If the rate of decline over the past 10 years continues, the dollar’s share will sink below 50% by 2034.

By Wolf Richter for WOLF STREET.

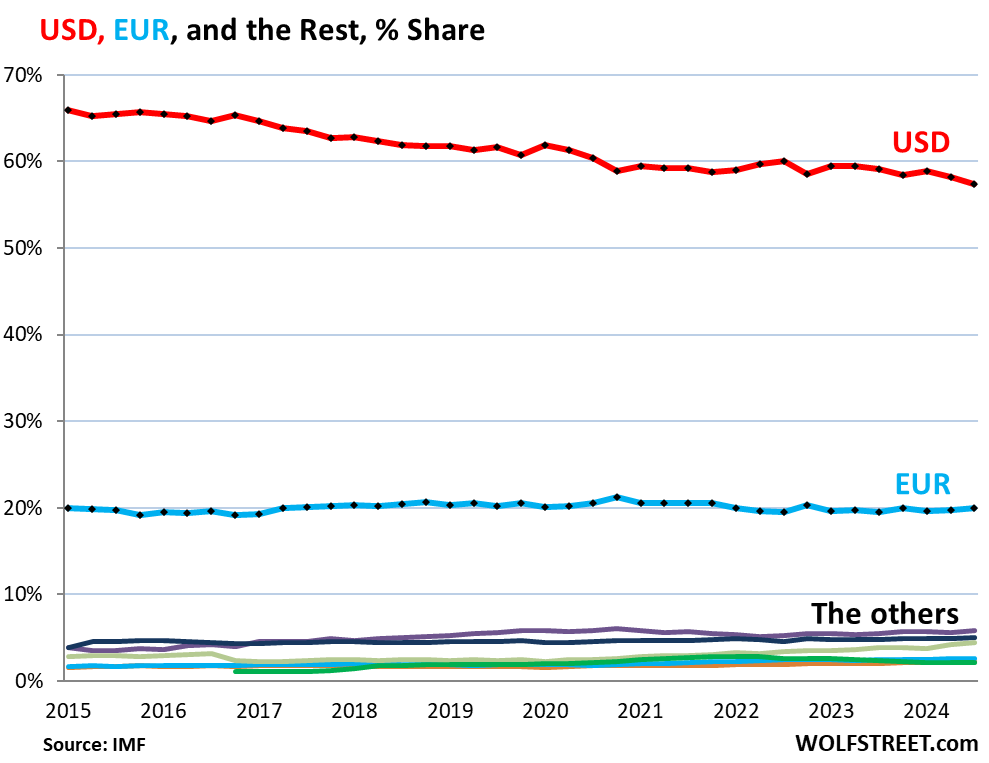

The US dollar lost further ground as global reserve currency among many reserve currencies held by central banks. Its share has been zigzagging lower for many years as central banks have been diversifying their holdings to assets denominated in currencies other than the dollar. And they’ve also been diversifying into gold. But the dollar remains by far the dominant global reserve currency.

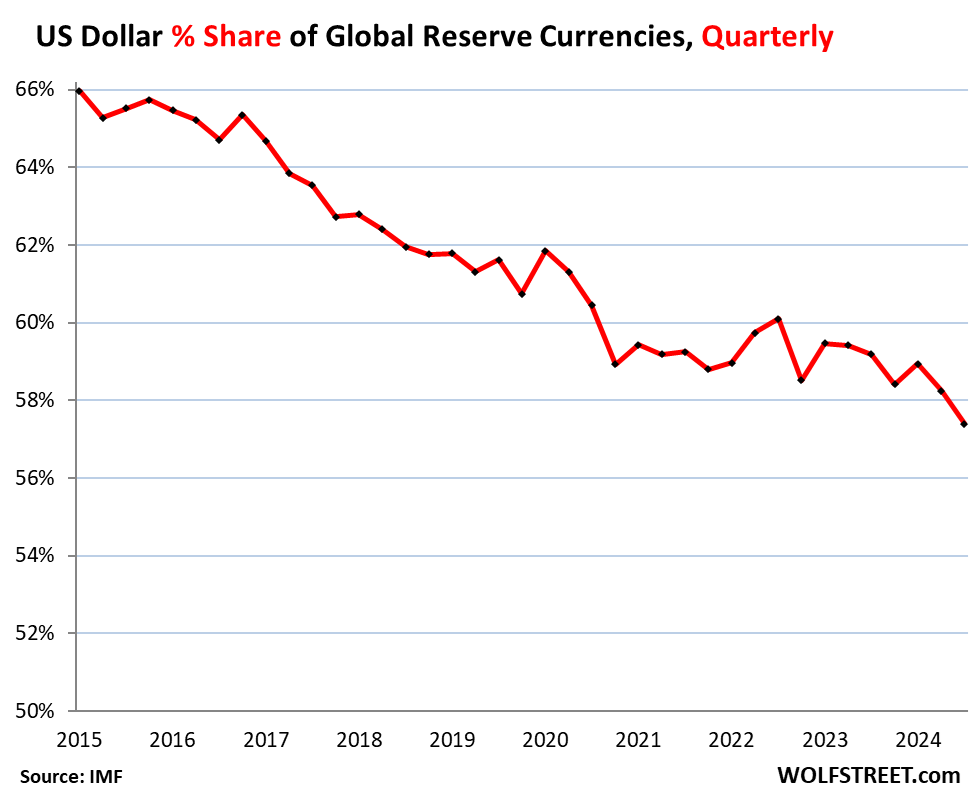

The share of USD-denominated foreign exchange reserves fell to 57.4% of total exchange reserves the lowest since 1994, according to the IMF’s COFER data for Q3 2024. USD-denominated foreign exchange reserves include US Treasury securities, US agency securities, US MBS, US corporate bonds, US stocks, and other USD-denominated assets held by central banks other than the Fed.

In Q1 2015, the USD’s share was still 66%. Over these 10 years, the dollar’s share of global reserve currencies has dropped by 8.6 percentage points. If this pace of decline continues, the dollar’s share will fall below 50% in less than 10 years, by the end of 2034.

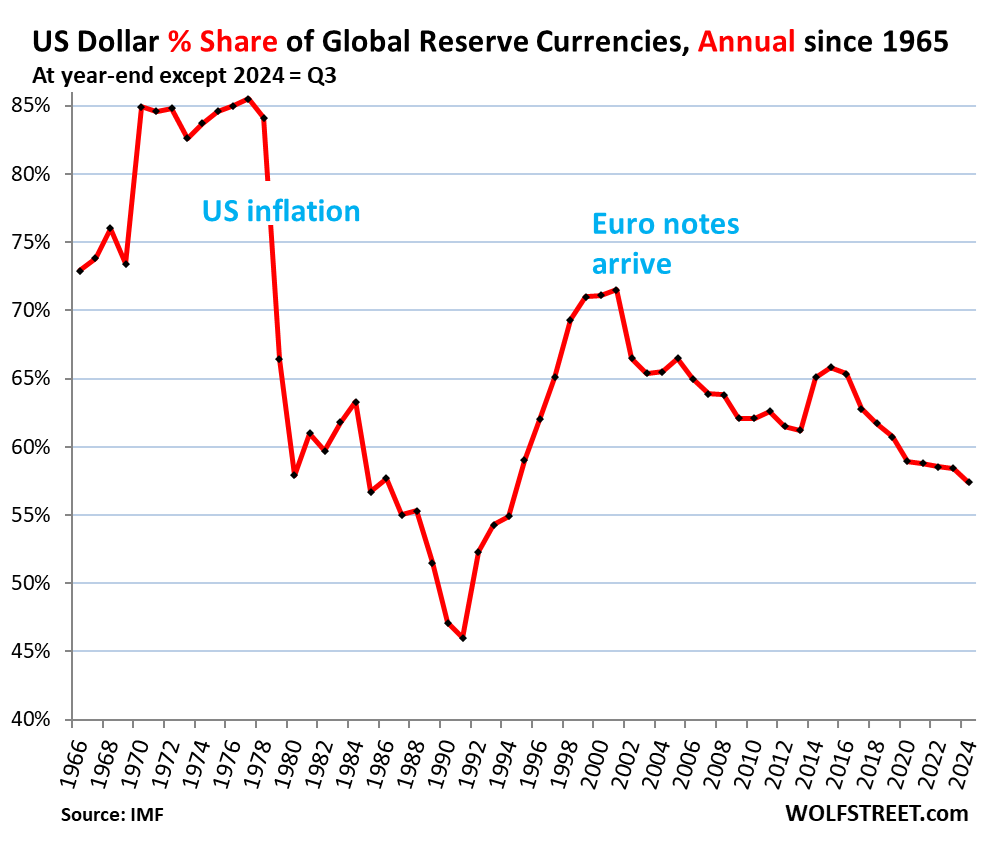

The dollar’s share had already been below 50% in 1990 and 1991, at the final leg of its long plunge from a share of 85% in 1977 to 46% in 1991, after inflation had exploded in the US in the 1970s, and eventually the world lost confidence in the Fed’s ability or willingness to get this inflation under control.

But by the 1990s, central banks loaded up on dollar-assets again, until the euro came along. This chart shows the dollar’s share at the end of each year (2024 = Q3).

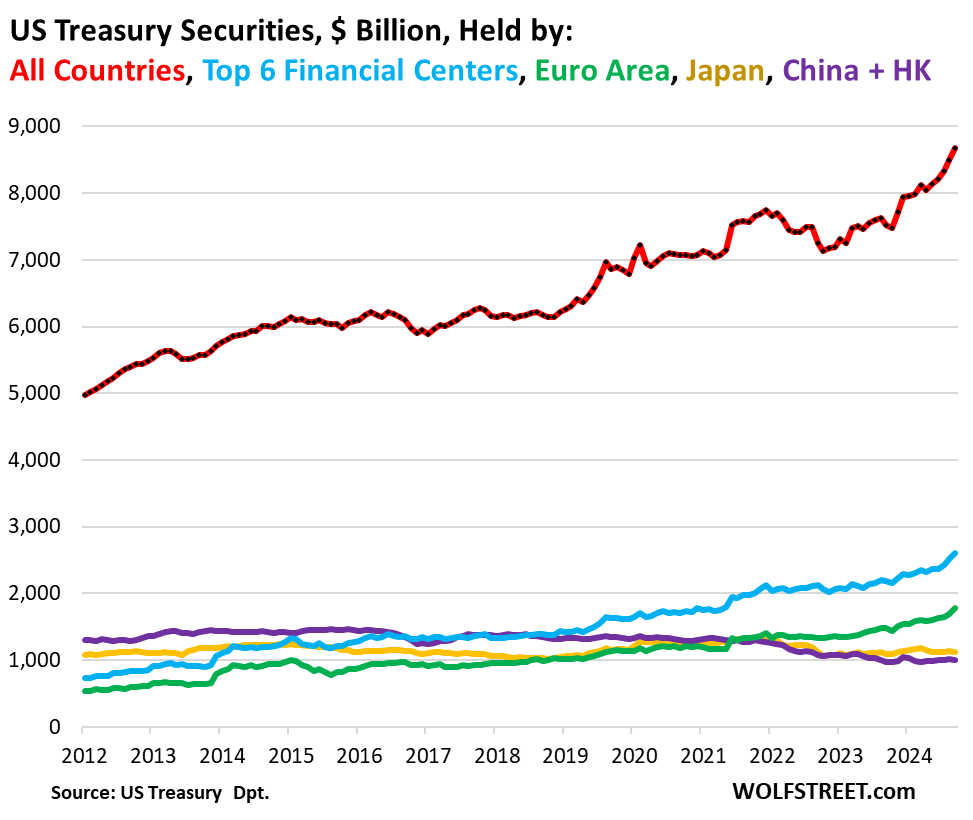

But they’re not dumping US Treasury securities.

Holdings of US Treasury securities by foreign central banks and other foreign holders have surged from record to record. Over the past 12 months, foreign holders added $880 billion, bringing their stash to a record $8.67 trillion, according to the Treasury Department’s TIC data earlier (we discussed the details here).

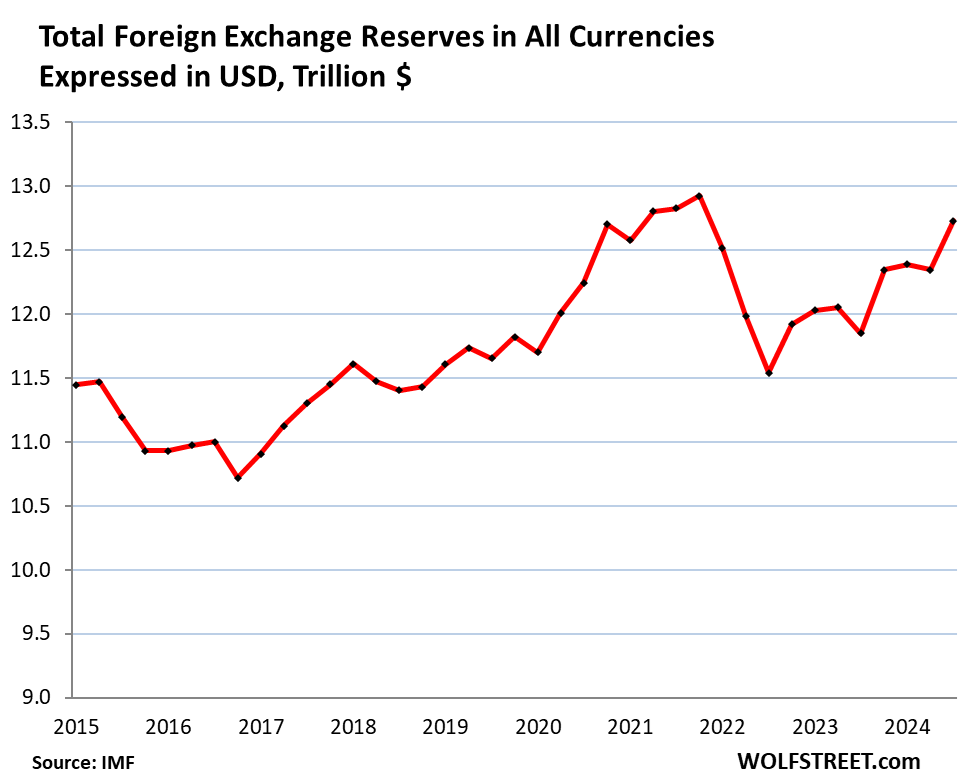

Total foreign exchange reserves.

Total foreign exchange reserves.

Central banks holdings of foreign exchange reserves denominated in all currencies, including in USD, rose to $12.7 trillion.

Excluded from the total are any central bank’s holdings of assets denominated in its own currency, such as the Fed’s holdings of Treasury securities and MBS, the ECB’s holdings of euro-denominated bonds, and the Bank of Japan’s holdings of yen-denominated assets.

Top holdings, expressed in USD:

- USD-denominated assets: $6.77 trillion

- EUR-denominated assets: $2.37 trillion

- YEN-denominated assets: $0.69 trillion

- GBP-denominated assets: $0.59 trillion

The other major reserve currencies.

The euro’s share, #2, ticked up to 20.0%, the highest since 2022. But the movements have been small. The euro’s share has been around 20% for years (blue in the chart below).

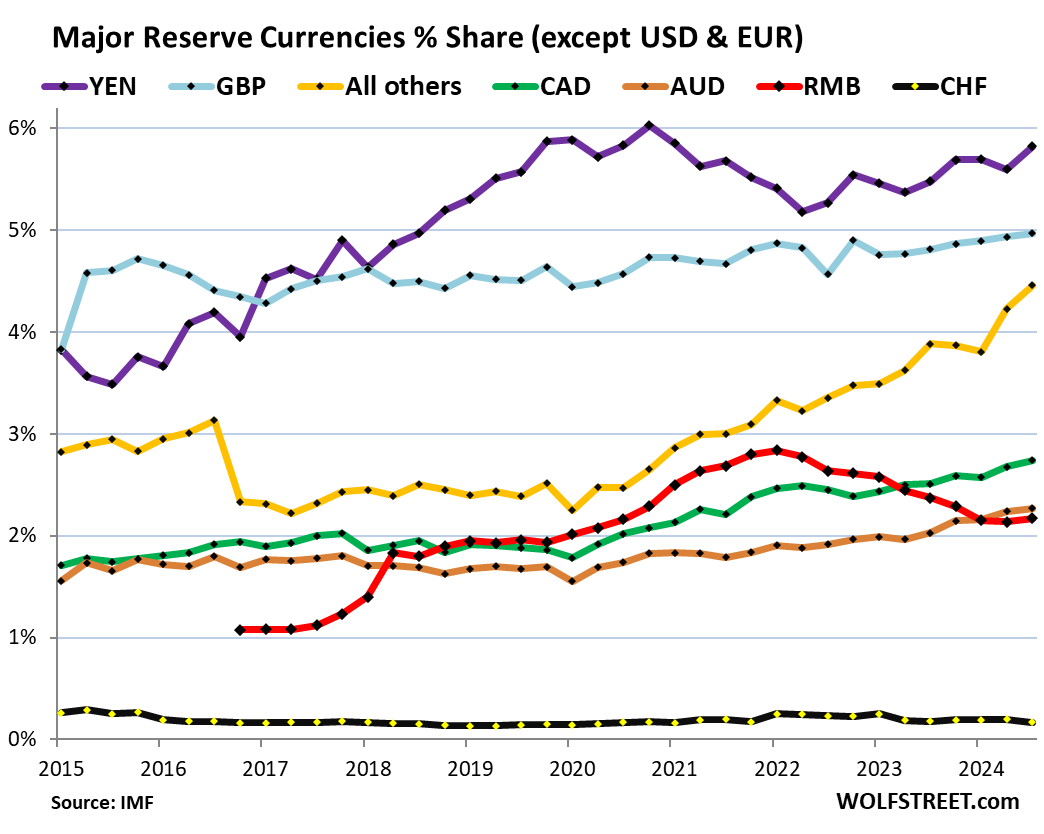

The other currencies are the colorful tangle at the bottom of the chart. More on those in a moment.

The rise of the “nontraditional reserve currencies.”

We will now hold a magnifying glass over the colorful tangle at the bottom of the chart above.

These other currencies, except for the Chinese renminbi, have all been gaining share, at the expense of the dollar, while the euro’s share has remained roughly stable.

This includes the basket of “nontraditional reserve currencies,” as the IMF calls them, that are combined into “All others” (yellow in the chart below), whose combined share has been surging since 2020.

China is the second largest economy in the world, but its currency plays only a small role as a reserve currency. And it has lost ground against the USD and other currencies since 2022.

In 2016, the IMF had added the RMB to its basket of currencies backing the Special Drawing Rights (SDR). That was a big step, and lots of folks thought that the RMB would quickly become a threat to the dominance of the USD as global reserve currency.

But central banks have not been enamored with RMB-denominated assets for a variety of reasons, including capital controls, convertibility issues, and other issues. Last year, the RMB was surpassed by the Australian dollar (AUD).

Far behind the USD and the EUR, the largest currencies by share:

- Japanese yen, 5.8% (YEN, purple).

- British pound, 5.0% (GBP, blue).

- “All other currencies” combined, 4.5% (yellow).

- Canadian dollar, 2.7% (green).

- Australian dollar, 2.3% (brown).

- Chinese renminbi, 2.2% (red).

- Swiss franc, 0.2% (blue).

Central banks diversify from the USD to other currencies.

The IMF found that there were 46 “active diversifiers” among central banks, including central banks in most of the G20 economies, according to a paper it published in 2022. It defined them as central banks that had at least 5% of their foreign exchange reserves in “nontraditional reserve currencies.”

Two factors contributed to the rise of the “nontraditional reserve currencies,” the IMF found:

- The growing liquidity of assets denominated in “nontraditional reserve currencies,” which makes them easier for central banks to trade in the quantities they deal with.

- Chasing higher-yielding assets elsewhere during the 0%-era in the US and Europe.

USD exchange rates impact foreign exchange reserves.

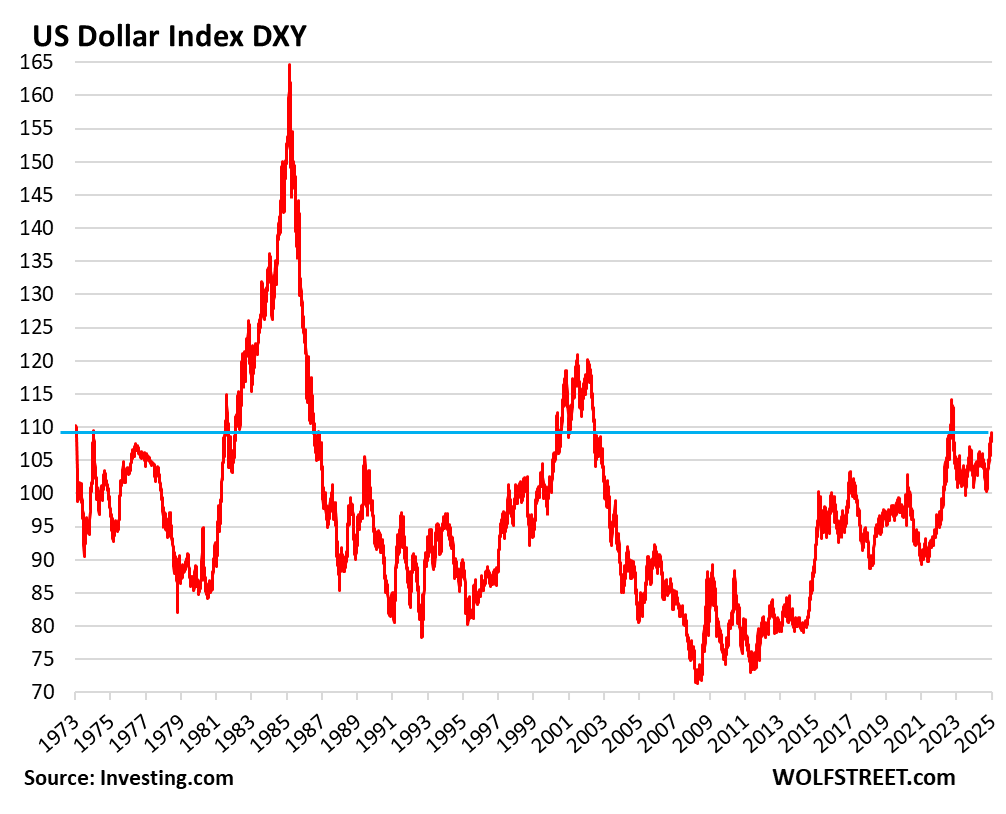

The USD has risen sharply against a basket of other currencies in recent months, as tracked by the Dollar Index [DXY], but remains below the 2022 high, well below the 2001 high, and hugely below the 1985 high. So we see these huge peaks and valleys, but now the dollar is about where it had been in 1977.

The DXY is dominated by the euro and the yen, the two largest trade currencies behind the USD. When euro arrived on the scene, the DXY’s local currencies that became part of the euro were replaced by the euro. At the DXY was started in 1973. Today it’s at 108.9 about where it had been during the high moments in 1973-1975 (data via YCharts):

Why this matters: The IMF reports foreign exchange reserves in USD. USD holdings are obviously reported in USD. But the holdings in EUR, YEN, GBP, CAD, RMB, etc. are translated into USD at the exchange rate at the time. So the exchange rates between the USD and other reserve currencies impact the magnitude of the non-USD assets – but not of the USD-assets.

For example, the Bank of Japan’s holdings of USD-denominated assets, expressed in USD, don’t change with the YEN-USD exchange rate. But its holdings of EUR-denominated assets are translated into USD at the EUR-USD exchange rate at the time. So the magnitude of Japan’s holdings of EUR-assets, expressed in USD, fluctuates with the EUR-USD exchange rate.

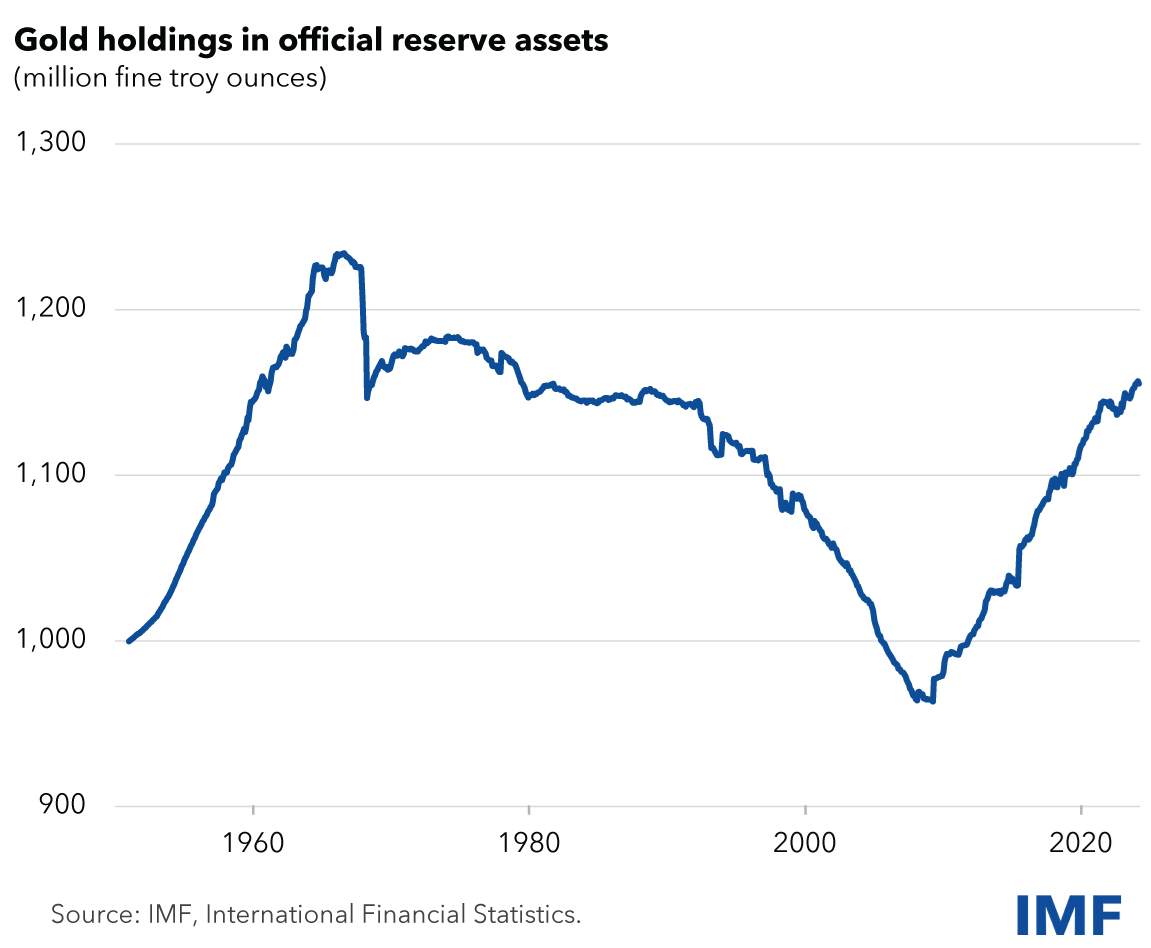

The other diversification: gold.

Gold bullion is not a “foreign exchange reserve” asset of central banks, and is not included in the data above. Instead, it’s a “reserve asset,” not involving foreign currency.

Central banks had spent decades unloading their gold holdings. But about 10 years ago, they started rebuilding their stash.

According to the IMF, central banks’ gold holdings have surged over this decade to 1.16 billion troy ounces – roughly $3.08 trillion, compared to $12.3 trillion in foreign exchange reserves (chart via the IMF):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

There is no other currency that even comes close to challenging the US Dollar either now or in the foreseeable future.

All the China hype of my youth looks very silly in hindsight. China has devolved into a stagnant economy with enormous debts, and it still hasn’t surpassed the USA in GDP. Most of the dominant currencies are either Western or Western-aligned (like Japan), and we are now in a tense period geopolitically. BRICS+ is trying to play catch up, but it will be difficult – a lot of this alliance is hampered with dysfunctional economies and disreputable currencies. I don’t see it living up to the hype either, any more than China itself did.

china still has an enormous, growing educated population. their corruption and limits on personal freedoms harms them, but they’ll be a formidable foe, debt aside, if they get that stuff under control.

China’s really big long-term problem is property rights.

Until credible property rights reform is incorporated into their long-range planning, the Remninbi and/or BRICS dominance is a dud.

IMHO.

the u.s. isn’t a paragon of property rights these days either. ever since the supreme court decided that the government can seize private property to give it a developer to build a mall, and when police can destroy someone’s house to get a shoplifter and not reimburse,

Touché. It’s all relative, and in perpetual flux.

“East is west and west is east, and soon the twain shall meet.”

Would rather live in US, all the same…

yep agree. the u.s. needs to permanently get rid of civil forfeiture if it wants to claim to have private property rights. that means that no forfeiture absent a criminal conviction.

i’m tired of hearing about cops seizing cash and then holding it until the person can prove it’s legit. wtf.

No, they have an aging and decreasing population

no, i meant the educated share of the population is growing.

Some societies such as German carry cash instead of all kinds of plastic cards. Some municipalities in the U.S.A. seize cash until it’s been proven to be legitimately obtained. It’s one reason why there are certain areas in the U.S.A. one should never set foot in. Who knew what that cash actually smells like, right ? Cocaine ? Cannabis ? Heroine ? 😂

Labor fueled growth -> Capital Squeezes labor for one last puff of massive growth -> capital shifts from investment to rent seeking and destroys growth.

Welcome to the 3rd phase, China. We’ve been here since 2001. -USA

CSH. I recently saw a chart somewhere (not sure where), that compared Chinese to USA manufacturing. But they were using something that I think was being calling PPP.

GDP may be a poor measure. Here is why. If a new car in China costs $6,000 and a similar car in the USA cost $65,000. Then using GDP the USA is ahead. But using this other measure, the Chinese were equal.

Perhaps some other quant can clarify this issue.

PPP you’re referring to Purchasing Price Parity – in other words, not based on formal exchange rates, but rather what it takes to purchase the same basket of goods in each country. For example, let’s say per capita GDP in the US is $82,000, and per capita GDP in Canada is $53,000. But (and I’m making these figures up) what if Canada’s $53,000 buys the same housing, transportation, food, medical, etc, as $82,000 in the US. Based on PPP, the two countries would be considered to be equal.

Japan and SK have set the bar for what a developing nation can become. It was indeed quite silly to think China could meet or surpass that.

Parts of China are already better than SK and Japan

SK is particularly a bad example consider its low wages and high prices.

I’m trying to reply to @Typecheck but I can’t. Here’s my comment for @Typecheck – it doesn’t matter what “parts” of China do or don’t do. That’s like saying people in Silicon Valley make more money than people Anniston, Alabama. The truth is that the wealth disparity in China today is greater than it has ever been. Much greater, in fact, than when the communist revolution occurred due to… wait for it… income disparity. The issue is NOT what the tiny minority of wealthy Chinese are doing. The issue is what the huge majority of lower class Chinese are doing – when they look at your elite “parts of China”.

China produces 8x the number of engineers every year as the US. And no, their average engineers are not all dummys and our average engineers are not all Tony Starks…sometime quantity itself is a quality all of it’s own.

Chinese save 30%+ of their income which covers a lot of fiscal sins.

A nation of 1.2 Billion (or whatever it is) could not possibly afford the kind of neo-liberal political disorder we label as “Democracy”. Our current government is evolved to maintain the status quo through the appearance of change. The current Chinese government is aimed at the same except in a narrower sense.

China certainly has it’s problems, but their problems are none of our business just like our problems are none of their business.

CSH — before it was China, it was JAPAN (a great excuse to re-watch the classic Die Hard, from back when we all thought the Japanese were going to buy the U.S. out from under us). Far back as I can remember, Japan was the big bad boogeyman that was going to teach Americans the foolishness of their spendthrift ways.

Before that? Probably the USSR, but I’m guessing. (Germany maybe?)

CSH, China has already surpassed the US in PPP (purchasing power parity) adjusted GDP.

A lot of US GDP is composed of economic rents — here’s a hint: those don’t produce anything.

I would recommend that you don’t take very seriously GDP statistics absent any consideration of their composition — failure to do so leaves you with a map terribly unrepresentative of the territory …

PPP GDP is a formula that distorts results by the way it is constructed. It has been debunked many times, and you can read this debunk material on Wikipedia even.

This is the scariest scenario. As long as China had hope for a seat at the big boy table they were determined to play by the rules of the international order. If they become disillusioned with the rules of the game, feeling like Charlie Brown with the football, they may respond with violence. That wouldn’t have been bad 10 years ago, but now they can cause real trouble.

Nonsense

What do you replace it with?

The yuan? eurodollar?rupie?peso???

Gimme a break

Not a chance

Absolutely

no other currency, sure, but something else has already challenged the u.s. dollar, assets.

the dollar is only doing well against other currencies. pretty much all currencies are doing horribly against gold, stocks, crypto and real estate.

in other words, nobody trusts any of the central banks, and buys assets instead.

sure, people will hold dollars to use for trade, but then they take them and try to buy overpriced tech stocks with them, like the swiss central bank did.

Central banks have started to rebuilding their stash of gold.

And then is the other non cash stash nations hold. China have built a strategic oil reserve. Where I live the government is rebuilding the reserve of wheat and sugguar. It look like building reserves of comodities if they where counted would erode the US dollar as a reserve.

That isn’t a challenge for the USD; it is a boon. Increasing asset prices benefit those who hold assets and no one holds more assets than the US and its citizens. The wealth disparity between the US and the rest of the world continues to widen, which makes the USD even more valuable.

this is exactly backwards. the value of the dollar is what the dollar can buy. period.

Those with means buy assets. Those without get poorer and the gap increases.

BRICS has literally decimated the USD by going back to the gold standard! Smart move!!

🤣❤️👍

But India, a BRICS member, has said they would not challenge the US dollar’s place as a reserve currency.

I think the decline over the past few decades of the US dollar’s place as a reserve currency can be explained by China’s rise, and in the past few years by efforts by China and India to avoid US sanctions kn Russian and Iranian oil by using non-US denominated currencies.

But China is in a period of economic stagnation and faces other problems. It seems to that they may be reaching the limits of their foreign investor- and export-driven economic model, and are also reaching the limits of their population’s ability to absorb the pressures of the relentless industrialization and urbanization of recent decades.

That’s why I don’t think the trend of the decline of the US dollar’s role as a reserve currency will continue to a significant extent in the near to medium future.

Spot on, in addition the Chinese have a serious demographic problem that is unpressinented in modern times…

👍That’s evident. Otherwise Donald wouldn’t even care to sound out threats to countries dumping dollars. Jokers here are living out their dreams.

Ehh..the gold standard is a two sided coin. Yes it keeps the value of a currency stable. But gold limits the growth of the money supply and the access to credit and capital funding. This limits the growth of GDP. Let’s take look at the global rotational OTC derivatives market. It is currently valued around $667 trillion dollars. The foreign exchange derivatives market is valued at $118 trillion dollars. My point with all of this is that no country has the complexity and depth of its financial markets to take on the responsibility of issuing the world’s reserve currency other than the United States. Do we manage it perfectly? No, Triffin’s dilemma shows that a nation’s domestic and international interests compete against each other and cause economic pain for other countries. It’s not a perfect international monetary system, but it is one that has been the most successful for over 80 years.

Gold, other hard money and monetary systems with fixed amount of money places some constraints on who can provide capital and who get the earnings. It make it difficult to have a income without working.

And yes, fixed amount of money may limit growt. On the other side, those preaching growth have never understod exponential functions.

Very obviously, the BRICS have done no such thing at all.

Sarc???

Sad how the oligarchs in America let the United States go from being the world’s producer to the world’s consumer society living off of debt all for quick profits. Even sadder how in the process they allow the declassing of the American people to do it. China will probably surpass the United States – if it hasn’t already – for two reasons: it has the productive capacity and is a planned economy. The two same characteristics that made America Great after WWII.

A first for me. First to comment and sadly nothing to add. Hope you all are having a great 2025.

I can’t wait to see how it all shakes out.

A Happy New Year to you too and may 2025 be a great year for all!

Covering gold last and without much comment is like the TV series where something is expected to happen and…..end of episode, see you next time….

What is there to say about gold other than that its primary purpose is for use in jewelry and its aggregate value is less than 1% of all of the other assets in the world now?

Hmmm… maybe I am not understanding. So foreign Central Banks are dumping US dollars but not US Treasuries?

1. They’re not dumping “dollars.” No one can dump dollars. Dollars are just a currency (a measure of value), like miles or pounds are measures of distance and weight. Even the paper dollars in your pocket are “Federal Reserve Notes,” they’re interest-free loans you made to the Federal Reserve, a dollar-denominated asset for you, and a liability for the Fed.

2. But you can dump dollar-denominated assets, such as, as I said in the article, and I quote, “USD-denominated foreign exchange reserves include US Treasury securities, US agency securities, US MBS, US corporate bonds, US stocks, and other USD-denominated assets held by central banks other than the Fed.”

3. But they’re not dumping dollar-denominated assets overall. See chart below of total holdings of USD-denominated assets. They’re diversifying — they’re ADDING new assets denominated in other currencies. They might dump some dollar-denominated assets, such as corporate bonds or stocks, while piling on Treasury securities. We know they’re adding to their Treasury holdings. So they’re getting rid of some other dollar-denominated assets.

Wolf-

You wrote: “But they’re not dumping dollar-denominated assets overall. See chart below of total holdings of USD-denominated assets. They’re diversifying — they’re ADDING new assets denominated in other currencies.”

When you say “they,” to whom do you refer, and how is the decision to “diversify” into foreign-denominated assets (and which assets within each currency pool) made?

Are these holdings decisions determined by CB committees, or are they somehow commerce-driven, or depositor driven?

Apologies if stupid or off-topic question. Thanks for any insights.

“They” is lots of individual central banks. You can ask central banks yourself how they make this is decision. I’m sure they have a phone number somewhere you can call. What we’re looking at here are the result.

John —

The World Gold Council actually polls central bankers regarding the reasons for their decisions.

I don’t know how the decision gets made (committee meetings or diktat) but that’s a good place to start wrapping your mind around the motivation.

…But the #1 reason, weirdly, is “historical position” — in other words, “We have gold because we have gold.”

¯\_(ツ)_/¯

What is the rate of overseas bank participation in treasury auctions? Falling pretty sharply of late, isn’t it?

China dumped hundreds of billions worth of US treasuries in the last few years. Though they’ve slowed down a bit.

So what?

https://wolfstreet.com/2024/11/18/us-treasury-debt-held-by-foreign-investors-ravenous-appetite-for-juicy-treasury-yields-juicy-compared-to-their-stuff-at-home/

They need the money. China is in the largest real estate crash in history.

The more people holding them US dollars, helps spread out inflation throughout the world.

With all of the talk about BRICS, it appears it is still in the blockchain stage and not a threat to the USD as a global exchange unit or am I missing something?

Check the plunge of the currencies of the BRICS countries against the USD (except the RMB).

Right. I’m no great prognosticator but when I see the countries in BRICS my first reaction was to laugh. But that’s mean.

The U.S. will have to screw up very badly to lose dollar dominance. Unlikely but not impossible, given our one-eyed foreign policy over the years. Still, with military bases all over the world I can’t see a significant number of countries backing a different horse.

It would be great, though, to see the financial sector getting spooked and forced to shift their focus to consider investing in infrastructure and manufacturing and building a car that someone wants to buy.

Manufacturing will never come back to the US, stop dreaming

The flip side is that holding gold is the result of central banks off-loading their currency and devaluing, i.e. not specifically because they actually want reserves!, and its harder to do with the dollar because 1) reversing this trade looks shaky 2) opposition from the USA.

Obtaining “reserves” getting harder. Gold is a very innocent reserve asset as its nobody’s main unit of currency.

“Gold is a very innocent reserve asset as its nobody’s main unit of currency”…

Sometimes things are simply decreed. For example, Uncle Sam dictates what I can use to pay my taxes. Regarding gold, it has remained the preferred collateral of the world for 5,000+ years…

If I were to summarize the world from a banking perspective I would simply say that I see a lot of liquidity/currencym but relatively little money-good collateral.

The only constant in life is change. Eventually the current system blows up or is abandon for a new system. The “currency” will change, the collateral (i.e. productive business assets, gold) won’t.

Hedge accordingly.

Gold even at its present value is only worth about 1% of the other assets of the world and is of no financial relevance whatsoever.

Your obvious disdain towards gold comes from an obvious ignorance about it, but you do you SoCalBeachDude.

Gold is a tier- one asset at the BIS, the central bankers’ central bank.

Most all the primates that I’m familiar with have a tendency to really enjoy a shiney object to play with from time to time.

The striking thing in those graphs is how total foreign exchange reserves have barely moved from 2012 to 2024. (around 11.5tn to 12.7tn looking the graph above.)

Compare that to the national debt 16tn in 2012 to 35tn in 2024. Or S&P 500 1426 in 2012 to 5881 in 2024. Or CPI of 229 in 2012 to 314 in 2024.

Still sizable, but not as important as they used to be.

That is an interesting observation. Do this indicate that less of the worlds money are hold as reserves by central banks?

If so, more of the money is circulating or hold by private enteties.

Thanks Wolf. A major difference between today and the 70’s/80’s is that central banks around the world have been openly working together on monetary issues. It’s been a “race to the bottom” for quite some time folks and the Federal Reserve Note (FRN) remains the cleanest dirty shirt in the laundry. The FRN is, to a large extent, backed by petroleum, one reason that the U.S. has increased it’s production. All fiat currencies rely on TRUST/FAITH, sometimes implemented with force (military might). As others have already pointed out, in the absence of a more “trustworthy” alternative, the majority of trade will continue to be conducted in FRNs. TRADE is really the only thing that matters to the global economy. If the exchange of goods/resources and services stops, then all hell breaks loose.

Same as it ever was…

We’re like the bad banker in monopoly, and the other players keeping a close eye out. Got to remember to get your 200 dollars when you pass “go” or your SOL…a good banker would make sure I got my 200.

On the game of monopoly: Try a few games where when you go past go you get nothing. Then try a few games where when you go past go you get $1000. For me the takeaway was, a little socialism goes a long way toward keeping the game going.

We are still cruising on our exorbitant privilege of the dollar as the world’s reserve currency of choice, along with the Euro subsidiary. And guess what, most of the rest of significant holdings are first world western countries as well. Might as well call most of the other alternative currencies a failure.

Indeed, one can sort of laugh at the thought of the brics challenging the dollar hegemony. The reality of the ruble is a continuous drop of 25 to the dollar fifteen years ago to 100 to the dollar today in the laughable official exchange rate. They can’t even manage stability for five years outside of China’s nonconvertible currency. If you are losing value against the US Dollar, which is slowly losing value, then you are a dirtier shirt, and money will flee, and your banking system will suck.

In short, we complain while others endure a much quicker slide in value. Continuously going only one way. The only question is how fast.

Nobody is doing a great job with their money management, it’s just obvious who is doing the worst. Further, so many payment apps let you do cheap currency conversions, which allows a bit of store of value in countries with total garbage currencies. The true irony is a stable coin tied to something like gold will probably provide the most long term stability, but it would be near suicidal to borrow in that currency.

Someday this war’s gonna end…

15 years ago? LOL!

I was in the Soviet Union in the 90’s and, depending on the day, it took 8,000-10,000 rubles to buy a dollar, so, from that perspective, they have improved the Ruble’s purchasing power. The question I have for western countries is; Doses the DEBT/GDP ratio matter or not? You might want to investigate Russia’s numbers…

According to Bernanke, “debt doesn’t matter” because the Fed can always print and purchase it. This is technically true, but pushed to an extreme Americans get to experience Soviet life in a hurry.

“…from that perspective, they have improved the Ruble’s purchasing power.”

LOL, no, they just chopped off 4 zeroes in the 1998 ruble revaluation, when 1,000 old rubles become 1 new ruble.

Still priced against the FRN Wolf. That is a fact. I have to spend more FRNs to get the ruble now! Again, purchasing power matters. I am sure CONgress will get right on balancing that budget…

LOL!

WB,

Such ignorant BS. During the times or the Iron Curtain in the early 1960s, the official exchange rate was set at about 1 ruble to $1. Obviously, this created a black market and the whole thing went downhill quickly. So in August 1996, I bought 5,000 rubles with $1. The ruble had already lost most of its value against the USD. And it kept losing value against the USD. Then in 1998 came the Russian Financial Crisis, and the ruble collapsed further. So a new ruble was invented with the value of 1 new ruble = 1,000 old rubles. And people exchanged their 1,000 old rubles for 1 new ruble, and the 100,000 old rubles in your bank account became 100 rubles in your bank account overnight, and a ruble-billionaire became a ruble-millionaire overnight. By the end of 1998, the new ruble had collapsed to 20 new rubles (= 20,000 old rubles) to $1. Now you can buy 107 new rubles (= 107,000 old rubles) with 1 USD.

I see what you did there AllenM – to which I can only say:

“Charlie don’t surf!!!”

Dominant reserve currencies seem to last between 80-110 years….without fail. Portugal and the Netherlands 80 years, Spain the longest at 110. US is at 101.

Which brings me to remember the old…

“More money has been lost because of four words than at the point of a gun. Those words are ‘This time is different.”

― Carmen M. Reinhart, This Time Is Different: Eight Centuries of Financial Folly

And:

“The lesson of history, then, is that even as institutions and policy makers improve, there will always be a temptation to stretch the limits. Just as an individual can go bankrupt no matter how rich she starts out, a financial system can collapse under the pressure of greed, politics, and profits no matter how well regulated it seems to be.”

― Carmen M. Reinhart, This Time Is Different: Eight Centuries of Financial Folly

It isn’t a question of If, it is WHEN. And what fuels eventual decline is excessive debt taken on in good times, then breaking bad when change gives a big push. I’m pretty certain the US is not immune from change and excessive debt.

I remember listening to a talk given by a British-Canadian historian named Gwynne Dyer. His conclusion was it was inevitable in the near/distant future that the US reserve would decline and lose status, and just get over it. Life doesn’t come to an end for citizens, it’s just different.

And it isn’t overnight, this article indicates a slow decline. However, tariffs, threats, chaos, and ever more and more debt does not portend a steady tiller. My personal conclusion has always been to avoid debt as much as possible and limit careful speculation to hard assets….live within my/our means. There is a lot of disarray out there right now, in every country. We need a more long term approach to finances and fewer rapid reactive fixes for political gains….in every country.

Good luck to all and have a good 2025. Hang on, imho.

PAUL S. Did your Carmen M. Reinhart cover the topic of war ?

If you want to speed up the demise of a paper currency, get involved in a war. And if you really want to see how fast a currency can go to Hades in a handcart, lose that war.

Life may not come to an end but it sure isn’t rosy. See the gradual decline of the economies in the Euro zone and GB.

A weak currency is not a cause; rather it is a symptom of a weak, noncompetitive economy.

So the USD has been strong recently and the other currencies have been weak.

Just like it was during Volcker’s time.

Current account deficit since we became a debtor nation in 1985

20,201,902T

I confused the trade deficit with the current account deficit. It’s much worse than I thought.

-63,635.356

billions of dollars.

” In economics, the current account measures the nation’s earnings and spendings abroad and it consists of the balance of trade, net primary income or factor income, and net unilateral transfers, that have taken place over a given period of time”

63 trillion invested in the balancing items, our stocks, bonds, real estate etc.

The wild card is AI and yes I know there is no real intelligence yet, but there is speed. We can buy and sell assetts faster and faster.

Soon we will be able to exchange anything for anything on a global scale instantly. There will be less need for reserves or reserve currancies.

They (most of the world) do not think highly of us and all the control we add to using dollars. Embargoes and tariffs would no longer harm them.

They will by paying far less and we will be driving a piece of crap ford at twice the price.

If the dollar is so great, please explain crypto and stock prices.

“If the dollar is so great, please explain crypto and stock prices.”

One word: MANIA

Excess liquidity leads to all kinds of capital mis-allocation. Duh.

You can explain crypto and stock prices in a single word: excess

The World Gold council talks about “country central bank gold holdings”, without the definition of whether these are paper promises to deliver — such as IOUs from a bullion bank or SPDR gold trust shares — or physical metal.

For the latter, I have been unable to find any concrete proof of physical delivery. So who knows how much of these gold “holdings” are real.

“Under Basel III, physical gold has been reclassified as a Tier 1 asset, a category reserved for the safest and most liquid assets, such as cash and high-quality government bonds.”

So, presumably the reported central bank gold holdings are specifically physical and not paper. Not open to debate. One can argue whether the reported holdings are accurate, but that is not the same question. You know the old joke about Ft. Knox and doubling the guard. Some claim that China under-reports their holdings, so who knows whether the numbers are accurate except insiders within each central bank. Gold lending and rehypothecation are also legitimate concerns, not to mention unwitting holdings of gold plated bars of some other metal (e.g. lead).

All of them are real. Research the definitions of futures and forwards and the fact that COMEX has never defaulted.

so today tech stonks are surging based on nothing. nvda is up 5% to a close to all time high and now has a p/e of 60 lulz.

the 10 year treasury however is up nearly 4 bps, to 4.63%. clearly the bond market isn’t buying what the stock market is selling.

MW: Federal Reserve governor Lisa Cook warns that the stock market is susceptible to a ‘large decline’

When the Fed starts “talking down” the stock market, I pay attention. This is not normal behavior for them.

It’s almost as if they need to take it down in order to justify the restart of QE …

or they need to take it down in an orderly fashion in order to get inflation under control or prevent a worse catastrophe if it crashes suddenly.

Cook was summarizing what was in the Financial Stability Report that the Fed issues twice a year and that no one ever reads. The Financial Stability Report has pointed at the risk that inflated stock prices pose for a long time. It’s just that no one ever reads it. Cook finally mentioned it.

MW: US Treasury 30-year yield hits highest in more than a year

Fed official issues a blunt message to the stock market, which ignores it

Fed probably doesn’t understand AI. AI will change everything. TO THE MOON. /s

Obviously AI (Artificial Idiocy) will change absolutely nothing.

“The dollar’s share had already been below 50% in 1990 and 1991, at the final leg of its long plunge from a share of 85% in 1977 to 46% in 1991, after inflation had exploded in the US in the 1970s, and eventually the world lost confidence in the Fed’s ability or willingness to get this inflation under control.

But by the 1990s, central banks loaded up on dollar-assets again, until the euro came along.”

So what was the cause(s) of the long decline from 1977-1991? and why did things then turn around for the $ as a reserve currency ?

Loss of long-term confidence due to the explosion of inflation in the late 1970s and the huge and ballooning government deficits in the 1980s surely were big drivers.

Interesting that Gold is up about 60% in price since pre-pandemic (~$1670) they reserves are only up a small fraction. Looks like reserves are going to test the pre 1971 levels and perhaps more individual buyers are buying as an inflation hedge especially in developing world?

The way the local currency has been devalued all over the world, it really shook the fait of the people on the fiat currency and hence the run to safety to all other assets which can at least protect the purchasing power of fiat currency. Hence the increase of price of assets like Gold, real estate, cryptos, and even stock market to some extent.

Govt is no more interested in making sure that the cost of living is contained, as evident in last 4 or so years.

1:04 PM 1/6/2025

Dow 42,706.56 -25.57 -0.06%

S&P 500 5,975.38 32.91 0.55%

Nasdaq 19,864.98 243.30 1.24%

VIX 16.31 0.18 1.12%

Gold 2,644.90 -9.80 -0.37%

Oil 73.44 -0.52 -0.70%

We are on a slippery slope.

From Adam Fergusson’s book, “When Money Dies”, regarding Wiemar Germany:

“The take-off point in the inflationary progress, after which the advent of hyperinflation was but a matter of time, the point indeed when it became self-generating and politically irreducible except for short periods, was not indeed to be found on the graph of the currency depreciation, or the velocity of its circulation, or of the balance of payments deficit. Nor in German’s case did it notably coincide with some ultimate crisis of confidence….Rather it lay on the falling curve of political possibility, with which was closely linked the degree of political power and courage that the government, sorely pressed as it was, was able to muster.”

In our case, government has been weakened by business interests and political disagreement. Fiscal and monetary policies appear timid in the face of Wall Street interests. Pain is deferred to the future. System integrity and trust has eroded.

It’s a bad path. History rhymes.

Inflation has fallen in the US to less than 3% from as high as 9%. Didn’t you get the memo from the Federal Reserve?

Don’t you know what the inflation target is? It’s not 3 to 9%.

MW: Stocks appear ‘rate sensitive once again’ as yields press higher

Presumably Central Banks around the world are diversifying their holdings as a form of insurance against possibly unpleasant outcomes of the ongoing shift from the American “unipolar moment” (roughly 1990-2008) back to “multipolarity” of some sort.

Think here of sanctions, trade wars, “hybrid warfare” and good old fashioned hot wars.

Wolf — been trying to find the best place to ask so figure this is good enough — when there’s talk of “eurodollars” does this simply refer to dollar assets held offshore from the US? And, presumably, this is accounted for by either currency in circulation and/or outstanding US debt that you update on, correct ?

Eurodollars are USD cash deposits in bank accounts offshore (anywhere, not just Europe) at foreign branches of US banks and at foreign banks. These deposits are in USD and are available in USD. They’re riskier because they’re less regulated and not insured. But they pay more in interest than USD deposits in the US. These facilities are used generally by companies or big investors to park large amounts of money temporarily to earn more interest than they could in the US. Foreign banks can then lend out these Eurodollars that they have on deposit.

This started in a big way after WW2 when the Marshall Plan sent lots of dollars overseas that needed to go into overseas USD bank accounts. It’s a huge well-oiled machine now.

Eurodollars are electronic deposits and have nothing to do with “currency in circulation” (paper dollars). That’s a separate thing.