Biggest consumer spending surge in nearly two years overpowered the drop in private domestic investment and change in private inventories.

By Wolf Richter for WOLF STREET.

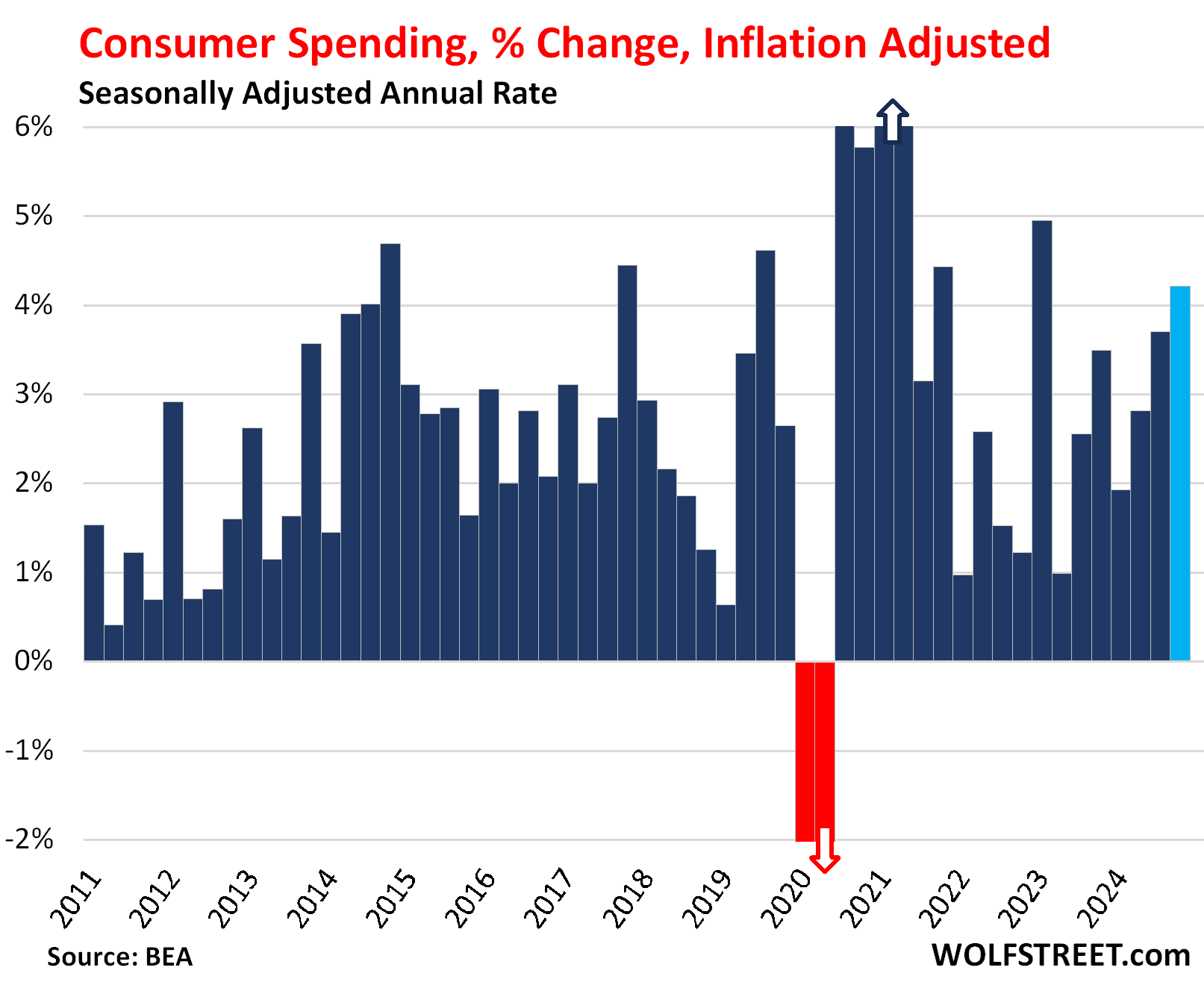

Our drunken sailors, as we’ve come to call them lovingly and facetiously, had a blast at the party in Q4. Consumer spending jumped by an annualized rate of 4.2% in Q4, adjusted for inflation, the biggest increase since Q1 2023.

They splurged massively on goods, especially motor vehicles and recreational goods, and they also splurged on services, and they accounted for over 69% of GDP.

And their massive spending propped up GDP growth despite the drop in private domestic investment and the drag posed by the change in private inventories.

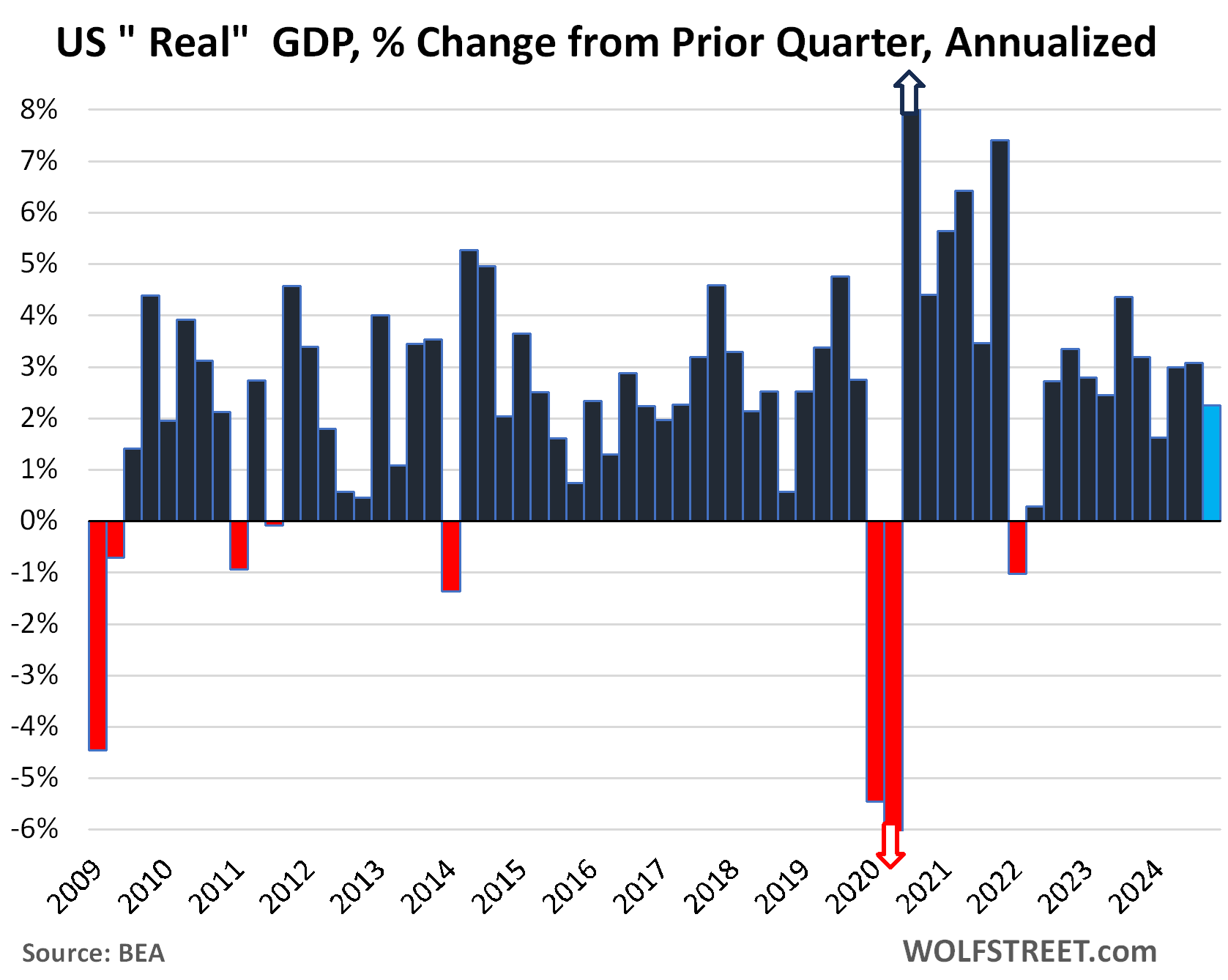

GDP, adjusted for inflation (“real GDP”), grew by an annualized rate of 2.3% in Q4, compared to growth rates of 3.1% in Q3, 3.0% in Q2, and 1.6% in Q1, according to the Bureau of Economic Analysis today.

By major category, adjusted for inflation, in annual rates:

- Consumer spending (69% of GDP): +4.2%, a sharp acceleration from the prior quarters, fastest growth since Q1 2023. It contributed 2.82 percentage points of the 2.3% GDP growth!

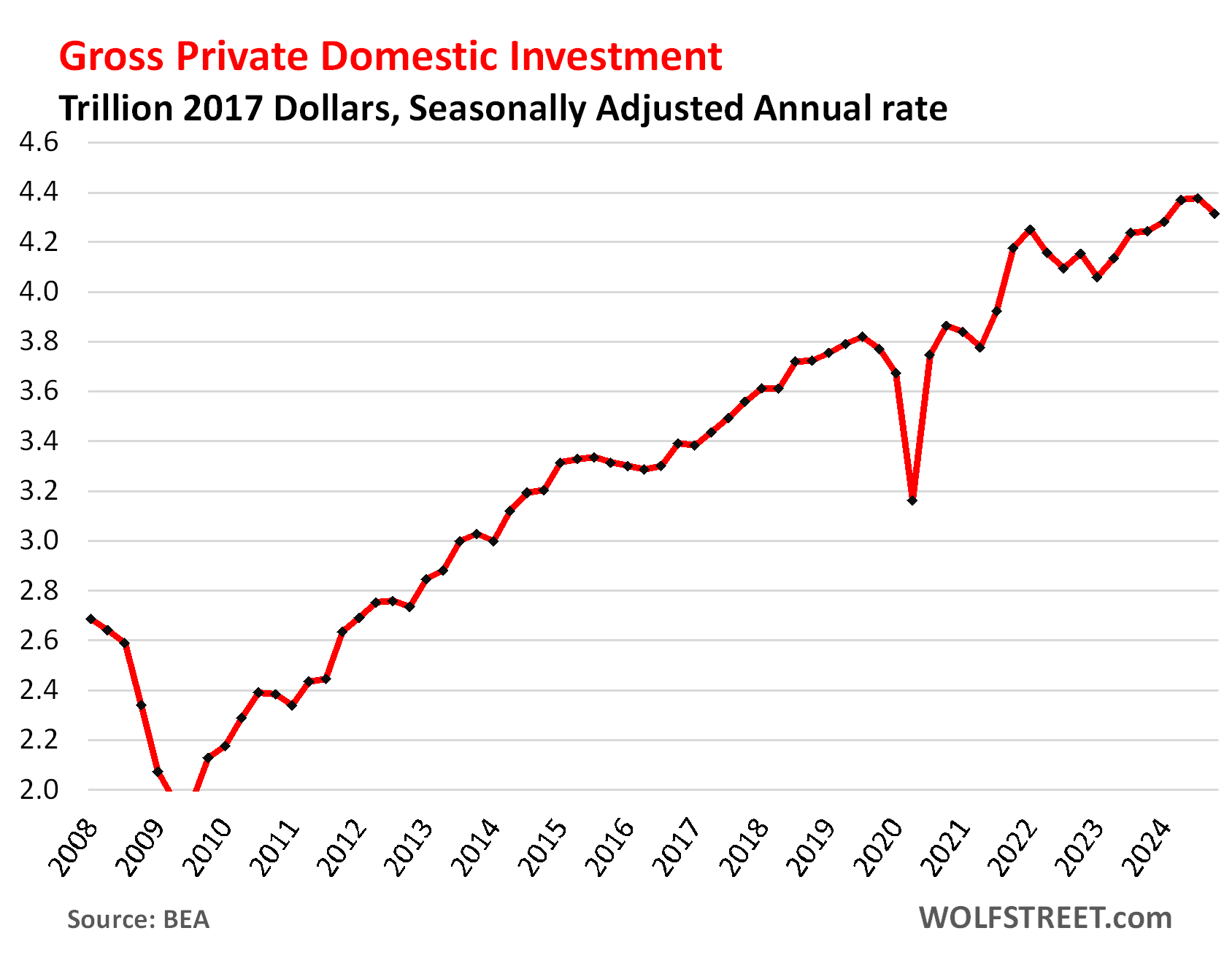

- Gross private domestic investment (18% of GDP): -5.6%, after six quarters of increases. It subtracted 1.03 percentage points from GDP growth.

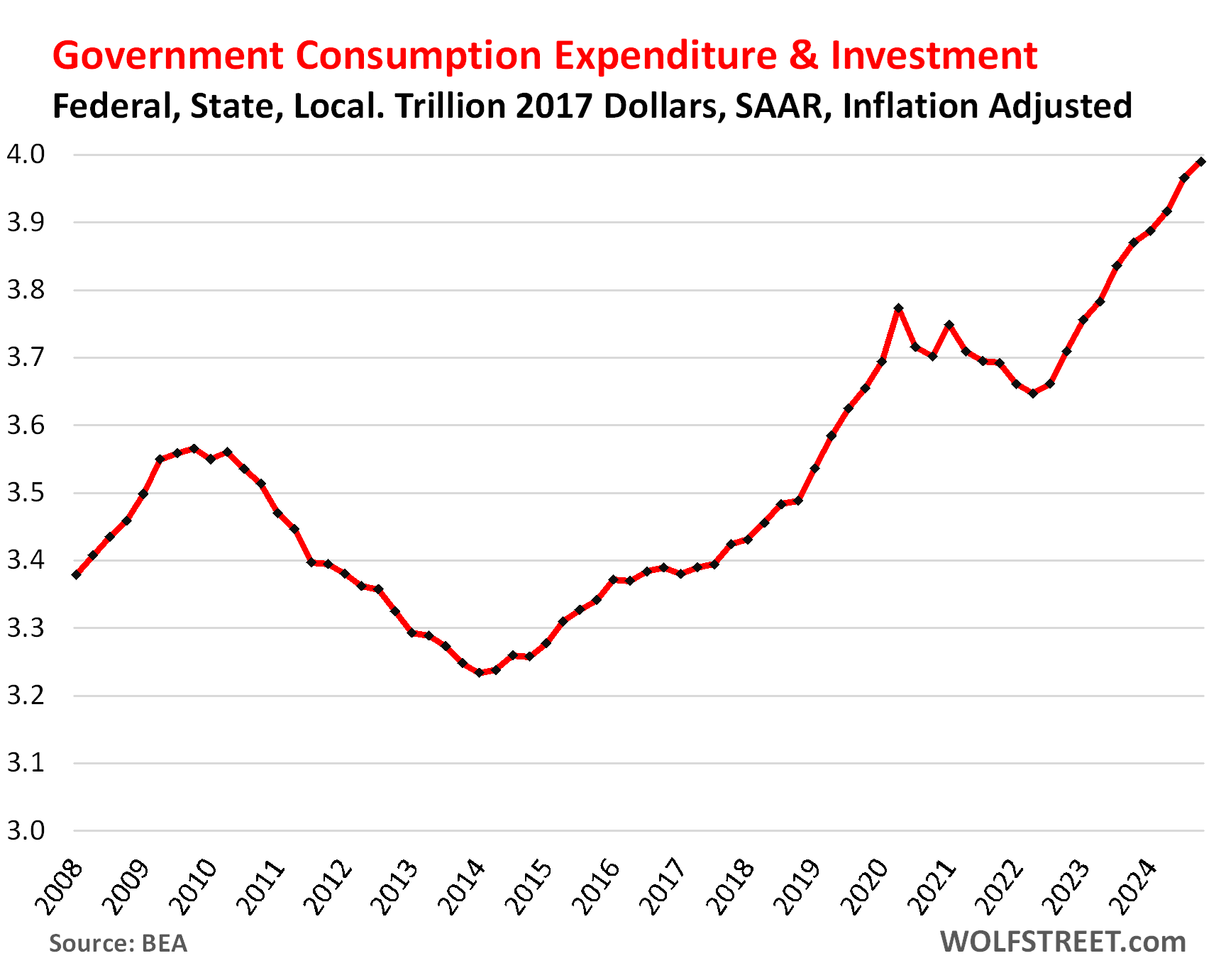

- Government consumption and investment (17% of GDP): +2.5%, a deceleration from the prior two quarters (federal government +3.2%, state and local government +2.0%). It contributed 0.42 percentage points to GDP growth.

- Change in private inventories dragged on GDP. This form of investment subtracted 0.93 percentage points from GDP growth.

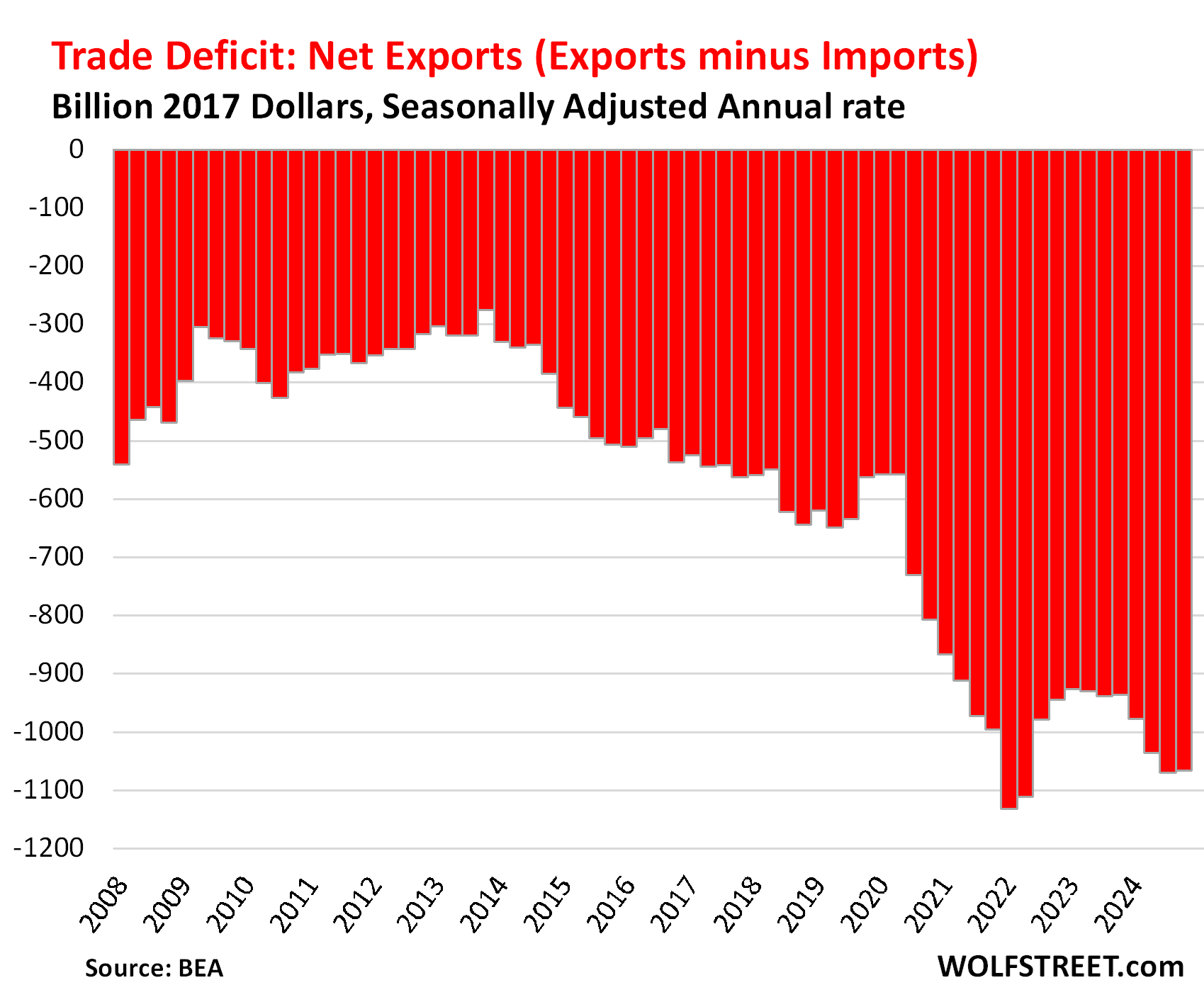

- Net Exports (Exports minus Imports): Roughly unchanged at near record levels. Imports drag on GDP. Exports add to GDP.

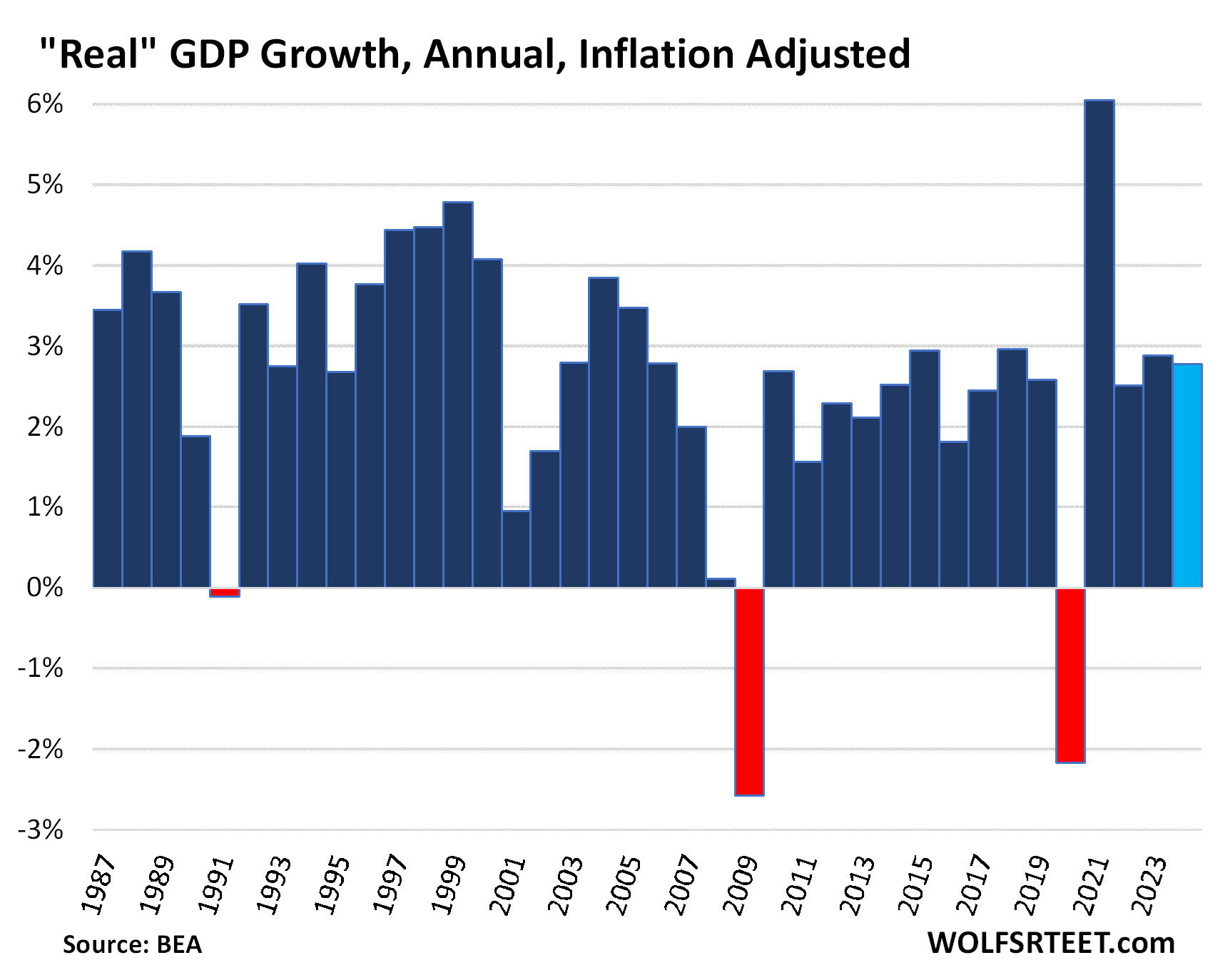

Annual “real” GDP for the whole year 2024 (inflation adjusted, but not seasonally adjusted, and not an annual rate) grew by 2.8%, driven by consumer spending, which also grew by 2.8%.

This annual real GDP growth of 2.8% was well above the 15-year average growth of 2.4%, despite the highest interest rates the economy faced in decades, with short-term rates above 5.4% for much of the year.

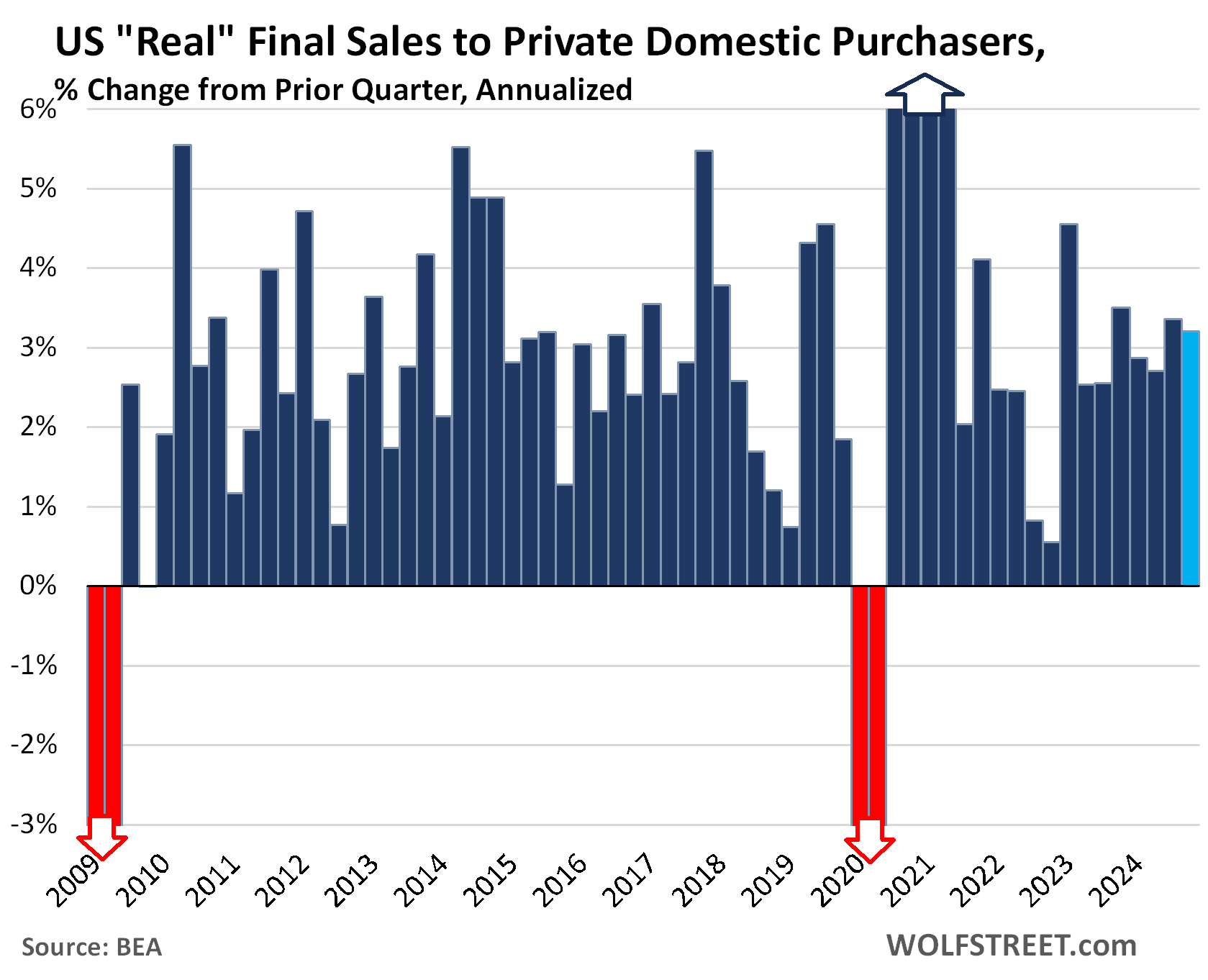

A purer indicator of private domestic demand: “Final sales to private domestic purchasers” is a metric that is part of the GDP report and tracks US private domestic demand ( = GDP less exports, less imports, less government consumption expenditures, less government gross investment, less change in private inventories). It covers about 87% of GDP.

Powell mentioned it from time to time as a purer indicator of private domestic demand from consumers and businesses – which is what monetary policy is trying to influence.

Adjusted for inflation, final sales to private domestic purchasers jumped by an annual rate of 3.2% in Q4, attesting to the strength of private domestic demand:

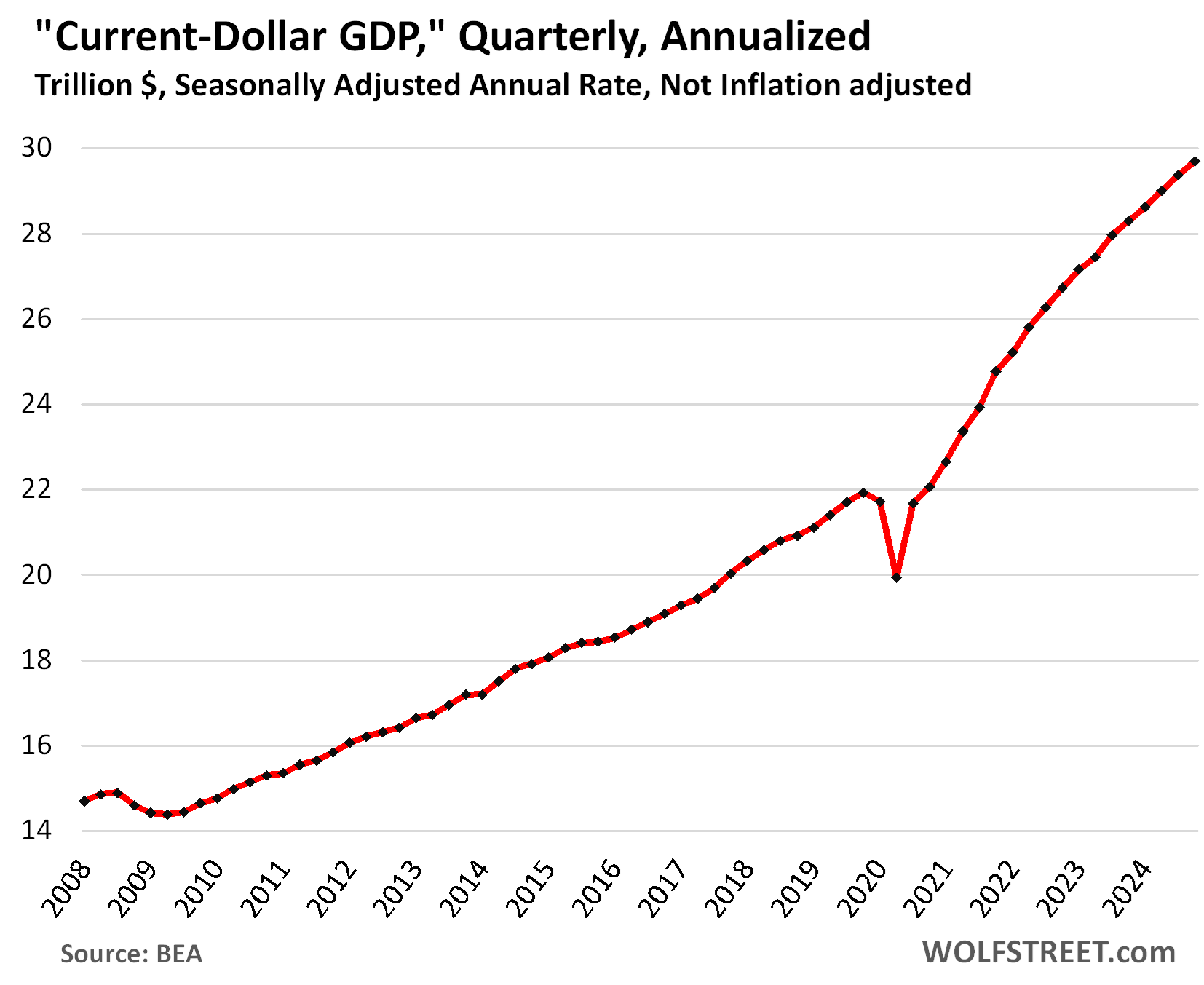

The actual size of the US economy: “Current-dollar” GDP, or “nominal” GDP (not adjusted for inflation and expressed in current dollars) rose by an annual rate of 4.5% in Q4, to $29.7 trillion. This is the amount we use for the US debt-to-GDP ratio here further down.

Consumer spending jumped by an annual rate of 4.2% in Q4, adjusted for inflation, the fastest growth since Q1 2023, and the second fastest since Q4 2021, powered by a huge splurge on durable goods, especially motor vehicles and recreational goods and vehicles.

- Services: +3.1%.

- Durable goods: +12.1%

- Nondurable goods: +3.8%.

This spending splurge on goods has been predicted by retail sales – which are sales of goods, not services – that have caused us to warn, The Fed Needs to Watch Out: Amid Strong Demand from our Drunken Sailors, Retail Sales Surged in Late 2024 and Inflation Caught its Second Wind.

Quarter to quarter, in terms of 2017 dollars, personal consumption expenditures, as they’re called officially, jumped by $167 billion, to an annual rate of $16.3 trillion in Q4.

Gross Private Domestic investment dropped by 5.6% annualized and adjusted for inflation, after six quarters of increases. That was a big hit to GDP, subtracting 1.03 percentage points from GDP growth. Of which:

- Nonresidential fixed investments: -2.2%:

- Structures: -1.1%

- Equipment: -7.8%

- Intellectual property products (software, movies, etc.): +2.6%.

- Residential fixed investment: +5.3%.

Government consumption expenditures and gross investment rose by 2.5% annualized and adjusted for inflation, the smallest increase since Q1.

Combined, federal, state, and local government consumption and investment accounts for 17% of GDP. State and local governments account for 61% of total government spending, the federal government accounts for 39% total government spending.

This does not include interest payments, and it does not include transfer payments (the biggest part of which are Social Security payments), which are counted in GDP if and when consumers and businesses spend these funds or invest them in fixed investments.

- State and local governments: +2.0%.

- Federal government: +3.2%.

- National Defense +3.3%.

- Nondefense +3.1%.

The Trade Deficit (“net exports”) in goods & services remained at near record-high levels, essentially unchanged overall:

- Exports: -0.8% (goods exports -5.0%, services exports +7.2%). Exports subtracted 0.08 percentage points from GDP growth.

- Imports: -0.8% (goods imports -4.0%, services imports +12.8%, driven by Americans spending overseas in the ongoing travel boom). Lower imports contributed 0.12 percentage points to GDP growth.

- Net exports (exports minus imports) remained at -$1.07 trillion.

The Debt-to-GDP ratio worsened to 121.8% in Q4 as the gross national debt in current dollars (not adjusted for inflation) ballooned by 2.0% from the prior quarter to $36.2 trillion, while current-dollar GDP (not adjusted for inflation) grew 1.1% to $29.7 trillion.

The spike in 2020 occurred as GDP collapsed during the lockdown while the gross national debt jumped on the government’s free-money-giveaway spree.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I always enjoy your articles. Kudos on the data gathering.

propped up GDP growth, is correct IMO, but hmm, let’s discect the underlying assumptions in the face of the elephant in the living room, the deficit.

Returning too macro 101, Keynesian economics:

GNP = C + G + E – I, and the E-I is negative and equivalent too the deficit which is the only way that the GDP growth could be positive.

I read Stef Kelton’s reasoning concerning zirp as a good thing. She makes a lot of good points without a sense of history.

Did the Boeing strike even register in the numbers?

Apparently not. It registered in the jobs numbers at the time. But it’s not like these workers on strike stopped spending.

However, the BEA added this comment about Hurricane Milton:

“Impact of Hurricane Milton on fourth-quarter 2024 estimates

Hurricane Milton made landfall as a Category 3 hurricane just south of Tampa Bay, Florida, on October 9, 2024, bringing damage from high winds, including significant tornado activity, and extensive inland flooding.

This disaster disrupted usual consumer and business activities and prompted emergency services and remediation activities. The responses to this disaster are included, but not separately identified, in the source data that BEA uses to prepare the estimates of GDP; consequently, it is not possible to estimate the overall impact of Hurricane Milton on fourth-quarter GDP. The destruction of fixed assets, such as residential and nonresidential structures, does not directly affect GDP or personal income. BEA estimates of disaster losses are presented in NIPA table 5.1, “Saving and Investment.” BEA’s preliminary estimates show that Hurricane Milton resulted in losses of $27.0 billion in privately owned fixed assets ($108.0 billion at an annual rate) and $3.0 billion in state and local government-owned fixed assets ($12.0 billion at an annual rate).“

A lot of people pulled their purchasing forward in anticipation of tariffs and rising cost of goods, I know we did a little.

For January, the threat of a Costco strike has the stores packed to the rafters with people stocking up. On Saturday afternoon ours was like trying to go to the mall on Christmas Eve.

When people come to realize that their dollars will buy less in the near future, they will rather spend today.

Nothing more scary than an uppity union worker disrupting a life style moment that is in need of re-calibration.

This is a time that the median is a much more descriptive statistic than the mean, the common average. A plot of inequality.

MW: Why the Fed may be done cutting interest rates, once and for all.

Even if the Fed cut the rates it can, wouldn’t the bond vigilantes at this point push back? If that makes sense, who wins that tug-of-war?

Given the “interesting” nominations coming from our new leadership, I can’t wait to see who — or what — is nominated for the next Fed chair. Maybe a ham sandwich that got un-indicted at some point?

Whoever it is, he/she will be 100% loyal and dedicated to the president. That much you can count on.

Judy Shelton will be the next Fed chair

I’d support Judge Judy for Fed chair!

Melania or Marla Maples? Choices, choices.

I think the next chair will have an OnlyFans site.

That gave me a good laugh. Probably.

Well, if the behavior of 47 is anything like 45, Powell is being verbally reminded each day to lower interest rates by the executive branch.

Hardly my bet that the Fed won’t fold like a cheap lawn chair and try to extend the unprecedented monetarist thought experiment of zero pct interest rates where, by definition, someone is picking up the tab for the risk premium.

Trump is likely to swap Powell out for a pliant minion. Dennis something or other, a former member of the BOG.

Actually, this time around, Trump attacked Powell for having caused this inflation, but didn’t push him to lower interest rates. Trump understands that lowering interest rates too far and stimulating inflation further would turn it into Trumpflation.

Wolf, I saw a stat that I was curious what you make of.

Nominal GDP; +1.4 Tril , +4.9% YoY

Treasury Debt outstanding ; ++2.2 Tril, +6.4% YoY

1. You’re comparing apples and oranges and get BS.

2. A lot of the money that government borrows and spends doesn’t go into GDP, including interest payments.

3. I discussed some of that in the article.

4. Including the debt-to-GDP ratio, which shows the burden of the debt on the economy.

5. Don’t drag trash that you pick up on the internet into here. Instead, RTGDFA

Wolf, you need to coach Powell on “How to handle stupid questions “.

Slick, lol, wouldn’t that be great!

Powell……BS..LTMGDFS!!

I still think he should be given a special Taser to zap reporters that ask stupid, repetitive, leading, loaded, and manipulative questions. ZZZZAPPP, “Next.”

I completely agree. It’s actually difficult for me to listen to the questions after Powell finishes his prepared remarks because many are way out of the purview of the Fed. And most of the rest are just uninformed or repetitive. At least someone asked about QT finally… I hope they don’t break anything. Sigh…

That’s hilarious. I could just see some fool reporter yelling “Don’t tase me, bro!”

Mr. Richter,

I’m guessing the “R T G D F A” keys on your keyboard tend to get worn out rather quickly. Does it get tiring having to replace keyboards so often?

My greatest wish in life is to never ever have to use that combination of keys again.

This maybe an easily answered question and I’m just not thinking atm.

But if over the “bad years” of Covid the fed decided to print money to assist the economy, thus creating the “good years”. Following that we had terrible inflation.

What was the ultimate brass tax damage versus if Covid never happened (and we continuing on the normal trajectory we were on)? Can we get a dollar amount figure of the damage? Or just history may show us later.

I mean there has been a lot of damage. Obviously

To the Fed’s credit, they had no crystal ball to see where the bottom was. But I fault them, once things had bounced back, for becoming lax about inflation risk. It was being discussed, BTW, right here.

“I mean there has been a lot of damage. Obviously”

Whoops !

Fed funds rate at 4.3% is a stimulus for big savers. It is for me anyway. I have lots more money to spend from interest alone compared to almost nothing a few years ago. If the Fed drops the rate below 4% I’ll shift to 20 year bonds which will then be yielding over 5%. I am okay with 4.3%, but I would be happy with 5%, very happy at 6%. Frankly, I am thinking about moving some to 20 years right now.

“Fed funds rate at 4.3% is a stimulus for big savers.”

It’s a stimulus for those who already have assets in general.

T Bills and chill is an alternative POV for us old fools.

The future for every single person on the planet, hopefully, to become an old fool.

Whats the multiplier effect of domestic funding? I suspect that the lion’s share of those dollars go to China companies. What a pity we no longer have much of a base economy.

The US is the second largest manufacturing economy in the world, larger than the next three combined. The problem is that the US is not THE largest, but ranks second far behind China.

Also, much of our manufacturing is completely dependent on components available only from China, because China through mercantilist exchange rate manipulation made the prices of those components so low no American source could compete — and no American manufacturer could use a non-Chinese source and still compete — driving U.S. sources out of business. Though not all the parts are coming from China, there are categories in which U.S. manufacturers were exempted from the previous Trump tariffs because they could show there was no alternative source.

IIRC it was the CEO of Raytheon who said they were heavily dependent on Chinese parts.

DeepSeek was just released, and ByteDance is releasing an AI agent. I see this as maybe the equivalent of dumping, but digitally. Even if Chinese entities do not directly profit, they seem to be wrecking our AI business model. I see it as somewhat like cheap drones suddenly being able to beat capital-intensive aircraft carriers.

This is really so funny. AI models have been stealing everything that anyone posted on line, and even emails. They’re crawling my server and putting a load on it, and they’re stealing my stuff. They don’t attribute it, they don’t pay me for it, nada, and they publish it as theirs, and they rake in the ad revenues, and then they whine when their business model gets whacked by some Chinese outfit that might have stolen part of their model, LOL. Divine retribution. Soap operas are going to made out of that, by AI of course. I hope that these AI models, that investors have plowed tens of billions of dollars into, will poison each other with fake and false data, steal each other’s fake and false stuff, and shred each other to death.

American capitalism hired the CCP to provide a compliant labor force for a fraction of the cost of American labor.

American labor is still the best in the world. Also, expensive.

Does “manufacturing” include software?

No, obviously not.

What do you think is the primary reason for a fall in domestic investment? If the demand is booming, why is there a pull-back in investment? What do corporations see in the future?

It was a one-quarter dip. If you look at the chart, they’re not uncommon. So maybe this was a sign that companies were waiting for the election to be over with and the new policies to shape up, so that they could take them into consideration, including tax considerations. Note that these are investments after they’re made, not when the decisions are made to make those investments. So there’s a lag.

Slowing QT was defacto QE.

Can anyone be surprised the “Zero Fox” contingency are still on a spending spree???

That’s internet BS that you stepped into somewhere.

slowing qt is de facto qe? does that mean that if i’m on a diet and lose 5 pounds a month, that if i only lose 3 pounds the next month i’ve de facto gained weight?

Powell for Dog Catcher!

The coming shock and awe of a reciprocal trade war with all our North American neighbors might have a moderating effect on spending….at least for spending which is largely discretionary.

All this talk about tariffs is like tossing a grenade into the outhouse. It’s likely to get messy.

The idea of a slow down in spending is hardly discretionary.

Tariffs seem appropriate as a necessary first step to counteract the chronic drag of the trade deficit which requires a budget deficit to pay for it.

I’m a mystery shopper…its a mystery why I shop

Well, if I had too evaluate your claim that, what you know damn well is not a mystery but an obsession.

About the rising debt, I can understand the Covid spike in 2020.

But then it was coming down for 2-3 years, before changing course a couple years ago and starting the new rise that we continue on today.

It makes a pretty sharp V – what is responsible?

I had been a bit of a drunken sailor these last few years, because I no longer needed to save for a house and I had all kinds of stuff to buy for my house.

Suddenly, though, I am feeling a lot more conservative, and thinking I need to put all the other crap I was gonna buy on the back burner.

I think that our leadership and his fake friends are colluding on how to cut labor costs for their businesses. When one group is taunted and suffering, the other groups fall in line, people stop leaving their jobs and try to get by. (My wife’s company is not giving the usual meager end of year pay bumps this year, as an anecdote).

OTOH, I suspect that the people with more money than us still have a lot more to spend. And maybe they don’t have employment to be concerned about. …It’s difficult to decide how to invest.

It depends on which is influencing the economy more. Looks like the spenders for now. Of course there are many other variables that impact the economy.

BTW, as a heads up, the stock market is a massive bubble right now and we all know that all bubbles eventually pop. Tread carefully.

No matter what you do, you are unlikely to effect the outcome. It means having a diversified portfolio will protect you from the tragedy associated with the crash of a single stock exposure.

Thank goodness when you get up tomorrow.

I wonder how much of the increase in spending and investment was driven by an expectation of some that price of goods n particular would increase substantially following the just announced implementation of tariffs by the orange one.

1. Investments fell a bunch, which was one factor why GDP growth was only 2.3%.

2. Consumer spending grew a lot, but consumers didn’t react to the threat of tariffs on manufactured goods because no one knew in December what would finally be tariffed, and if it even would get passed on to consumers. In addition, services, which are 69% of consumer spending, don’t get tariffed at all.

Well, the price of goods is not the issue, it is the lopsided balance of trade, causing the USG to run a budget deficit sufficient to keep the GDP positive so as not to hint at a string of negative GDP measurements, a recession.

The data in “The Trade Deficit (“net exports”) in goods & services” show a an inflection point in ~ 2014. What is the root cause of the increasing trade deficit? It suggests a 3X-4X shift in goods and services being imported instead of exported over a ~ 10 year period, so why the dramatic trend?

Also, it would seem to matter where the profits land, if we are accounting for the health of the U.S. economy. The U.S. could have a $1T trade deficit, but if the profit from the goods and services all goes to U.S. companies, that is different than if the profit leaves the country. For example, if I import a widget that costs me $1, and it is manufactured at $0 profit, then I sell it for $2, at a 100% mark-up, the entire profit lands in the U.S. This is quite different from the foreign manufacturer making 50 cents profit, and my selling it at $1.50, and so the U.S. gets 50% of the $1 total profit, and another country gets 50%. So do we need to know where the profits are landing to interpret the trade deficit?