We’re in the 4th cycle of the subprime profit motive after auto-loan securitizations became a thing in the early 1990s.

By Wolf Richter for WOLF STREET.

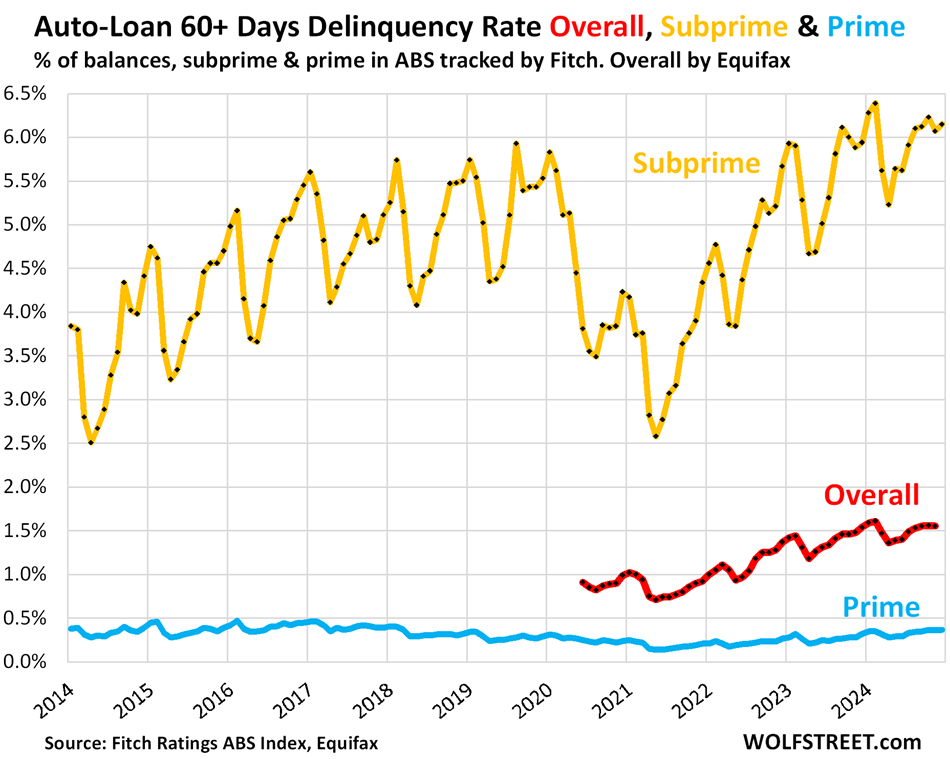

The 60-plus-day delinquency rate of subprime auto loans rose to 6.15% in December, a new record for December in the data from Fitch, which tracks subprime auto-loan asset-backed securities (ABS), going back to their origins in the early 1990s. Subprime delinquency rates rose to record highs in 2023 and rose further in 2024. They peak seasonally in January in February. If January and February 2025 follow seasonal patterns, subprime delinquency rates will set new all-time highs (gold in the chart below).

But for “prime” auto loan ABS, the 60-plus-day delinquency rate has been in pristine condition, at 0.37% in December, according to data from Fitch (blue in the chart below). Even during the Great Recession, the prime delinquency rate rose to only 0.87% at the worst moments.

The overall 60-plus-day delinquency rate for auto loans and leases has been getting pushed higher in 2023 and 2024 by the surge in subprime delinquency rates. But in November, the latest data available from Equifax, it ticked down a hair to 1.55% though it normally ticks up in November. The seasonal peaks also occur in January and February (red).

Subprime is always in trouble, which is why it’s subprime. Subprime doesn’t mean “poor.” It means “bad credit,” such as a FICO score below 620. The young dentist just starting out and getting into it over his head and falling behind on his debts, and therefor getting his credit score cut to 596, is an example of high-income subprime. Low-income people often cannot borrow at all, often don’t qualify for a credit card, and if they qualify for a credit card, they’re going to have a low credit limit. Subprime isn’t a permanent state; it’s a phase borrowers go through, and from which most borrowers emerge after they’ve gotten their act together.

In terms of auto loans, subprime lending is largely confined to older used vehicles, sold by specialized subprime dealer-lender chains, or financed by specialized subprime lenders. All these lenders then package these subprime auto loans into Asset Backed Securities (ABS) and sell them as bonds to institutional investors that buy them for their higher yield.

Subprime lending is small in the overall auto world. Lots of buyers pay cash and don’t finance: 60% of used vehicle purchases and 19% of new vehicle purchases were paid for with cash in Q3 2024, according to Experian. Of the deals that were financed in Q3, 16.9% were subprime.

Why this surge in subprime auto-loan delinquencies?

There have been four cycles with spikes in delinquencies of subprime auto-loan ABS. The first occurred in the early to mid-1990s, when subprime auto-loan securitizations were a new thing, and everyone jumped on it:

- Specialized dealers and lenders because it was hugely profitable and low-risk since they sold the dubious subprime paper to Wall Street and were off the hook. So their lending became recklessly aggressive.

- Institutional investors that bought the ABS from Wall Street because they offered higher yields, at minimal risk, since ABS are structured, with the lowest-rated slices taking the first losses, but paying the highest yields. So if you bought higher-rated slices, you’d still get a good yield, but little risk.

Obviously, the whole thing, like so many new financial products, turned into an epic mess with the delinquency rate exploding to 6% in 1996. The episode was followed by tightening credit standards, and delinquency rates dropped.

But then in the early 2000s, the profit motive took over again, and lending standards loosened, and when the economy tanked and unemployment soared in 2008-2010, delinquency rates spiked again. This spike then set off another credit tightening cycle. But by 2014, with the free money washing over the land, here we went again; delinquency rates began to surge until… That cycle was interrupted by the pandemic and the free money that came with it, and the free money flooded the people, and the people paid down their credit and caught up with their arrears, entailing huge profits for the segment, which led to even more reckless lending. And so that blew up again. And now subprime credit is tightening again….

This long view shows those four cycles:

Buyers with a subprime credit rating have few choices and lost their power to negotiate. They were irresponsible with their credit before, which is why they’re rated subprime. They’re considered high-risk, with a high probability of default. Regular dealers, banks, and finance companies have already turned them down. So specialized dealers sell them older used vehicles at gigantic profit margins, provide financing with big-fat interest rates, and then send the loans into the securitization pipelines. These are hugely profitable sales, and the ABS make investors happy because of their higher yields and loss mitigation that comes with the securitization.

What happens when the cycle turns as delinquencies get out of hand, the most aggressive subprime auto-dealer-lenders get in trouble. In 2023, several PE-firm-owned subprime-specialized dealer-chains filed for bankruptcy. Even the large publicly traded subprime dealer-lender America’s Car-Mart disclosed massive problems in December 2023, and its shares [CRMT] tanked and were inducted into our pantheon of Imploded Stocks. This is a high-profit business whose risks are often underappreciated by investors. And after the mess gets somewhat cleaned up, the risk-taking starts all over again because the profits are just too juicy, and eventually delinquency rates will get out of hand again.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

If subprime doesn’t imply poor, I’d like to see a few examples of some people who are rich but subprime. I know about strategic defaults from the last bubble, how much of a hit does one take to their fico when doing that?

Nicolas Cage defaulted on a couple of leases back when I was consulting with a finance co specializing in exotics cars. This is in the public domain so nothing proprietary about it. I don’t recall specifics of his balance sheet (and I wouldn’t share them here if I did), but he certainly wasn’t poor at the time. There were also many professional athletes, both active and retired who had similar problems but I don’t remember any names.

Sometimes subprime just means having too much money to remember to mail a check (or whatever people do these days to pay bills).

I wonder if Nicholas Cage still owns the Lamborghini Miura SV that was previously owned by the Shah of Iran (the only Lamborghini model I like). The guys at “Cars of San Franciscio” (an exotic car dealer that was on Van Ness Ave. in SF in the 90’s) told me some great stories about Nicholas Cage and other actors and pro athletes (who almost all have crappy credit).

at least here in Arizona, subprime auto dealers get your 1st payment with another due in week.

when they don’t pay – oops, car won’t start since they put kill switch on it

Cage lost all of his New Orleans real estate except for this tomb in St. Louis Cemetery #1, as that couldn’t be taken from him. Not sure about the car, but I’d be inclined to wager no.

Loans are the bread and butter of the American consumerist version of capitalism. The new deal laws established fair loan provisions as well as usuary constraints.

What is being bought and sold is the mundane tendencies of the every day people.

There can also be cash flow issues even if you have a lot of assets, liquidity can be a problem and if a contract gets delayed or a strike happens you may end up way short of funds.

In the words of the Joe Walsh classic song:

I live in hotels, tear out the walls.

I have accountants to pay for it all.

Sometimes, it seems, they forget …

Don’t forget, his Maserati does 185…

But he lost his license – etc

Now he doesn’t drive …

My vote for the best guitarist and composer that defined an era.

dang – check out a movie called “Zachariah” from 1971. It’s free on youtube. Opens with the James Gang ripping through a tune called “Laguna Salada” in the middle of the desert. They later appear as villain Job Cain’s gunmen/backup band.

Great song and a fun film if you’re into acid induced western absurdism. Very early Don Johnson (yes that Don Johnson), Elvin Jones (John Coltrane’s drummer) as Job Cain, Dick Van Patton, Country Joe and the Fish. Looks like it was fun to make.

I am in mortgage lending. Many people with top 5% income levels are subprime. I’ve seen 100k in credit card debt, 12% car loan rates on 100k cars. Very common.

12% on 100k car is very common? That’s mind boggling. Maybe I’m on the wrong planet!

they have good incomes and only look at amount payment

Income affluent vs balance sheet affluent.

Plus tremendous swings in cash flow. That, more than anything tends to put a lot of people in subprime. One month you make $2k, the next you make 12k. So you live larger than the 7k average and instant subprime is born.

It is also how so many people get into trouble with their taxes, those variations encourage under withholding, and bam April comes and the bill is due.

It does appear we are now late in the expansion phase of the business cycle, so the recession will come, possibly sped up by chaos in the markets due to politics.

The correct term is “Big hat, no cattle.”

The correct term is “all hat, no cattle”.

Sometimes, convenience is more important than saving money. Especially when one has an excess of money.

As in rich people don’t have to wait in line to consume the normal needless things? The ones who are living day to day or homeless wait in even longer lines for their safety net “transfer payments” (I believe that is the econ term used here).

An article on how income and net worth are divvied up in this society is long overdue.

Social repercussions also may be close……one could almost say down to a matter of weeks/months, following the election, and apparent rapid fire changes.

‘Net-Worth rich’ and subprime may be rare, ‘income rich’ and subprime not so much. Just live above your means, possible at any level of income if you just try.

Sometimes it’s difficult to live according to a budget. Even the wealthy have budgets of a sort. When you get accustomed to a certain life style, it exerts a hypnotic hold on you which can only act as a hole you dig yourself deeper into…

Subprime is a credit rating, and implies someone has mismanaged credit regardless of their income level which can be very high. The paragraph under the first graph explains all of this very succinctly.

One can be rich or one can act like they are rich, but it is hard to be both!

From back in the day, MC Hammer.

According to Experian, as reported by CNBC last May, but with a lag back to Q1 2020:

Subprime Borrowers on average have $68,567 yearly income and an average $55,135 debt. Note that the median US income is ~$38,000. The Median recent college graduate (2023) is around $60k. So it looks like the typical Subprime Borrower makes enough money.

To continue with Experian:

Credit cards: 2.8

Credit card balance across all cards: $5,805

Additional retail / store credit cards: 2.2

Retail / store credit card balance across all cards: $1,799

Student loan balance: $36,389

Auto balance: $18,815

Mortgage balance: $163,505

Who are the subprime? Look for people wearing designer clothing, $100 haircuts, and driving BMWs. Believe it or not, I met several of them in the finance profession, early in their careers. The bill collectors would call them at work. They were mismanaging their own money while giving advice to other people.

If I’d be a subprime lender, I’d hope for a Covid 25.

H5N1 is a contender.

Well there is a case to be made that subprime lenders lend money to subprime quality borrowers. At a higher interest rate, which has always been a solid bet.

Which the acceptance is more a ritual of surrender than aggression.

Good analysis, I’m watching to see what happens to the 84 month loans turning into negative equity. We had several years of auto sales at and above MSRP pricing. Automobile manufacturers are starting to offer rebates reducing prices below MSRP. This will definitely affect used car valuations.

Just bought a brand new Honda Civic Hybrid for $2000 under MSRP 3 weeks ago. I looked at a few different cars and everyone was willing to go under MSRP except the Toyota dealer, who still didn’t have any inventory except plenty of trucks. I’m not a truck guy, but they were pushing them hard so I’m sure they would have gone well under a wildly excessive MSRP too.

Thanks! That’s good to know, we’re shopping for Civic Hybrid Hatchback and expect to buy in a few weeks.

Inventory seems pretty low still as it’s a new model, I get the impression dealers are nervous.

Strike my last comment. We just got quoted $38k …for a Civic. That’s a hard pass, back to shopping for used Priuses.

The separation of loan underwriting/origination and ultimate responsibility (risk of loss on loan) is absolutely key and almost inherently toxic – 2008 (and earlier) demonstrated that.

Product selling pitch people very much have a mind-set/personality type/incentive structure that prioritizes immediate sales over long-term *successful* sales (loans that don’t turn to sh*t).

So divorcing power (to “underwrite”/place financing) from responsibility (for making sure loan actually g*ddamn pays off) is like handing a live grenade to a 7 year old (they are unsuited to give a sh*t about long term consequences).

In *theory*, ABS buyers should recognize the perpetual risk of “adverse selection”/toxic crapola loans being sold into the marketplace and demand accordingly high interest rates – or smarter still, walking quickly away from the toxic waste dump.

But 2008 showed that is *very* frequently not the case because,

1) There are a lot of investment intermediaries out there with their own perverse/perverted incentives to place money in absurdly dangerous neighborhoods despite long term consequences and,

2) ZIRP encourages/forces the handing of *more* hand grenades to #1’s batch of 7 year olds (created by the political system’s own – large- batch of 7 year olds).

I apologize to the real 7 year olds whose morality (if not mentality) is almost always far superior to that of their toxic adult counterparts.

I do think that it is more like handing a 7 year old a mighty fireworks than a hand grenade. Reasonable safe for the one who light the fuse, not so for those in the direction of fire.

That securisation of debt lessen the risk for the originator of the debt.

“lessen the risk for the originator of the debt.”

But if the now-risk-shorn originator of debt is the one whose underwriting determined the qualification of the loan, there is a *huge* “moral hazard” problem created – since the originator/underwriter makes money from creating a likely crap loan (doomed to default) whose *costs* (default) are borne by the sucker/fool who buys the bundled crap loans in the secondary market.

The willfully blind originators profit from generating garbage (loans).

Even leaving aside the implications for *those* parties (quite possibly hustlers and fools…) an entire false lending ecosystem gets created where the level of alleged economic activity is misleadingly high, being basically founded on little more than an ocean of crap loans, doomed to ultimately default.

Tranched, securitized loan bundles segment out the risks, but *every* tranched security (CMBS, ABS, etc.) has 1+ toxic waste tranches at the bottom, where the highest risk of default is concentrated – those tranches shift risk from the higher rated tranches (which can still be pretty awful risk-return wise) and every securitized product has them. These sorts of “investment” products have only really existed for 30-35 years (wherein unprecedented levels of debt boom-bust have occurred).

Again, without those *toxic* risk tranches, no other part of the securitized loans can be sold – and those indispensable toxic tranche markets are the most skittish/unsalable/unstable (who really wants to gamble on investment time bombs, absent the bayonets of ZIRP, etc.)

The whole CLO/etc ecosystem can evolve into a thorough-going economic illusion (“look at our product sales levels!! Through the roof baby!!”) founded upon essentially fraudulent loan underwriting at the outset – since the loan originators/underwriters don’t bear most/all of the costs of making crappy, crappy loans.

This economic illusion can create a lot of collateral damage.

Having a excellent credit rating and able to borrow has been a curse on many, putting them in a deep debt hole….the sidewinding smiling deviant salesman showing the vulnerable lad all the colorful cars available.

Those corner used car lots that: “carry our own paper” always had a subprime profit motive.

That’s a different ballgame: they sell old junk that they have little money in, and they carry the note themselves. They don’t securitize.

They are sub-prime loans so I would expect more to default.

…Is this the crack in the dike??

Why is it seasonal?

Holiday spending and travel, including skiing, challenge budgets of subprime borrowers because they were already maxed out going into the season, r else they wouldn’t be subprime. Bankruptcies are also seasonal. Lots of stuff is seasonal.

Speaking of seasonal, I wonder what summer 2025 will be like? Especially with my other personal thoughts mentioned above.

Lost your job and behind on your car payment with no chance of catching up? There is only one sane course of action. High step down to Payday loan and borrow as much as they allow at 50% per month. Then put it all into $Trumpie meme coin while laying off say 20% into something stable and safe like $Doge coin. Wait a week and cash out…. becoming an instant mega millionaire. Pay back Payday, and then buy the whole car agency your ride is from and its gypo loan company. Problem solved.

Are there other tiers between Prime and Subprime borrowers for auto loans? According to CFPB and Experian, a FICO score of a prime borrower would be above 660 and subprime is below 620. I would be curious the long-term trend of those in between 621 and 660. Also when lenders package them as an ABS, what tranches are considered prime, above single-A or even higher than that? Do the ratings on the tranches factor in LTV and other calculations beyond just the credit-worthiness of the borrower?

If you draw one dividing line, there’s prime and subprime — like the line between “investment grade” and “high-yield” (“junk”) in the bond world.

If you slice it up further, there is super-prime, prime, near prime, subprime, and deep subprime.

I agree but suggest that the only fairly priced Fed issuance is the short term FFR treasuries.

If one were to read to the bottom of the cogent article they would find Wolf’s summary, “What happens when the cycle turns as delinquencies get out of hand, the most aggressive subprime auto-dealer-lenders get in trouble.”

As I have espoused, anyone who buys a piece of crap car built in this century is a moron.

I hope you enjoy driving your old deathtrap junk and live through it when you have an accident.

My 30 year veteran fireman just ordered a new Ram truck 2025 model says the safety features are outstanding. Our health is paramount the older model vehicles especially anything without side airbags are risky if one can afford the higher price why not ?

Well,I do drive a few older vehicles from the 80’s,that said,well maintained/built to the hills 4×4’s.

I would love to as said before get meself a old diesel rabbit 4 speed like I had in the 80’s,ease to maintain and 40 + around town.

I while excepting say air bags feel one will do fine in a older vehicle accident wise but to each their own.

The new vehicles with all their “gadgetry” push me over the edge especially maintenance but you want new and have a good tech go at it.

We have a Kia dealer in area that’s been around for decades,lifetime drive train warranty as long as you keep on the basic maintenance,really looked but just couldn’t do it!