Sales of new houses in 2024 were decent, while massive demand destruction crushed sales of existing houses because prices are way too high.

By Wolf Richter for WOLF STREET.

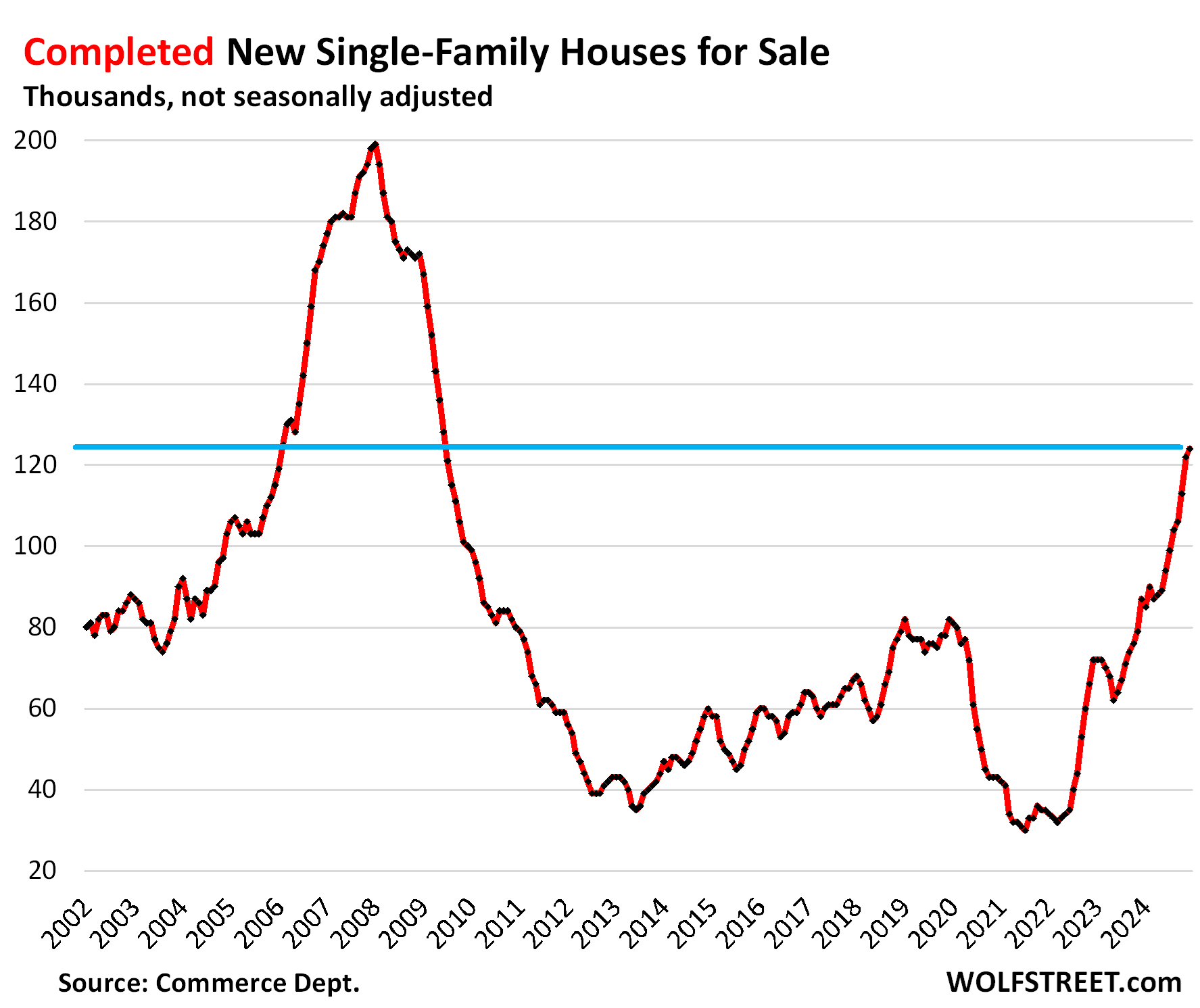

Bring on the supply of new houses: Unsold inventory for sale of completed new single-family houses has spiked by about 50% from the peaks of 2018 and 2019, and by nearly 50% year-over-year to 124,000 houses in December, the highest since June 2009, according to Census Bureau data today.

Homebuilders need to sell this inventory of “spec houses” quickly because they’ve sunk a lot of capital into it, and because they’re continuing to build at a faster clip than they’re selling them because they want to run growth-businesses and please Wall Street, thereby adding to the pile on a monthly basis.

But they’re also selling them at a robust pace by motivating buyers with lower prices and huge incentives, including very costly mortgage-rate buydowns, that eat into their still fat profit margins. They obviously haven’t done nearly enough to trim their inventories that continue to balloon, and they’ll have to bring prices and payments down further to stimulate more demand.

The current surge of completed, move-in ready inventory of spec houses for sale is good news for the overall housing market, whose biggest problem is that existing homes are now way overpriced, after the 50% price explosion between 2020 and 2022, on top of being already overpriced before.

This surge of completed inventory for sale should help brush aside the zombie-like undying real-estate hype about the “housing shortage,” that has been spread for eons by the real estate industry and its trolls in an effort to keep driving up prices.

And that lack of “affordable” existing homes, after the ridiculous run-up in prices, can be fixed by the collapsed demand for existing homes, whose sales in 2024 plunged to the lowest levels since 1995. There is a buyers’ strike in effect because prices are way too high. And lower prices will bring out the buyers.

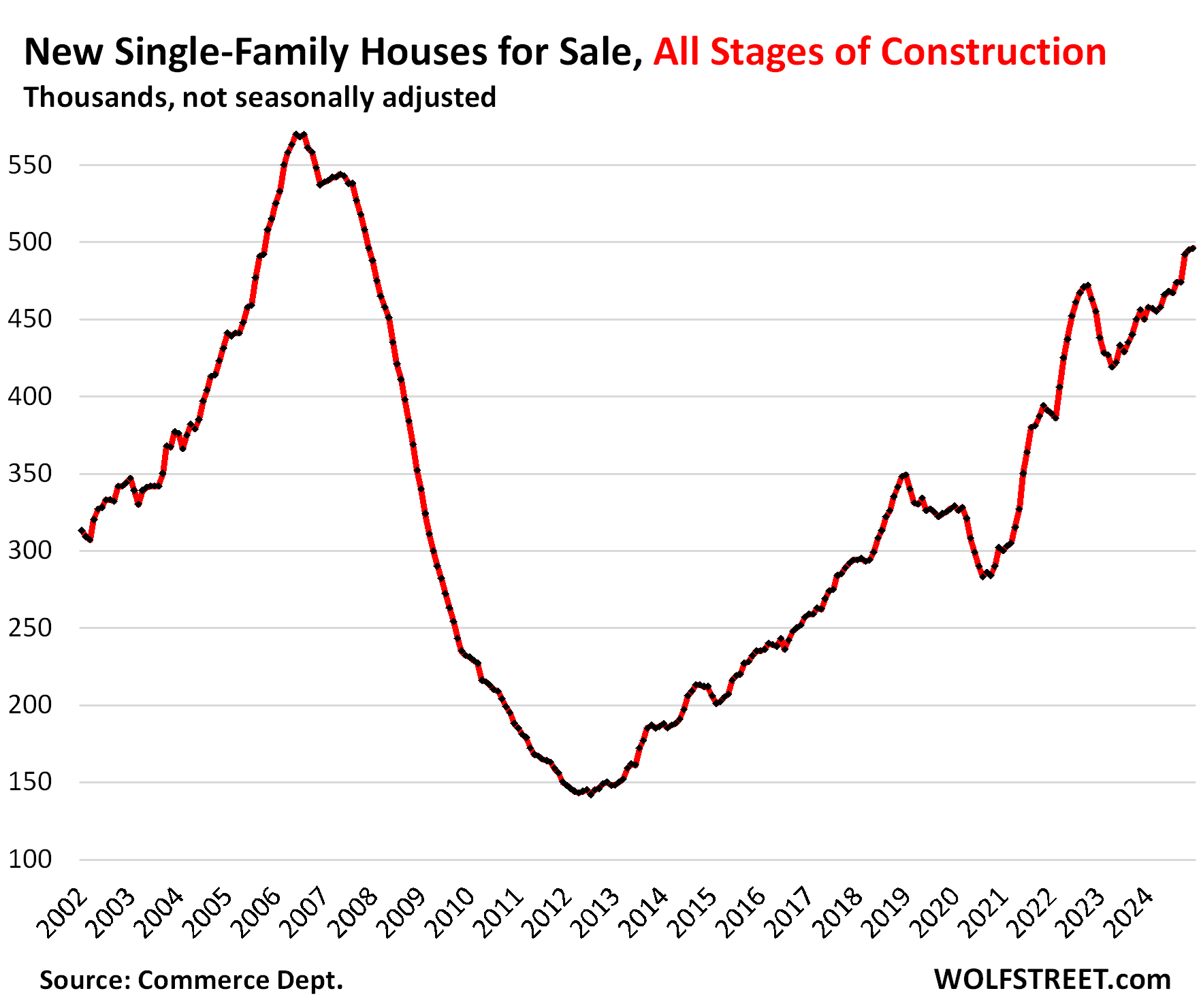

Unsold inventories for sale at all stages of construction – from not yet started to completed – rose by 10% from the already bloated levels a year ago, to 496,000 houses, the highest since December 2007. Supply jumped to 9.4 months.

Stimulate demand with lower prices, bigger incentives, smaller houses.

Big publicly traded homebuilders have to build and sell homes regardless of the market because they have to keep their businesses intact and growing, and they have to please Wall Street to keep their shares from tanking.

So they’re building smaller, less costly homes, and they’re cutting prices, and they’re making deals, they’re buying down mortgage rates, and they’re throwing in other incentives at a substantial expense to them to maintain sales volume by taking share away from the resale market.

The costs of the mortgage-rate buydowns and some other incentives are included in the gross profit margins of the home builders, and are therefore reflected on homebuilders’ financial statements.

D.R. Horton, the largest homebuilder in the US, in its Q4 quarterly filing with the SEC on January 23, lined out its strategy in dealing with this market: higher incentives (including the costs of mortgage rate buydowns), lower prices, and smaller houses. As a result, its operating margin and net income dropped, but sales remained solid, down just a hair from a year ago, in this market where demand for existing homes has withered.

Its strategy of reduced prices, bigger incentives, and smaller houses:

“We remain focused on managing the pricing, incentives and sales pace in each of our communities to optimize the returns on our inventory investments and adjust to local market conditions and new home demand. To adjust to changes in market conditions during recent years, we have used a higher level of incentives and reduced home prices and sizes of our home offerings where necessary to provide better affordability to homebuyers. We expect our incentive levels to remain elevated, assuming similar market conditions and no significant changes in mortgage interest rates.”

So operating margins dropped:

“Our pre-tax operating margin was 14.6% compared to 16.1% [a year ago].

Net income dropped:

“Net income was $851.9 million in the three months ended December 31, 2024 compared to $955.7 million in the prior year period.”

And incentives were “elevated” and are expected to stay that way:

“We expect our incentive levels to remain elevated, assuming similar market conditions and no significant changes in mortgage interest rates.”

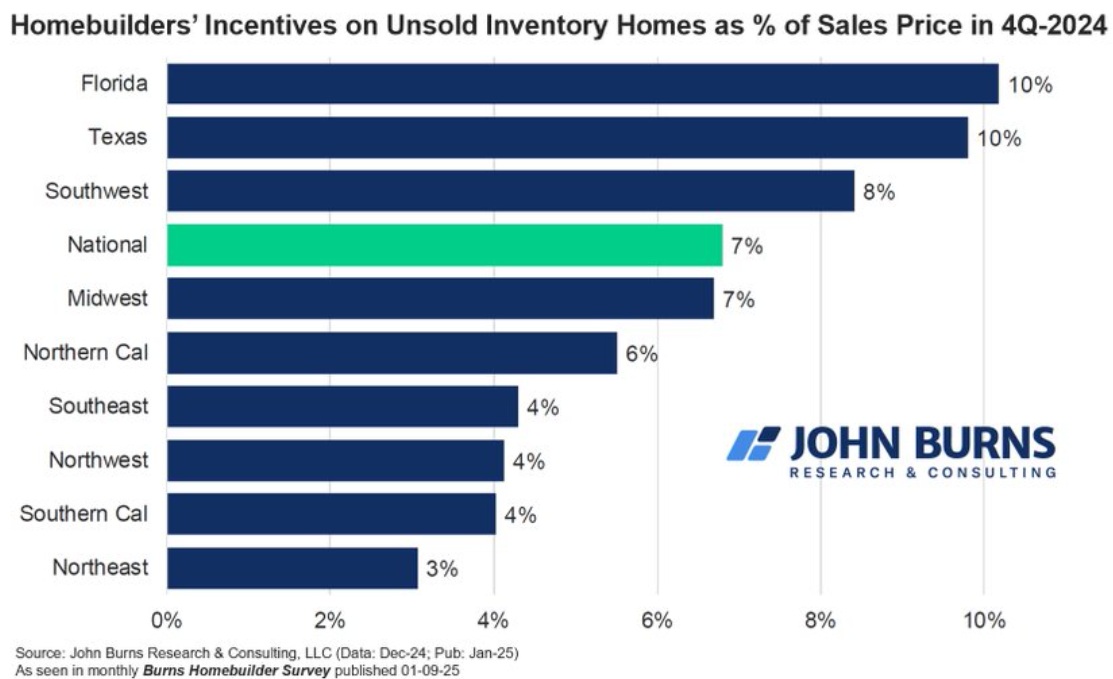

Total incentives that builders are offering on unsold houses for sale has reached 10% of the selling price in Florida and Texas, and 7% for the US overall, according to the most recent Burns Homebuilder Survey, of which Rick Palacios Jr., Director of Research at John Burns Research & Consulting, posted this chart on X:

But incentives are not reflected in the “Contract Price” of the house.

The costs of the mortgage-rate buydowns and incentives, such as free upgrades, are not reflected in the prices written into the sales contracts when customers buy these homes, though they’re included in the profit margins of the homebuilders, and discussed in their financial disclosures, as in the Q4 filing by D.R. Horton above.

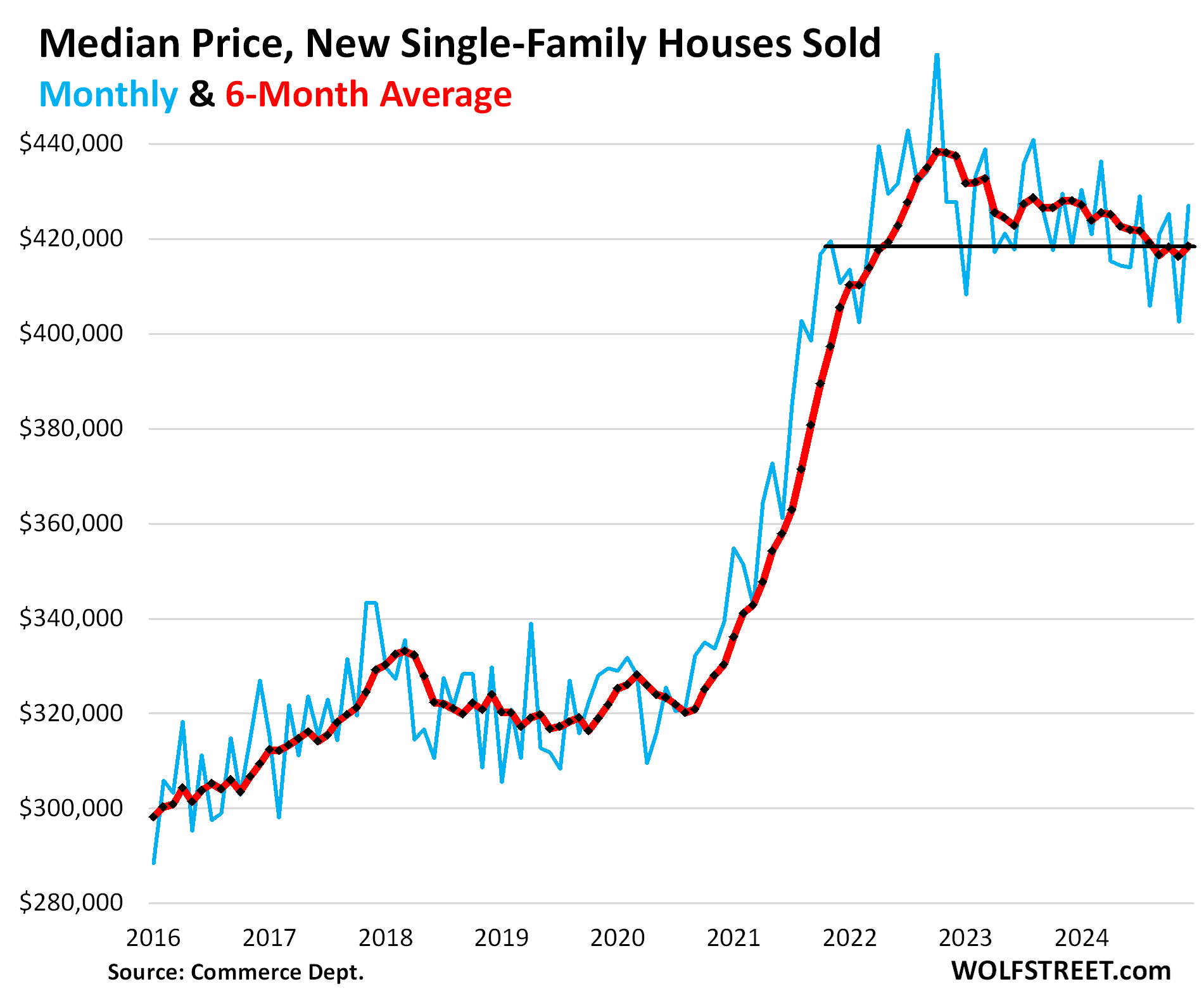

The Census Bureau tracks these contract prices, and while they have fallen quite a bit from the peak in late 2022, they do not include these incentives that effectively reduce the price of these homes, and with these incentives included, the median contract price would have fallen quite a bit further.

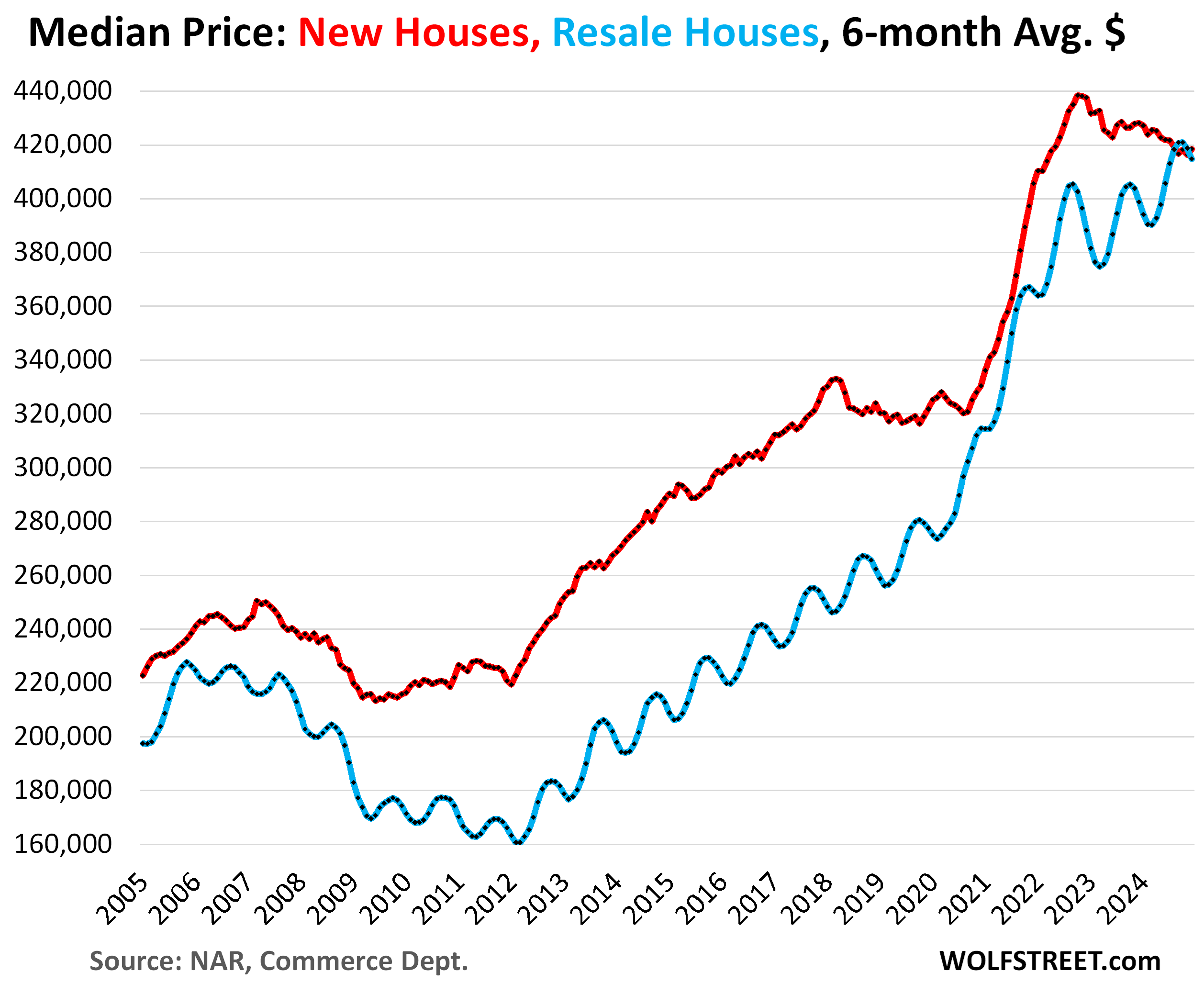

The median contract price of new single-family houses sold at all stages of construction – a super-volatile figure that jumps randomly up and down and is often revised sharply – jumped to $427,000 in December, after the plunge in November, and is down by over 7% from its peak in October 2022 (blue in the chart below).

The six-month average, which irons out most of the month-to-month zigzags and includes the revisions, ticked up to $418,450, down by nearly 5% from its peak in October 2022.

The six-month average shows the multi-year trend. But again, these contract prices do not include the substantial costs to homebuilders of mortgage rate buydowns and other incentives, though they do include price cuts.

Sales have been solid thanks to reduced prices & higher incentives.

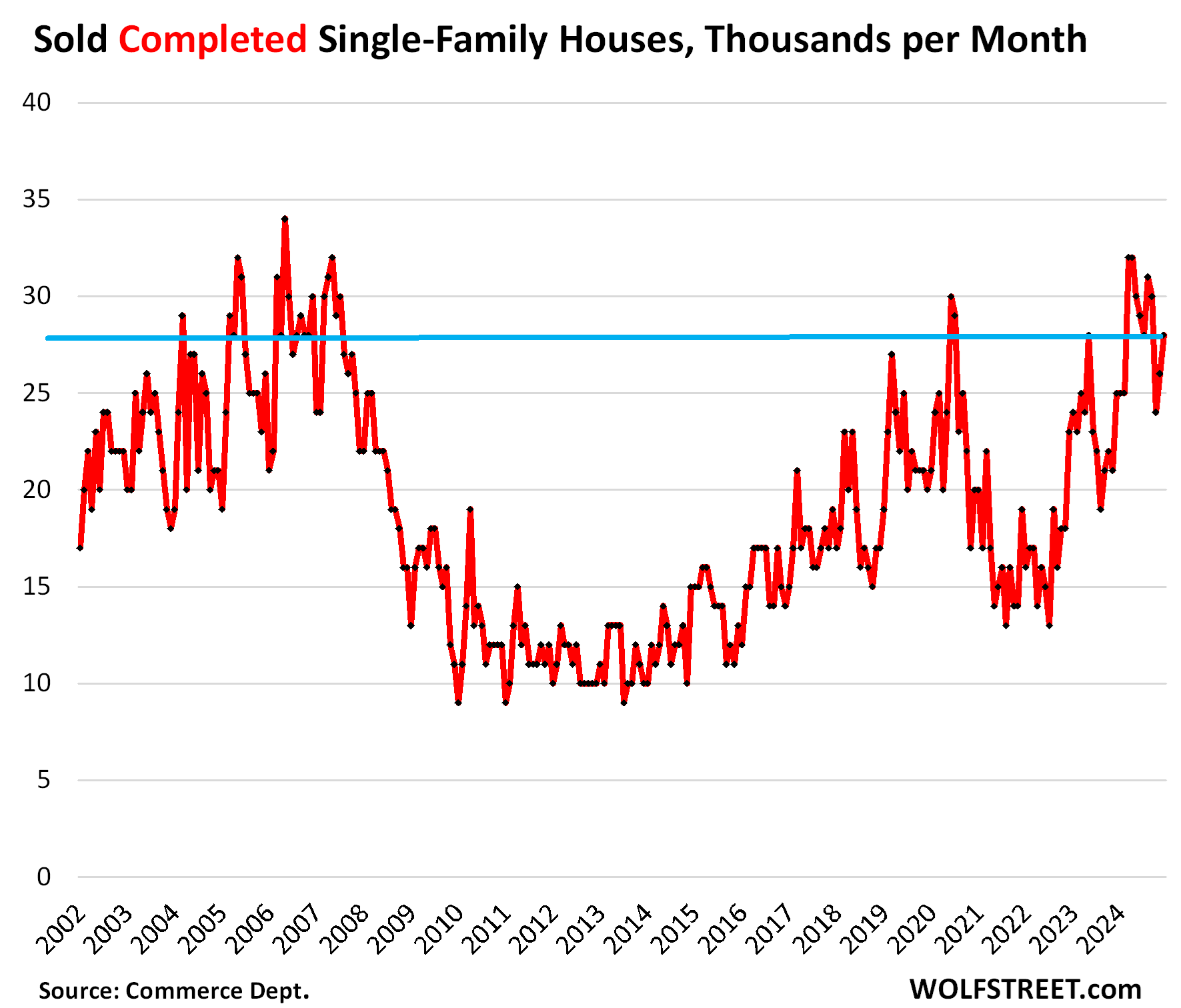

Sales of completed houses – propped up by incentives, mortgage rate buydowns, and lower prices – rose by 12% year-over-year in December, to 28,000 houses, up by 22% from December 2022, and up by 40% from December 2019.

Sales of new houses at all stages of construction, from not started to completed, rose by 6.1% year-over-year in December, to 52,000 houses, up by 12% from December 2019.

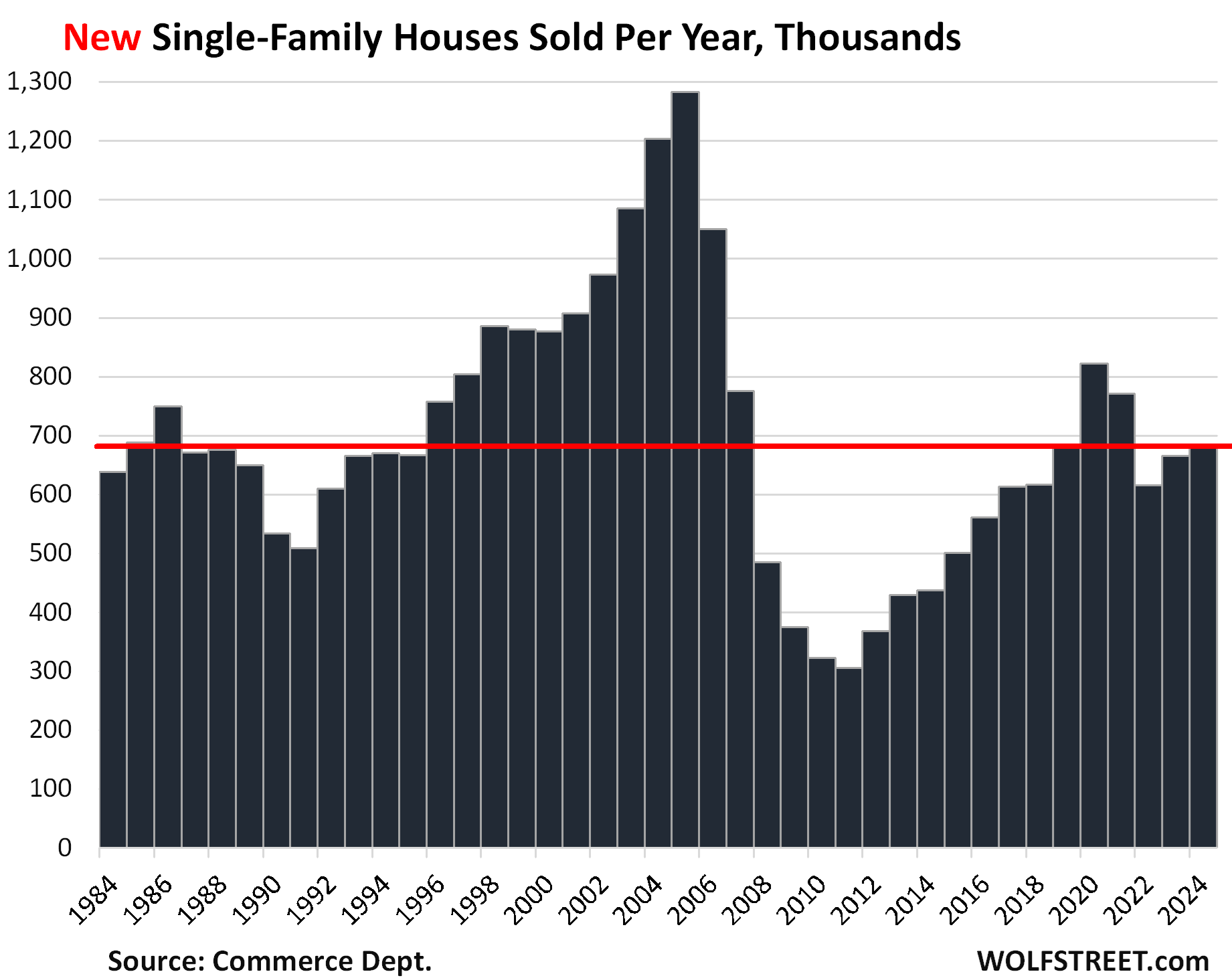

For the whole year 2024, sales of new houses have been decent, rising by 2.6% year-over-year to 683,000 houses, the same as in 2019, unlike sales of existing single-family houses:

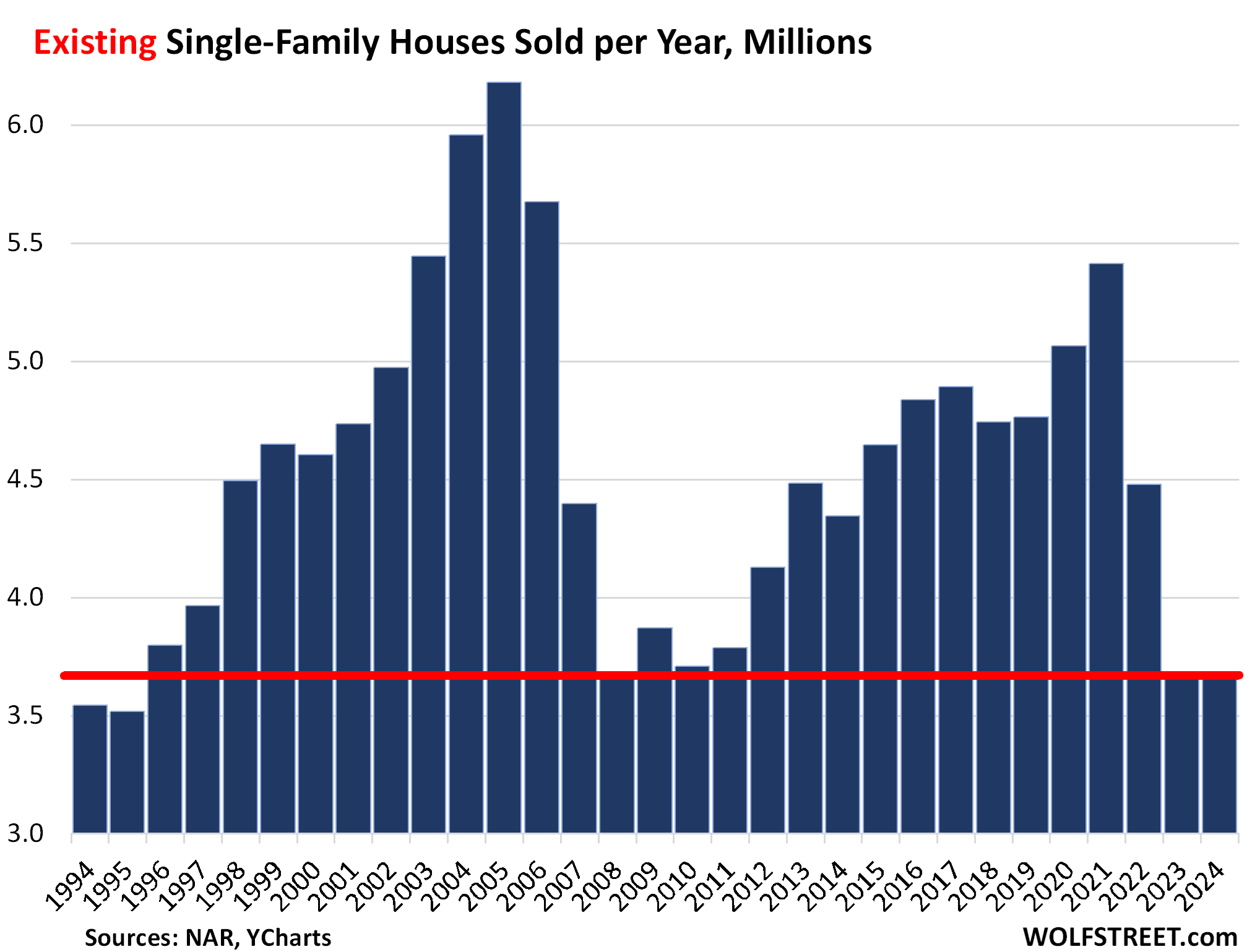

By contrast, sales of existing single-family houses in 2024 and 2023 plunged to 2008 levels, the worst since 1995 because prices were way too high, which triggered this enormous demand destruction.

Prices of new houses versus existing houses.

Over the past four decades, the median contract price (six-month average) of new houses exceeded the median price of existing houses (six-month average) all of the time, with new houses being usually 5-30% more expensive than existing houses. This scenario changed when the median price of new houses began to decline.

And for new houses, these contract prices do not include the incentives and costs of mortgage rate buydowns. With them included, effective prices are substantially lower than those of equivalent existing houses, which explains why homebuilders’ sales have been solid, while sales of existing homes have plunged, as some buyers shifted from buying existing homes to new homes.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Price fixes everything.

Yes. Anything can be sold, at the right price.

I am patiently waiting for this existing home price drop of which you speak. Hope I live to see it.

Likely to be a long slide. Sellers are attached to these prices, only the ones who are distressed are willing to cut prices. Some see the handwriting on the wall and are listing lower right at the start.

I’d bet we see big influx of homes at ridiculous prices in the spring and a bunch of those just sit there. NAR will blame interest rates and talk about how much appreciation they expect to see in 2025 (shorthand for “buy now before you are priced out”). By mid summer there will be deafening wails of interest rates killing the market and demands from the administration to lower rates, stat.

Meanwhile the distressed sellers who MUST sell, will drop prices until a buyer steps up. That resets comps and slowly drops expectations.

This may be a wash, rinse, repeat for a couple of years.

Oldguy,

In some big cities (I don’t track smaller cities), prices have already dropped by the double digits:

https://wolfstreet.com/2025/01/19/the-big-cities-with-the-biggest-price-declines-of-single-family-houses-or-condos-from-their-peaks-from-9-to-21/

Minus the inflation of the past 4 years and real prices have dropped quite a bit.

The stock market bubble popping will do wonders for you

i don’t see that happening. nvidia and some other tech companies got crushed, but investors “rotated” in staples like johnson and johnson, and unilever.

there are too many investors who think all money should always be invested in stocks for them to ever fall much.

“…for them to ever fall much” = “this time, it’s different” = most expensive four words ever.

i hear you, and i feel like all of my schooling is irrelevant, but what will it take to break this manic “buy the dip” no matter how bad the valuations?

The reality is that they have fallen and all signs point to them falling again and soon. No thanks from us, on housing or stocks. We’ll keep our money as long as it takes for the craziness to end.

C’mon man. Look at PE’s, look at total market cap to GDP. We are defying gravity here…sure, it can continue, it can go higher, but it can’t go on forever. Eventually, something breaks. Pretending we are under a new set of rules won’t make anything sustainable. Reality will set in, eventually.

blake, many of us have been awestruck by gravity not kicking in for several years now.

Franz, remember the saying “the market can stay irrational longer than you can remain solvent.”

“It can’t happen here.”

Not so sure if the 2025 tech stock market bubble pop would drop home prices. I would not count on it. In 2000 when the dot com bubble popped and Nasdaq lost 75%, home prices went up. I know a lot of people at that time who said they were swearing off stocks and were moving money out of the stock market and putting into a home.

Also, I just read that 42% of U.S. stock equities is foreign owned. At the end of 2022, foreign investors held the largest single block, 42 percent, of total outstanding US stock. This is likely due, in large part, to US tax policy, including rules that generally exempt capital gains of foreign investors and only lightly tax their dividends.

The next 30%ish is held in IRAs or 401ks. Thus only 25% is held in taxable liquid accounts. Most IRA and 401k holders are buy and hold people?

What will drop house prices is extra supply and high prices just like the HB1. People do not need stocks but they need shelter.

the difference is that a lot more of perceived “wealth” is based on stocks today, leading people to overpay for houses, and everything else.

Ok. Look up the median home price to median household income ratio of 2000 and then today. Then list them both and in the same sentence tell me that you don’t think home prices will drop when the bubble pops because they didn’t in the year 2000. And mean it.

Things are different than in 2000.

More and more industries have become oligarchs. There are fewer mom and pop small businesses.

This causes the Gini index to increase. In 2000, 27% of the the lowest 1/4 percentile owned a home. If I recall, it is now down to 15%. The same will happen with the median income percentage who will own a home.

The home builders, in earnings calls, say they target the $100k to $200k family incomes and the number of people in this range is still growing. They are also building a lot of apartments that are targeted for the median income and lower families.

Just my opinion.

Considering we have not recovered from the rate at which we were building houses during the financial crisis in 2007-2008, you definitely have an expectation like we’re going to have some big crash and I’m sorry to disappoint you but it doesn’t look like that’s going to happen. It might be more like a slower discount that happens over time but by waiting you are probably going to do yourself more a disservice by losing out on potential equity than anything else.

Potential slowly decreasing equity, lol? Anyone holding out right now is probably being smart. This is quite predictable I feel.

I think we will visit 08 again, and i will be ready with cash.

Omg, Nvidia lost $0.6 Trillion in value in a single day – a world record. If you take the top 3 semiconductor stocks, then close to a Trillion imaginary bucks wiped out in a day. Quickly, cut the rates!!

But if you look at a three-year chart of NVDA, it’s just a little dipper today.

Have longer term calls in double-short Nvidia etf (NVD). Nvd was up 34% today. I am so out there that some contracts have open interest of 1. Lol

Andy,

Hoping DeepSink and what it achieved puts both reality into the AI market and hopefully some cost sanity. Software models are free and you can host you own but if you pay them to host it is less than 1/30 the cost. Very impressive and a focus on the efficiency side of the house is a positive too, less massive data centers hopefully.

Yes, it is becoming painfully clear that (compared to DeepSeek) our geniuses here (Meta, Google, OpenAI, etc) found the dumbest and most brute-force ways of doing AI. Why wouldn’t they; they have untold $billions to burn on moar Nvidia chips.

They thought they were building moats around their businesses. But they were building mainframes and DeepSeek just came out with the first powerful mini (ala Sun Microsystems). Still waiting for the first PC to explode the market.

China has several million more engineers than the US now; no one can come close to them on cost. DeepSink was a small team of several hundred and $5 million. China politburo also fully supports it’s tech industry – complete synergy.

I would tell people, that NVDA is does not have a moat around AI engineers. There are a lot of smart people out there and when big profits are involved, they start migrating to that industry.

I have to believe a more efficient and less energy intensive solution will also replace BTC at some point. Technology is always improving and BTC is just just software code and files.

Nicko2,

More STEM than combined in world. Synergy is good. Most people don’t realize 70% of what is in iPhone all started out as tax payer investments. They package it up and add value with final mile and get all the proceeds. China allows private sector to flourish there but can’t control the reins which down the road would be in societies interests. But the US is and has been an Empire in Decline and denial is strong. Hopefully it adjusts while it still has a window.

Those margins are hanging in there so far. Trending down. But hanging in there.

Yes. Quite a bit left to cut through fat, then flesh, before it hits bone.

Many of these new houses are built so far from the employment centers that people are not willing to pay top dollar and then endure a long commute. After the pandemic ended traffic has gotten intolerable as people had shunned public transportation during the pandemic. The traffic issue are much worse than prior to the pandemic. Many people are now have to got back to their offices 5 days and 40 hours per week. Buying existing homes in the city and close in suburbs may be more attractive option than buying a new home in the far out suburbs. I see a lot of For Sale signs at the exits leading into some of these new developments.

That has been my conjecture about this unsold housing inventory as well, based on the SF Bay Area.

New homes are mostly large scale developments very far away, or else relegated to areas like the Hunters Point Shipyard, a superfund site.

There’s probably a good reason why they’re going unsold, besides just the price.

You people have got to get it out of your mind that single-family houses are being built in the urban cores of the most densely populated cities in the US, such as New York City, San Francisco, and Boston. Not happening. Hasn’t happened in decades. Everyone knows that. What they’re building is multifamily (condo and rentals) in big buildings and towers. Density at the urban core (multifamily) always increases unless you shut down immigration and stop having kids. And urban sprawl (single-family) always increases unless you shut down immigration and stop having kids. It’s just that simple. You choose where you want to live.

In Manhattan, there probably hasn’t been a new single-family house in a hundred years. They tear down a low-rise and replace it with a tower. The short time we lived there (brand-new tower on 1st Ave and 90th), they did that to two old low-rise buildings across the street. One of them was a grocery store, and losing it was a bummer. They tore those down, and six months later there were two big residential towers in their place. All higher-end stuff, as was our tower. Here in San Francisco, nearly all of what is getting built is multifamily, all of it expensive. Occasionally, someone includes a few townhouses in a larger new development. Just about the only new single-family dwellings are ADUs in a backyard, and the occasional teardown that is getting replaced.

In densely populated cities, if you want to buy a new single-family house, you’re heading much further out. There is something for everyone, but not in the same place.

Does a single family home that is torn down to the studs and rebuilt consider a “new home” for the purpose of these discussions or does it have to be down to the foundation?

Your instincts seem like they’re on target here– I know in Housing Bust 1 a lot of the new far-out homes (i.e. San Bernadino County) got completely crushed. Same thing in Florida, where wages are pretty low.

Seems reasonable that the further the distance a home is from the kinds of jobs that could pay the mortgage, the riskier the purchase is.

A friend in real estate is feeling the pain. Scoffs at the new construction and their 1,700 sq ft homes. He’s been in the business 5 decades and can’t sell the overpriced behemoths of yesteryear.

I would say your friend and others who have done well thru the years can change careers if needed,perhaps “learn to program?”.

Now now, that’s no longer a thing. Learn to plumb . Haha

That is so true it is not a joke. Good plumbers are cleaning up like hedge fund managers.

It takes 4 years to get a plumbing license, no quick fixes.

Early retirement is the real game.

Need to tell your friend that he needs a better understanding of market dynamics, and so do his clients. His clients need to lower their list prices…by a lot.

“Big publicly traded homebuilders have to build and sell homes regardless of the market because they have to keep their businesses intact and growing, and they have to please Wall Street to keep their shares from tanking”

Mostly I agree – but what happened during 2010 through 2016, when new supply was pretty darn low?

The *really* important question is what happened to this dynamic from 2002 to 2006 (ZIRP 1.0 – “The Beast is Born”) – builders could have moved a *ton* of new supply product at 2003 sales prices (ZIRP supercharging affordability – Fed’s presumed plan).

But the builders went another direction (and the Fed went brain dead) – ginning up massive margin McMansions at double the 2003 prices (but at 2003 volumes…) exploiting ZIRP to keep monthly mtg payments constant.

The builders got filthy rich and the country got RRE implosion 1.0 (2008 edition).

History is going to be aghast and agog at the inability of DC and the Fed to see the immediate, profound, and poisonous effects of ZIRP…and fail to course correct (in any way) for years, and years, and years.

Yeah, and Bernanke got a Nobel prize in economics in 2022. Bernanke didn’t understand what he was doing. He lacked an adequate knowledge of money and central banking.

In the long run, Bernanke will be called “Zimbabwe Ben”.

He deserves it – the pure DC/academic arrogance of “We have a technology called a printing press…” is going to go down in history just like Weimar “cleverness” or “permanent high plateau”.

It really is mind boggling how the Fed could not see (within 2 years) how ZIRP (both pre and post 2009) was *not* mainly stimulating volume increases in the production of homes (thereby hiking *employment*) but mainly just enabling the *huge* expansion of homebuilder profit margins (via ZIRP, powering the McMansion McMorons and other speculative idiocies).

The standard excuse is that “there is only one interest rate” (not really, but whatever). Regardless, *many* *many* different types of ZIRP course modification could have been planned/experimented with/tried – but the Fed kept bankers’ hours (as it were) and turned off their eyeballs and brains once they turned on the printing press. I guess the DC golf courses beckoned.

I do agree they will go down in history looking like idiots, eventually. It’s funny because they know bad monetary policy creates asset bubbles, what happened in Japan is well documented. Yet they still pursued it, even though they know better.

Blake,

To a (very) limited extent, I sympathize with DC/Fed (I know it never seems like it).

Basically, they (fairly foolishly) try to kinda/sorta centrally manage (mismanage…) a nation of 330 million people using a smallish handful of tools, which they make ever smaller by ideologically taking certain tools off the table (cough, reduce spending, cough, focus on industrial base, cough reconsider perpetual war drums and delusions of global pseudo-empire, cough, rely on disclosure rather than command, cough, cough, cough).

And to this, they add a sort of air of inarguable inerrancy to their policy pronouncements (relying upon a historically corrupted media to almost never call out the Emperor for dropping his shorts).

All this has added up (post WW II, especially post full fiat) to a government that has continually slid downwards (as manifested in a Federal debt-to-GDP in accelerating excess of 100%) and yet finds it almost impossible to course correct on clearly failed policies (20 years of ME wars, refusal to reform entitlements, refusal to effectively police multi-decade subsidy recipients in medicine, higher education, refusal to tax on a level adequate to fund foregoing policy delusions, etc etc).

In short, the US tries to run the world, when it cannot even run itself.

Florida condo crises underway, 1mm plus units over 30 years old out of 1.5 mm total, it also surged in 20,21 on existing inventory, structurally looks like a 40 percent drop to realistically bring on buyers, if at all…assessments, repairs, reserve funds and insurance in hurricane prone areas, 2x maybec3x increase in monthly hoa…

Gaz — I’m a 40 cents on the current $ price for one (wide ocean view, walkable, lots of palm trees). Let me know when they hit that 60% off. :-)

Forty percent is not enough. With Florida HOAs having already increased 2-3x and more increases guaranteed, very high and unknown assessments guaranteed, with many existing owners unable to pay those, I wouldn’t pay 20K for a nice oceanfront condo at the moment. I really wouldn’t. I can’t see anything changing my opinion, even the steepest of price cuts. And we would otherwise be very interested. Those days are gone forever, I’m afraid.

In the meantime the insurance on my Wisconsin rentals have gone up another 15% on top of last years 20% (no claims), while my Florida insurance decreased 1.8%.

Can’t wait to get my California renewal

David: Wisconsin has benefit of “sharing” risk from Florida and California.

Since everything is now for profit (especially the nonprofit and mutual companies) the risk “sharing” is just offloading and profit taking.

Insurance, while good in concept, has completely lost the plot of protection, and benefits from being a mandatory service (even when disaster is gobbling up the leftovers, the CEO gets paid).

I’m a huge fan of the not so big house idea. I hope that the current trends stick around. I shake my head when i walk through some of these 3,000 + square foot homes from the 90’s. The amount of wasted space is amazing and the egress and ingress is often oddly routed , such that it takes you through a tiny mudroom off the garage or something. Packages used to “disappear” from my parents house when I was younger, only to be discovered on the neglected front entry some time later. I often wonder what will become of these bigger homes as they age. They are very costly to update, and the floor plans make little sense for the way we live today. I’ll find out in the not too distant future, as my mom is gone and my dad is 73. I guess supply and demand will have it’s say.

i like having space, but only if it’s efficiently used. i shake my head at 4000 sf houses with 4 bedrooms and enormous common areas that nobody uses.

with a lot of people working at least sometimes from home, it’s important to have more rooms that people can have quiet.

Agree. Ours isn’t that big, but it was find for a family with 4 kids. Now that we’re down to one remaining to fledge, we can’t wait to downsize. We’ll still need that many bedrooms through, since we both work from home and each want our own office. Master, guest and two offices will be next for us.

But both a living room and family room? Nah, wasted space. I get why to split them up (so you can have a nice space for guests and a lived in space for the mess that kids create) but I don’t see us needing that in our “retirement” house. Besides, who wants to heat and cool all that extra space? Even in temperate California that adds up.

yes, exactly. and also, i have no need for huge bedrooms. what’s the point of a 30 * 20 ft master? 600 square feet in a bedroom? for what?

i also would rather have a tool/work room than a formal living room but seems i’m in the minority.

Franz, I’m 100% with you. Ours in this house is ridiculous, and for no good reason. Wasted space.

3 kids in a 1700 sq ft house, half of their childhoods, then moved up to 2300 sq ft for their teenage years. Worked fine. Probably still underused the living room.

“i shake my head at 4000 sf houses with 4 bedrooms and enormous common areas that nobody uses.”

McMansions for McMorons.

Very much reminds me of the dying British Aristocracy that got bankrupted by their country estates (looked amazing – think Downton Abbey – but cost a fortune to maintain with very few free market revenue opportunities.

Also – home sizes zoomed for a while there (from 1500 sf starter in the 1980’s to 3000 sf McMansion post 2000) even as actual family sizes were collapsing (from 4 in the 60’s to 3 in the 80’s to 2.5 in the 90’s to 2 in the aughts to 0-1 going forward…).

And yet 4+ bedroom McMansions are still frequently the focus of new builder efforts.

Who are these exactly *for* – if not, perhaps, “undocumented” extended stay motels (see California)?

I wouldn’t be surprised at all if heavily levered real estate interests aren’t a lot of the “money” behind the undocumented explosion/fighting deportations.

Wolf doesn’t like links and I don’t have a source for this, but the average home size tripled from the 1950’s.

1950s: The average new home sold for $82,098. It had 983 square feet of floor space and a household size of 3.37 people, or 292 square feet per person. Homes had more shower space than sleep space: 1.5 bedrooms and 2.35 bathrooms. The most popular colors for kitchen appliances were canary yellow and petal pink.

1960s: The average new-home size grew to 1,200 square feet, giving its 3.33 residents a spacious 360 square feet of room apiece. The bedroom-bathroom ratio flipped from the previous decade, with 2.5 bedrooms and 1.5 bathrooms. Turquoise and coppertone were the appliance colors of choice. The average price: $118,657.

1970s: Homes continued to get bigger — an average of 1,500 square feet. With the household size shrinking to 3.14, each person luxuriated in 478 square feet of personal space. The average price was $160,338. Kitchen appliances achieved an iconic color balance: avocado and harvest gold.

1980s: The average amount of space per household resident more than doubled in a generation, to 630 square feet (a total of 1,740 square feet for a household of 2.76 people). The average price more than doubled since the ’50s as well, climbing to $216,338. Television sets per household totaled 1.57, unchanged from the previous decade. Kitchen appliances eased back on the color schemes to almond and beige.

1990s: The average new home sold for $268,055. It had 2,080 square feet of floor space and a household size of 2.63 people, or 791 square feet per person — enough to make those luxurious accommodations in the 1970s look positively skimpy. In the kitchen, black was the favorite color for appliances. The number of bedrooms and bathrooms were little changed from the 1960s: three and two, respectively.

2000s: The amount of square feet per person continued its inexorable climb, now at 865 (2,266 total square feet for a household of 2.62 people). The price: $281,141. The number of television sets per household reached two for the first time. Black appliances gave way to stainless steel — a sign of the new millennium?

2010s: The average new home ($292,700) offers 924 square feet per person (2.59 people per household, 2,392 total square feet) — three times the space afforded in the 1950s. Television sets per household jumped to 2.93, while kitchen appliances held steady with stainless-steel finishes.

Sandy,

Very, very useful, detailed history.

All those historical prices have to be in 2024 dollars, right?

You are right. After 20 years of being a Yankee, my wife and I just retired from the Northeast back to the Dallas north suburbs. We are “down sizing” from a 6,000 square foot home (had three kids, now empty nesters) to a 3,500 square foot home in the process. Rented a home for one year while we searched. The North Dallas area we are returning to was built out in the late 80’s and 90’s. It took us 8 months of house hunting, and looking at 50+ houses, to find a house with floor plan that was not a bunch of “wasted space” and “oddly routed”. When we walked into the house we are currently under contract for it was immediately obvious that the original owners had overridden the standard McMansion floor plan and built a floor plan that had common sense. House was unique for the area and fairly priced. We close in 3 weeks. The vast majority of houses we saw had horrible floors plans, were poorly maintained, and were over priced.

3500 sqft is still a HUGE house.

…typing this from a 960 sqft 3/1…

No kidding! Typing from an 1800 with family of nine.

What’s the simple take away in the discrepancy between homes completed and homes in all stages of construction? Basically all stages of construction now is up near housing bubble 1.0 levels (06-08 timeframe), yet completed numbers are quite a bit lower compared to 06-08 days. What explains this? More permitting/delays/slower construction process now vs back then?

Completed houses for sale are very high and surging. What explains that? That’s the question you need to ask.

I’m not worried about empty lots where they haven’t started construction yet because they haven’t put a lot of capital into them yet.

The difference, in 2006 – 2007 a lot of to be build homes were being sold to individual for speculation before construction started and they would flip them when completed. Builders were having to limit buyers to the number they could contract for. When the music stopped all these houses flooded the market.

Both good thoughts, thanks!

Blake,

There is a significant lag effect between “starts” and “completions” but you do ask a good question (despite some pooh-poohing from others).

Even in the last 5 to 10 years, there seems to be a fairly sizeable number of homes that somehow got started yet never actually showed up as finished (per the G’s definitions). Even with reasonable lags.

That really matters since inflated “starts” may dissuade *real* starts that could have added to *real* supply – mitigating the 20-25% rent explosion in 2021-22.

The missing “completions” issue has been discussed over at the Mish blog.

cas127.

You’re posting, as very often, stupid ignorant conspiracy BS. That’s what you traffic in. I understand it’s a lot of fun. But post this BS on Mish’s site.

Usually, I delete this BS because I don’t want to waste my time crushing it manually. But occasionally, when I’m on coffee break, I waste my time, like right now, to crush it.

So: “Even in the last 5 to 10 years, there seems to be a fairly sizeable number of homes that somehow got started yet never actually showed up as finished.”

BS. And then you go on building your conspiracy theory on this BS.

According to the government data that you despise so much, from the Census Bureau data, which provides this data on starts and completions:

From Jan 2000 through December 2024:

24.158 million single-family houses started.

24.051 million single-family houses completed.

The difference (107,000 houses) = current batch of houses that hasn’t been completed yet.

This is public data. All you have to do is look it up. But that’s too hard to do. it’s just easier and more fun to traffic in ignorant conspiracy BS.

Wew!

The scoreboard on this one reads

Wolf 100

cas127 0

Sorry I didn’t mean to get you guys into a conspiracy theory argument. I respect all thoughts. My point was, if we went back to 2004-2005ish, would we see the same pattern? Or is this differential between the two unique in 2024? It’s hard because today’s data is emerging as we speak. And 20 years ago I was skateboarding during recess, not looking this up.

Wish these downward prices would come to New Jersey, it’s still insane here.

Same in my part of Oregon. Sellers on Zillow have erased the Zestimate history from most all of the listings to hide the $300k price they paid 5 years ago, and make their $800k price look better.

You can’t erase the data from the county assessor’s records though.

Zillow is not due diligence, more like “dude” diligence.

It’s an ecommerce site that doesn’t sell anything. My wife loves the online shopping for real estate.

There’s no buying though.

I’m curious if you have more data on their mortgage rate buydowns. They started doing them maybe 1-2 years ago, and I imagine they did them by buying interest rate hedges. You mentioned before most of these buydowns were usually for ~5 years or so. If they expected rates to have come down substantially by now, they may not have hedged fully for the entire 5 years, since hedging costs money. If their hedges don’t provide protection for current rates for the full term of their buydowns, then they might end up unhedged and facing the full cost of the difference in interest rates.

I wouldn’t be surprised if some of the lenders skimped on their hedges in order to goose their annual profits for that year, and may end up having to pay the piper if interest rates don’t come down in the upcoming years… (a double whammy of increased costs and fewer people refinancing since rates are still high)

When D.R. Horton’s interest-rate hedges for their mortgage-rate buy-downs blew up in Q4 2023, they talked a little bit more about mortgage-rate buydowns in the conference call for Q4 2023 to explain the loss they took on their hedges. They said that just about everything around these mortgage-rate buydowns is essentially a trade secret, so no one discloses much of anything. But they also said that many of them are PERMANENT buydowns.

https://wolfstreet.com/2024/01/24/d-r-horton-sheds-some-light-on-the-massive-costs-of-mortgage-rate-buydowns-as-a-hedge-went-awry-stock-tanks/

Average incentive for some builders (Lennar disclosed 10%) reflects the costs of the mortgage rate buydowns, plus the incentives they give to cash buyers. So it seems close enough to guess that if the average incentive for a builder is 10% of the sales price, then the cost of the mortgage-rate buydown for sales that come with a mortgage would be about 10% of the sales price. And cash buyers get 10% in other incentives, such as freebees, and/or additional discounts.

People trying to sell their houses at these insane prices, I have two words for them. Greedy *#$%$#&s. When you get your new property tax assessments, new insurance rates, new hoa fees, and you need major maintenance, give me a call so I can laugh at you. I won’t mention wildfires, mudslides, floods, deteriorating roads and sewer, increasing crime, hurricane, and tornado damage. Oops, I just did.

Always the “greed card”.

Yeah, or they see what the next house they’re going to buy costs and need/want to clear that much to be able to do it.

When was the last time you sold a car or something, looked at the comps and then said “nah, I’ll list mine 15% lower.” Like never.

Like always. Every time I get rid of one. I’m 64 and have only had to get rid of 3 of them. I usually get several hundred thousand miles out of a car. When I’m done with it, I want it gone. Two have gone to the scrapper, and one went to a dealer. Hit the big row of car dealers in town and drove from dealer to dealer until one gave me a cash offer.

:)

Me too. Almost 60, only have ever sold one car, drove 4 cars until they literally died on the road or my kids wrecked them. Driving two Toyotas now with cumulative age of 40 years and 350K miles, my annual cost of car ownership based on depreciation of the vehicle is about as low as it can be, and my guess is these two cars have another 10 years in them.

BrianC, doesn’t sound like you’re intentionally selling it for 15% less than you could. You’re taking the market price. Greedy! ;-)

Ok so you guys and your car anecdotes is saying that you happily sell stuff below market price? Seems unrelated. I drive my cars a long ways too. Regardless, if the market will pay me xx amount for my car or house, I will set it for that. I don’t consider myself overly greedy for it either.

buying a house for 600,000 in 2018 and expecting to get 1,500,000 today is the definition of greed.

At some point we should find the bag holders. I will not feel sorry for them.

Disagree. “Expecting” to get $X is not greed. They believe it’s worth it. How is that greed?

A well-known realtor around here likes to joke about sellers “well, I’m not going to GIVE it away.”

Every market eventually gets a bag holder. I’m not old enough but I saw the bag holders in 2000s, 2008 – 11 and I’m sure I’ll see some of the bag holders in 2025 – 2030 from all the real estate we sold.

I already see one that bought and now is renting the home at a loss because they overpaid and tried to sell due to some issues with-in a year.

It’s the same story every time. Paper gains mean nothing unless you make a sale to realize those gains.

kracow, this is very true, and it bears repeating that prices are set at the margins.

people might feel rich because of their assets going up, but if any signfiicant number of them tried to sell at the same time, prices would plummet.

it’s paradoxical how high prices depend on very few people selling to realize the gains from those high prices.

But it’s not just greed. The market was boosted higher. People want to sell it for what it’s worth. Yes maybe they are stupid and wrong and they will soon have to get with the times and adjust their price, but I don’t know that everyone just woke up greedy here. They were trained that homes are worth way more and they are rich. They will now need to be trained that things also go down in value. And trained they will be.

House for sale similar to mine in my town, with property taxes and insurance the monthly but is probably over 5x what I pay in rent. This insanity will not end well.

“When you get your new property tax assessments…”

You realize these insane property tax assessments are part of what’s driving the bubble, right?

Price x Quantity = total revenue (10 units sold x 50 dollars a unit = 500 dollar revenue). I wonder where the squeeze is being felt. In the areas I monitor, prices have been remarkably resilient, increasing even. Number of houses sold x price is definitely less. But double the monthly payment or more x half the units sold means… revenue is still high for… some entities.

A lot of us thought houses prices would adjust down because of the monthly payment jump. But… I guess someone is still making money. I wonder if this angle of observation can provide some light on what and who drives the housing market.

Realtors, government (transaction + property taxes), GSE’s, mortgage lenders – it’d be interesting to understand the impact on these entities. Also buyers, what kind of buyers are out there.

I’d heard the housing market years ago described as a strata of plankton to whales. Plankton are the lower priced houses, whales are the more expensive ones. Is there move-up happening? What’s happened to the various strata – have the plankton been killed off? Is that a flawed view?

If houses were described like cars, high volume, lower priced Kia volumes have collapsed but low volume, high priced Bentleys are still moving briskly, it seems to me.

Lot of moving parts.

if I wanted to move across the street, my total payment would increase 130%. If I wanted to move up to what I wanted pre-2020 at today’s prices my payment would increase 300%. I just don’t know where people are getting to The money to do these transactions, but obviously they are happening, even at a low rate. Median household income, has not gone up enough to justify the increase in prices. I guess people are just paying more as a percentage of their income if they are buying in this market.

“This surge of completed inventory for sale should help brush aside the zombie-like undying real-estate hype about the “housing shortage,” that has been spread for eons by the real estate industry and its trolls in an effort to keep driving up prices.”

lol, that about sums it up. I still see realtors out there talking about 6 months supply being the “norm” and the steadily increasing months of supply is nothing to be concerned about. Well, maybe before the internet, 6 months supply was the norm, but not anymore.

If you were to factor in the incentives & rate buy downs into the contract prices, new home prices may be down over 20% from their peak in 2022.

One of the things I keep trying to tell people on social media and elsewhere is to not allow these housing developments to buy down their rates and make sure that they actually lower the price of the house. If they won’t do that then walk away and find another house. One of the things that this is doing is hurting the housing market because instead of those lower priced homes posting and then new sales being based off of those new comparables they are propping up home prices artificially by writing them down on the back end.

Also paying a higher price for the house means that your property taxes will likely be higher as well. And your insurance. The only one it really benefits is the company selling the house. Don’t let them win

New houses are getting smaller and more affordable, but what’s the pricing like on a sq footage basis? Is it up or flat or down?

thurd2, Greed is Good! 🤣 I question how much house prices will come down. Mainly because of the now higher cost of building a new one. Prices for land, materials, and labor have gone up. People in California that have just lost their home to fire are finding out that they are underinsured! My average home that cost $100k in 2006 would probably cost $250k to rebuild.

That is why the market value is about $275k to $350k. And then demand and location are big factors too. In my area, people from California have been moving in! They pay cash and they bring their Tesla cars. 🤠

Prices of materials have plunged since 2022, including lumber (by about 60%). Appliances have gotten cheaper, lots of stuff has gotten cheaper since 2022. Labor has gotten more expensive. The homebuilders are talking about this stuff during their earnings calls.

The current housing market in the US is the United States’ FrankenMonster. It is kept alive by devious means and gives the appearance of a healthy economy – we have a middle class of millionaires (the million or millions being inflated home values). The reality is that FrankenMonster’s veins are filled with formaldehyde and his eyes are sewn open. He’s not healthy; in fact, FrankenMonster died many year ago. FrankenMonster is very close to or past his expiration date as a magician’s prop. He’s not fooling anyone anymore.

It looks like the price of existing homes would need to be in the $340,000 to $380,000 range to stay within the historic relative value to new homes (which, with incentives, are now worth around $390,000 to $400,000 when factoring in incentives). So new homes need to drop 10% to 20% for sales volumes to climb.

Well that’s convenient because your pricing levels are easily achieved with a small adjustment in their profit margin numbers

My best guess is that for a lot of areas, there will be 5-10 years without appreciation.

The good news in that is it wrings the speculators out of the system. I’d be fine if our next house never appreciated, we’re not speculating or intending to use the equity to buy another.

Limited appreciation means the buyers are people who want to live there and stay there for a long time. Good for neighborhoods, good for stability.

New home sales are less than 10% of sales in the real estate market. There is no shortage of supply of homes as many baby boomers continue to downsize like me. The problem is a mismatch between home prices and first time buyers. This is further exacerbated by the interest rates, which were artificially low from 2016 until 2023. My first house, 35 years ago, carried a mortgage with 10.5% interest for a 30 year loan. People looking for rates to drop into 3 to 4 percent range are unrealistic. Bite the bullet, buy the house you love and deal with it. This is not only your home, but also your largest investment. If interest rates drop in the future, you can either refinance or sell and move to your next house. Cheers.

“New home sales are less than 10% of sales in the real estate market.”

That’s wrong. I gave you both charts: new SF house sales in 2024: 683,000. Existing SF house sales in 2024: 3.67 million. Total house sales = 4.35 million. New house sales = 15.7% of total house sales, and 18.7% of existing house sales.

I bit the bullet on my first home in 04. We wanted to buy so badly, that we bought an overpriced turd. By 07-08’ we were underwater. We were trapped in that turn until 2015 when we sold for a loss.

Biting the bullet is the worst financial advice you can give someone. You’re literally telling them to overextend themselves for less than they want. If less people “bit the bullet” the rich would be less rich, and housing would be more affordable.

This is good advice. Biting the bullet perpetuates problems and pretends that it’s just how it has to be. Educating people and understanding that there is no shortage of homes and simply bad policies, is a good start. Better than biting any bullets, IMO

So, so wrong. Boomers like us are ready to downsize but the prices even for smaller homes are way out of sanity. Why downsize and pay the same for the house we have now? We can just stay where we are at – which is why the boomers aren’t selling.

As we discuss so often, rates aren’t going anywhere for a while, that means prices have to come down until price discovery with a buyer happens. Nobody out there at this point is waiting on rates, they’re waiting on prices.

Sandy,

I agree. We could downsize to half the house we have now but the following reasons hold us back.

1) It would be more expensive. If we sold our current house with commissions (6%), moving expenses, we still couldn’t pay cash for an overpriced smaller house. We’d need to take on a new mortgage a few years before retirement. Sitting on a 3% mortgage has that advantage. The Fed were geniuses to motivate people to stay in a house they can afford instead of flooding the market with sellers.

2) We do have large family gatherings. We had 11 people stay with us comfortably over the holidays. A smaller house would not cover this so putting family up into hotels or AirBnB at $200-$400 per night would be required and cramming in seating for meals would be a challenge.

3) When I retire, I will have hobbies. I still need the home office, craft room, workout room, workshop, etc to stay mentally and physically happy.

These sound like 1st World problems but why would I pay more for a lower quality of life?

Exactly, same for us …and for a lot of boomers. They run the numbers and decide to stay in their large homes. Turn this bedroom into a craft room, turn that bedroom into an exercise room.

We’d probably consider doing that except ours is a two story and hubby and I want a no stairs lifestyle for our aging knees. We also want to get out of Southern California and never have to consider what the traffic on the 405 looks like again. We will sell this summer and then rent while prices cool down further up the coast.

Sandy,

From my experience in selling several houses (not new) over the past two years. Its recently retired boomers with far more in market equity than they had expected that are plopping down cash for over priced homes. As you said, it doesn’t matter to them if it will appreciate. The market run up (real estate and stocks) to their retirements left them ahead of their plan. Its like found cash.

I just hope it holds until I have this last one ready. Its part of my Gen-X escape plan.

“Bite the bullet, buy the house you love and deal with it.”

Most people would love to bite bullet and buy it now but only problem is they just can’t afford at current price and rates. Some thing has to give in.

Why are mortgage rates buydowns and incentives more popular than simply decreasing the price by a corresponding amount?

Keeps the selling price high!

Exactly, it provides the comps to support existing pricing. Also fills the coffers of the local property tax people.

If they drop the price on one, they’re dropping the price on all of them as that information is public.

Rate adjustments and other incentives are not public, so they can change them as the market changes.

Oh, the games corporations play to defeat price-finding.

Unfortunately, we have to wait for the prices of existing homes to keep coming down. Then these games will not work.

Which is happening surely but slowly.

There is a calculation behind this strategy. Most 30-year mortgages get paid off after a few years. The average life of a 30-year mortgage is about 7 years. People sell the house (job change, divorce, more kids on the way, death, downsizing, etc.) and the mortgage gets paid off, or they refi (including cash-out because they need the money to do a project) and the old mortgage gets paid off. Or they default, and eventually the old mortgage gets paid off by the bank, etc.

So homebuilders can figure that the bought-down mortgage on average lives only 7-8 years. So the cost of buying down the mortgage is a monthly cost, and if the mortgage gets paid off after 7 years, the monthly cost is only over 7 years, which is a much smaller amount than a 30-year amount. And then they can hedge, or partially hedge, that amount with counterparties taking the other side of the bet.

So are permanent mortgage-rate buydown on average might cost $40,000 to the homebuilder if the mortgage is paid off within 7-8 years. So if the builder cuts the price by $40,000, the payment at a market mortgage rate would be substantially higher than the payment with a buydown. That’s why buydowns are so attractive. The auto industry has done this successfully for eons to sell new vehicles (such as “0% financing,” or “1.99% financing,” or subsidized leases, and they offer cash incentives at equivalent cost to cash buyers).

“home price appreciation does seem to track very closely with bank reserves at The Fed (6mo lag)”

Bank reserves down, liquidity down, interest rates up, housing prices down.

Housing Affordability Index (Fixed) (FIXHAI)

“Since stocks and equity, i.e., claims for profits, are mainly held by the top of the wealth distribution, QE might disproportionately benefit that part of the distribution.”

If you go out 20 miles from DC to a suburb where Ms Swamp gets a hair treatment you see dozens of Real Estate signs for new homes up for sale at big sale prices, subsidized by the builder. If you go into central city crime ridden DC you see no ‘FOR SALE SIGNS”. When one of these 19th Century homes go up for sale, it is usually sold in a matter of days, sometimes “As IS”. Condos also are selling like hotcakes, as they are the only housing that first time homeowners can afford.