Why the Fed vigorously backpedaled on further rate cuts and pivoted to wait-and-see: Long-term interest rates matter.

By Wolf Richter for WOLF STREET.

Fed Chair Powell, at his testimony before the Senate Committee on Banking, Housing, and Urban Affairs today, included his nearly standard line about longer-term inflation expectations being “well anchored, as reflected in a broad range of surveys of households, businesses, and forecasters, as well as measures from financial markets.” The first three are survey-based – what households, businesses, and forecasters see coming at them. The last is based on trading results in the Treasury market, what the Treasury market sees coming at it. It’s the bond market talking here, and the bond market is getting worried again about inflation.

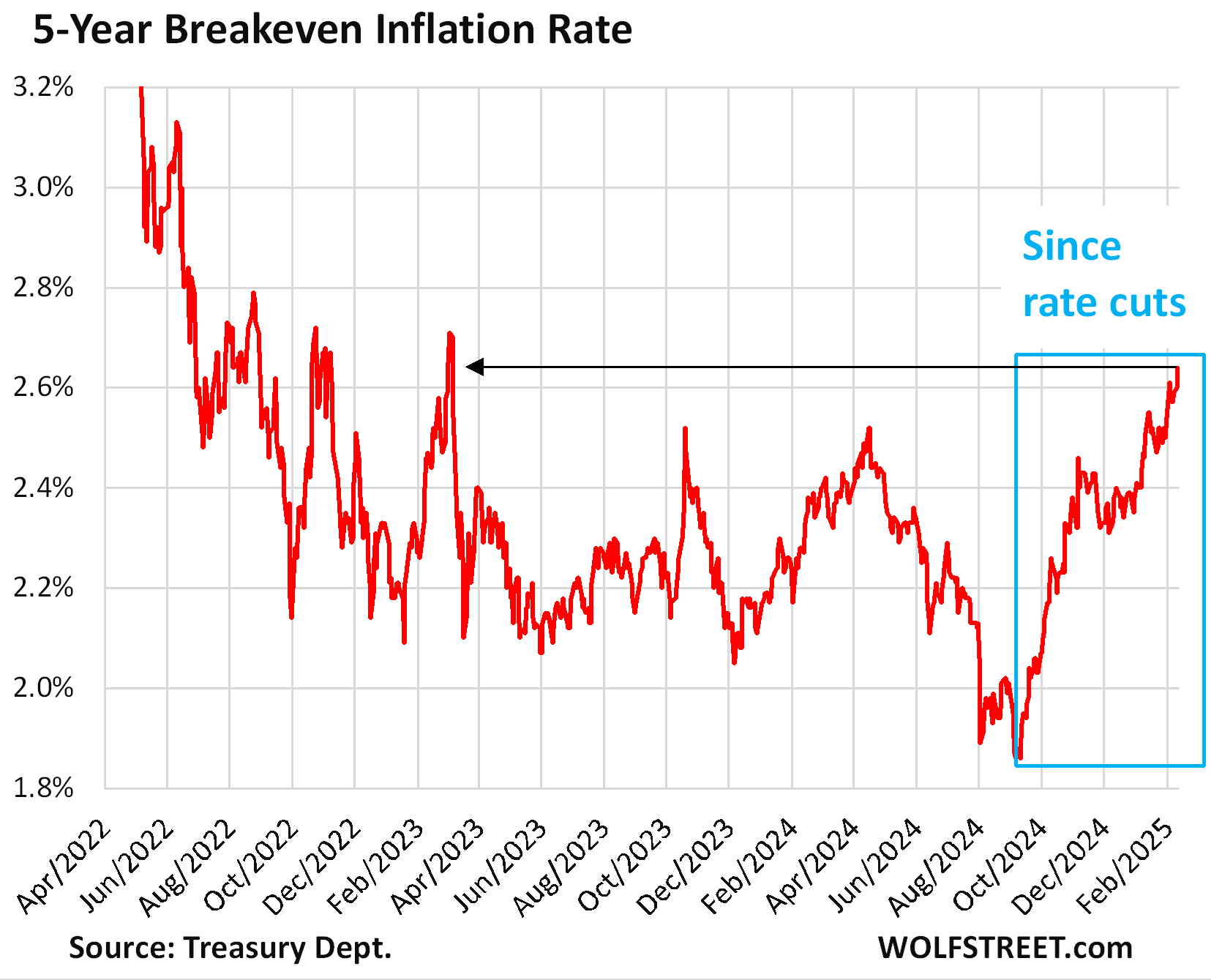

The 5-year breakeven inflation rate rose to 2.64% today, the highest since March 2023, having shot up by 78 basis points since just before the Fed’s September rate cut. This measure (5-year Treasury yield minus the 5-year Treasury Inflation Indexed Real Yield) shows what the bond market saw today as the average inflation rate over the next five years.

The Fed has cut by 100 basis points, while this measure of market-based inflation expectations for average inflation over the next five years has shot up by 78 basis points. It has become “unanchored,” as one might say to needle Powell during the FOMC press conference:

A Fed that is lax about inflation scares the bond market once inflation starts rumbling. And the Fed has seen that reaction from the bond market too – including the surge of longer-term yields, such as the 10-year Treasury yield, since the beginning of the rate cuts – which is why it has walked back any talk of further rate cuts and instead has pivoted into wait-and-see mode to not unnerve the bond market further.

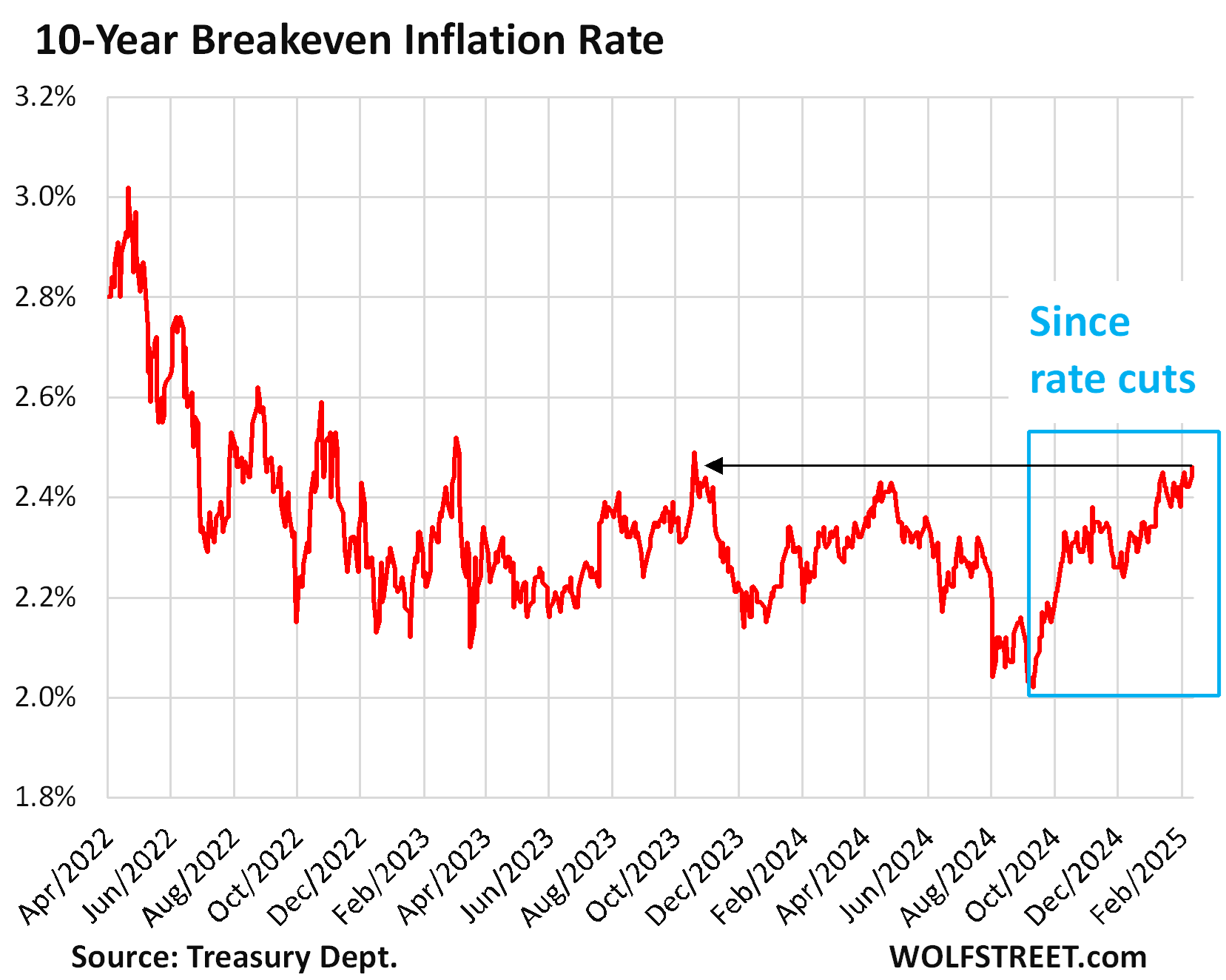

The 10-year breakeven inflation rate (10-year Treasury yield minus the 10-year Treasury Inflation Indexed Real Yield) is a little more sanguine but is also coming unanchored. This measure of what the bond market saw today as the average inflation rate over the next 10 years rose to 2.46%, the highest since October 19, 2023, and before that day the highest since March 2023. It shot up by 44 basis points since just before the Fed’s September rate cut.

The rate cuts unnerved the bond market. The bond market saw that inflation wasn’t quite done with yet when the Fed was cutting rates just as inflation was starting to re-accelerate. This infused the bond market – and not just the bond market – with concerns that the Fed would be more tolerant about inflation going forward, along with signs of fear that inflation would on average be higher over the next five years in particular.

This jump in inflation expectations by the markets, along with the surge of the 10-year yield following the rate cuts, likely triggered the energetic backpedaling by the Fed on further rate cuts. It is now in official wait-and-see mode. Powell and the other Fed governors now keep hammering home the point that they can be “patient” with their rate cuts.

The bias today is still for cuts, not hikes. Inflation would have to make larger and more sustained moves higher for the Fed to switch the bias to rate hikes.

But a bond market freakout over accelerating inflation and a lax Fed – resulting in higher long-term yields that really matter for the economy – would nudge the Fed to switch its bias to rate hikes again. To keep long-term yields from rising too much, the Fed will need to show the bond market that it’s serious about inflation, and that it will crack down again if inflation re-accelerates substantially.

That’s the irony: The Fed might have to hike short-term rates again to make sure long-term interest rates remain “moderate” – paying attention to the third part of its mandate, to conduct monetary policy “so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.” The mandate is silent about the Fed’s short-term policy rates. It’s “long-term interest rates” that are in the mandate, and the way to get there is to keep inflation in check.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thank you for another clear explanation of what is happining currently with the bond market and the Fed.

Yes, I appreciate the clear explanation.

“To keep long-term yields from rising too much, the Fed will need to show the bond market that it’s serious about inflation”

I wish there were a way to send this article to Powell.

He said that today and before. Hence the wait-and-see.

But what does serious about inflation look like?

Wait & see, rate cuts, rate hikes???

Wait & see sounds like “transitory”

Rate cuts sound just as crazy today as they did back in Nov & Dec

Rate hikes is where the bond market expects this to go, so how long does wait & see take?

Nothing the Fed has done since last Sept has made any sense.

All inflation measures are still a LOT lower than the Fed’s policy rates. There is no reason for the Fed to hike now. Inflation rates can rise by a full percentage point, and they’d still be below the Fed’s policy rates. The Fed is at 4.33%! CPI yoy = 2.9%. What’s your problem?

Some of us just like the chaos and spectacle, I think. Writing comments on blogs demanding the Fed hike rates has its own jouissance.

I have heard that interest rates above inflation are restrictive and rates below are expansionary… But where, mathematically, does this come from? Or is it just “past experience”?

This succinct reply, Wolf, is what we love about your work. Thank you. Sums it all up so perfectly

According to the BoLS CPI has been above the Feds 2% target since Jan 2021. The was a substancial decrease in CPI in 2022, but CPI has remained about 50% higher than the Feds target. For the last 6 months CPI has been trending up. The target rates are indeed above CPI, but not enough to finally drive CPI back to target. By all accounts the economy and labor markets are holding their own, and yet the last moves from the Fed were rate cuts.

“The Fed is at 4.33%! CPI yoy = 2.9%.”

That was through yesterday. As of this morning, CPI is 3.0%.

Nice job, inflation!

Hi Wolf, inflation measures are lower than the Fed’s policy rates, got it, that’s clear. But shouldn’t the gap and the rate of change between the Fed’s inflation measure and its inflation target be more meaningful? I mean, the inflation measure is around 3%, while the long-term target is 2%, and the gap seems to be widening. Wouldn’t this suggest that policy rates might not be high enough?

Wait, when inflation peaked @ 9.06% in 2022, the Effective FFR was 1.21%. That’s a much larger gap than what it is today. Granted, the Fed had just gotten out of their “transitory” syndrome, but my problem is that the Fed seems to be getting into another “transitory” headspace.

Granted, this is conjecture which you typically label as BS, but I wonder if the Fed cut in Nov & Dec, IN PART (but of course not only), because they knew Trump would come into office screaming for the Fed to lower interest rates.

Nobody should be surprised that CPI has risen from 2.4% to 3% in a span of 5 months. At this pace, we’re looking at 3.6% inflation by June. 3.6% is a long way from 9%, but it’s just around the corner from 4.33%.

Again, the Fed clearly is slow poking a decision. Why? Trump is going to go ballistic, and them holding rates down helps Treasury borrowing.

I guess my question is this: Does anyone expect this to end well?

” when inflation peaked @ 9.06% in 2022, the Effective FFR was 1.21%.”

In January 2022 and for months after that, I called the Fed “the most reckless Fed ever.” Google it, LOL

Obviously, if CPI gets to 5%-plus and the Fed is still at 4.33%, we’re all going to start screaming here, and I’m going to take “reckless” out of my drawer again and start flinging it around.

I think current rates are far less restrictive than the Fed believes. The relevant metric is often NOT nominal yield vs. inflation rate.

For instance, for buy-now-vs-buy-later decisions, after-tax interest rates matter, not nominal rates. If I know I’m going to need something, I might buy it later if I think my savings will earn some money, but if that something is going to cost more and my savings aren’t earning enough, I’m better off buying it now. You might say that at a 4-ish% return on a T-bill vs. 3-ish inflation, I’m better off saving for now, but the reality is that after taxes, for many people in higher brackets, that T-bill (or the equivalent muni bond) pays less than inflation.

So for a large slice of the consumer economy, after-tax yields are below inflation, and it makes more sense to spend now rather than saving. This accelerates inflation.

There are many other similar mechanisms that apply to other parts of the economy. Bottom line is that rates are too low to slow inflation.

One could also argue that a higher term or risk premium is needed given the rampant policy uncertainties being generated by both the new administration and the old guard resistance.

“I think current rates are far less restrictive than the Fed believes.”

Among Fed governors there is a huge disagreement about how restrictive rates are currently. Some believe that we’re at or near neutral already, meaning they’re no longer restrictive, including Cleveland Fed president Hammack who said yesterday: “we may be at or close to a neutral setting already.” She may be right. Her speech.

But others believe, incredibly, that we’re still pretty far from neutral. Powell keeps trying to gingerly walk the middle ground between these two camps.

I can tell you right now my groceries cost more my insurance is more everything is. No need to wait and see. The amount of borrowing by consumers and companies has gone up so the rate hikes were never restrictive

Neal white

So you would prefer that 10 million OTHER people — not you — lose their jobs so that YOUR food prices and insurance costs rise more slowly?

I think the fed should increase rates to near that of the 1970s to curb inflation and insane housing prices and growing consumer debt. If bumped to 7-9% it will help to ease housing prices, it will also force banks to make better decisions for loans, it will reduce consumer debt spending and will balance inflation over a relatively short period (about a decade).

Just my opinion. I have no issues at all paying 14% on a home, but houses being an average of almost half a million is pushing first time home buyers out and increasing the age of first time home buyers. Lower rates are also encouraging real estate portfolios for the wealthy, where with higher rates they are less likely to buy large swaths of homes and focus on cash purchases for homes they believe will turn a profit. Nobody who bought a house 20 years ago for 65k should be able to sell it for half a mil plus. Homes should average between 2-5% increase in appreciation a year, meaning that 65k home should now be 98k to 130k after 20 years.

I’ve seen homes bought by people in the 1970s when rates were crazy high and the house was only 60-80k and now they want 500-700k and in some areas as crazy and 1 to 2 million. With inflation, wage increase over time, and appreciation it makes it near impossible for another family with comparable income to the original owner to get in the home. We have millions of homes unoccupied, 15 million to be closer to exact, and millions who want homes but can’t afford it. For average cost home, 414k, a family has to make roughly 125k, and have a down payment of over 80k for conventional. Most Americans don’t even have 10k saved and the average income for the american household is 80k. So many are just completely priced out.

Fed need to raise rates. And people need to stop thinking their 80k purchase 20 or 30 years ago is so special that they can become a millionaire off of it. Never before in American history has this been how housing was treated. The market is hyper inflated because of the poor choice to lower rates to almost nothing.

Just here waiting

So the Fed should kick 10 million Americans out of work by raising its policy rates to 7-9%, when CPI inflation is 3%, so that you can pay less for a house?

Americans are a funny bunch.

Powell understands. Now it’d be nice if Trump understood as well so he would stop trying to pressure the Fed to lower rates.

Dear Wolf….help me understand this please

If the saving rate (public plus private) is less than the deficit then shouldn’t the long term interest rate go up (or remain high).

Unless of course the world is generous enough to fund our deficits are low rates.

So assuming there is 2% (current) inflation but the world doesn’t fund our expenses then long term interest rates should still remain high.

Would that be reasonable to think? Or are there more variables at play.

The market drives long-term interest rates, not any particular equation or savings rate or whatever. The market consists of supply and demand. There is a LOT of supply from the deficit spending, but there is also a lot of demand from the US and globally, which is why the 10-year yield is only 4.5% and not 6%. Yield makes sure that there is always enough demand, that’s the job of yield, that’s what it does. If inflation is seen as higher in the future, demand will take that into account and will materialize only at a high enough a yield so these buyers are compensated for their inflation expectations, and so higher inflation expectations translate eventually into higher yields.

Gold near to $3,000/ounce. Pennies being taken out of circulation. Mtg rates up. Inflation doesn’t look like it’s going anywhere but up. Waiting for the bond vigilantees to come out of the woodwork.

re: “bond Vigilantees’.

If and when ‘they’ come out of the woodwork, what will they do? I have never really understood the phrase. Thanks.

Bond vigilantism is when major fund managers essentially boycott Treasuries – in principle due to out-of-control deficits. Lack of demand causes yields to go up a lot.

Theoretically the Fed wants to avoid this scenario.

@ShortTLT Nobody in finance does anything out of “principle”. They stop buying bonds because it does not make financial sense and they fear losing money. There are no principles involved. The whole phrase “bond vigilantes” is non-sensical.

ShortTLT:

You are onto it. Bond vigilantes are not a group, and they don’t convene. Bond vigilanty-ism manifests as a reduction in market demand for bonds. Less demand > lower price > higher yields.

Also, not just fund managers, but individuals, banks, corporations and governments spanning the globe.

Nemi5150:

The principle of protecting oneself from an anticipated market decline in the price of treasuries seems both sensible and principled to me. Having to do with property rights and individual volition.

It seems like a mistake to have lowered rates by so much over a short period of time. But who am I ??

Hindsight may show that it was perhaps not the ideal choice but it is unlikely to have been an “error”.

And that’s hindsight. It was certainly a valid choice based on the information at the time.

Survey based expectations haven’t exactly been “well anchored” lately either.

1-year UofMich expectations have spiked +1.7% since the rate cut.

And, as far as I can tell, the 5-year UofMich expectations have hit a 30-year high (excepting maybe a month or two in 2008)

But the UofMich survey just shows the political divide in the US, with Republican-leaning respondents seeing very little inflation and Democrat-leaning respondents seeing red-hot inflation. This totally flipped after the election. Before the election, it was the opposite. In the data, look at the political divisions of it. Just funny.

The New York Fed’s survey of inflation expectations yesterday wasn’t particularly hot (3.0% for 3 years, unchanged from prior month)

Wolf, I entirely concur with your observations but I have a couple of queries:

Real yields have remained remarkably well contained in the last few years despite breakevens threatening to break higher. Doesn’t unanchored inflation expectations suggest that real yields should be higher and rising?

I pay fairly close attention to 10 yr real yields vs 10 yr breakeven and recall past periods such as dot com when 10 yr real yields were 4% at a time when the deficit/debt levels were well contained and credit risk of treasuries was comparatively low.

I appreciate that demand for treasuries is keeping yields in check but given the above, the question is, why? Any thoughts?

“I appreciate that demand for treasuries is keeping yields in check but given the above, the question is, why? Any thoughts?”

Cleanest dirty shirt?

How many Japaneese investors are buying Treasuries instead of JGBs? Etc etc.

So it seems the Democrats are predicting inflation correctly? lol.

Another reason for the run-up in prices could be consumers pulling ahead demand before tariffs.

I spent tens of thousands of dollars on Asian-made shoes, electronics, and tires and immigrant-labor home improvements in December and January. Now I’m set for years in some categories of purchasing, and will be less vulnerable to the tariffs. But my spending is about to decrease dramatically.

I probably should have bought a car.

No.

Over the last 4 years, Republicans were most accurate predicting inflation rates for 2.5 yrs, while independents were best for the remaining 1.5 yrs. The poll is an expectation of inflation rate 1 year in the future so we don’t know which group is most accurate now.

Maybe the opposition party is typically more accurate?

Hard to envision any near or medium term situation where the demand for treasuries will go down enough to make long term yields rise significantly. Any event that might cause that would likely not be isolated to the US. Our political system also makes all of this impossible to predict given the pendulum nature where the only constant is lots of spending. The Fed is really just reactionary to the political machine.

I don’t think much would be needed. We have all the necessary drivers in progress right now:

1) Treasury can’t shift more of its debts into shorter duration (Yellen QE is over)

2) FED continuing QT (but they will definitely stop if 10y gets too high)

3) China further divesting

What would be needed as a counterweight is a recession / some trouble in the stock market.

Hide and watch!

But mostly hide.

There was no landing, soft or hard. So, rates are fine unless you are long on housing, hoping for personal wage inflation, or long on BTC/Big Tech.

Bitcoin is bound to rise just like gold. It is only trading as a “risk asset” because people don’t understand it. It’s an entropic store of value. You burn energy mining Satoshis and have cryptographic guarantees for that work done. It is symbiotic with our AI future.

Farts are energy spent. Energy spent doesn’t equate value. Proof work is done doesn’t equate value. This is beyond nonsense. People are welcome to invest in whatever they want. But trying to make it sound like logic, as if this is a universal truth is absurd.

Wow!

‘Cryptographic guarantees’?

‘Entropic store of value’?

You are being funny surely?

Cryptocurrency is Ponzi distilled and just like all Ponzi schemes, a deep recession would be it’s undoing.

Now where did I put those tulips? That’s where the ‘smart’ money is going!

Interest rates is a function that cause the amount of money to grow exponentially to infinity.

Those cryptocurrencies gaining value is tulip bulbs soaking up excess money supply. There is a story to the tulip mania, excessive money supply.

A deep recession may undo the “gains” in assets values, cryptocurrencies and others. Maybe even the value of fiat currencies backed by state actors. If not the exponential growt make fiat money worthless first.

I don’t pretend to understand crypto valuation, but crypto strikes me as more of a wish for a “money” backed by more than just the debt, taxing authority, and military prowess of one country. All liable to be temporary.

Perhaps James Grant is right when he yearns for a yesteryear where a consumer, saver, or shop-keeper would exclaim “ouch” when he dropped a dollar on his big toe…

Crypto’s valuation is denominated in the one thing that has value: US dollars. Why do we never hear of crypto valued in ounces of gold, or vice-versa?

Kent-

Not sure I understand when you said: “the one thing that has value: US dollars.”

??

John H,

Kent is correctly observing that nothing is ever priced in crypto.

When you buy gas at the gas station, you’re paying three and a half DOLLARS per gallon. At the grocery store, chips are two for five DOLLLARS.

When you buy things online with crypto, the merch is priced in dollars and then the website just does the xccy conversion before you send the funds.

“It is only trading as a “risk asset” because people don’t understand it. It’s an entropic store of value.”

???

Entropic store of value. That’s a new one.

It takes me about three hours to dig a roughly one cubic yard hole out in the yard. I’m old, I work slow. But the energy I expended digging that hole (breakfast) had value so therefore the hole has value and should have a cryptographic representation of its value that I can use as an asset.

Hmm. I shall call it “Bithole”. Miners, that is Diggers, will take a picture of their dug holes and I will credit them “Shoveltoshis” with my AI assistant and they’ll have wealth from the entropy. I recommend eggs and bacon, seems to make for higher quality entropy out in the yard.

Problem you have is nobody wants to pay 100k for your hole, and you can’t sell it over the internet.

Surely this work is worth at least one Fartcoin

I wonder if you can reverse the mining process and use the “entropic value” of the Bitcoin to get your electricity back? I mean, really, that’s all you spent on getting it in the first place.

Securitized “Spent Energy”. That’s wonderful. I’ve been missing out on the opportunity to turn my electric bill into an NFT all these years!

If I trade in a “Spent Energy” security, can I receive that spent energy in return? What can I do with this absence of energy I’ve accumulated, exactly?

“cryptographic guarantees for that work done. It is symbiotic with our AI future”

The whole bitcoin debate is very interesting and will be unresolved for decades. Gold has centuries of history. Bitcoin has 10 years. It may be everything people say or it may be tulips.

The FED has conducted a propaganda war against gold for decades. Meanwhile gold has flowed east into the hands of “our enemies”. At this point the US is entirely committed to denying a monetary role for Gold. So the US is trapped by it’s own rhetoric.

However, BITCOINS inherent scarcity ironically probably counts against it as a monetary answer. That and its proof-of-work scheme and low, low transaction capacity.

I’m thinking that what will happen is that other, more “flexible” schemes will emerge with claimed ties back to BTC. The whole stable coin universe linked to virtual tokenization of Treasury securities maybe the direction he US will head for. At bottom the scheme will be to create a new market of Treasury demand.

Who knows, but it’s interesting to watch. Meanwhile I see that a bunch of Senate Republicans are calling for an additional 150 billion in new military spending…what DOGE gives, the congress will take away…

Bitcoin is correlated with tech, not with gold.

The theory that Bitcoin will serve as a hedge against inflation is unproven, at best, and likely wrong. The marketing may look like gold coins but it is not gold in character.

Where you may have an arguable hedge is against “government fiat currency”. I don’t buy it myself because there are better hedges, commodities and gold, and Bitcoin assumes current encryption is uncrackable in an age where we haven’t seen the full effects of quantum tech and whether their encryption will be similarly robust and cheap.

I also question the long term notion of a non-state-sponsored currency. Hate all you want against the dollar, euro, and yuan, at least those you can use to pay your taxes. If the USA & EU turned against Bitcoin like China, the currency is toast.

How is it symbiotic with our AI future? Because they’re both techy? If you said it’s symbiotic with our scammy future I’d agree

“On balance, the influence of the Federal Reserve System in its early decades served to lower interest rates below what they otherwise would have been, both in periods of falling and in periods of rising interest rates.” —Sydney Homer and Richard Sylla, A History of Interest Rates

It was true in the “early decades,” as Homer and Sylla saw it. Is the bond market beginning to sense that it’s equally true now?

We can be assured that whatever the fed does, it will be late, early, or just wrong!

We can be assured that Washington will not agree on anything and the hot air will increase global warming.

I could surely be wrong, but everything I see, points to inflation.

Wait, see, and pass the pop corn.

“We can be assured that whatever the fed does, it will be late, early, or just wrong!”

That just depends on where you stand. If you’re in real estate, the Fed was wrong hiking rates and keeping them high. It should have kept 0%. If you like T-bills, the Fed was wrong cutting rates.

The prices of houses were getting absurd with zirp, with charts going parabolic. Some people dont like to and wont pay high prices even if the rate is low. I think the housing market and overall economy would be a lot better if they arent used as gambling chips.

But then the party in power (whichever one) wouldn’t be able to point to a line going up and to the right and say “See? The economy is doing great!”

I’d like un-inverted yields, savings rate a point or two higher than inflation. I think getting those two require most things to be in balance.

People with a lot of money only have a fraction of their net worth in real estate.

“If you fast-forward 10 or 15 years, there are going to be regions of the country where you can’t get a mortgage,” he said during his semiannual testimony to Congress, noting that banks and insurance companies have been pulling out of coastal and fire-prone areas they deem too high risk.

IMO, maybe his most important comment.

Price discovery based on risk – reward eventually settles distorted markets, just not in my lifetime.

Robert

(QSLV)

Given what’s happened in other government departments, it may not be long before the DOGE people start interfering in the official statistics. That would make global buyers queasy about buying US debt. Can we even be sure this US government won’t default on the debt? Confidence matters.

Section 4 of the 14th amendment was designed to settle that issue.

Kent: is that the same “14th Amendment”

That, by my reading asserts equal enforcement of the law upon ALL (president to resident), but the high (AF) court read as: Presidential Immunity?

The constitution has been corrupted over a decade (see Citizens United). Probably more than 4 (too young to really know).

No problem there, the American people voted for the Constitution to become irrelevant. Problem solved!

“Can we even be sure this US government won’t default on the debt?”

Yes.

With this government, everything is negotiable. Perhaps they will insist on repaying in a new digital currency.

Look at the price of gold. No kidding, it is going up! Default gets closer every day. Perhaps the Fed will buy all the Treasuries, if nobody else wants them. Just think of all those dollars rattling around in the system. Inflation come to mind.

I want them. Just bought some Tbills today. 4.X% with inflation at ~3% seems fair.

The “default” is happening all the time. That 20% inflation from 2021-2024?

Someday a bottle of soda from a vending machine will cost $5. And the US will still pay all Treasuries on time at full value in “dollars”.

It is impossible for the U.S. to default on the debt. The issue is whether or not the FRN has any purchasing power. Personally, I think that the smartest thing Trump could do would be to work with the Fed and use the 1934 Gold Reserve Act to revalue gold held by the treasury and support a very slightly higher rate of interest, if congress agrees to a universal cut in spending across all programs and no tax breaks. This has actually been done before.

The new administration seems to be pretty out in the open about ending the rule of law. If they get their way then I can’t imagine that US debt is going to be seen as an entirely safe asset for much longer, when the questions of if or when it gets paid back are only based on the president’s whims.

Also, given that they’re already interfering with information sources like medical and climate science, it’s not a stretch to imagine them going with fictional economic numbers as well. I would actually be surprised if they didn’t.

When I checked the inflation data for my MSA last month they said they were no longer going to report energy. Specifically electricity snd natural gas. The data that I used to easily check on water resources from the Corp of Engineers is not being reported in some locations either. No data .. no problem

What do you think the odds are that the Fed actually has to hike short term rates again–rather than just holding the current rate where it is for some long period of time?

Good question. It depends on inflation. If it settles back down, the odds of a rate hike are nil. If it continues to accelerate, the odds get better every month that it accelerates. Rate hikes would be a real mess. But it would be a classic inflation scenario, where inflation comes in waves, interrupted by head fakes.

Correct, and if history is any guide, those wave get larger, not smaller. Gold and the longer end of the yield curve are certainly indicating no rate cuts, in fact, I would argue they are suggesting the a rate hike is actually more likely then a rate cut. Finally, yes, wouldn’t be a shock to see the Fed wrong-footed again and hiking into a recession in a year.

I dunno they don’t seem to be going crazy. Both did indicate early, however, that there were still inflation worries and a long pause for the fed. Best I can tell, no one has a great handle on what inflation is going to do because the US might stall out, Europe and Japan are blah as always, and China is stumbling.

The investors that look like they should sweat are whut is stonk valuation lol types and folks that levered themselves at the top of housing, IMHO.

Interesting from the 5 year and 10 year that as soon as inflation gets at or slightly below their 2% target, immediately a large rate cut. Almost like the Federal Reserve wants to send inflation back up.

– I actually see there is a REAL possibility that the FED is going to cut rates again when I look at what Mr. Market signals. When ? Perhaps not right now but perhaps in March ?

LOL.

The 3-month yield has risen just a tad since the Dec cut and is now at 4.33%, right where the EFFR is. There is no sign of a rate cut in its 3-month window.

The 6 month yield has also risen since the Dec rate cut. It’s now at 4.35%, above the EFFR. There is no sign of a rate cut in its six-month window.

So what is “Mr. Market” telling you after today’s CPI and 10Y auction?

Lowering short term rates raises long term rates which is a brake on the economy. Raising short term rates lowers long term rates, which is an economic stimulus. No wonder the Fed is fked.

What?? Lowering short term raises long term rates? Don’t think I understand. It does not appear to track with what happens.

That is EXACTLY what happened in this rate-cut cycle. Did you miss that?

Fed cut by 100 basis points, 10-year yield rose by 100 basis points.

I did not miss that. However is there some link as implied that one (lowering short term) causes the other? That is the part I am unclear about. If anything I’d think it the other way around. When conditions lead to the long term going up it is the kind of conditions that a in line with short term going down.

Wolf said: ”The Fed might have to hike short-term rates again to make sure long-term interest rates remain “moderate” – paying attention to the third part of its mandate, to conduct monetary policy “so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.” “

Bond vigilantes are whispering their concerns of Fed’s inflationary bias, while the Fed is broadcasting that it is serious about capping inflation. But doesn’t the Fed’s 2% inflation target confirm the bias in question.

“Stable prices” would be more convincing if targeted at 0%, IMHO.

The “bond vigilantes” are long dead. Stop believing in fairy tales. Real rates of return have been negative for a very long time as inflation has been under-reported for quite some time (~1980), completely by design. If there were such a mystical class of “investor” bond yields would be more closely matched to what shadowstats has been reporting (using the pre-1980 formula).

That nutcase Bill Gross might have been the last what you might consider a bind vigilante. He really was a nut job too. I lived around the corner in Carona Del Mar for a while. Bat shit crazy that one.

From Investopedia-

“Bond vigilantes are investors who sell government bonds in response to fiscal policies they view as inflationary or irresponsible, driving up borrowing costs for the government.”

The real “fairy tale” would be a belief that large numbers of investors will never, in unison, decide to lighten up on their long bond positions. (That fairy tale is right up there with “it’s different this time.”)

When some future episode of large-scale bond selling occurs, the term “Bond Vigilante” will be resurrected.

What will the Fed do if there is a spike in interest rates and the market crashes?

Sit there and watch it while grabbing some very expensive popcorn.

My imagination isn’t big enough to answer.

Decades of zero interest rate policy turned Japan into a basket case with a worthless currency. If not for the upcoming election in America interest rates should never have been cut. Everything seems to be politics and everything always ends up worse when politics plays into it.

Gold has been screaming this for quite a while. Stop with the “bond vigilante bullshit already. It’s laughable.

Core CPI MoM January jumps .44 percent, or about 5.2 percent annualized. Mr Powell has a problem.

Yeah, Powell listens to his Ph.Ds.

INFLATION COMES IN HOT

GAS PRICES SOAR

GROCERIES SPIKE

Howdy Youngins. It all comes down to Govern ment Spending. Will our Federal Govern ment Balance its Budget? My Lava Lamp shows it cannot.

Good Luck

I think the more the ridiculous spending that gets exposed, the more American citizens will demand that the budget needs to be balanced. There are so many wasted tax payer dollars spent here at home and overseas. Congressional representatives better pay attention to their constituents otherwise they will be looking for a new job.

Right. The pendulum has been swinging back and forth (red/blue) for 80+ years. It’s almost as if neither party actually represents the interests of the people…

…something about a divided society being a conquered society.

How does the “citizen demand” in an oligarchy?

CONgress doesn’t care: it’s just sales.

The people are bought and sold, with their own tax dollars.

Federal employees are some of the few that can qualify for an actual pension anymore. Plus, the speaking engagements are generally well paid. IE: No job hunting required.

Are you serious? The voters do not choose their representatives, the representatives choose their voters through gerrymandering. I used to live in a competitive district but then the R team decided it was too competitive. Now there is no point to my even voting.

Hey Bubba. The government could balance the budget by taxing back some of the Covid money that ended up in the bank accounts of the 1%. Taxing money takes it out of circulation (destroys it).

But the prevailing economic theory says deficits-are-cured-by-tax-cuts-to-the-super-rich. So I look forward to more tariffs (paid mostly by consumers) and more tax cuts to the already morbidly rich.

What do the super rich spend their money on you ask ? They mostly buy assets. So they are bidding against you for houses, land, gold, education, etc. etc., and those $500 million yachts don’t pay for themselves

Yup. “The deficit for the first three months of the 2024-2025 fiscal year – in other words, the fourth quarter of 2024 – reached a record $711 billion, $200 billion more than for the same period in 2024. “

Bring on the disco!

FORD CEO Warns Tariffs Will ‘Blow Hole’ In Auto Industry…

These braindead managers at Ford should have decided to manufacture in the US and source more in the US. Ford is the worst about offshoring production to Mexico, China, and elsewhere.

SO – question is why did they outsource? Was the senior management team pushed by some force to go out of the US? Having worked for many companies that DID outsource it came down to 1 thing – cost of labor. I help set up a plant in mexico making assemblies for the aircraft industry – the workers in mexico made product equal to the quality of the ones made in the US factory – all products were rigorously tested and passed. The mexican workers put in 48 hours per week for $2.00 per hour – and no the price of things they bought wasn’t cheaper – the Walmart supercenter in that city charged the same for a gallon of orange juice as the one in the US town i lived in. Perhaps the Union workers could cut back on their demands for more pay/benefits to retain their jobs in the US – if they don’t American manufacturing will not continue.

Lots of automakers manufacture in the US, including all the Japanese automakers. Most of the Hondas you can buy in the US are made in the US, and all Teslas are. Both of them are on top of the list of US content in their vehicles.

Ford was on the forefront of offshoring production to Mexico. Its Hermasillo plant opened in 1986, and I remember — this was when I was running a big Ford dealership — having to deal with Escorts made in Mexico.

So why has Ford been run by such braindead morons? Now they whine that Trump is destroying their fat profit margins, LOL.

Modern industrial robots cost the same everywhere. In a highly automated plant, the cost of labor per vehicle isn’t that much anymore.

Walmart was on the forefront of offshoring to China. It’s one of the primary culprits. That’s exactly why the US needs universal tariffs. 25% would be good to start. You can still offshore, but that tariff will come out of your profit margin.

The US has a $1.2 trillion goods trade deficit a year. Everyone bitches about the budget deficit, but the trade deficit is somehow good because it fattens up profit margins and stock prices by sacrificing the US economy and financial health???

MW: Markets tank over hot inflation report as Trump demands interest rate cut amid soaring gas and grocery prices

Trump’s first inflation report since beginning his second term shows prices have risen more than expected.

‘Trump says interest rates should be ‘lowered’ to go ‘hand in hand’ with his tariffs’

CNBC Markets, Feb 12

His billionaire handlers said “He meant long-term interest rates.”

He truly doesn’t have the foggiest idea how the economy works. If he spent a few hours a week reading Wolf, the country might have a chance… although literacy is a pre req

A friend of mine once said “Trust water.”

“March bond requests are up fourfold in Vermont’s biggest cities and towns”

“The state’s 29 municipalities with at least 5,000 people are set to ask voters for nearly $275 million in capital projects — a leap from $60 million last year — in a collective wish list heavy with water and sewer plans.”

https://vtdigger.org/2025/02/11/march-bond-requests-are-up-fourfold-in-vermonts-biggest-cities-and-towns/

0.5% MoM inflation right after .4% MoM. Things aren’t looking great.

invalid comp btwn CPI YOY and EFFR. The spike in inflation mid 21 is still there and inflation is rising faster than EFFR which is fixed (ex for the 1/2 pt mistake). higher consumer prices undid the incumbent. do not assume Fed is independent (see potus) and do not assume you know what treasury is going to do (the said they will monetize gold < 12 mos) Fed is like KC chiefs nite before the game when NFL refs called and said, your offensive line will not be able to hold on every play. they're onto us.

“The 5-year breakeven inflation rate rose to 2.64% today, the highest since March 2023, …….This measure (5-year Treasury yield minus the 5-year Treasury Inflation Indexed Real Yield) shows …….”

Wolf, I feel like I have learned a ton from your writing over the years, but this doesn’t fully make sense to me.

Why would this represent the breakeven inflation rate? Wouldn’t that be better represented by Treasury yield minus CPI/PCE? and even then any positive value would seem to represent a net gain versus being truly “breakeven”.

Secondarily, 5 year yield minus the inflation indexed real yield, shouldn’t this ratio remain ~constant as the inflation indexed value increases with increasing inflation? Or does this just show a mismatch between TIPS and regular treasuries?

This may seem like a silly question, but I did rtgdfa(always do), and it still sort of bugs me.

Thanks for all you do!

-Bio

“5-year breakeven inflation rate” is the name of this metric.

The FED has been aiming for a “Soft Landing” and trying to avoid a Recession. I am and have been highly skeptical of this happening.

The wild card now is will President Trump’s axing of government workers have substantive impact on demand going forward?

Thus creating the Recession needed to stomp out Inflation?

Is the U.S. economy clicking on all cylinders and thus inflation while our neighbors are struggling?

I have notice our neighbor south of the border Mexico just cut rates another 50 bps. Canada did another 25 BPS a couple of weeks ago because of slowing economic conditions or is it because of tariffs?

Catch 22 for Canada:

“The Bank of Canada would be in a tough situation but our view is that they would become more aggressive in terms of rate cuts if that’s [US tariffs] what we’re faced with,” said Doug Porter, chief economist at BMO Capital Markets.

The bank’s challenge is that US tariffs might both drive up inflation – in theory, prompting the need for higher rates – and also cut growth, which could on paper mean more stimulus in the form of lower rates.

Balanced on a knife’s edge.

Which seems to apply to a lot of things rt now, in the U.S. economy, GeoPolitics, etc.

That last paragraph had me laughing. Was that doublespeak.

Raise rates to cause you to lower rates. haha.

Inflation was pretty uniform amongst the developed nations during COVID. I’d guess why we’re running a bit hotter than Japan/EU is because we stimulated a bit more during towards the end, so we avoided a landing. Whether you think that’s worse than job losses is a matter of perspective.

As most people are sellers rather than buyers of labor, I think we were better off. But if you’re retired, a business owner, or part of the wealthy classes, I could see why you think that was a policy error.

It could also be that china is eating more of Europe & Japan’s lunch in higher tier manufacturing, too. But I am more skeptical because you would expect to see China doing great and they’re in the doldrums as well with their current not so bright political management. So, no, I think it’s just crappy growth or inflation that was on the menu during the last few years and here is where we are at.

“inflation wasn’t quite done with yet when the Fed was cutting rates”

Ya’ think?

It’s essential to differentiate between short-term and long-term inflation expectations. While short-term expectations might become unanchored due to immediate economic conditions or shocks, long-term expectations can be more stable if anchored by credible monetary policy. Understanding the nuances of inflation expectations can help policymakers, investors, and economists respond effectively to shifts in the economic landscape.

I wonder what would have happened to inflation if the FED had not cut at all. If rates were still 5.5 for the last year. Would that had snuffed out inflation? Suppose we’ll never know.

Also – I thought the fed had a dual mandate. Now I am learning it has 3 mandates. And that doesn’t even count the unspoken 4th mandate.

Everyone is getting their insurance renewals. My California house is up almost 30% (doubling in 2 years) and I’ll count myself lucky since it’s on a hillside. My Wisconsin rentals’ insurance is up another 10%. Guess what I’m going to do rents in August?

Can’t wait to see the next hike in car insurance.

The multiple thousands of dollars in insurance hikes matters a lot more than whatever the price increase in eggs is.

The statutory debt ceiling will keep rates in check until after it’s removed.

Sarc? It’s been moved every time it comes up.

Powells other tool is liquidity. Taking money out of circulation is poorly understood and does not raise red flags like raising interest rates does.

Frosty,

I think you are onto something. Given all the attention that the EFFR gets in the media, it is the slow drawn down of liquidity via QT that’s going to end up doing the heavy lifting. Seems Powell is happy keeping the attention on rates while QT continues working quietly in the background.