Prices are still way too high, that’s the problem in the housing market, but they’ve been dropping substantially in some cities.

By Wolf Richter for WOLF STREET.

Oh my, here goes the real estate industry’s dream of a recovery for existing homes. Pending sales – a forward-looking indicator of “closed sales” of existing homes to be reported over the next couple of months – dropped 5.5% in December from November, seasonally adjusted, and were down 5.0% from the already collapsed levels a year ago, according to the National Association of Realtors today.

The Buyers’ Strike continues because prices are too high. Compared to the Decembers in prior years:

- Dec. 2023: -5.0%

- Dec. 2022: -2.8%%

- Dec. 2021: -36.1%

- Dec. 2020: -41.2%

- Dec. 2019: -28.2%.

Pending sales have been relentlessly hobbling along the bottom for over two full years. This is what happens when prices spike by 50% in a couple of years. Now they’re just way too high. These too-high prices have frozen the resale market and crushed the brokerage and mortgage industry, including employment (historic data via YCharts):

Pending sales are based on contract signings and track deals that haven’t closed yet and could still fall apart or get canceled. There has been quite a bit of talk of deals falling apart or getting canceled because buyers cannot afford the homeowner’s insurance, or cannot even get it. This is a particular issue in states where homeowner’s insurance has spiked in recent years. These deals that go nowhere are included in pending sales figures, but are not included in the figures of closed sales.

Pending sales by region. Seasonally adjusted, transactions fell in all regions in December:

- West: -10.3%

- Northeast: -8.1%

- Midwest: -4.9%

- South: -2.7%

What NAR said today about this situation in the West and the Northeast: “Contract activity fell more sharply in the high-priced regions of the Northeast and West, where elevated mortgage rates have appreciably cut affordability.” Ah yes, the too-high prices.

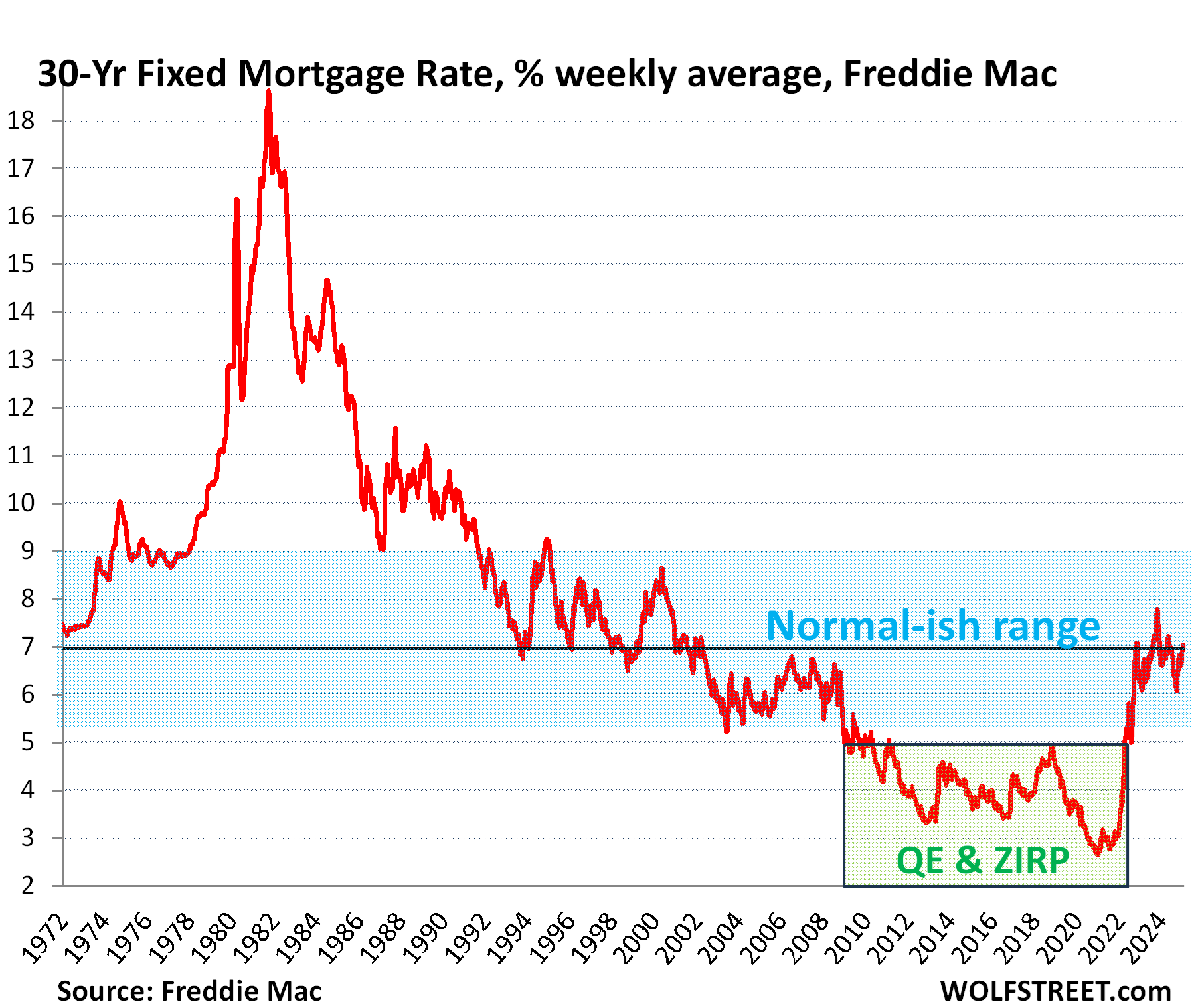

Mortgage rates are back in the old-normal range.

The average 30-year fixed mortgage rate inched down a tad to 6.95% in the latest reporting week, according to Freddie Mac today.

In December, when those pending deals were made, this weekly measure of mortgage rates was between 6.60% and 6.91%, lower than in January.

While those rates are far higher than they had been during the era of the Fed’s interest rate repression and QE, they’re now back roughly in the old normal range before QE.

But the Fed’s QE, which included the purchase of $2.7 trillion in mortgage-backed securities (MBS) to drive down mortgage rates and inflate home prices, ended in early 2022. And in mid-2022, the Fed began shedding those securities, and has so far shed $2.11 trillion. And mortgage rates have sort of re-normalized.

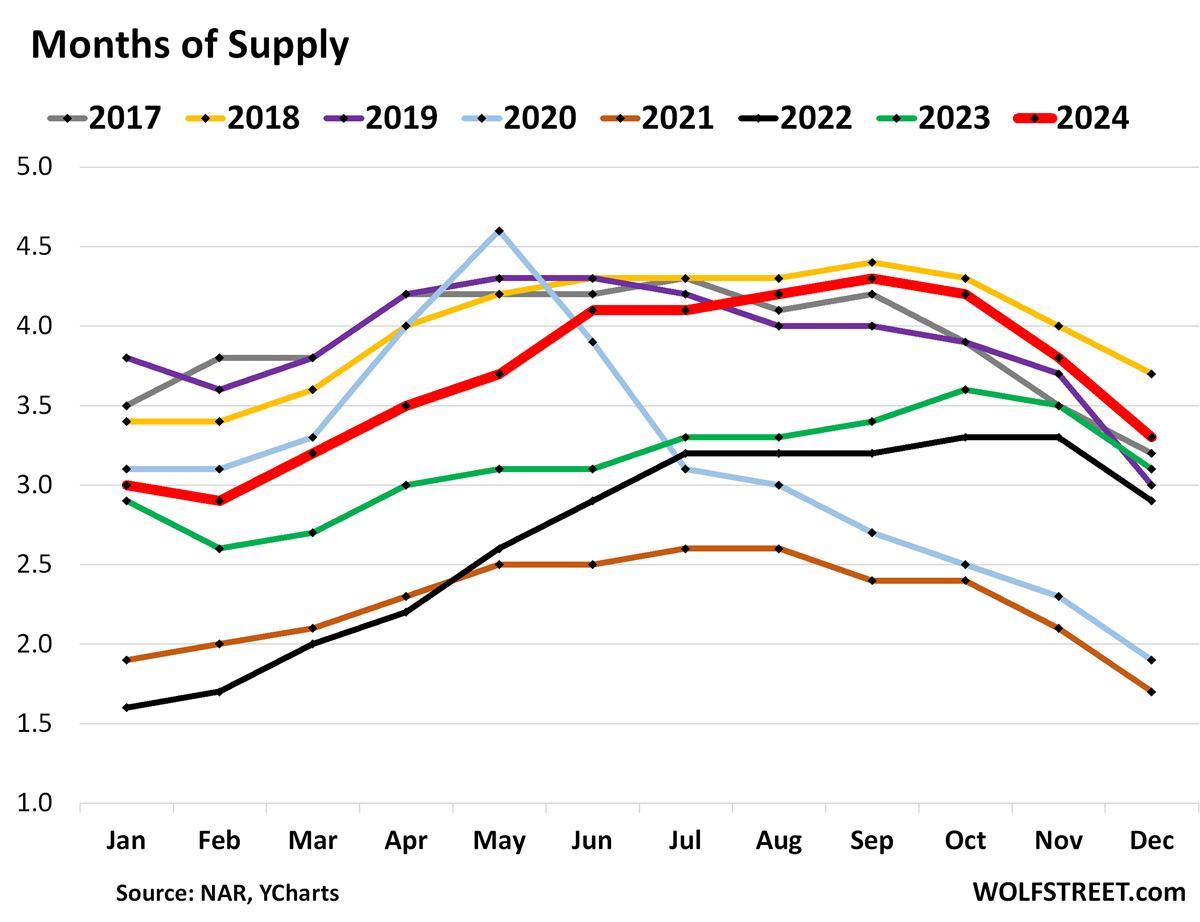

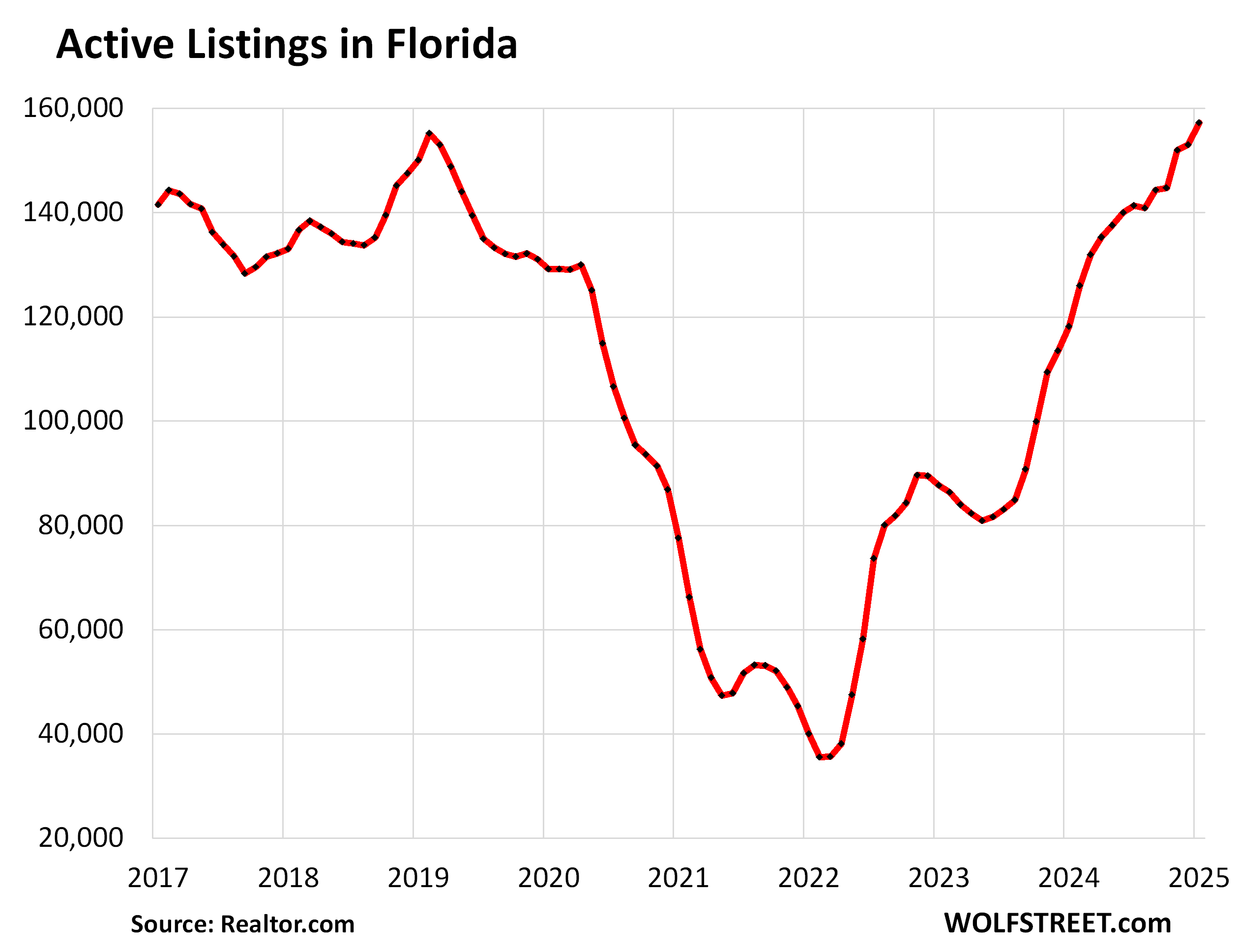

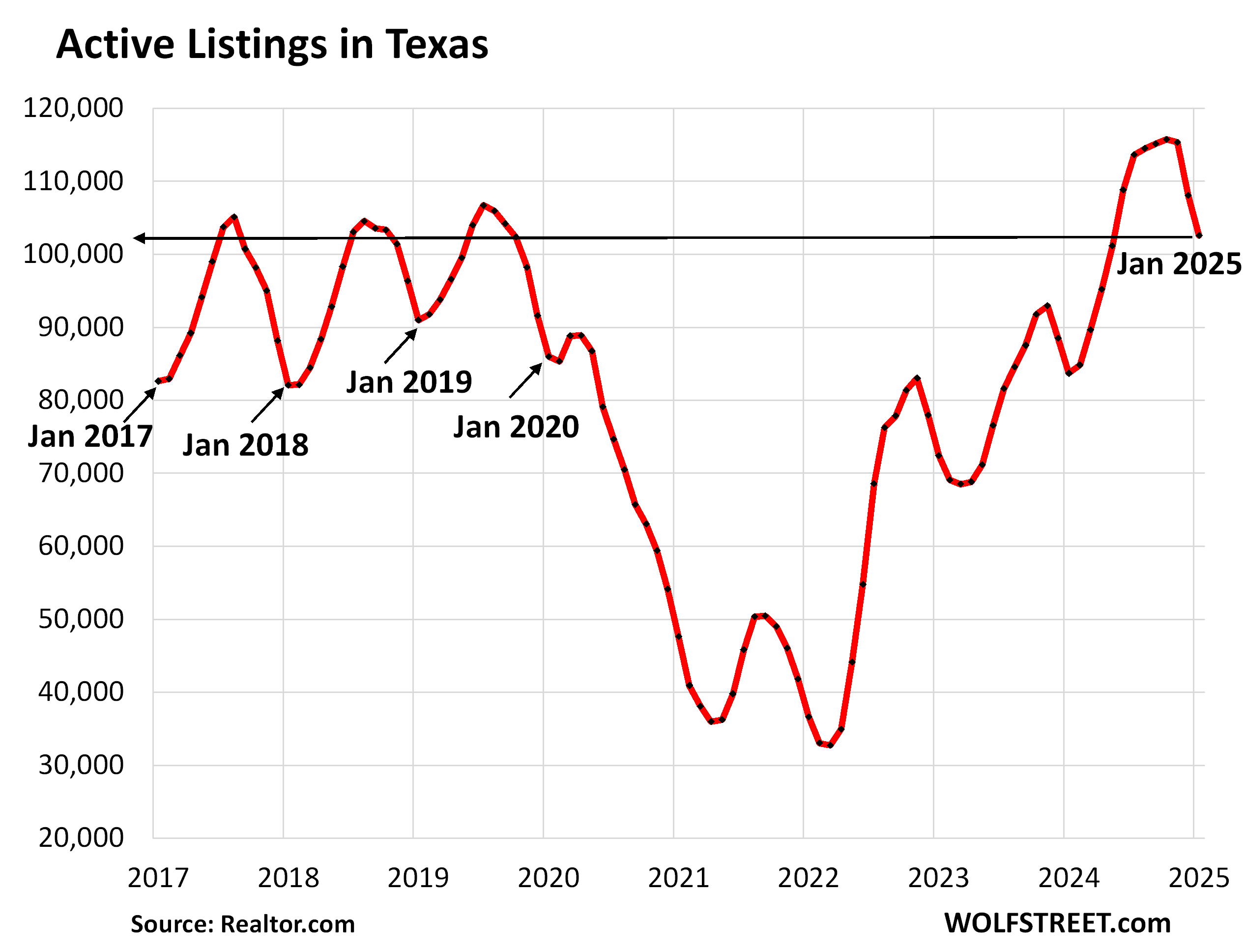

Inventory of existing homes & new construction is piling up, particularly in the South and West.

Supply of existing homes for sale in the US overall, at 3.3 months in December (fat red line in the chart below), was the second highest for any December since 2016, below only 2018, according to NAR data:

In Florida, active listings of existing homes in January ballooned to a record high in today’s data from Realtor.com going back to 2016:

In Texas, active listings of existing homes in January reached the highest level for any January in the data from Realtor.com going back to 2016. Since May 2024, active listing in every month were the highest for that month in the data of Realtor.com (fat red line):

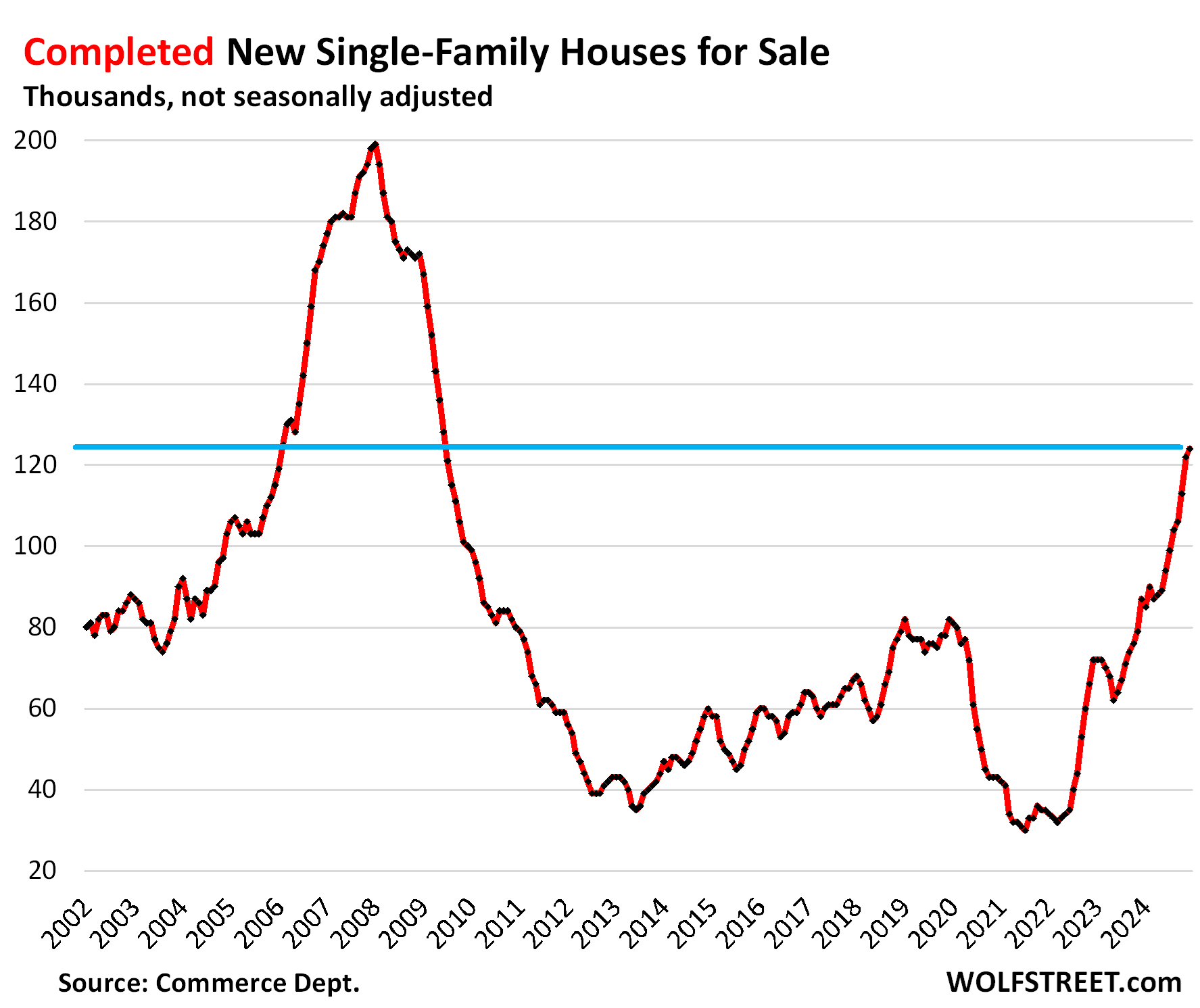

In the US, inventory of completed new houses for sale has spiked by about 50% from the peaks of 2018 and 2019, and by nearly 50% year-over-year to the highest since June 2009, according to Census Bureau data, as we have discussed a couple of days ago:

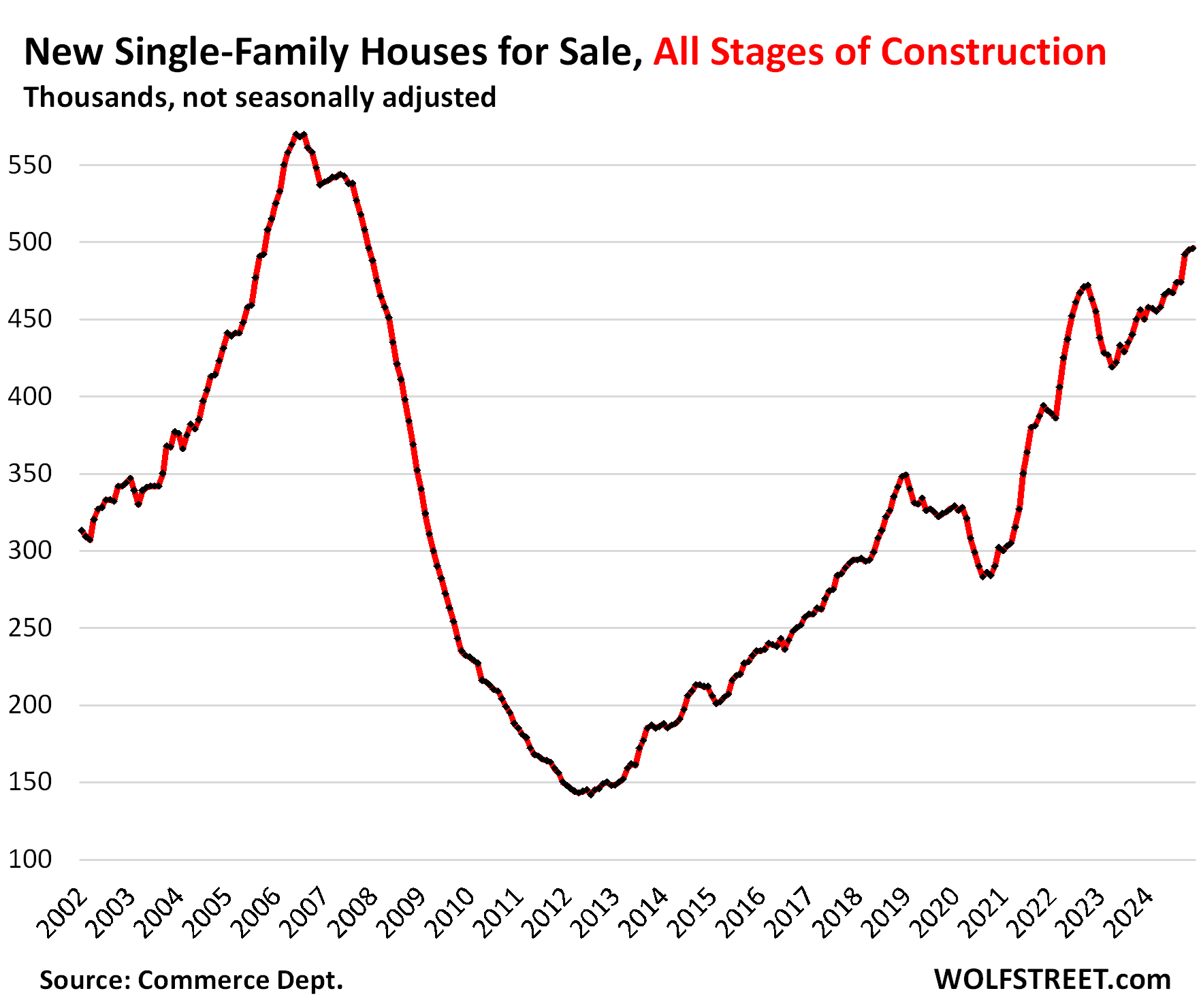

In the US, inventory for sale of new houses at all stages of construction – from not yet started to completed – has ballooned to the highest since December 2007.

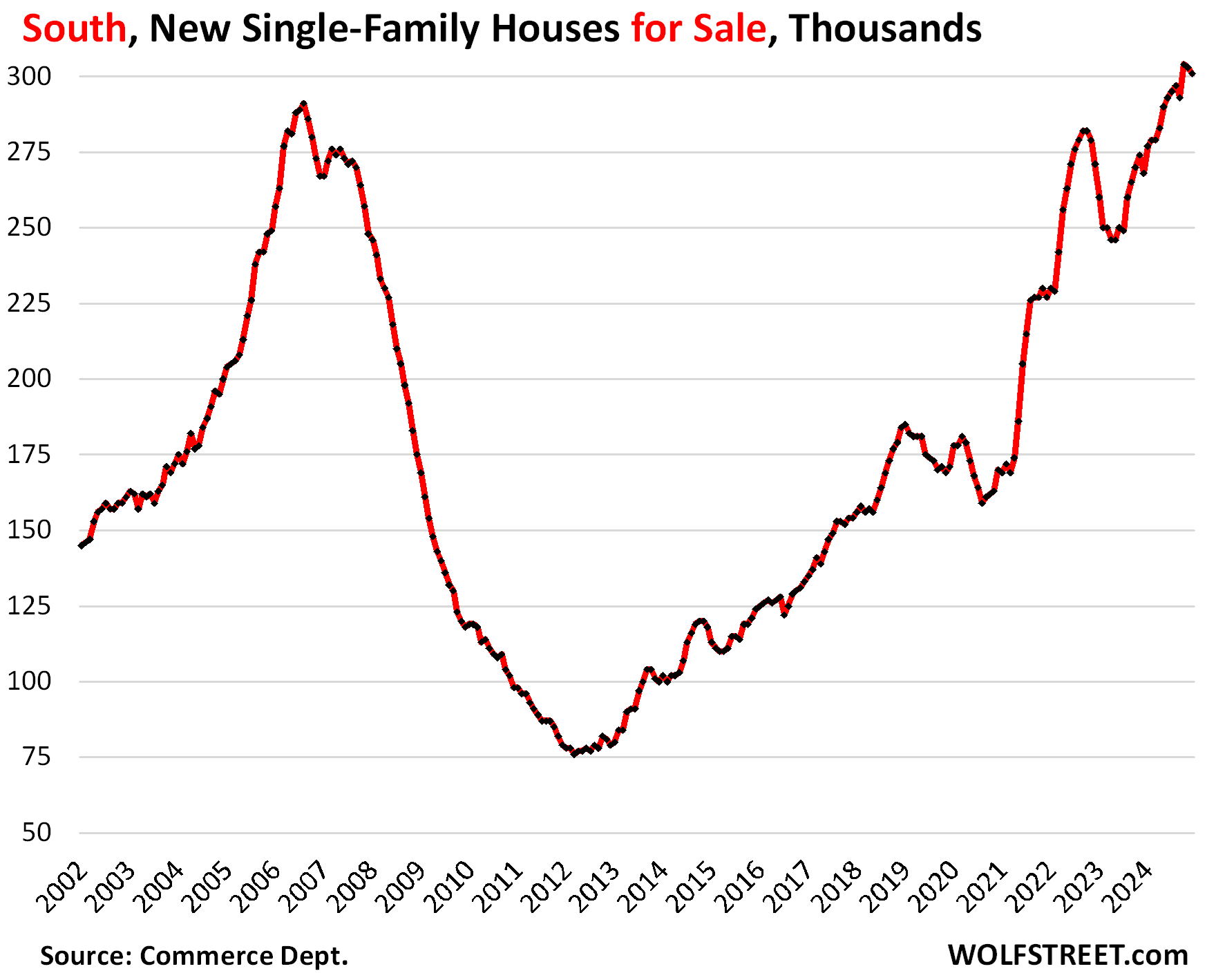

In the South, inventory for sale of new houses at all stages of construction has ballooned past the records during the Housing Bust:

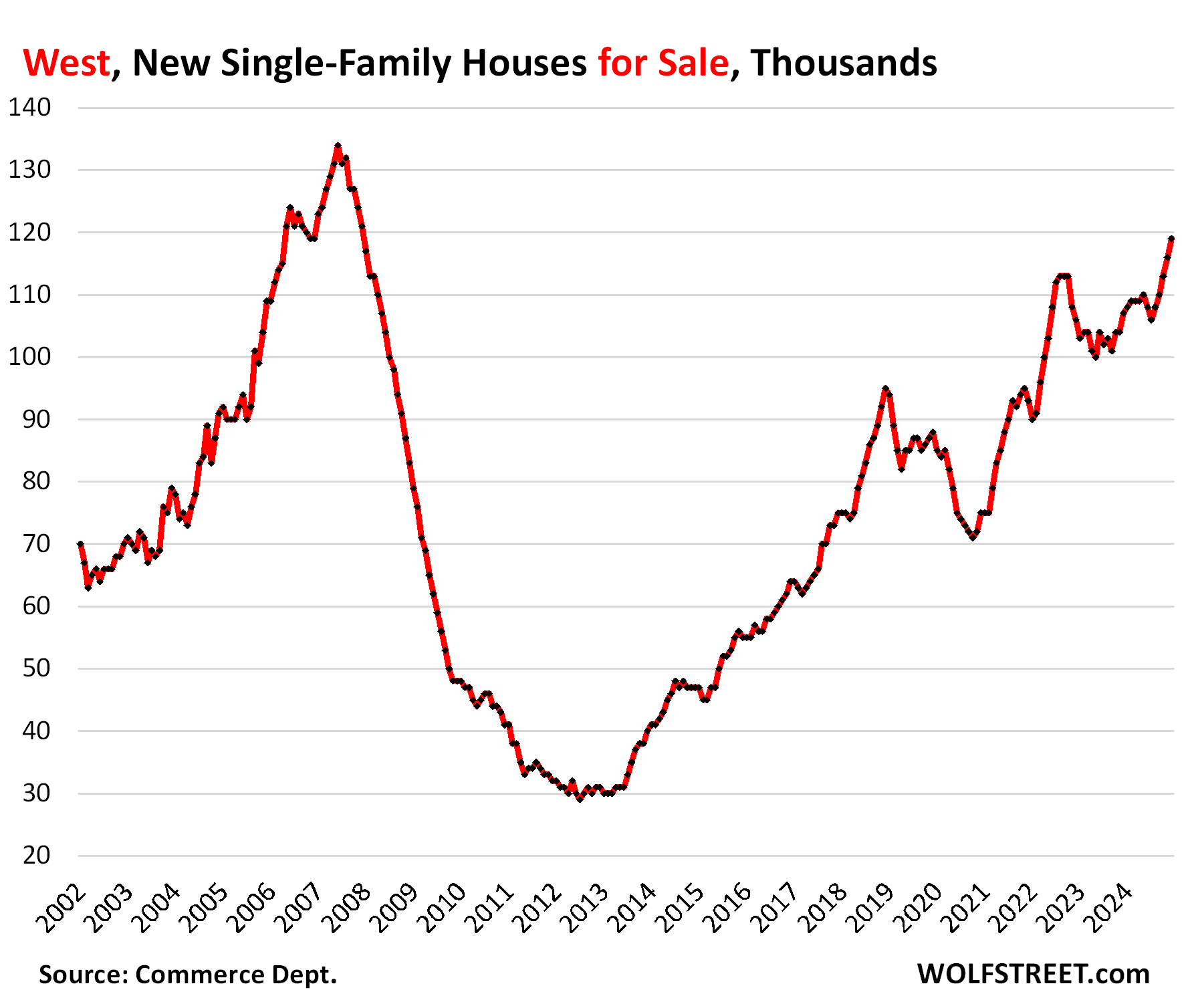

In the West, inventory for sale of new houses at all stages of construction is getting close to the highs of the Housing Bust:

Buyers’ Strike continued because prices are too high.

Pending sales of existing homes, as we’ve seen above, are wobbling along near the bottom, and did so again in December.

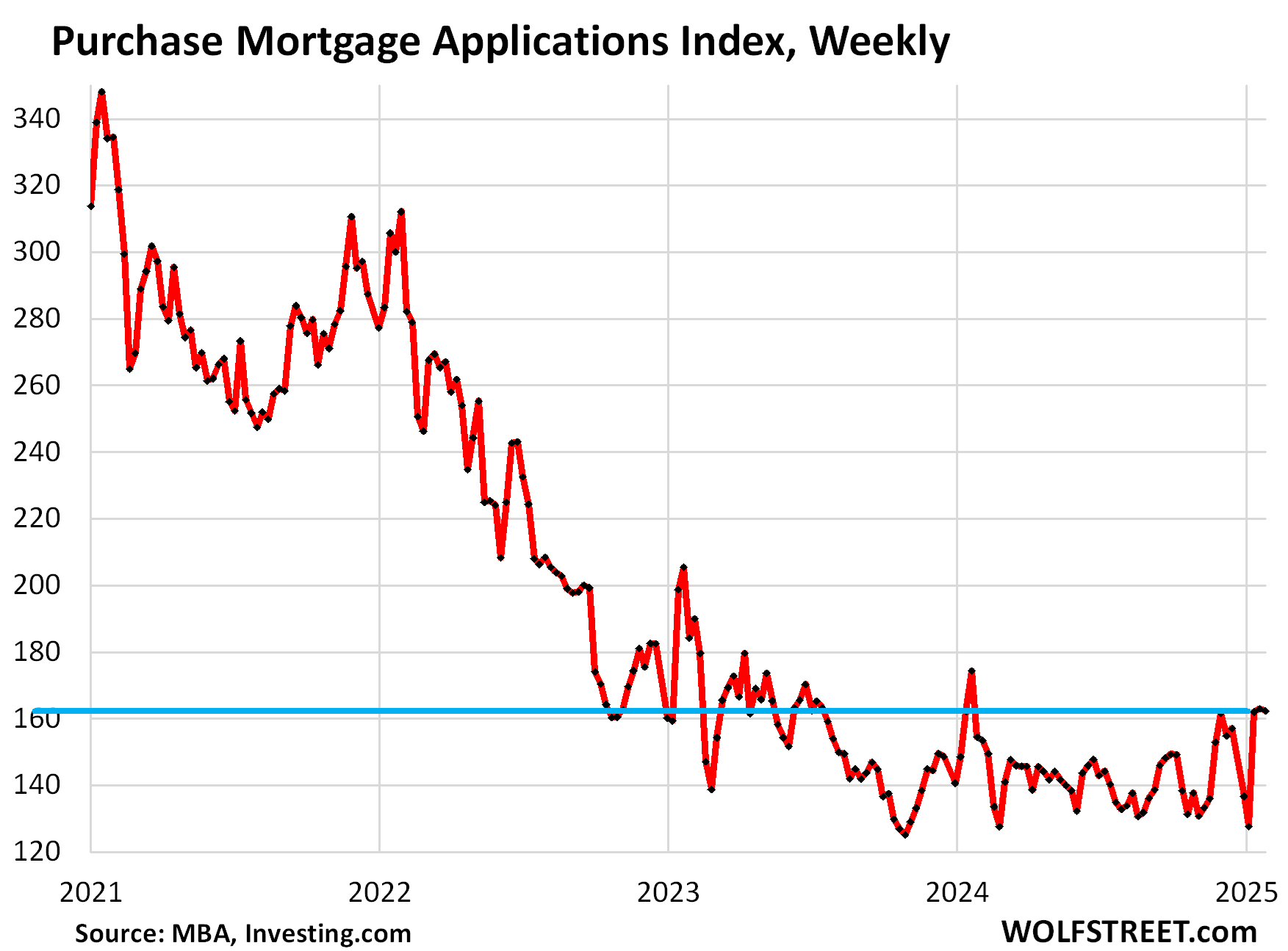

Applications for mortgages to purchase a home, after closing in on the prior lows in November, ticked up a little in December, seasonally adjusted, and in January stayed there, still down by 48% from January 2019 and from January 2021, according to the weekly index of purchase mortgage applications from the Mortgage Bankers Association.

Mortgage applications are an early indication of home sales: like pending sales, up only a smidgen from rock bottom:

Prices have started to decline in many cities. But in some cities – we only track the biggest cities here – prices of single-family houses and/or condos have come down from 9% to over 20%, dropping to levels first seen years ago, for example, in Austin, Oakland, New Orleans, San Francisco, Washington D.C., New York City, Detroit, Seattle, Portland, Tampa, depicted in lots of charts: The Big Cities with the Biggest Price Declines of Single-Family Houses or Condos from their Peaks: From -9% to -21%

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I just purchased a duplex in Minneapolis around a month ago. It was probably 10% off its all time highs but still cost me over 300k. It’s kind of amazing how crappy these 1900 – 1960 duplex are, they they are still selling for 300, 400, 500k. These are the types of houses that would have sold for 20 grand back in the 80s.

There really is a point where it is better to,

1) rent,

2) move to another metro

Obviously everyone’s situation is unique (family size, job situation, level of savings, age, etc.) but writ large, having housing prices double/triple nationwide since 2000, when median incomes did nowhere remotely as well, was always going to be a recipe for disaster.

The paper illusions of ZIRP were the only thing making it possible.

Those 80’s duplexes are 15x to 25x the 80’s prices you site.

There are essentially no sustainable financial rationales that could possibly justify such a price rise – either Minn adds more supply (and isn’t Minn one of the leaders on looser zoning?) or an exodus out of Minn starts…just like the SF/SJ/LA exodus (which was hidden for a while due to *birth* rates netting against adult migration rates).

but writ large, having housing prices double/triple nationwide since 2000, when median incomes did nowhere remotely as well, was always going to be a recipe for disaster.–

Right on

re above comment…the “theme/topic strip” on the left margin helps…but it is so broad, it doesn’t help a bunch in terms of tracking particular data sets/charts from month to month – too many posts get returned as hits.

if it’s crappy, why did you buy it? why not rent.

Hi Franz – I bought it as an investment property. It meets the 1% rule so it’s still has positive cash flow.

I bought my first house at 1208 como Avese minneapolis in 1980. 500sf piece of crap. I got a good deal at 30k with 5k down and a 5 year contract for deed with balloon from the seller for financing. 12% interest which was a good deal. I then bought a duplex on e 25st by the art Institute. In ok shape but needing some up dating. 65k which was a good deal. Then another on Pillsbury Ave so for 85k. That was a gingerbread Victorian. Not sure where those 20k duplexes were. If so they were burned out hulks. Best of luck on the 300k find.

There in a Nutshell is the problem. Rediculous home price. Positive cash flow

The housing market needs a major crash before anything is going to change. Houses are no longer affordable for people who want to buy and the houses that are on the market are so overly priced nobody can afford to buy them unless you have 3 or 4 incomes in the house and no life to live

Could you really buy a move in ready duplex in MN for $20K?

In 1984 a low end Camaro cost $10K and a new Corvette was just over $20K.

For most of my life the price of a Corvette has lined up with what the average skilled blue collar guy (plumber, electrician, etc.) makes in a year.

I’ve been involved with real estate since the early 80’s and it has been rare for the price of a rental unit not needing a TON of work to ever be even close to the price of a new Camaro.

we paid $83 for nice duplex in ’94

we get offers in mail every day in low $200’s

but listed are in the $300 range

5% ROI maybe isn’t what I say is a deal

I ended up buying houses instead-fixup so I ADD VALUE

I paid 65 thousand for a single family in Minneapolis in 85.

20k might be low. Looking at the price index the average house price was between 50 to 60k in the 1980s. So 20k might have been findable, but that might have been more of a 70s price. Either way. For a wood frame house with very average construction material….as Wolf says, the price are way too high.

Redfin has a 1,400sf Duplex in Palo Alto on the market for $2.6 million that is WAY overpriced, but I think @Amon-Ra will do fine with his $300K duplex if it was even close to move in ready. There was a lot of inflation in the 70s with many homes in the Bay Area going up 5x from 1970 to 1980.

A new Corvette starts at a about 80k with taxes. A plumber makes over 100k in the Seattle market, and can be much mor than that if they work their own business instead of for another company.

I bought my first house in St Paul in 1977 for $39,500. I had friends buying duplexes in S Minneapolis and they didn’t sell for $20 grand then or in the 80s. Why do these “crap shacks” sell for the prices you mention? It’s the land value, i.e., location, location, location. Buildings depreciate but land does not. And, land is a good hedge for inflation.

You bought a duplex (which means an opportunity to offset your mortgage with rent) for $300k

That’s a much better deal that Boston, Denver. Miami, Seattle, Austin, And dozens of other cities where $300k won’t get you a 3BR

Yeah somethings not right, too many people r greedy

Just a thought experiment, I wonder what would happen when you calculate the prices of the average/median income growth of the middle and lower class over the past 20 years then overlay a graph of how much prices of consumer goods increased and then overlay a graph in comparison to average house price. What would the result be?

1. You’re looking for a housing affordability index that factors in local home prices, interest rates, local wages, local insurance costs and property taxes. The Atlanta Fed has an interactive affordability tracker where you can select the location. I have zero interest in that. But go look at it over there.

2. You’re looking for “real” household incomes (incomes adjusted for consumer price inflation). We do that here occasionally when we discuss inflation-adjusted income and spending, including here:

https://wolfstreet.com/2024/09/27/consumer-income-savings-rate-were-revised-massively-higher-going-back-2-years-spending-revised-up-too-stunning-numbers/

Dear @Wolf,

You said this – The Atlanta Fed has an interactive affordability tracker where you can select the location.

*****I have zero interest in that. But go look at it over there.*****

Why do you have zero interest in that ? It seems like a useful way to see if homes might be affordable or not.

There is a nearly unlimited number of things I have zero interest in as a publisher.

I think the results would still be cyclical.

But still wreaking havic on these buyers continuing to making homeownership out of reach. It would probably be better to track this just in the past year, because of the effect, the lawsuits against NAR affected the industry. Buyer agreements required for a buyer to pay their agent before they even walk into a property.

Just putting more pressure on the buyer which they don’t need at this point.

In December UWS Manhattan 1bd 680k.

Wolf, considering maintaining Manhattan focused index.

Can you index the Philadelphia area

All you have to do is read it when I publish it, which is on the 12th of every month:

https://wolfstreet.com/2025/01/12/the-most-splendid-housing-bubbles-in-america-dec-2024-in-21-of-the-33-metros-prices-have-now-dropped-below-2022-peaks/

Along these lines, is there a page on site linking to those topics you monthly/periodically update?

Having such a page would save you from having provide an endless array of one-off links, and your readers from having to resort to customized Google searches.

I’m pretty sure you’ve been migrating somewhat to a fixed list of systematically, periodically updated topics/charts (makes a lot of sense from an administrative point of view).

But it would help if the site made a road map available reflecting that.

The narrative in SoCal now has shifted to fire victims are now scrambling to buy and rent, therefore driving up price and demand in OC and surrounding areas.. Guess msm is trying to drum up the frenzy in this neck of wood.

Who knows, maybe there’s a grain or whole celler worth of truth in that, at least for now they can still claim price is holding high so demand must be there…FOMO all day everyday here

Interesting fallout from the Cali fires; such as the revelation nearly half of the fire engines were out of commission (100 out of 183) at the time of the fires — reason; Private Equity firm consolidated fire truck manufacturers with consequent price increases and parts shortages….

There has been quite a bit of talk of deals falling apart or getting canceled because buyers cannot afford the homeowner’s insurance, or cannot even get it.

—

IMHO the entire insurance industry needs to change

just like govt FLOOD insurance, catastrophic insurance now needs to come from govt(I’m here to help remember)

—

ouch- I bit my tongue

—

however in that way insurers can insure property for normal reasons

burns down due to electric fire – paid, burns down due to forest fire, -govt paid with 30% deductible of course

It’s simply unfair to ask the entire population to provide deep subsidies for properties that, by definition, only a portion of the population can occupy and enjoy.

https://insurancenewsnet.com/oarticle/taxpayer-subsidizing-of-flood-insurance-unfair

Private equity is a cancer that is spreading across America. They’ll wring every last dollar out of everything.

It also is what is driving up housing costs with all these REIT and partial ownership investments. As far as homes too expensive, people are going for relative value and with the cost of materials amd labor where it is to build new shelter that is lower quality in general than older homes the need for shelter keeps prices high.

The aformentioned investment groups also target low end housing artificially raising rent rates through marketshare leverage.

We moved from SoCal to Savannah 6 years ago. Love Savannah (downtown), the Deep South not so much. We had planned to move back to SoCal this spring/summer – family changes and we miss friends, sunsets over the ocean, topography, etc. – but with the fallout from the fires jacking up rents, I’m afraid that ship has sailed for the time being.

I’ll keep hoping for better times, but as a wise man once said: “Hope is nothing more than unrealized disappointment.”

Master P always called it, “The Dirty South”; consequently, I still do.

@Phoenix_Ikki I have a friend that lives in Suburban Irvine who has lived next to a realtor for years. He just told me that the guy told him there is now crazy demand from people that lost homes knowing that there is no chance that they will be able to rebuild any time soon (or afford a place in Santa Monica or West LA). At the end of 2024 I read that only 10% of the homes that burned in the big 2020 Santa Cruz Mountains fire had been rebuilt and it is WAY more of a nightmare to build anything in LA County (I just read yesterday that LA wants a huge number of apartments rebuilt as “affordable” apartments)…

Yeah I don’t doubt this…funny how many people still ignoring long-term risk of SoCal as if OC is some disaster-free paradise, free of earthquake, weather, and fire risks…

Then again, I can imagine a major earthquake literally rip open the ground and people will be clamoring to build right by the fault line…

@Phoenix_Ikki I live in a ~100 year old home just a couple miles from the San Andreas fault surrounded by hundreds of other ~100 year homes that are even closer to the fault and in the past 100 years none of the homes in the area have had any major damage caused by earthquakes (The guy I bought my home from showed me where he had to to some plaster repair in one place after the 1989 Loma Prieta earthquake). Few well well designed wood frame homes have any problems with earthquakes since CA bacame a state in 1850 (all the apartments with tuck under parking that collapsed after the 1994 Northridge earthquake were poorly designed).

There are not a lot of fully risk free areas to live in (just ask the insurance companies). SoCal has the draw of amazing climate and a lot of people don’t want to give that up. The also have friends and family here, which is hard to walk away from.

And then there’s jobs.

ApartmentInvestor

Mostly agree but… “there is now crazy demand”

Why does anyone still believe anything a Realtor says about housing? “…there is now crazy demand” is the same copy-and-paste bullshit propaganda they always say. Your friend is an idiot for listening to this Realtor and spreading his propaganda.

@Wolf Realtors as a whole lie almost as much as Used Car Salesmen and Politicians but when Google says “In just a single month, 2025 is the second most destructive fire year in California history, with more than 16,000 homes and other structures damaged or destroyed by two fires in the Los Angeles area” I’m pretty that some of the owners of the 16,000 properties are calling Realtors aka “Used Home Salesmen”. Most Realtors will ALWAYS tell you there is strong demand and it is a great time to buy and sell, but just like a broken clock is right twice a day Realtors really did have strong demand in Covid when more people wanted space to work from home and I’m guessing (with tens of thousands of people without a home) that demand really is up in LA/OC.

ApartmentInvestor

Data from Realtor.com, through Jan 25: pending sales (homes put under contract in January) plunged in January, and listing price per square foot fell further. That’s the data. The fire started Jan 7. What the Realtor was telling your friend was propaganda.

And it makes sense because wealthy people now usually have multiple homes, and they’re not going to look for anything right now in the area; they’re living in one of their other homes, and are trying to sort out this tragedy and fight with the insurance company. And others that don’t own multiple homes are also fighting with their insurance companies for a settlement, and they’re not buying anything – and many cannot buy anything – until they got the cash, and sold the lot, so that they can pay off the mortgage, and then buy something new. This process takes quite a while. And there are others that have had it with the risks and costs, and they’re leaving the area entirely. And that’s what you see in the data for January already.

Between waiting on an insurance payout, waiting months for approved building permits, and then trying to find contractors to build a house in the burned out lot you have, it will be years before people are back into their own homes again in these burned out LA geographical areas.

I heard from someone in pacific palisades that the owners in that neighborhood are mostly committed to rebuilding, and they are expecting a timeline of 5 years or more to rebuild. Those are people who have options though. They can rent in other cities while they wait on insurance, building permits and construction financing. Most others likely cannot follow suit. I would expect a large number of permanently displaced residents to emerge in the coming months.

I feel like that is all BS because look how many were displaced. 10,000 structures burned and that includes non living places like schools and businesses or garages. Let’s assume 7,000 families were displaced. La county is 12 million people and the city of LA is just under 4 million. That represents 1/10th of a percent of LA and even less for county. I smell greed. The surrounding Brentwood, Santa Monica neighborhoods might experience price hikes, but i live in Long Beach. Nobody should be talking about that anywhere close to here.

The housing market needs a major crash before anything is going to change. Houses are no longer affordable for people who want to buy and the houses that are on the market are so overly priced nobody can afford to buy them unless you have 3 or 4 incomes in the house and no life to live

It feels like the writing is on the wall

Are houses in the Mountain states (CO, ID, etc) in the West data or the Midwest data? I re-read the article twice to see if I missed it.

They’re in the West

I think MD belongs in the North and PA belongs in the South.

I think TX and OK belong in the West. If you go out into West Texas or western Oklahoma, and especially the Panhandle, there is nothing South about it. It’s West all the way through. If you draw a line going north, from just east of Dallas to east of Tulsa, everything on the left of that line is clearly the West, including Dallas and Tulsa.

Those two states are often called the Southwest. And that’s a better fit.

But these are the Census designated regions, and good luck trying to argue with the Census about it.

If we’re going down that road, ‘old timers’ in Florida used to say everything north of a line between TPA and Daytona was actually LA, meaning lower Alabama!

Everything south of that line being Florida,,,

LOTS of folx in that LA were happy to tell all about their grandparents walking down there from AL in the 1800s…

and BTW, having driven through TX and OK many times, I agree w WR about their western parts being the very epitome of ”West.”

Vintage- there is actually a (very small) movement in South Florida to draw that line and split the state into two – South Florida and North Florida. I have lived in both parts my whole life and while Jacksonville has many features that scream “south Georgia” I am a Floridian through and through.

FL and TX seem to have the most available inventory right now. Hint hint first-time buyers: perhaps you should move there instead of bidding up homes in the frozen tundra known as the Northeast.

Short, hint…they are coming here. I have new neighbors (families) from California and Denver, Colorado. (North side of Houston – Montgomery County)

People want it all. They want to live in an unaffordable place so they can complain about how much things cost. They also want an affordable house in the same unaffordable place so they can have money for spending.

There are affordable places to live in the US, with good paying jobs, but it’s not “sexy” to live in some of those places. The glitz and glamor will always attract people. But if we didn’t complain about our first world problems, then we wouldn’t be human. But because we’re human and live in a first world country, we will continue to complain.

You sound like you live in an affordable place and have spending money. Did you buy before things were outrageous?

Short,

They are coming here to our little hood that did not flood at all in recent ‘canes in the saintly part of the TPA bay area:

Young folx,renting down the street for years, just scored a fixer across the street for $200K PLUS two months of getting years of stuff from hoarding out, PLUS a couple months reworking the place to suit, mostly their own labor so far, but other neighbors volunteering their skills also.

Most sales of older 2/1 houses going for land value…

Three new houses under construction, MUCH bigger, two sold the day listed, the 3rd built by GC to move off the beach. 4th just demo’d the lot that sold for $275K day it was listed.

Duke actually undergrounding the power to the new places, and apparently going to do the whole hood sooner and later…

Currently nothing for sale or rent in this hood.

“Most sales of older 2/1 houses going for land value…”

Would be nice to see that around here.

I saw the chart about more homes for sale this past December than usual. Oddly, in my town in MD – or at least the few neighborhoods I keep tabs on – there was nothing for sale for all of December (well, one sort of crappy place on the fringes that went pending in January). But perhaps that is because those homes belong to wealthier people who aren’t in a rush to sell and figured December was a bad time to try?

An expensive one popped up early January and went pending that weekend, with one of those belligerent listings that give an offers deadline.

Let’s face it. First time buyers who have no equity in a prior residence will be hard pressed to fund both a down payment and closing costs. Many are still stuck with school loans (I know, I know they should have thought first before taking on that massive debt). I don’t see any way out of this mess without house prices declining significantly.

i’ve wondered how many buyers are just trading up or down these days, given that volume has collapsed by what 40%?

I love your analysis articles. Really great share of statistics. I have been saying for years that rates will go up and the locked in would happen. No one listened to me. I have only a minor in economics and an MBA. I’m a bit worried because if my calculations are correct I will find myself about 100k upside down on my house next year. Military moves have forced us into markets where buying was the best option but we can never time the market correctly. We end up splitting our family up to do so each time so we have come out ahead but I am seeing a market correction in the next year. Trump did say he would make home prices more affordable. Sadly I don’t think people realize the strings being pulled that will do that is going to stiff most of us. As inflation rises the Fed will stick to the high rates (despite the fact that part of the number for inflation is cost of housing! Circular reasoning madness) but he has to stay strong on the interest rates or the risk is the dollar weakens. So in the meantime people are going to get squeezed out of ownership. Wall Street will gobble up the homes unchecked. Then Fed Chair will get axed. He will also be replaced by a yes man that will drop rates. Inflation will spike even higher from tariffs. This will weaken the dollar. Then they crypto crowd will push even harder to flip to a crypto currency. We will hit hyper inflation and the rich will simply transfer their money into crypto while the rest of us will have dollars now worth 30 cents trying to buy eggs for $30 with no home equity no borrowing ability and stagnant wages. We will be a docile group to rule Then.

The ATF estimates there are over 500,000,000 firearms in the United States owned by citizens (non-military). That number definitely includes antiques and non-functional guns, but even if you cut the number in half, there are likely AT LEAST 250 million fully-functioning weapons available to the hoi polloi. My household has six.

Do you really think such a well armed populace is just going to sit idly by and let the oligarchs take total control? If (when?) it gets to that point…

@SingleMaltScotch

If the propaganda from said oligarchs is successful in shifting the blame away from them and toward another segment of the working class, then the oligarchs will be successful as Candice N suggests. It’s been working for them so far.

Take out college loans in hope of getting a job paying enough to buy a home, or avoiding that cost and knowing that it’s unlikely that you’ll ever be able to buy a home. Decisions, decisions.

As to home prices – people don’t like selling for a loss, or overpaying for a different home better suited to their needs. So, prices remain high.

If that was the calculus, everyone would be in STEM studies. I’m in undesirable flyover land, but most of the successful people I know are business owners in trades-related fields.

Just wait for this AI nonsense bubble to pop…double your figures across all levels…possibly the fed buys stocks verses bonds to keep the bubble alive…no company is worth a trillion dollars, but 3 trillion..rubbish…propaganda.

Can housing prices fall below the cost of building them? Prices don’t seem to have much downward price flexibility.

1. Look at their profit margins: there is lots of room for prices to fall before builders are running negative gross margins.

2. Builders did run negative gross margins during the housing bust. Lots of them keeled over. Same as anywhere.

3. Costs of materials have plunged, but new house prices haven’t plunged, they just dipped a little.

Rule of thumb for home builders was 1/3 for cost of land/infra; 1/3 cost of construction; 1/3 profit margin/soft costs.

So, when you read Wolf’s analysis of new home builders subsidizing the sale/mortgage, you know how that subsidy is built into the pricing.

My Seattle suburb neighborhood of $2M older homes, $950 sq/ft, is turning into a rental community. sales transaction volume has dried up to practically nothing. Some people are moving out to change location, including those entering the spirit world, and their homes are put up for rent.

I find this odd because the cap rate is about 1% in my neighborhood. There must be stubborn owners out there who favor RE no matter what, even when other investments offer much greater yield. I don’t think the typical MaPa real estate investor in my area has broad financial knowledge. They don’t recognize that prices are abnormal relative to rents.

Several older residents have complained that the neighborhood is turning transient.

People don’t want to sell because they believe real estate will continually return 10%+ forever. This is just a blip due to high interest rates. The general public, including many well educated upper middle class people aren’t that financially literate.

Anytime inflation has breached 5% it’s taken on average 10 years to go back to 2% so expect interest rates where they are plus or minus 1% for a decade or so.

Rents are starting to fall. Down 5% yoy in CO. So that will decrease the value of houses as rental properties.

Return to office, many people who ran up prices are having to move back hcol cities.

Travel normalization – we had a large increase in airbnbs in 2020 and 2021 and now we’re seeing a decrease in demand for them. This means falling prices and less nights booked. Not to mention increasing property taxes and insurance.

The cards are all stacked for a decrease in prices. Just needs some sort of triggering event. But then again the govt will probably freeze all mortgages or print money to prop up prices. So hard to say.

@Bobber I don’t know the rent in your neighborhood but I’m betting that a family renting a $2mm 2,100sf home is getting more than $1,666/month after expenses (more than a 1% cap rate). I’m sure that cap is low and it was low when a friend moved to his family from the Bay Area to CT about ten years ago. The home he bought for ~$500K in the 90’s was worth about $2mm and we got $4K rent since I managed it for him in case the job didn’t work out and he moved back. Today I still rent it (for $6,400/month) and Zillow says it is worth just over $3mm. A low cap rate but my friend is not in a hurry to sell it

The cash flow in my area is negative right now on the typical $2M home. Assuming current home prices, 20% down and a $1.6M mortgage, you get the following annual expenses:

Mortgage interest $110k

property tax $15k

Maintenance $5k

Insurance $5k

So we are looking at annual expenses of About $135k to derive $48k to $60k of rental income.

The return is cash flow negative. If the price of the home drops, salt will be rubbed into the wound.

Investing in rentals in my area is extremely risky. Buyers are depending on 4-5% home appreciation just to break even.

Wolf, I am curious what you think of peoples decisions to purchase in this environment. People need homes and have many reason why they want to buy. Assuming that there is an ability to purchase, should people be buying any real estate at this point? Is it possible that we will just hobble along like this for many years while inflation eats away at the price increases and wages just catch up? And what of the tariffs. For example here in California we just had massive fires that now require rebuilding of thousands of homes just as Trump is set to tariff Canadian imports, which would include wood necessary for building, which would drive up cost of construction. To me that would indicate that prices would only stay elevated as there is a home shortage combined with rising cost of building replacement or new units.

1. in terms of buying a house: I always say, if you need to buy a house, rather than rent a house (need because your significant other is driving you up the wall or whatever), and if you can afford the down-payment and the monthly payments, the insurance, property taxes, etc., and can even afford them for a while if you lose your job, and if you’re going to live in that house for many years, sure, buy a house. Just understand that a house is an expense, and that you can lose lots of money in RE very quickly because it’s highly leveraged. So if house prices sag for years in your city, just stay put, make your payments, quit looking at Zillow every day, and go on with life. And after 15 or 20 years or so, even if home prices sagged a lot in your city, you may have made enough principal payments to where you can sell your house and pay off the remaining mortgage with the proceeds.

If you want to buy a house for a rental, you better know what you’re doing.

2. In terms tariffs on Canadian lumber: the US has LOTS of timber and is a HUGE lumber producer. Logging is a big business here. You city boys need to get around a little, and you’ll see. Or you can just look down from the airplane, and you’ll see too, just like you’ll see the fracking sites carpeting the land.

And the US is also a big lumber exporter. In 2023, the US exported $38 billion in forest products, $10 billion of which was exported to Canada, LOL.

The US also imported $51 billion in forest products, including $20 billion from Canada. So the US had a forest products deficit of only $13 billion (exports minus imports), and its forest products deficit with Canada was only $10 billion.

So the tariffs will shift more production to the US, and Canada is going to lose some production, or its producers will cut their price to compete, and in that case, Canadian producers eat the tariffs.

Until prices come back down to $250-300K, nobody is going to buy them. Anything more than for a 3 bedroom house is over priced. I don’t give a crap where it is. I can get beach front property in a nicer, cleaner country for less than $100K. Why the hell would I waste $400k to live in a shithole like Los Angeles.

$400k for a shithole in LA would be a steal.

Americans expatriating for retirement seems like a trend worth keeping an eye on.

If it were me, I’d probably look to Mexico, particularly Jalisco. There’s lots of facets to consider beyond just the cost of housing though. I think.

It appears as if the chart displays the interest rate, rather than home prices, as when I purchased my condo in 2020 (just before COVID), I made a sizable profit selling it in 2024, just four years later (to an investor who clearly didn’t understand the upside down market). I purchased the home before 4%. However, with the base price increase, as well as the 6.5% APR now, added to the increase in prices.

When I purchased the condo, the price was $210k. The investor purchased it for an extremely low $250k, and tried selling it for $320k. It’s still on the market—$293,800