Prices are still way too high, but… “Buyers are in a better position to negotiate as the market shifts away from a seller’s market”: NAR.

By Wolf Richter for WOLF STREET.

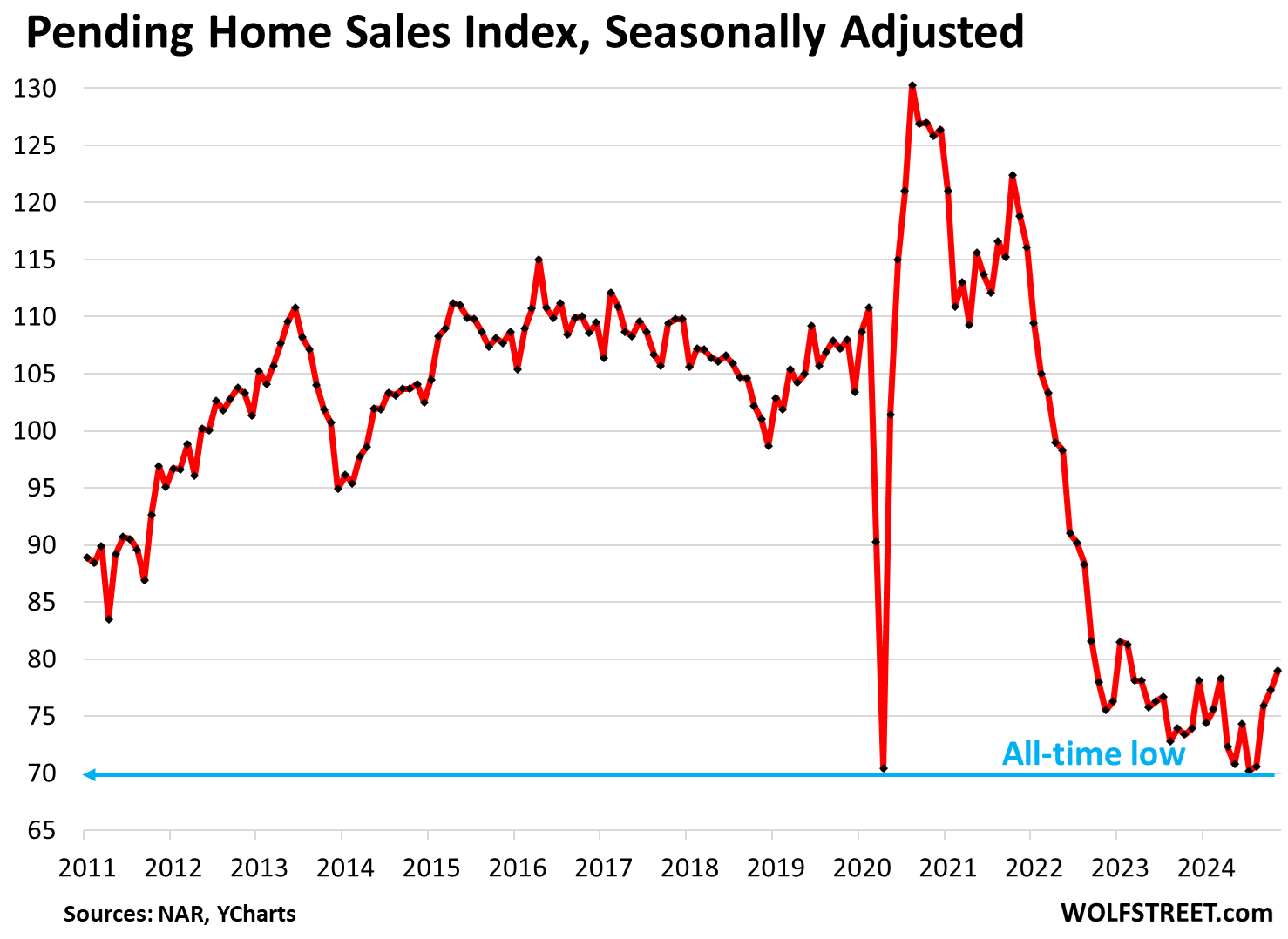

Pending home sales – a forward-looking indicator of “closed sales” over the next couple of months – obviously plunged in November from October because of the Thanksgiving week, and this time they plunged by 20.1% from October, according to the National Association of Realtors today. But they do that sort of thing every November, and so NAR uses big seasonal adjustments to iron out the month-to-month plunge, and this time turned it into a month-to-month rise of 2.2%.

Compared to the collapsed levels in November last year, not seasonally adjusted pending sales rose 5.6%, while seasonally adjusted pending sales rose 6.9%. July had set an all-time low in the history of the data.

So compared to the Novembers in prior years, seasonally adjusted, pending sales were up from rock-bottom, but remain in the frozen zone as the Buyers’ Strike continues because prices are too high (historic data in the chart via YCharts):

- November 2022: +4.6%

- November 2021: -33.5%

- November 2020: -37.2%

- November 2019: -26.9%.

Pending sales are based on contract signings and track deals that haven’t closed yet and could still fall apart or get canceled.

Pending sales by region.

Seasonally adjusted, transactions fell in the Northeast (-1.3%), inched up in the Midwest (+0.4%) and in the West (+0.5%), and jumped in the South (+5.2%).

Not seasonally adjusted, transactions plunged in all four regions (-27.0%, -26.2%, -20.3%, and -12.9% respectively).

What NAR said about this situation:

“Consumers appeared to have recalibrated expectations regarding mortgage rates and are taking advantage of more available inventory.”

“Mortgage rates have averaged above 6% for the past 24 months. Buyers are no longer waiting for or expecting mortgage rates to fall substantially.”

“Furthermore, buyers are in a better position to negotiate as the market shifts away from a seller’s market.”

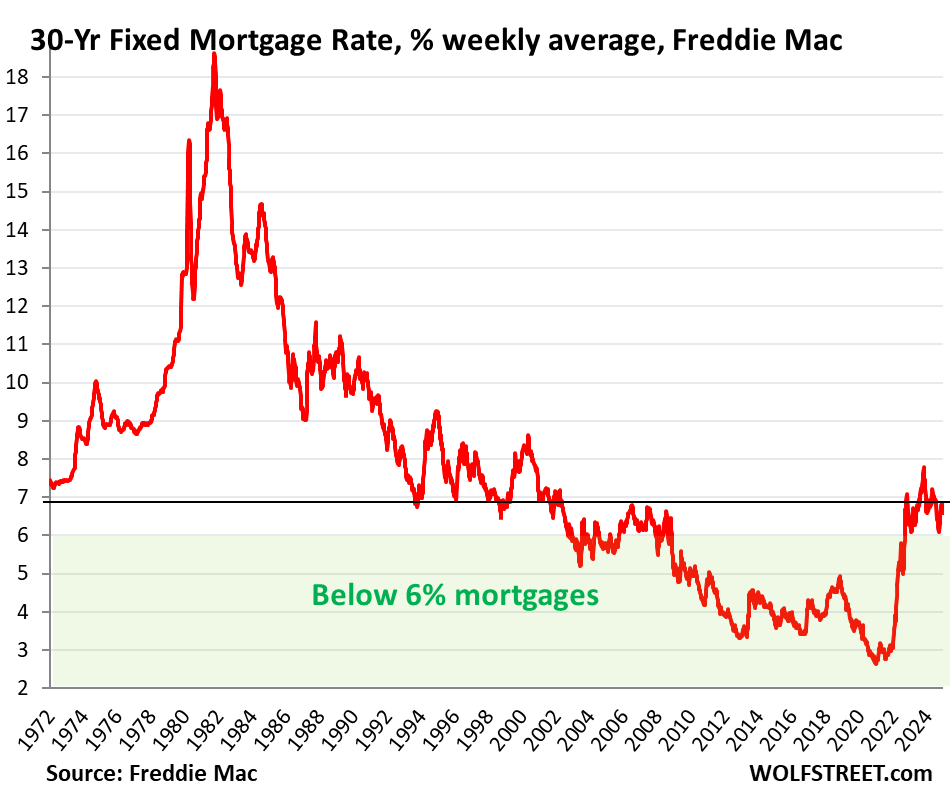

Mortgage rates are back in the old-normal range.

The average 30-year fixed mortgage rate, as of December 26, rose to 6.85%, according to Freddie Mac’s weakly measure.

In November, when those pending deals were made, that measure of mortgage rates was still a little lower, in the range between 6.69% to 6.84%.

Those rates are far higher than they had been during the Fed’s interest rate repression and QE, which included buying trillions of dollars of mortgage-backed securities. But that phase ended in early 2022. And in mid-2022, the Fed started shedding securities, including MBS, and has so far shed $2.1 trillion of its total holdings.

So mortgage rates are now back into the old normal range before QE, and the industry, including NAR and Fannie Mae, are starting to suggest that those extra-fancy low mortgage rates aren’t coming back, and that it’s time to get re-used to the old-normal mortgage rates.

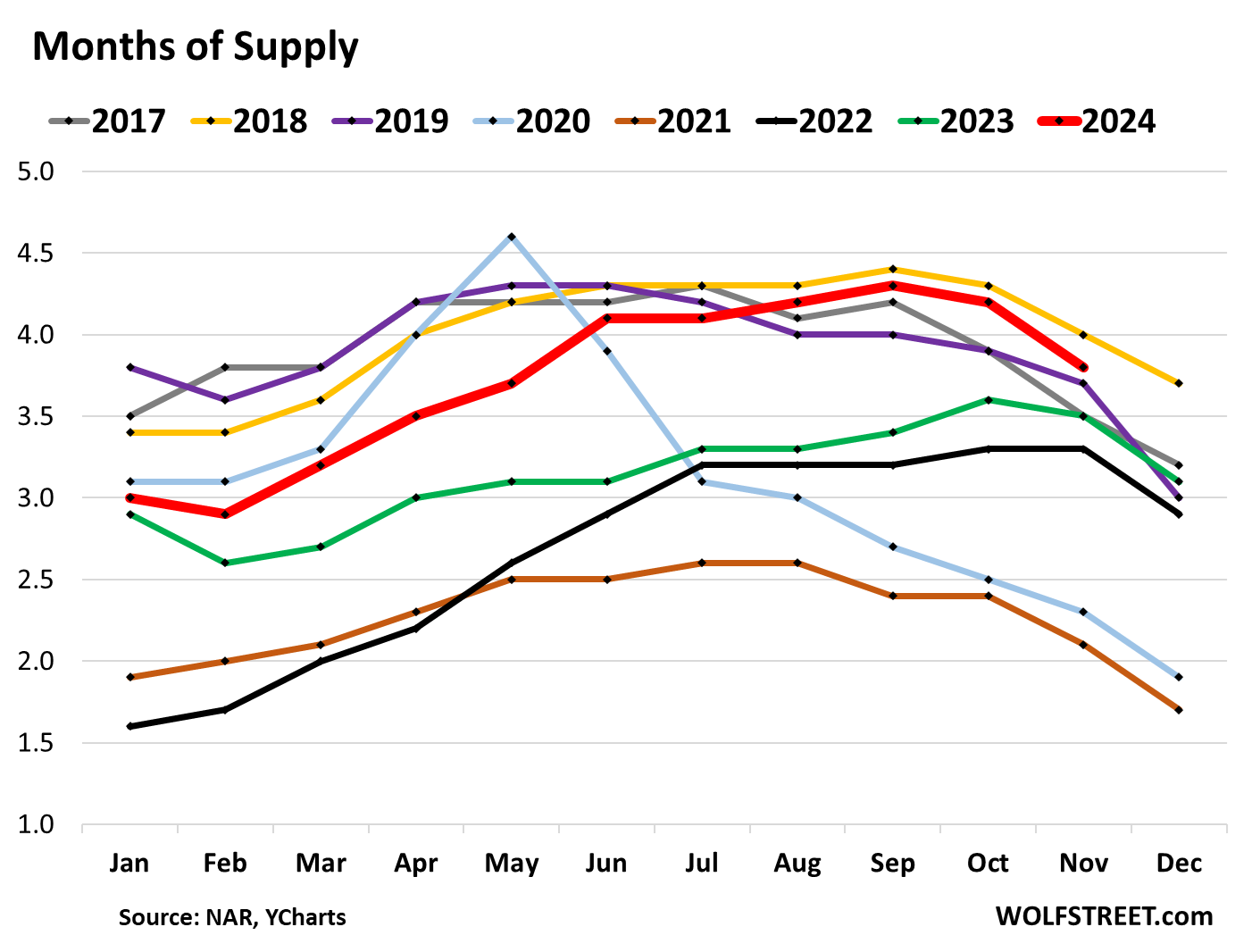

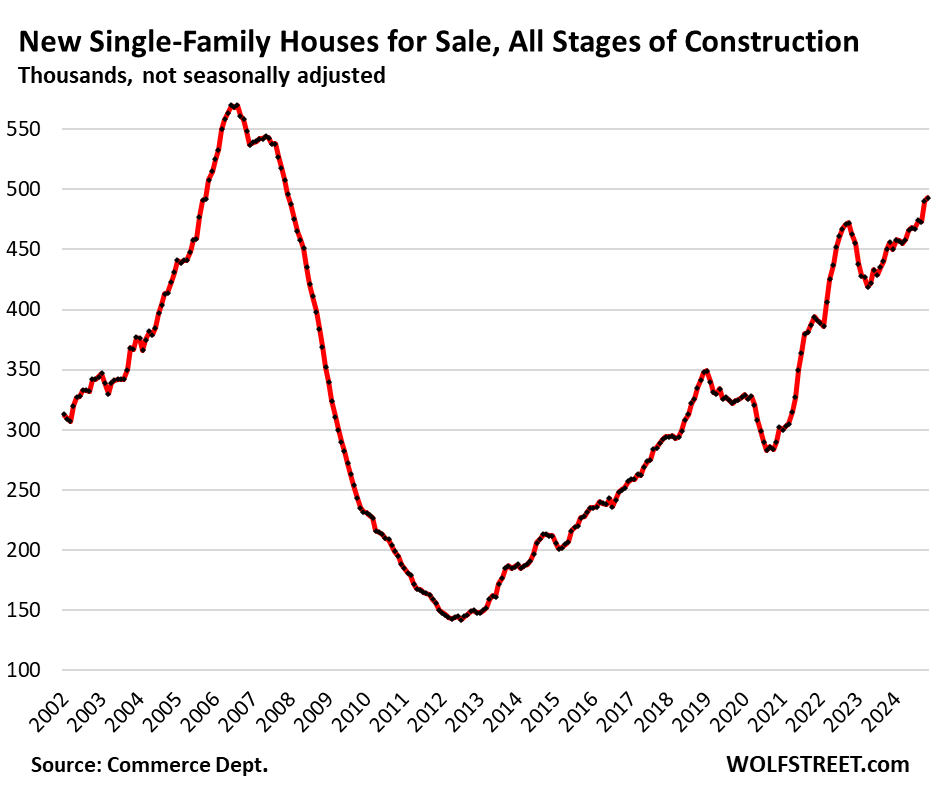

Supply is piling up – including from new construction.

Buyers now have lots of inventory to choose from, including heavily promoted new houses (not to speak of new condos, of which there is a flood of supply on the market and coming on the market, which isn’t included in the figures here).

Supply of existing homes for sale, at 3.8 months (red line in the chart below), was the second highest for any November over the past eight years, 2017 through 2024, behind only 2018 (yellow).

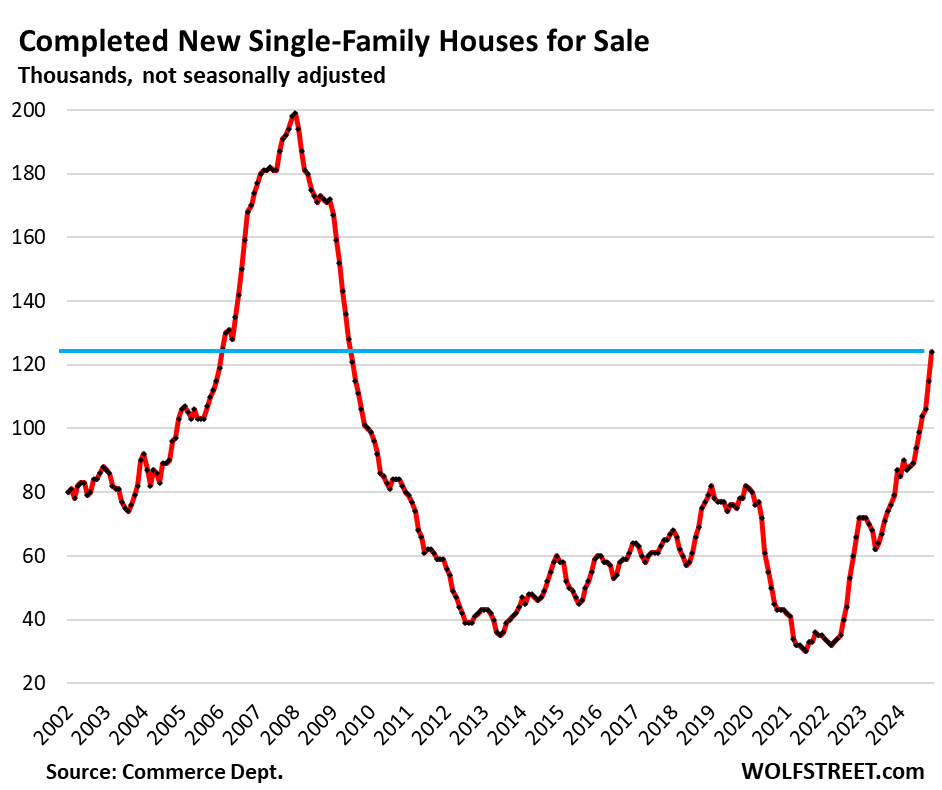

Inventory of completed new houses for sale spiked by 57% year-over-year to 124,000 houses in November, according to Census Bureau data. This is supply to the overall housing market. Homebuilders are trying to find buyers for these completed “spec” houses by piling on incentives, including costly mortgage-rate buydowns, and by cutting prices, thereby bringing monthly payments below those of equivalent existing homes, and their sales have held up reasonably well, while existing home sales have plunged to historic lows, from which they’re now inching back up.

Inventory for sale at all stages of construction – from not yet started to completed – rose by 8.1% from the already bloated levels a year ago, to 493,000 houses, the highest since December 2007. Supply jumped to 9.1 months. This does not include inventory of new condos for sale:

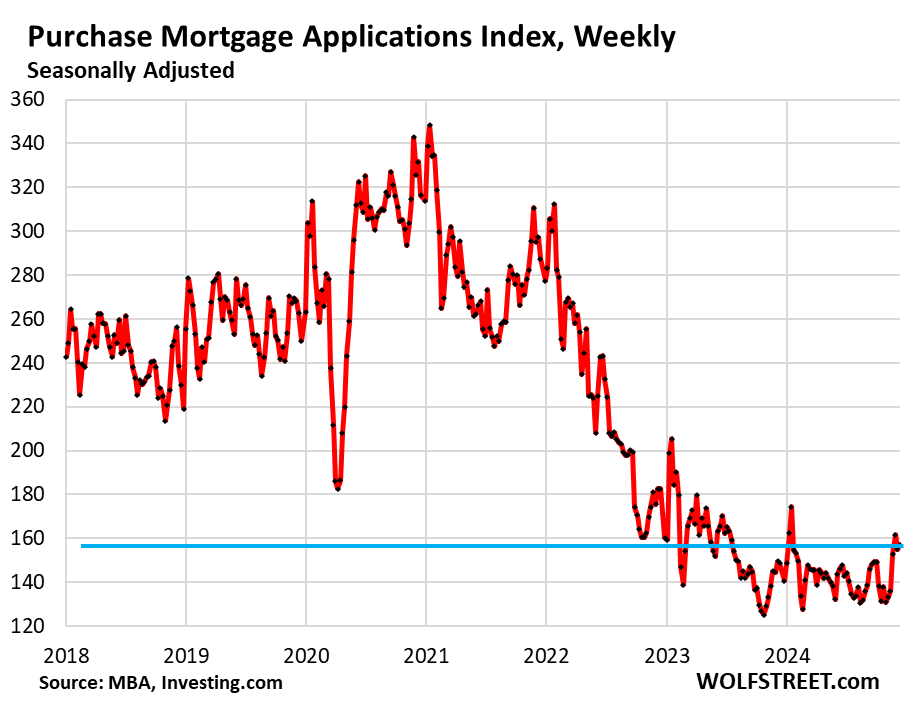

And the Buyers’ Strike Continued into December.

Applications for mortgages to purchase a home in the latest reporting week, seasonally adjusted, rose 5.6% from the collapsed levels a year ago, but were still down by 14% from the same period in 2022, by 45% from 2021, and by 40% from 2019, according to data from the Mortgage Bankers Association. Mortgage applications are an early indication of home sales – so like pending sales, up a little from rock bottom, but still in the frozen zone:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Good, with so much bad stuff to look forward to, or prepare for in 2025, Maybe this will be the final nail in the coffin to the start of some major price correction to come, especially in still extremely high price markets like SoCal (OC and SD). One tiny silver lining or hopium for 2025.

Then again 2025 will likely be a S***show so I also wouldn’t be surprise if price somehow spike back up or demand will come out of nowhere..who knows anymore

Just remember, prices won’t go to zero and mortgage rates will remain competitive. This is a slow burn since most sellers don’t have to sell quickly. It’s not like 2009 – 2011 when scads of bad loans went in the tank and there were foreclosures everywhere.

The old saying still applies: “This too, will pass”.

Things would change quickly if a recession happens and job losses follow.

Also, life events can’t be avoided: Death, divorce, relocation etc .

ON top of this, prices are going down although slow.

a steady increase in foreclosures is happening

however, unless your mortgage originated post 2020, you likely have huge equity

so while filing rates are much higher, the actual court house sales remain low

8 out of 10 are getting settled outside court house

ie investors buying at discounted prices and owners walking away with SOME CASH

joedidee, currently, they’re walking away with some cash because prices are still high. once they start dropping more rapidly, then that dynamic will change.

Until the biggest everything mania in world history subsides, we will not get price discovery anywhere.

You should’ve bought the 2022 dip. Plenty of price discovery then. Maybe you caught the covid dip?

If one of the bubbles pops then the rest will follow.

I’m seeing a lot of homes that were pending end up back on the market, I’m thinking people want but not getting because they don’t qualify at these higher mortgage rates and higher home prices. It’s probably for the better in many cases…just dodged a bullet.

But you guys knew all that anyways, but here’s something you didn’t know, the gift horse left town and says sayonara.

Yes, and quite a few deals are now falling apart over the issue of homeowner’s insurance. Either buyers cannot get it at all, or it’s way to expensive, and so the deal gets scuttled.

A guy I know, bought a home in middle class neighborhood, for $1.6 million in So Cal, is paying $36K per year for Prop Tax, HOA and Insurance.

A bargain. A comparable house in San Antonio has an annual cost of $42,456 for property tax and insurance.

From the flyover section of the country.

Not critical. Just truly curious what income is considered

middle class in So. Cal.?

but in Texas you don’t pay income tax

and the price is much lower than $1.6mil in Texas

Yup sounds about right for SoCal. The insanity and what people will do to obtain that American dream, not all but some will also look at the appreciation over the last decade and especially last couple of years and think they have a sure bet, on fire investment…

Sorry, just even simple math, paying $36K per year on top of mortgage is pretty absurd if you look at it from an investment perspective. This is also on top of any maint cost..etc but let’s say you put $1.6M in even 30 years treasury, you get approx $72K pre-tax income vs paying $36K of straight up expense…ok let’s say that person doesn’t have $1.6M, say they put $500K down, you’re still looking at $22K income vs $36K expense. For that $72K income, it can pay your monthly rent for a similar place if not nicer and still have grocery money left over..

but hey I get it, that’s the price you pay for belonging to owner class vs poor renter class..plus when you talk to your friends and family, you can now also complain about having to redo the kitchen, bathroom and have to run to home depot on the weekend to pick up some home improvement items..etc. Things that I am sure a lot of renters are missing out on..

@Escierto

A 1.6 million $ home in San Antonio is a 6,000 sq ft mansion on an acre. It’s going to have a 3 car garage and a pool.

A 1.6 million $ home in Orange County is a crummy 60 year old 1,600 square ft ranch crammed on a 5th of an acre. And the owner is likely paying 30K in CA income tax if they can afford a mortgage on a property like that.

More to the point though, the OC house would cost 400K in San Antonio and the property tax and insurance would probably be 15K at most, with no state income tax to boot. Hence people are moving from CA to TX, they can live a middle class life on a median income. They certainly aren’t moving for the weather.

The house I mentioned was 4,000 square feet on a third of an acre with a two car garage and a pool. Nice house but no palace.

Anyone who thinks they are getting bargains in SA is dreaming. For sure, it’s much much cheaper than Austin but the era of cheap houses is over here.

The home i mention is classifieds as town home and is 2600 square ft tri level house with no front yard and small back yard

It’s a good new community

Great point Mr. Richter, insurance and property taxes.

You have to figure we’ve burdened a whole generation with school debt. I’m sure they’d rather put those funds in a home.

I think it’s safe to say many people would rather not pay off their existing debts, regardless of the source of those debts, and spend those payments on something else. I had significant student loans when I finished college and never really thought about it as someone else burdening me with them. After all, I signed the promissory notes. That said, I do think some type of bankruptcy option should be available to discharge student loans, maybe after 10 years or something.

really

We have 3 kids – 23, 26, 29

2 went to college and graduated with exactly $0 in debt

and we didn’t help them pay for it

1st had full ride and ended up with paltry accounting/MIS degrees

2nd didn’t go and at 26 is married with 2 kids about to build new home using C A S H

3rd is now doing her masters – undergrad was paid for(she works) and she bought $30k vehicle at graduation for C A S H

of course our youngest is doing ONLINE liberty college masters programs at 20% cost of local STATE UNIVERSITY(they wanted $65k) she paying $15k

Exactly this! Weather it’s 10 or 20 years or whatever. Income based repayment until the loan is payed or the time is up, then pass the unpaid balance back to the schools to balance moral hazard.

Current system allows people of all aptitudes, who may not be credit worthy, to borrow nearly unlimited sums, to pursue degrees with questionable ROIs, all backed and made possible by federal guarantees.

Didn’t take long for institutions to realize they could bigger their budgets and salaries by luring in suckers with extravagant false expectations, Olympic sized swimming pools, manicured gardens, and posh recreation areas/dorms… All of which can be financed to people ripe enough in age to sign for it but still not trusted enough to buy a beer.

Education has great value, but allowing institutions to decouple that value from measurable risk, outcomes and consequences has produced predictable results and created a new generation of indentured servitude.

I am on buyers strike and have been for years, but I think the time is coming near.

Once I hear on MSM that the world is coming to an end, I’ll wait about 6 months to a year and then buy.

I have seen the same thing in Dallas

There is a veritable tsunami of used house inventory which is poised to come onto the market in late winter/early spring.

DC-

Please elaborate…

Thanks

I’m seeing higher inventory numbers do to lower monthly sales

lots getting pulled and put back on at lower prices

$10k-25k price drops normal now

in summer my wife sold one and I told her to be aggressive and she cut $25k and got immediate activity(ready to move in)

still had to give 8% rebate for financing

month later I sold similar home, but carried mortgage(making more now on interest)

of course both were FREE AND CLEAR

My spidey-sense is that most people won’t list in the winter when they know buyers are scarce unless they badly need to sell ASAP. Under normal circumstances they wait until spring when parents are shopping school districts. What may significantly increase inventory is the investors seeing prices are declining and deciding to get out before prices decline further.

That could put a lot of inventory onto the market that’s currently being rented out short term to take advantage of the run up in price. All those Covid investors could well decide it’s time to take their profits and run.

1:04 PM 12/30/2024

Dow 42,573.73 -418.48 -0.97%

S&P 500 5,906.94 -63.90 -1.07%

Nasdaq 19,486.78 -235.25 -1.19%

VIX 16.91 0.96 6.02%

Gold 2,622.60 -9.30 -0.35%

Oil 71.16 0.56 0.79%

MW: Natural-gas prices see biggest jump in nearly 3 years, leading oil higher

Yep. Polar Vortex coming. Then the rug will be pulled out of the price of nat gas. The US is producing more than it needs.

Natural gas has been… unnaturally cheap vis-a-vis the price of oil. The former was bound to go up relative to the latter.

In the Permian, natty gas prices were negative for much of the year due to it being a byproduct of oil extraction.

NAR and some in the press are outdoing themselves for 2025 and putting out ‘information’ claiming 3.7% rises in most housing markets and significant increases in housing prices will be seen in 2025 in 16 major markets! Too funny! Desperate?

DM: The 16 large US cities where housing prices are set to soar the most in 2025

House prices are expected to rise by 3.7 per cent across America next year, but analysts warn that housing prices are expected to soar to unprecedented heights in 16 cities across the US.

RE trolls and promoters have completely taken over the media long ago. There is no stopping the RE trolls. Well there is, at least right here in this joint.

real indicator is when VACAY/airbnb homes go on sale

til then

In the Florida markets I watch, I’ve been seeing a lot of obvious VRBO/AirBNB type properties popping up. All of which claim to be excellent sources of revenue… So why sell, hmmm???

Exactly. In my neighborhood over the last five years, 8 out of 10 houses were purchased by real estate “investors” who purchased the property to immediately flip them as AirBnb/VRBO short term rentals. Locally, the short term rental market is experiencing a glut of supply. If underlying prices start to look shaky, it may trigger a rush for the exits. A small local house sold for $680K a few years ago, they fixed it up, and they tried to make a go of it as an AirBnb. After two years of losses, they sold the property for $800K to someone else… who tried to do the exact same thing.

For the SoCal real estate trolls: An examination of an Atlas will show that the land mass doesn’t end at the southern end, but continues into baja and especially the future twin city of Tijuana, Mexico. The future of affordable living growth region for USA remote workers.

Future?

I was joking with my coworkers a several weeks ago about Trump may simply annex Canada and Mexico as a way to solve a lot of problems.

Fast forward a bit and Trump has already jumped onboard with Canada (and apparently Greenland too). Maybe soon we’ll hear about Mexico. After all, we need more Lebensraum (living space).

Makruger-

Perilously close to fulfilling Godwin’s Law…

Mexico is a failed state which is run by narcos. And it’s our border. Sending the US military into the country to wage a war to lay waste to and end all of the cartels and then make it a part of the USA under the US constitution and with fully open borders makes perfect sense. I would love to see that in my lifetime.

Those trolls include ZH, inexplicably. You’d think they’d be doomsayers as always.

Like a broken record I’ll suggest again:

Houses will slowly and painfully change hands for the next four to maybe ten years as prices, population, inflation and rates all find their new equilibrium. I’d expect prices to more or less remain flat the whole time. Which means massive drops in inflation adjusted terms.

Probably the most realistic used house transaction for a while will have both the buyer and seller come away angry: “I can’t believe we paid that much and our rate is still so high. Forget about a vacation for the next few years!”. “I can’t believe we sold for so little – isn’t this what the neighbors got for their smaller house three years ago?!”

New home builders will do what it takes to sell new homes at a rate that keeps them in business, period. Is there a market for 7.5 foot ceilings and 1.5 bathrooms anymore?

Buy WR articles are stating that prices are dropping across the spectrum, they are not staying flat.

The hottest markets saw the biggest drops: Austin and SFO

You’re arguing with a shill. The charts above scream epic RE crash, pretty much covering the entire country. This country is in denial and betting on unicorns to save them a la bitcon. Just read a message board where they’re calling 90k cheap and predicting 200k as early as spring 2025. People are unhinged and I think it will take nukes being detonated for many to come back to reality.

Gee whiz, a shill?

I said more or less stay flat. To me after decades of.. everything..+/-10% is more or less flat. I’ve seen it all (almost).

Anyway, flat/down a bit house prices while inflation is around 3% means you’ve lost about 35% in pricing power in a decade. For a house that’s catastrophically down. Nobody buys expecting to just barely get out clean a decade later.

I do agree that Bitcoin is funny but it could go to $200k or even a million before just evaporating away.

Happy New Year.

You think housing is going to have an epic crash because of the froth in bitcoin?

Even in 2008, it took 5 years peak to trough.

Housing that trades sideways for the next decade+, while wage inflation widdles away at the price:income ratio, is a very reasonable prediction imo.

I was in the trenches in the last RE bubble and called it spring/summer of 2004. This time it’s much much worse and we have 2 generations that have no clue about economics and a lot of older people with mush for brains as well. I didn’t mention nukes flippantly, I think the government could use a catastrophic event to shift the blame for an imploding economy.

“If the nukes are flying, I’ll be buying”

Seriously – it’s a great trade because if you’re right, you just bought the most epic dip ever. And if you’re wrong… well it won’t really matter.

Home prices are already flat going on 3 years nationally and we probably have a few more years of flat to declining prices. Given the rise of the markets and inflation, prices in real terms are down quite a bit since the 2021/2022 peak.

But the prices are going down even in nominal terms.

One of the hottest market Austin is down 22 percent from peak

You think this can’t happen to other places??

Prices went up like crazy in almost all the places.

That’s why it’s down so much – because it was one of the hottest markets, not in spite of it.

What goes up must come down.

“ Probably the most realistic used house transaction for a while will have both the buyer and seller come away angry: “I can’t believe we paid that much and our rate is still so high. Forget about a vacation for the next few years!”. “I can’t believe we sold for so little – isn’t this what the neighbors got for their smaller house three years ago?!””

This is so true now. Though, thinking back, it has always been true whenever I bought or sold a house to a lesser extent. This is why some people say a good RE agent’s value is being a psychologist and keeping both buyer and seller calm. It is an intense psychological process with a lot of money. Nobody wants to overspend buying anything or ‘lose’ money they thought they had.

However, looking at Wolf’s excellent data, Looking at the Sacramento chart above, prices have fallen about 5% from the peak. Buyers should be relieved by this unless they think prices will fall further or the house isn’t perfect. Prices have increased 30% in 5 years and nearly 100% in 10 years!! Sellers should be overjoyed with this since on average, people own a house for 7 years. Typical sellers have made a killing. People tend to look at the glass half full.

Over the last year most markets have transitioned from an inventory shortage to and inventory surplus. For example Denver has inventory above its 2019 levels the last few months. If inventory stays high and supply out weighs demand prices will drop. For prices to stay flat you typically need supply and demand to be in equilibrium but that’s not the trend we’re seeing.

I also have to wonder how everyone who bought with the marry the house, date the rate moto is doing.

Come spring if supply still outweighs demand but a significant amount I think we’ll finally see more widespread price decreases. Hard to say though.

And on the small chance we get a recession I think those price drops will be faster.

National data, while useful to track trends, doesn’t reflect local markets, each of which has a unique basket of houses, new construction, regulations, taxes, insurance, jobs, etc.

In my corner of NorCal, there is very little inventory. Houses that didn’t sell in summer went off the market and are slowly being re-listed, mostly at prices higher than what they didn’t sell for previously. Fixers are priced at top $$, and ugly white and gray flips are priced even higher. There is some new construction, big houses on tiny lots. But, the excess new homes are mostly in states like FL and TX, which is only useful if your job or family is in one of those areas.

I’m hoping something will change in 2025. I’m more than willing to take a hit on my current house, if I could find the next property in one of the states I have searches in.

LOL, never fails, not my neighborhood. You’re in a small town near Sacramento that is part of the Sacramento metro:

Thank you for your patience to refute these ‘not in my neighborhood ‘ people

We are naturally biased as we think we are special and this time is different at least for our neighborhood.

Rural anecdote with an okay local economy.

17 houses for sale in area.

Of which:

I personally know of two people just walking away from their mortgage. They do have equity, but are just letting the lender do the selling and settling up. One is choosing to live in a small travel trailer at his work site, and the other has another home somewhere else.

They are fed up with the whole process, know they will get slapped down, and choose to let a third party find a buyer. The other places have the signs up with no action or sales. Some have been for sale for over 2 years, with no reduction in asking.

There are tons of new builds where I live in south Texas. There is also lots of work here too. These houses (new ones) are 1,300 – 2,500 sq. ft. in size on small lots and they are selling for around $170/sq.ft. Yes, a cheap builder’s grade home with some nice upgrades, but that’s what you get unless you custom build a home.

There are mostly SOLD signs in the houses where I live in the new development and many retirees like me are buying them along with young working families or couples. A nurse and her husband (in IT) live next door to me. Two local cops live in the neighborhood too.

The local builders are discounting about 10% (end of year closeout of newly started homes) and offering 5.99% for the first three years of financing.

It’s all good.

I happened to stumble into a new build neighborhood outside a small town in (very) south Texas while exploring and touring last week. Most looked completed, with maybe a few still getting interior finishes. All were listed under $200K, not many pending.

I would think these would fly with retirees, a quiet rural location 45 minutes inland. Not all is great.

MaddieB,

Just curious, what states are you looking at? Also, why wait? There will always be people who are selling and buying regardless of the “wait and see” crowd. My point being, there could be a buyer in your area waiting to see your house and buy it. If you’ve already accepted “taking a hit”, what’s preventing you from moving forward with your plans?

Try Omaha or Tulsa ,great vaues

In my midwest metro things are basically frozen. Prices are not dropping significantly and sellers just wait things out. We’ve watched homes not drop prices for 4-6 months until they find a buyer and we’ve seen houses we like sell in 1-4 days after they come on the market.

This is what my spouse and I have been noticing as well.

I just purchased a duplex in Minneapolis. It had been on the market for around 50 days and I was able to get it for 90% of asking price. I may have been able to save money by waiting, but houses are still fairly affordable in Minneapolis. I don’t seem them falling as much as some of the other metros where there were huge runups in price.

From Egyptian deserts to Minneapolis winters will be quite a shock…

Agreed.

I sold my Minneapolis condo last summer for 100% asking price. Buyer found a private lender to finance her at 3%. It was on the market for about 2 weeks.

I agree prices in our metro are still pretty reasonable. There are plenty of jobs and lots of really good parks and outdoor activities. Some people hate the cold but I love it. I get the best, most refreshing sleep in the winter, it heals all my injuries. Welcome to the Twin Cities!

I can’t absolutely fathom how are prices staying so high in mid west

I can at least understand the allure of places like coastal CA but cmon mid west ..

Things have really gone crazy..

Demand will be deferred. Bond prices have entered a new bear market.

Professor emeritus Leland James Pritchard (Ph.D., Chicago Economics 1933, M.S. Statistics, Phi Beta Kappa) never minced his words, and in May 1980 pontificated that:

“The Depository Institutions Monetary Control Act will have a pronounced effect in reducing money velocity”.

Now we have the opposite scenario.

Sales in the Northeast still dropped 1.3%; even with the seasonally adjusted number. Here in the Boston area, not a lot of new construction either (lack of land). Talking to some of my friends in real estate and they’re not sure what to think for Q1 2025.

Zillow Home Price Index

Manchester, NH +7.3% year over year

Providence RI +8.7% year over year

Quincy, MA +4.2% year over year

Brockton, MA +6.0% year over year

Boston area will never go down, too many jobs and nor enough room.

Once remote work is embraced… do you think metro/urban areas will decrease?

I mean why live there when you get 2x as much for your dollar and make the same income elsewhere…

I think so, but just speculating of course 😁

Great question, but anecdotally many of my friends and family are back in the office 4 days a week (up from no days or 1 or 2 days a week a couple years back).

Once remote work has embraced? Huh? Based on increasing traffic on 93 and 128 over the last 4 years, I’d say exactly the opposite is happening.

There are 1/4 of a million college students in the Boston area. None of them are going to stop coming to town.

I went to school near the muddy banks of the Charles. I would have never believed that commuter night school NEU would be now considered a top ranking school. HA! Yet, they did develop that area and even ventured in Southie land. Maybe, I should have stayed for grad school, but the west was calling. Best decision ever.

I used to live in Boston

Good city but just could not tolerate the weather .

Came to Ca and never looked back.

Just a general comment/pet peeve… units on the y axis would be nice

Otherwise really just delete this comment 😂

Open your eyes and LOOOOOOOOK at the effing TITLE before you post this effing BS. Units are indicated in huge font in the effing TITLE. “Index” means index value. Why do I hafta put up with this braindead BS?

Wolf, you never have the x-axis labeled either.

How is anyone supposed to know what those numbers refer to? 2020, 2021, 2022, 2023, 2024… they could be anything.

/s

They’re cryptos. Everyone knows that. X-axis is always cryptos.

Prices are too high.

65% of Americans own homes, “most” would disagree with you, because home prices have doubled they have all been given hundreds of thousands of dollars of imaginary money. They would like to keep the illusion in tact.

It’s very unlikely home prices will go up but it’s fine by me and the 65% if they do.

I own two homes and I’d say prices are too high

These high prices are not good for the society and economy in general.

But only time would tell

I own my home and think prices are too high. Including my own recently asessed value, which is an absurd and unrealistic number.

My house is worth to much, make it go away…my boss is paying me to much, please help me…

You know I’m just joking around my greedy American friends.

Why not do a multi unit article too? “Multi family” aka condos, apartments, anything attached.. is being wayyy over built. I do not know how they stay in business. It seems the occupancy rate needed for profit is 75% on them (? But i really do not know how to derive that), while in the “population booming” southeast we are doing 40% or so and alot of changing hands..

2021, 2022, and 2023 were the highest multifamily construction starts since the 1980s multifamily bubble. All you have to do is read the articles here, and you’d have known that:

https://wolfstreet.com/2024/01/18/residential-construction-starts-fall-in-2023-multifamily-from-38-year-high-single-family-for-2nd-year-both-still-higher-than-pre-covid/

Condo prices have been sagging for years in many markets. Here are a couple:

Many of the condos in Seattle would be owned by the Chinese when they were crushed with new taxes in Vancouver, Canada back in April 2017. If the Yuan keeps falling the condo prices will keep falling in Seattle.

I always wonder about this every time you post this data, but finally feel like asking. Does the “months supply” data gear adjusted for the current monthly sales figures?

Fractions get hard to compare when both the numerator and the denominator are changing with each reading

Yes: Month-end inventory (say 150 houses) divided by that month’s sales (say 50 houses) = 3 months of supply (150 divided by 50), meaning it would take three months to sell the entire inventory at the current rate of sales.

Showing inventory in terms of months’ or days’ supply is a classic way in business in general, including retail, to see if inventory levels are overstocked, understocked, or about right given current demand. You’ll hear me talk about days supply when it comes to new and used vehicle inventories as well. It’s a very important concept.

This obviously gets more complicated if you try to use seasonally adjusted annual rates, which is kind of a no-no, and which I don’t do.

So I use actual November inventory divided by actual November sales, and we understand that this is seasonal, and so in my chart I show it as “stacked,” where each year is one line, and you can see the seasonality and compare November to other Novembers.

Lets see how this market holds up when there are mass layoffs OR when companies with 100% remote work demand some return to office, or go bankrupt.

How common is it to be fully remote in the current time?

As I mentioned in a previous comment – traffic in my city has gotten progressively worse since 2020, implying a steady decline in remote work.

It depends quite a lot on the company. Mine has offices but 75% of us are remote. Companies looking for top talent often have to offer remote as the top talent has discovered they can work from anywhere.

My company is based in Atlanta. But they just hired a new C-suite executive who lives in Pennsylvania. My entire team of 8 live in 8 different places. It’s an entirely remote company (~ 500 employees) and I have no fears of a forced RTO any time soon. Anecdotal, of course but it makes me very happy!

No Gen Z in their right mind wants to enter this market even with the wealth transfer down payment. Insurance, taxes, and interest rates are eating folks for lunch. Mortgages are now luxury item in U.S. The juice is not worth the squeeze, when you can rent or lease and walk away. The man’s Man’s mantra Shit, Shave, and Shower does not required cutting your throat to blow your nose. In a Nation that is heading into $40 trillion into debt, stay liquid and free of restraints. We have narrowly escaped the Californification of America this election.

Alt take: homebuilders should hang on to their inventory.

1. Low-wage construction labor gets deported;

2. Without labor, supply dries up;

3. Homebuilder cash in on their hoard.

But they could also get crushed by a flood of supply of existing homes, which seems like a reasonable prediction at this point. Remember, new homes are a relatively small % of overall home sales.

CZ,

“Alt take: homebuilders should hang on to their inventory.”

That will kill them. Is that what you want? They have billions of dollars tied up in this inventory; the carrying costs of the new houses, and the interest expense and related costs, would be eating them alive. Completed unsold inventory is very risky if it doesn’t turn over quickly.

He’s not going to deport anyone. Just like everything else he said, it was just a campaign slogan nothing more. The only thing he’s actually going to DO is lower taxes some more on the rich and corporations. Oh and make our country one big reality t.v. show for 4 years. The end!

DM: Border Patrol chief issues shock comments on mass deportations ahead of Trump’s second White House term

The head of the National Border Patrol Council is warning Democrats that Donald Trump is going to keep his promises on mass deportations to clean up the border.

Border will tighten. Harder to go home for a visit and return via walking across the southern border. Violators will be refused entry at ports of entry (the normal way visitors enter a sovereign country.)

What is wrong with having control of one’s border, scanning passports, enforcing length of stay,etc. Every country I travel to makes me submit my passport, declare my travel plans, etc.

That assumes no new home builders enter the fray. What’s stopping them at this point? A great opportunity for some hot shit private equity or startup money to step up. Get a big Trump pat on the back. Else call up a Congressional investigation, why don’t we ..

Wolf, I must admire your extraordinary patience with the comment section.

And, by the way, thanks for all you do, and have a safe and Happy New Year!

All sporting events in which you can wager on are scripted by athletic actors…NFL is a glorified Grifting Operation…this ends the lesson for the day….

It is my opinion that Wolf and Co. give out some great info about the real estate market but often do not delve deeper to explore the ‘why’ or likely scenarios to develop. This all to me portends impending disaster.

First paragraph-

Prices are still way too high, but… “Buyers are in a better position to negotiate as the market shifts away from a seller’s market”: NAR

Why should I negotiate $10K or $20K off of a home price when many homes are priced at 300% of what they were a few year ago?

“What NAR said about this situation:”

If the NAR saw a tsunami coming in they would likely report ‘The sea is not quite as calm as one normally observes.’

Happy 2025