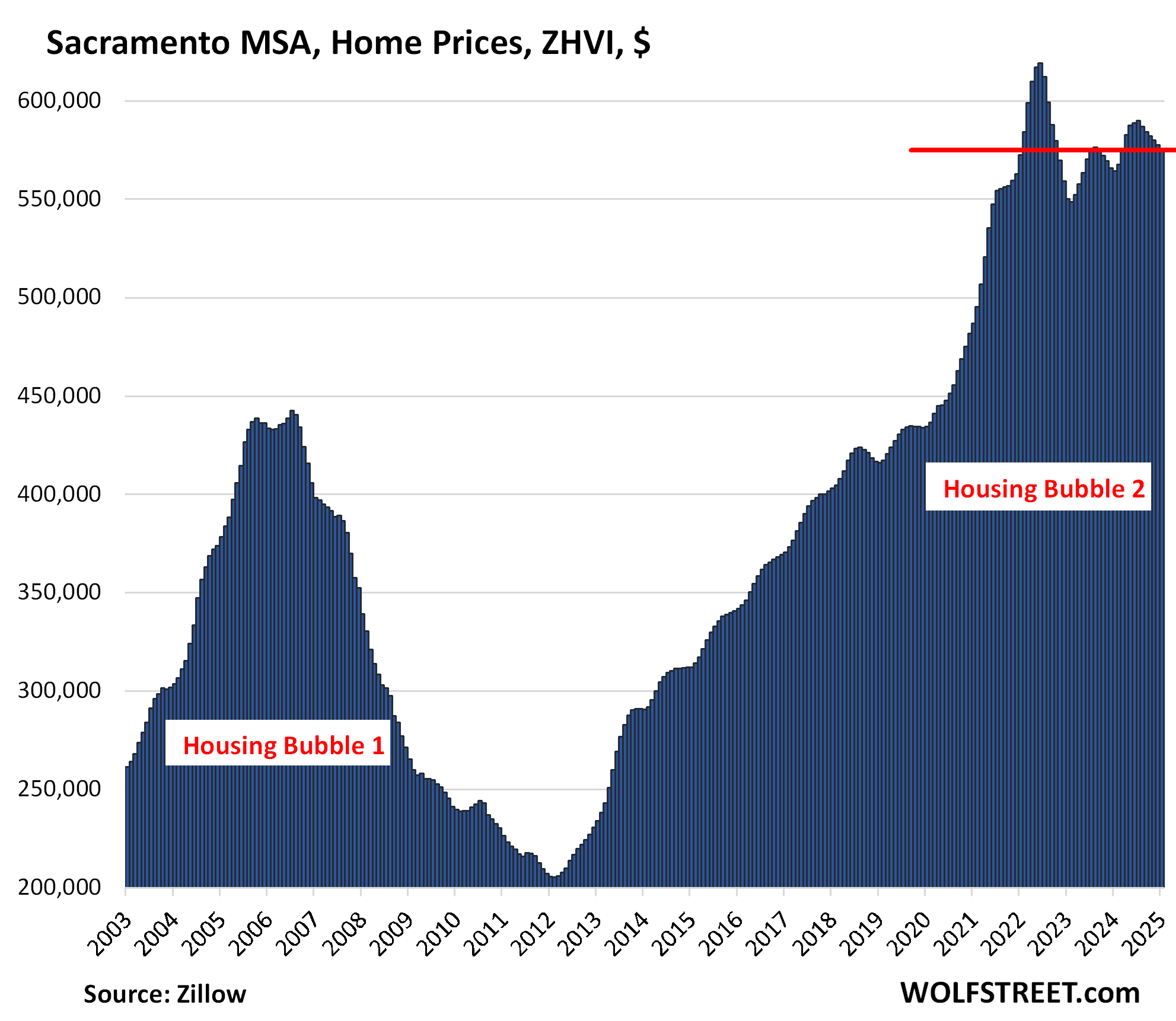

| Sacramento MSA, Home Prices | |||

| From July 2022 peak | MoM | YoY | Since 2000 |

| -7.2% | -0.5% | 1.9% | 243.1% |

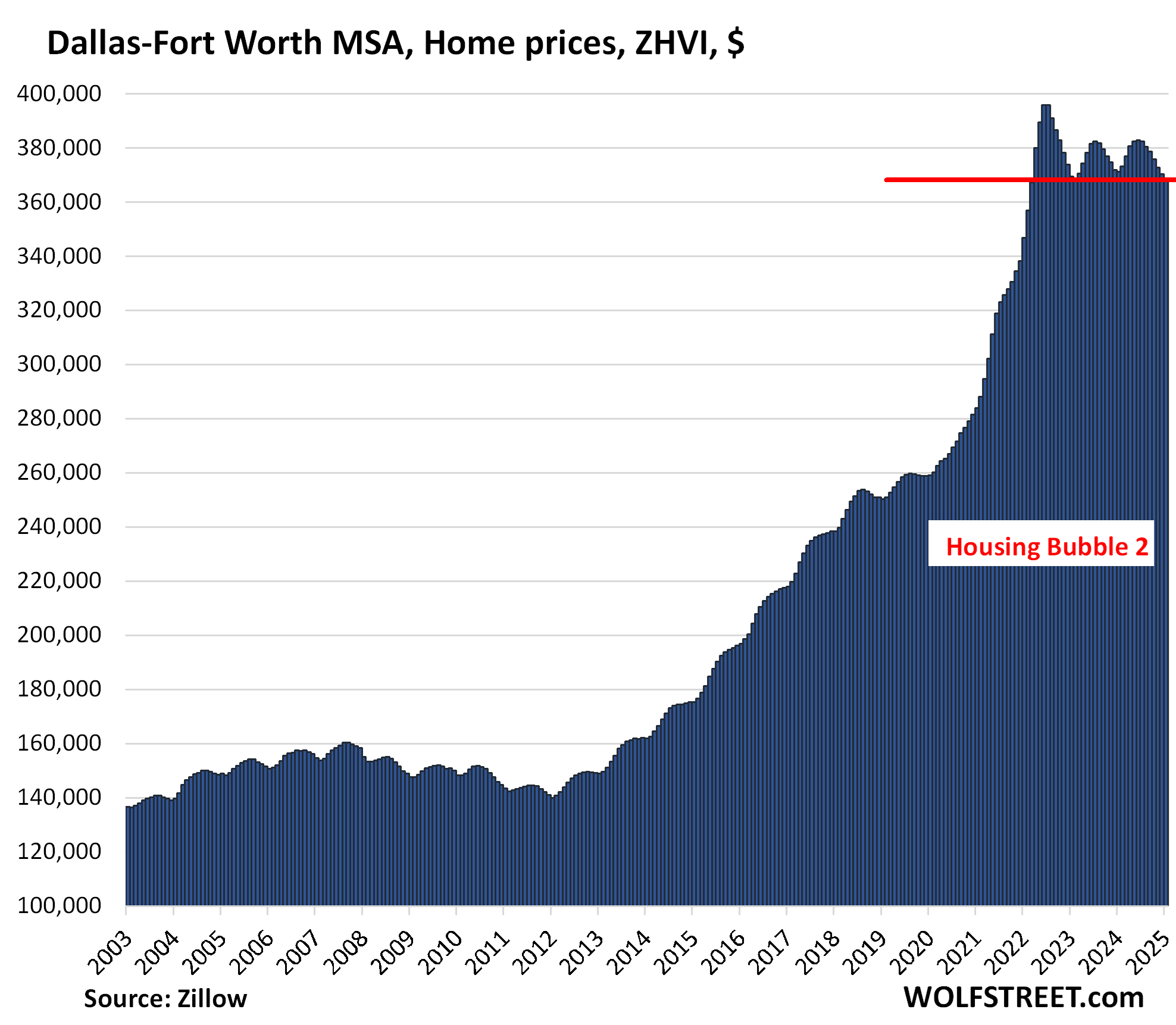

| Dallas-Fort Worth MSA, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -6.9% | -0.5% | -0.7% | 190% |

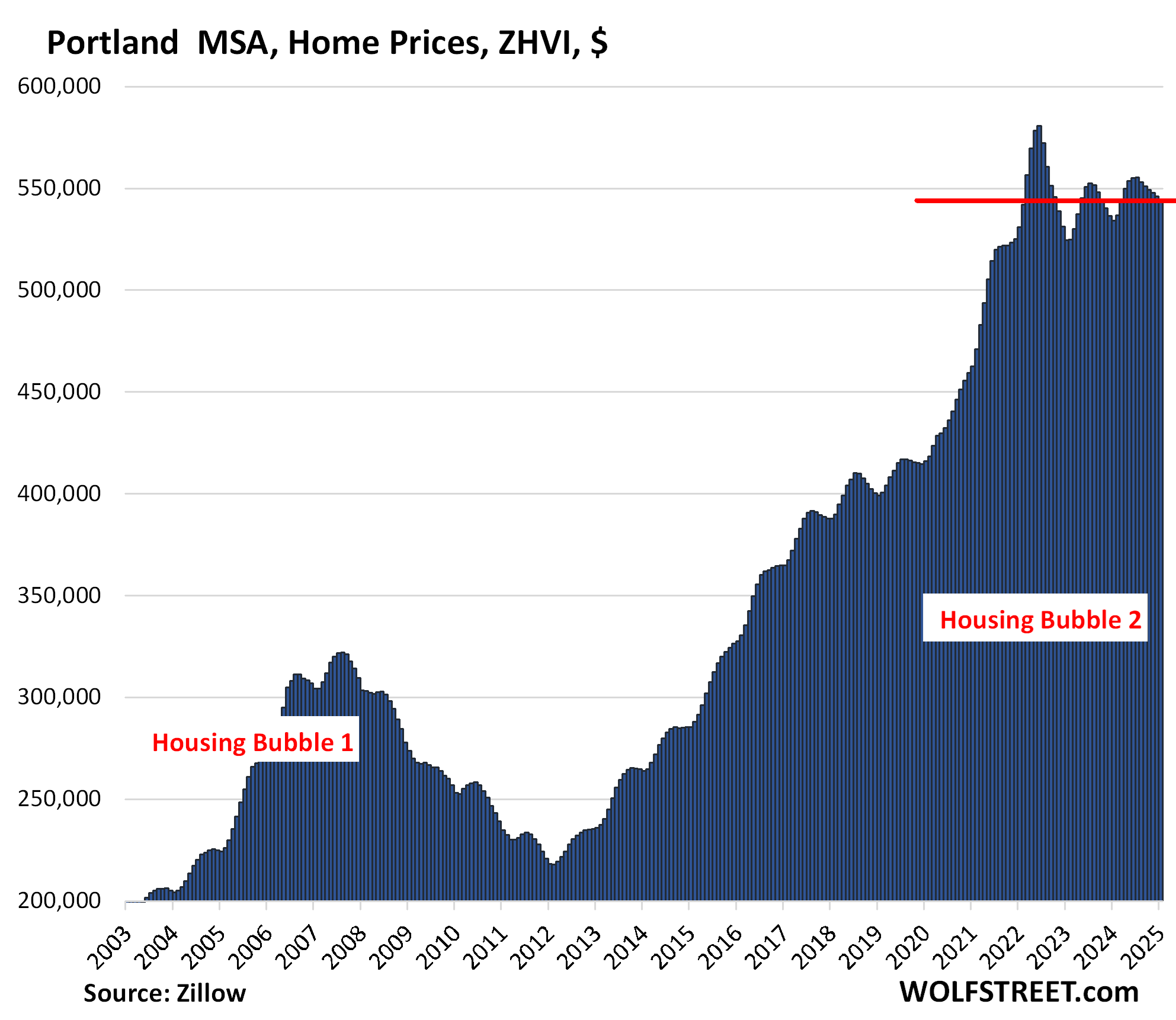

| Portland MSA, Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -6.4% | -0.5% | 1.7% | 215% |

Prices are back where they’d first been in January 2022.

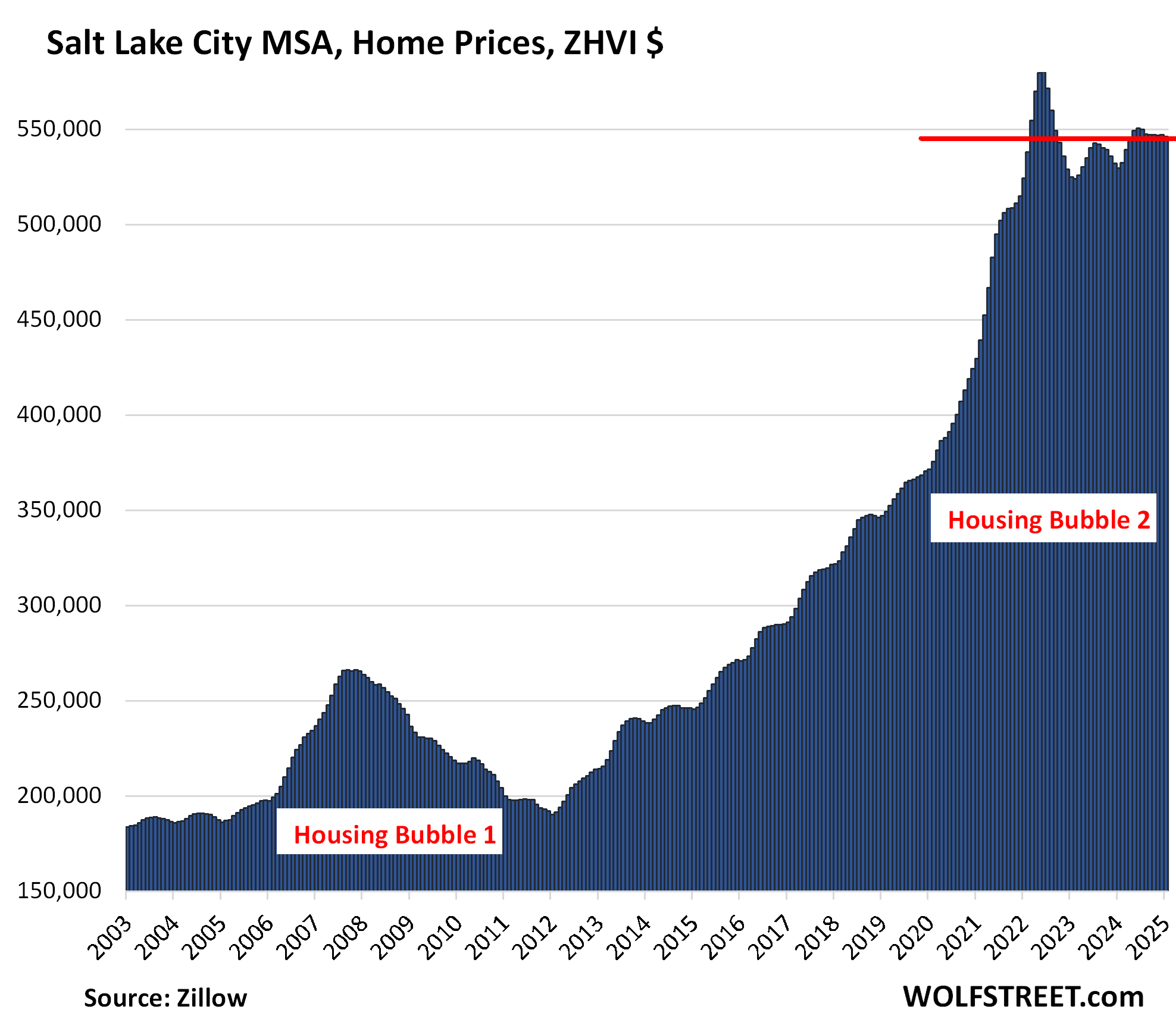

| Salt Lake City MSA, Home Prices | |||

| From July 2022 peak | MoM | YoY | Since 2000 |

| -5.9% | -0.2% | 3.1% | 213% |

Back to March 2022:

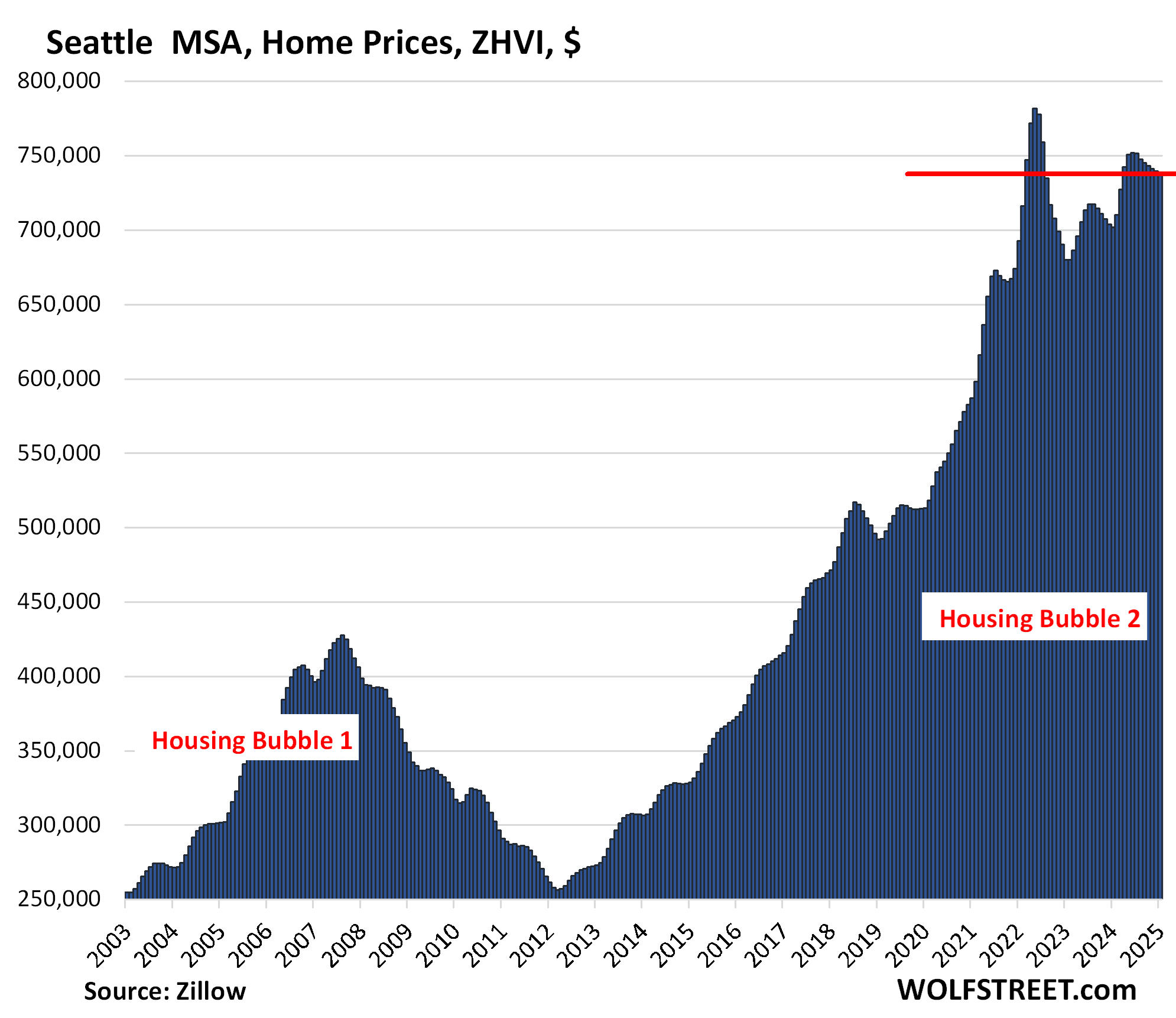

| Seattle MSA, Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -5.6% | -0.3% | 5.1% | 237% |

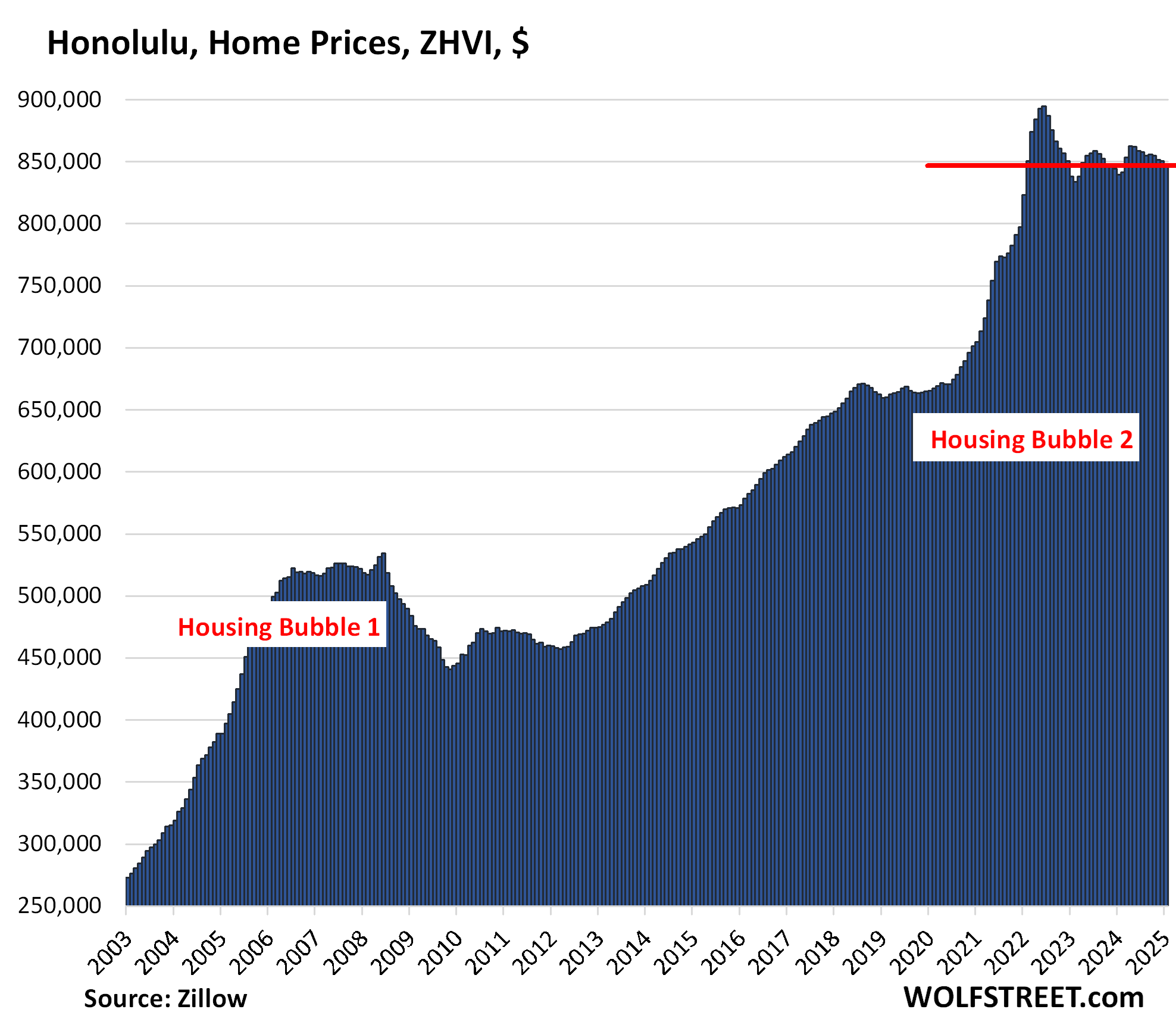

| Honolulu, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -5.3% | -0.4% | 0.9% | 278% |

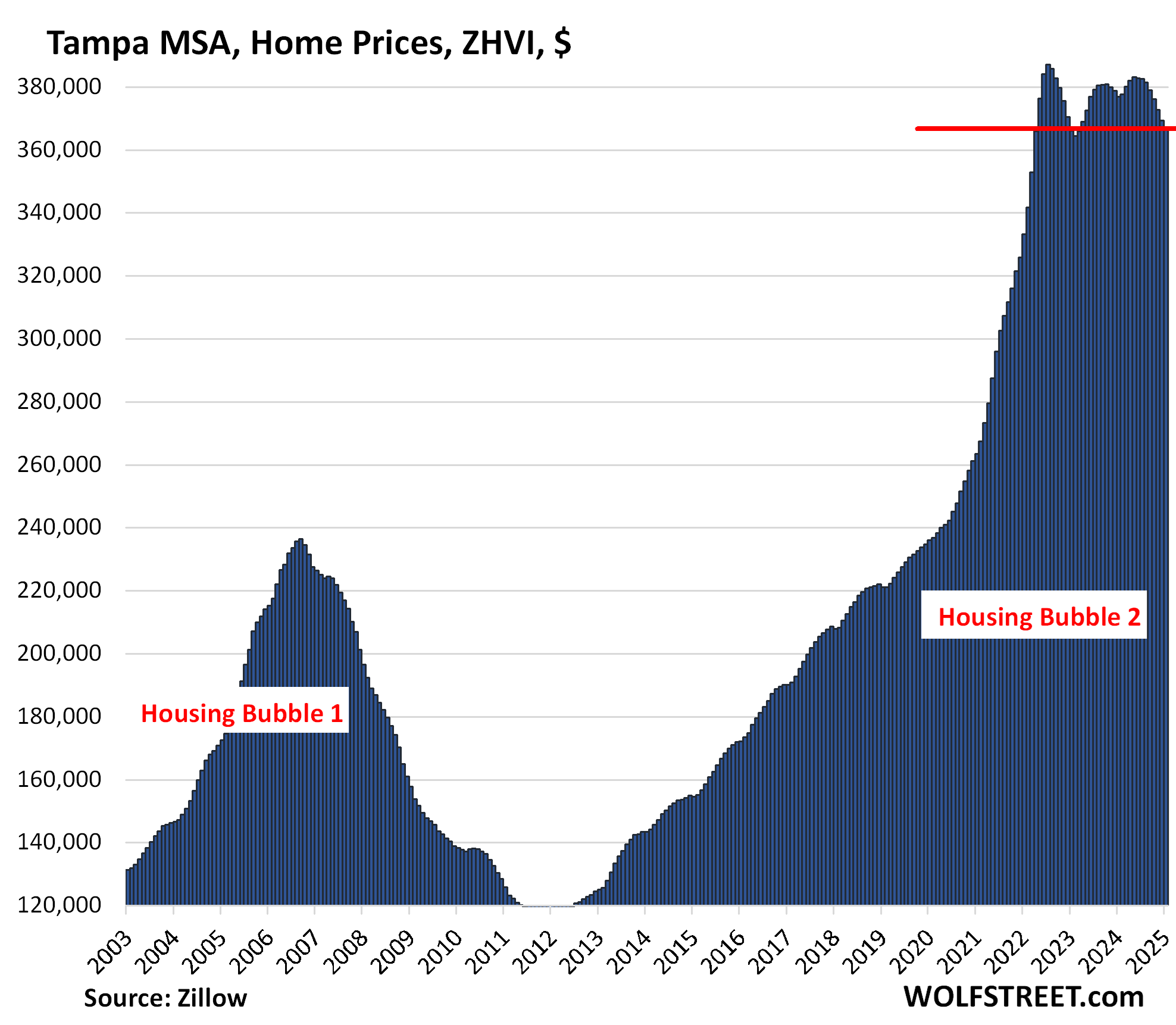

| Tampa MSA, Home Prices | |||

| From Jul 2022 peak | MoM | YoY | Since 2000 |

| -4.5% | -0.6% | -0.9% | 208% |

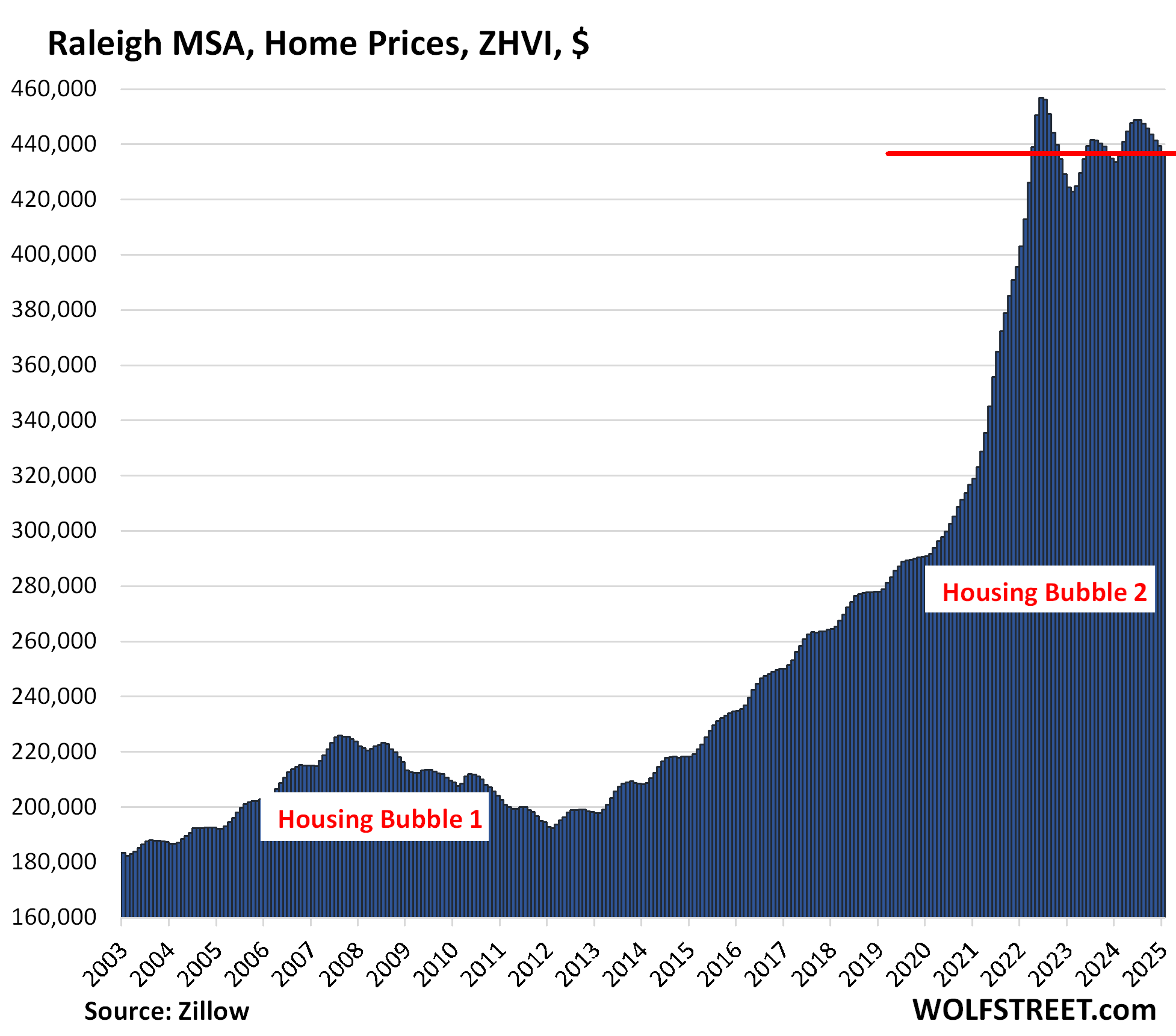

| Raleigh MSA, Home Prices | |||

| From July 2022 peak | MoM | YoY | Since 2000 |

| -4.4% | -0.6% | 0.8% | 156% |

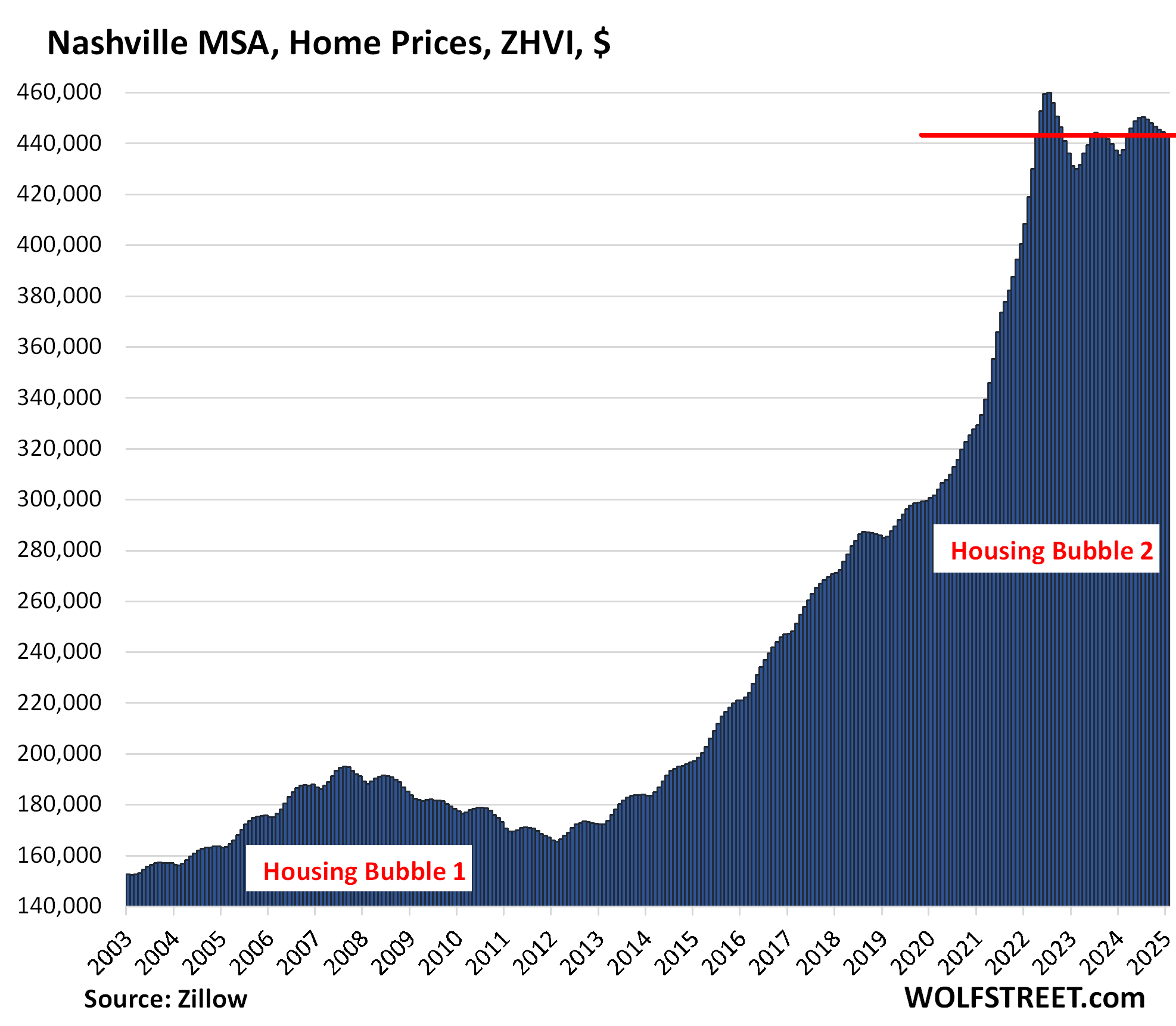

| Nashville MSA, Home Prices | |||

| From July 2022 peak | MoM | YoY | Since 2000 |

| -3.6% | -0.2% | 1.9% | 216% |

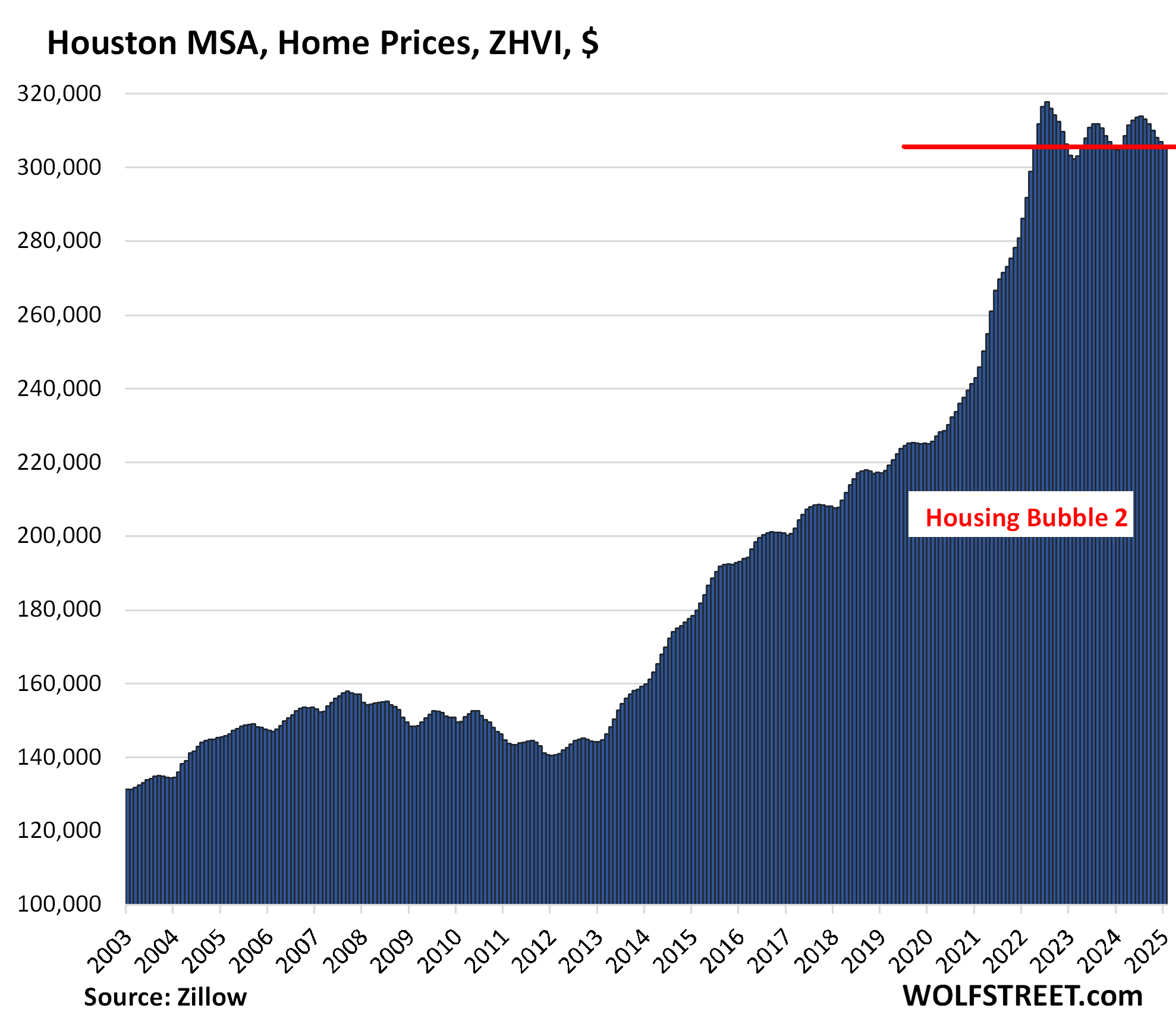

| Houston MSA, Home Prices | |||

| From Jul 2022 peak | MoM | YoY | Since 2000 |

| -3.7% | -0.3% | 0.4% | 149% |

Back to April 2022.

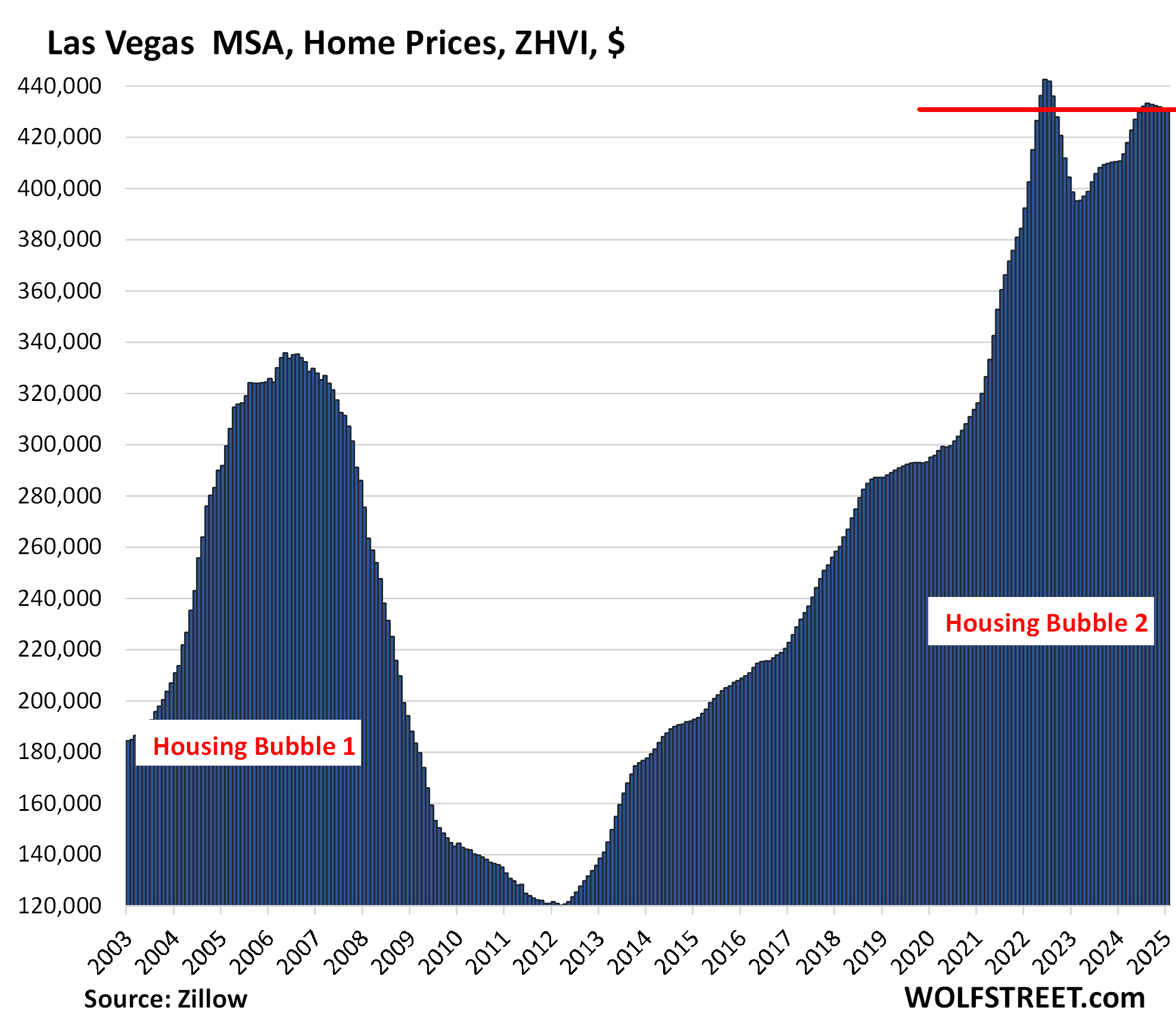

| Las Vegas MSA, Home Prices | |||

| From June 2022 peak | MoM | YoY | Since 2000 |

| -2.6% | -0.1% | 5.0% | 178% |

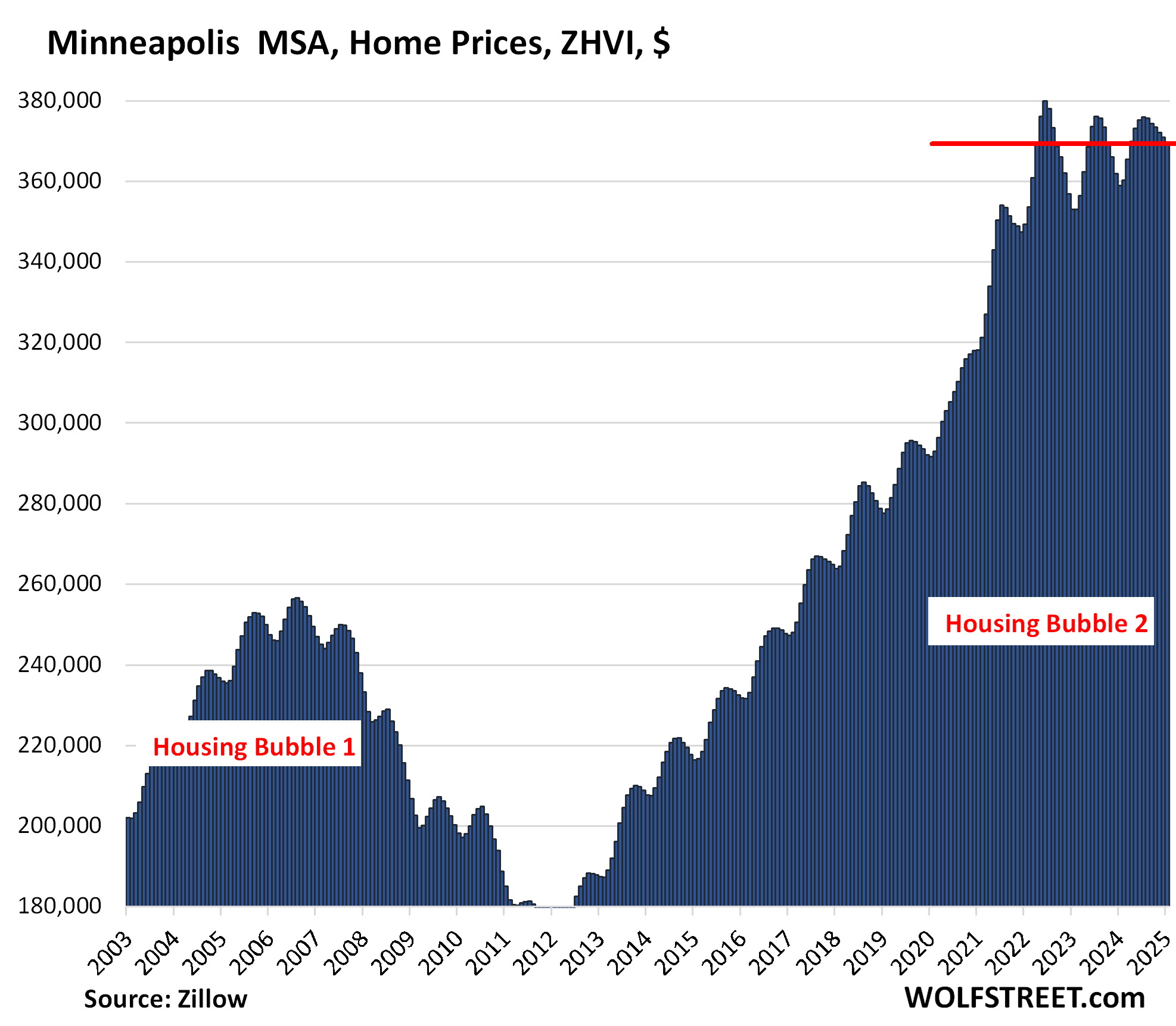

| Minneapolis MSA, Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -2.9% | -0.5% | 2.8% | 155% |

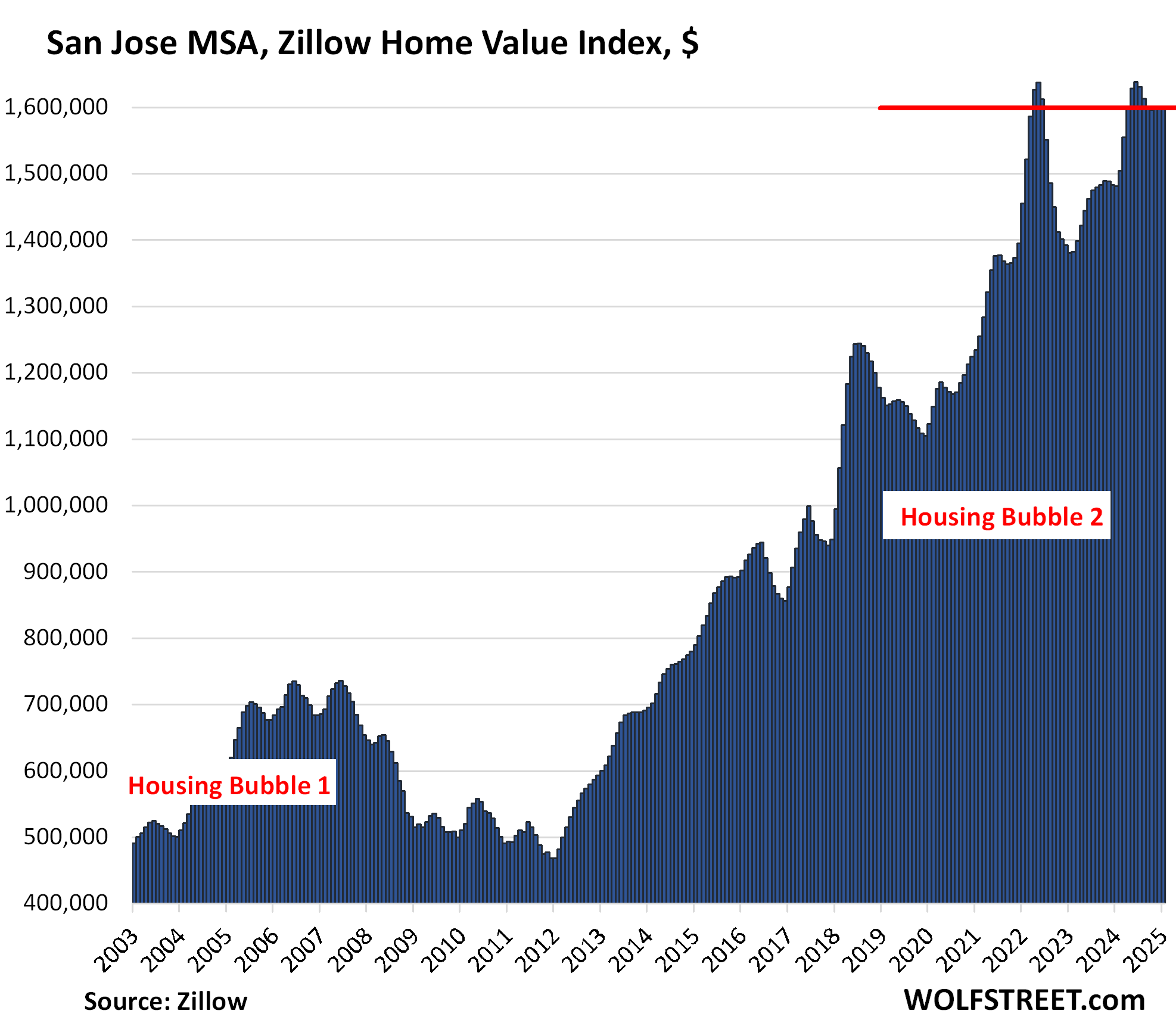

| San Jose MSA, Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -2.3% | 0.0% | 8.1% | 337% |

Prices have been essentially unchanged for the past five months.

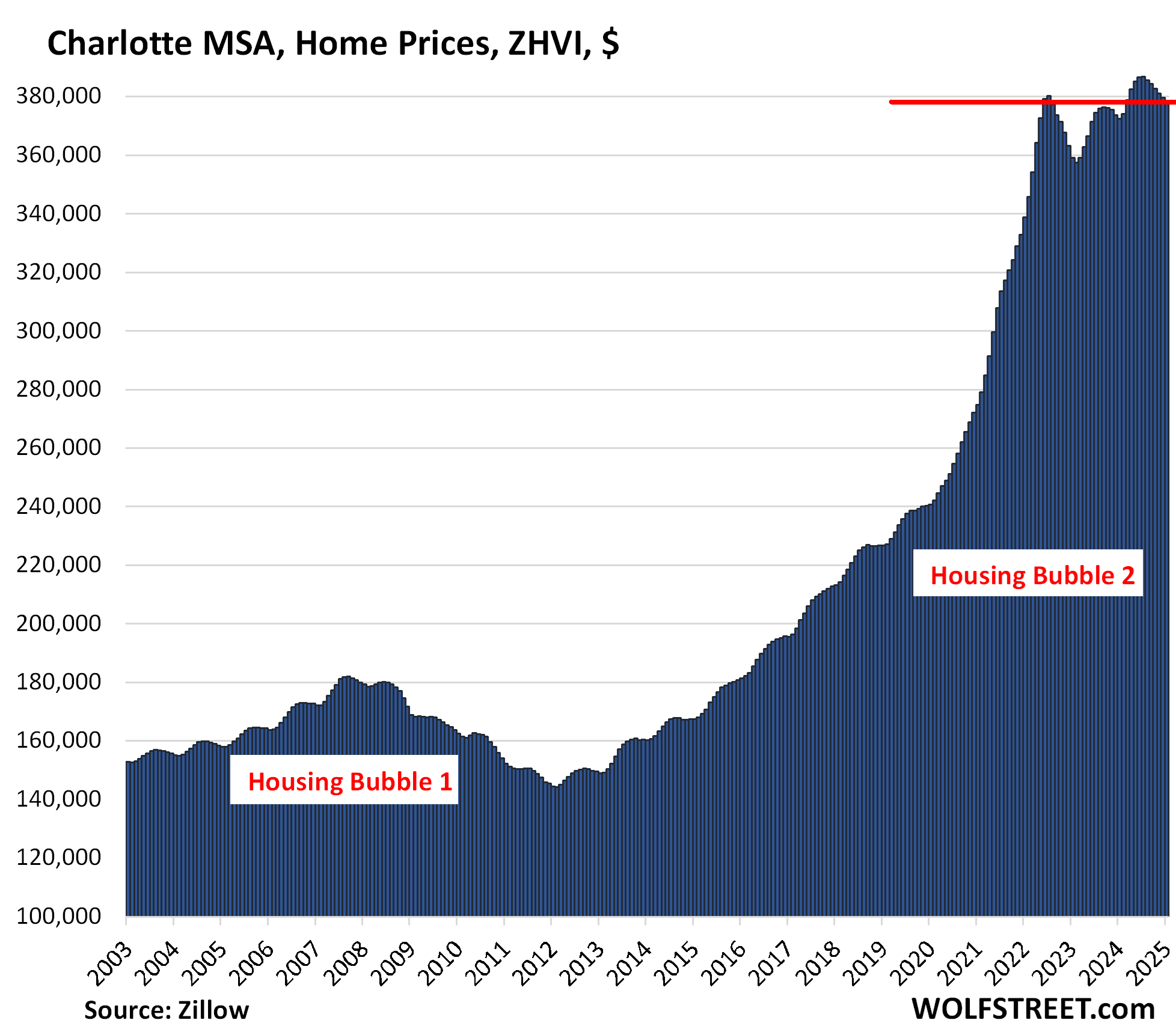

| Charlotte MSA, Home Prices | |||

| From June 2022 | MoM | YoY | Since 2000 |

| -0.5% | -0.4% | 1.6% | 168% |

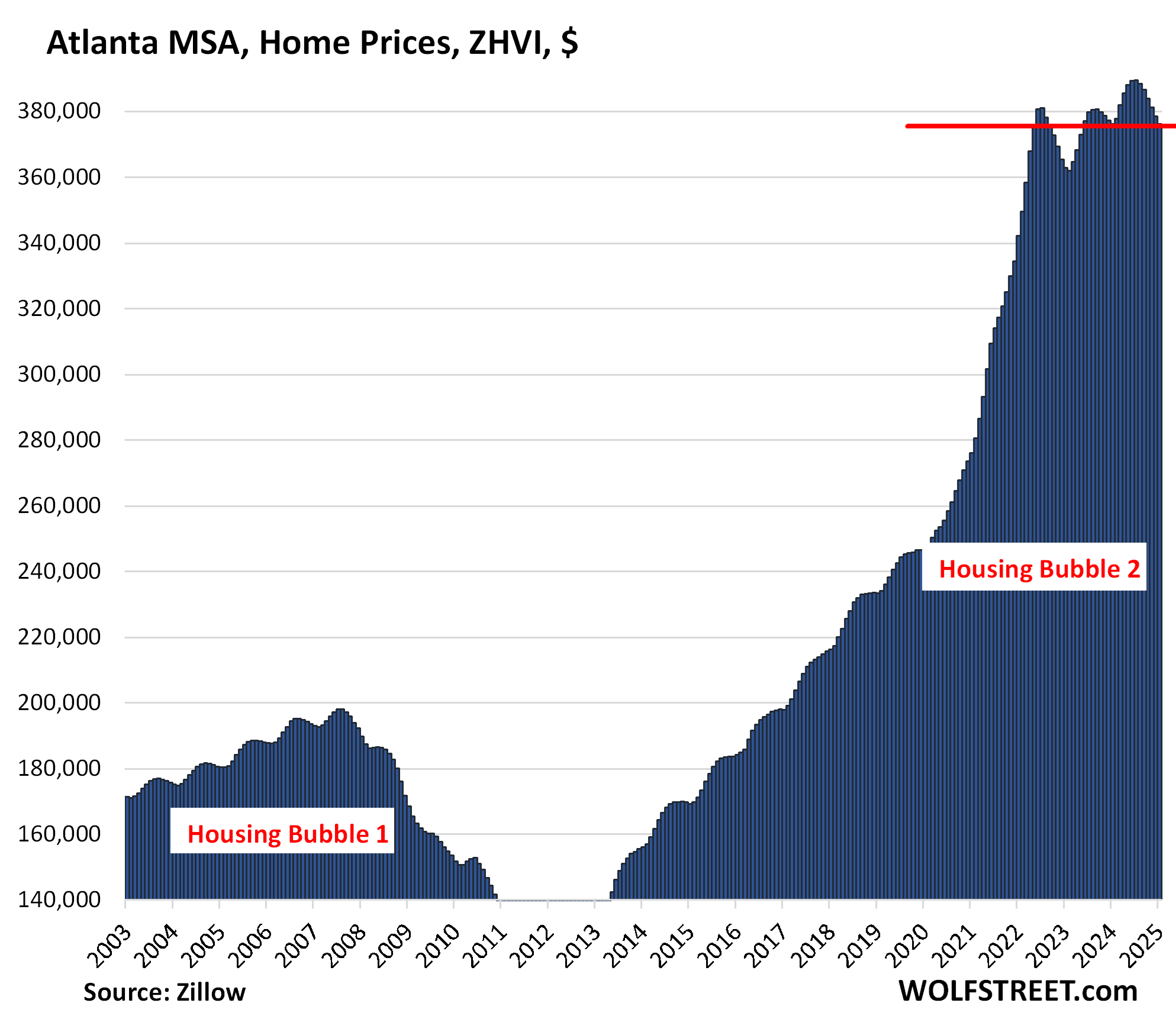

| Atlanta MSA, Home Prices | |||

| From July 2022 | MoM | YoY | Since 2000 |

| -1.3% | -0.6% | 0.0% | 158% |

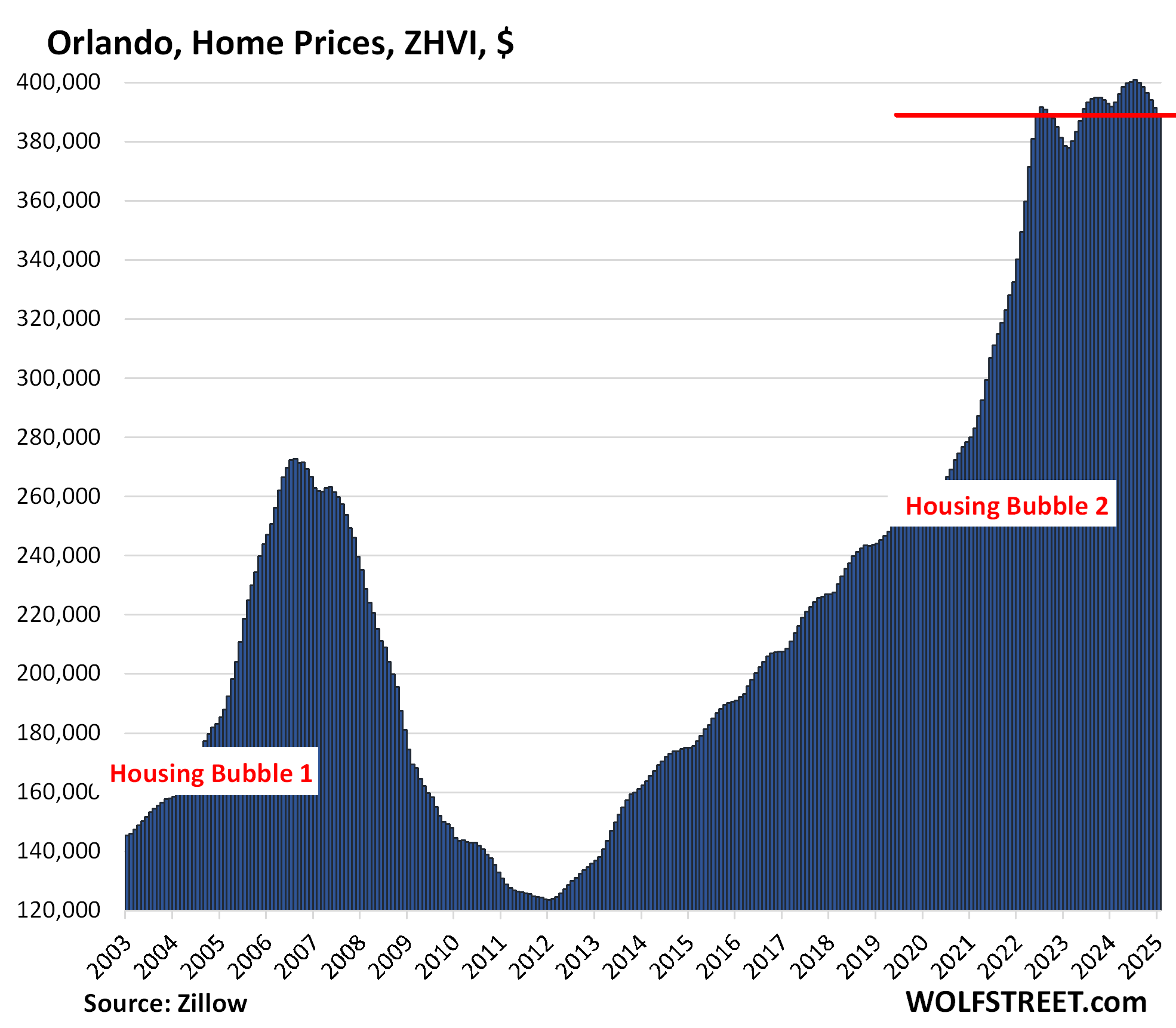

| Orlando MSA, Home Prices | |||

| From June 2022 | MoM | YoY | Since 2000 |

| -0.56% | -0.5% | -0.6% | 232.6% |

The next 12 markets powered on after mid-2022, but declined more recently (seasonally or not seasonally):

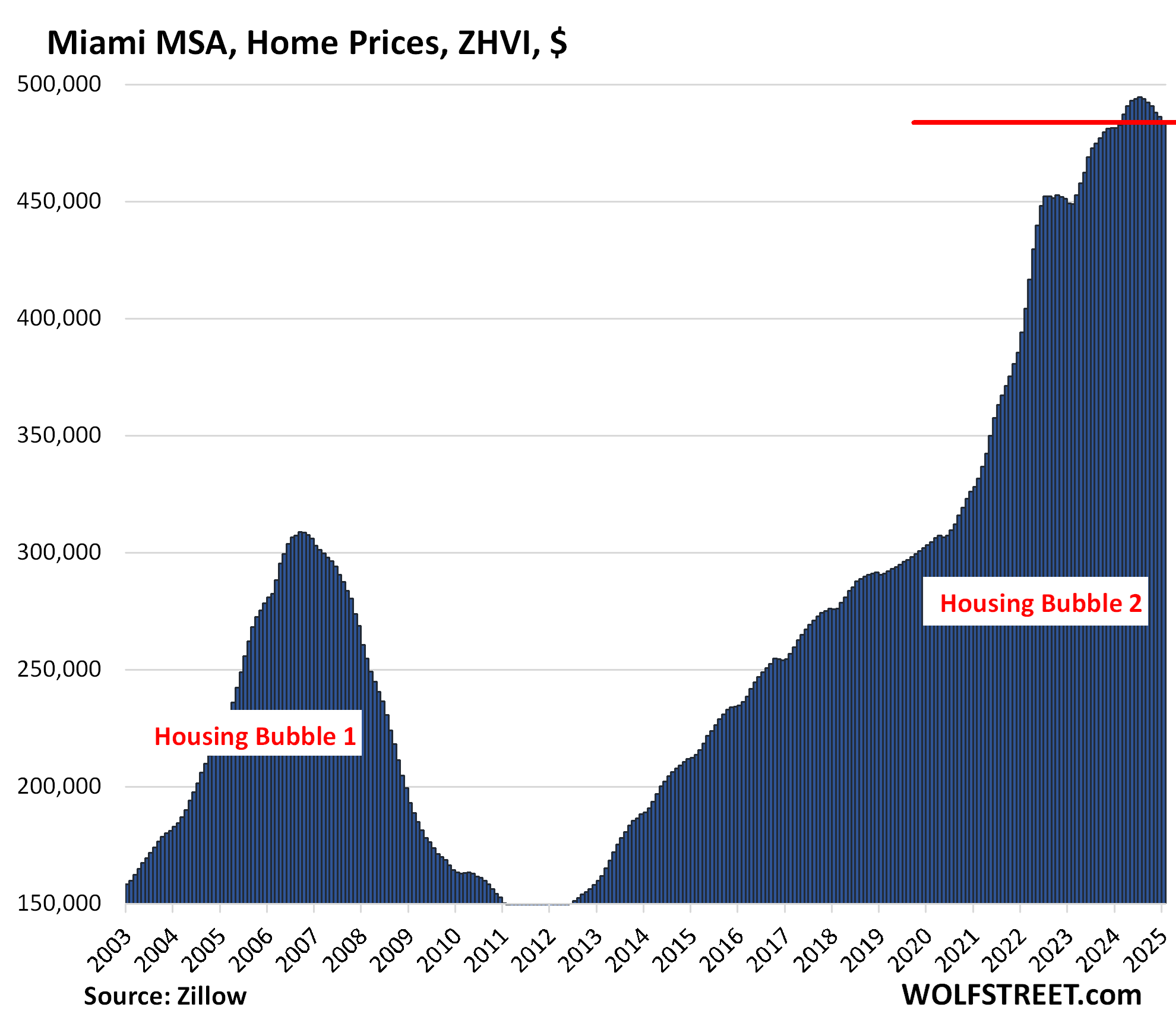

| Miami MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| -0.5% | 0.5% | 327.3% |

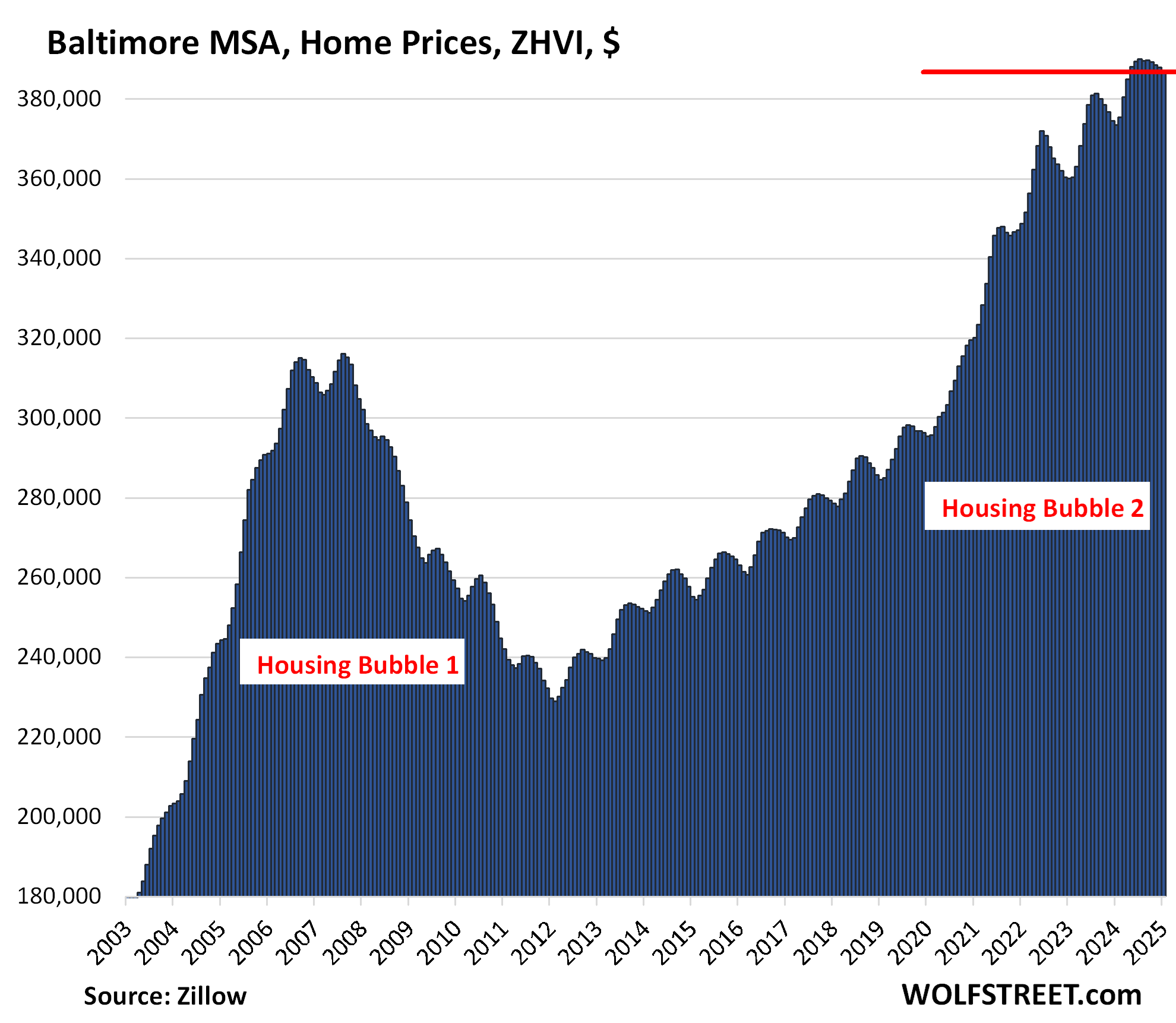

| Baltimore MSA, Home Prices | |||

| MoM | YoY | Since 2000 | |

| -0.2% | 3.7% | 173% | |

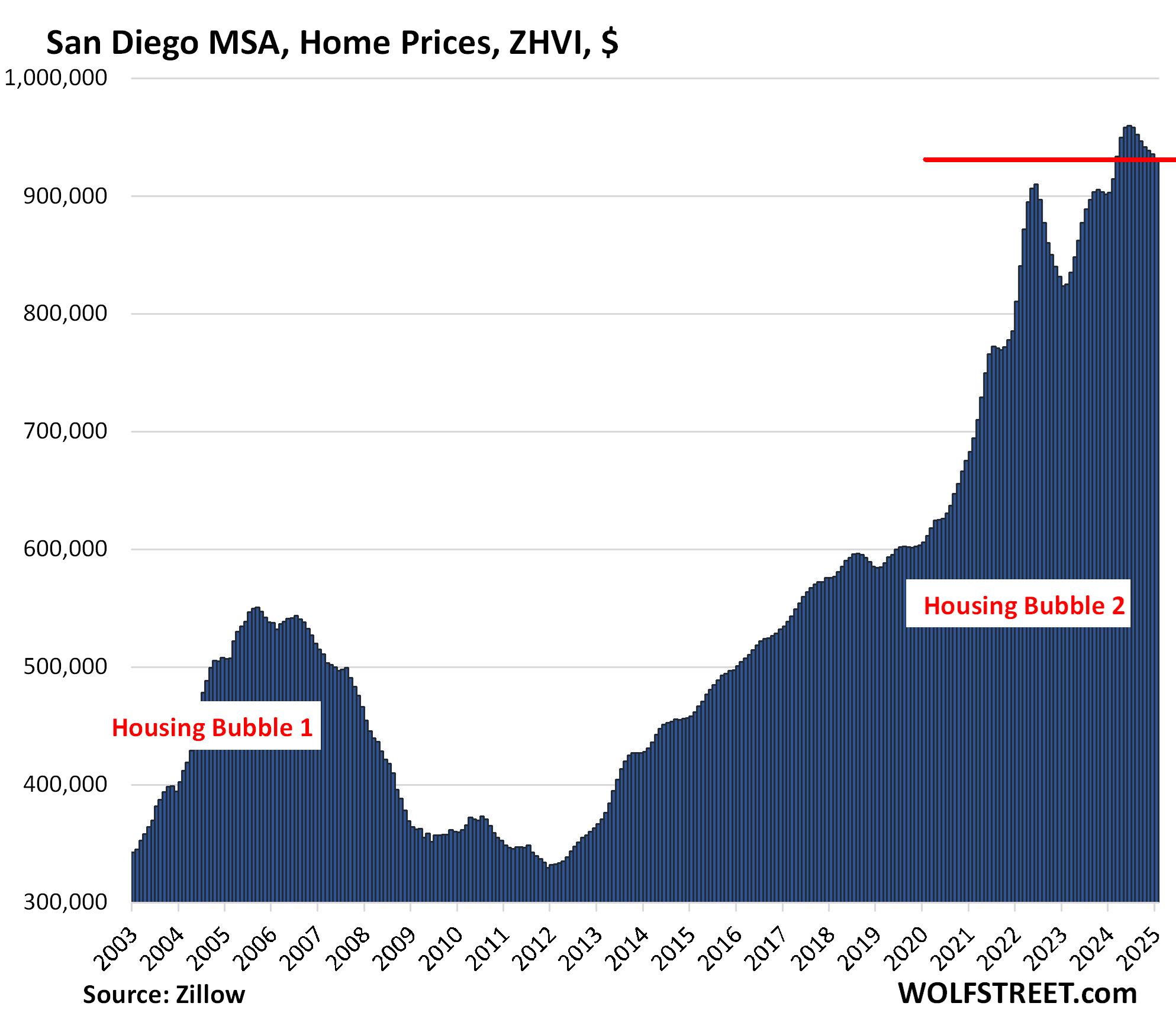

| San Diego MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| -0.4% | 3.2% | 331% |

| Kansas City MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| -0.3% | 3.7% | 174% |

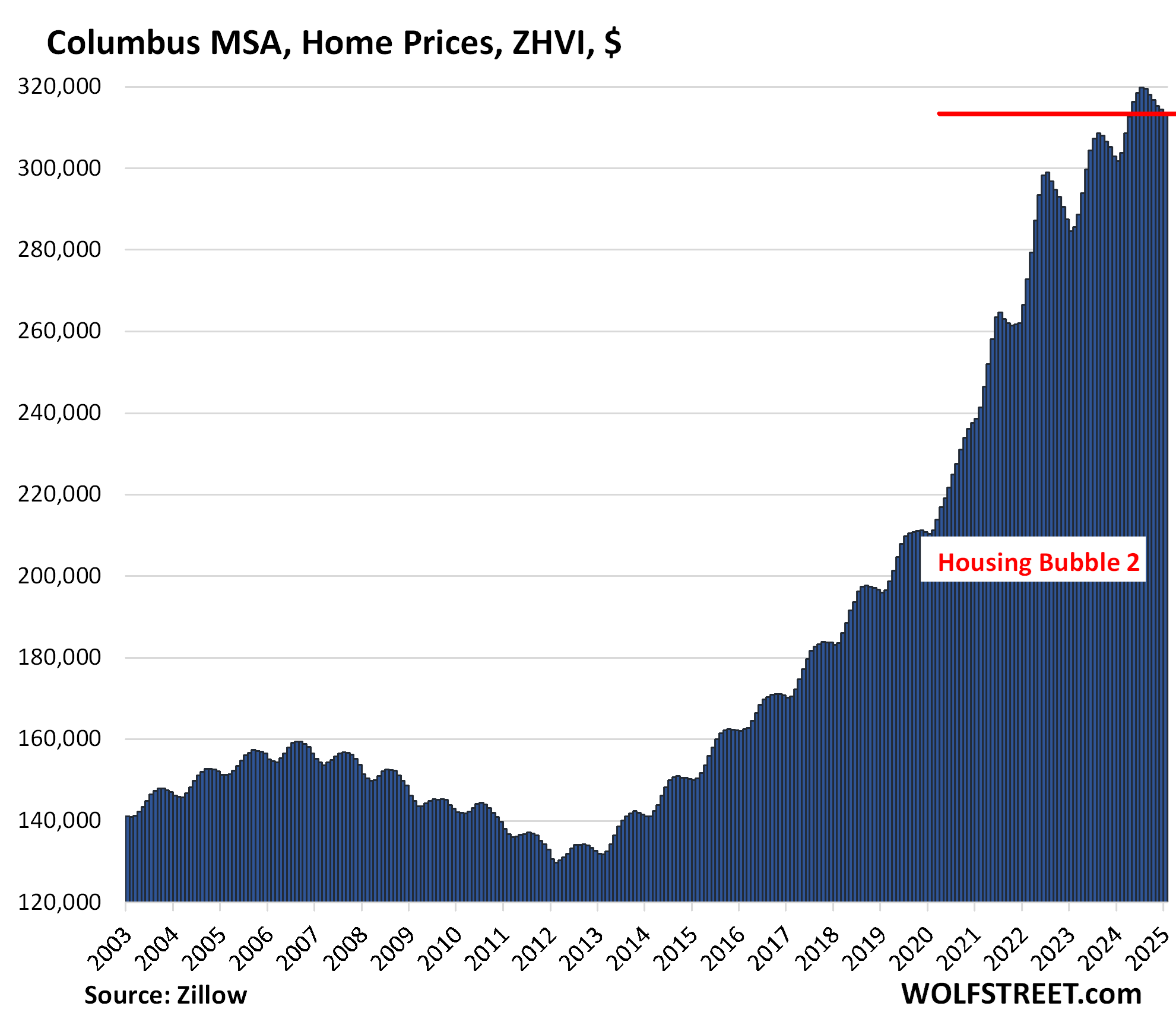

| Columbus MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| -0.3% | 3.8% | 152% |

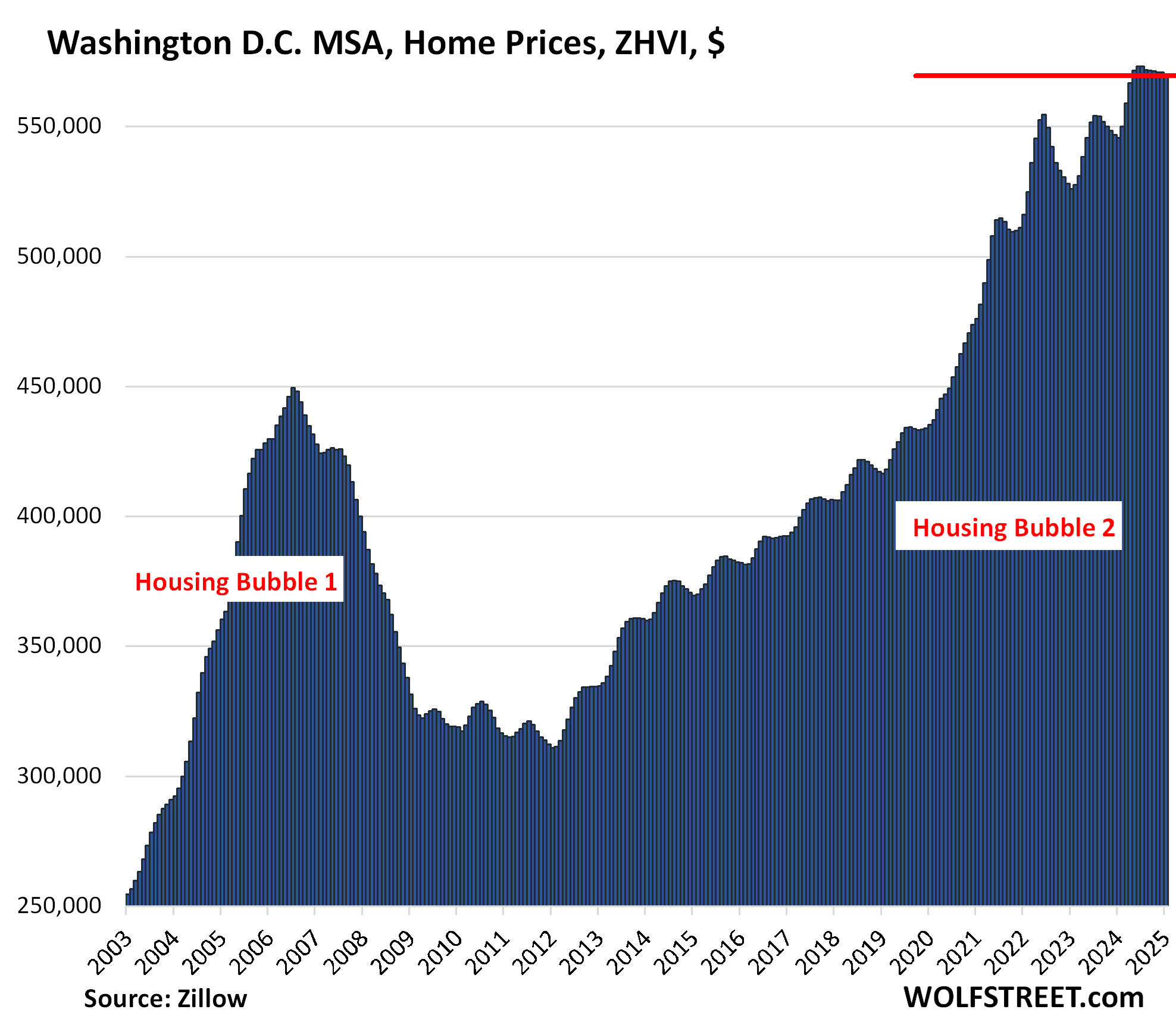

| Washington D.C. MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| -0.1% | 4.5% | 215% |

The huge metro includes Washington D.C. and parts of Maryland, Virginia, and West Virginia.

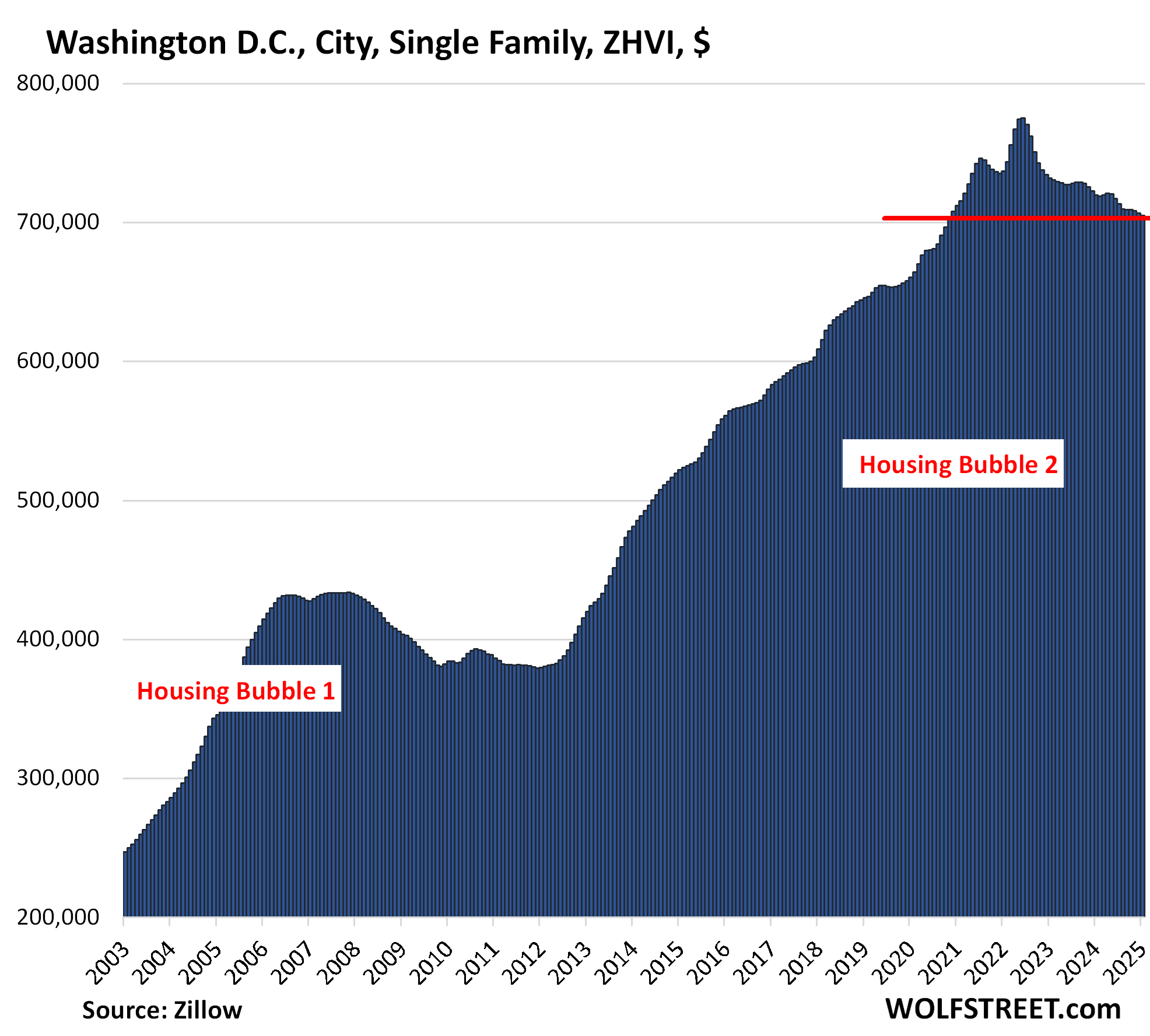

But in Washington D.C., the city by itself, prices of single-family houses, seasonally adjusted, have dropped by 9.1% from the peak, to the lowest level since November 2020.

This shows how there can be a big difference between the MSA index, which covers a lot of different markets, and the index of a city by itself:

| Washington D.C., City, Single-Family Home Prices | |||

| From Jun 2022 | MoM | YoY | Since 2000 |

| -9.1% | -0.3% | -2.1% | 287% |

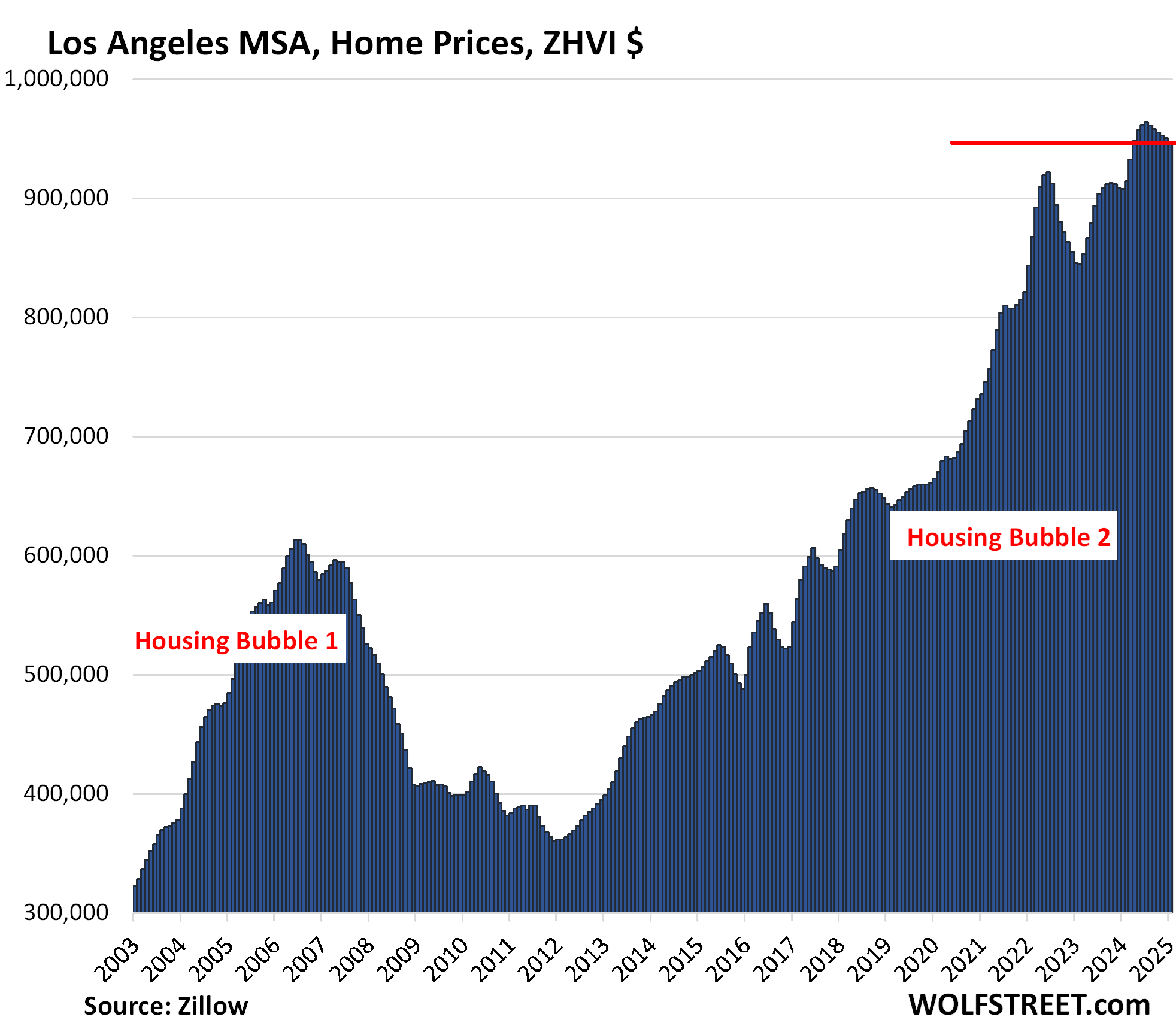

| Los Angeles MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| -0.4% | 4.3% | 327% |

| Philadelphia MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| -0.3% | 4.6% | 199% |

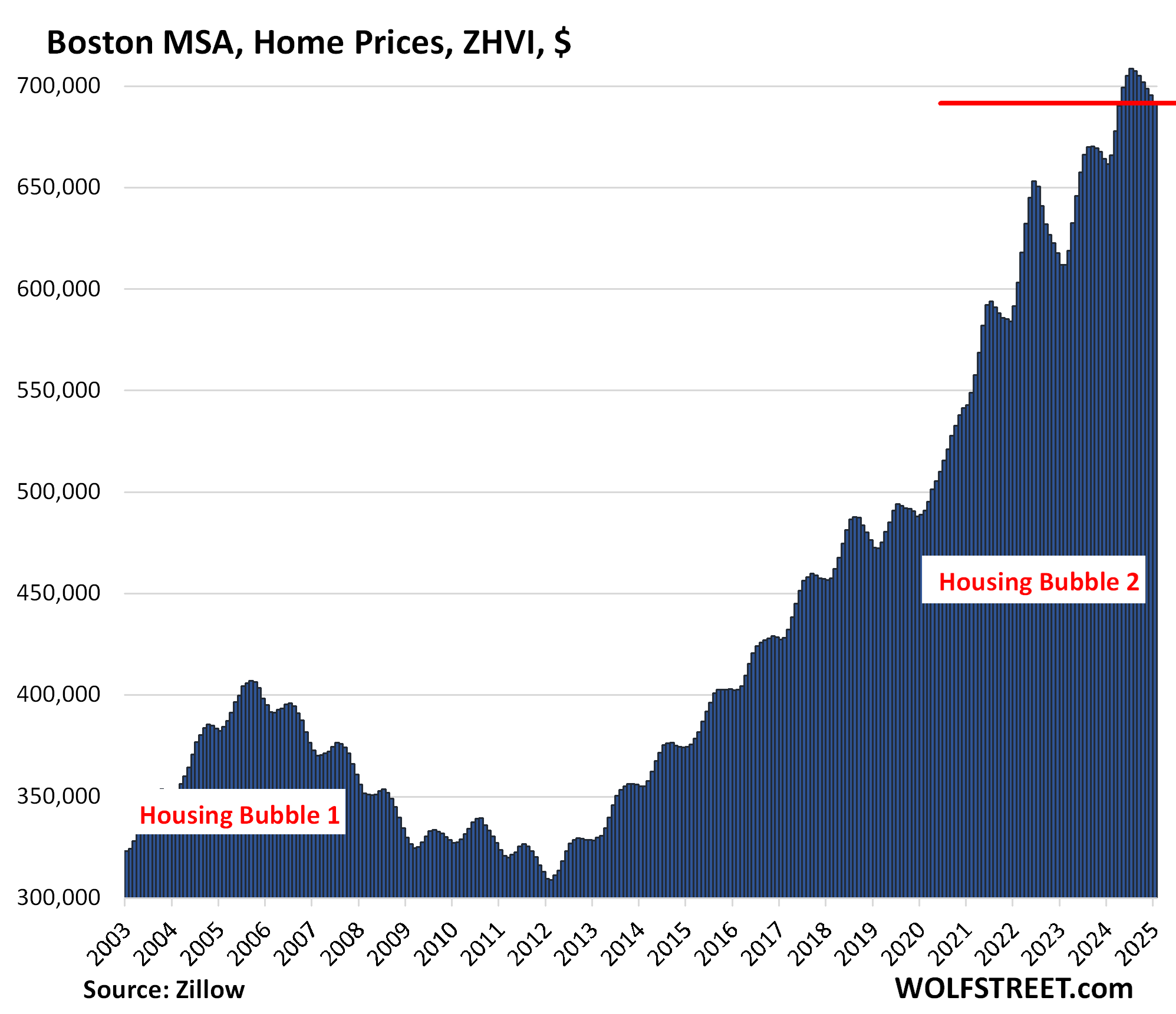

| Boston MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| -0.5% | 4.6% | 222% |

| Milwaukee MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| -0.4% | 5.5% | 141.3% |

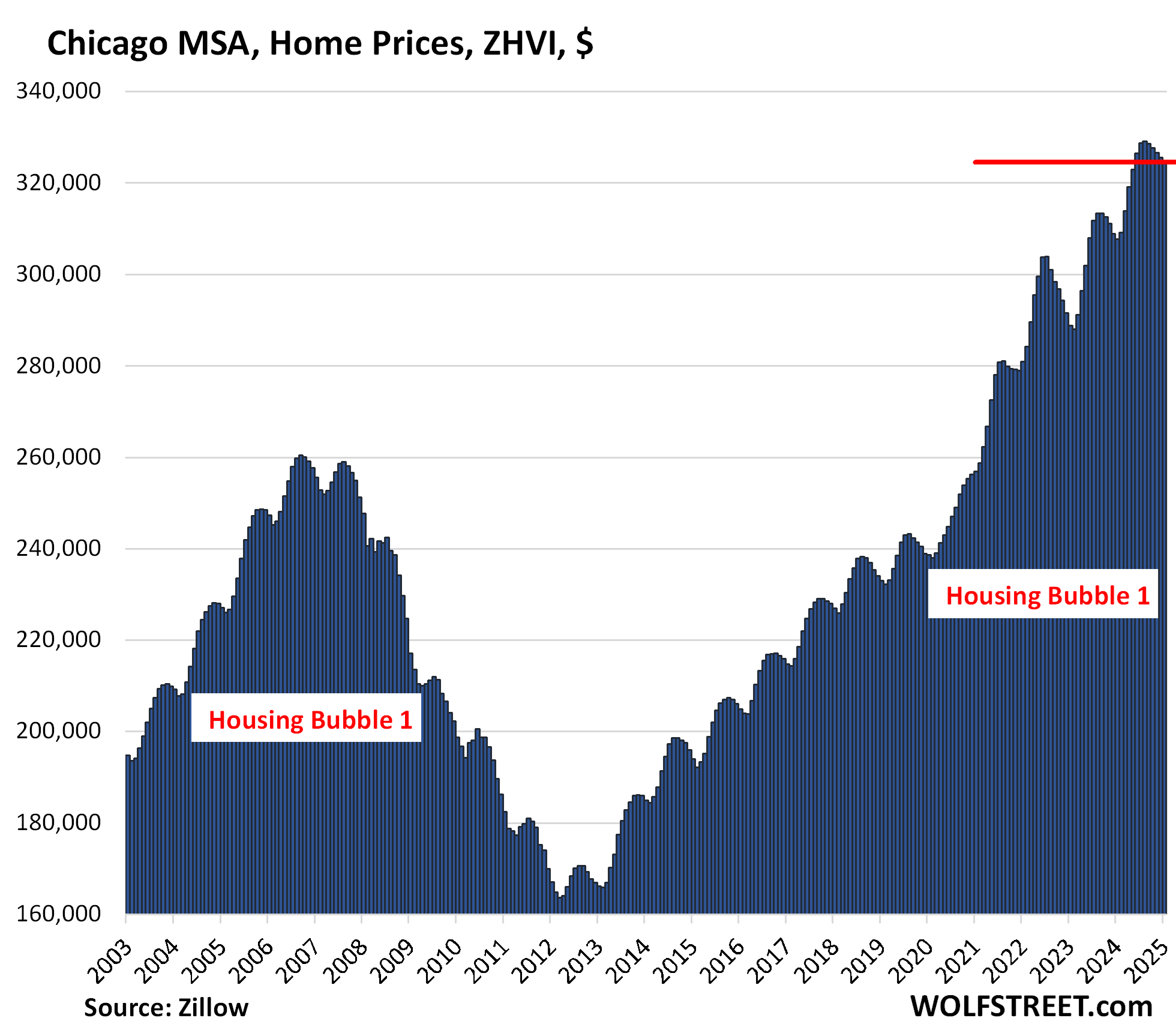

| Chicago MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| -0.3% | 5.5% | 111% |

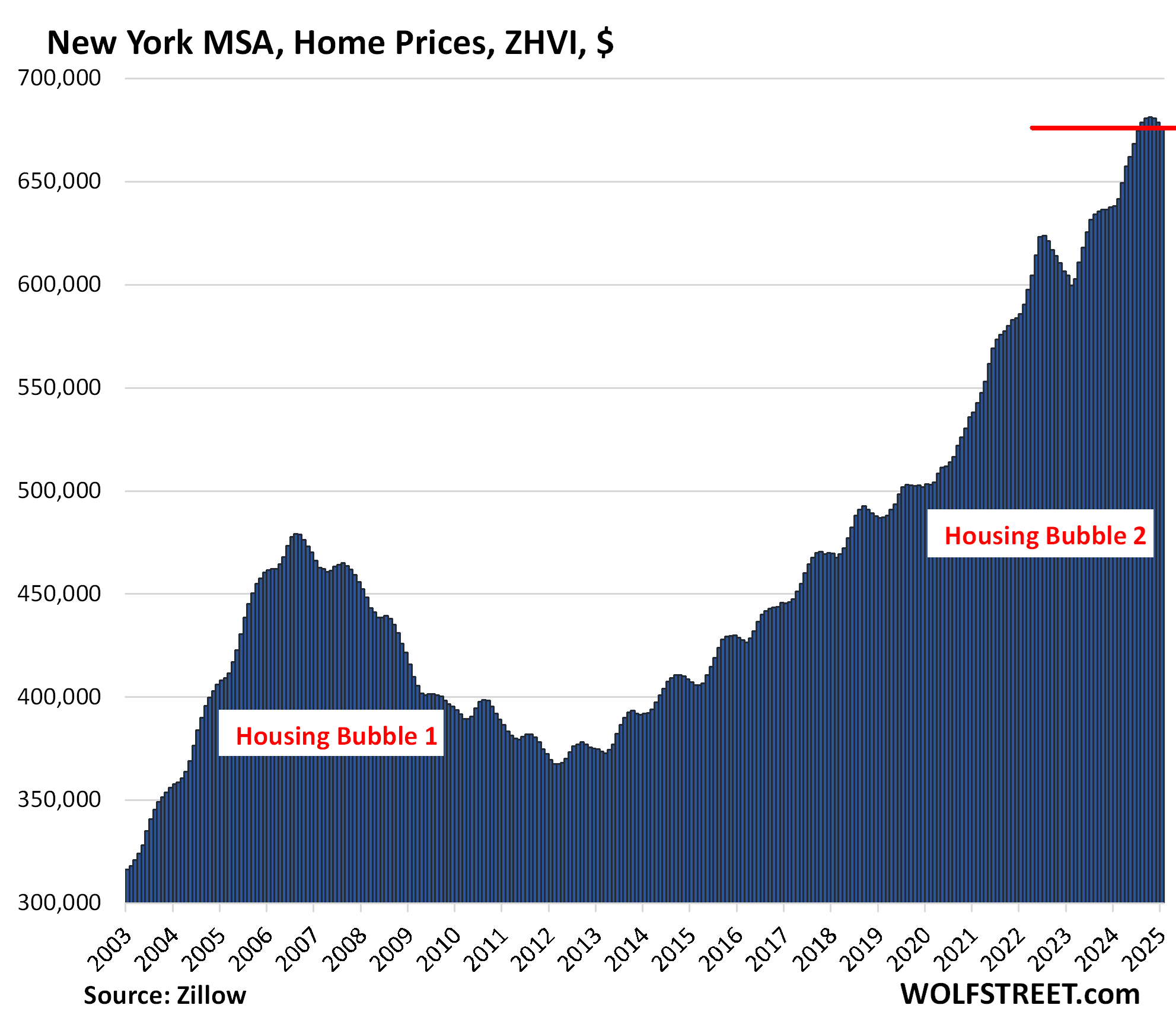

| New York MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| -0.3% | 6.0% | 210% |

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

To da MOON in 11570!!!

80 percent of mortgages under 5%…50% under 4%… the FED fueled the bubble and local governments which benefit from the bubble need their own Doge…many mortgage free are dropping homeowners insurance, putting up fences, no trespassing signs and always having one party at the residence in case of fire…rolling the dice on storms…they simply don’t have the funds.

Team Bubble is still winning….. Would be interesting to see what the land only price is for the homes that burned in LA. Likely nearly as much as before the house burned down. Maybe with the USG resignations/layoffs/DOGE, Washington DC will weaken??? A bubble made of steal, especially inside the beltway.

“A bubble made of steal, especially inside the beltway.”

RTGDFA, at least look at the pictures, including this one from way upstairs, so I just repost it down here:

With federal RTO/DOGE the Washington MSA will plummet and the Washington City will go up.

You forgot the layoffs of government employees, and the gazillion contractors and employees of government contractors getting cut loose? Are they going to suddenly buy homes in DC after they’re out of a job? Or are they going to sell their home in DC or in the metro after they lose their job?

Lots of known unknows here. And prolly some unknown unknowns (sorry, Rumsfeld).

Any cautious government employee is going to trim back spending whether their job is targeted or not. All federal jobs are less stable now. It will create deflationary pressures in the short term and maybe the long term. State and local government jobs might get caught in the wave as well.

Could this prick the stock market bubble?

Yes, I think the bubble will pop in the DC, Maryland and Virginia Area within 30 miles of the nation’s capitol. But what I’m seeing is 2 bubbles, this last one worse than 2007; and people are trapped in their 3% mortgages. Inventory is rising and houses are unaffordable for many Americans. I’m considered moving to Thailand where rent and condo prices are 30% of what they are in the states. And the foods a lot better. I’ve been in Thailand and Malaysia and liked them both. I’ve also been in China but the cost of living there is more.

From a practical standpoint, I can see why the San Jose market stays buoyant. For anyone shifting to a hybrid or remote position, its alluring to move out of the city to a place like SJ where there is seemingly less crime and more open space, per se. If you need to go into office, a commute on the 280 will suffice.

We have a lot of California equity refugees here in Oregon. We don’t want anymore of them.

Ah! The famous Not In My Backyard …

Lived in Denver before it exploded and became the California destination. You should preemptively move. It will only get worse and worse

They say the exact same thing in Boise, Idaho and Salt Lake City, Utah. Probably say it a lot of other places too.

I’ll second this. Tried to drive home from skiing yesterday and stuck, spun out, and abandoned cars with CA plates everywhere left in the middle of driving lanes. Took 5 hours to drive 16 miles, a fleet of tow trucks was towing them up to the Eisenhower tunnel. These were normal winter conditions, not a blizzard, not white out, not slippery. The roads had been plowed just a had maybe 1/2 inch of snow on them since it was flurrying. Once I got past them I was able to drive 45 mph without issue on these same roads with out any slipping or sliding

Not to mention them brining their politics, the more CA liberals we’ve gotten (no problem with actual liberals, just the pretentious hypocritical ones) the more crime and homeless we’ve gotten. My favorite is let’s try to cut police spending and make urban camping legal, but oppose the metro to Boulder because the rich people don’t want poor or homeless people in their town.

Every time CA threatens to secede, I hope they do it. Then they’d be subject to our immigration controls to move to other parts of the US.

Half the license plates here in Dallas Texas are California, the governor was thinking about renaming Texas to CalTex

The narrative of an “invasion of Californians”…even as far away as Portugal….is comically half-baked.

The reality is less hysterical; it’s simply a case of large numbers: California is home to 1 in every 8 Americans, as well as 1 in every 7 dollars of the nation’s GDP, so its actions are simply the most noticeable when larger trends occur.

The irony is that many of the same Americans who b**** and moan about Californians have a very different take on the negative impact that people from their own wealthy cities produce when they also choose to relocate to cheaper cities, counties, states, and countries; they just shrug their shoulders and justify their behavior as doing what’s best for themselves.

You said many times that the turning of the home price tide would be slow.

It proceeds much slower than the great molasses flood of 1919 that killed 21 people.

John H, no one can say how fast the fall in prices will continue or if there will be a fall in all cities.

The fact is that housing prices are ridiculously high, not only in the United States, but everywhere in the world!

There isn’t going to be a fall in numerical terms.

There already is in a bunch of cities.

I’m watching Feb, Mar, and April -> if we get MOM declines in the Spring across multiple a significant % of large metros, that will be he beginning. People have been trying to wait this out, but once it becomes clear declines are coming there will be a race to the door.

Redfin even recently released an article saying a lot of people who bought their houses in recent years (2020-2022) are listing them because they aren’t getting the price increases/appreciation they were anticipating. These are most likely vacant homes, investment properties, rental properties, airbnb’s. If prices start declining, instead of just stagnating they’ll be a lot more of these on the market.

More people? (Certainly an increase in certain locations… ie Columbus, austin) retirees not moving away? Low mortgage rates for long period, and lots of equity built up? Shift in demographics? Covid?

I saw a picture from the visual capitalist regarding population changes by state since 2020.

It was interesting, in that it was NOT a “zero sum.” The percentage declines (and numerical values) seemed to indicate a net increase, with the largest increases in Texas, Then Florida in terms of numbers.

This was to the tune of a few million people. Not associated commentary but I inferred that it must have been immigration related (certainly not births).

Very good report. I see the same things with my own eye. Washington D.C. has turned into a crime ridden disaster. The last 4 years have seen the entire RE market collapse. Add in the property values are getting hit by the massive government layoffs. There is trash, homeless, and graffeti all over the city. No one where I live in the close in suburbs ever goes into DC unless they have to. I have go there because I work there. And mostly the worst neighborhoods. This could turn around, as the new administration wants to turn the place around for the better.

Public safety in Washington DC has been severely underfunded for years.

Underfunded?

I wonder how much is lack of enforcement of basic laws by local govt. and courts ect.

It has been over ten years since I saw a cop in San Antonio handing out a traffic ticket. The last time I saw one, it was a motorcycle cop and I shook his hand to congratulate him. I see criminals driving 60 mph in residential neighborhoods. Of course our city councilman is a drunk driver so what do you expect?

There is a serious move to take home rule away from the District of Columbia, and go back to the way it was in 1973. Right now the city is un-governable. The crime is so out of control that is affecting everyone’s daily life. If current trends continue it will soon be named the murder capitol in the USA like it was in 1991 This can all be fixed but nothing will get done with the current people. Trump’s campaign promise is to fix Washington D.C. He will have to fire everyone and start all over. They need to do what Rudy Gulliani did in NYC in the 1990s.

Rudy who….???

During Giuliani’s administration, crime rates dropped in New York City.[93] The extent to which Giuliani deserves the credit is disputed.[96]

Wiki.

I too thought Giuliani deserved all the credit for cleaning up NYC; alas, I was mistaken. He in fact was fortunate to take office while three previous years had seen falling crime rates (partly due to Mayor Dinkins hiring 7,000 police officer and also coinciding with a national decline), and of course having the good fortune in the person of Bill Bratton, a strong willed commissioner, to guide him along.

Houses will stay high until it becomes very clear that the gov’t is out of the business of bailing out asset holders.

The fed should have never gotten involved in the mortgage market. They’ve essentially stolen the American dream from future generations. Personally, I think it was one of the big reasons the election went the way it did. Not affording shelter is a pretty big problem for people.

“ Personally, I think it was one of the big reasons the election went the way it did”

That would definitely be ironic, considering that it was Trump who “keelhauled” Powell regularly when the fed tried to allow rates to go up back around 2017.

More or less agree with you on the other stuff, BTW

@Just dropping by:

Don’t think people care who is really at fault. They just look to who is in charge when things went sideways. In this case, it was Biden. He got booted for inflation.

“If the American people ever allow private banks to control the issue of their currency first by inflation then by deflation the banks and corporations that will grow up around them will deprive the people of all property until their children wake up homeless on the continent their Fathers conquered… I believe that banking institutions are more dangerous to our liberties than standing armies… The issuing power should be taken from the banks and restored to the people to whom it properly belongs.” – Thomas Jefferson

We gettin’ close yet?

I think the image of that man beating the crap out of women in the Paris Olympics for a gold medal in boxing was the death of DEI, and a big part of the election results.

Hi Wolf,

Great graphs.

Possible typo in the title: ‘ Jan 2024 ‘

Best regards from a persistently cold and damp England!

Can’t change that anymore. Article got picked up by various Android properties that linked it shortly after I published it last night, and it’s getting huge traffic, and if I change the title, that traffic fizzles. Some mistakes you just gotta live with and embrace.

Wolf,

You can post a second article identical but with correct title. That way you get old traffic, and new.

Jeff

I’m going to correct the title (but not the URL) after the traffic dies down. The internet algos are pretty finicky in my experience. But it’s confusing, and eventually I’ll need to change it.

Posting the same content twice is a total no-no for the internet algos. They hate that.

It’s because people want to go back to Jan 2024 and have a year off from this shit show.

Unrelated to the story, sorry…

Reading and seeing alarming/interesting stories and graphs about Gold, monetization of the asset side, etc.

Yours being a most trusted source I hope to read your take soon.

Yeah they say “A U, you look dumb”

Just need the Vegas market to hold for another 60 days as our last portfolio property is heading to the market in the next few weeks.

I’m going to play devil’s advocate here. Just because something has gone up in price, doesnt mean it’s in a bubble and is destined to crash.

Take Dallas and some other markets. 190% increase over 24 years is only 2.7% per year compounded annually – 7.9% non compounded. Average inflation during that period was 2.5% per year or 83% total.

Stock prices have gone up 565% and gold 400% during the same period! So which is in a bubble?

You’ll know when they pop…

Let’s simplify. Houses more than doubled in the last 5 years here in FL. Does that make any sense? No. It doesn’t. Will it give back those gains now that the QE firehose of liquidity that caused it is now in QT? Most likely. In fact, we’ve already started to see the declines. It’s a more transitory market than others, so what goes up quicker goes down quicker. The others will follow at their own pace.

re: “so what goes up quicker goes down quicker.”

Unless the FED tightens reserve balances, there is limited downward price flexibility in the economy.

People like yourself, blinded by selfish, delusional greed, can’t see bubbles until after they pop and wipe you out to the point of suicidal ideation. Normals, able to rationally think things through, look at prices and easily conclude that it’s the most obvious bubble in history.

“By hindsight, it is a fairly simple task to identify the handwriting on the wall indicating the nature of this “hothouse prosperity”: overextended and illiquid credit structures, overgrown production capacities and inventories, nonsustainable [sic] yet rigid commodity prices and wage rates, extraordinary speculative “orgies,” including cold-blooded mischiefs of rapacious and financially powerful operators. It is difficult to comprehend the apparent lack of insight, and foresight, displayed by a majority of contemporaries in all walks of life, their ignoring the signals that should have served as warnings.”

—Malchior Palyi, The Twilight of Gold, 1972

That said recognizing the obvious signs of a speculative “bubble” is a simpler task than accurately predicting the price peak or ensuing trough.

Landlords on one side are/have been saying, “The crash is just around the corner, keep renting!” and realtors on the other side saying “buy now or be priced out forever, it’s only going to keep going up”. Realtors have been right for the past 15 years.

Where is it going? If there is a can’t-lose asset, money will pile into that asset and there will be a bubble in that asset. If the government seeks to reinforce that thought, through strategic interventions in those asset markets, then it keeps going up.

Stocks (and tulip bulbs) serve one purpose for the vast majority of holders – to generate more currency. If that goes away, there’s no reason to hold them. Houses however, fill an essential human need – shelter – in addition to being cant-lose assets. So the situation becomes more murky.

They talk about “entrenched inflation expectations” – inflation expectations in housing are about as entrenched as can be. From like 1970 and beyond, the Boomers think housing only goes up. Human psychology determines price trajectory because humans value things.

IF there is a large volume of houses being held solely as investments, and housing prices flatten, they could start coming on the market and push down prices. IF immigration declines, that could put downward pressure on prices (but there are more than a few locales with declining populations and rising house prices – see Baltimore). IF mortgage rates stay at current levels, that could suppress price appreciation and thus the desire to hold onto houses. If there is a recession and my first speculation about houses held solely as investments, that could be a perfect storm brewing.

But, on the other side, the government has demonstrated its commitment to keeping house prices boosted.

Inflation is Player 3 which suppresses the quick jump to lower interest rates. BUT government loves low interest or zero interest rates, as does business. They have a large seat at the table.

If you look at the Case-Shiller index going back to the 40s, there was a huge surge after WWII and then prices stayed stable for 15 years until they resumed their upward trajectory after the government started intervening again when Freddie Mac was created (Fannie in 1938). And note, that’s an index, not actual prices. Actual prices probably* had a gentle increase during that era.

tl;dr: Perfect storm of large number of investment houses held off the market, stable interest rates and recession could provoke a pronounced slide in house prices; but government has demonstrated it would push down rates and other interventions; inflation is a wild card; government and business loves free money.

That’s my free, often wrong, Internet opinion. YMMV.

I think you have to look at what drove the increase in prices, and whether or not it will continue.

With housing, I think it’s pretty much a no-brainer that decreasing rates over the last 40 years have driven price increases.

The question is, what would be the next catalyst for pricing increases/decreases?

Will the mentality that property ownership is such a good investment (for a substantial percentage of the population) change, either up or down? You know, stuff like that.

Seems like you’d have to evaluate the situation in its current context, and try to understand how we got here before you can decide for yourself with a bubble or not.

Buddy, a 190% increase = almost triple in value. 2.7% compounded annually over 24 years is only a 1.9x increase, not 2.9x… Look at how much inflation has been according to the govt in that time frame and look at how much the median household income has increased and you’ll pop like a bubble.

Math error methinks. 190% increase is about 4.5% per year for a 24 year period. The new price is 2.9x of the original.

“So which is in a bubble?”

All of the above.

And on top of that, existing houses depreciated significantly over that span, while new houses

have recently been built smaller and on smaller plots.

Totally agree.

Inflation and average capital or investment return have to be taken into consideration

Dallas doesn’t sound like a terrible bubble then…. other cities are not lucky. I think the historical normal was 2.5%-3% for housing appreciation. Which once one factors in home owners insurance and property taxes, repair and maintenance, updates, etc it was actually considered a bad financial investment. That you buy a home as a place to live and for financial security, but single family homes weren’t an investment.

I feel that calling the housing bubble splendid is not showing much concern for people who are looking for a home. Of course there will be people who make out like bandits when they go to sell their house, but overall, I think that housing prices exploding as they did is very bad for the country in many ways.

If you don’t get the subtext of Wolf’s post, you might be irony deficient.

“irony deficient” 🤣 gonna steal that from someday

There are only 2 ways that seem likely for this to play out… Either prices drop significantly or prices stay flat while the dollar inflates to meet those prices.

I am on the record here claiming to expect this to play out like it did in the 1990s. Down a little, then flat prices meet warm inflation. So far, my prediction is looking good. As a whole, these markets are mostly flat after a dip a few years back. National median pricing dropped a bit, then flattened out as well. It’s early 90s v2.0

The DIDMCA of March 31st, 1980, caused the S&L crisis. The transaction’s velocity of funds fell into negative territory for the 1st time since the GD.

Greenspan then lowered required reserves by 40 percent causing the boom in housing. By 1995 reserves ceased to be binding on the upside.

Sources of mortgage funds shifted from the subsidized rates formally provided by the small saver to “bond-backed” sources which reflecting the interest rates prevailing in the longer-dated loan-funds markets.

One of the principal purposes of this Act was to provide the housing industry with a reliable source of funds. Instead, that was achieved through various governmental & quasi-governmental corporations as predicted. The role of the S&Ls in housing finance diminished significantly. Securitization, originate to distribute, became the new trend.

“The DIDMCA of March 31st, 1980, caused the S&L crisis.”

The S&L crisis was caused by widespread FRAUD, and hundreds of executives went to jail over it. I wrote my grad school accounting thesis on one of them before the scandal blew up.

WR is absolutely correct re ’80s S&L debacle.

Kinda sorta looked similar to what appears to be developing these days, with the Bush family heavily involved and then left out of the purge.

Don’t remember if WE the People, in this case we who had gotten mortgages from the corrupt S&Ls were hurt or not.

Maybe Wolf can complete the concept, especially in light of what’s happening right now with the ”coins” etc.

The DICMCA turned the nonbanks into banks. The S&L’s had to act like banks in order to survive. The liquidity problems of the Savings and Loans became acute largely because of sharply rising interest rates in the 70’s and early 80’s combined with their longtime competitive need to “borrow short and lend long”. This in turn led many S&L managements to accept “brokered” loans. Further compounding the problem was the action of Congress and State legislators, under the rubric of competition, allowing S&Ls to engage in almost any type of lending, from direct developer financing to the right to purchase “junk” bonds. Unfortunately, many S&L managements, responding to apparent economic necessity, or because of greed and/or incompetence, have engaged in reckless financial practices.

The fraud was so bad that one federal official described it as “fiduciary pornography.” Google the “I-30 condo scandal” and read what comes up, or “Vernon Savings”.

Of course, as it turns out, these people were just country bumpkins in the world of fraud. The ones who are still alive have to be thinking that they went to jail, while fraudsters on a scale they couldn’t have imagined then retired rich.

I read the book:

“The Daisy Chain: How Borrowed Millions Sank a Texas S&L”

in the early 90’s when it came out, great page turner for anyone that wants to learn about the 80’s S&L crisis.

Is your thesis available on line?

There was no internet back then (ca. 1985) the way we know it today. Nothing was “online.” People didn’t even know what that meant other then on a telephone, LOL. I forget how good we have it today with everything on the internet at our fingertips.

I think we’ll find out this year.

1. People holding out for rates cuts and housing to take off again are realizing it’s not going to happen and listing (redfin recently said this)

2. A lot people who moved during the pandemic that are using their former properties as airbnb’s and rental properties are likely going to have to decide if they want to become permanent landlords/investors from a tax standpoint and lose their $250k/$500k capital gains exclusion

3. The last of the FOMO buyers already bought, so there’s not a lot of demand

4. Lots of new housing inventory

5. Combined for sale housing inventory (new and pre-owned) up significantly in many major metros

5. Lots of new apts/rental inventory

6. Rental prices significantly below the price of owning and dropping in some major metros.

7. Tech is still suffering which impacts a lot of the HCOL cities

8. Impact of fed job cuts, and spending cuts that will flow to NGO’s and corporations

9. Tourism returning to normal pre-pandemic levels

I think if we see month over month declines in a lot of major metros this Spring Feb/Mar/Apr/May it’s going down. If it stays flat, or up, then I agree the downturn might never come without a significant recession.

The only thing I think that is a positive for housing at the moment is the stock market is at all time highs.

Gee… what else would you expect from a pseudo-socialized government influenced housing market? Everything the government touches eventually turns to sh$t.

Yes, I’ve often said that about the FDA and FAA.

Yes, it would be much better to let pilots decide when and where to land, and for food and pharmaceutical companies to put whatever they want into their products without the onerous burden of having to label them, let alone testing for safety. Freedom!

Yeah, this whole “the government is always and everywhere incompetent and useless” trope is profoundly ignorant.

Perhaps Somalia is more congenial for these types?

The cliche “Somalia” trope in response to government criticism is ignorant and racist.

Somalia doesn’t have no state, they have different factions fighting for control of the state. And this line of reasoning implies Somalis are incapable of statehood because they are backwards and uncivilized.

Ok but now the government is run by a pack of 5 year olds who ate bags of Cheetos, too much pop and are rebelling because mommy wants them to nap.

What your graphs show is that apart from Austin, TX and Washington D.C., is that there has been no price correction. TPTB want this, bcuz if they can elevate and support this fairy tale fallacy, the citizens will not see the avalanching economy. This is the largest bubble and FRAUD in all of history.

Easy money pulled out of a hat has replaced American production and innovation. Housing and cryptocurrencies.

There always seems to be a general vibe that things will return to some idolized state that really never existed the way we imagined. Sure, I remember a time with virtually no homelessness in comparison to today, and that things like housing, health care and education might get you a little in debt but for many were still in reach (but of course out of each for many).

Seems like we rationalize a broken system by pointing out breaks like CDOs for the real estate crash, or COVID, or a myriad of other things. Perhaps we have reached a point where systemic issues can’t be ignored and hope the promise of the next election cycle will fix them!

Nah. Pull yourself up by your bootstraps(whatever that means) and everything will be fine and equitable.

Not sure when there were not unhoused people Glen???

Far as I have read, and admittedly I haven’t read everything on the subject, there have always been some people without ”proper housing”…

It is clear that today’s unhoused folx are a TON more visible, but I can remember the days when ”hobos” were around, especially in FL in the winter, sometimes marking the curb or sidewalk with signs indicating homeowners willing to give food, or the total opposite.

Allsop gives a fairly thorough report on this in his 1967 book, ”Hard Traveling” that is basically a history of the hobo in USA, but ”migrant workers” even if temporarily housed when needed for harvests, etc., have been around for ever.

I just had a ‘Eureka moment’ – if your ordinary abode (or fixer upper in many places in California) runs a cool $One Million, $20 Big Macs are a bargain! $10 eggs – a giveaway. $10/gallon gas – almost as cheap as water! When homes are a million or two, what’s a lousy hundred?

Ha! I have a new appreciation for how cheap my everyday necessities are. I’m a new man. Excuse me while I go look for my Monopoly set.

Eggs are actually $3 a dozen in Australia right now.

And no you can’t buy the country.

The vast majority of contractors and even Federal workers that will be laid off and lose their jobs as a result of DOGE live in Northern Virginia. So I see a big hit there due to this factor. Add in the RTO mandate and you’ve got a double wammy. Many of those N VA commuters come in from the Exurbs, which is very long commute. Their WFH boondoggle is coming to an end for even those who keep their jobs. A third factor is the pandemic hangover where vast numbers of commuters abandoned public transportation, leaving the roads congested as hell. All and all I see Washington DC, actually bottoming out as it just can get any worse than it is already. I see the big hit in Real Estate values in the far out suburb of N VA and Maryland, and Washington D.C. holding it’s own. The building of a new stadium to replace RFK stadium is a done deal and will lead to a boom in a large southeast section of the city.

“The whole house smells of shaving lotion.”

“Figure it out. Work a lifetime to pay off our house, you finally own it. There’s nobody to live in it.” – Death of a Salesman

Phoenix and Vegas:not seeing anything significant there when you look at your chart. Nothing like 2008. Not even close to bubble bursting it seems.

John H.-

The “economist’s trap,” the top never looks like the top before “the top is in.”

Much like calling the recession — only conclusive with benefit of hindsight.

Vegas has a gazillion new houses being built. That market won’t hold up much longer.

Same for Pheonix. I could not understand the allure of high real estate price of cities which has got ample large swathe of land to build and thousands of new homes in the pipeline.

“I could not understand the allure of high real estate price of cities which has got ample large swathe of land to build and thousands of new homes in the pipeline.”

My thoughts exactly.

I genuinely think all these new builder incentives / rate buydown etc. are distorting the market.

Will there be enough water to sustain substantial new development in some of these drier places?

Wow! Still a long way to drop! Given the choice between a deflationary depression and an inflationary depression, I’ll take the former.

I said this a long time ago, and I still see this unfolding some day in the not too distant future…there will come a point where it will be difficult to GIVE away houses. Some people would say this is an absolute insane statement, but when millions are laid off due to AI and unemployment, and with overburdening taxes and home insurance and natural disasters, yes, I believe homes will be very cheap. A home will become a burden for many. High costs of energy and food will make owning a home a dream of the past. And if your home becomes worth $5 Million to $10 Million or more, it is meaningless when $10 Million will not buy a month’s worth of groceries. Demographic changes and a declining birth rate will also contribute to the housing market collapse. Finding qualified workers to service and repair homes will also be a major problem. Not a rosy picture.

“there will come a point where it will be difficult to GIVE away houses”

Correct me if I’m wrong, but I believe this has been the case in Japan recently.

Yes that is true in many places in Japan, and South Korea is not far behind. I saw a video recently that showed the birth rate is 0.68 children per woman, way far below the replacement rate.

This is a crisis level number that will prove to be disastrous on multiple levels. This is an extinction level birth rate.

It’s eerie how closely the Austin trend line looks like the Fed’s Total Assets graph that you publish every now and again (example https://wolfstreet.com/2025/02/06/fed-balance-sheet-qt-42-billion-in-january-2-15-trillion-from-peak-to-6-81-trillion-lowest-since-may-2020-bye-bye-btfp/)

Criminals drive up real estate in a substantial way. Why isn’t anyone mentioning the huge role money laundering plays in US real estate, by citizens and foreign interests alike? It needs to be front-page everywhere. It isn’t just California, New York, and Miami. I come across records of suspicious shell companies in rural areas and know it’s just the tip of the iceberg.

Not that the American people care about real corruption, electing real estate shills who are national security risks with all their foreign money ties.

@MountainTime there has always been “some” money laundring in real estate (like when 360 Mountain Home Road in Woodside down the Peninsula from me sold for ~$100 million “above market” over ten years ago) but it is not “substantial”. I have been keeping track of EVERY apartment sale around my properties and EVERY home and cabin sale hear my home and cabin for “decades” and I have never seen (or heard of) even one that had a hint of “money laundering” (in the cases where I don’t personally know the buyers and sellers someone I know almost always knows them).

>sold for ~$100 million “above market”

Ironically this is hugely beneficial for whichever municipality gets to collect the property tax. Unless the local tax collector is in on it…

Why Austin and San Antonio fell more than other markets when the burden of 7% is same for all.

Perhaps property tax and near market estimates for property taxes in these markets.

The main problem to correct in housing is that homes are not affordable for the average joe or working-class household. That’s where everything starts. Any American should be able to buy a 2bed/1 bath home if he/she is willing to work 40hrs/wk. Anytime there is a monopoly in something, the least of these gets thrown over the bridge. D.R. Horton, KB Home, Lennar Corp, PulteGroup etc have deleted the 2bed/1 bath home so that has eliminated the traditional building of equity as we have known it in the USA. Even at 7% interest, a $100k 2bed/1 bath home with 30yr conventional, would be under $700/mo and this affordability would stop people from giving up on life and becoming the homeless beggar that we see such much today. We need an influx of small builders who are willing to build subdivisions with small homes like what was done after WW2. The billionaires and multi-millionaires are playing a winner take all game so if the middle-class aren’t willing to fight back by becoming the small builders, then they will be next as the working-class today are basically living in a fiefdom with 70% of their money going to landlords.

Average,while I like your idea those tract homes built after WW2 were constructed in a different world.With the international building code/insane permitting costs/environmental reports/the list is endless the costs before construction and then meeting new codes makes this at moment not happening(unfortunately).

I saw as a carpenter/licensed builder with many useless certs we will really have to change all levels of govt. to even come close to this,a worthwhile fight.

We could do this while building homes safer and less impact but the will needs to be there,literally a revolution at least idea wise/thinking ect.

I understand certain places have a block on what kinda homes can be built. Of course municipalities want more expensive homes that pay greater taxes but that’s what the vote is for. If your city council or county commissioners are adverse to the 2bed/1bath house, vote those suckers out. Even if I lived in a mansion, it still should be legal for someone to build a small house that fits them somewhere in the city/county. Gotta get back to the basics & people gotta realize everything isn’t about amenities and living in excess. Sometimes you need just the basics before you have the savings or equity to move up. All these REITs who don’t pay corporate tax want to keep people renting from them of course until someone loses a job and can’t pay the high rent, now you have to put your stuff in their other REITs like Extra Storage or Life Storage. Yep, those are non-corporate tax paying REITs as well

Paragraphs.

If you think homes are too expensive, try building something that you want new or do a real remodel. Not the tv bull, but a real update.

Average homes in my area go for around 400k and are few and far between One went quick for 225k.

The new owner wanted a full update that includes what you don’t see. Best offer was near 300k.

Now it is listed again.

Services inflation.

We’ve seen that here. On TV, the RE agent casually throws out the 10K estimate for a new kitchen when asked. In reality, labor and a RE agent living in the past for materials, bumps that up to close to 100K.

Even the handymen are asking $50-100 per hour. That’s 100-200k per year full time.

$100 K in many areas of California is almost poverty level wages. After taxes, you are treading water to stay afloat. With the cost of housing, energy and food, there’s very little left over.

Howdy Folks. Good Deal. Lone Wolf charts show the RE Bubble hissing down its merry way. How long before Govern ment decides to prop up the RE Market AGAIN??? Place your bets

1. No $ down loans

2. No income verification loans

3. If you like your 3 % Mortgage, you can keep it and move it to your next home. No questions asked. Just make sure you check the proper box.

How’s this for housing bubble..

I was on MaeketWatch earlier and saw a pic of a new home with the street sign. I looked it up..

Here’s the “lovely” home that came up…it’s a McMansion on a tiny lot for $1.4 Million. Brand new. Tiny lots are awful-no privacy.

I punched in some numbers and found the monthly payment to be approx $8570 per month, if 20% is put down. I estimated tax and insurance. What a whopper of a payment!

Anyone, anyone…Bueller?

I refuse to agree with the way inflation is being measured. The most of my expenses is for housing. And the housing is up at least 100% pretty much everywhere. I can pay 10, 20 or even 50 more percent for eggs or bread. I can not pay 400K instead 200K for a home. Or 4K instead 2K for rent. So the biggest problem is the biggest amount of the inflation – the housing, that is what causes the inflation, that is what they have to fix with measures, not to tell me inflation is 2 percent, we will cut the rates 0.25, this is bullshit.

“the housing, that is what causes the inflation”

Most of the inflation is in services.

@ShortTLT wrote:

“Most of the inflation is in services.”

I spent $565 to have a drain cleared last week. With more and more baby boomer blue collar workers retireing each year the cost of my repair and maintenance “services” is going up way faster than my rents.

AI – hopefully $565 got you more than just the guy snaking the drain and showing you his buttcrack.

Services inflation is why I now do all my own car repairs instead of going to a shop. And I’m trying to learn the DIY home repair stuff too…

P.s. recently unclogged my shower drain with a combination of boiling water and a sink drain plunger. I refuse to use draino on my pipes.

To ApartmentInvestor and Short TLT –

The butt crack exhibition is listed on the bill as item # 4

4) Butt Crack Ex………..….NAC

No Additional Charge.

The best things in life…. 🤓

Wolf, I don’t see it as a big drop. For me drop is 30% or 50%.

it took 5-6 years last time to get to the 50% drop that some markets saw. Tulsa was in a housing depression for decades that started in the mid-1980s and lasted until about five or so years ago. And now prices have suddenly doubled. Every market dances to its own drummer, but it’s a slow dance.

100%?

Metro Denver will continue to see the California and Texas gold rush buyers moving in groves. It’s like a war of license plates and bad driving tactics with just a few inches of snow falling. The building has never stopped outside the beltway, the Eastern Plains turns into suburban sprawl. The land grab thirst will reach full peak once the new location of the Denver Broncos Stadium is decided by the billionaire Walton family. The spring selling season is upon us, with the last snow expected around Mother’s Day, will be interested to see what the market does.

Wolf, if there’s a sea change, and people are ordered RTO, especially in SF, do you think it might stay at this plateau and then keep moving up? I’m agreeing with Ram above, that looks like a pause, not a crash. You are right to mention that it takes years, like Tulsa, but Tulsa is not SF. (That said, I remember driving through Tulsa when I was a kid, and there was some nice housing stock. Charming homes. And folks in Tulsa are good people, and kind.) Note to all: I’m super conservative (and live in Berkeley), but don’t believe very much of the negative stuff you read about SF. 80% of the city is gorgeous. Don’t be a tourist who stays in a hotel anywhere close to Union Square. Go to the Richmond; go to the Sunset, Noe Valley, Cole Valley, Bernal Heights, Cow Hollow, ad infinitum.

“… especially in SF, do you think it might stay at this plateau and then keep moving up? ”

Plateau??? 🤣❤️

City of San Francisco, Plateau in condo prices… note that the majority of sales in SF are condos, so this is the condo plateau, with prices back where they’d been years ago, when Obama was still President.

And the plateau of single-family prices.

Oh, and the condo plateau in Oakland:

More details here on other cities too:

https://wolfstreet.com/2025/01/19/the-big-cities-with-the-biggest-price-declines-of-single-family-houses-or-condos-from-their-peaks-from-9-to-21/

I keep seeing Cincinnati and Louisville pop up in ICE and AEI reports as having high home price appreciation rates. Will they qualify for inclusion if they $300k or are the metros monitored set?